Applications of the Beta Distribution Part 1: Transformation Group Approach

Abstract

A transformation group approach to the prior for the parameters of the beta distribution is suggested which accounts for finite sets of data by imposing a limit to the range of parameter values under consideration. The relationship between the beta distribution and the Poisson and gamma distributions in the continuum is explored, with an emphasis on the decomposition of the model into separate estimates for size and shape. Use of the beta distribution in classification and prediction problems is discussed, and the effect of the prior on the analysis of some well known examples from statistical genetics is examined.

keywords:

1 Introduction

The beta distribution of the first kind, usually written in terms of the incomplete beta function, can be used to model the distribution of measurements whose values all lie between zero and one. It can also be used to model the distribution for the probability of occurrence of some discrete event. The most widely known technique for estimating the parameters, the method of moments, simply selects that beta distribution with the same first and second moments as found empirically from the data. However, such a procedure is not well-justified from the perspective of probability theory. To evaluate the reliability of the estimate of a model’s parameters, as well as to determine the net evidence for a particular model relative to some other, one needs to follow the mathematical procedure which has come to be known as Bayesian data analysis.

Use of the beta distribution can be found in a variety of applications; for an overview of this and related classes of discrete statistical models and their use in Bayesian analysis, see Pereira and Stern (2008). One common use is as a model for an input process within a stochastic simulation (Kuhl et al., 2010). Another is in the calculation of costs expected from a civil or industrial engineering project (Bȩtkowski and Pownuk, 2004). It also has widespread use in the study of population genomics (Balding and Nichols, 1995; Price et al., 2006). This paper concerns itself not so much with the choice of application but rather focuses on the methodology used to evaluate the parameters of the model given a set of measurements and the relative merit of competing models. Various methods have been suggested for the estimation of its parameters, including the method of moments (AbouRizk, Halpin and Wilson, 1991) and variants of the Kolmogorov-Smirnov test (Press et al., 1992), as well as tests based on Bayesian significance values (Pereira, Stern and Wechsler, 2008; Bernardo, Lauretto and Stern, 2012; Stern and Pereira, 2013). However, in this paper we will follow the traditional approach based on Bayes factors expressed in terms of the joint distribution for the quantities of interest.

This paper is organized as follows. After a brief description of Bayesian data analysis, we explore the relation between the beta distribution and the Poisson and gamma distributions in the continuum. The joint density for the size and shape parameter estimates can be expressed in alternate coordinate systems through geometric transformations which preserve the volume. Marginalization over the size parameter leaves behind the beta distribution which describes the shape (distributed occurrence of events) of the possible outcomes. After that, we examine the use of the beta distribution in the classification problem, where one tries to predict the type of some new object from the comparison of its features to those of a set of known objects. The model is then applied to some well known examples of genomic inference from population statistics of an observable locus We will conclude with a discussion of our findings and a summary of our results.

Some readers may find our use of the transformation group approach reactionary, archaic, or even naive, in light of the voluminous literature discussing other, more complicated strategies for deriving the form of the prior given some model for the likelihood of the observations, such as conjugate and entropic methods (Raiffa and Schlaifer, 1961; Lazo and Rathie, 1978). Our response is that the analysis of similarity transformations has a long history in physics, leading one to statements of conservation of energy and momentum respective to translations in time and space. When discussing the analysis of data, one should never forget that real measurements carry an index for location on the universal manifold and are subject to the laws of nature; how much use is made of that information depends upon the application and the investigator.

2 Brief description of Bayesian data analysis

The Bayesian approach to data analysis is best discussed using the language of conditional probability theory (Bretthorst, 1988; Durrett, 1994; Sivia, 1996). The expression for “the probability of A given B” can be written most compactly as

| (1) |

where and can have arbitrary dimensionality; for example, could be a vector of measurements, and could include both the vector of parameters associated with some model as well as any other conditioning statements such as the model index. The notation on the RHS of Equation (1) is more economical than that of the LHS in terms of both the amount of ink on the page and the amount of mental effort required to keep track of the distinction between propositional statements in the superscript and conditional statements in the subscript; it also helps maintain identification of the units of density, which are carried by the propositional statements alone. The sum and product rules of probability theory yield the expressions for marginalization and Bayes’ theorem,

| (2) | |||||

| (3) |

where marginalization follows from the requirement of unit normalization, and Bayes’ theorem follows from requiring logical consistency of the joint density . Let us write as the vector the parameters for some model , and let the data be written as . Bayes’ theorem then relates the evidence for the parameters given the data to the likelihood of the data given the parameters through the expression

| (4) |

where the factor describes the prior expectation over the parameter manifold in the absence of data, and the constant of proportionality represents the chance of measuring the data, which is usually recovered from the normalization requirement of the evidence density .

The essential feature of Bayesian data analysis which takes it beyond maximum likelihood analysis is the inclusion of the prior density . The selection of the appropriate form of the prior for some coordinate mapping of the parameter manifold is guided by the principle of indifference applied to the behavior of the model under similarity transformations (Jaynes, 1968; Sivia, 1996; Dose, 2003). Here, indifference is realized by examining the transformation group of the parameter manifold given by . Having found the prior measure for one coordinate system, the prior measure for alternate coordinate systems can be found through the use of a Jacobian transformation.

When only one model is in play, its quality of fit is irrelevant. If no other description of the data is available, the most one can do is fit the parameters for the model at hand. In order to accomplish the task of hypothesis testing, Bayesian data analysis forces one to specify explicitly the alternatives. For a set of models indexed by , the factors in Equation (4) must be conditioned on the choice of . For two models , the relative evidence is given by the ratio of the net evidence for each model,

| (5) |

where the factor describes any prior preference between the models and usually is identified as unity. The factors in the likelihood ratio are given by the marginalization of the joint density over the parameter manifold for each model,

| (6) |

where the use of properly normalized densities for the likelihood and prior is required. In particular, the prior is normalized to unity over the parameter manifold while the likelihood retains its physical normalization.

An interesting feature of Bayesian model selection is that it accounts naturally for Occam’s principle of efficiency. Assuming model 1 has some parameter with uniform prior of extent , and taking the quadratic (Gaussian) approximation of its likelihood, without prior preference for either model the evidence ratio becomes

| (7) |

where is the optimum value of the parameter and is its variance. With an adjustable parameter, model 1 very likely provides a better quality of fit as measured by the first ratio ; however, that is not the only factor in the net evidence ratio. The improved fit to the data comes at the cost of the Occam factor which measures the distribution of the evidence density relative to the parameter domain. One requirement for the Gaussian approximation is that the prior not severely restrict the likelihood , thus the Occam factor works against the peak likelihood in the net evidence ratio in Equation (7). Another interesting feature is that, all else being equal, the model whose parameters have the larger variance is the one preferred by probability theory, as more of its parameter space is compatible with the measurements. Suppose model 2 has its own parameter with comparable domain and provides a comparable fit to the data . In this case, the net evidence ratio reduces to , so that the net evidence for model 1 relative to 2 is given by the ratio of the deviation of their parameters.

One criticism that is often leveled at those who use Bayesian methods (Gelman, 2008) is that the “prior and posterior [evidence] distributions represent subjective states of knowledge.” By working in the language of conditional probability theory, what Bayesian methods require is that one specify the background knowledge upon which any inference of likelihood is based. For example, one’s estimate of the likelihood of rain today depends upon whether one has seen satellite images of clouds in the area. Investigation of the transformation group associated with the parameters in a model leads one to specify the Haar measure as the intrinsic density which can serve as an objective prior in the absence of any further information. The existence and uniqueness of the Haar measure hold under very general conditions on the set of parameters considered.

3 Beta, Poisson, and gamma distributions in the continuum

The beta distribution can be derived from consideration of the Poisson and gamma distributions in the continuum (Press et al., 1992; Abramowitz and Stegun, 1964). Physically, a continuum quantity is understood to be one for which the quantum unit is too small to measure. Let us begin by supposing the amount for some quantity observed per unit time is given by a Poisson process with rate parameter expressed in the same physical units , thus the likelihood can be written

| (8) |

in terms of the gamma function . The discrete Poisson distribution is of course given by for integer (quantized) , such that the sum over all of the probability mass function is normalized, . One should keep in mind, however, that is a probability density function which carries units of such that is a pure number. The integral cannot be easily evaluated; however, a collection of heuristic arguments (given in Appendix A) indicate that its value also is unity.

According to Jaynes (1968), the parameter for a Poisson process must satisfy the same functional equation for transformations in scale as does the deviation parameter of a Gaussian distribution, thus the intrinsic (prior) density for is given by

| (9) |

which defines the infinite constant . Note that is formally equal to the mass of a distribution with infinite extent and unit density, for , thus it also appears in the ubiquitous uniform prior of the maximum likelihood method. Readers who are uncomfortable with infinite normalization constants may instead consider for , using equivalent limits such that symmetry with respect to scale is maintained. The intrinsic density , whose sole proposition is the existence of , is recognized as the Haar measure for the group of positive real numbers closed under the operation of multiplication. Note that Jaynes’ expression for the prior differs by a power from that obtained by application of the Jeffreys procedure, defined in terms of the square root of (the determinant of) the Fisher information (matrix). That procedure yields the prior when applied to the Poisson distribution. The Jaynes prior is functionally invariant under transformations of the form for given and , such that , whereas which is invariant only for . In the limit one finds , which can be interpreted heuristically (but maybe not correctly) as follows. When evaluating the Fisher information, the expectation value is taken over only a single datum, whereas the measurement process could be repeated any number of times, which for the Poisson process amounts to changing the unit of time. It seems, then, that the Jaynes prior accounts for the possibility of an infinite number of measurements when assigning the most general form of .

The joint density over the manifold can be written as the product of the conditional density and intrinsic density ,

| (10) |

and its integral over can be evaluated explicitly,

| (11) |

which is recognized as the chance of measuring . Having equivalent physical units, the quantities and possess the same transformation group, thus their intrinsic densities must be functionally identical. That the expression represents a valid probability density function is verified by next taking the integral over ,

| (12) |

thus the joint density has unit mass over the infinite quarter plane in .

According to Bayes’ theorem, the evidence for parameter conditioned on observable in the Poisson likelihood is given by the gamma distribution,

| (13) |

which is normalized to unit mass, . One also can verify the integral (permissible since ), thus the likelihood is normalized over the parameter as well; logically, given the existence of a value for , it must be true that the sum of all its conditional probabilities is equal to unity. By similar logic, the normalization of both and over should also be true, but a direct evaluation of those integrals analytically is difficult (see Appendix A). For comparison, consider the joint density of a measurement and parameter given by a Gaussian of known deviation which sets the scale, , with intrinsic densities . In this case, one can easily show that as well as . That similar normalizations hold in the continuum for the Poisson and gamma densities is the main conjecture of this paper.

Note that the joint density does not care whether and are identified as parameter and observable, respectively, or vice versa. The identification of evidence, chance, likelihood, and prior similarly is arbitrary, as long as one is consistent (Sivia, 1996). The decomposition through Bayes’ theorem of the joint density in terms of intrinsic densities given by the Haar measure allows one to write

| (14) |

thus the gamma distribution is the evidence for a Poisson process likelihood, and vice versa. The second (shape) parameter commonly associated with the gamma distribution can be identified as the ratio of the units for the parameter and observable , which here is specified as unity.

Now let us consider the joint density , which can be written as

| (15) |

Under a change of coordinate mapping such that

| (16) |

with domain and , the Jacobian matrix is given by

| (17) |

whose determinant is . The intrinsic density in the new coordinates is thus

| (18) |

and the conditional density is

| (19) |

Since , one can then write

| (20) |

which integrates to unity,

| (21) |

using the evaluations

| (22) | |||||

| (23) |

Marginalization then yields

| (24a) | |||||

| (24b) | |||||

which is the main result of this section. With the interpretation of as a normalized frequency (rate of observance), one can state that the intrinsic density for an absolute likelihood is , while that for a relative likelihood is . Note that is infinite only when the parameter is allowed to obtain the extreme values of its domain, and in fact is comprised of two independent infinities , one from each boundary of the manifold.

While the relationship between these three distributions has been explored by many authors, nowhere have we found a derivation within the framework of conditional probability theory that ties them together under the conjecture of the continuum normalization. The literature has instead focused on the relation between discrete random variables rather than the continuous case. Partly that may be because the expression of the Poisson distribution in the continuum is not so widely known, owing to the difficulty of evaluating its normalization integral analytically. Another reason may be because use of transformation group arguments has been championed primarily by physicists rather than statisticians. Whatever the reason, the establishment of Equation (14) in the continuum leads one naturally to the beta distribution, which displays explicitly the transformation group prior for the normalized frequency .

Let us now consider the parametrization given by

| (25) |

with domain . In these coordinates, the prior density is uniform , thus the evidence is proportional to the likelihood, and the joint density equals

| (26a) | |||||

| (26b) | |||||

| (26c) | |||||

| (26d) | |||||

The first two factors above are reminiscent of the logistic regression model (Peng and So, 2002); however, the parameter , commonly called “the intercept”, makes an appearance as the argument of a double exponential in the third factor as well as in the terms without . The third factor is not related to the prior thus must be part of the likelihood. Rather than conflating the parameters, keeping the likelihood models and independent leads to a more efficient evaluation (Johnson, 2017).

4 Application to prediction and classification

Let us begin this section by talking about baseball. Specifically, let us consider the use of the seasonal batting average as a predictor for whether a player will reach base on his next appearance. Let each appearance be indexed by time given by integer , and let us identify a successful appearance as an event of type , while outs are of type . The record of successful appearances can be notated by for , and similarly for of dimension , such that . The evidence for the value of the batting average is the product of the prior and likelihood factors, yielding the beta distribution with mode and expectation value , which coincides with the likelihood mode and gives the predicted rate of success for the next appearance.

One can incorporate into the form of the prior additional information pertinent to the problem at hand. In particular, one can use knowledge of the seasonal nature of the sport to impose sensible limits on the domain . If our player’s season is not yet over, then there must be at least one more at bat scheduled. A sensible limit is thus given by , which incorporates the notions that nobody is perfect (1 is excluded) and of the benefit of the doubt (0 is excluded); assuming our player is a professional at least one event of each type should be observed per season, even for pitchers. One effect of such a prior is that it does not allow observations of only one type of event to pull the evidence mode all the way to the hypothetical limits of 0 and 1. Another effect is that early in the season the domain of requires an observation of the batter before starting to make predictions; once we are certain the batter is playing this season , we can state the expected chance of success is equal to 1/2, the only allowed point, with further observations expanding the domain until at the end of a long season the prior is wide open.

Let us now turn to consideration of classifying some new event as type or on the basis of its location relative to those for observations whose classification is assigned. The elements of the measurement vectors and are now locations along some axis , with a measurement uncertainty expressed by the Gaussian deviation . If the chance an event is of type is independent of location, one can write , where is a Gaussian centered on the mean location of all the events and each margin is normalized independently. That is obviously not the solution we are looking for, which should give an expectation of the form based on a joint density that can be factored as for .

Another way to express the notion that location has become irrelevant is by taking the limit . In that case, one should require for all , which corresponds to neglecting the stadium of appearance in the batting average problem above. In doing so, we have not said that location does not exist, but rather that location does not matter. For finite , we should write , whose limit for is ; observations nearby should not significantly affect our prediction for a galaxy far, far away. The problem now is one of assigning the appropriate form for the likelihood factor. For inspiration, we have looked at various approaches suggested in the literature (Terrell and Scott, 1992; Hall, Park and Samworth, 2008; Kim and Scott, 2012; Eberts and Steinwart, 2013).

At this stage the discussion becomes a bit heuristic. When the observations are independent, we can factor the likelihood into the form

| (27) |

where represents the chance datum is of type , and similarly for . What, then, is the form of that yields sensible results for all and irrespective of the underlying spatial distributions of the two types of events? A form which suggests itself is more clearly notated in terms of its logarithm , where is the probability of an event at relative to that at . The log of the likelihood can then be written as

| (28) |

whose limits are for and 0 for , in accord with our requirements for the evidence density. Let us identify , and similarly for ; then the likelihood can be written as , and the evidence for the value at is given by

| (29) |

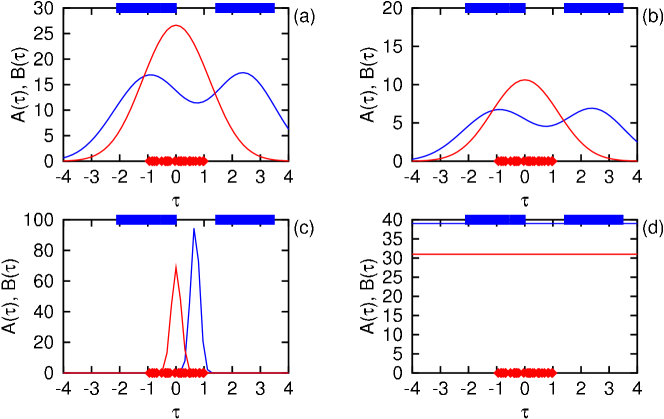

which has the form of a beta distribution at all locations. An example of and for an arbitrary distribution of and in units of the deviation is shown in panel (a) of Figure 1. The values are drawn uniformly over two disjoint regions each with a span of 2 units, and the values are selected from a region spanning 2 units which overlaps partially one of the type regions.

Out of respect for our heuristic argument, we should consider some alternative definitions for the likelihood. If instead of the relative probabilities one defines as the sum of the absolute probabilities such that , one has in the limit the result , which does not recover the beta distribution in terms of and . If one uses the product of the datum likelihoods to define for , which also integrates over to , one’s estimate for the evidence depends upon only the first moments of the event distributions, a procedure which is easily foiled when the underlying location distribution are not Gaussian. Finally, if one uses , one recovers simply the independent distributions over and . Examples of these definitions of and are displayed in panels (b) through (d) respectively of Figure 1 for the same distributions of and .

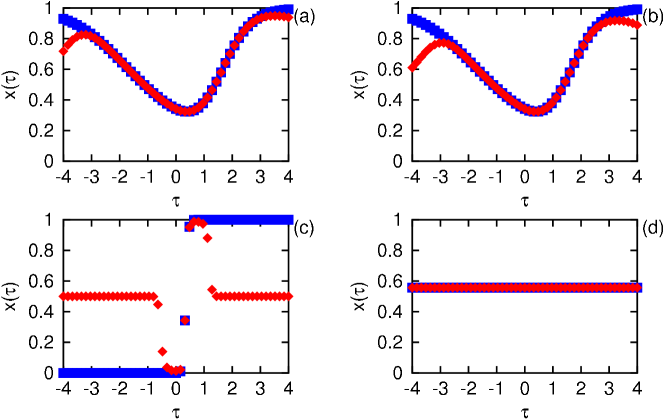

A maximum likelihood predictor can be formed from the expression

| (30) |

which is evaluated from the measurements and with respect to . The expectation value , however, takes into account the full domain of as measured by the evidence density. In Figure 2 we display the maximum likelihood and expected value predictors for the distributions and shown in Figure 1. The likelihood estimate is the same in panels (a) and (b), since the ratio in terms of the summed likelihoods does not depend on their normalization. The expectation value in panel (b) is more conservative, in that it more quickly approaches the expectation value of the prior, compared to panel (a). The likelihood estimate for the method of panel (c) gives a prediction for the region that is contrary to the observations, while its expectation value is very quickly drawn to that of the prior, even in the region where only type events are observed. The likelihood and expectation value predictors are identical when the location information is ignored, as seen in panel (d).

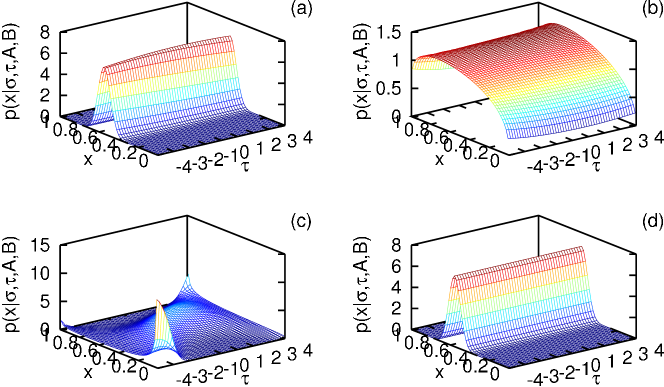

Let us now repeat the evaluation of the evidence densities for the various definitions of and , but this time let us suppose that for the same locations and . Let us also inspect the evidence densities directly, to see which one best encodes a reasonable estimate of the solution to our problem. In Figure 3 we display the evidence density for as a function of for the various likelihood models. We can see that panel (a) is the one most like panel (d), which evaluates the beta distribution without regard to location. The other models, panels (b) and (c), are not in accord with the conclusions a reasonable observer would draw intuitively from the presented data; surely with close to 100 observations the relative rate of production should be fairly well determined over the common region of the events. While our justification of Equation (28) is heuristic, its form is the same as that of a Gaussian with unequal weights, where each datum factor in the likelihood is an absolute probability to the power of a relative probability.

What can we say about the limit , which indicates that observations are relevant only to predictions at the same location? With respect to the finite resolution of whatever apparatus is used to take the location measurements, what we really mean in that limit is that locations are resolved over a set of discrete channels which have no influence or bearing on events in other channels. Returning to the baseball analogy, that model asserts that batting averages for each stadium should be evaluated independently, which is not an unreasonable procedure, given by and similarly for . The parameter can in fact be an abstract location, not just a physical one, with the interpretation of as the relevance of observations in one channel to predictions in another. We should also point out that we have been treating the location of the predicted classification as a quantity known exactly; if the location of the unclassified event is itself subject to measurement deviation , then one must convolute the evidence density with its normalized distribution, . Furthermore, if the value of is unknown, it can be integrated out by treating it as as a nuisance parameter, for .

5 Application to the Balding-Nichols model

Next let us look at how the beta distribution is used in the analysis of genetic profiles. Suppose the gene at some locus has a dominant allele and a recessive allele such that the genotypes , , and are distinguishable. According to Balding and Nichols (1995), the allele frequency for finding at the locus follows a beta distribution with parameters and . The measurements are now not values for but rather the number of members of each genotype observed within a sampling of the th population, . In terms of the parameters, the probability for an individual to be a member of the genotype is given by

| (31a) | |||||

| (31b) | |||||

for the dominant homozygote, and by

| (32a) | |||||

| (32b) | |||||

for the recessive homozygote, while the heterozygote appears with probability

| (33a) | |||||

| (33b) | |||||

where the factor of 2 accounts for the indistinguishability of the order of the alleles. In matrix form with unit 1-norm, the joint distribution of the genotypes can be written

| (34) |

yielding the interpretation of as the mean dominant allele frequency and of as a measure of heterozygote suppression. The parameter may be identified with Wright’s inbreeding coefficient .

The probability of obtaining the measurements given knowledge of the parameter values is the product of the genotype likelihoods weighted by the number of members. For a single population,

| (35) |

thus the information content of the data (negative log likelihood) is

| (36) |

recalling . The nontrivial solution of yields the maximum likelihood estimate of the optimal parameter values

| (37) |

which corresponds to the location

| (38) |

on the manifold. Suppose now instead of the genotype observations our data consists of the raw allele counts for and , given by and such that . The log likelihood in this case becomes

| (39a) | |||||

| (39b) | |||||

whose optimal estimate is the same with undetermined. From the raw allele counts one can resolve only the dominant allele frequency for a single population.

The merit function for the evidence density in terms of the parameters can be written as

| (40) |

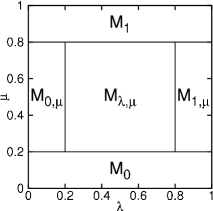

using an unnormalized prior. When , the population is said to be in Hardy–Weinberg equilibrium with a single parameter for the dominant allele frequency; however, one should observe that is also an equilibrium solution with a single parameter . Those two cases correspond to the peaks in the prior for when the boundary is not excluded. In the limit , the normalized prior has the value 1/2 at equal to 0 or 1 and the value 0 everywhere else. Similarly, when equals 0 or 1, one finds that is undetermined by the likelihood, thus those models have zero free parameters. The five models under consideration (for a single population) can thus be labeled , , , , and , where the first is a two parameter model, the next two are one parameter models, and the last two zero parameter models, all of which are conditioned on the value of the boundary exclusion determined in principle by the nature of the measurement apparatus. A similar approach is suggested by Johnson and Rossell (2010). See Figure 4 for a depiction of the mapping from the parameter manifold to the model labels using a large value of for clarity.

It is instructive to look at the information content of the data with respect to the various models. For with two parameters, is given by Equation (36), whose mode provides a good starting point for the numerical optimization of ; four other points to consider are the projections of the likelihood mode onto the boundaries of the manifold. The model has an information density of

| (41) |

retaining the constant term with , and has

| (42) |

supported only when such that ; otherwise, . For either one parameter model, it is possible for certain values of the input data to yield an evidence density which is uniform in ; in those cases, the mode is undetermined and the unnormalized evidence density is equal to 1. For the zero parameter models,

| (43) |

which equals 0 when only else is infinite, and by symmetry

| (44) |

Since the zero parameter models have a manifold of a single point, their net evidence (mean likelihood) is either 0 or 1 according to whether they are supported by the data, which sets the unit of evidence when comparing the other models.

| 1469 | 138 | 5 | 2.270 | 95.409 | 0.831 | 63.8 |

|---|

| model: | |||||

|---|---|---|---|---|---|

| mode: | (0.001,95.438) | 95.438 | NaN | NaN | NaN |

| mean: | (0.985,95.407) | 95.409 | NaN | NaN | NaN |

| : | 510.4 | 509.6 | Inf | Inf | Inf |

| : | 30.2 | 69.8 | 0.0 | 0.0 | 0.0 |

As an illustration, let us look first at some data from Ford (1971) shown in Table 1. Also shown are the maximum likelihood values and in units of percent. From these numbers one can evaluate Pearson’s statistic from the Hardy–Weinberg expectation values and so on. The accumulation of the statistic for 1 degree of freedom (3 from the data less 2 used in the model) gives the significance of the deviation from equilibrium, and for comparison for in the notation used by Press et al. (1992). The conventional interpretation is to state that the equilibrium model is not rejected on account of the small value of ; however, since only two models are considered, one may interpret the value of as the amount of probability not assigned to the equilibrium model, in which case the maximum likelihood analysis is showing some preference, if not overwhelming, for the non-equilibrium model.

The evidence analysis of the same data is shown in Table 2 for all five models. A value of is selected, consistent with the amount of data ; in other words, we select a mathematical resolution slightly beyond that given by the measurement procedure which excludes the extreme boundary. The location of the mode, when it exists, is displayed, as are the expected values of the parameters; for model the global optimum of evidence is located on the boundary, and for model the mean value for is equal to as expected analytically. The net evidence for each model is given in terms of its negative logarithm for parameter vector and data vector . The value for each model, interpreted as the probability that the model describes the data, is determined from

| (45) |

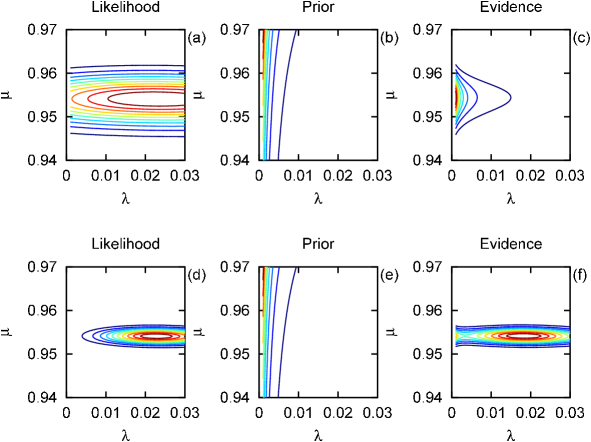

such that . Of the two models supported by the data, that for Hardy–Weinberg equilibrium is assigned a probability close to 70%. A graphical comparison of the likelihood and evidence analysis is shown in Figure 5 panels (a)–(c); in panels (d)–(f) we show the analysis of a hypothetical data set with 10 times as many observations per channel at the same ratios. With that much data, the evidence is mostly around the likelihood peak, but a noticeable fraction is left along the manifold boundary. For the amounts of data commonly found in observational studies, the prior can have a significant effect on the analysis.

Next let us look at some data from James et al. (1983) as summarized by Holsinger (2006), displayed in Table 3. This time the data is broken down into that for subpopulations indexed by according to the geographic region of the observations. Since none of the populations have only , the model can be discarded immediately. The practical question we are interested in is whether any single population is significantly different than the remainder. To answer that question, the net evidence (expected likelihood) for the models applied to the entire population is compared to the product of the evidence for the subdivision into and . The results of this analysis are shown in Table 4 using a value of . Values of 0 or 1 for the parameter mode appearing in the table are understood to be on the boundary given by .

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 29 | 14 | 15 | 9 | 9 | 23 | 23 | 29 | 5 | 1 | 0 | 1 | |

| 0 | 3 | 2 | 0 | 0 | 5 | 3 | 3 | 0 | 0 | 1 | 0 | |

| 0 | 3 | 3 | 0 | 0 | 2 | 4 | 1 | 0 | 0 | 0 | 0 |

| 0 | 0.55 | 0.89 | 0.89 | NaN | 0.55 | 0.89 | 0.89 | NaN | 110.05 | 125.93 | Inf | Inf |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 1.00 | 1.00 | 1.00 | 1.00 | 0.52 | 1.00 | 1.00 | 1.00 | 1.16 | 1.21 | 1.11 | 0.00 |

| 2 | 0.00 | 0.79 | 0.79 | NaN | 0.45 | 0.77 | 0.78 | NaN | 21.41 | 22.43 | Inf | Inf |

| 3 | 0.00 | 0.82 | 0.82 | NaN | 0.62 | 0.80 | 0.80 | NaN | 19.62 | 21.76 | Inf | Inf |

| 4 | 1.00 | 1.00 | 1.00 | 1.00 | 0.52 | 0.99 | 0.99 | 0.99 | 1.01 | 1.05 | 0.96 | 0.00 |

| 5 | 1.00 | 1.00 | 1.00 | 1.00 | 0.52 | 0.99 | 0.99 | 0.99 | 1.01 | 1.05 | 0.96 | 0.00 |

| 6 | 0.00 | 0.86 | 0.86 | NaN | 0.19 | 0.85 | 0.85 | NaN | 25.19 | 25.12 | Inf | Inf |

| 7 | 0.00 | 0.83 | 0.83 | NaN | 0.63 | 0.82 | 0.82 | NaN | 26.51 | 29.81 | Inf | Inf |

| 8 | 0.00 | 0.94 | 0.94 | NaN | 0.20 | 0.92 | 0.92 | NaN | 18.69 | 18.59 | Inf | Inf |

| 9 | 1.00 | 1.00 | 1.00 | 1.00 | 0.52 | 0.98 | 0.99 | 0.98 | 0.93 | 0.98 | 0.89 | 0.00 |

| 10 | 1.00 | 1.00 | 1.00 | 1.00 | 0.52 | 0.93 | 0.95 | 0.91 | 0.74 | 0.78 | 0.69 | 0.00 |

| 11 | 0.00 | 0.50 | NaN | NaN | 0.18 | 0.50 | 0.50 | NaN | 3.85 | 3.14 | Inf | Inf |

| 12 | 1.00 | 1.00 | 1.00 | 1.00 | 0.52 | 0.93 | 0.95 | 0.91 | 0.74 | 0.78 | 0.69 | 0.00 |

| 1 | 0.54 | 0.87 | 0.87 | NaN | 0.53 | 0.86 | 0.86 | NaN | 104.50 | 118.23 | Inf | Inf |

| 2 | 0.54 | 0.90 | 0.90 | NaN | 0.53 | 0.90 | 0.90 | NaN | 91.97 | 104.33 | Inf | Inf |

| 3 | 0.52 | 0.90 | 0.90 | NaN | 0.51 | 0.90 | 0.90 | NaN | 94.29 | 105.81 | Inf | Inf |

| 4 | 0.55 | 0.88 | 0.88 | NaN | 0.54 | 0.88 | 0.88 | NaN | 108.43 | 123.69 | Inf | Inf |

| 5 | 0.55 | 0.88 | 0.88 | NaN | 0.54 | 0.88 | 0.88 | NaN | 108.43 | 123.69 | Inf | Inf |

| 6 | 0.61 | 0.90 | 0.89 | NaN | 0.60 | 0.89 | 0.89 | NaN | 88.24 | 103.50 | Inf | Inf |

| 7 | 0.51 | 0.90 | 0.90 | NaN | 0.50 | 0.90 | 0.90 | NaN | 87.66 | 97.79 | Inf | Inf |

| 8 | 0.58 | 0.88 | 0.88 | NaN | 0.57 | 0.88 | 0.88 | NaN | 94.90 | 109.60 | Inf | Inf |

| 9 | 0.55 | 0.89 | 0.88 | NaN | 0.54 | 0.88 | 0.88 | NaN | 109.16 | 124.70 | Inf | Inf |

| 10 | 0.55 | 0.89 | 0.89 | NaN | 0.55 | 0.89 | 0.89 | NaN | 109.87 | 125.69 | Inf | Inf |

| 11 | 0.57 | 0.89 | 0.89 | NaN | 0.56 | 0.89 | 0.89 | NaN | 107.59 | 124.32 | Inf | Inf |

| 12 | 0.55 | 0.89 | 0.89 | NaN | 0.55 | 0.89 | 0.89 | NaN | 109.87 | 125.69 | Inf | Inf |

To identify which single population displays the most significant deviation from the remainder, for each the minimum is added to the minimum , then the minimum is subtracted to yield the (negative) log evidence for the subdivision relative to the net population . Those values are then exponentiated and normalized to yield the quality factors . From Table 4 one sees that is the model best supported by the net population and all the remainder populations, but all four models can be supported by some of the subpopulations . In Table 5 we display which model best fits population as well as the relative log evidence and the quality factors in units of percent. Of the thirteen models under comparison, the most significant is the subdivision of the first population from the remainder, whose is close to 94%. The suppression of the recessive allele in that population would appear to be significant, while that for the other populations displaying only is less so. A thorough analysis would consider all possible groupings of the subpopulations to determine the most statistically significant division of the net population from the given data. A more thorough analysis would make use of knowledge of the geographical regions sampled to consider only those groupings of populations in physical contact. The possibilities are endless and left as an exercise for the reader.

| 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.00 | -5.55 | 3.33 | 3.87 | -1.61 | -1.61 | 3.31 | 4.13 | 3.45 | -0.89 | -0.18 | 0.68 | -0.18 | |

| 0.37 | 93.96 | 0.01 | 0.01 | 1.84 | 1.84 | 0.01 | 0.01 | 0.01 | 0.89 | 0.44 | 0.18 | 0.44 |

6 Discussion and conclusion

Those who use Bayesian methods are often asked to explain the significance of the prior. On its own, Bayes’ theorem does not tell one how to assign the intrinsic probability density for the parameter manifold. For that task, one must turn to some other maxim. The principle of indifference is essentially a geometric argument that posits the existence of some coordinate mapping of the parameter manifold for which the information content is uniform. That mapping might not be the one most convenient for the investigator, thus the appearance of the prior may be nonuniform in one’s chosen coordinates. The main effect of the prior is to prevent one from overestimating structure in the model not supported by imperfect data. If the prior is neglected, one may unintentionally introduce a bias into one’s results.

With respect to the beta distribution, use of the transformation group prior is implicit in its functional form. In the absence of observations, what remains is the Haldane prior expressing complete indifference to the value of an absolute probability. If the observations and are restricted to integer counts of class membership, then the effect of the prior is to require an observation of each type of event before one is certain both types are present within the population; until both types have been observed, the evidence density is infinite on the boundary at either 0 or 1. If one of each type has been observed, we are then certain that the production rate is between 0 and 1 with uniform distribution. Further observations then refine that estimate until the likelihood and evidence modes converge in the limit of infinite data.

The transformation group approach leads one to specify as the logarithm of the unnormalized prior measure over the manifold. In the course of this project we investigated use of the entropic prior , where

| (46) |

is evaluated from the Shannon-Jaynes expression (Lazo and Rathie, 1978). The entropic expression for the prior was discarded after finding in the context of the Balding-Nichols genotype analysis that it did not lead to a hierarchy of models. The Jeffreys invariant prior, with logarithm

| (47) |

and proportional to the square root of the determinant of the Fisher matrix, likewise was considered. Its prior density is very similar to that given by the transformation group, thus results based on that prior should be close to the results presented here. Finally, the conjugate prior approach is discounted because there is no physical reason to suppose that the evidence and prior should be of the same algebraic form, mathematical convenience notwithstanding. Note that the appearance of the beta function in the beta distribution results from the normalization over the axis ; if the domain of is more restrictive, the expression for the normalization as a function of the parameters and is more complicated. In that case, neither the entropic nor the Jeffreys prior is appropriate without severe modification, whereas the transformation group prior is unaltered.

Many investigators are troubled by the use of an improper prior, leading to an entire industry devoted to the generation of ever more complicated functions to be used as priors for statistical analysis of data. One should think very carefully before deciding to employ any of those alternative strategies. Stern (2011) argues that good choices for the functional form of the probability densities used in a statistical model must be based on the natural symmetries and invariance properties of the quantities of interest. The transformation group approach is based on the physical properties of the objects under consideration, with respect to the nature of the universe that we live in. The prior it yields represents a measure of uniform information content over the parameter manifold. The one dimensional improper transformation group priors are in fact all just different views of the uniform prior under a change of coordinates, for and . The appearance of infinite densities on the boundary of the prior indicate where simpler models with fewer parameters exist; these models can be addressed by evaluating their Bayes factor relative to the model with the most complexity.

An outstanding issue when using the transformation group approach is the imposition of the finite cutoff . In the realm of physics, one argues that the measurement apparatus has a finite domain of resolution, from which a sensible value of may be derived. Practically, one often sets to some value well beyond the expected domain of resolution with the understanding that one should check for boundary effects, and for many problems with well resolved parameters that is sufficient. For counting experiments with a Poisson likelihood, the total number of observations is constrained by the patience of the investigator, thus it provides a finite limit to the resolution. The sharp cutoff at , though, is not appealing, when intuitively one expects a proper prior with finite normalization to have a smooth behavior. Forthcoming in Part 2 is an extension of the approach presented here that incorporates depth of data in a manner that yields a smooth, normalizable prior function whose domain extends to the boundaries.

In summary, we have explored the relation between the Poisson and gamma distributions in the continuum with respect to the transformation group prior whose marginalization yields the beta distribution. To impose normalization on the prior, we consider the limit on resolution of the parameters given by a finite set of observations. Some examples of the approach are presented which display the flexibility of the beta distribution to model observational experiments. Its study has a long history in the literature, and it continues to be quite useful in the modern day.

Appendix A Normalization of the continuum Poisson distribution

In Section 3 we encountered an integral that could not be put into closed form analytically. In this appendix we present some heuristic arguments for its evaluation. Let

| (48) |

represent the integral in question, and what we want to show is that . Physically, the argument of the exponential function must carry no units, thus what we really mean by is

| (49) |

since and . Similarly, carries units of , as can be seen from the Euler integral of the second kind , thus is a pure number, as is . In taking the limit of Eqn. (49), one must consider carefully the meaning of the denominator on the RHS. When writing the factorial function as a product of descending integers, one typically stops at the factor 1; however, recalling that , one sees that the factor completes the factorial so that the expressions carry the same units. Since does not appear on the LHS, taking the limit establishes the relation .

Without an antiderivative with respect to in hand for the densities and , the most we can do analytically is investigate the properties of their integrals. From the normalization of the joint density , whose units are carried by the first factor in parentheses, one can write

| (50) |

which implies that if , then . Since , one can say that

| (51) |

whereby the establishment of yields the normalizations and , as required by the logical interpretation of Bayes’ theorem, .

References

- AbouRizk, Halpin and Wilson (1991) {barticle}[author] \bauthor\bsnmAbouRizk, \bfnmSimaan M.\binitsS. M., \bauthor\bsnmHalpin, \bfnmDaniel W.\binitsD. W. and \bauthor\bsnmWilson, \bfnmJames R.\binitsJ. R. (\byear1991). \btitleVisual Interactive Fitting of Beta Distributions. \bjournalJournal of Construction Engineering and Management \bvolume117 \bpages589-605. \bdoi10.1061/(ASCE)0733-9364(1991)117:4(589) \endbibitem

- Abramowitz and Stegun (1964) {bbook}[author] \bauthor\bsnmAbramowitz, \bfnmMilton\binitsM. and \bauthor\bsnmStegun, \bfnmIrene A.\binitsI. A. (\byear1964). \btitleHandbook of Mathematical Functions with Formulas, Graphs, and Mathematical Tables, \beditionninth Dover printing, tenth GPO printing ed. \bpublisherDover, \baddressNew York, NY. \endbibitem

- Balding and Nichols (1995) {barticle}[author] \bauthor\bsnmBalding, \bfnmDavid\binitsD. and \bauthor\bsnmNichols, \bfnmRichard\binitsR. (\byear1995). \btitleA method for quantifying differentiation between populations at multi-allelic loci and its implications for investigating identity and paternity. \bjournalGenetica \bvolume96 \bpages3-12. \bnotedoi: 10.1007/BF01441146. \endbibitem

- Bȩtkowski and Pownuk (2004) {binproceedings}[author] \bauthor\bsnmBȩtkowski, \bfnmM.\binitsM. and \bauthor\bsnmPownuk, \bfnmA.\binitsA. (\byear2004). \btitleCalculating Risk of Cost Using Monte Carlo Simulation with Fuzzy Parameters in Civil Engineering. In \bbooktitleProceeding of NSF workshop on Reliable Engineering Computing \bpages179-192. \bpublisherCenter for Reliable Engineering Computing, Georgia Tech Savannah. \endbibitem

- Bernardo, Lauretto and Stern (2012) {binproceedings}[author] \bauthor\bsnmBernardo, \bfnmG. G.\binitsG. G., \bauthor\bsnmLauretto, \bfnmM. S.\binitsM. S. and \bauthor\bsnmStern, \bfnmJ. M.\binitsJ. M. (\byear2012). \btitleThe full Bayesian significance test for symmetry in contingency tables. In \bbooktitleAmerican Institute of Physics Conference Series (\beditor\bfnmP.\binitsP. \bsnmGoyal, \beditor\bfnmA.\binitsA. \bsnmGiffin, \beditor\bfnmK. H.\binitsK. H. \bsnmKnuth and \beditor\bfnmE.\binitsE. \bsnmVrscay, eds.). \bseriesAmerican Institute of Physics Conference Series \bvolume1443 \bpages198-205. \bdoi10.1063/1.3703636 \endbibitem

- Bretthorst (1988) {bbook}[author] \bauthor\bsnmBretthorst, \bfnmG. L.\binitsG. L. (\byear1988). \btitleBayesian Spectrum Analysis and Parameter Estimation. \bpublisherSpringer-Verlag, \baddressBerlin, Germany. \endbibitem

- Dose (2003) {barticle}[author] \bauthor\bsnmDose, \bfnmV.\binitsV. (\byear2003). \btitleHyperplane priors. \bjournalAIP Conference Proceedings \bvolume659 \bpages350-360. \bdoi10.1063/1.1570552 \endbibitem

- Durrett (1994) {bbook}[author] \bauthor\bsnmDurrett, \bfnmRichard\binitsR. (\byear1994). \btitleThe Essentials of Probability. \bpublisherDuxbury Press, A Division of Wadsworth, Inc., \baddressBelmont, CA. \endbibitem

- Eberts and Steinwart (2013) {barticle}[author] \bauthor\bsnmEberts, \bfnmMona\binitsM. and \bauthor\bsnmSteinwart, \bfnmIngo\binitsI. (\byear2013). \btitleOptimal regression rates for SVMs using Gaussian kernels. \bjournalElectron. J. Statist. \bvolume7 \bpages1-42. \endbibitem

- Ford (1971) {bbook}[author] \bauthor\bsnmFord, \bfnmE. B.\binitsE. B. (\byear1971). \btitleEcological Genetics, \bedition3rd ed. ed. \bpublisherChapman and Hall, \baddressLondon, UK. \endbibitem

- Gelman (2008) {barticle}[author] \bauthor\bsnmGelman, \bfnmAndrew\binitsA. (\byear2008). \btitleObjections to Bayesian statistics. \bjournalBayesian Analysis \bvolume3 \bpages445-449. \bdoi10.1214/08-BA318 \endbibitem

- Hall, Park and Samworth (2008) {barticle}[author] \bauthor\bsnmHall, \bfnmP.\binitsP., \bauthor\bsnmPark, \bfnmB. U.\binitsB. U. and \bauthor\bsnmSamworth, \bfnmR. J.\binitsR. J. (\byear2008). \btitleChoice of neighbor order in nearest-neighbor classification. \bjournalAnnals of Statistics \bvolume36 \bpages2135-2152. \bdoi10.1214/07-AOS537 \endbibitem

- Holsinger (2006) {bbook}[author] \bauthor\bsnmHolsinger, \bfnmK. E.\binitsK. E. (\byear2006). \btitleLecture notes in population genetics. \bpublisherStorrs-Mansfield: Dept. Ecology and Evolutionary Biology, University of Connecticut. \endbibitem

- James et al. (1983) {barticle}[author] \bauthor\bsnmJames, \bfnmS. H.\binitsS. H., \bauthor\bsnmWylie, \bfnmA. P.\binitsA. P., \bauthor\bsnmJohnson, \bfnmM. S.\binitsM. S., \bauthor\bsnmCarstairs, \bfnmS. A.\binitsS. A. and \bauthor\bsnmSimpson, \bfnmG. A.\binitsG. A. (\byear1983). \btitleComplex hybridity in Isotoma petraea V. Allozyme variation and the pursuit of hybridity. \bjournalHeredity \bvolume51 \bpages653–663. \endbibitem

- Jaynes (1968) {barticle}[author] \bauthor\bsnmJaynes, \bfnmEdwin T.\binitsE. T. (\byear1968). \btitlePrior probabilities. \bjournalIEEE Transactions On Systems Science and Cybernetics \bvolume4 \bpages227-241. \bdoi10.1109/TSSC.1968.300117 \endbibitem

- Johnson (2017) {bincollection}[author] \bauthor\bsnmJohnson, \bfnmRobert W.\binitsR. W. (\byear2017). \btitleA physicist’s perspective on how one converts observation into information. In \bbooktitleInformation Studies and the Quest for Transdisciplinarity, (\beditor\bfnmMark\binitsM. \bsnmBurgin and \beditor\bfnmWolfgang\binitsW. \bsnmHofkirchner, eds.) \bvolume9 \bpublisherWorld Scientific \bnoteto appear. \endbibitem

- Johnson and Rossell (2010) {barticle}[author] \bauthor\bsnmJohnson, \bfnmValen E.\binitsV. E. and \bauthor\bsnmRossell, \bfnmDavid\binitsD. (\byear2010). \btitleOn the use of non-local prior densities in Bayesian hypothesis tests. \bjournalJournal of the Royal Statistical Society: Series B (Statistical Methodology) \bvolume72 \bpages143-170. \bdoi10.1111/j.1467-9868.2009.00730.x \endbibitem

- Kim and Scott (2012) {barticle}[author] \bauthor\bsnmKim, \bfnmJooSeuk\binitsJ. and \bauthor\bsnmScott, \bfnmClayton D.\binitsC. D. (\byear2012). \btitleRobust Kernel Density Estimation. \bjournalJournal of Machine Learning Research \bvolume13 \bpages2529-2565. \endbibitem

- Kuhl et al. (2010) {barticle}[author] \bauthor\bsnmKuhl, \bfnmM E\binitsM. E., \bauthor\bsnmIvy, \bfnmJ S\binitsJ. S., \bauthor\bsnmLada, \bfnmE K\binitsE. K., \bauthor\bsnmSteiger, \bfnmN M\binitsN. M., \bauthor\bsnmWagner, \bfnmM A\binitsM. A. and \bauthor\bsnmWilson, \bfnmJ R\binitsJ. R. (\byear2010). \btitleUnivariate input models for stochastic simulation. \bjournalJournal of Simulation \bvolume4 \bpages81-97. \bdoidoi:10.1057/jos.2009.31 \endbibitem

- Lazo and Rathie (1978) {barticle}[author] \bauthor\bsnmLazo, \bfnmA. V.\binitsA. V. and \bauthor\bsnmRathie, \bfnmP.\binitsP. (\byear1978). \btitleOn the entropy of continuous probability distributions (Corresp.). \bjournalIEEE Trans. Inf. Theor. \bvolume24 \bpages120–122. \bdoi10.1109/TIT.1978.1055832 \endbibitem

- Peng and So (2002) {barticle}[author] \bauthor\bsnmPeng, \bfnmChao-Ying Joanne\binitsC.-Y. J. and \bauthor\bsnmSo, \bfnmTak-Shing Harry\binitsT.-S. H. (\byear2002). \btitleLogistic Regression Analysis and Reporting: A Primer. \bjournalUnderstanding Statistics \bvolume1 \bpages31-70. \bdoi10.1207/S15328031US0101_04 \endbibitem

- Pereira and Stern (2008) {barticle}[author] \bauthor\bsnmPereira, \bfnmCarlos A de B\binitsC. A. d. B. and \bauthor\bsnmStern, \bfnmJulio Michael\binitsJ. M. (\byear2008). \btitleSpecial characterizations of standard discrete models. \bjournalREVSTAT–Statistical Journal \bvolume6 \bpages199–230. \endbibitem

- Pereira, Stern and Wechsler (2008) {barticle}[author] \bauthor\bsnmPereira, \bfnmCarlos A de B\binitsC. A. d. B., \bauthor\bsnmStern, \bfnmJulio Michael\binitsJ. M. and \bauthor\bsnmWechsler, \bfnmSergio\binitsS. (\byear2008). \btitleCan a significance test be genuinely Bayesian? \bjournalBayesian Analysis \bvolume3 \bpages79–100. \endbibitem

- Press et al. (1992) {bbook}[author] \bauthor\bsnmPress, \bfnmWilliam\binitsW., \bauthor\bsnmTeukolsky, \bfnmSaul\binitsS., \bauthor\bsnmVetterling, \bfnmWilliam\binitsW. and \bauthor\bsnmFlannery, \bfnmBrian\binitsB. (\byear1992). \btitleNumerical Recipes in C, \bedition2nd ed. \bpublisherCambridge University Press, \baddressCambridge, England. \endbibitem

- Price et al. (2006) {barticle}[author] \bauthor\bsnmPrice, \bfnmAlkes L.\binitsA. L., \bauthor\bsnmPatterson, \bfnmNick J.\binitsN. J., \bauthor\bsnmPlenge, \bfnmRobert M.\binitsR. M., \bauthor\bsnmWeinblatt, \bfnmMichael E.\binitsM. E., \bauthor\bsnmShadick, \bfnmNancy A.\binitsN. A. and \bauthor\bsnmReich, \bfnmDavid\binitsD. (\byear2006). \btitlePrincipal components analysis corrects for stratification in genome-wide association studies. \bjournalNature Genetics \bvolume38 \bpages904-909. \bdoi10.1038/ng1847 \endbibitem

- Raiffa and Schlaifer (1961) {bbook}[author] \bauthor\bsnmRaiffa, \bfnmHoward\binitsH. and \bauthor\bsnmSchlaifer, \bfnmRobert\binitsR. (\byear1961). \btitleApplied statistical decision theory. \bpublisherDivision of Research, Graduate School of Business Adminitration, Harvard University Boston. \endbibitem

- Sivia (1996) {bbook}[author] \bauthor\bsnmSivia, \bfnmD. S.\binitsD. S. (\byear1996). \btitleData Analysis: A Bayesian Tutorial. \bseriesOxford Science Publications. \bpublisherOxford University Press, \baddressOxford, UK. \endbibitem

- Stern (2011) {barticle}[author] \bauthor\bsnmStern, \bfnmJulio Michael\binitsJ. M. (\byear2011). \btitleSymmetry, invariance and ontology in physics and statistics. \bjournalSymmetry \bvolume3 \bpages611–635. \endbibitem

- Stern and Pereira (2013) {barticle}[author] \bauthor\bsnmStern, \bfnmJulio Michael\binitsJ. M. and \bauthor\bsnmPereira, \bfnmCarlos A de B\binitsC. A. d. B. (\byear2013). \btitleBayesian epistemic values: focus on surprise, measure probability! \bjournalLogic Journal of IGPL. \bnotedoi: 10.1093/jigpal/jzt023. \bdoi10.1093/jigpal/jzt023 \endbibitem

- Terrell and Scott (1992) {barticle}[author] \bauthor\bsnmTerrell, \bfnmGeorge R.\binitsG. R. and \bauthor\bsnmScott, \bfnmDavid W.\binitsD. W. (\byear1992). \btitleVariable kernel density estimation. \bjournalAnnals of Statistics \bvolume20 \bpages1236-1265. \bdoi10.1214/aos/1176348768 \endbibitem