Iterative Estimation of Solutions to Noisy Nonlinear Operator Equations in Nonparametric Instrumental Regression

Abstract: This paper discusses the solution of nonlinear integral equations with noisy integral kernels as they appear in nonparametric instrumental regression. We propose a regularized Newton-type iteration and establish convergence and convergence rate results. A particular emphasis is on instrumental regression models where the usual conditional mean assumption is replaced by a stronger independence assumption. We demonstrate for the case of a binary instrument that our approach allows the correct estimation of regression functions which are not identifiable with the standard model. This is illustrated in computed examples with simulated data.

MSC: AMS 2000 subject classification.

primary 62G08, secondary 62G20

JEL classification: C13, C14, C30, C31, C36

Keywords and phrases: Nonparametric regression, nonlinear inverse problems, iterative regularization, instrumental regression

1 Introduction

In this paper we will propose and analyze an iterative method for estimating the solution of nonlinear integral equations which appear in nonparametric instrumental regression problems. Examples will be discussed below, see eq. (4) and Section 2. Such integral equations can be written as nonlinear operator equations

| (1) |

where the operator is unknown, but where an estimator of is available. We will assume that maps from a convex set in a Banach space to a Hilbert space . Typically such operator equations are ill-posed in the sense that is not continuous. In particular this is the case for integral operators with smooth kernels on a compact set. In such cases the straightforward estimator will not be consistent since it has infinite variance. Regularization techniques must be applied to solve (1) or its empirical version . We will use a generalized version of the iteratively regularized Gauß-Newton method. In numerical analysis this is one of the most popular computational methods for solving nonlinear ill-posed operator equations. It avoids some problems of nonlinear Tikhonov regularization given by

| (2) |

where is some initial guess of . In practice the iteratively regularized Gauß-Newton method does not suffer from the problem that minima of the functional in (2) need not to be unique and it avoids computational difficulties due to the presence of local minima. We will compare both methods in more details later. Moreover, instead of a quadratic penalty, we allow for a more general penalty term with domain of definition . We only assume that is a convex, lower semi-continuous functional that is not identically equal to . With this choice an iteratively regularized Gauß-Newton method is given by the iterations

| (3) |

In each Newton step a convex optimization problem has to be solved with a sequence of regularization parameters . We assume that tends to in a way that will be specified in Section 4. In the special case that is a Hilbert space, the most common choice for the penalty term is . Here is the norm of the Hilbert space and is the initial guess at which the iteration is started. This is the iteratively regularized Gauß-Newton method as suggested by Bakushinskiĭ (1992) and further analyzed by Blaschke et al. (1997) and Hohage (1997) for low order Hölder or logarithmic source conditions, respectively. We also refer to the monographs by Bakushinskiĭ and Kokurin (2004) and Kaltenbacher et al. (2008) and to further references therein.

The use of more general convex regularization terms in the general case where is a Banach space allows for a flexible incorporation of further a-priori information. Common choices are entropy regularization, penalties and bounded variation () penalties. Loubes and Pelletier (2008) studied entropy regularization for instrumental variable models but they gave no theoretical results for the rates of convergence of their estimators. If a basis or a frame of is given, an penalty of the coefficients with respect to this basis or frame enhances sparsity properties of the estimator with respect to this basis or frame. A penalty is particularly appropriate for piecewise constant estimates.

Our main result gives rates of convergence for the estimator where the distance between the estimator and the solution of (1) is measured by the Bregman distance, see Theorem 1. For entropy regularization this directly implies convergence estimates measured by the -norm. Our scheme allows for the incorporation of structural a-priori information of the form where is a closed convex set (e.g. a-priori information on non-negativity, monotonicity or convexity/concavity). This can be done by setting if .

For convex regularization terms, the analysis differs from the mathematical approaches used for studying quadratic regularization. One has to employ variational methods rather than spectral methods. Recently, a number of papers have appeared on this subject, we only mention Eggermont (1993), Burger and Osher (2004), Resmerita (2005), Hofmann et al. (2007), Scherzer et al. (2009). A first variational convergence rate analysis of Newton-type methods in a deterministic setting without errors in the operator and given by Banach norms has recently been done by Kaltenbacher and Hofmann (2010). Our analysis is closest to that of the last reference. However, all the references above only treat perturbations of the right hand side of the operator equation, and hence these results are not applicable to nonparametric instrumental regression. Our treatment of nonlinear ill-posed operator equations with errors in the operator may be of independent interest and relevant for other applications.

For the special case that is a Hilbert space convergence rates of the nonlinear Tikhonov regularization were discussed in Engl et al. (1989) in a deterministic setting. Rates for a model with random errors were obtained in Bissantz et al. (2004). In Horowitz and Lee (2007) nonparametric instrumental variables estimation is considered in a quantile regression model. This is one example of a statistical model where the unknown nonparametric function is given as the solution of a nonlinear integral equation. We will describe this model in the next section.

In Horowitz and Lee (2007) it is assumed that the singular values of the Fréchet derivative decay polynomially and results are given on the rates of convergence under these assumptions. Horowitz and Lee pointed out that a convergence analysis for exponentially decreasing singular values is an important open problem. We will show that singular values of integral operators with infinitely smooth kernels do in fact decrease super-algebraically and present a convergence analysis without an assumption on the rate of decay of the singular values.

Besides the analysis of the iteratively regularized Gauß-Newton method for noisy operators the second main innovation of this paper is a nonparametric instrumental regression models where the instrument is independent from the error :

| (4a) | |||

| (4b) | |||

| (4c) | |||

Here, is a scalar response variable, is an observed random vector of endogeneous explanatory variables. It is shown in Section 2 that this model leads to a nonlinear integral equation of the form (1) with a kernel, that has to be estimated from data.

This model slightly differs from nonparametric instrumental regression with mean independent instruments given by

| (5a) | |||

| (5b) | |||

The latter model has been studied intensively in econometrics by a number of authors, see e.g. Florens (2003), Newey and Powell (2003), Hall and Horowitz (2005), Blundell et al. (2007), Chen and Reiss (2010) and Breunig and Johannes (2009). In this model the regression function is defined as the solution of a linear first kind integral equation

| (6) |

where both the kernel of the integral operator and the right hand side have to be estimated from the data.

Actually, in specific econometric applications, the conditional mean assumption (5b) is typically established by arguing that the stronger independence assumption (4b) holds. Therefore, it is a natural question if one can improve the accuracy of estimation of by using the stronger condition (4c), (4b) directly. We will give a first partial positive answer to this question: a necessary condition for identifiability in the model (5) is that the instrumental variable must have at least as many continuously distributed components as the explanatory variable . This is not necessary in model (4). As an example we will demonstrate that can be identifiable even if is binary and is one-dimensional and continuously distributed. Hence, the model (4) contains strictly more information on than the model (5). A more detailed comparison of the two models is very complex because the integral equations obtained from these two models are related only very implicitly.

The plan of this paper is as follows: in the following section we give more details on our motivating examples from instrumental variable regression. Section 3 recalls the definition of source conditions and discusses their relation to smoothness conditions. In particular, we show that for integral equations of the first kind with smooth kernels, Hölder type source conditions are too restrictive, and discuss variational forms of source conditions. In Section 4 we present our main convergence result for the iteratively regularized Gauß-Newton method with noisy operators. Afterwards, we discuss in Section 5 how this result applies to the regression problem (4). Section 6 reports on numerical simulations for an instrumental variable regression model with binary instruments.

2 Examples

2.1 Instrumental quantile regression

In Horowitz and Lee (2007) the following quantile regression model has been studied:

| (7a) | |||

| (7b) | |||

Here, is a response variable, is an endogeneous explanatory variable, is a fixed constant, is an unobserved error variable and an observable instrument. The quantile is defined conditional on .

We assume from now on that each of the random variables , and is a vector of continuous or discrete random variables. Further, we assume that a joint density exists with respect to the Lebesgue measure, the counting measure or a product of both measures respectively. Let , and let denote the marginal density of . Then solves a nonlinear operator equation (1) with the operator

It is pointed out in Horowitz and Lee (2007), that the model (7) subsumes nonseparable quantile regression models of the form

| (8) |

as studied in Chernozhukov & Imbens & Newey Chernozhukov et al. (2007), see also Chernozhukov & Hansen Chernozhukov and Hansen (2005). Here is an unobserved, continuously distributed random variable independent of an instrument , and the function is strictly increasing in its second argument. Assuming w.l.o.g. that , (8) reduces to (7) with and .

2.2 Nonparametric regression with independent instruments

2.2.1 Operator equations

The model (4a), (4b) leads to the nonlinear integral equation

| (9a) | |||

| where we assume as above that the joint density of exists. The marginal densities of and are denoted by and respectively. Note that if is a solution to (9a), then any function with is another solution to (9a). The additive constant can be fixed by taking into account eq. (4c), which may be rewritten as | |||

| (9b) | |||

with the marginal densities and of and .

The system of equations (9a), (9b) can be written as a nonlinear ill-posed operator equation (1) with the operator

| (10) |

If we assume the existence of the joint density of unconditional and conditional given , say and respectively we can use the equivalent operator

| (11) |

Alternatively, it may be advantageous to integrate (11) once with respect to . Introducing and yields an other operator formulation of the model (4) with the operator

| (12) |

Let us set . Then the last operators can be written as

2.2.2 Identification

In the following we discuss sufficient conditions for the injectivity of the Gateaux derivative of at the solution . Local identifiability of the nonlinear problem in an open neighborhood of is not necessarily implied by injectivity of . Additional assumptions that guarantee local identifiability are Frechet differentiability and tangential cone conditions, compare (27). For a discussion we refer to Kaltenbacher et al. (2008), Chen et al. (2011) or Florens and Sbaï (2010). The Gateaux derivative of at is given by

where the Gateaux derivative of at satisfies

| (13) |

Injectivity of is equivalent to injectivity of on the linear subspace of functions with . We denote by the marginal density of . Then by employing the independence of and a change of variables allows us to write

| (14) |

Alternatively, we may consider the linear operator

| (15) |

mapping from a function space of mean zero functions in into a function space in . Roughly speaking, injectivity of the operator and hence local identification is possible if the dependence between the endogenous regressor and the error term varies sufficiently with respect to the instrument . The next example illustrates this fact.

Example 1.

Let , and be real valued independent random variables and let be a function defined on and taking values in . Define the endogenous regressor

If and are standard normally distributed, which we assume in this example, then it is easily seen that the conditional distribution of given is Gaussian:

| (16) |

Note that in this situation and are marginally standard normally distributed, both unconditional and conditional on . In other words, and as well as and are independent. But obviously, the random vector and the instrument are dependent. Interestingly, in the commonly studied case of mean independence, that is , identification is guaranteed if and only if the conditional distribution of given is complete (cf. Carrasco et al. (2006)) which rules out the independence of and and hence this example. However, in this example the linear operator defined in (15) can be injective and thus local identification might be still possible. In order to provide sufficient conditions to ensure injectivity of , let us recall the eigenvalue decomposition of the conditional expectation operator for normally distributed random variables.

The following development can be found in Carrasco et al. (2006) while it has been shown thoroughly in Letac (1995). Consider random variables and satisfying

for some . Obviously, and are marginally identically distributed with standard normal density which in turn implies . Note, that by an elementary symmetry argument the conditional expectation operator of given mapping to itself is self-adjoint and hence permits an eigenvalue decomposition. Moreover, for let be the th derivative of and let denote the th Hermite polynomial. The Hermite polynomials form a complete orthogonal system in , see e.g. Problem IV-29 on page 117 in Letac (1995). Furthermore, holds true for all , see e.g. Problem IV-30 on page 120 in Letac (1995). From these assertions we readily conclude that the eigenfunctions of are up to multiples given by the Hermite polynomials and that is the corresponding sequence of eigenvalues.

Keeping in mind that the distribution of conditional on given in (16) is Gaussian let us reconsider the operator defined in (15). By employing that and are independent it is straightforward to conclude that

for all with , where the basis are multiples of the Hermite polynomials. Consequently, the operator is injective if and only if for all , (keep in mind Parseval’s identity, i.e. for all ). This in turn holds if and only if the random variable is not constant. Surprisingly, even in case of a binary instrument taking only two values, say and with , the condition is sufficient to ensure the injectivity of the operator .

Example 2.

We now give another example for injectivity of . We consider again a binary instrument and we make the additional assumption that the conditional copula function of and , given does not depend on . This assumption has been made by Imbens and Newey (2009) in case of a continuous instrument. Under this assumption it holds that is independent of where for the conditional distribution function of given . Note that in the case of a binary instrument injectivity of is equivalent to the injectivity of the map

on the space of all functions with . We use that

because of independence of and . If the family of conditional densities of given is complete this equation implies that almost surely. The latter equation can be used to get that under some additional assumptions on the function is almost surely constant, see the arguments used in Torgovitsky (2012) and D’Haultfœuille and Février (2011). Because of we get that a.s. Thus is invertible. Note that our discussion differs from the results in Imbens and Newey (2009), Torgovitsky (2012) and D’Haultfœuille and Février (2011). We make the assumption on the conditional copula function only for the underlying distribution and argue that - under additional conditions - local identifiability holds for a neighborhood of distributions for which this assumption may not apply whereas in the latter papers the conditional copula assumption is used as a model assumption for all distributions of the statistical model. This heuristic discussion can be generalized to more general instruments with discrete and/or continuous components.

We will continue the discussion of binary instruments in the next subsection. Section 6 contains further numerical evidence of identifiability in a particular case.

2.2.3 Binary instruments

We consider the above mentioned special case that the instrument is binary and it only takes the values and . Furthermore, the explanatory variable is a scalar. Then the marginal density (w.r.t. the counting measure) has the two values

Equation (9a) is equivalent to the system of equations

It follows from the identity that these two equations are linearly dependent and can be rewritten as

| (17) |

So is a root of the nonlinear ill-posed operator

| (18) |

In analogy to (12), the equation can equivalently be rewritten as with

| (19) |

3 Smoothness in terms of source conditions

In this section we collect some material on source conditions that will be needed in the next section to state our main result. We are primarily interested in source conditions in Banach spaces. However, we start with a motivation for spaces and present in a first step a definition of source conditions in the special case of Hilbert spaces. For the sake of simplicity we discuss the relevance of source conditions for nonparametric instrumental regression problems in this special case. Afterward, we introduce source conditions for the general case of Banach spaces.

3.1 Source conditions in Hilbert spaces

Let us recall the relationship between the smoothness of a kernel of a compact linear integral operator ,

and the decay of its singular values . If is a singular system of , then according to the Courant-Fischer characterization (see e.g. Kress (1999)) of the singular values the operator with kernel satisfies

In particular, if there exist functions , , and numbers for all such that , then since . It follows from standard results in approximation theory (see e.g. Prössdorf and Silbermann (1991)) that for smooth bounded domains the singular values decay at least polynomially if belongs to a Sobolev space, super-algebraically if , and at least exponentially if is analytic.

In regularization theory, smoothness of the solution to an inverse problem is usually formulated in terms of source conditions, which describe smoothness relative to the smoothing properties of the operator. For a linear operator between Hilbert spaces and , such source conditions have the form

| (20) |

Here , is an initial guess (typically in the linear case), is the adjoint operator of with respect to the scalar product of the Hilbert space, and is a continuous, strictly monotonically increasing function with . is defined by using the spectral calculus. So with the notations above . For a nonlinear operator between Hilbert spaces the Gateaux derivative at is used.

If we choose a fixed the source condition is the more restrictive the faster the singular values decay. I.e. for integral operators it is the more restrictive the smoother the kernel. For the most common choice for some these condition are called Hölder-type source conditions. We refer to the monographs Engl et al. (1996); Bakushinskiĭ and Kokurin (2004); Kaltenbacher et al. (2008) for further information.

3.2 Impact on nonparametric instrumental regression

Let us discuss source conditions in the context of nonparametric instrumental variable models. The kernel of the integral operator in (13) is composed of probability densities. For the derivatives of the alternative operators (10) and (11) it is composed of partial derivatives of densities. Many typical probability density functions are analytic, i.e. the density of the normal. Hence, in applications it will frequently occur that the kernel of the operator in the source condition is infinitely smooth or even analytic.

Let us have a closer look at these cases. The singular values of the operator in (13) will decay super-algebraically or even exponentially. As a consequence, Hölder-type source conditions are extremely restrictive smoothness conditions, since the eigenvalues will decay super-algebraically or exponentially, too. Hence, Hölder-type source conditions imply that the Fourier coefficients with respect to of the difference between initial guess and regression function decay super-algebraically or exponentially. For standard Fourier coefficients this entails that has to be infinitely smooth or even analytic. Hence, the initial guess must be very good and already capture some features of the unknown function . In applications, one would typically expect only polynomial decay of the Fourier coefficients of which corresponds to finite Sobolev smoothness instead of infinite smoothness. Therefore, it is desirable to consider also functions which decay to more slowly than . For exponentially decaying singular values the logarithmic functions

with a parameter are a natural choice corresponding to a polynomial decay of the Fourier coefficients of . (Here we always assume that the operator is scaled such that or alternatively use a dilated version of the above function .) The importance of logarithmic source conditions for nonparametric instrumental regression is also pointed out in Blundell et al. (2007) and Horowitz and Lee (2007).

3.3 Variational source conditions for Banach spaces

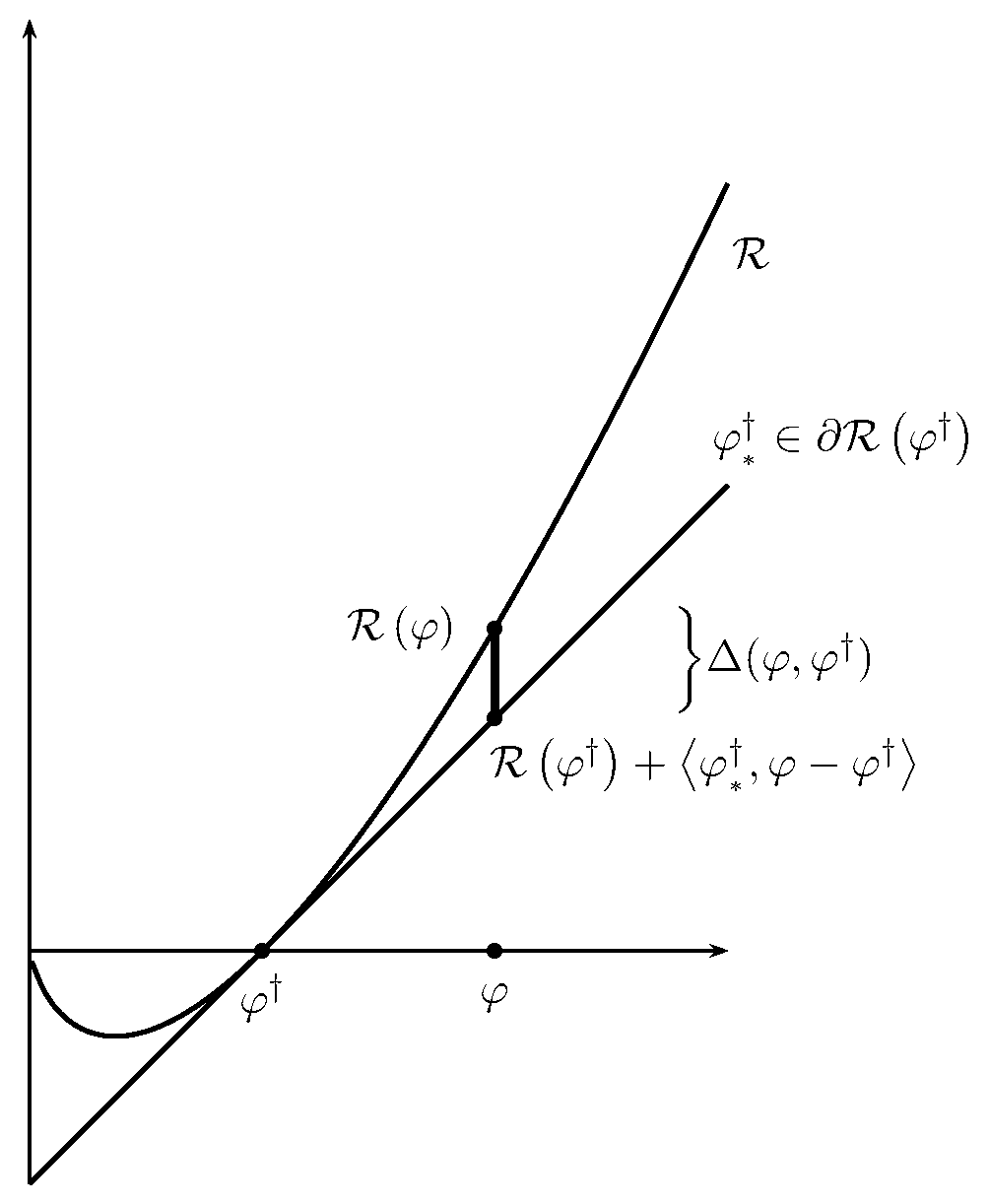

In our analysis we will not restrict ourselves to Hilbert spaces, but study the more general situation where is a Banach space, which we assume in the following. Note that in this case the operator maps from to the dual space , so even integer powers of are not well-defined. Therefore, spectral source conditions as introduced above must be generalized. For this purpose we use variational methods which have been explored in regularization theory recently in a number of papers. We will prove convergence results with these methods in terms of the Bregman distance in with respect to the convex functional .

Let be a fixed element of the subdifferential of at (i.e. , if is differentiable at ). Then the Bregman distance with respect to and is defined as

| (21) |

Here denotes the classical dual paring , i.e. is the evaluation of the functional at . Hence, the Bregman distance measures how much the linearization of at and differ at the point . This is illustrated in Figure 1. For strictly convex we have if and only if . The Bregman distance is nonnegative and convex in the first argument, but it does not define a metric since it is neither symmetric nor does it satisfy the triangle inequality in general. However, Bregman distances provide a generalization of the simpler case, where is a Hilbert space and for some . Because, in this situation

Although, Bregman distances are in general not metrics they have meaningful interpretations in some Banach space settings. If and (entropy regularization), then can be bounded from below by (see e.g.Resmerita (2005)), i.e. the error bounds formulated in the next theorem can be interpreted as bounds with respect to the squared norm. Our framework also allows the incorporation of convex constraints by setting if does not belong to some convex set . Obviously, this does not change in .

Following Kaltenbacher and Hofmann (2010) we formulate the source condition as a variational inequality

| (22) |

Again, this is a generalization of the Hilbert space case. It is shown in Kaltenbacher and Hofmann (2010) that if is a Hilbert space, and is convex, the classical source condition (20) implies the variational one (22).

Let us close this section with a technical remark. Note that if is chosen such that is on the boundary of , then possibly can be chosen smaller than in the case where is in the interior of . Theorem 1 yields that this may lead to faster rates of convergence. Hence, a convex constraint on the regression function can improve estimation. To captures this fact it is important that, opposed to the formulation in Kaltenbacher and Hofmann (2010), no absolute values appear on the left hand side of (22). A typical example where is on the boundary of is the assumption that is a positive function.

4 Convergence results

Let be a Banach space, a Hilbert space, convex and a root of the operator :

| (23) |

Assume that is approximated by a series of estimators

which maps to some (possibly finite-dimensional and/or data dependent) Hilbert space . and all are assumed to be Gateaux differentiable on with linear derivatives and , which are “bounded with respect to ” in the sense that

| (24) |

whenever and analogously for all . Now we can state the main theorem of this paper, which is proved in Appendix A:

Theorem 1.

Let (22) hold true with a concave for which is monotonically increasing. Assume that the sequence has the following convergence properties:

| (25a) | |||

| (25b) | |||

| (25c) | |||

Here must be sufficiently small, such that . Suppose that the convex minimization problems (3) are uniquely solvable for every (see Remark 1 for sufficient conditions), i.e. the method is well defined. Further assume that and that for all with a constant . Let the iteration be stopped at the smallest index for which

| (26) |

Then

Remarks:

-

1.

Sufficient conditions for uniqueness of solutions to the minimization problem (3) are strict convexity of or injectivity of .

-

2.

Sufficient conditions for existence are reflexivity of , weak closedness of , and the boundedness of the sets in for any . This is a standard argument: If is a minimizing sequence, it must be bounded due to our last condition. Since is reflexive, there exists a weakly convergent subsequence, and by weak closedness of a weak limit point . Since the Tikhonov functional is convex and lower semi-continuous, it is also weakly lower semi-continuous, and hence is a minimizer.

-

3.

Note that if is a Hilbert space and Fréchet differentiable, then , so .

-

4.

The bound on the Taylor remainder of

(27) used in (LABEL:eq:probtc) is known as the tangential cone condition. This condition is commonly used in the analysis of regularization methods for nonlinear ill-posed problems, see Kaltenbacher et al. (2008). The right hand side of (27) may be replaced by (see (39) below), and in this form it corresponds to Assumption 2 in Chen et al. (2011).

Corollary 2.

Let the assumptions of Theorem 1 hold true.

-

1.

If for some (Hölder-type source conditions), then

(28) -

2.

If is scaled such that and for some (logarithmic source conditions), then

(29) for all sufficiently small.

Let us discuss some properties of the method. First of all it is a local method like any Newton method. Convergence is only guaranteed if the initial guess is sufficiently close to the true solution . How close it has to be depends on the special problem, i.e. the operator . This property appears in the assumptions (22) and (LABEL:eq:probtc) in Theorem 1.

We emphasized in the introduction that the method requires only solutions of convex minimization problems. Therefore, it does not suffer from the problem of multiple local minima which frequently occur in nonlinear Tikhonov regularization (2) and make it hard to find the actual minimum.

Unlike for nonlinear Tikhonov regularization our theoretical results do not require the strong assumption that we can always find the minimum of a functional with an arbitrary number of local minima. In turn we have to assume (LABEL:eq:probtc), which is usually hard to check. Although, rigorous proofs for (LABEL:eq:probtc) are often missing, it seems to hold in many cases at least in a neighborhood of .

An important advantage for the numerical implementation is that a lot of efficient algorithms converging always towards the true solution are known for convex minimization problems. The error of these minimization algorithms plays a minor role compared to the regularization error for the applications of Section 2. We refer to Langer and Hohage (2007) for a detailed discussion of the interplay of these errors in other applications.

5 Examples revisited

The assumptions of Theorem 1 and Corollary 2 are rather abstract and need some explanations concerning the application to the nonparametric regression with independent instrument (4). They are applicable in a similar way to the nonparametric quantile regression (7). In (10) the operator for the regression with independent instrument is an integral operator with a kernel composed by marginals of . Hence, an estimator yields an estimator of the kernel and thereby of .

Condition (24) that all must be bounded with respect to the Bregman distance is fulfilled if the derivatives of are bounded according to (24), the estimation of is strongly consistent and is large enough. Strong consistency is established for many density estimators. The boundedness of with respect to the Bregman distance is reasonable. It holds if the partial derivative of the joint density is bounded for the operator (10) or if is bounded for the operator (12) and the Bregman distance is bounded from below by the power of a norm. As mentioned in Section 3.3, the latter is for example the case for quadratic and maximum entropy penalty.

It can be argued with strong consistency as well that the probabilistic tangential cone condition (LABEL:eq:probtc) holds if the exact operator fulfills the tangential cone condition (27). But, it is known that a verification, whether or not the tangential cone condition is true, is often difficult for a given operator.

In analogy to (12) the operator

can be considered for model (4). With this operator the conditions (24) and (27) are more explicitly assumptions on the primitives of the model.

In the rates for Hölder source conditions (28) in Corollary 2, has a smaller exponent than . However does not necessarily dominate the convergence. In the nonparametric instrumental regression corresponds to the estimation of a density, while is determined by the estimation of a partial derivative of that density. Hence, decays usually slower than . Which of the terms or dominates the convergence depends on the properties of the special problem, namely the number of instruments and covariates as well as on the smoothness of the density and the initial error .

The situation becomes clearer in the case of logarithmic source conditions. If the kernel of the operator is analytic, but the initial error in the regression function is not smooth or has only finite Hölder smoothness, merely a logarithmic rate of convergence can be expected. As discussed in Section 3.2 this situation can occur in many applications. Even for estimating an analytic density a nonparametric density estimator will attain only a polynomial rate in . Due to (29) our estimator for will end up asymptotically with the logarithmic rate .

6 Numerical simulations

In this section we present some numerical simulations for nonparametric instrumental regression with independent binary instrument and real-valued continuous explanatory and dependent variables. This leads to the nonlinear operator equation (18). Our simulations show that the solution computed by the method (3) approximates the exact solution. As mentioned above, due to dimensionality, the regression function cannot be identified with a binary instrument if the standard regression model (5) is used.

In our simulations we choose as real valued, with values in and with values in . We assume the regression function is

Moreover, we take and . To make endogenous, let us choose the error term as with and . The functions and describe precisely the correlation between the explanatory variable and the error term, which should be removed using the information contained in the instrumental variable. Although varies with and the condition can be assured by a proper choice of . We write the joint density as

| (30) |

Now has to be determined such that and are independent, which is equivalent to (17). Let us show that setting achieves this. With a substitution of variables we compute

This shows that (17) holds with our definition of what ever looks like. Here we take it to be normally distributed with variance and expectation truncated to the interval , i.e.

with some scaling factor chosen such that . By this construction, the error term also meets the condition of the regression model (4): To see this, note that and are even, while and are odd functions with respect to the point . Hence,

This construction allows an easy formulation of how the solution of a nonparametric regression without instrumental variable and without noise would look like:

![[Uncaptioned image]](/html/1307.6701/assets/regressionsolution1.jpg)

To approximately solve the integral operator equation (18) by the method (3)

we discretized the domain by

points and chose the regularization parameters by

and . The iteration was stopped using Lepskiĭ’s principle as in Bauer, Hohage & Munk Bauer et al. (2009).

The initial guess was chosen as the constant function . For a

first test we used the exact density , which actually has to be

estimated from the data, of course.

The -error was reduced from to . The remaining error is

due to discretization noise. This suggests that the example is identifiable

and can be solved by the method (3). Compared to the error for

densities estimated from simulated data below, the observed discretization error is very small. Hence, the

discretization is fine enough and discretization error is insignificant for our simulations.

The singular values of are shown in Figure 4.

They exhibit an exponential decay, so according to Corollary 2

we can only expect slow rates of convergence.

![[Uncaptioned image]](/html/1307.6701/assets/exact_data.jpg) Figure 3: Result of the iterative inversion

using the exact density .

Figure 3: Result of the iterative inversion

using the exact density .

![[Uncaptioned image]](/html/1307.6701/assets/sv_log.jpg) Figure 4: Singular values of

Figure 4: Singular values of

In further tests the algorithm was evaluated for finite samples of with , and points. Given such a sample, the joint density was estimated non-parametrically by the kernel density estimator developed by Botev, Grotowski & Kroese Botev et al. (2010). Afterwards again (18) was solved, but the exact density was replaced by the estimated one. We made samples for each tested sample size.

The following table and histograms in Fig. 5–7

show the -errors of the approximate

solution normed by the error of the initial guess (i.e. the error of the initial guess is ). It can be seen that small samples produce unwanted outliers, but the method becomes reliable

when the sample size is large enough. Fig. 8–10

show median reconstructions for each sample size.

The results demonstrate that our method computes an asymptotically correct

estimator of the regression function with an endogeneous

explanatory variable using only a binary instrument .

the exact solution is and the error of the initial guess is . It can be seen that small samples produce unwanted outliers, but that the method becomes reliable, when the sample is large enough.

| sample size | mean | quantiles | ||||

|---|---|---|---|---|---|---|

| 0.6159 | 0.4057 | 0.5751 | 0.7921 | 0.9575 | ||

| 0.3694 | 0.2496 | 0.3524 | 0.4574 | 0.5729 | ||

| 0.3264 | 0.2592 | 0.3278 | 0.3882 | 0.4610 |

![[Uncaptioned image]](/html/1307.6701/assets/Fehler_KS_Lepskii_3.jpg)

![[Uncaptioned image]](/html/1307.6701/assets/Fehler_KS_Lepskii_4.jpg)

![[Uncaptioned image]](/html/1307.6701/assets/Fehler_KS_Lepskii_5.jpg)

![[Uncaptioned image]](/html/1307.6701/assets/1000first.jpg)

![[Uncaptioned image]](/html/1307.6701/assets/10kfirst.jpg)

![[Uncaptioned image]](/html/1307.6701/assets/100kfirst.jpg)

Appendix A Proof of the main theorem

Before we come to the proof of Theorem 1, let us first formulate a result with deterministic error in the operator. We assume that is approximated by some deterministic operator

Let both and be Gateaux differentiable on with derivatives and , which are “bounded with respect to ” in the sense that and whenever and analogously for . The error of the approximation is described by:

| (31a) | |||||

| (31b) | |||||

Moreover, we assume that the tangential cone condition

| (32) |

holds for all in some neighborhood of .

Lemma 3.

Assume that (22), (31) and (32) hold true with sufficiently small, such that

| (33) |

Further assume that the convex minimization problems (3) are uniquely solvable and that the iteration is stopped at the smallest index for which

| (34) |

In addition it should hold that and for all with a constant . Moreover, let be concave and assume that is monotonically increasing.

Then there exists a constant independent of the such that

| (35) |

Proof.

Let us introduce the following notation:

From the optimality condition (3) with we find that

| (36) |

From the definition (21) of the Bregman distance and the source condition (22) we obtain

| (37) |

Plugging this into (36) yields

| (38) |

Note that the tangential cone condition (32) implies

| (39) |

To estimate the first term on the left hand side of (38) we use (32) and (39) to get that

Together with this yields

For the right hand side of (38) we get from (31) and another application of (32) that

Plugging the last two inequalities into (38) and using the simple inequalities and we obtain that

Using (31b) and the monotonicity of we find that . Together with the stopping rule (34) this implies

| (40) |

We will show the following error bounds

| (41a) | |||||

| (41b) | |||||

with

We will prove these claims by induction in . For this is arranged by the definitions of and . For the induction step we distinguish two cases:

Case 1: .

Now by using the induction hypothesis (41a) equation (40) simplifies to

We have as is monotonically increasing. While is concave and the definition of concavity implies for . Now taking and gives and therefore

Putting the last two equations together results into the bound

Firstly, this implies by omitting the second term on the left hand side that

Hence, it is necessary that , which is equivalent to the inequality (33) assumed in the Lemma. Then (41a) is true with .

Secondly, omitting the first term of the left hand side shows , so we have (41b) with .

Case 2: .

In this case (40) simplifies to

Using again and the concavity we get for all . Taking now and respectively implies . Thus we have

| (42) |

It is again convenient to study two cases:

Case 2.1: .

Now the monotonicity of entails

This shows that and thereby (41b) with . Plugging this into the right hand side of the last inequality and using the case assumption for the left hand side we get

Hence (41a) holds with .

Case 2.2: .

Dividing formula (42) by results in

Since the functions and are monotonically decreasing, we obtain

This shows that , so (41a) is true with . Plugging this into the left hand side of the last equation gives

Now we see that and therefore that (41b) is valid with

. This completes the proof.

Now Theorem 1 follows easily:

References

- Bakushinskiĭ (1992) Bakushinskiĭ, A. B. 1992. On a convergence problem of the iterative-regularized Gauss-Newton method. Zhurnal Vychislitel’noi Matematiki i Matematicheskoi Fiziki, 32(9):1503–1509.

- Bakushinskiĭ and Kokurin (2004) Bakushinskiĭ, A. B. and Kokurin, M. Y. 2004. Iterative Methods for Approximate Solution of Inverse Problems. Springer, Dordrecht.

- Bauer et al. (2009) Bauer, F., Hohage, T., and Munk, A. 2009. Regularized Newton methods for nonlinear inverse problems with random noise. SIAM Journal on Numerical Analysis, 47:1827–1846.

- Bissantz et al. (2004) Bissantz, N., Hohage, T., and Munk, A. 2004. Consistency and rates of convergence of nonlinear Tikhonov regularization with random noise. Inverse Problems, 20:1773–1791.

- Blaschke et al. (1997) Blaschke, B., Neubauer, A., and Scherzer, O. 1997. On convergence rates for the iteratively regularized Gauss-Newton method. IMA Journal of Numerical Analysis, 17:421–436.

- Blundell et al. (2007) Blundell, R., Chen, X., and Kristensen, D. 2007. Semi-nonparametric IV estimation of shape-invariant Engel curves. Econometrica, 75(6):1613–1669.

- Botev et al. (2010) Botev, Z. I., Grotowski, J. F., and Kroese, D. P. 2010. Kernel density estimation via diffusion. Annals of Statistics, 38(5):2916–2957.

- Breunig and Johannes (2009) Breunig, C. and Johannes, J. 2009. On rate optimal local estimation in nonparametric instrumental regression. arXiv:0902.2103v1.

- Burger and Osher (2004) Burger, M. and Osher, S. 2004. Convergence rates of convex variational regularization. Inverse Problems, 20(5):1411–1421.

- Carrasco et al. (2006) Carrasco, M., Florens, J.-P., and Renault, E. 2006. Linear inverse problems in structural econometrics: Estimation based on spectral decomposition and regularization. In Handbook of Econometrics, volume 6. North Holland.

- Chen et al. (2011) Chen, X., Chernozhukov, V., Lee, S., and Newey, W. K. 2011. Local identification of nonparametric and semiparametric models. Cowles Foundation Discussion Paper No. 1795.

- Chen and Pouzo (2012) Chen, X. and Pouzo, D. 2012. Estimation of nonparametric conditional moment models with possibly nonsmooth generalized residuals. Econometrica, 80(1):277–321.

- Chen and Reiss (2010) Chen, X. and Reiss, M. 2010. On rate optimality for ill-posed inverse problems in econometrics. Econometric Theory, 27:497–521.

- Chernozhukov and Hansen (2005) Chernozhukov, V. and Hansen, C. 2005. An IV model of quantile treatment effects. Econometrica, 73(1):245–261.

- Chernozhukov et al. (2007) Chernozhukov, V., Imbens, G. W., and Newey, W. K. 2007. Instrumental variable estimation of nonseparable models. Journal of Econometrics, 139(1):4–14.

- D’Haultfœuille and Février (2011) D’Haultfœuille, X. and Février, P. 2011. Identification of nonseparable models with endogeneity and discrete instruments. Preprint.

- Eggermont (1993) Eggermont, P. P. B. 1993. Maximum entropy regularization for fredholm integral equations of the first kind. SIAM J. Math. Anal., 24:1557–1576.

- Engl et al. (1996) Engl, H. W., Hanke, M., and Neubauer, A. 1996. Regularization of Inverse Problems. Kluwer Academic Publisher, Dordrecht, Boston, London.

- Engl et al. (1989) Engl, H. W., Kunisch, K., and Neubauer, A. 1989. Convergence rates for Tikhonov regularization of nonlinear ill-posed problems. Inverse Problems, 5:523–540.

- Florens (2003) Florens, J.-P. 2003. Inverse problems and structural economics: The example of instrumental variables. In Dewatripont, M., Hansen, L. P., and Turnovsky, S., editors, Advances in Economics and Econometrics: Theory and Applications, pages 284–311. Cambridge Univ. Press.

- Florens and Sbaï (2010) Florens, J.-P. and Sbaï, E. 2010. Local identification in empirical games of incomplete information. Econometric Theory, 26:1638–1662.

- Hall and Horowitz (2005) Hall, P. and Horowitz, J. L. 2005. Nonparametric methods for inference in the presence of instrumental variables. Annals of Statistics, 33:2904–2929.

- Hofmann et al. (2007) Hofmann, B., Kaltenbacher, B., Pöschl, C., and Scherzer, O. 2007. A convergence rates result for Tikhonov regularization in Banach spaces with non-smooth operators. Inverse Problems, 23(3):987–1010.

- Hohage (1997) Hohage, T. 1997. Logarithmic convergence rates of the iteratively regularized Gauss-Newton method for an inverse potential and an inverse scattering problem. Inverse Problems, 13:1279–1299.

- Horowitz and Lee (2007) Horowitz, J. L. and Lee, S. 2007. Nonparametric instrumental variables estimation of a quantile regression model. Econometrica, 75(4):1191–1208.

- Imbens and Newey (2009) Imbens, G. W. and Newey, W. K. 2009. Identification and estimation of triangular simulataneous equations without monotonicity. Econometrica, 77:1481–1512.

- Kaltenbacher and Hofmann (2010) Kaltenbacher, B. and Hofmann, B. 2010. Convergence rates for the iteratively regularized Gauss-Newton method in Banach spaces. Inverse Problems, 26(3):035007, 21.

- Kaltenbacher et al. (2008) Kaltenbacher, B., Neubauer, A., and Scherzer, O. 2008. Iterative Regularization Methods for Nonlinear ill-posed Problems. Radon Series on Computational and Applied Mathematics. de Gruyter, Berlin.

- Kress (1999) Kress, R. 1999. Linear Integral Equations. Springer Verlag, Berlin, Heidelberg, New York, 2nd edition.

- Langer and Hohage (2007) Langer, S. and Hohage, T. 2007. Convergence analysis of an inexact iteratively regularized Gauss-Newton method under general source conditions. J. Inverse Ill-Posed Probl., 15(3):311–327.

- Letac (1995) Letac, G. 1995. Exercises and Solutions Manual for Integration and Probability by Paul Malliavin. Springer. Translated by Kay, L.

- Loubes and Pelletier (2008) Loubes, J.-M. and Pelletier, B. 2008. Maximum entropy solution to ill-posed inverse problems with approximately known operator. Journal of Mathematical Analysis and Applications, 344(1):260–273.

- Newey and Powell (2003) Newey, W. K. and Powell, J. L. 2003. Instrumental variable estimation of nonparametric models. Econometrica, 71(5):1565–1578.

- Prössdorf and Silbermann (1991) Prössdorf, S. and Silbermann, B. 1991. Numerical Analysis for Integral and Related Operator Equations. Birkhäuser, Basel.

- Resmerita (2005) Resmerita, E. 2005. Regularization of ill-posed problems in Banach spaces: convergence rates. Inverse Problems, 21(4):1303–1314.

- Scherzer et al. (2009) Scherzer, O., Grasmair, M., Grossauer, H., Haltmeier, M., and Lenzen, F. 2009. Variational methods in imaging, volume 167 of Applied Mathematical Sciences. Springer, New York.

- Torgovitsky (2012) Torgovitsky, A. 2012. Identification of nonseparable models with general instruments. Preprint.