Option pricing with non-Gaussian scaling and infinite-state switching volatility

Abstract: Volatility clustering, long-range dependence, and non-Gaussian scaling are stylized facts of financial assets dynamics. They are ignored in the Black & Scholes framework, but have a relevant impact on the pricing of options written on financial assets. Using a recent model for market dynamics which adequately captures the above stylized facts, we derive closed form equations for option pricing, obtaining the Black & Scholes as a special case. By applying our pricing equations to a major equity index option dataset, we show that inclusion of stylized features in financial modeling moves derivative prices about closer to the market values without the need of calibrating models parameters on available derivative prices.

Keywords: option pricing; anomalous scaling; Markov switching; GARCH

JEL Classifications: C58; G13; C22; C51; C52; C53

1 Introduction

Dynamical properties and stylized facts of financial time series have raised considerable interest in both theoretical and applied econometrics. Within these fields, one topic widely discussed is related to the memory properties observed over return sequences, in particular regarding their absolute value (volatility). A variety of techniques have been developed to include realistic volatility dynamic features into a continuous time model, thus improving the geometric Brownian motion assumption underlying the classic Black-Scholes (BS) model. We mention, among many others, the stochastic volatility, see, e.g., Fouque et al. (2000) and therein cited references, the and GARCH-based approach of Heston (1993), and Heston and Nandi (2000). In what follows, volatility memory properties, and in particular the long-memory behaviour, are taken into account on the basis of the “scaling symmetry” concept, that has a long tradition in statistical mechanics and in the physics of complex systems. Our main purpose is to discuss the impact of memory and scaling properties on the price of financial derivatives, and to compare them with those coming from the BS framework.

Long-memory behaviour has been often associated with the evaluation of the Hurst exponent, , introduced in the seminal work of Hurst (1951). The Hurst exponent links the time series fluctuations with the time scale over which they are observed. Indeed, in the presence of a simple scaling symmetry for a stochastic process () supposed to generate the time series of interest, the th order moment satisfies , where defines the time scale at which the terms of the series are aggregated and is an amplitude. This follows from the fact that the probability density function of satisfies the scaling identity, , where is the scaling function and is also called scaling exponent. Well-studied forms of scaling were first observed in the study of critical phenomena, as in a critical magnetic system, see (see, e.g., Sethna et al. (2001), and therein cited references, or disordered systems, see Bouchaud and Georges (1990). Indeed, if the elements of a time series are extracted independently from a Gaussian probability density function, the Hurst exponent has a value equal to . In several empirical studies, deviations from this reference behaviour have been observed, and are referred to as forms of “anomalous scaling”. These deviations are generally considered a consequence of long-memory effects.111However, we point out that, strictly speaking, an anomalous Hurst exponent is not necessarily a consequence to the existence of long-memory, Cont (2005). It is important to point out that anomalous scaling conditions can also arise in cases in which the scaling exponent is equal to , whenever is not Gaussian. Finally, a more general form of anomalous scaling called “multiscaling” is associated with those cases in which the scaling exponent depends on the moment order . If multiscaling is present, the scaling or Hurst exponent can be expressed as a function of the moment order, leading to . Non-Gaussian scaling plays a central role in the present study, where an interesting case is made for the existence of multiscaling associated with long-memory behaviour of financial data.

A seminal contribution linking scaling properties to the financial framework was made by Mandelbrot (1963). Further studies appeared only at the beginning of the ’90s, mainly starting with the newly available high frequency data on currencies. We cite, among others, Muller et al. (1990), Dacorogna et al. (1993, 2001), and Guillaume et al. (1997). Subsequently, additional works analysed the scaling properties of financial assets other than currencies such as bonds (Ballocchi et al. 1999) and equities (Di Matteo et al. 2005). Finally, scaling properties of financial data have been also analysed from an econo-physics point of view (see Mantegna and Stanley 1995, Ghashghaie et al. 1996, and Stanley and Plerou 2001), establishing a connection with the physics of critical phenomena.

The presence of non-Gaussian or anomalous scaling in financial log-return time series introduces a relevant challenge for practitioners, in particular when their purpose is the determination of a derivative contract price. As a matter of fact, the dynamics of underlying prices assumed in the BS framework is well known to be not consistent with the scaling properties of equity indices. This is a source of derivative pricing inefficiencies.

Rather than relying on concepts like implied volatility to correct the BS framework, our aim here is an evaluation of the effects on pricing of a substantial improvement of the model describing the dynamics of the underlying asset, while maintaining a link with the BS formalism. The main contribution of the present paper is the derivation of closed-form formulae for option pricing and associated hedging strategy, based on an equivalent martingale measure. This is obtained by means of a model recently introduced in statistical mechanics by Zamparo et al. (2013) whose advantage is to be consistent with the observed features of financial data, thus including non-Gaussian scaling behaviour. The general results provided here include as a special case the BS pricing formula. Although we rely on a Monte Carlo computation to evaluate probabilities related to the underlying dynamics, these formulae define a priori the option price and the associated strategy, conditioned on the previously observed values of the underlying asset’s returns. Also, we differ from the stochastic volatility pricing approaches (see, e.g., Fouque et al. 2000, or Heston, 1993) since our formulae are closed in the sense that the pricing parameters are directly inferred from the underlying model dynamics and do not need any calibration with respect to known derivatives’ market prices. Indeed, an empirical application shows that compared with BS the proposed approach determines a price sensibly closer to the market one. We postpone to future works the derivation of Greeks and the use of our pricing approach within option trading strategies.

The paper proceeds as follows: Section 2 introduces the stochastic process for the underlying risky asset; Section 3 reports the novel approach for option pricing based on the model presented in Section 2; an empirical analysis is outlined in Section 4 and Section 5 concludes. Proofs are reported in the Appendix.

2 Non-Gaussian scaling in financial data

We consider the dynamics of a financial asset or index whose value at time is denoted by , , while its log-returns are given as . The existence of non-Gaussian scaling properties may be associated with different effects, including various kind of data seasonality, see Dacorogna et al. (1993), among others, or long-range dependencies. The latter have been extensively studied in statistics (Beran, 1994), econometrics (Robinson, 2003), and finance by the pioneering work of Lo (1991). For financial time series, and for time scales ranging from minutes to months, significant deviations from Gaussianity of the scaling function have been observed; see Cont (2001), among others. Moreover, whereas a scaling exponent is observed for , multiscaling behaviour with -dependent is often observed for higher-order moments (see, e.g., Di Matteo et al., 2005).

Following the original suggestion by Baldovin and Stella (2007), Zamparo et al. (2013) assume the anomalous scaling symmetry of the density for the aggregated returns. Taking this as a guiding criterion, they propose stochastic processes whose realizations are able to replicate the long-range dependence and non-Gaussianity typical of a financial time series. At the same time, the use of scaling symmetry leads to processes which are relatively easy to manipulate for both calibration purposes and analytical calculations. High frequency models based on the same criterion were already proposed in Baldovin et al. (2011) and adopted for trading strategies in Baldovin et al. (2014).

While referring to the original publication (Zamparo et al. 2013) for motivations and details of the model construction, we give here the basic definitions of the process used then in a derivative pricing framework. In the proposed structure, two independent stochastic components affect the asset returns’ dynamical evolution. The first one, is a fully endogenous process called , dependent on the past asset history through an auto-regressive scheme of order . Once the memory range is established,222The memory range can be fixed according to the data frequency, or with respect the objective of the researcher. With daily data, one might take , that is one month, given it is a sufficient range to approximate a truly long-memory process as shown in Corsi (2009). Alternatively, one could set , close to three months, to provide a better approximation. the conditional probability density function of only depends on the previous values of , as can be deduced by the following definitions for its joint probability density :

| (1) |

if , and

| (2) |

if . The probability densities (for simplicity, we now suppress the first index) are assumed to be Gaussian mixtures:

| (3) |

where is a Gaussian with volatility and , with . The defined in (3) allows recovering proper empirical scaling properties while fat tailed densities for lead to fat tailed marginal distributions for the (Zamparo et al. 2013). Notably, the process defined in this way is similar to an ARCH process of order , with the difference that is in general heterodistributed in place of just heteroskedastic. Indeed, not only the variance, as in ordinary ARCH schemes, but also the form of the conditional PDF of depends on the previous values . Specific choices for the density give the advantage of enabling the explicit integration over . This is what happens, for instance, when choosing to be distributed according to an inverse-Gamma density. The density is then associated with a “shape parameter” and a “scale parameter” , according to

| (4) |

Upon explicit integration over , the endogenous component becomes in this case a genuine ARCH process (see Zamparo et al., 2013) described by

| (5) |

where the return residual process is given as a sequence of independent Student’s t-distributed variables:

| (6) |

with . 333Zamparo et al. (2013) also show that is a strictly stationary process. For a general overview of covariance and strict stationarity in GARCH processes, see Francq and Zakoian (2010).. Below, we will assume the previous form for , since a number of analytical results can be obtained in closed form, see Zamparo et al. (2013). For any memory order , the endogenous component is thus specified by two parameters only: , determining the form of the distributions; identifying the scale of the process. The parsimonious number of parameters, independent of the memory order, is a further advantage coming from the implementation of the scaling symmetry.

The second component describing the model is partly exogenous and partly endogenous and is introduced as a modulation of the process :

| (7) |

where the component is defined as

| (8) |

with a suitable parameter. The process is a Markov chain in , defined by

| (9) |

and

| (10) |

being the Kronecker delta. Thus, the definition of this latter component involves two additional parameters: and . The quantity is the average interval between two random external inputs, where each input event restarts from the sequence of integers , thus re-setting to (for this reason we will call “restarts” these inputs which could be either endogenous or exogenous). The exponent in (8) regulates how fast the restart is absorbed by market dynamics. In particular, corresponds to the case in which the restart produces a volatility burst due to some external input that then decays in time. The component determines the generalized Hurst exponent associated with the model, which is influenced by both and , and conveys realistic time properties to the volatility autocorrelation function. Since the process multiplies , it can be regarded as a Markov process switching the value of the volatility. In such a way, the combination of the two components becomes a Markov-SWitching ARCH (SWARCH) process. Differently from the proposal of Hamilton and Susmel (1994), the process assumes values in and implies that the switching process is endowed with an infinite number of states.

One can prove that the composed process is stationary, ergodic, and displays realistic multiscaling and volatility autocorrelations if properly calibrated on reasonably long daily returns series (Zamparo et al. 2013). The estimation of model parameters is performed by matching various moments of the model’s distributions. The model parameters are in total, . Since represents a lower limit for the range up to which memory effects are supposed to be properly taken into account by the model, one can fix this parameter in relation with the time scale relevant for the application of interest. For instance, in the present work we consider , corresponding to a month of market activity, and coherently with the common practice adopted for modeling realized volatility sequences, see Corsi (2009).

3 Pricing with non-Gaussian scaling

One of the basic features of the BS model (Black and Scholes, 1973; Merton, 1973; see also Hull, 2000, and references therein) is that it derives a closed formula for the value of, say, a European call option depending only on two free parameters: the risk-free interest rate and the volatility of the underlying asset . In principle, these parameters can be identified a priori on the basis of historical data. However, in view of the unrealistic assumption of memoryless Gaussian returns, financial practitioners are forced to correct the BS option value at different strike prices with appropriately chosen different values of . This allows compensating for volatility changes and for the so-called “smile effect” observed in the implicit volatility of the real-market option value. From a logical perspective, however, a model for determining “derivative prices” should not rely on “market derivative prices”, the latter being what determines the implicit volatility. Instead, derivative prices should be identified by a proper rational price (obtained, e.g., through an equivalent martingale measure) and an efficient hedging strategy associated with the stochastic dynamics of the underlying asset (i.e., with the “physical probability”).

Many models have been proposed to overcome the BS limitations. Among others, we cite Heston (1993), Heston and Nandi (2000), Borland and Bouchaud (2004) and Christoffersen et al. (2006). On the one hand, approaches like those using continuous-time stochastic-volatility models are capable of defining a priori formulae for option prices and associated hedging strategies that reproduce the volatility smile. However, they still need to be calibrated on some real-market derivative prices in order to determine the price of other ones. On the other hand, pricing methods relying entirely on the underlying asset’s dynamics typically do not provide explicit formulae. As a consequence, they require the use of Monte Carlo approaches that simulate many possible asset’s trajectories to identify efficient hedging strategies and the derivative prices (see Bouchaud and Potters, 2003).

In view of the fact that the model for the underlying log-returns presented in the previous section generalizes Gaussian dynamics, we wish here to follow a different approach, which aims at deriving closed expressions for derivative prices and associated hedging strategies generalizing those of BS to this more complex situation. If, consistently with the spirit of our model, one assumes that the dynamical evolution of the primary asset’s returns could be described as a mixture of Gaussian processes, a natural way of pricing an option and finding a hedging strategy is by averaging the BS formula through the Gaussian mixture density (see, e.g., Peirano and Challet, 2012). Our basic idea is then to find the Gaussian mixture density that most effectively reproduces the underlying asset’s dynamics, given the historical conditions observed at the moment the derivative contract is written. Additional effort must then be made in order to properly take into account time restarts that may occur either before the contract stipulation or between the writing and the maturity of the contract. Through this approach we will prove that, indeed, we are defining an equivalent martingale price. In section 4 we will then show that for S&P500 options, prices calculated on the basis of the anomalous scaling dynamics are closer to market prices than BS ones by about 30% on average (see table 4 in section 4). We stress that such an evaluation is performed by comparing models performances on a common playground, without thus correcting the BS volatility across option maturity and/or strike prices. Adjustments on the BS inputs would favour the BS model being closer to the observed prices, thus producing a biased evaluation of the impact of non-Gaussian scaling on the option prices. An assessment of the efficacy of the hedging strategy is instead left to future work.

3.1 Closed-form option pricing formulae

We first point out that, in accordance with the model outlined in Section 2 for the underlying asset dynamics, our derivation of option prices assumes discrete time. The market includes a riskless bond evolving at rate according to and a stock described through its returns and mean return rate , such that , where is the asset value at time . We denote by the “physical probability measure” associated with the returns , as described in section 2, and by the -algebra generated by , with . is adapted to the filtration . The market is assumed free of arbitrage, liquid, with no transaction costs, no interest spread, no dividends, and with unlimited short selling for an unlimited period of time.

Notice that by choosing and for all (e.g., with ), our model degenerates into a discrete-time version of the geometric Brownian motion for , without memory effects or volatility bursts. Our basic pricing strategy is then to define a general equivalent martingale measure which reproduces (in discrete time) the BS formula in the above degenerate conditions. We aim first at obtaining equivalent martingale measures for general (arbitrary) choices of the parameters and , that will thus be valid even if they become random variables. In the next subsections, we will identify the most appropriate distributions for and conditioned to the past dynamics of .

Let be the joint density of in the range and the volatility density conditional to some past values for and . The following Lemma introduces the martingale measures equivalent to used later for option pricing.

Lemma 1. Consider the function

| (11) |

with and . Given , for the probability density function444 Since we need now to explicitly indicate the time partition to which a probability density function is referred to, we slightly change the notation with respect to Section 2. In the case of a conditional probability density function, we will explicitly indicate the conditioning values among the arguments after the usual vertical bar, .

| (12) |

defines an equivalent martingale measure .

More generally, for any

given parameters distributions and

, also the probability density function

| (13) |

defines an equivalent martingale measure .

The price at time of a European call option with maturity at time and strike price satisfies where is the option pay-off at maturity (see, e.g., Föllmer et al., 2011). The conditional expectation is taken with respect to the -algebra since we assume that while computing the price , valid at time , we still do not know the value of the return . The following theorem provides the option price.

Theorem 1. Given the equivalent martingale measure defined in Lemma 1, the call price conditioned by the values and is

| (14) |

where is the standard normal cumulative distribution function, and

| (15) |

| (16) |

More generally, given the equivalent martingale measure , defined in Lemma 1, the call price is

| (17) |

By assuming and for any , all equivalent martingale measures coincide with each other, (16) simplifies into , and the call price obtained in (17) equals the standard BS formula. Although not explicitly addressed in the present paper, we highlight that, by means of (14) and (17), one also obtains Delta-hedging formulas which generalize BS’ one. Namely, and

| (18) |

So far, and are generic distributions for the parameters and . In the next subsections, we will link these parameters to the dynamics characterizing the evolution of . This will also motivate the dependence of the distribution of on the ’s for and on the ’s for . Moreover, we will propose for a Gaussian mixture density representing both the “state of the market” summarized in the returns previous to the derivative contract pricing day, and the possible future evolutions of the market up to the maturity time. Since our model contains the hidden component , in order to calculate it is also needed to include a dependence on the random time both before the contract pricing day and between the pricing day and the maturity of the contract. The density will then identify the probability of the random time string . Those two elements are fundamental for the evaluation of (17), our main result for derivative pricing. The evaluation of (17) will be discussed in a following subsection (3.4).

3.2 Identification of

Within this subsection, the sequence is assumed to be given. At the time at which we wish to price a European option expiring at time , the “state of the market” for the underlying asset is characterized by the historical values . Indeed, since , the assumed knowledge of means that we can identify also as . We aim at finding an approximation for the probability density function , so that the pricing scheme in Section 3.1 could be applied. We propose to approximate as a Gaussian mixture with mixing density :

| (19) |

In such a way, the returns’ dynamic can be viewed as a superposition of Gaussian processes with a fixed (although stochastic) volatility . Consistently, the mixture density so identified enters in (17) to determine the option price. The approximation is realized by matching the expected fluctuation of the return from to calculated through with that obtained using .

Theorem 2. Consider the cumulated return from to , . If

| (20) |

with

| (21) |

| (22) |

then the expected value of coincides for and : .

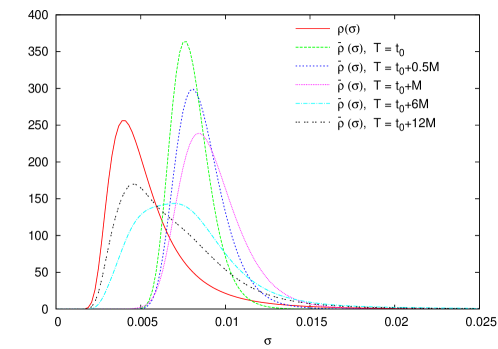

As shown in Fig. 1, the distribution is peaked around the present value of the volatility if the maturity is very close to , whereas it becomes if . For , also degenerates to a delta, . In practice, can be evaluated by simulating the process conditionally to past values and given . In the Appendix we give an explicit expression for when is parametrized as in (4). For the empirical application in Section 4, for each couple , the distribution has been evaluated averaging over different simulated realizations.555We verified by simulations that realizations are sufficient to obtain convergence of the distribution.

3.3 Identification of

Here we specify a numerical scheme which enables the extraction of the random time string and of their associated probability , according to the model’s dynamic and the historical information available at time . This is instrumental to the evaluation of the option price as discussed in the following subsection. Given that the process is not directly identifiable, and given its Markovian nature, we have that the probability of the string depends on the whole historical time series . This prevents the direct evaluation/estimation of the density. To solve this problem we propose a Monte Carlo procedure which relies on local information only, within a window whose size is taken to be , to facilitate notations. Numerical constraints limit the value of to some units, as specified in what follows. More precisely, we present a numerical method to calculate the probability .

It is convenient to distinguish between the distribution of the stochastic variables before the pricing time and the distribution of from to . Since the random time process is a Markov chain, we have

| (23) |

Before , one can exploit the local information contained in the historical returns. In details, we suggest considering

| (24) |

where the approximation comes from to the fact that on the r.h.s. of the equation only local information is considered. The appendix shows explicit expressions for the r.h.s. of (3.3); using these expressions, a Monte Carlo procedure can extract the string according to our approximation of the probability .

From to , according to (10) we simply have

| (25) |

3.4 The evaluation of the option price

Since we have now specified in (20), and in (3.3), (3.3), and (25), the option price can be computed according to (17), which however contains multiple series with infinite terms. To evaluate these series with respect to the past of , we propose the use of a Monte Carlo method. We suggest calculating the option price as the weighted average on a number of histories extracted with probability . In addition, to reduce the computational complexity, in the range from to , we restrict the sums in (17) on all possible realizations with at most two restarts occurring in the interval . Despite the apparent strong assumption, we highlight that this corresponds to a second order approximation of the option price with respect to , which is indeed a small parameter. In addition, unreported tests with a third order approximation in (at most three restarts in ) provided negligible changes.

Numerical tests suggest that a local window with in (3.3) is enough to implement an appropriate Monte Carlo sampling. In the empirical application outlined in Section 4, the Monte Carlo scheme has been realized by sampling Monte Carlo realizations, with since is sharply peaked.666Higher values of do not sensibly affect the option prices. Given a Monte Carlo realization with and given the random time sequence , we can indicate the associated option price as

| (26) |

Therefore, we denote with the option price in the above expression when no restarts occur between and , while is the option price in the above expression when only a single restart occurs between and at time . Finally, is the option price in the above expression when only two restarts occur between and at time and . Using those three elements, the final explicit expression for the option price becomes

| (27) |

where is the normalization constant

| (28) |

In (27), the probability of the random time sequence past to , , has been replaced by a sum over the Monte Carlo realizations, since the ’s are extracted according to , whereas the probability of the random time sequence beyond , , has been explicitly calculated at second order in .

Summarizing, the numerical evaluation of the option price includes the following steps: (i) Given the historical information, extract the past random time sequence ’s through the Monte Carlo algorithm; (ii) Consider then a possible future random time sequence with zero, one or at most two restarts between and ; (iii) Evaluate as described in subsection 3.2; (iv) Calculate a partial option price using (26); (v) Take the average across sequences described in (i) and (ii) using, (27). In terms of CPU time-consumption, points (i) and (iii) are the bottlenecks in the implementation of this algorithm, and are independent of the strike price .

We close this section, by noting that the stochastic process previously introduced and the associated option pricing approach allow generating asset returns and option prices characterized by a volatility smile effect, as we will show in the next section.

4 Empirical application

4.1 Options database

We now compare the pricing approach previously introduced and the standard BS model with market prices for options on the S&P500 index as recovered from Datastream. We consider European call options with maturity between June 2007 and May 2013, and for those contracts we download the prices available from January 2007 up to May 2012.777We consider options with maturity in the twelve months following the reference download date, the 31 May 2012. The S&P500 index options have already been used in several studies dealing with option pricing, see Bakshi et al. (1997), Ait-Sahalia and Lo (1998), Dumas et al. (1998), Chernov and Ghysels (2000), Heston and Nandi (2000) and Christoffersen et al. (2006), among others. Similarly to Christoffersen et al. (2006), we evaluate the pricing performances both in-sample and out-of-sample.888The present paper reports out-of-sample pricing results only. In-sample results are available from the authors upon request. We fix the in-sample to the range starting in January 2007 and ending at December 2010. The remainder period, January 2011 to May 2012, is used as out-of-sample. The Appendix reports additional details on the database and the filters applied to the option prices, following Bakshi et al. (1997), Dumas et al. (1998), Ait-Sahalia and Lo (1998), Bakshi et al. (2000), Christoffersen and Jacobs (2004) and Christoffersen et al. (2006). Table (1) reports the number of option contracts, the average option price, and the average implied volatility from the BS model, distinguishing on the basis of the moneyness (computed as the ratio between the equity index level and the option strike price) and time to maturity. Excluding the extreme moneyness classes (below 0.5 and above 2.5), we observe the presence of a volatility smile effect, with implied volatility differing across strike prices, and characterized by some asymmetry. In fact, call options highly in-the-money have higher implied volatility compared to out-of-the money call options. Notably, the options’ implied volatility is extremely high, in many cases well above 100%. This is related to the peculiar features of the time range analysed in the current paper, which is characterised by very high volatility.999Similar evidences are provided for the in-sample period.

In comparing our approach to the BS model, option prices are filtered from the dividends effects, as in Bakshi et al. (1997), Ait-Sahalia and Lo (1998) and Christoffersen et al. (2006). In addition, the risk-free rate is proxied by a set of interbank rates, at 1, 3, 6 and 12 months, recovered from Thomson Datastream, and matched with the options maturity; see the Appendix for details.

4.2 Scaling and persistence in the S&P500 index

The pricing of call options starts from the estimation of the model outlined in section 2. We use a time-series length of five years to determine the model parameters , and, for computational simplicity, we impose a grid over the model parameters with precision for , for and for .101010Parameters have been estimated with a minimum-distance-type estimator, see Zamparo et al. (2013), for additional details.

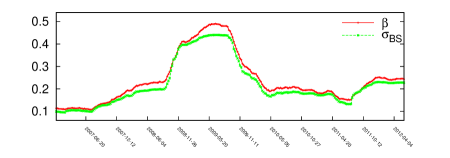

For the in-sample period, the years 2007-2010, we estimate the model parameters using the S&P500 index in the range 2006-2010 (five years). As previously mentioned, we set and the estimated parameters are . The in-sample parameter shows evidence of some long-range persistence in the second order moment of the daily S&P500 returns. In addition, the shape parameters of the volatility density are quite high. Finally, the parameter suggests that the average time between two restarts, creating a regime change, is equal to about 5000 days.111111We also estimated the model with obtaining . This suggests an interval between regime changes equal to 1250 days. The parameter changes across values of and this might be counter-intuitive as it represents a memory-independent part of the model. This is however an estimation/calibration issue. In fact, as in the estimation step we assume a priori the value of , the estimation of all remaining parameters becomes in fact -dependent. We nevertheless point out that the obtained values for are not much different, and the most relevant outcome is the evidence of having rare regime changes. The scale parameter of the volatility density, , plays a role similar to the volatility parameter in the BS model. In view of a fair comparison with this benchmark model, we estimate these two parameters on the basis of the same sample data. In preliminary evaluations, we have verified that the use of the above in-sample interval, 2006-2010, to determine in the BS formula gives very poor results in comparison with the market option prices. For this reason, and have been both estimated in an out-of-sample framework, using the historical data of one year previous to the pricing day. Using common convention, the volatility of the BS model is defined as the returns’ standard deviation. The last plot of Figure 2 compares the historical evolution of the (for ) and of the BS volatility. We note that the two quantities share a common pattern, a somewhat expected result given the two parameters are evaluated over the same sample. In turn, this highlights that the two models will provide option prices derived from a common playground. This would have not been the case, for instance, if the BS prices were derived by changing the underlying volatility according to the option time to maturity and moneyness. As a consequence, the differences observed in the option prices reported below are due to the different dynamic behaviour of the underlying models.

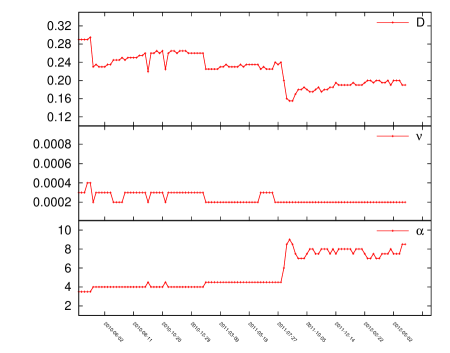

For the out-of-sample evaluation, we estimate the model parameters , and using the five years data prior to the pricing day.121212The appropriate estimation of those parameters requires longer samples compared to the parameter as discussed in Zamparo et. al (2013). As a result, we obtain a sequence of parameters values. The parameter evolution is reported in the first to third plots of Figure 2, while some descriptive quantities are included in Table (2) (in all cases we consider ). We observe that the memory parameter has a decreasing pattern, suggesting a reduction of the persistence of the equity index. The parameter shows evidence of limited oscillations, influenced by the grid used in its evaluation (its value ranges from to ). Finally, the shape parameter has a sharp increase in the last part of the sample.

4.3 Pricing and non-Gaussian scaling

The pricing approach presented in this paper is contrasted to a more traditional BS pricing.

Table (3) reports the out-of-sample pricing outcomes expressed as root mean squared errors (RMSE) between the prices implied by the two models and the observed market prices. The Table shows a preference for the pricing consistent with the scaling property of the S&P500. The BS approach turns out to be preferred for higher levels of moneyness and shorter maturities. The pricing with anomalous scaling and switching volatility gives, overall, smaller pricing errors for moneyness levels up to 1.75, independently of the time to maturity, and for moneyness levels above 1.75, only for options with maturity in more than three months. If we focus solely on the moneyness, the introduction of scaling properties provides pricing errors smaller than those associated with the BS model for most moneyness levels. Differently, if we consider only the time to maturity, the BS pricing gives smaller pricing errors for maturities above three months. Finally, we observe that the largest differences across the two pricing approaches occur for moneyness levels below 1.5 independently of the time to maturity. In those cases, the pricing with anomalous scaling provides smaller RMSE with a sensibly larger frequency.

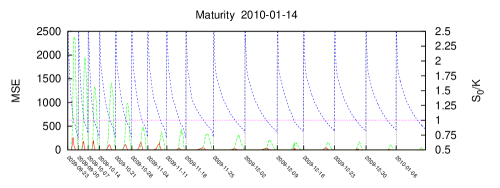

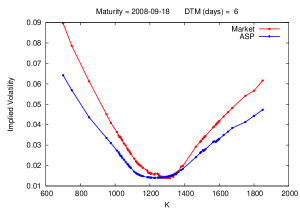

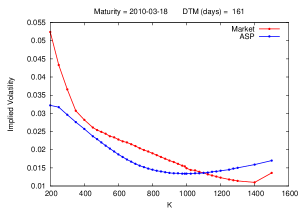

However, as one might expect, those results are given by a combination of cases where the preference for our approach is striking, with cases where the BS pricing is preferred, at least in some dates or for some maturities. We provide an example in Figures 3.131313Additional examples are available upon request. where we report the mean squared error for options with a given maturity for different moneyness levels and different pricing days (the Wednesdays of several consecutive weeks). In many cases we observe that the BS model provides substantially greater pricing errors than those of the anomalous scaling-based prices. Pricing errors might be either increasing or decreasing when approaching time to maturity. Finally, the proposed model provides option prices consistent with a volatility smile effect, as shown for a specific cases in Figure 4.141414Additional examples are available upon request.

5 Conclusions

Self-similarity is a remarkable symmetry linking properties observed at different scales. Whenever a system is (at least approximately) self-similar, this symmetry may be exploited as a guiding line for an appropriate modelling of non-trivial behaviours (e.g., those induced by non-Gaussianity and long-range dependence).

We analysed a stochastic model recently introduced in physics (Zamparo et al., 2013) as a tool for modelling assets’ dynamics on the basis of the anomalous scaling properties observed on financial returns. Thanks to the scaling symmetry, presence of exogenous and endogenous effects, few parameters, and analytical tractability, coexist within the model. We discussed the model properties, in particular with respect to an implementation that amounts to an infinite-state, Markov switching, auto-regressive model. We framed the model components in a financial perspective and described the estimation of its parameters.

Building on the model

potential, we worked out novel closed-form pricing

and associated hedging strategy formulae

for a European call option. We provided details on

the derivation of the pricing equation and of the associated relevant

quantities.

Our work includes an empirical comparison of the

proposed pricing approach with real market prices, together

with benchmark comparisons with a more traditional BS pricing.

We focused on European call options written on the

S&P500 index, with maturity between 2007 and 2013.

Results exhibit

evidence that the novel derivative prices are closer to the market prices than BS ones.

Assessment of the efficacy of the proposed strategy, together with the development of specific Greeks for the aforementioned pricing approach, are left to future research work.

Acknowledgements: The authors are most grateful to the Editors and two anonymous referees for their insightful comments; The authors acknowledge financial support from the Fondazione Cassa di Risparmio di Padova e Rovigo within the Progetti di Eccellenza 2008-2009 program, project Anomalous scaling in physics and finance.

References

- [1] Ait-Sahalia, Y., Lo, A.W., 1998, Nonparametric estimation in state-price densities implicit in financial asset prices. Journal of Finance 53, 499-547.

- [2] Bakshi, G., Cao, C., Chen, Z., 1997, Empirical performance of alternative option pricing models. Journal of Finance 52, 2003-2050.

- [3] Bakshi, G., Cao, C., Chen, Z., 2000, Pricing and hedging long-term options. Journal of Econometrics 94, 277-318.

- [4] Baldovin, F., and Stella, A.L., 2007, Scaling and efficiency determine the irreversible evolution of a market, Proc. Natl. Natl. Acad. Sci. USA 104, 19741-19744.

- [5] Baldovin, F, Bovina, D., Camana, F., and Stella, A.L., 2011, Modeling the Non-Markovian, Non-stationary Scaling Dynamics of Financial Markets, in Abergel, F., Chakrabarti, B.K., Chakraborti, A. Mitra, M. (eds.), Econophysics of order-driven markets (1st edn), New Economic Windows, Springer 239–252.

- [6] Baldovin, F., Camana, F., Caporin, M., Caraglio, M., and Stella, A.L., 2014, Ensemble properties of high frequency data and intraday trading rules, Quantitative Finance.

- [7] Ballocchi, G., Dacorogna, M.M., Gencay, R., and Piccinato, B., 1999, Intraday statistical properties of Eurofutures. Derivatives Quarterly 6, 28-44.

- [8] Beran, J., 1994, Statistics for long-memory processes, Chapman & Hall/CRC.

- [9] Black F., Scholes M. (1973), The Pricing of Options and Corporate Liabilities. J. Polit. Econ. 81, 637-654.

- [10] Borland, L., and Bouchaud, J.P., 2004, A non-Gaussian option pricing model with skew, Quantitative Finance, 4, 499-514.

- [11] Bouchaud, J.P., Georges, A., 1990, Anomalous diffusion in disordered media: Statistical mechanisms, models and physical applications. Physics Reports 195, 127–293.

- [12] Bouchaud, J.P., Potters M., 2003, Theory of Financial Risk and Derivative Pricing: from Statistical Physics to Risk Management, 2nd edn., Cambridge University Press.

- [13] Chernov, M., Ghysels, E., 2000, A study toward a unified approach to the joint estimation of objective and risk neutral mearues for the purpose of option valuation. Journal of Financial Economics 56, 407-458.

- [14] Christoffersen, P., Heston, S., Jacobs, K., 2006, Option valuation with conditional skewness. Journal of Econometrics 131, 253-284.

- [15] Christoffersen, P., Jacobs, K., 2004. Which GARCH model for option valuation? Management Science 50, 104-1221.

- [16] Cont, R., 2001, Empirical properties of asset returns: stylized facts and statistical issues, Quantitative Finance, 1, 223-236.

- [17] Cont, R., 2005, Long range dependence in financial time series, in Lutton E., Levy Véhel J. (eds.), Fractals in Engineering, Springer-Verlag, New York.

- [18] Corsi, F., 2009, A simple approximate long-memory model of realized volatility, Journal of Financial Econometrics 7, 174-196.

- [19] Dacorogna, M.M., Muller U.A., Nagler, R.J., Olsen, R.B., Pictet, O.V., 1993, A geographical model for the daily and weekly seasonal volatility in the foreign exchange market, Journal of International Money and Finance 12, 413-438.

- [20] Dacorogna, M.M., Gencay, R., Muller U.A., Olsen, R.B., and Pictet, O.V., 2001, An introduction to high frequency finance. Academic Press, San Diego, CA.

- [21] Di Matteo, T., Aste, T., and Dacorogna, M.M., 2005, Long-term memories of developed and emerging markets: using scaling analysis to characterize their stage of development. Journal of Banking and Finance 29, 827-851.

- [22] Dumas, B., Fleming, J., Whaley, R., 1998, Implied volatility functions: empirical tests. Journal of Finance 53, 2059-2106.

- [23] Fouque, J.-P., Papanicolau, G., Sircar, K.R., 2000, Derivatives in Financial Markets with Stochastic Volatility, Cambridge University Press, New York.

- [24] Francq, C., and Zakoian, J., 2010, GARCH Models. Structure, statistical inference and financial applications., Wiley, UK.

- [25] Ghashghaie, S., Breymann, W., Peinke, J., Talkner, P., Dodge, Y., 1996, Turbulent cascades in foreign exchange markets, Nature 381, 767-770.

- [26] Guillaume, D.M., Dacorogna, M.M., Dave, R.R., Muller, U.A., Olsen, R.B., Pictet, O.V., From the bird’s eye to the microscope: a survey of the new stylized facts of the intra-daily foreign exchange market, Finance and Stochastics 1, 95-129.

- [27] Hamilton, J.D., and Susmel, R., 1994, Autoregressive Conditional Heteroskedasticity and Changes in Regime, Journal of Econometrics 64, 307.

- [28] Heston, S.L., 1993, A closed-form solution for options with stochastic volatility with applications to bond and currency options, Review of Financial Studies, 6, 337-343.

- [29] Heston, S.L., Nandi, S., 2000, A closed-form GARCH option pricing model. Review of Financial Studies 13, 585-626.

- [30] Hull, J.C., 2000, Options, Futures and Other Derivatives. Prentice-Hall.

- [31] Hurst, H.E., 1951, Long-term storage capacity of reservoirs. Transactions of the American Society of Civil Engineers 116, 770-808.

- [32] Lo, A.W., 1991, Long-term memory in stock market prices. Econometrica 59, 1279-1313.

- [33] Mandelbrot, B.B., 1963, The variation of certain speculative prices. Journal of Business 36, 394-419.

- [34] Mantegna, R.N., and Stanley, H.E., 1995, Scaling behaviour in the dynamics of an economic index. Nature 376, 46-49.

- [35] Merton, R., 1973, Theory of Rational Option Pricing. Bell Journal of Economics and Management Science 4 , 141-183.

- [36] Muller, U.A., Dacorogna, M.M., Olsen, R.B., Pictet, O.V., Schwarz, M., and Morgenegg, C., 1990, Statistical study of foreign exchange rates, empirical evidence of a price change scaling law, and intraday analysis, Journal of Banking and Finance 14, 1189-1208.

- [37] Peirano, P.P., and Challet, D., 2012, Baldovin-Stella stochastic volatility process and Wiener process mixtures, Eur. Phys. J. B 85, 276.

- [38] Robinson, P.M., 2003, Time series with long-memory. Oxford University Press.

- [39] Sethna, J.P., Dahmen, K.A., and Myers, C.R., 2001, Crackling noise, Nature 410, 242-250.

- [40] Stanley, H.E., and Plerou, V., 2001, Scaling and universality in economics: empirical results and theoretical interpretation. Quantitative Finance 1, 563-567.

- [41] Zamparo, M., Baldovin, F., Caraglio, M., and Stella, A.L., 2013, Scaling symmetry, renormalization, and time series modeling, Phys. Rev. E 88, 062808.

| DTM (days) | All | ||||

|---|---|---|---|---|---|

| Moneyness | |||||

| Number of contracts | |||||

| All | |||||

| Average option price | |||||

| All | |||||

| Average implied volatility | |||||

| 0.581 | 0.447 | 0.337 | 0.380 | ||

| 0.675 | 0.317 | 0.256 | 0.188 | 0.227 | |

| 0.186 | 0.173 | 0.171 | 0.177 | 0.175 | |

| 0.300 | 0.257 | 0.247 | 0.246 | 0.265 | |

| 0.498 | 0.353 | 0.313 | 0.301 | 0.383 | |

| 0.646 | 0.422 | 0.330 | 0.316 | 0.456 | |

| 0.745 | 0.492 | 0.347 | 0.304 | 0.493 | |

| 0.813 | 0.493 | 0.356 | 0.302 | 0.459 | |

| 0.904 | 0.542 | 0.389 | 0.315 | 0.475 | |

| 1.430 | 0.790 | 0.508 | 0.329 | 0.650 | |

| All | 0.448 | 0.307 | 0.285 | 0.256 | 0.326 |

| mean | 0.224 | 0.0002 | 5.50 | 0.241 | 0.221 |

|---|---|---|---|---|---|

| st. dev. | 0.033 | 0.0001 | 1.75 | 0.108 | 0.101 |

| min. | 0.155 | 0.0002 | 3.50 | 0.108 | 0.096 |

| max. | 0.295 | 0.0004 | 9.00 | 0.490 | 0.440 |

| median | 0.230 | 0.0002 | 4.50 | 0.207 | 0.187 |

| DTM (days) | Total | ||||

|---|---|---|---|---|---|

| Moneyness | |||||

| Pricing with anomalous scaling and switching volatility | |||||

| All | |||||

| Pricing with Black-Scholes | |||||

| Total | |||||

Appendix

Proof of Lemma 1.

For all

the measures introduced in Lemma 1 and for , it is

straightforward to see that

.

Proof of Theorem 1.

Using the equivalent martingale measure , we have

| (29) |

Since , making the change of variables we obtain

| (30) |

where for the last equality we have used the closeness of the Gaussian under aggregation with .

Following now standard steps as in the BS derivation, we

end up with (14).

Taking the expectation over the distributions of and

, (17) derives then from (14) .

Proof of Theorem 2.

We have

| (31) |

Using and conditionally to the sequence , for we can write

| (32) | |||||

where we have used the fact that depends on the previous values only. Assuming, for simplicity of notation that , setting and exploiting (2) and (3) we get

| (33) |

with given by (21). Putting together, we obtain

| (34) |

Notice that (34) is exact but has the disadvantage that is a conditional density for a “dynamical stochastic volatility” that also depends on the endogenous values future to and is not then identified by historical data only. Using the fact that and the parity of with respect to all its arguments, we have

| (35) | |||||

where we use the facts that

| (36) |

| (37) |

and

| (38) |

On the other hand:

| (39) | |||||

where

| (40) |

By direct inspection, we thus see that .

An explicit expression for

An explicit expression for

In order to write explicitly the r.h.s. of (3.3), let us start with the model’s probability density function of return variables for (see Zamparo et al., 2013, for details):

| (44) |

where

| (45) |

With a slightly more complex notation, let us also define:

| (46) |

where .

Option database filters and data management

Similarly to Dumas et al. (1998), Christoffersen and Jacobs (2004), and Christoffersen et al. (2006), we focus on the Wednesday prices to reduce the computational burden associated with the pricing of several options with different maturities and strike prices. We then apply to the raw Wednesday data filters similar to those proposed by Bakshi et al. (1997): we discard the last week of trading for each option contract to limit the effects associated with option expiration; we drop prices below a threshold set at 0.125 US dollars, to avoid effects associated with price discreteness; we control for prices not satisfying the arbitrage restriction in equation (15) in Bakshi et al. (1997). Similar filters have been applied in previous studies (Ait-Sahalia and Lo, 1998, Bakshi et al., 2000, and Christoffersen et al.,2006, among others). Finally, for each Wednesday, we consider options with maturities in maximum one year.

In performing the option pricing exercise, we consider S&P500 index levels recorded at 3 p.m. US Central Time (Chicago time), to maintain the temporal alignment with the option prices (we consider the closing price recorded at the close of the option trading, at 3 p.m. Chicago time). Moreover, we follow Bakshi et al. (1997), Ait-Sahalia and Lo (1998) and Christoffersen et al. (2006), and account for the effects of dividends paid by the stocks included in the index. To perform the pricing, we remove from the current index level the future dividends which are expected to be paid during the life of the option. We evaluate the dividends following Ait-Sahalia and Lo (1998), starting from the relation between the index price and its future value:

where is the Future price with maturity in periods, is the constant risk-free interest rate from to and is the constant, and unknown, divided rate expected from to . We determine the Future price from the put-call parity

| (49) | |||||

| (50) |

Note that the discounted Future price equals the Index level discounted from future dividends. The dividend yield might be recovered using the actual equity index level. In computing the dividend discounted index, (50) must be evaluated using reliable option prices with, obviously, the same strike price and the same maturity. We select, for each point in time (each Wednesday) and each maturity, the pair of put and call options which are closer to at-the-money (with the strike closest to the equity index level). The interest rates are obtained from Thomson Datastream. We download the interbank rates at 1, 3, 6 and 12 months. For options expiring in less than 41 (open market) days, we use as risk-free the one month interbank rate. The three months rate was used for values of between 41 and 82 days, while the six months rate was considered for options expiring in more than 82 days but less than 183 days. Finally, the 12 months rate was used for options expiring in more than 183 days. After this procedure, for each point in our sample and each maturity we obtain a set of discounted index levels which are then used in the pricing, together with the set of risk-free rates and the option prices previous described.