Flow-level performance of random wireless networks

Abstract

We study the flow-level performance of random wireless networks. The locations of base stations (BSs) follow a Poisson point process. The number and positions of active users are dynamic. We associate a queue to each BS. The performance and stability of a BS depend on its load. In some cases, the full distribution of the load can be derived. Otherwise we derive formulas for the first and second moments. Networks on the line and on the plane are considered. Our model is generic enough to include features of recent wireless networks such as 4G (LTE) networks. In dense networks, we show that the inter-cell interference power becomes normally distributed, simplifying many computations. Numerical experiments demonstrate that in cases of practical interest, the loads distribution can be well approximated by a gamma distribution with known mean and variance. 111Richard Combes is with KTH. Major parts of this work were done when he was in INRIA.

Index Terms:

Wireless networks, Performance Evaluation, Queuing theory, Traffic models, Flow-level dynamics, Stochastic geometry, Point processes.I Introduction

The most straightforward approach to performance evaluation of wireless networks is to assume that BS locations are deterministic and follow a regular pattern such as an hexagonal grid on the plane. A more recent trend is to consider random BS locations. Namely BS locations form a stationary point process rather than a deterministic pattern. One of the motivations for this approach is that operational networks are hardly regular, due to irregular city planning, legal constraints on BS placement and non homogeneity of traffic density. When the BS locations follow a PPP (PPP), many performance indicators can be calculated in closed form or with simple numerical integrals, so that this approach is tractable. A summary of both the theory and networking applications can be found in [1, 2].

Another characteristic of wireless network is the dynamic user behavior (also called flow-level dynamics). Users enter the network at random locations and instants to receive a service, and leave after service completion. Users may move during their service. Network resources are shared between active users so that the time spent by different users is not independent i.e there is congestion. Congestion due to dynamic user behavior is modeled by queueing theory: each BS is modeled as a queue, and the system performance is derived from its stationary distribution, providing that the queue is stable. Queuing models for wireless networks serving streaming traffic [3, 4, 5], elastic traffic [6, 7] and a mix of both [8] have been studied in the literature. An important characteristic is the performance of a BS is its load. In particular, without admission control, the number of active users grows without bound if the load is strictly larger than .

Related work:

Assuming that users are served by the closest BS, the zones served by BS are Poisson-Voronoi cells. The geometry of Poisson-Voronoi cells is a well studied topic because of its applications to physics and more recently networking. The mean and variance of the cell area is studied in [9]. Statistical studies show that the cell area distribution can be approximated with good accuracy by a gamma distribution [10] or a generalized gamma distribution [11]. [12] investigates the distribution of the smallest disk containing the Voronoi cell which can serve as an upper bound. The number of sides of the cell was studied in [13]. Conditional to the number of faces of the cell, [14] showed that the fundamental area of the cell follows a Gamma distribution and [15] gives the distribution of the cell area. A more general gamma-type result is given in [16]. In [17], the authors consider the distribution of the integral of a function of the distance over the cell, and calculate its first and second moments as well as its tail behavior.

There is a large amount of recent results on the performance evaluation of wireless networks using stochastic geometry. Most works assume that BS locations follow a PPP. Distribution of the covered areas is studied in [18]. The distribution of the SINR (SINR) and data rate in downlink cellular networks is derived in [19]. [20] treats the uplink case. Downlink heterogenous networks are considered in [21, 22, 23, 24, 25], and the different types of BS are assumed to follow independent PPP. User association and fractional frequency reuse are studied in [26] and [24] respectively. The handover probability of a typical user is studied in [27]. Concerning non-Poisson networks, [28] studies the distribution of shot-noise and [29] examines the performance gap between PPP and non-Poisson networks.

All these results concern “single user” performance evaluation and do not take into account dynamic user behavior. Namely, only the distribution of the SINR, data rate etc. for a single user located at the origin are derived. In [30, 21, 22], a random number of users is considered. However, the time a user spends in the network does not depend on his position or on the number of users connected to the same serving BS i.e the congestion is not taken into account. For elastic traffic for instance, the time spent by a user to transmit a given amount of data depends on his throughput which is a function of its position, interference and congestion. Furthermore [30, 21] approximate the cell size distribution by a gamma distribution, as proposed by [10, 11].

Our contribution:

In this paper, we combine stochastic geometry and queuing theory. We assume that BS locations follow a PPP, and we study the distribution of the BS loads. The BS load is expressed as the integral of a function over the area covered by this BS, depending both on the distance to the BS and the interference power created by interfering BS. Hence the time spent in the network by a user can depend on its location, the interference and the number of users connected to the same BS. We derive formulas to calculate characteristics of the loads distribution. We study both line and plane networks. In the case of line networks, in many cases of interest we can derive the full distribution of the load in terms of its Laplace/Fourier transform. For plane networks, we give formulas for the first and second moments of the loads. Hence we extend the results of [17] to take into account inter-cell interference. We do not use the gamma approximation of the cell size distribution as in [30, 21]. Interference is modeled as Poisson shot-noise and its distribution is well studied , e.g [31, 1, 32].

The rest of the paper is organized as follows: in section II, we introduce the model considered and highlight the link between queuing theory and stochastic geometry. In section III, we explain how our model describes many features of wireless networks, including types of traffic (voice, streaming, data etc.), frequency reuse, channel-aware scheduling and so on. In section IV we consider PPP networks on a line and show that in some cases the full distribution of the load can be obtained. We turn to PPP networks on the plane in section V, and calculate the first and second moments of the load. In section VI we perform numerical experiments to study the load distribution statistically. Section VII concludes the paper.

II The model

II-A The basic model

We consider BS placed in a Euclidian space equipped with the usual Euclidean norm . Typically we will consider for networks on a line and for networks in the plane. The BS form a PPP on with intensity denoted . We denote by and the Palm probability and expectation with respect to . See [33] for instance for the definition of Palm probability. Users are connected to the closest BS (in distance) and we define the zone served by BS :

We use the convention that . The set is a Voronoi cell, and the collection is known as the Poisson-Voronoi tessellation of . We define the Voronoi cell of the point process . By Slivnyak’s theorem, and have the same distribution under Palm probability. We call the typical cell. Consider marks in , and a function . We define the shot-noise at location by:

The random variable serves to model the inter-cell interference received at location . The function models the signal attenuation due to distance. The marks model for instance shadowing and frequency reuse. We assume that the marks are i.i.d. (i.i.d.) and that they are independent of . Results on the distribution of shot noise generated by a PPP are recalled in appendix A. By a slight abuse of notation we denote by when it does not create confusion. We define:

the Fourier/Laplace transform of . We will sometimes consider the path-loss to follow a power law (assumption 1).

Assumptions 1 (Power law path-loss).

and the path-loss is with and .

Finally we define the load of the typical cell:

| (1) |

with a positive measurable function. The quantity denotes the infinitesimal load created by users whom enter the network at location . The goal of this work is to study the Palm distribution of the load of the typical cell. We consider two possible simplifying assumptions on .

Assumptions 2 (No interference).

There is a positive function such that for all :

Assumptions 3 (Affine function of interference).

There are positive functions such that for all :

The Palm distribution of the load is linked to the stationary distribution of the load by Slivnyak’s inversion formula:

with any positive bounded function. We denote by the Euclidean ball centered at of radius . For and we define:

We denote by the Lebesgue measure of .

We will often consider the distribution of conditional to the fact that a given set of points belong to the typical cell . Conditional to the event , under Palm probability, is a PPP on with intensity . Therefore, for a function of the point process we define the expectation of conditional to the event that are in the typical cell:

III Propagation, Data Rate and Traffic models

The load as defined in equation (1) appears in several models for the performance evaluation of wireless networks with flow-level dynamics. Namely, users enter the network at random times and locations, they are connected to the closest BS and leave the network after receiving service from the BS. The time spent by a user in the network depends on:

-

•

his location with respect to the serving BS because the power of the received signal decreases with distance,

-

•

his location with respect to the other BS because the BS interfere with each other,

-

•

the number of active users and their positions because of congestion. Namely the radio resources are shared between active users at each BS.

We describe a few queuing models used for different types of traffic. Users enter the network according to a homogeneous PPP of intensity (not to be confused with ). We will denote by the data rate of a user located at i.e his throughput when he is the only active user served by the closest BS.

III-A Traffic models

III-A1 Voice traffic

The available bandwidth is divided into circuits (sometimes called subcarriers). When a user enters the network he is assigned a circuit. If there are no circuits available the user is blocked and leaves the network. A user stays an exponential time with mean in the network. Therefore, each BS is a M/M/C/C queue. The load is:

The performance indicator of interest is the blocking rate (the proportion of blocked users), which is a function of the load, and is given by the Erlang B formula (see for instance [34]).

III-A2 Streaming traffic

For streaming traffic, the amount of resources allocated to a user depends on his data rate. A user stays an exponential time with mean in the network. The bandwidth is divided into circuits of equal size. Users must achieve a minimal data rate and are allocated circuits. If a user arrives and there are not enough circuits to serve him he is blocked. The load is:

This model is known as Multi-rate Erlang model and the blocking rate can be calculated rapidly using the Kaufman-Roberts algorithm ([3, 4]). The blocking rate is not always an increasing function of the load ([35]), but the load can serve as a first-order performance measure.

III-A3 Adaptive streaming traffic

For adaptive streaming traffic, users can adjust their instantaneous throughput based on the available bandwidth. Video-on-demand services usually follow this model, and the throughput is adjusted by changing the level of video encoding. A user stays an exponential time with mean in the network. Each BS can be modeled as a M/M/ queue with load . The number of active users in stationary state is a Poisson random variable with mean . Assume that the available bandwidth is shared equally among active users. Denote by a Poisson random variable with mean . Then the expected throughput of a user at in steady state is:

III-A4 Elastic traffic

For elastic traffic, the bandwidth is shared fairly between active users as for adaptive streaming. Users download a random amount of data with expectation . Each BS is an M/G/1 processor sharing queue ([34, 6]) with load:

| (2) |

In particular both the mean number of active users and the blocking rate are functions of the load ([6]). For instance the mean number of active users in stationary regime is . It is noted that for elastic traffic, the time spent by a user is inversely proportional to his data rate, so that cell edge users stay longer than cell center users.

III-B Data rate calculation

III-B1 Spectral efficiency

We define the SINR at location :

with the thermal noise power. The user data rate at a given location depends on the interference because it is a function of the SINR. Assuming that the channel between a BS and a user is AWGN (AWGN), the data rate is given by the Shannon formula:

| (3) |

with the bandwidth used for data transmission. As shown in [36] a modified Shannon formula with and provides a very good approximation to the practical performance of LTE.

For wide-band systems such as CDMA (CDMA) where is large and the SINR is low, the data rate can be well approximated by a linear function of the SINR:

and in this case, is an affine function of the interference .

III-B2 Path-loss, shadowing and fading

Distance-dependent path-loss is captured by the function . Shadowing is captured by , and typically can be taken as a log-normal variable. We can also account for Rayleigh fading of the useful signal by considering ([37]):

with the exponential-integral function. The fast-fading of interfering signals has a relatively small impact because there is typically a large number of interfering BS with independent fading processes (see for instance [38]).

Similarly, MIMO (MIMO) can be taken into account by changing the function mapping SINR into the corresponding data rate.

III-B3 Channel-aware scheduling

In downlink cellular networks serving elastic traffic, channel measurements are available at the BS so that a scheduler picks the user with the best channel condition to transmit e.g a proportional fair scheduler. We can account for channel-aware scheduling in queuing models (e.g [6, 39]). Define the data rate of a user when his fading is maximal. In practice is the data rate provided by the highest modulation and coding scheme. Then, for elastic traffic we can define the load as equation (2), and the stability condition is . Each BS can be represented by a M/G/1/PS queue with state-dependent service rate.

III-B4 Frequency reuse schemes

In interference limited networks, it can be beneficial that BS do not transmit on the whole bandwidth at full power. We consider the following soft reuse scheme. The bandwidth is split into sub-bands of size . Based on a threshold on the distance to the serving BS, users are split into far users (“edge users”) and close users (“center users”). Each BS chooses one of the sub-bands at random on which it transmits at full power and serves edge users. On the other sub-bands, the BS serves center users and transmits at reduced power. The ratio between the reduced power and the maximal power is denoted . It was shown in [40] that soft reuse noticeably increases the network capacity for elastic traffic.

Since choice of sub-bands by different BS are independent, the interference received by a user is a shot noise with:

By a thinning argument, the interference is also the sum of two shot noises generated by two independent PPP with intensity and respectively.

A BS can be represented by two M/G/1/PS queues, one for the edge users and one for the center users with respective loads and :

The data rates are calculated by:

We also consider a scheme called hard reuse where a BS chooses one of the sub-bands on which it transmits at full power and does not transmit on the others. This scheme can be seen as a particular case of soft reuse with and . Namely all users are considered as edge users.

III-B5 BS activity patterns

In a realistic setting, BS only transmit when they have users to serve, so that the inter-cell interference they create depends on their state. Namely neighboring BS can be represented by coupled queues. For more than two BS, this model is known to be intractable. [41] proposes a “fluid approximation”: BS are modeled by independent queues, but the amount of time they transmit is equal to their load. The loads are obtained as a solution to a fixed point equation. While this is tractable for regular networks, in Poisson networks, even the expected load seems difficult to obtain, because the load of a BS depends on the load of its neighbors.

We suggest to use the (tractable) approximation introduced by [22]: the BS are modeled by independent queues, and they are active with probability . This is an independent thinning, so that the interference received at location is a shot noise generated by a PPP with intensity . The value of can then be found as a solution to a fixed point equation.

Furthermore, this issue is only significant in low loads, when the traffic demand is small compared to the network capacity. Hence, in operational networks, it should not be a major issue if we assume proper network dimensionning.

Also, the “sleep mode” functionality studied in [42] can be modeled the same way: BS are switched off with probability resulting in an independent thinning.

IV Line networks

We first analyze line networks (). Line networks are interesting because we can obtain the full distribution of the load in some cases. In this section and .

IV-A Typical cell

Under Palm probability, there is a BS at , that is . We define and , which are the neighbors of the central BS on the left and right respectively. The typical cell is:

The cell load is:

| (4) |

The geometry of the typical cell follows from the definition of a PPP.

Proposition 1.

are independent and both follow an exponential distribution with parameter .

Proof.

By definition of the PPP , for :

∎

This is the main reason why the distribution of the loads can be derived in some cases: the geometry of typical cell is described by two independent exponential variables.

IV-B No interference

In this subsection we consider assumptions 2, so that the load does not depend on interference. We derive its Laplace transform in Theorem 1. The proof of Theorem 1 is given in appendix B-A. We define the auxiliary function :

| (5) |

Theorem 1.

With assumptions 2, the Laplace transform of the load is:

Corollary 1.

-

•

(i) If , follows an Erlang distribution with parameters .

-

•

(ii) If , , is distributed as the sum of two independent Weibull r.v. with parameters .

Proof.

(i) If , then so that

From proposition 1, is the sum of two independent exponentially distributed r.v. with parameter . Hence has an Erlang distribution with parameters .

(ii) If , , then so that:

is exponentially distributed with parameter , so that follows a Weibull distribution with parameter . Hence is indeed a sum of two i.i.d. Weibull r.v. with parameters . ∎

IV-C Affine function of interference

In this subsection we consider assumptions 3, so that the load is an affine function of interference. This is of interest for instance in wide-band systems serving elastic traffic as mentioned in subsection III-B. In this case as well we can derive the full distribution of the BS load.

The BS load can be written:

| (6) |

We define two auxiliary functions and :

and:

The Laplace transform of the load is given by Theorem 2. The proof of Theorem 2 is given in appendix B-B.

Theorem 2.

With assumptions 3, the Laplace transform of the BS load is given by:

The moments of the load can be recovered from the Laplace transform. Corollary 2 gives a fairly simple expression for the expected load.

Corollary 2.

If we further consider power law path loss, the expected load has a simple form given by Corollary 3.

V Plane networks

We now turn to plane networks so that . Analysis for plane networks is more involved than for line networks because the geometry of the typical cell is more complex. In this section we derive the first and second moments of the cell loads.

V-A Moments of the cell load

In this section we identify with the complex plane to simplify notation. are locations in the complex plane, with , their polar coordinates (with the imaginary unit) and are locations in the complex plane used as integration variables. It is noted that and:

with the area of the intersection of the unit disk, and a disk of center and radius .

The -th moment of the cell load can be calculated as a dimensional integral. The moments might be infinite.

Theorem 3.

The -th (Palm) moment of the load is:

| (7) |

The Laplace transform of the interference conditional to is given by proposition 2 stated in the appendix. Also, the expectation on the r.h.s. (r.h.s.) of (7) can be calculated using the Plancherel theorem (proposition 3).

While it is theoretically possible to calculate all the moments of the load using Theorem 3, the amount of computing power required increases exponentially with . Hence its practical use is limited to the first and second moments.

Theorem 4.

(i) The first (Palm) moment of the load is:

| (8) |

with: .

The Laplace transform of , conditional to is given by proposition 4.

Proof.

The second moment of the cell load is given by theorem 5, and its proof is presented in appendix B-D.

Theorem 5.

a) The second (Palm) moment of the load is:

with:

and:

The Laplace transform of conditional to is given by specialization of theorem 2 to and .

V-B Affine function of interference

As done for plane networks in subsection IV-C, we consider the case where the load at a location is an affine function of the interference (assumptions 3). In this case calculating the full distribution of the interference is not needed. Obtaining the first and second moments is sufficient which simplifies the calculations.

Corollary 4.

V-C Elastic traffic in the low SINR regime

When considering elastic traffic in the low SINR regime, the expected load has a remarkably simple expression derived in corollary 6. The equation for the load (the function ) for elastic traffic is explained in section III. The proof of corollary 6 is found in appendix B-E.

Corollary 6.

It is noted that the lower bound (10) is particularly simple and is tight in the low SINR regime. Corollary 6 states that the average load becomes infinite for elastic traffic when the signal attenuation is a power law, with path-loss exponent close to free space propagation. Another interesting fact is that the average load does not depend on the transmitted power in the interference limited regime. Indeed, in stationary probability, the average distance between a user located at and the closest BS is . So the term is the ratio between the received power at distance and the thermal noise power . When this term is large, the first term of (10) becomes negligible, and

Also, in this regime, the load is inversely proportional to the BS density. Namely, the network capacity is proportional to the number of deployed BS .

V-D Dense networks

In dense networks (), the interference becomes normally distributed. Then and can be calculated as integrals of the Gaussian distribution, and we only need to calculate the first and second moments of the interference. In the case of a PPP on the line (i.e ), convergence of shot noise to a Gaussian process is well known ([45, 46, 31]). Theorem 6 provides a generalization. We prove a more general result (Theorem 7) in appendix B-F.

Theorem 6.

Consider a homogenous PPP on a closed set with intensity , and given by assumptions 1. Then, for all , , the distribution of converges in distribution to a multivariate normal distribution when . Namely:

with its covariance matrix. The covariance is given by:

Specializing theorem 6 to and we obtain the limit distribution of and which can be used to compute and respectively. We do not write the case for clarity.

Corollary 7.

With assumptions 1, conditional to , the interference at converges in law to a normal distribution:

with:

VI Numerical experiments

In this section we perform numerical experiments to study the distribution of the loads. We consider elastic traffic, so that the function is given by equations (2) and (3).

We use the following parameters: path-loss with , , no shadowing , total bandwidth Mhz, total BS transmit power dBm, thermal noise power dBm/Hz, traffic Mbits/km2/s. We use unless otherwise stated, which corresponds to typical dense urban environments. To simulate the distribution of the loads we proceed similarly to [47] to simulate the typical cell. To simulate the interference received over the typical cell, we simulate the PPP on a window large enough so that there are interfering BS on average. To evaluate the distribution of the loads, independent samples of the typical cell are drawn. Numerical integrals are computed using Gauss-Kronrod quadrature.

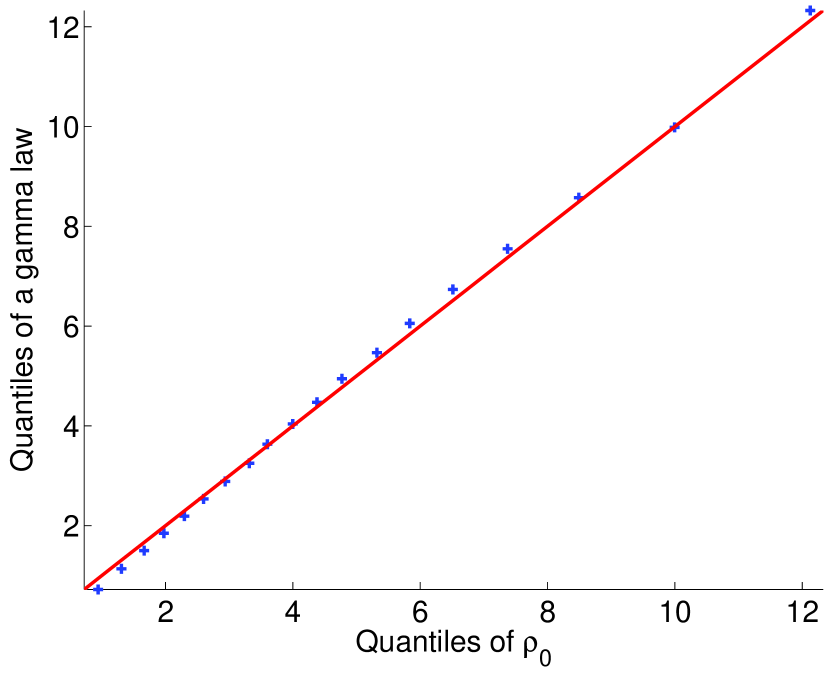

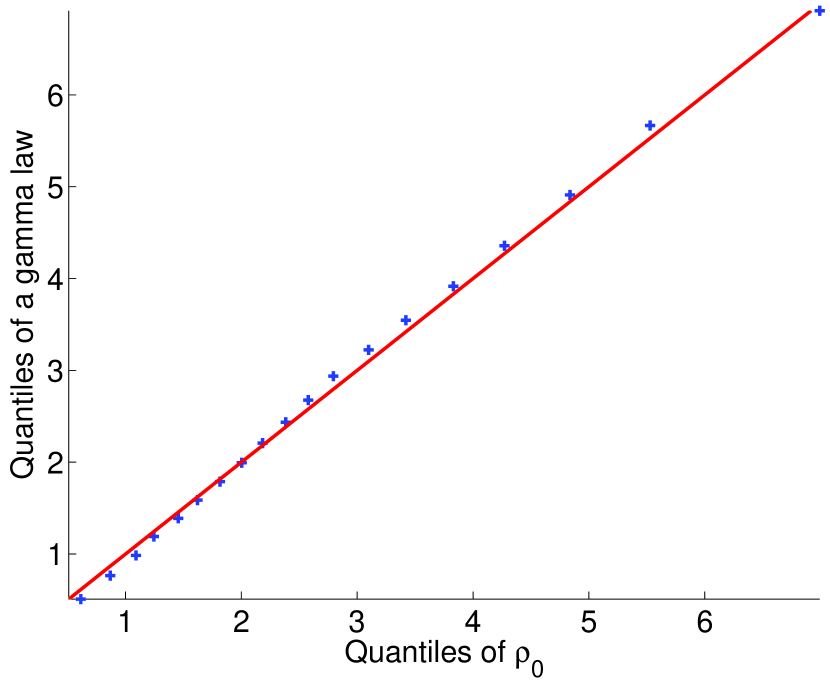

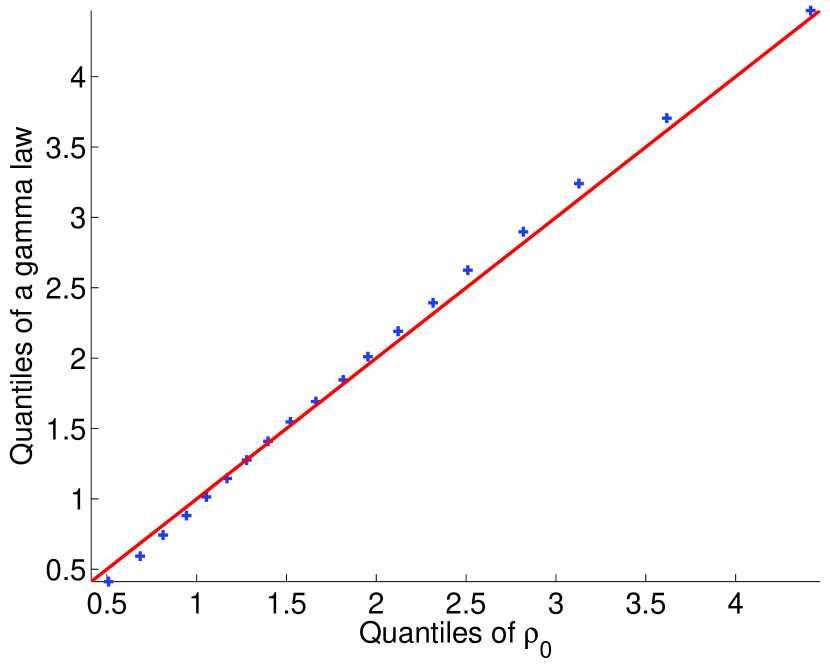

VI-A Loads distribution

On figure 1 we compare the distribution of the loads obtained by simulation to a gamma distribution with the same mean and variance for using a quantile-to-quantile plot. For the three values of we observe a good fit between the two. It is noted that from the results of [15], even the area of the Voronoi cell does not follow a gamma distribution, so in general the load cannot be gamma distributed. For practical purposes however, the gamma distribution provides a good approximation.

It is noted that choosing a gamma distribution with the same mean and variance is not the maximum likelihood estimation, since the maximum likelihood involves the expectation of the logarithm of the load. We use this moment estimator because we only know the mean and variance of the loads by Theorems 4 and 5. We recall that from corollary 6 the load distribution becomes heavy-tailed () when , so that it cannot be approximated by a light-tailed distribution such as the gamma in this case.

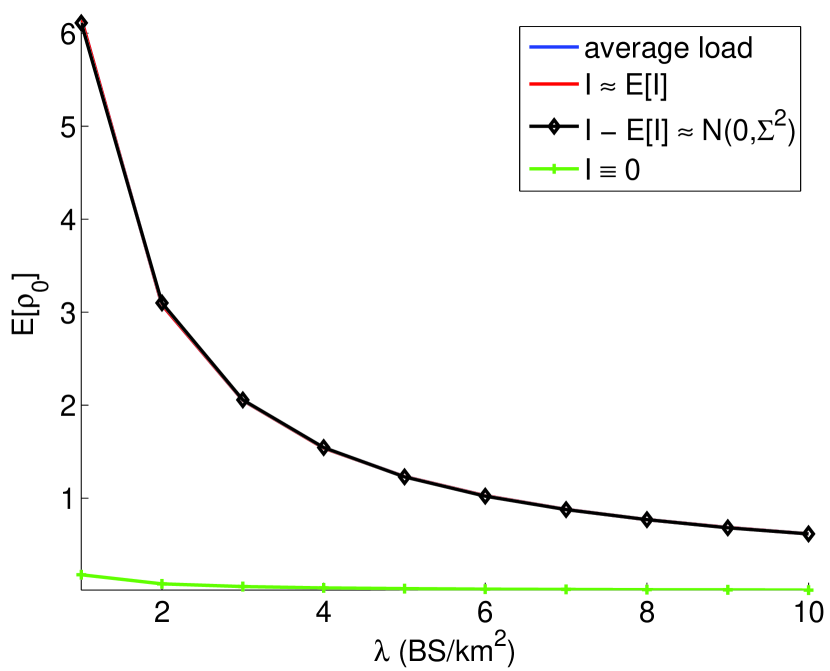

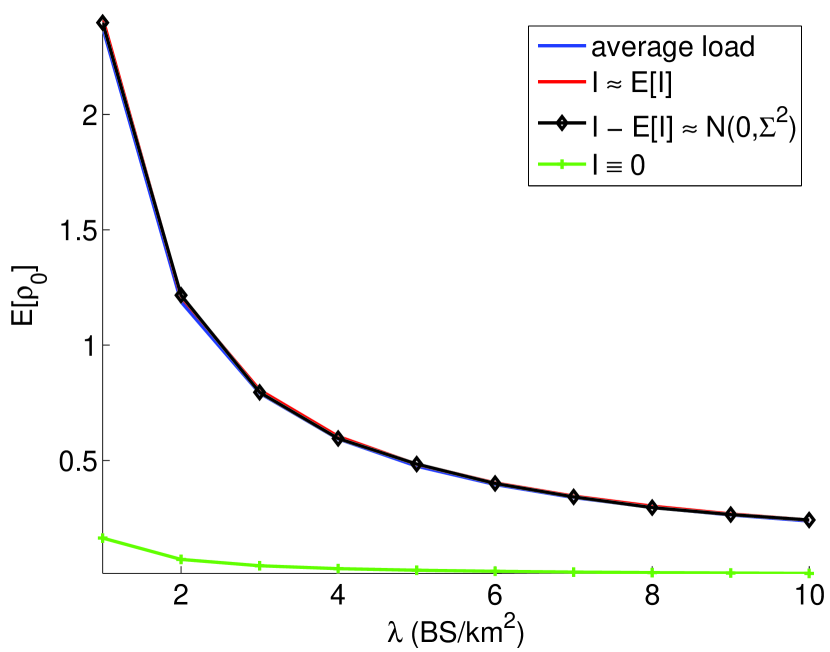

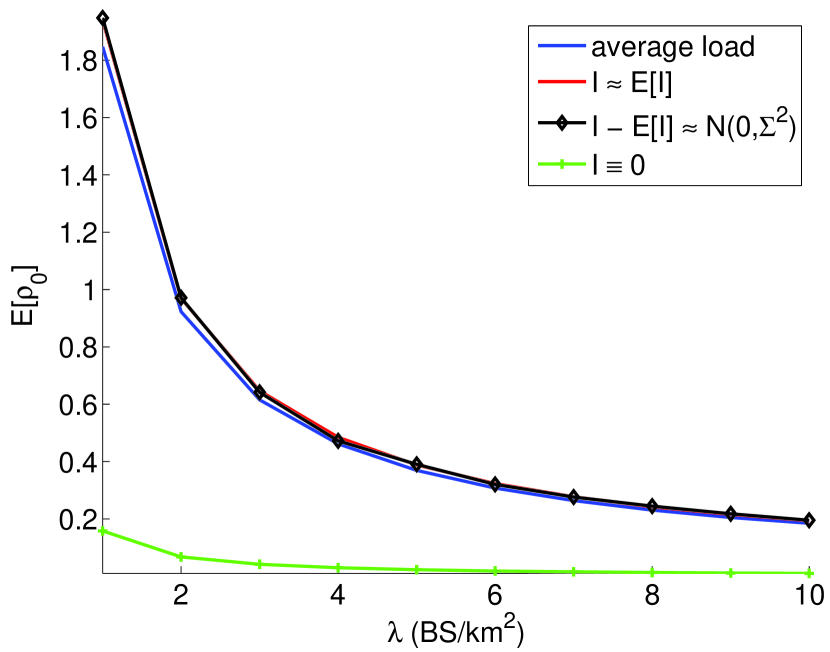

VI-B Average loads

On figure 3, we plot the average load as a function of the BS density with . The four curves are denoted:

- •

-

•

b) “”: an approximation of the average load by replacing the interference at a given location by its expectation .

-

•

c) “”: an approximation of the average load by replacing the interference at a given location by a normally distributed r.v. with variance given by corollary 7.

-

•

d) “”: the average load when there is no interference, i.e .

When increases, the interference increases, but the size of the typical cell decreases so that the amount of traffic served by a given BS decreases. Namely there is more interference but less congestion. On all curves, the average load decreases with which shows that the effect of reduced congestion dominates the effect of increased interference.

We observe that approximations b) and c) are fairly accurate, and that the accuracy is better when is close to . This is because, when decreases, the ratio between interference and path loss increases, we get closer to the low SINR regime and becomes closer to a linear function as explained in subsection III-B. The same argument also justifies the fact that for a given value of , the average load increases when the path-loss exponent decreases.

There is a large difference between the load with interference a) and without d), showing that taking into account interference for predicting the loads distribution is indeed necessary.

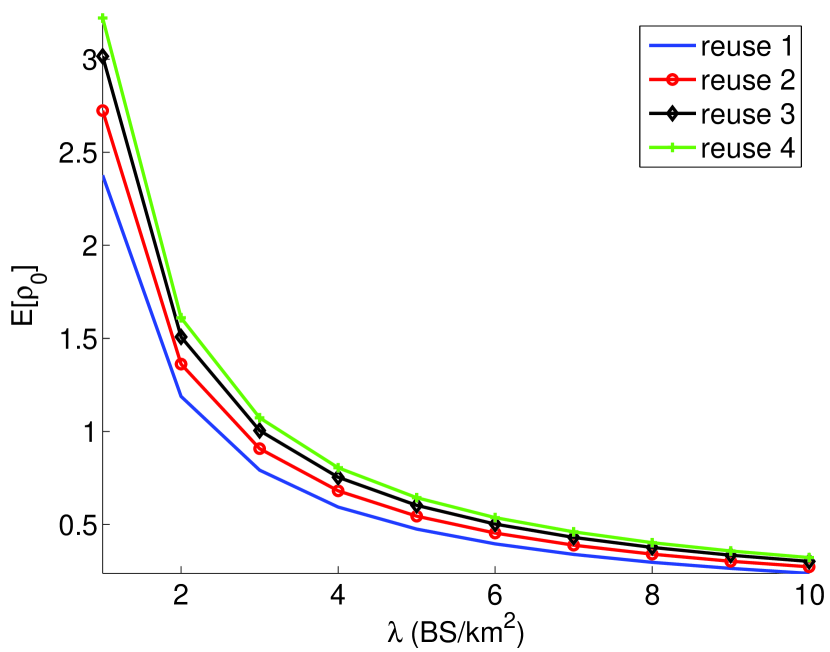

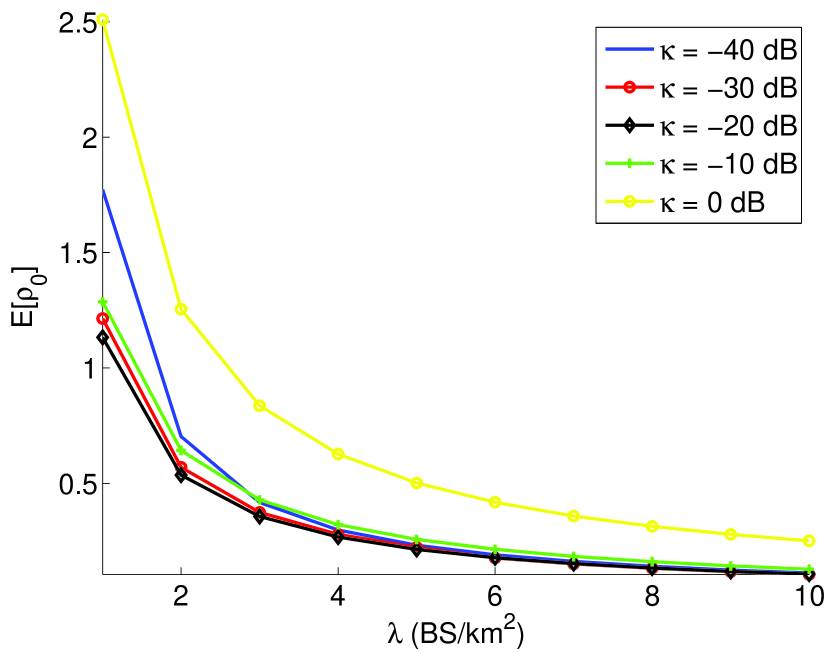

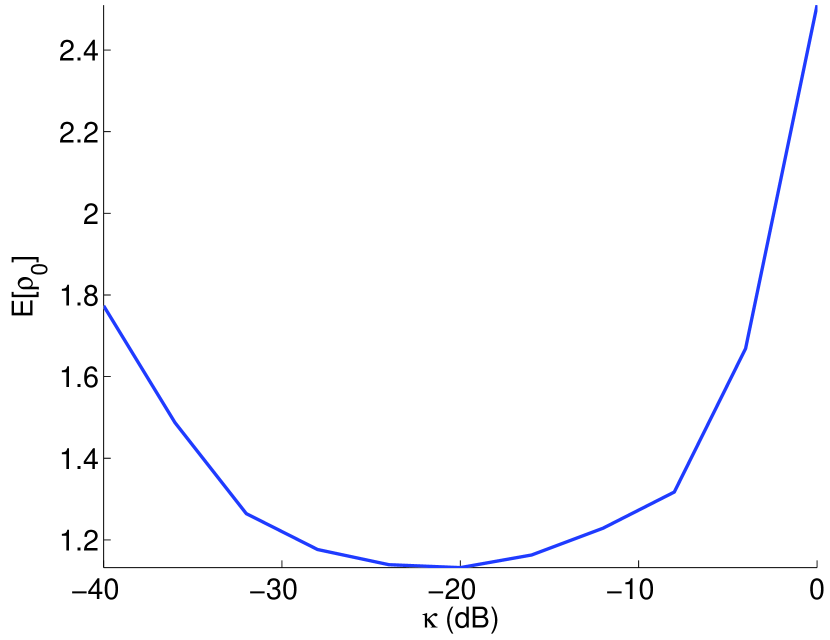

VI-C Frequency reuse

On figure 3, we plot the average load as a function of for different frequency reuse strategies as explained in subsection III-B4. On figure 3(a) we consider hard reuse with reuse factor . On figure 3(b) we consider soft reuse with and dB. For each value of and , the threshold between edge and center is chosen so that the average load of the center and edge are equal: . On figure 3(c) we consider a soft reuse with , and dB.

We see that hard reuse schemes actually diminish the network performance by increasing the average load. Reuse gives the best performance. This is true regardless of the BS density . On the other hand, soft reuse schemes bring considerable improvement. The value dB gives the best performance, and the average load for this value is about half of the average load for reuse . This shows that for PPP networks, soft frequency reuse allows to serve twice as much traffic with the same number of BS.

Those results are in line with previous work such as [40] where the capacity of a regular network (possibly with small random perturbations) serving elastic traffic was studied. Namely soft reuse increases the network performance noticeably, while hard reuse brings little to no improvement. A noticeable difference though is that the optimal power reduction for the completely random PPP networks is dB, while for regular networks it is around dB. Namely there is more than an order of magnitude of difference.

optimal

VII Conclusion

We have considered the flow-level performance of random wireless networks. The locations of BS follow a PPP. We take into account flow-level dynamics by modeling each BS as a queue. The performance and stability of each BS depends on its load. In certain cases the full distribution of the load has been derived through its Laplace transform. In all cases, we have given formulas to calculate the first and second moments of the loads. Networks on the line and on the plane have both been considered. Our model is generic enough to include features of recent wireless networks such as 4G networks (LTE). In dense networks, we have shown that the inter-cell interference power becomes normally distributed. Hence some computations reduce to an integral with respect to the Gaussian distribution. Using numerical experiments we have demonstrated that in certain cases of practical interest, the loads distribution can be approximated by a gamma distribution with known mean and variance, and that this approximation is very accurate.

Acknowledgment

The authors are thankful to Alexandre Proutière for his helpful comments on the traffic models.

References

- [1] F. Baccelli and B. Blaszczyszyn, “Stochastic geometry and wireless networks, volume 1: Theory,” Foundations and Trends in Networking, vol. 3, no. 3-4, pp. 249–449, 2009.

- [2] ——, “Stochastic geometry and wireless networks, volume 2: Applications,” Foundations and Trends in Networking, vol. 4, no. 1-2, pp. 1–312, 2009.

- [3] J. Kaufman, “Blocking in a shared resource environment,” IEEE Transactions on Communications, vol. 29, no. 10, pp. 1474 – 1481, oct 1981.

- [4] J. W. Roberts, “A service system with heterogeneous user requirements,” in Performance of Data Communications Systems and Their Applications, 1981, pp. 423–431.

- [5] F. Baccelli, B. Blaszczyszyn, and M. K. Karray, “Blocking rates in large CDMA networks via a spatial erlang formula,” INRIA, Rapport de recherche RR-5517, 2005.

- [6] T. Bonald and A. Proutière, “Wireless downlink data channels: User performance and cell dimensioning,” in Proceedings of ACM MOBICOM, 2003.

- [7] E. Altman, “Capacity of multi-service cellular networks with transmission-rate control: a queueing analysis,” in Proceedings of ACM MOBICOM, 2002, pp. 205–214.

- [8] T. Bonald and A. Proutière, “On performance bounds for the integration of elastic and adaptive streaming flows,” SIGMETRICS Perform. Eval. Rev., vol. 32, no. 1, pp. 235–245, Jun. 2004.

- [9] E. N. Gilbert, “Random subdivisions of space into crystals,” The Annals of Mathematical Statistics, vol. 33, no. 3, pp. 958–972, 1962.

- [10] T. Kiang, “Random Fragmentation in Two and Three Dimensions,” Zeitschrift für Astrophysik, vol. 64, p. 433, 1966.

- [11] J.-S. Ferenc and Z. Néda, “On the size distribution of Poisson Voronoi cells,” Physica A Statistical Mechanics and its Applications, vol. 385, pp. 518–526, Nov. 2007.

- [12] P. Calka, “The distributions of the smallest disks containing the Poisson-Voronoi typical cell and the Crofton cell in the plane,” Advances in Applied Probability, vol. 34, no. 4, pp. 702–717, 2002.

- [13] ——, “An explicit expression for the distribution of the number of sides of the typical Poisson-Voronoi cell,” Advances in Applied Probability, vol. 35, no. 4, pp. 863–870, 2003.

- [14] S. A. Zuyev, “Estimates for distributions of the Voronoi polygon’s geometric characteristics,” Random Struct. Algorithms, pp. 149–162, 1992.

- [15] P. Calka, “Precise formulae for the distributions of the principal geometric characteristics of the typical cells of a two-dimensional Poisson-Voronoi tessellation and a Poisson line process,” Advances in Applied Probability, vol. 35, no. 3, pp. 551–562, 2003.

- [16] J. Møller and S. Zuyev, “Gamma-type results and other related properties of Poisson processes,” Advances in Applied Probability, vol. 28, no. 3, pp. 662–673, 1996.

- [17] S. G. Foss and S. A. Zuyev, “On a Voronoi aggregative process related to a bivariate Poisson process,” Advances in Applied Probability, vol. 28, no. 4, pp. 965–981, 1996.

- [18] F. Baccelli, B. Blaszczyszyn, and F. Tournois, “Spatial averages of coverage characteristics in large CDMA networks,” Wireless Networks, vol. 8, no. 6, pp. 569–586, 2002.

- [19] J. G. Andrews, F. Baccelli, and R. K. Ganti, “A tractable approach to coverage and rate in cellular networks,” IEEE Transactions on Communications, vol. 59, no. 11, pp. 3122–3134, Nov. 2011.

- [20] T. Novlan, H. Dhillon, and J. Andrews, “Analytical modeling of uplink cellular networks,” IEEE Transactions on Wireless Communications, no. 99, pp. 1–11, 2013.

- [21] S. Singh, H. Dhillon, and J. Andrews, “Offloading in heterogeneous networks: Modeling, analysis, and design insights,” IEEE Transactions on Wireless Communications, vol. 12, no. 5, pp. 2484–2497, 2013.

- [22] H. Dhillon, R. Ganti, and J. Andrews, “Load-aware modeling and analysis of heterogeneous cellular networks,” IEEE Transactions on Wireless Communications, vol. 12, no. 4, pp. 1666–1677, 2013.

- [23] H. Dhillon, R. Ganti, F. Baccelli, and J. Andrews, “Modeling and analysis of k-tier downlink heterogeneous cellular networks,” IEEE Journal on Selected Areas in Communications, vol. 30, no. 3, pp. 550–560, 2012.

- [24] T. Novlan, R. Ganti, A. Ghosh, and J. Andrews, “Analytical evaluation of fractional frequency reuse for heterogeneous cellular networks,” IEEE Transactions on Communications, vol. 60, no. 7, pp. 2029–2039, 2012.

- [25] X. Lin, J. G. Andrews, and A. Ghosh, “Modeling, analysis and design for carrier aggregation in heterogeneous cellular networks,” CoRR, vol. abs/1211.4041, 2012.

- [26] H.-S. Jo, Y. J. Sang, P. Xia, and J. G. Andrews, “Heterogeneous cellular networks with flexible cell association: A comprehensive downlink SINR analysis,” CoRR, vol. abs/1107.3602, 2011.

- [27] L. Decreusefond, P. Martins, and T.-T. Vu, “An analytical model for evaluating outage and handover probability of cellular wireless networks,” in Proceedings of WPMC, Taïwan, 2012, pp. 1–5.

- [28] R. Ganti, F. Baccelli, and J. Andrews, “Series expansion for interference in wireless networks,” IEEE Transactions on Information Theory, vol. 58, no. 4, pp. 2194–2205, 2012.

- [29] A. Guo and M. Haenggi, “Spatial Stochastic Models and Metrics for the Structure of Base Stations in Cellular Networks,” IEEE Transactions on Wireless Communications, 2013, submitted. Available at http://www.nd.edu/ mhaenggi/pubs/twc13b.pdf.

- [30] S. M. Yu and S.-L. Kim, “Downlink capacity and base station density in cellular networks,” CoRR, vol. abs/1109.2992, 2011.

- [31] S. Lowen and M. Teich, “Power-law shot noise,” IEEE Transactions on Information Theory, vol. 36, no. 6, pp. 1302 –1318, nov 1990.

- [32] K. Gulati, B. Evans, J. Andrews, and K. Tinsley, “Statistics of co-channel interference in a field of Poisson and Poisson-Poisson clustered interferers,” IEEE Transactions on Signal Processing, vol. 58, no. 12, pp. 6207–6222, 2010.

- [33] D. J. Dalay and D. Vere-Jones, An introduction to the theory of point processes. Springer, 2002.

- [34] L. Kleinrock, Queueing Systems: Theory. Wiley, 1976, vol. 1.

- [35] T. Bonald and M. Feuillet, Network Performance Analysis. ISTE Ltd and John Wiley and Sons Inc, September 2011.

- [36] P. Mogensen, W. Na, I. Kovacs, F. Frederiksen, A. Pokhariyal, K. Pedersen, T. Kolding, K. Hugl, and M. Kuusela, “LTE capacity compared to the Shannon bound,” in Proceedings of IEEE VTC, 2007, pp. 1234–1238.

- [37] B. Błaszczyszyn and M. K. Karray, “Fading effect on the dynamic performance evaluation of OFDMA cellular networks,” in Proceedings of ComNet, 2009.

- [38] R. Combes, Z. Altman, and E. Altman, “Scheduling gain for frequency-selective rayleigh-fading channels with application to self-organizing packet scheduling,” Performance Evaluation, Feb. 2011.

- [39] S. Borst, “User-level performance of channel-aware scheduling algorithms in wireless data networks,” IEEE/ACM Transactions on Networking, vol. 13, no. 3, pp. 636–647, Jun. 2005.

- [40] T. Bonald and N. Hegde, “Capacity gains of some frequency reuse schemes in OFDMA networks,” in Proceedings of IEEE GLOBECOM, dec. 2009, pp. 1–6.

- [41] T. Bonald, S. Borst, N. Hegde, and A. Proutière, “Wireless data performance in multi-cell scenarios,” in Proceedings of ACM SIGMETRICS, 2004, pp. 378–387.

- [42] D. Tsilimantos, J.-M. Gorce, and E. Altman, “Stochastic Analysis of Energy Savings with Sleep Mode in OFDMA Wireless Networks,” in Proceedings of IEEE INFOCOM, 2013.

- [43] W. Weibull, “A statistical distribution function of wide applicability,” Journal of Applied Mechanics, vol. 18, pp. 293–297, 1951.

- [44] F. Yilmaz and M.-S. Alouini, “Sum of Weibull variates and performance of diversity systems,” in Proceedings of IWCMC, 2009, pp. 247–252.

- [45] W. Davenport and W. Root, An introduction to the theory of random signals and noise, ser. Lincoln Laboratory publications. McGraw-Hill, 1958.

- [46] W. Feller, An introduction to probability theory and its applications, ser. Wiley series in probability and mathematical statistics. Probability and mathematical statistics. Wiley, 1966.

- [47] C. Gloaguen, F. Fleischer, H. Schmidt, and V. Schmidt, “Simulation of typical Cox-Voronoi cells with a special regard to implementation tests,” Math. Meth. of OR, vol. 62, no. 3, pp. 357–373, 2005.

Appendix A Auxiliary results on shot noise generated by a PPP

A-A Laplace transform of shot noise

The Laplace transform of shot noise is given by Theorem 2. A proof can be found for instance in [1].

Proposition 2.

Consider a PPP on with measure . for all , , : with strictly positive real part:

A-B Expectation of a function of shot noise

It is noted that once the Fourier/Laplace transform of a random variable is known, the expectation of any function of can be calculated using the Plancherel-Parseval theorem recalled in proposition 3.

Proposition 3 (Plancherel theorem).

Consider a real random variable and a positive function:

with the Fourier transform of , and the complex conjugate of .

It is noted that if is not square integrable, the Fourier transform should be taken in the sense of tempered distributions.

A-C Shot noise distributions of interest

We can specialize Theorem 2 to obtain results on the distribution of shot noise generated by an homogenous PPP, conditional to the event .

Proposition 4.

The Laplace transform of , conditional to is:

and its first and second moments are:

Proof.

By specialization of theorem 2 to and :

Once again, using polar coordinates and centering (i.e ) gives the result:

∎

Proposition 5.

With assumptions 1, the Laplace transform of , conditional to is given by:

with the lower incomplete gamma function and the gamma function. Its first and second moments are:

Proof.

See [19]. ∎

Appendix B Proofs

B-A Proof of theorem 1

B-B Proof of theorem 2

Proof.

We first consider to be known. The interference at can be decomposed into:

The interference dependent term in (6) can be written:

| (12) |

By definition of (eq. IV-C), the r.h.s. of (B-B) becomes:

| (13) |

The third term on the r.h.s. of (B-B) is a shot noise with respect to the point process , with impulse response . Conditional to , is a PPP on with intensity . Hence we can apply proposition 2:

| (14) |

Furthermore, the Laplace transform of the two first terms of (B-B) is:

| (15) |

Combining (B-B) and (B-B) we obtain the Laplace transform of the interference dependent term in (6):

The Laplace transform of the load conditional to is then:

| (16) |

Since are i.i.d. and exponentially distributed, the load distribution is obtained by un-conditioning (B-B):

| (17) |

The expression under the integral in (B-B) is symmetrical in which proves the result. ∎

B-C Proof of Theorem 3

Proof.

We first write the definition of the load:

Taking expectations:

The probability of belonging to is given as a void probability of the PPP:

and by conditioning on , we obtain the first result:

Conditional to , is a PPP on with intensity . Hence applying proposition 2 proves the second result. ∎

B-D Proof of Theorem 5

B-E Proof of Corollary 6

Proof.

By concavity of the logarithm:

Applying corollary 5, with and :

We have that:

and:

We have used the following identity twice (by a change of variables):

for . We obtain the announced result by summing:

∎

B-F Proof of Theorem 6

Instead of proving Theorem 6, we prove a more general result, Theorem 7. We introduce assumption 4 on the decay of the path loss function . In particular, with assumption 1, assumption 4 holds.

Assumptions 4.

There exists , and a constant such that for .

Theorem 7.

Consider a PPP on with measure where and is a measure on such that the following integrals are finite for all :

-

•

,

-

•

.

Furthermore we assume that for all , where is taken with respect to measure and that .

For all , , converges in distribution to a multivariate normal distribution when . Namely:

with its covariance matrix. The covariance is given by:

Proof.

We recall the Laplace transform of the shot noise from proposition 2:

| (20) |

The expectation of shot noise is given by:

| (21) |

Replacing (21) in (B-F) we have that:

Consider fixed and consider . Since , there exists so that -almost everywhere:

Using a Taylor expansion for in a neighborhood of , there exists a function such that:

with , . Therefore:

| (22) |

It is noted that we can choose arbitrarily small when is arbitrarily large. Therefore the r.h.s. of equation (B-F) is, up to a negligible term, the Laplace transform of the multivariate Gaussian distribution which proves the convergence in distribution.

The covariance is obtained by inspection of the Laplace transform (B-F). ∎