Modelling energy spot prices by volatility modulated Lévy-driven Volterra processes

Abstract

This paper introduces the class of volatility modulated Lévy-driven Volterra () processes and their important subclass of Lévy semistationary () processes as a new framework for modelling energy spot prices. The main modelling idea consists of four principles: First, deseasonalised spot prices can be modelled directly in stationarity. Second, stochastic volatility is regarded as a key factor for modelling energy spot prices. Third, the model allows for the possibility of jumps and extreme spikes and, lastly, it features great flexibility in terms of modelling the autocorrelation structure and the Samuelson effect. We provide a detailed analysis of the probabilistic properties of processes and show how they can capture many stylised facts of energy markets. Further, we derive forward prices based on our new spot price models and discuss option pricing. An empirical example based on electricity spot prices from the European Energy Exchange confirms the practical relevance of our new modelling framework.

doi:

10.3150/12-BEJ476keywords:

, and

1 Introduction

Energy markets have been liberalised worldwide in the last two decades. Since then we have witnessed the increasing importance of such commodity markets which organise the trade and supply of energy such as electricity, oil, gas and coal. Closely related markets include also temperature and carbon markets. There is no doubt that such markets will play a vital role in the future given that the global demand for energy is constantly increasing. The main products traded on energy markets are spot prices, futures and forward contracts and options written on them. Recently, there has been an increasing research interest in the question of how such energy prices can be modelled mathematically. In this paper, we will focus on modelling energy spot prices, which include day-ahead as well as real-time prices.

Traditional spot price models typically allow for mean-reversion to reflect the fact that spot prices are determined as equilibrium prices between supply and demand. In particular, they are commonly based on a Gaussian Ornstein–Uhlenbeck (OU) process, see Schwartz [62], or more generally, on weighted sums of OU processes with different levels of mean-reversion, see, for example, Benth, Kallsen and Meyer-Brandis [24] and Klüppelberg, Meyer-Brandis and Schmidt [53]. In such a modelling framework, the mean-reversion is modelled directly or physically, by claiming that the price change is (negatively) proportional to the current price. In this paper, we interpret the mean-reversion often found in commodity markets in a weak sense meaning that prices typically concentrate around a mean-level for demand and supply reasons. In order to account for such a weak form mean-reversion, we suggest to use a modelling framework which allows to model spot prices (after seasonal adjustment) directly in stationarity. This paper proposes to use the class of volatility modulated Lévy-driven Volterra () processes as the building block for energy spot price models. In particular, the subclass of so-called Lévy semistationary () processes turns out to be of high practical relevance. Our main innovation lies in the fact that we propose a modelling framework for energy spot prices which (1) allows to model deseasonalised energy spot prices directly in stationarity, (2) comprises stochastic volatility, (3) accounts for the possibility of jumps and spikes, (4) features great flexibility in terms of modelling the autocorrelation structure of spot prices and of describing the so-called Samuelson effect, which refers to the finding that the volatility of a forward contract typically increases towards maturity.

We show that the new class of processes is analytically tractable, and we will give a detailed account of the theoretical properties of such processes. Furthermore, we derive explicit expressions for the forward prices implied by our new spot price model. In addition, we will see that our new modelling framework encompasses many classical models such as those based on the Schwartz one-factor mean-reversion model, see Schwartz [62], and the wider class of continuous-time autoregressive moving-average (CARMA) processes. In that sense, it can also be regarded as a unifying modelling approach for the most commonly used models for energy spot prices. However, the class of processes is much wider and directly allows to model the key special features of energy spot prices and, in particular, the stochastic volatility component.

The remaining part of the paper is structured as follows. We start by introducing the class of processes in Section 2. Next, we formulate both a geometric and an arithmetic spot price model class in Section 3 and describe how our new models embed many of the traditional models used in the recent literature. In Section 4, we derive the forward price dynamics of the models and consider questions like affinity of the forward price with respect to the underlying spot. Section 5 contains an empirical example, where we study electricity spot prices from the European Energy Exchange (EEX). Finally, Section 6 concludes, and the Appendix contains the proofs of the main results.

2 Preliminaries

Throughout this paper, we suppose that we have given a probability space with a filtration satisfying the ‘usual conditions,’ see Karatzas and Shreve [52], Definition I.2.25.

2.1 The driving Lévy process

Let denote a càdlàg Lévy process with Lévy–Khinchine representation for , and

for , and the Lévy measure satisfying and . We denote the corresponding characteristic triplet by . In a next step, we extend the definition of the Lévy process to a process defined on the entire real line, by taking an independent copy of , which we denote by and we define for . Throughout the paper denotes such a two-sided Lévy process.

2.2 Volatility modulated Lévy-driven Volterra processes

The class of volatility modulated Lévy-driven Volterra () processes, introduced by Barndorff-Nielsen and Schmiegel [11], has the form

| (1) |

where is a constant, is the two-sided Lévy process defined above, are measurable deterministic functions with for , and and are càdlàg stochastic processes which are (throughout the paper) assumed to be independent of . In addition, we assume that is positive. Note that such a process generalises the class of convoluted subordinators defined in Bender and Marquardt [21] to allow for stochastic volatility.

A very important subclass of processes is the new class of Lévy semistationary () processes: We choose two functions such that and with whenever , then an process is given by

| (2) |

Note that the name Lévy semistationary processes has been derived from the fact that the process is stationary as soon as and are stationary. In the case that is a two-sided Brownian motion, we call such processes Brownian semistationary () processes, which have recently been introduced by Barndorff-Nielsen and Schmiegel [12] in the context of modelling turbulence in physics.

The class of processes can be considered as the natural analogue for (semi-) stationary processes of Lévy semimartingales (), given by

The class of processes can be embedded into the class of ambit fields, see Barndorf-Nilsen and Schmiegel [9, 10], Barndorff-Nielsen, Benth and Veraart [6, 5].

Also, it is possible to define and processes for singular kernel functions and , respectively; a function (or ) defined as above is said to be singular if (or ) does not exist or is not finite.

2.3 Integrability conditions

In order to simplify the exposition, we will focus on the stochastic integral in the definition of an (and of an ) process only. That is, throughout the rest of the paper, let

| (3) |

In this paper, we use the stochastic integration concept described in Basse-O’Connor, Graversen and Pedersen [20] where a stochastic integration theory on , rather than on compact intervals as in the classical framework, is presented. Throughout the paper, we assume that the filtration is such that is a Lévy process with respect to , see Basse-O’Connor, Graversen and Pedersen [20], Section 4, for details.

Let denote the Lévy triplet of associated with a truncation function . According to Basse-O’Connor, Graversen and Pedersen [20], Corollary 4.1, for the process with is integrable with respect to if and only if is -predictable and the following conditions hold almost surely:

| (4) | |||||

When we plug in , we immediately obtain the corresponding integrability conditions for the process.

Example 1.

In the case of a Gaussian Ornstein–Uhlenbeck process, that is, when for and , then the integrability conditions above are clearly satisfied, since we have

2.3.1 Square integrability

For many financial applications, it is natural to restrict the attention to models where the variance is finite, and we focus therefore on Lévy processes with finite second moment. Note that the integrability conditions above do not ensure square-integrability of even if has finite second moment. But substitute the first condition in (2.3) with the stronger condition

| (5) |

then is square integrable. Clearly, is constant in case of stationarity. For the Lebesgue integral part, we need

| (6) |

According to the Cauchy–Schwarz inequality, we find

for any constant . Thus, a sufficient condition for (6) to hold is that there exists an such that

which simplifies to

| (7) |

in the case. Given a model for and , these conditions are simple to verify. Let us consider an example.

Example 2.

In Example 1, we showed that for the kernel function and in the case of constant volatility, the conditions (2.3) are satisfied. Next, suppose that there is stochastic volatility, which is defined by the Barndorff-Nielsen and Shephard [13] stochastic volatility model, that is , for , and a subordinator . Suppose now that has cumulant function for a Lévy measure supported on the positive real axis, and that has finite expectation. In this case, we have that for all . Thus, both (5) and (6) are satisfied (the latter can be seen after using the sufficient conditions), and we find that is a square-integrable stochastic process.

3 The new model class for energy spot prices

This section presents the new modelling framework for energy spot prices, which is based on processes. As before, for ease of exposition, we will disregard the drift part in the general process for most of our analysis and rather use with

| (8) |

as the building block for energy spot price, see (1) for the precise definition of all components. Throughout the paper, we assume that the corresponding integrability conditions hold. We can use the process defined in (8) as the building block to define both a geometric and an arithmetic model for the energy spot price. Also, we need to account for trends and seasonal effects. Let denote a bounded and measurable deterministic seasonality and trend function.

In a geometric set up, we define the spot price by

| (9) |

In such a modelling framework, the deseasonalised, logarithmic spot price is given by a process. Alternatively, one can construct a spot price model which is of arithmetic type. In particular, we define the electricity spot price by

| (10) |

(Note that the seasonal function in the geometric and the arithmetic model is typically not the same.) For general asset price models, one usually formulates conditions which ensure that prices can only take positive values. We can easily ensure positivity of our arithmetic model by imposing that is a Lévy subordinator and that the kernel function takes only positive values.

3.1 Model properties

3.1.1 Possibility of modelling in stationarity

We have formulated the new spot price model in the general form based on a process to be able to account for non-stationary effects, see, for example, Burger et al. [38], Burger, Graeber and Schindlmayr [37]. If the empirical data analysis, however, supports the assumption of working under stationarity, then we will restrict ourselves to the analysis of processes with stationary stochastic volatility. As mentioned in the Introduction, traditional models for energy spot prices are typically based on mean-reverting stochastic processes, see, for example, Schwartz [62], since such a modelling framework reflects the fact that commodity spot prices are equilibrium prices determined by supply and demand. Stationarity can be regarded as a weak form of mean-reversion and is often found in empirical studies on energy spot prices; one such example will be presented in this paper.

3.1.2 The initial value

In order to be able to have a stationary model, the lower integration bound in the definition of the process, and in particular for the process, is chosen to be rather than 0. Clearly, in any real application, we observe data from a starting value onwards, which is traditionally chosen as the observation at time . Hence, while processes are defined on the entire real line, we only define the spot price for . The observed initial value of the spot price at time is assumed to be a realisation of the random variable and , respectively. Such a choice guarantees that the deseasonalised spot price is a stationary process, provided we are in the stationary framework.

3.1.3 The driving Lévy process

Since and processes are driven by a general Lévy process , it is possible to account for price jumps and spikes, which are often observed in electricity markets. At the same time, one can also allow for Brownian motion-driven models, which are very common in, for example, temperature markets, see, for example, Benth, Härdle and Cabrera [23].

3.1.4 Stochastic volatility

A key ingredient of our new modelling framework which sets the model apart from many traditional models is the fact that it allows for stochastic volatility. Volatility clusters are often found in energy prices, see, for example, Hikspoors and Jaimungal [50], Trolle and Schwartz [64], Benth [22], Benth and Vos [26], Koopman, Ooms and Carnero [55], Veraart and Veraart [65]. Therefore, it is important to have a stochastic volatility component, given by , in the model. Note that a very general model for the volatility process would be to choose an process, that is, and

| (11) |

where denotes a deterministic, positive function and is a Lévy subordinator. In fact, if we want to ensure that the volatility is stationary, we can work with a function of the form , for a deterministic, positive function .

3.1.5 Autocorrelation structure and Samuelson effect

The kernel function (or ) plays a vital role in our model and introduces a flexibility which many traditional models lack: We will see in Section 3.2 that the kernel function – together with the autocorrelation function of the stochastic volatility process – determines the autocorrelation function of the process . Hence our – based models are able to produce various types of autocorrelation functions depending on the choice of the kernel function . It is important to stress here that this can be achieved by using one process only, whereas some traditional models need to introduce a multi-factor structure to obtain a comparable modelling flexibility. Also due to the flexibility in the choice of the kernel function, we can achieve greater flexibility in modelling the shape of the Samuelson effect often observed in forward prices, including the hyperbolic one suggested by Bjerksund, Rasmussen and Stensland [31] as a reasonable volatility feature in power markets. Note that we obtain the modelling flexibility in terms of the general kernel function here since we specify our model directly through a stochastic integral whereas most of the traditional models are specified through evolutionary equations, which limit the choices of kernel functions associated with solutions to such equations. In that context, we note that a or an process cannot in general be written in form of a stochastic differential equation (due to the non-semimartingale character of the process). In Section 3.3, we will discuss sufficient conditions which ensure that an process is a semimartingale.

3.1.6 A unifying approach for traditional spot price models

As already mentioned above, energy spot prices are typically modelled in stationarity, hence the class of processes is particularly relevant for applications. In the following, we will show that many of the traditional spot price models can be embedded into our process-based framework.

Our new framework nests the stationary version of the classical one-factor Schwartz [62] model studied for oil prices. By letting be a Lévy process with the pure-jump part given as a compound Poisson process, Cartea and Figueroa [40] successfully fitted the Schwartz model to electricity spot prices in the UK market. Benth and Šaltytė Benth [27] used a normal inverse Gaussian Lévy process to model UK spot gas and Brent crude oil spot prices. Another example which is nested by the class of processes is a model studied in Benth [22] in the context of gas markets, where the deseasonalised logarithmic spot price dynamics is assumed to follow a one-factor Schwartz process with stochastic volatility. A more general class of models which is nested is the class of so-called CARMA-processes, which has been successfully used in temperature modelling and weather derivatives pricing, see Benth, Šaltytė Benth and Koekebakker [30], Benth, Härdle and López Cabrera [23] and Härdle and López Cabrera [49], and more recently for electricity prices by García, Klüppelberg and Müller [45], Benth et al. [25]. A CARMA process is the continuous-time analogue of an ARMA time series, see Brockwell [33], Brockwell [34] for definition and details. More precisely, suppose that for nonnegative integers

where and is a -dimensional OU process of the form

| (12) |

with

Here we use the notation for the -identity matrix, the th coordinate vector (where the first entries are zero and the th entry is 1) and is the transpose of , with and for . In Brockwell [35], it is shown that if all the eigenvalues of have negative real parts, then defined as

is the (strictly) stationary solution of (12). Moreover,

| (13) |

is a process. Hence, specifying in (13), the log-spot price dynamics will be an process, but without stochastic volatility. García, Klüppelberg and Müller [45] argue for dynamics as an appropriate class of models for the deseasonalised log-spot price at the Singapore New Electricity Market. The innovation process is chosen to be in the class of stable processes. From Benth, Šaltytė Benth and Koekebakker [30], Brownian motion-driven models seem appropriate for modelling daily average temperatures, and are applied for temperature derivatives pricing, including forward price dynamics of various contracts. More recently, the dynamics of wind speeds have been modelled by a Brownian motion-driven model, and applied to wind derivatives pricing, see Benth and Šaltytė Benth [28] for more details.

Finally note that the arithmetic model based on a superposition of processes nests the non-Gaussian Ornstein–Uhlenbeck model which has recently been proposed for modelling electricity spot prices, see Benth, Kallsen and Meyer-Brandis [24].

We emphasis again that, beyond the fact that processes can be regarded as a unifying modelling approach which nest many of the existing spot price models, they also open up for entirely new model specifications, including more general choices of the kernel function (resulting in non-linear models) and the presence of stochastic volatility.

3.2 Second order structure

Next, we study the second order structure of volatility modulated Volterra processes , where , assuming the integrability conditions (2.3) hold and that in addition is square integrable. Let and . Recall that throughout the paper we assume that the stochastic volatility is independent of the driving Lévy process. Note that proofs of the following results are easy and hence omitted.

Proposition 0

The conditional second order structure of is given by

Corollary 0

The conditional second order structure of is given by

The unconditional second order structure of is then given as follows.

Proposition 0

The second order structure of for stationary is given by

where denotes the autocovariance function of , for .

The unconditional second order structure of is then given as follows.

Corollary 0

The second order structure of for stationary is given by

where denotes the autocovariance function of , for . Hence, we have

| (14) | |||

Corollary 0

If or if has zero autocorrelation, then

The last corollary shows that we get the same autocorrelation function as in the model. From the results above, we clearly see the influence of the general damping function on the correlation structure. A particular choice of , which is interesting in the energy context is studied in the next example.

Example 3.

Consider the case for and , which is motivated from the forward model of Bjerksund, Rasmussen and Stensland [31], which we shall return to in Section 4. We have that This ensures integrability of over with respect to any square integrable martingale Lévy process . Furthermore, . Thus,

Observe that since can be written as

it follows that the process is a semimartingale according to the Knight condition, see Knight [54] and also Basse [18], Basse and Pedersen [19], Basse-O’Connor, Graversen and Pedersen [20].

3.3 Semimartingale conditions and absence of arbitrage

We pointed out that the subclass of processes are particularly relevant for modelling energy spot prices since they allow one to model directly in stationarity. Let us focus on this class in more detail. Clearly, an process is in general not a semimartingale. However, we can formulate sufficient conditions on the kernel function and on the stochastic volatility component which ensure the semimartingale property. The sufficient conditions are in line with the conditions formulated for processes in Barndorff-Nielsen and Schmiegel [12], see also Barndorff-Nielsen and Basse-O’Connor [4]. Note that the proofs of the following results are provided in the Appendix.

Proposition 0

Let be an process as defined in (2). Suppose the following conditions hold: (

-

iii)]

-

(i)

.

-

(ii)

The function values and exist and are finite.

-

(iii)

The kernel function is absolutely continuous with square integrable derivative .

-

(iv)

The process is square integrable for each .

-

(v)

The process is integrable for each .

Then is a semimartingale with representation

| (15) |

where for and

Example 4.

An example of a kernel function which satisfies the above conditions is given by

For , is given by a volatility modulated Ornstein–Uhlenbeck process.

In a next step, we are now able to find a representation for the quadratic variation of an process provided the conditions of Proposition 6 are satisfied.

Proposition 0

Let be an process and suppose that the sufficient conditions for to be a semimartingale (as formulated in Proposition 6) hold. Then, the quadratic variation of is given by

Note that the quadratic variation is a prominent measure of accumulated stochastic volatility or intermittency over a certain period of time and, hence, is a key object of interest in many areas of application and, in particular, in finance.

The question of deriving semimartingale conditions for processes is closely linked to the question whether a spot price model based on an process is prone to arbitrage opportunities. In classical financial theory, we usually stick to the semimartingale framework to ensure the absence of arbitrage. Nevertheless one might ask the question whether one could still work with the wider class of processes which are not semimartingales. Here we note that the standard semimartingale assumption in mathematical finance is only valid for tradeable assets in the sense of assets which can be held in a portfolio. Hence, when dealing with, for example, electricity spot prices, this assumption is not valid since electricity is essentially non-storable. Hence, such a spot price cannot be part of any financial portfolio and, therefore, the requirement of being a martingale under some equivalent measure is not necessary.

Guasoni, Rásonyi and Schachermayer [47] have pointed out that, while in frictionless markets martingale measures play a key role, this is not the case any more in the presence of market imperfections. In fact, in markets with transaction costs, consistent price systems as introduced in Schachermayer [61] are essential. In such a set-up, even processes which are not semimartingales can ensure that we have no free lunch with vanishing risk in the sense of Delbaen and Schachermayer [42]. It turns out that if a continuous price process has conditional full support, then it admits consistent price systems for arbitrarily small transaction costs, see Guasoni, Rásonyi and Schachermayer [47]. It has recently been shown by Pakkanen [57], that under certain conditions, a process has conditional full support. This means that such processes can be used in financial applications without necessarily giving rise to arbitrage opportunities.

3.4 Model extensions

Let us briefly point out some model extensions concerning a multi-factor structure, non-stationary effects, multivariate models and alternative methods for incorporating stochastic volatility.

A straightforward extension of our model is to study a superposition of processes for the spot price dynamics. That is, we could replace the process by a superposition of factors:

| (16) |

and where all are defined as in (8) for independent Lévy processes and independent stochastic volatility processes , in both the geometric and the arithmetic model. Such models include the Benth, Kallsen and Meyer-Brandis [24] model as a special case. A superposition of factors opens up for separate modelling of spikes and other effects. For instance, one could let the first factor account for the spikes, using a Lévy process with big jumps at low frequency, while the function forces the jumps back at a high speed. The next factor(s) could model the “normal” variations of the market, where one observes a slower force of mean-reversion, and high frequent Brownian-like noise, see Veraart and Veraart [65] for extensions along these lines. Note that all the results we derive in this paper based on the one factor model can be easily generalised to accommodate for the multi-factor framework. It should be noted that this type of “superposition” is quite different from the concept behind supOU processes as studied in, for example, Barndorff-Nielsen and Stelzer [15].

In order to study various energy spot prices simultaneously, one can consider extensions to a multivariate framework along the lines of Barndorff-Nielsen and Stelzer [16, 15], Veraart and Veraart [65].

In addition, another interesting aspect which we leave for future research is the question of alternative ways of introducing stochastic volatility in processes. So far, we have introduced stochastic volatility by considering a stochastic proportional of the driving Lévy process, that is, we work with a stochastic integral of with respect to . An alternative model specification could be based on a stochastic time change , where . Such models can be constructed in a fashion similar to that of volatility modulated non-Gaussian Ornstein–Uhlenbeck processes introduced in Barndorff-Nielsen and Veraart [17]. We know that outside the Brownian or stable Lévy framework, stochastic proportional and stochastic time change are not equivalent. Whereas in the first case the jump size is modulated by a volatility term, in the latter case the speed of the process is changed randomly. These two concepts are in fact fundamentally different (except for the special cases pointed out above) and, hence, it will be worth investigating whether a combination of stochastic proportional and stochastic time change might be useful in certain applications.

4 Pricing of forward contracts

In this subsection, we are concerned with the calculation of the forward price at time for contracts maturing at time . We denote by a finite time horizon for the forward market, meaning that all contracts of interest mature before this date. Note that in energy markets, the corresponding commodity typically gets delivered over a delivery period rather than at a fixed point in time. Extensions to such a framework can be dealt with using standard methods, see, for example, Benth, Šaltytė Benth and Koekebakker [29] for more details.

Let denote the spot price, being either of geometric or arithmetic kind as defined in (9) and (10), respectively, with

where the stochastic volatility is chosen as previously defined in (11). Clearly, the corresponding results for processes can be obtained by choosing . We use the conventional definition of a forward price in incomplete markets, see Duffie [43], ensuring the martingale property of ,

| (17) |

with being an equivalent probability measure to . Here, we suppose that , the space of integrable random variables. In a moment, we shall introduce sufficient conditions for this.

4.1 Change of measure by generalised Esscher transform

In finance, one usually uses equivalent martingale measures , meaning that the equivalent probability measure should turn the discounted price dynamics of the underlying asset into a (local) -martingale. However, as we have already discussed, this restriction is not relevant in, for example, electricity markets since the spot is not tradeable. Thus, we may choose any equivalent probability as pricing measure. In practice, however, one restricts to a parametric class of equivalent probability measures, and the standard choice seems to be given by the Esscher transform, see Benth, Šaltytė Benth and Koekebakker [29], Shiryaev [63]. The Esscher transform naturally extends the Girsanov transform to Lévy processes.

To this end, consider defined as the (generalised) Esscher transform of for a parameter being a Borel measurable function. Following Shiryaev [63] (or Benth, Šaltytė Benth and Koekebakker [29], Barndorff-Nielsen and Shiryaev [14]), is defined via the Radon–Nikodym density process

| (18) |

for being a real-valued function which is integrable with respect to the Lévy process on , and

(for ) being the log-moment generating function of , assuming that the moment generating function of exists.

A special choice is the ‘constant’ measure change, that is, letting

| (19) |

In this case, if under the measure , has characteristic triplet , where is the drift, is the squared volatility of the continuous martingale part and is the Lévy measure in the Lévy–Khinchine representation, see Shiryaev [63], a fairly straightforward calculation shows that, see Shiryaev [63] again, the Esscher transform preserves the Lévy property of , and the characteristic triplet under the measure on the interval becomes , where

This comes from the simple fact that the logarithmic moment generating function of under is

| (20) |

It is important to note here that the choice of (as, e.g., in (19)) forces us to choose a starting time since the function will not be integrable with respect to on the unbounded interval . Recall that the only reason why we model from rather than from is the fact that we want to be able to obtain a stationary process under the probability measure . Throughout this section, we choose the starting time to be zero, which is a convenient choice since , and it is also practically reasonable since this can be considered as the time from which we start to observe the process. With such a choice, we do not introduce any risk premium for . In the general case, with a time-dependent parameter function , the characteristic triplet of under will become time-dependent, and hence the Lévy process property is lost. Instead, will be an independent increment process (sometimes called an additive process). Note that if , a Brownian motion, the Esscher transform is simply a Girsanov change of measure where for and a -Brownian motion .

Similarly, we do a (generalised) Esscher transform of , the subordinator driving the stochastic volatility model, see (11). We define to have the Radon–Nikodym density process

for being a real-valued function which is integrable with respect to on , and being the log-moment generating function of . Since is a subordinator, we obtain

where and denotes the Lévy measure associated with . {rem*} Our discussion above on choosing a starting value applies to the measure transform for the volatility process as well, and hence throughout the paper we will work under the assumption that for . Note in particular, that this assumption implies that under the risk-neutral probability measure, the characteristic triplets of and only change on the time interval . On the interval , we have the same characteristic triplet for and as under . Choosing , with a constant , an Esscher transform will give a characteristic triplet , which thus preserves the subordinator property of under . For the general case, the process will be a time-inhomogeneous subordinator (independent increment process with positive jumps). The log-moment generating function of under the measure is denoted by .

In order to ensure the existence of the (generalised) Esscher transforms, we need some conditions. We need that there exists a constant such that , and where . (Similarly, we must have such a condition for the Lévy measure of the subordinator driving the stochastic volatility, that is, ). Also, we must require that exponential moments of and exist. More precisely, we suppose that parameter functions and of the (generalised) Esscher transform are such that

| (21) |

The exponential integrability conditions of the Lévy measures of and imply the existence of exponential moments, and thus that the Esscher transforms and are well defined.

We define the probability as the class of pricing measures for deriving forward prices. In this respect, may be referred to as the market price of risk, whereas is the market price of volatility risk. We note that a choice will put more weight to the positive jumps in the price dynamics, and less on the negative, increasing the “risk” for big upward movements in the prices under .

Let us denote by the expectation operator with respect to , and by the expectation with respect to .

4.1.1 Forward price in the geometric case

Suppose that the spot price is defined by the geometric model

where is defined as in (3). In order to have the forward price well defined, we need to ensure that the spot price is integrable with respect to the chosen pricing measure . We discuss this issue in more detail in the following.

We know that is positive and in general not bounded since it is defined via a subordinator. Thus, (for ) is unbounded as well. Supposing that has exponential moments of all orders, we can calculate as follows using iterated expectations conditioning on the filtration generated by the paths of , for :

To have that , the two integrals must be finite. This puts additional restrictions on the choice of and the specifications of and . We note that when applying the Esscher transform, we must require that has exponential moments of all orders, a rather strong restriction on the possible class of driving Lévy processes. In our empirical study, however, we will later see that the empirically relevant cases are either that is a Brownian motion or that is a generalised hyperbolic Lévy process, which possess exponential moments of all orders.

We are now ready to price forwards under the Esscher transform.

Proposition 0

Suppose that . Then, the forward price for is given by

4.2 Change of measure by the Girsanov transform in the Brownian case

As a special case, consider , where is a two-sided standard Brownian motion under . In this case we apply the Girsanov transform rather than the generalised Esscher transform, and it turns out that a rescaling of the transform parameter function by the volatility is convenient for pricing of forwards. To this end, consider the Girsanov transform

| (22) |

that is, we set for . Supposing that the Novikov condition

holds, we know that is a Brownian motion for under a probability having density process

Suppose that there exists a measurable function such that

| (23) |

for all , with

Furthermore, suppose the moment generating function of exists on the interval . Then, for all such that , the Novikov condition is satisfied, since by the subordinator property of (restricting our attention to )

and therefore

Specifying , we have that , and condition (23) holds with equality.

4.2.1 Forward price in the geometric case

We discuss the integrability of with respect to . By double conditioning with respect to the filtration generated by the paths of , we find

From collecting the conditions on and for verifying all the steps above, we find that if is integrable on (recall that for ) and is integrable on for all , then as long as

| (24) |

We assume these conditions to hold.

We state the forward price for the case and the Girsanov change of measure discussed above.

Proposition 0

Suppose that and that is defined by the Girsanov transform in (22). Then, for ,

Let us consider an example.

4.2.2 On the case of constant volatility

Suppose for a moment that the stochastic volatility process is identical to one (i.e., that we do not have any stochastic volatility in the model). In this case, the forward price becomes

where for . Hence, the logarithmic forward (log-forward) price is

with

for . Note that , for , is a -martingale with the property (for )

In the classical Ornstein–Uhlenbeck case, with , for , we easily compute that

and the forward price is explicitly dependent on the current spot price.

In the general case, this does not hold true. We have that , not unexpectedly, since the forward price converges to the spot at maturity (at least theoretically). However, apart from the special time point , the forward price will in general not be a function of the current spot, but a function of the process . Thus, at time , the forward price will depend on

whereas the spot price depends on

The two stochastic integrals can be pathwise interpreted (they are both Wiener integrals since the integrands are deterministic functions), and both and are generated by integrating over the same paths of a Brownian motion. However, the paths are scaled by two different functions and . This allows for an additional degree of flexibility when creating forward curves compared to affine structures.

In the classical Ornstein–Uhlenbeck case, the forward curve as a function of time to maturity will simply be a discounting of today’s spot price, discounted by the speed of mean reversion of the spot (in addition comes deterministic scaling by the seasonality and market price of risk). To highlight the additional flexibility in our modelling framework of semistationary processes, suppose for the sake of illustration that . Then

If furthermore , we are in a situation where the long end (i.e., large) of the forward curve is not a constant. In fact, we find for that

Since is random, we will have a randomly fluctuating long end of the forward curve. This is very different from the situation with a classical mean-reverting spot dynamics, which implies a deterministic forward price in the long end (dependent on the seasonality and market price of risk only). Various shapes of the forward curve can also be modelled via different specifications of . For instance, if is a decreasing function, we obtain the contango and backwardation situations depending on the spot price being above or below the mean. If has a hump, we will also observe a hump in the forward curve. For general specifications of we can have a high degree of flexibility in matching desirable shapes of the forward curve.

Observe that the time-dynamics of the forward price can be considered as correlated with the spot rather than directly depending on the spot. In the Ornstein–Uhlenbeck situation, the log-forward price can be considered as a linear regression on the current spot price, with time-dependent coefficients. This is not the case for general specifications. However, we have that and are both normally distributed random variables (recall that we are still restricting our attention to ), and the correlation between the two is

Obviously, for , the correlation is 1. In conclusion, we can obtain a weaker stochastic dependency between the spot and forward price than in the classical mean-reversion case by a different specification of the function .

4.2.3 Affine structure of the forward price

In the discussion above, we saw that the choice yielded a forward price expressible in terms of . In the next proposition, we prove that this is the only choice of yielding an affine structure. The result is slightly generalising the analysis of Carverhill [41].

Proposition 0

The forward price in Proposition 9 is affine in and if there exist functions and such that and . Conversely, if the forward price is affine in and , and and are strictly positive and continuously differentiable in the first argument, then there exists functions and such that and .

Obviously, the choice of and coming from OU-models,

satisfy the conditions in the proposition above. In fact, appealing to similar arguments as in the proof of Proposition 10 above, one can show that this is the only choice (modulo multiplication by a constant) which is stationary and gives an affine structure in the spot and volatility for the forward price dynamics. In particular, the specification considered in Example 3 gives a stationary spot price dynamics, but not an affine structure in the spot for the forward price.

4.2.4 Risk-neutral dynamics of the forward price and the Samuelson effect

Next, we turn our attention to the risk-neutral dynamics of the forward price.

Proposition 0

Assume that the assumptions of Proposition 9 hold and that is given by the (simple) Esscher transform. Then the risk-neutral dynamics of the forward price is given by

where . Moreover is a -martingale, where denotes the Poisson random measure associated with , and is the Lévy measure of under .

We observe that the dynamics will jump according to the changes in volatility given by the process . As expected, the integrand in the jump expression tends to zero when , since the forward price must (at least theoretically) converge to the spot when time to maturity goes to zero.

The forward dynamics will have a stochastic volatility given by . Hence, whenever exists, and , we have ,

When passing to the limit, we have implicitly supposed that we work with the version of having left-continuous paths with right-limits. By the definition of our integral in , where the integrand is supposed predictable, this can be done. Thus, we find that the forward volatility converges to the spot volatility as time to maturity tends to zero, which is known as the Samuelson effect. Contrary to the classical situation where this convergence goes exponentially, we may have many different shapes of the volatility term structure resulting from our general modelling framework.

In Bjerksund, Rasmussen and Stensland [31], a forward price dynamics for electricity contracts is proposed to follow

| (25) |

where and are positive constants. They argue that in electricity markets, the Samuelson effect is stronger close to maturity than what is observed in other commodity markets, and they suggest to capture this by letting it increase by the rate close to maturity of the contracts. This is in contrast to the common choice of volatility being , resulting from using the Schwartz model for the spot price dynamics. There is no reference to any spot model in the Bjerksund, Rasmussen and Stensland [31] model. The constant comes from a non-stationary behaviour, which can be incorporated in the framework. However, here we focus on the stationary case and choose . Then we see that we can model the spot price by the process

Thus, after doing a Girsanov transform, we recover the risk-neutral forward dynamics of Bjerksund, Rasmussen and Stensland [31]. It is interesting to note that with this spot price dynamics, the forward dynamics is not affine in the spot. Hence, the Bjerksund, Rasmussen and Stensland [31] model is an example of a non-affine forward dynamics. Whenever , we do not have that , and thus the Bjerksund, Rasmussen and Stensland [31] model does not satisfy the Samuelson effect, either.

4.2.5 Option pricing

We end this section with a discussion of option pricing. Let us assume that we have given an option with exercise time on a forward with maturity at time . The option pays , and we are interested in finding the price at time , denoted . From arbitrage theory, it holds that

| (26) |

where is the risk-neutral probability. Choosing as coming from the Esscher transform above, we can derive option prices explicitly in terms of the characteristic function of by Fourier transformation.

Proposition 0

Let be the probability measure obtained from the Esscher transform. Let , and suppose that . By applying the definitions of Fourier transforms and their inverses in Folland [44], we have that , with is the Fourier transform of defined by Suppose that . Then the option price is given by

where and

One can calculate option prices by applying the fast Fourier transform as long is known. If is not integrable (as is the case for a call option), one may introduce a damping function to regularize it, see Carr and Madan [39] for details.

4.3 The arithmetic case

Let us consider the arithmetic spot price model,

We analyse the forward price for this case, and discuss the affinity. The results and discussions are reasonably parallel to the geometric case, and we refrain from going into details but focus on some main results.

Under a natural integrability condition of the spot price with respect to the Esscher transform measure , we find the following forward price for the arithmetic model.

Proposition 0

Suppose that . Then, the forward price is given as

The price is reasonably explicit, except for the conditional expectation of the stochastic volatility . By the same arguments as in Proposition 10, the forward price becomes affine in the spot (or in ) if and only if for sufficiently regular functions and .

In the case , we can obtain an explicit forward price when using the Girsanov transform as in (22). We easily compute that the forward price becomes

| (27) |

We note that there is no explicit dependence of the spot volatility except indirectly in the stochastic integral. This is in contrast to the Lévy case with Esscher transform. The dynamics of the forward price becomes

| (28) |

If we furthermore let for some sufficiently regular functions and , we find that

| (29) |

Hence, the forward curve moves stochastically as the deseasonalised spot price, whereas the shape of the curve is deterministically given by . This shape is scaled stochastically by the deseasonalised spot price. In addition, there is a deterministic term which is derived from the market price of risk .

We finally remark that also in the arithmetic case one may derive expressions for the prices of options that are computable by fast Fourier techniques.

5 Empirical study

In this section, we will show the practical relevance of our new model class for modelling empirical energy spot prices. Here we will focus on electricity spot prices and we will illustrate that they can be modelled by processes – an important subclass of processes. Note that the data analysis is exploratory in nature since the estimation theory for or processes has not been fully established yet.

5.1 Data description

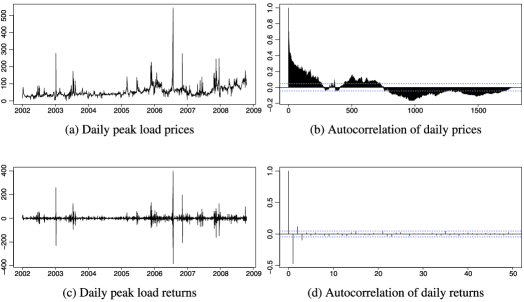

We study electricity spot prices from the European Energy Exchange (EEX). We work with the daily Phelix peak load data (i.e., the daily averages of the hourly spot prices for electricity delivered during the 12 hours between 8am and 8pm) with delivery days from 01.01.2002 to 21.10.2008. Note that peak load data do not include weekends, and in total we have 1775 observations. The daily data, their returns and the corresponding autocorrelation functions are depicted in Figure 1.

5.2 Deseasonalising the data

Before analysing the data, we have deseasonalised the spot prices. Here, we have worked with a geometric model, that is, . Then where, as suggested in, for example, Klüppelberg, Meyer-Brandis and Schmidt [53],

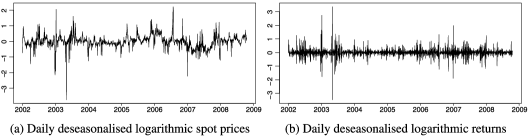

which takes weakly and yearly effects and a linear trend into account. In order to ensure that the spikes do not have a big impact on parameter estimation, we have worked with a robust estimation technique based on iterated reweighted least squares. We have then subtracted the estimated seasonal function from the logarithmic spot prices from the time series and have worked with the deseasonalised data for the remaining part of the Section. Figure 2 depicts the deseasonalised logarithmic prices and the corresponding returns.

5.3 Stationary distribution of the prices

The class of processes is very rich and hence in a first step we checked whether we can restrict it to a smaller class in our empirical work. We have carried out unit root tests, more precisely the augmented Dickey–Fuller test (where the null hypothesis is that a unit root is present in the time series versus the alternative of a stationary time series); we obtained a -value which is smaller than 0.01 and, hence, clearly reject the unit root hypothesis at a high significance level. Also the Phillips–Perron test led to the same conclusion. Hence, in the following, we assume that is an process.

Next, we study the question which distribution describes the stationary distribution of appropriately. We know that in the absence of stochastic volatility an process is a moving average process driven by a Lévy process and hence the integral is itself infinite divisible. We are hence dealing with a stationary infinitely divisible stochastic process, see Rajput and Rosiński [59], Sato [60], Barndorff-Nielsen [3] for more details. The literature on spot price modelling suggest to use semi-heavy and, in some cases, even heavy-tailed distributions in order to account for the extreme spikes in electricity spot prices, see, for example, Klüppelberg, Meyer-Brandis and Schmidt [53] and Benth et al. [25] who suggested to use the stable distribution for modelling electricity returns.

Here we focus on a mixture of a normal distribution in the sense of mean-variance mixtures, see Barndorff-Nielsen, Kent and Sørensen [8]. In particular, we will focus on the generalised hyperbolic (GH) distribution, see Barndorff-Nielsen and Halgreen [7], Barndorff-Nielsen [1], Barndorff-Nielsen [2], which turns out to provide a good fit to the deseasonalised logarithmic spot prices as we will see in the following.

5.3.1 The generalised hyperbolic distribution

A detailed review of the generalised hyperbolic distribution can be found in, for example, McNeil, Frey and Embrechts [56] and details on the corresponding implementation in R based on the ghyp package is provided in Breymann and Lüthi [32].

Let and let denote a -dimensional random vector. is said to have multivariate generalised hyperbolic (GH) distribution if

where , , . Further, is a one-dimensional random variable, independent of and with Generalised Inverse Gaussian (GIG) distribution, that is, . The density of the GIG distribution with parameters is given by

where denotes the modified Bessel function of the third kind, and the parameters have to satisfy one of the following three restrictions

Typically, we refer to as the location parameter, to as the dispersion matrix and to as the symmetry parameter (sometimes also called skewness parameter). The parameters of the GIG distribution determine the shape of the GH distribution. The parametrisation described above is the so-called -parametrisation of the GH distribution. However, for estimation purposes this parametrisation causes an identifiability problem and hence we worked with the so-called -parametrisation in our empirical study. Note that the -parametrisation can be obtained by from -parametrisation by setting

and remain the same, see Breymann and Lüthi [32] for more details.

5.3.2 Estimation results

In our empirical study, we work with the one-dimensional GH distribution. That is, and and are scalars rather than a matrix and vectors, respectively. We have fitted 11 distributions within the GH class to the deseasonalised log-spot prices using quasi-maximum likelihood estimation: The asymmetric and symmetric versions of the

-

•

generalised hyperbolic distribution (GHYP): , (),

-

•

normal inverse Gaussian (NIG) distribution: , (),

-

•

Student- distribution (with degrees of freedom): , (),

-

•

hyperbolic distribution (HYP): , (),

-

•

Variance gamma distribution (VG): , (),

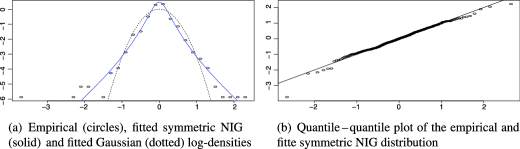

and the Gaussian distribution. We have compared these distributions using the Akaike information criterion, see Table 1, which suggests that the symmetric NIG distribution is the preferred choice for the stationary distribution of the deseasonalised logarithmic spot prices. The diagnostic plots of the empirical and fitted logarithmic densities and the quantile–quantile plots of the fitted symmetric NIG distribution are depicted in Figure 3. We see that the fit is reasonable.

| Model | Symmetric | AIC | Log-Likel. | |||||

|---|---|---|---|---|---|---|---|---|

| NIG | TRUE | 0.395 | 1313.14 | |||||

| GHYP | TRUE | 0.392 | 1314.13 | |||||

| NIG | FALSE | 0.395 | 1315.10 | |||||

| GHYP | FALSE | 0.392 | 1316.10 | |||||

| Student-t | TRUE | 0.458 | 1327.28 | |||||

| Student-t | FALSE | 0.458 | 1329.26 | |||||

| HYP | TRUE | 0.375 | 1331.38 | |||||

| HYP | FALSE | 0.375 | 1333.33 | |||||

| VG | TRUE | 0.379 | 1333.85 | |||||

| VG | FALSE | 0.379 | 1335.42 | |||||

| Gaussian | TRUE | NA | Inf | 0.395 | 1742.94 |

5.4 Stationary processes with generalised hyperbolic marginals

In our empirical study, we have seen that the symmetric normal inverse Gaussian distribution fits the marginal distribution of the deseasonalised logarithmic electricity prices well. Hence, it is natural to ask whether there is a stationary or process with marginal normal inverse Gaussian or, more generally, generalised hyperbolic distribution? The answer is yes, as we will show in the following. Note that the following investigation extends the study of Barndorff-Nielsen and Shephard [13], where the background driving process of an Ornstein–Uhlenbeck process was specified, given a marginal infinitely divisible distribution.

Let us focus on a particular process given by

| (30) |

for constants and for stationary and a standard Brownian motion independent of . {rem*} Note that we have introduced a drift term in the process again in order to derive the general theoretical result. For our empirical example, however, it would be sufficient to set as suggested by our estimation results above. The conditional law of given is normal:

Now suppose that follows an process given by

where is a subordinator. Then, by a stochastic Fubini theorem we find

where , the convolution of and . Similarly,

with . Let denote the gamma density with parameters and , that is,

Now we define

| (31) |

for , which ensures the existence of the integral (30); then we have

Hence, if, for ,

and if, moreover,

we obtain

In other words,

where

We define the subordinator with Lévy measure by . Then

Then one can easily show that the marginal distribution of does not depend on , and the parameter determines the autocorrelation structure of .

It follows that if the subordinator is such that has the generalised inverse Gaussian law then the law of is the generalised hyperbolic .

Is there such a subordinator? The answer is yes. To see this, let and note that is infinitely divisible with kumulant function

On the other hand, the subordinator (here assumed to have no drift) has kumulant function

where is the Lévy measure of . Combining we find

That is, the Lévy measure of is

| (32) |

Thus, the question is: Does there exist a Lévy measure on such that given by (32) is the Lévy measure of the law. That, in fact, is the case since the laws are self-decomposable, cf. Halgreen [48] and Jurek and Vervaat [51].

5.4.1 Implied autocorrelation structure

Next, we focus on the autocorrelation structure implied by the choice of the kernel functions which lead to a marginal GH distribution of the process.

Proposition 0

Let be the process defined in the previous subsection with kernel function as defined in (31). In the case when and , we have

where and denotes the modified Bessel function of the third kind.

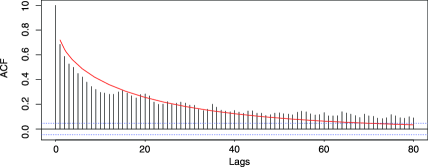

We have estimated the parameters and using a linear least squares estimate based on the empirical and the theoretical autocorrelation function using the first lags. We obtain and . Figure 4 shows the empirical and the corresponding fitted autocorrelation function.

Note that the estimate implies that the corresponding process is not a semimartingale, see, for example, Barndorff-Nielsen and Schmiegel [12] for details. In the context of electricity prices, this does not need to be a concern since the electricity spot price is not tradeable. We observe that the autocorrelation function induced by the gamma-kernel mimics the behaviour of the empirical autocorrelation function adequately. However, it does not fit the first 10 lags as well as, for example, the CARMA-kernel which we have fitted in the following subsection, but performs noticeably better for higher lags. The fit could be further improved by choosing to be a GIG supOU process rather than a GIG OU process. Then one obtains an even more flexible autocorrelation structure.

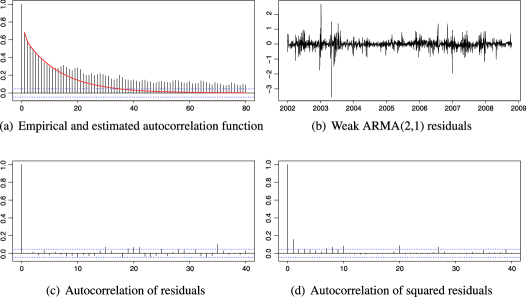

5.5 Empirical performance of a CARMA model

The recent literature on modelling electricity spot prices has advocated the use of linear models, that is, CARMA models, as described in detail in Section 3.1.6. Since CARMA models are special cases of our general modelling framework, we briefly demonstrate their empirical performance as well. It is well known, see, for example, Brockwell, Davis and Yang [36], that a discretely sampled process (for ) has a weak ARMA(, ) representation. An automatic model selection using the Akaike information criterion within the class of (discrete-time ARIMA) models suggests that an ARMA(2,1) model is the best choice for our data. We take that result as an indication that a process (which has a weak ARMA(2,1) representation) might be a good choice. However, it should be noted that the relation between model selection in discrete and continuous time still needs to be explored in detail. We have estimated the parameters of the kernel function which corresponds to a process using quasi-maximum-likelihood estimation based on the weak ARMA(2,1) representation. Diagnostic plots for the estimated model are provided in Figure 5. First, we compare the empirical and the estimated autocorrelation function, see Figure 5(a). Recall that the autocorrelation of is given by (4) and it simplifies to

if either the driving Lévy process has zero mean or if the stochastic volatility process has zero autocorrelation. After deseasonalising (which also includes detrending) the data, we have obtained data which have approximately zero mean.

The empirical and the estimated autocorrelation function implied by a kernel function match very well for the first 12 lags. Higher lags were however slightly better fitted by the gamma kernel used in the previous subsection. Figure 5(b) depicts the corresponding residuals from the weak ARMA(2,1) representation and Figures 5(c) and 5(d) show the autocorrelation functions of the corresponding residuals and squared residuals. Overall, we see that the fit provided by the kernel function is acceptable.

Note that in addition to estimating the parameters of the function coming from a CARMA process one can also recover the driving Lévy process of a CARMA process based on recent findings by Brockwell, Davis and Yang [36]. This will make it possible to also address the question of whether stochastic volatility is needed to model electricity spot prices or not. See Veraart and Veraart [65] for empirical work along those lines in the context of electricity spot prices, whose results suggest that stochastic volatility is indeed important for modelling electricity spot prices.

6 Conclusion

This paper has focused on volatility modulated Lévy-driven Volterra () processes as the building block for modelling energy spot prices. In particular, we have introduced the class of Lévy semistationary () processes as an important subclass of processes, which reflect the stylised facts of empirical energy spot prices well. This modelling framework is built on four principles. First, deseasonalised spot prices can be modelled directly in stationarity to reflect the empirical fact that spot prices are equilibrium prices determined by supply and demand and, hence, tend to mean-revert (in a weak sense) to a long-term mean. Second, stochastic volatility is regarded as a key factor for modelling (energy) spot prices. Third, our new modelling framework allows for the possibility of jumps and extreme spikes. Fourth, we have seen that and, in particular, processes feature great flexibility in terms of modelling the autocorrelation function and the Samuelson effect.

We have demonstrated that processes are highly analytically tractable; we have derived explicit formulae for the energy forward prices based on our new spot price models, and we have shown how the kernel function determines the Samuelson effect in our model. In addition, we have discussed option pricing based on transform-based methods.

An exploratory data analysis on electricity spot prices shows the potential our new approach has and more detailed empirical work is left for future research. Also, we plan to address the question of model estimation and inference. It will be important to study efficient estimation schemes for fully parametric specifications of - and, in particular, -based models.

Appendix: Proofs

Proof of Proposition 6 In order to prove the semimartingale conditions suppose for the moment that is a semimartingale, so that the stochastic differential of exists. Then, calculating formally, we find

which indicates that can be represented, for , as

| (34) |

Clearly, under the conditions formulated in Proposition 6, the above integrals are well defined, and , defined by (15), is a semimartingale, and exists and satisfies equation (Appendix: Proofs). A direct rewrite now shows that (Appendix: Proofs) agrees with the defining equation (2) of , and we can then deduce that is a semimartingale.

Proof of Proposition 7 The result follows directly from the representation (15) and from properties of the quadratic variation process, see, for example, Protter [58].

Proof of Proposition 8 First, write

and observe that the first integral on the right-hand side is -measurable. The result follows by using double conditioning, first with respect to the -algebra generated by the paths of and , and next with respect to .

Proof of Proposition 9 By the Girsanov change of measure, we have

where we set for . By following the argumentation in the proof of Proposition 8, we are led to calculate the expectation

But, by the stochastic Fubini theorem, see, for example, Barndorff-Nielsen and Basse-O’Connor [4],

Using the adaptedness to of the first integral and the independence from of the second, we find the desired result.

Proof of Proposition 10 If it holds that

Similarly, if ,

and affinity holds in both the volatility and the spot price.

Opposite, to have affinity in we must have that

for some function , which means that the ratio is independent of . is differentiable in as long as is. Furthermore, by definition. Thus, by first differentiating with respect to and next letting , it holds that

where we use the notation and for the corresponding partial derivatives with respect to the first argument. Hence, we must have that

and the separation property holds.

Likewise, to have affinity in the volatility , we must have that must be independent of . Denote the ratio by , and differentiate with respect to to obtain

Hence,

for and . Differentiating with respect to , and next letting gives

Whence,

and the separation property holds for . The proposition is proved.

Proof of Proposition 11 Let . From Proposition 9, we have that

for a deterministic function given by

Note that the process is a (local) -martingale for . Moreover, from the stochastic Fubini theorem it holds that

where we note that Hence,

The result is then a direct consequence of the Itô formula for semimartingales, see, for example, Protter [58]. {pf*}Proof of Proposition 12 From Proposition 9, we know that we can write the forward price as

Let now , and suppose that . Recall that , with is the Fourier transform of defined by . Suppose that . Hence, we find

Next, by commuting integration and expectation using dominated convergence and -adaptedness, we obtain

which holds by the stochastic Fubini theorem. Using the independent increment property of and double conditioning, we reach

where we define . Using the stochastic Fubini theorem again, we get

Altogether, we obtain

The above expression can be further simplified by noting that

Then

Proof of Proposition 13 Observe that

We then proceed as in the proof of Proposition 8, and finally we perform the differentiation and let .

Proof of Proposition 14 We have

which is a probability density and hence . Now we derive the explicit formula for the autocorrelation function.

Note that according to Gradshteyn and Ryzhik [46], Formula 3.383.8

for and , where is the modified Bessel function of the third kind. Hence,

Now we apply Gradshteyn and Ryzhik [46], Formula 8.335.1, to obtain

Then

Since according to Gradshteyn and Ryzhik [46], Formula 8.486.16, the result follows.

Acknowledgements

We would like to thank Andreas Basse-O’Connor and Jan Pedersen for helpful discussions and constructive comments. Also, we are a grateful to the valuable comments by two anonymous referees and by the Editor. F.E. Benth is grateful for the financial support from the project “Energy Markets: Modelling, Optimization and Simulation (EMMOS)” funded by the Norwegian Research Council under grant eVita/205328. Financial support by the Center for Research in Econometric Analysis of Time Series, CREATES, funded by the Danish National Research Foundation is gratefully acknowledged by A.E.D. Veraart.

References

- [1] {barticle}[auto:STB—2012/12/11—15:27:38] \bauthor\bsnmBarndorff-Nielsen, \bfnmO. E.\binitsO.E. (\byear1977). \btitleExponentially decreasing distributions for the logarithm of particle size. \bjournalProc. R. Soc. Lond. Ser. A Math. Phys. Sci. \bvolume353 \bpages401–419. \bptokimsref \endbibitem

- [2] {barticle}[mr] \bauthor\bsnmBarndorff-Nielsen, \bfnmO. E.\binitsO.E. (\byear1978). \btitleHyperbolic distributions and distributions on hyperbolae. \bjournalScand. J. Stat. \bvolume5 \bpages151–157. \bidissn=0303-6898, mr=0509451 \bptokimsref \endbibitem

- [3] {barticle}[mr] \bauthor\bsnmBarndorff-Nielsen, \bfnmOle E.\binitsO.E. (\byear2011). \btitleStationary infinitely divisible processes. \bjournalBraz. J. Probab. Stat. \bvolume25 \bpages294–322. \biddoi=10.1214/11-BJPS140, issn=0103-0752, mr=2832888 \bptokimsref \endbibitem

- [4] {barticle}[mr] \bauthor\bsnmBarndorff-Nielsen, \bfnmOle E.\binitsO.E. &\bauthor\bsnmBasse-O’Connor, \bfnmAndreas\binitsA. (\byear2011). \btitleQuasi Ornstein–Uhlenbeck processes. \bjournalBernoulli \bvolume17 \bpages916–941. \biddoi=10.3150/10-BEJ311, issn=1350-7265, mr=2817611 \bptokimsref \endbibitem

- [5] {bmisc}[auto:STB—2012/12/11—15:27:38] \bauthor\bsnmBarndorff-Nielsen, \bfnmO. E.\binitsO.E., \bauthor\bsnmBenth, \bfnmF. E.\binitsF.E. &\bauthor\bsnmVeraart, \bfnmA. E. D.\binitsA.E.D. (\byear2010). \bhowpublishedModelling electricity forward markets by ambit fields. CREATES Research Paper 2010–41, Aarhus Univ. \bptokimsref \endbibitem

- [6] {bincollection}[mr] \bauthor\bsnmBarndorff-Nielsen, \bfnmOle E.\binitsO.E., \bauthor\bsnmBenth, \bfnmFred Espen\binitsF.E. &\bauthor\bsnmVeraart, \bfnmAlmut E. D.\binitsA.E.D. (\byear2011). \btitleAmbit processes and stochastic partial differential equations. In \bbooktitleAdvanced Mathematical Methods for Finance (\beditor\bfnmG.\binitsG. \bsnmDi Nunno &\beditor\bfnmB.\binitsB. \bsnmØksendal, eds.) \bpages35–74. \blocationHeidelberg: \bpublisherSpringer. \biddoi=10.1007/978-3-642-18412-3_2, mr=2752540 \bptokimsref \endbibitem

- [7] {barticle}[mr] \bauthor\bsnmBarndorff-Nielsen, \bfnmO. E.\binitsO.E. &\bauthor\bsnmHalgreen, \bfnmChristian\binitsC. (\byear1977). \btitleInfinite divisibility of the hyperbolic and generalized inverse Gaussian distributions. \bjournalZ. Wahrsch. Verw. Gebiete \bvolume38 \bpages309–311. \bidmr=0436260 \bptokimsref \endbibitem

- [8] {barticle}[mr] \bauthor\bsnmBarndorff-Nielsen, \bfnmO. E.\binitsO.E., \bauthor\bsnmKent, \bfnmJ.\binitsJ. &\bauthor\bsnmSørensen, \bfnmM.\binitsM. (\byear1982). \btitleNormal variance-mean mixtures and distributions. \bjournalInternat. Statist. Rev. \bvolume50 \bpages145–159. \biddoi=10.2307/1402598, issn=0306-7734, mr=0678296 \bptokimsref \endbibitem

- [9] {barticle}[mr] \bauthor\bsnmBarndorff-Nielsen, \bfnmO. E.\binitsO.E. &\bauthor\bsnmSchmiegel, \bfnmJ.\binitsJ. (\byear2004). \btitleSpatio-temporal modeling based on Lévy processes, and its applications to turbulence. \bjournalUspekhi Mat. Nauk \bvolume59 \bpages63–90. \biddoi=10.1070/RM2004v059n01ABEH000701, issn=0042-1316, mr=2068843 \bptokimsref \endbibitem

- [10] {bincollection}[mr] \bauthor\bsnmBarndorff-Nielsen, \bfnmOle E.\binitsO.E. &\bauthor\bsnmSchmiegel, \bfnmJürgen\binitsJ. (\byear2007). \btitleAmbit processes: With applications to turbulence and tumour growth. In \bbooktitleStochastic Analysis and Applications, (\beditor\bfnmF. E.\binitsF.E. \bsnmBenth, \beditor\bfnmG.\binitsG. \bsnmDi Nunno, \beditor\bfnmT.\binitsT. \bsnmLindstrøm, \beditor\bfnmB.\binitsB. \bsnmØksendal &\beditor\bfnmT.\binitsT. \bsnmZhang, eds.). \bseriesAbel Symp. \bvolume2 \bpages93–124. \blocationBerlin: \bpublisherSpringer. \biddoi=10.1007/978-3-540-70847-6_5, mr=2397785 \bptokimsref \endbibitem

- [11] {bincollection}[mr] \bauthor\bsnmBarndorff-Nielsen, \bfnmOle E.\binitsO.E. &\bauthor\bsnmSchmiegel, \bfnmJürgen\binitsJ. (\byear2008). \btitleTime change, volatility, and turbulence. In \bbooktitleMathematical Control Theory and Finance (\beditor\bfnmA.\binitsA. \bsnmSarychev, \beditor\bfnmA.\binitsA. \bsnmShiryaev, \beditor\bfnmM.\binitsM. \bsnmGuerra &\beditor\bfnmM.\binitsM. \bsnmGrossinho, eds.) \bpages29–53. \blocationBerlin: \bpublisherSpringer. \biddoi=10.1007/978-3-540-69532-5_3, mr=2484103 \bptokimsref \endbibitem

- [12] {bincollection}[mr] \bauthor\bsnmBarndorff-Nielsen, \bfnmOle E.\binitsO.E. &\bauthor\bsnmSchmiegel, \bfnmJürgen\binitsJ. (\byear2009). \btitleBrownian semistationary processes and volatility/intermittency. In \bbooktitleAdvanced Financial Modelling, (\beditor\bfnmH.\binitsH. \bsnmAlbrecher, \beditor\bfnmW.\binitsW. \bsnmRungaldier &\beditor\bfnmW.\binitsW. \bsnmSchachermeyer, eds.). \bseriesRadon Ser. Comput. Appl. Math. \bvolume8 \bpages1–25. \bpublisherWalter de Gruyter, Berlin. \biddoi=10.1515/9783110213140.1, mr=2648456 \bptokimsref \endbibitem

- [13] {barticle}[mr] \bauthor\bsnmBarndorff-Nielsen, \bfnmOle E.\binitsO.E. &\bauthor\bsnmShephard, \bfnmNeil\binitsN. (\byear2001). \btitleNon-Gaussian Ornstein–Uhlenbeck-based models and some of their uses in financial economics. \bjournalJ. R. Stat. Soc. Ser. B Stat. Methodol. \bvolume63 \bpages167–241. \biddoi=10.1111/1467-9868.00282, issn=1369-7412, mr=1841412 \bptnotecheck related\bptokimsref \endbibitem

- [14] {bbook}[mr] \bauthor\bsnmBarndorff-Nielsen, \bfnmOle E.\binitsO.E. &\bauthor\bsnmShiryaev, \bfnmAlbert\binitsA. (\byear2010). \btitleChange of Time and Change of Measure. \bseriesAdvanced Series on Statistical Science and Applied Probability \bvolume13. \blocationHackensack, NJ: \bpublisherWorld Scientific Co. Pte. Ltd. \bidmr=2779876 \bptokimsref \endbibitem

- [15] {barticle}[mr] \bauthor\bsnmBarndorff-Nielsen, \bfnmOle Eiler\binitsO.E. &\bauthor\bsnmStelzer, \bfnmRobert\binitsR. (\byear2011). \btitleMultivariate supOU processes. \bjournalAnn. Appl. Probab. \bvolume21 \bpages140–182. \biddoi=10.1214/10-AAP690, issn=1050-5164, mr=2759198 \bptokimsref \endbibitem

- [16] {bmisc}[auto:STB—2012/12/11—15:27:38] \bauthor\bsnmBarndorff-Nielsen, \bfnmO. E.\binitsO.E. &\bauthor\bsnmStelzer, \bfnmR.\binitsR. (\byear2013). \bhowpublishedThe multivariate SupOU stochastic volatility model. Math. Finance 23 257–296. \bptokimsref \endbibitem

- [17] {bmisc}[auto:STB—2012/12/11—15:27:38] \bauthor\bsnmBarndorff-Nielsen, \bfnmO. E.\binitsO.E. &\bauthor\bsnmVeraart, \bfnmA. E. D.\binitsA.E.D. (\byear2012). \bhowpublishedStochastic volatility of volatility and variance risk premia. Journal of Financial Econometrics 11 1–46. \bptokimsref \endbibitem

- [18] {barticle}[mr] \bauthor\bsnmBasse, \bfnmAndreas\binitsA. (\byear2008). \btitleGaussian moving averages and semimartingales. \bjournalElectron. J. Probab. \bvolume13 \bpages1140–1165. \biddoi=10.1214/EJP.v13-526, issn=1083-6489, mr=2424990 \bptokimsref \endbibitem

- [19] {barticle}[mr] \bauthor\bsnmBasse, \bfnmAndreas\binitsA. &\bauthor\bsnmPedersen, \bfnmJan\binitsJ. (\byear2009). \btitleLévy driven moving averages and semimartingales. \bjournalStochastic Process. Appl. \bvolume119 \bpages2970–2991. \biddoi=10.1016/j.spa.2009.03.007, issn=0304-4149, mr=2554035 \bptokimsref \endbibitem

- [20] {bmisc}[mr] \bauthor\bsnmBasse-O’Connor, \bfnmAndreas\binitsA., \bauthor\bsnmGraversen, \bfnmSvend-Erik\binitsS.E. &\bauthor\bsnmPedersen, \bfnmJan\binitsJ. (\byear2013). \bhowpublishedStochastic integration on the real line. Theory Probab. Appl. To appear. \bptokimsref \endbibitem

- [21] {barticle}[mr] \bauthor\bsnmBender, \bfnmChristian\binitsC. &\bauthor\bsnmMarquardt, \bfnmTina\binitsT. (\byear2009). \btitleIntegrating volatility clustering into exponential Lévy models. \bjournalJ. Appl. Probab. \bvolume46 \bpages609–628. \biddoi=10.1239/jap/1253279842, issn=0021-9002, mr=2560892 \bptokimsref \endbibitem

- [22] {barticle}[mr] \bauthor\bsnmBenth, \bfnmFred Espen\binitsF.E. (\byear2011). \btitleThe stochastic volatility model of Barndorff–Nielsen and Shephard in commodity markets. \bjournalMath. Finance \bvolume21 \bpages595–625. \biddoi=10.1111/j.1467-9965.2010.00445.x, issn=0960-1627, mr=2838577 \bptokimsref \endbibitem

- [23] {bincollection}[mr] \bauthor\bsnmBenth, \bfnmFred Espen\binitsF.E., \bauthor\bsnmHärdle, \bfnmWolfgang Karl\binitsW.K. &\bauthor\bsnmLópez Cabrera, \bfnmBrenda\binitsB. (\byear2011). \btitlePricing of Asian temperature risk. In \bbooktitleStatistical Tools for Finance and Insurance (\beditor\bfnmP.\binitsP. \bsnmCivek, \beditor\bfnmW.\binitsW. \bsnmHärdle &\beditor\bfnmR.\binitsR. \bsnmWeron, eds.) \bpages163–199. \blocationHeidelberg: \bpublisherSpringer. \biddoi=10.1007/978-3-642-18062-0_5, mr=2856922 \bptokimsref \endbibitem

- [24] {barticle}[mr] \bauthor\bsnmBenth, \bfnmFred Espen\binitsF.E., \bauthor\bsnmKallsen, \bfnmJan\binitsJ. &\bauthor\bsnmMeyer-Brandis, \bfnmThilo\binitsT. (\byear2007). \btitleA non-Gaussian Ornstein–Uhlenbeck process for electricity spot price modeling and derivatives pricing. \bjournalAppl. Math. Finance \bvolume14 \bpages153–169. \biddoi=10.1080/13504860600725031, issn=1350-486X, mr=2323278 \bptokimsref \endbibitem

- [25] {bmisc}[auto:STB—2012/12/11—15:27:38] \bauthor\bsnmBenth, \bfnmF. E.\binitsF.E., \bauthor\bsnmKlüppelberg, \bfnmC.\binitsC., \bauthor\bsnmMüller, \bfnmG.\binitsG. &\bauthor\bsnmVos, \bfnmL.\binitsL. (\byear2012). \bhowpublishedForward pricing in electricity markets based on stable CARMA spot models. Unpublished manuscript. \bptokimsref \endbibitem

- [26] {bmisc}[auto:STB—2012/12/11—15:27:38] \bauthor\bsnmBenth, \bfnmF. E.\binitsF.E. &\bauthor\bsnmVos, \bfnmL.\binitsL. (\byear2013). \bhowpublishedCross-commodity spot price modeling with stochastic volatility and leverage for energy markets. Adv. in Appl. Probab. To appear. \bptokimsref \endbibitem

- [27] {barticle}[auto:STB—2012/12/11—15:27:38] \bauthor\bsnmBenth, \bfnmF. E.\binitsF.E. &\bauthor\bsnmŠaltytė Benth, \bfnmJ.\binitsJ. (\byear2004). \btitleThe normal inverse Gaussian distribution and spot price modelling in energy markets. \bjournalInt. J. Theor. Appl. Finance \bvolume7 \bpages177–192. \bptokimsref \endbibitem

- [28] {barticle}[auto:STB—2012/12/11—15:27:38] \bauthor\bsnmBenth, \bfnmF. E.\binitsF.E. &\bauthor\bsnmŠaltytė Benth, \bfnmJ.\binitsJ. (\byear2009). \btitleDynamic pricing of wind futures. \bjournalEnergy Economics \bvolume31 \bpages16–24. \bptokimsref \endbibitem

- [29] {bbook}[auto:STB—2012/12/11—15:27:38] \bauthor\bsnmBenth, \bfnmF. E.\binitsF.E., \bauthor\bsnmŠaltytė Benth, \bfnmJ.\binitsJ. &\bauthor\bsnmKoekebakker, \bfnmS.\binitsS. (\byear2008). \btitleStochastic Modelling of Electricity and Related Markets. \bseriesAdvanced Series on Statistical Science and Applied Probability \bvolume11. \blocationSingapore: \bpublisherWorld Scientific. \bptokimsref \endbibitem

- [30] {barticle}[mr] \bauthor\bsnmBenth, \bfnmFred Espen\binitsF.E., \bauthor\bsnmŠaltytė Benth, \bfnmJūratė\binitsJ. &\bauthor\bsnmKoekebakker, \bfnmSteen\binitsS. (\byear2007). \btitlePutting a price on temperature. \bjournalScand. J. Stat. \bvolume34 \bpages746–767. \biddoi=10.1111/j.1467-9469.2007.00564.x, issn=0303-6898, mr=2396937 \bptokimsref \endbibitem