When terminal facelift enforces Delta constraints 111Research supported by the ANR grant LIQUIRISK and the Chair Finance and Sustainable Development.

Abstract

This paper deals with the super-replication of non path-dependent European claims under additional convex constraints on the number of shares held in the portfolio. The corresponding super-replication price of a given claim has been widely studied in the literature and its terminal value, which dominates the claim of interest, is the so-called facelift transform of the claim. We investigate under which conditions the super-replication price and strategy of a large class of claims coincide with the exact replication price and strategy of the facelift transform of this claim. In dimension , we observe that this property is satisfied for any local volatility model. In any dimension, we exhibit an analytical necessary and sufficient condition for this property, which combines the dynamics of the stock together with the characteristics of the closed convex set of constraints. To obtain this condition, we introduce the notion of first order viability property for linear parabolic PDEs. We investigate in details several practical cases of interest: multidimensional Black Scholes model, non-tradable assets or short selling restrictions.

Keywords: super-replication, portfolio constraints, viability, facelift, BSDEs.

MSC Classification (2010): 93E20, 91G20, 60H30

1 Introduction

In a complete financial market, the absence of arbitrage opportunities leads to the definition of a unique fair price for any contingent claim using replication arguments. This uniqueness property disappears as soon as constraints are introduced in the replication procedure, see e.g. [13, 6] and references therein. This implies the existence of a closed interval of arbitrage-free prices. A commonly considered prudential pricing methodology consists in selecting the upper bound of this interval. This so-called super-replication price coincides with the minimal initial amount of money required to constitute an admissible portfolio strategy satisfying the constraints and whose terminal value dominates the claim of interest. The super-replication price under convex delta constraints has been thoroughly studied in the literature. In [7], the authors obtain a dual representation of the super-replication price in terms of a well chosen set of risk neutral probabilities. In [8], closely related to the previous work, the super-replication price process is shown to be the unique solution of a Backward Stochastic Differential Equation (BSDE) with constraints on the gain process . All these works mainly rely on probabilistic and duality arguments. In a Markovian setting, the super-replication price is characterised using direct dynamic programming arguments and PDE techniques, see [19, 1].

In [4], the authors observe that, for the classical Black Scholes model, the super-replication price of a claim under convex delta constraints coincides with the unconstrained replication price of a so-called facelift transform of this claim. They consider constraints in terms of number of shares in dimension 1, wealth proportion or money amount in any dimension, and exhibit the three corresponding facelifting procedures. In more general Markovian models, the super-replication price function under convex portfolio constraints of a non path-dependent claim interprets as the smallest function above the unconstrained price of the claim, which is stable under the corresponding facelift transform, see e.g. [1]. The goal of this paper is to state a necessary and sufficient condition under which the noteworthy result of [4] extends to general local volatility models in dimension .

To exhibit this condition presented in Theorem 3.1 below, we rely on a BSDE representation of the replicating strategy. We show in Proposition 4.1 that the replicating strategy is the unique solution of a multidimensional linear BSDE with terminal value , where is a smooth payoff function and denotes the assets price process.

If satisfies the portfolio constraint, i.e. is valued in some convex set , the condition given in Theorem 3.1 ensures that the solution of a multi-dimensional linear BSDE with terminal value is valued in a convex set . Namely, the super-replication price of the claim with payoff under convex delta constraints coincides with its unconstrained replication price. It is crucial to observe that we cannot rely on

classical viability results for BSDEs [5] since the class of possible terminal value for the BSDE is restricted here to gradient type terminal conditions of the form . The condition obtained in [5] is thus only a sufficient condition for our problem.

Contrary to this paper, we take advantage here of the linear structure of the problem. It appears that the study of the viability condition for the convex set boils down to the study of the viability condition for the tangent half-spaces to . This makes the proof - in some sense - simpler. Our approach allows us also to remark that, under the exhibited condition of interest, the super-replication price of an American option with exercise payoff under convex delta constraints also coincides with its unconstrained replication price.

In practice, the payoff function does not satisfy that is valued in nor any smoothness property. Nevertheless, our main result still holds using the facelift transform of . The proofs in the general case are based on regularisation techniques.

We also discuss in this paper various practical cases which are of interest in Finance, see Section 3. We first observe that the result of [4] in the Black Scholes model does not extend to the consideration of a financial market with assets. The hypercubes are the only convex set of constraints for which facelifting the payoff allows to get rid of the portfolio constraints in a multidimensional Black Scholes model. This property extends also to most of the common local volatility models, in which each asset follows its own dynamics. In particular, hypercubes include the consideration of non-tradable assets or no short sell restrictions. More specifically, we observe that the only model dynamics in which no short sell restrictions on Asset can be relaxed using a facelifting procedure are the one for which the quadratic covariations between the other assets do not depend on Asset .

The rest of this paper is organized as follows. In Section 2, we specify the problem formulation and exhibit the main properties of the super-replication methodology and related facelift operator. In Section 3, we produce the main result of the paper which gives a tractable analytical necessary and sufficient condition, ensuring that the exact replication property holds for a large class of payoff functions. We describe practical examples of interest and provide a simple probability-change argument in dimension . Focusing on regular payoff functions stable under the facelifting procedure, Section 4 is dedicated to the proof of the necessary and sufficient condition for the so-called first order viability property. Namely, the first order viability property ensures that the gradient of the solution of a linear PDE lies in a convex set on as soon as it does at time . This section revisits arguments of [5] in our framework. Section 5 provides the proof of the main theorem and details in particular the corresponding regularization procedure. The Appendix collects useful properties of the facelift transform and some technical proofs.

Notations. Any element will be identified to a column vector with -th component and Euclidian norm , is the canonical basis of . We denote by the set of matrices with lines and columns, and the subset of symetric elements of . For a matrix , denotes its trace, its -th column, its -th row, and the -th term of . The transpose of a matrix or a vector will be denoted . For a vector , denotes the diagonal square matrix with diagonal terms given respectively by . For a function from to , we denote by and the -dimensional row vector and the matrix in defined by

| and |

We shall also note , for and , .

denotes the set of function from to which are differentiable with continuous and bounded first derivatives.

We denote by the Lebesgue-measure and by the Doleans-Dade exponential of a process .

Finally, for a given closed convex set , is the (non-negative) distance function to this set, namely, .

2 Super-replication and facelift properties

In this section, we introduce the market model and formulate the super-replication problem under Delta constraints, namely when the number of shares constituting the portfolio must remain in a closed convex set.

2.1 The market model

We consider a financial market defined on a probability space , endowed with a -dimensional brownian motion . For , we denote by the completion of the filtration generated by and by the -field of progressively measurable processes associated to . In the sequel, we interpret the probability as a pricing measure.

We suppose that the financial market is composed of risky assets and one non-risky asset, whose interest rate is assumed to be for ease of presentation. Up to considering discounted processes, all the results of the paper extend straightaway to financial markets with deterministic interest rates.

For an initial condition , where represents the vector value of the assets at time , the vector of risky asset price process is described by the diffusion defined as the unique solution of the stochastic differential equation

| (2.1) |

where is the volatility function. The Dynkin second order linear differential operator associated to the dynamics (2.1), denoted by , is given by

for any .

We denote by the interior of the the support of the function i.e. the open subset of defined by

Throughout this paper, we work under the condition that the function is and shall sometimes use the following assumption:

The function is continuous on and for any , the process is well defined.

Starting with an initial wealth at time , an investment strategy is described by a -measurable process valued in , where represents the number of shares of asset detained at time . We denote by the set of self financing strategies such that

The portfolio process corresponding to an initial wealth at time and a self-financing strategy is denoted and satisfies

The set of admissible strategies is given by the strategies in such that the portfolio value is bounded from below by a constant.

2.2 Super-replication under constraints

Due to regulatory or structural reasons, we suppose that the possible investment strategies are restricted to take their values in a deterministic closed convex subset of s.t. .

For any , the subset of admissible constrained strategies is then defined by

Observe that the constraint is not imposed on the portfolio value but on the investment strategy itself.

The addition of constraints on the investment strategy implies that exact replication of a given contingent claim is not always possible, see e.g. [13]. Here, we intend to focus on super-replication strategies.

Definition 2.1 (Super-replication valuation)

For a measurable function bounded from below, we define the super-replication price of the contingent claim under constraint at time by

for any .

The super-replication price of a contingent claim has been widely studied in the literature see e.g. [7, 19, 1]. In our context, a complete characterization of the super-replication price under constraint is given in [2] and we will use a supersolution property of proved therein. Let us recall that the support function of the convex set is defined by

whose domain is denoted

Using the support function of , we define the following global differential operator related to the constraints:

Let us also introduce

Definition 2.2 (Facelift)

The facelift operator for the admissibility set maps any measurable function , to its facelift transform , defined by

We collect in the Appendix, Section 6.1, some useful properties of the Facelift transform.

In the sequel, we shall use the following assumption related to the payoff function and its facelift transform:

The function is lower semi-continuous, bounded from below and such that

Remark 2.1

Assumption is satisfied, e.g., in the following cases.

(i) When i.e. the no short sell constraint and is the payoff of a Put option. Indeed, is then a constant function equal to the strike of the Put option.

(ii) When is bounded or is Lipschitz continuous, since then is Lipschitz-continuous.

Let us now recall the following result proved in [2].

Proposition 2.1

The super-replication price under -constraint is a viscosity supersolution of the following PDE

and satisfies

provided that is l.s.c, with linear growth and bounded from below.

We conclude this section with a consequence of the previous result.

Corollary 2.1

Assume that h is l.s.c, with linear growth and bounded from below, then

For sake of completeness, we provide a proof in the Appendix, see Section 6.2.

3 Relaxing portfolio constraints via terminal facelift

In this section, we investigate under which conditions, super-hedging any claim under Delta constraints is equivalent to simply hedge the facelift transform of this claim. We first consider the particular case where the number of shares for each asset is constrained to stay in-between two constant bounds. In this context, we show that the ‘replication property’ is always satisfied in the one-dimensional case but not systematically in the multi-dimensional case. This motivates the second part of this section which presents in Theorem 3.1 a tractable analytical necessary and sufficient condition ensuring this property to hold for general multi-dimensional convex constraints. We finally focus on several practical examples of importance (Black Scholes model, short selling, non-tradable asset, etc.) in order to emphasize the range of applications for Theorem 3.1, which is the main result of the paper.

3.1 A motivating example

We consider first a simple practical example where the investor faces constant restrictions on the number of shares of each asset held in the portfolio. More precisely, the admissibility set is a closed hypercube given by

| (3.1) |

Observe that this form of convex set allows to consider, for example, the realistic practical case where short-selling one or several assets is not allowed. It also covers the natural case where some of the assets cannot be traded on the financial market ().

We first focus on the particular case where only one asset is traded (). As detailed in the next proposition, a direct probability change argument shows that super-replicating a claim under -portfolio constraints simply consists in replicating without constraint the facelift transform of this claim. For sake of simplicity, we consider here payoff functions with regular facelift transform, but this strong regularity property is relieved in the following subsection, see Theorem 3.1.

Proposition 3.1

Let and be a payoff function such that . Then, for any starting point , the super-replicating price and hedging strategy under -constraints of the claim coincides with the exact replicating price and unconstrained hedging strategy of .

Proof. Let and consider a payoff function such that . By construction of the facelift transform, is necessarily valued in . We now consider the exact replicating strategy of and intend to prove that is valued in on . Due to the regularity of , observe that the exact replicating strategy rewrites

where denotes the tangent process of and satisfies

Since has bounded derivatives, we deduce that is a positive martingale with constant expectation equal to . Therefore, it also interprets as a probability change on and we denote by the probability defined by . This allows us to rewrite directly

Since is valued in the convex set , is also valued in .

The hedging strategy of being valued in , it coincides with the super-hedging strategy under -constraints of , see Corollary 2.1. Hence, the super-replicating price of and the replicating price of also coincide.

Remark 3.1

Interpreting the gradient of the stock process as a probability change has already been used for example in [11].

We now turn to the multi-dimensional case. As detailed in the next proposition, the previous result easily extends to the particular case where each asset has its own dynamics, since the previous arguments can be applied on each component of the price process .

Proposition 3.2

Let be a payoff function such that . Fix and suppose that the dynamics of each asset is given by

Then, the super-replicating price and hedging strategy under -constraints of the claim coincides with the replicating price and hedging strategy of .

Proof. Following the same reasoning as in the one-dimensional case, we only require to verify that the exact replicating strategy of is valued in . As in the one dimensional case, we have

where is the tangent process of . Due to the particular form of the stock dynamics, each tangent process is a positive martingale starting from . Observe that, contrary to the one-dimensional proof, we cannot use a common probability change for all the components of the hedging strategy . Nevertheless, due to the special form of and the fact that , we work separately on each component. We compute

for and . Hence, the replicating strategy is valued in and the proof is complete.

Unfortunately, this nice property does not remain valid for general multi-dimensional stock dynamics. Consider for example the 2-dimensional case where the dynamics of the first asset is given by

and the second asset (the stochastic volatility) is not tradable, i.e. . In this framework, the super-replicating price of a call (or any convex payoff) option on is simply the -volatility Black Scholes price of this call, see e.g. [9].

Hence, even for hypercube type constraints, the exact replication of the facelifted terminal payoff does not always match the constrained super-replication of the payoff. The purpose of the next section is to investigate the conditions one should impose on the model dynamics and the convex set , in order to retrieve this useful property.

3.2 The main result: general convex constraints

We now consider general Delta constraints characterized by a subset of satisfying the following assumption :

is a closed convex subset of with non empty interior and .

We consider a stocks’ price process with general dynamics (2.1). The next theorem provides a tractable necessary and sufficient condition ensuring that, in order to super-replicate under -constraints any option with payoff function satisfying , one simply needs to replicate the facelift transform of the terminal payoff.

For any point on the boundary of , we denote by the set of unitary outward normal vectors to at i.e.

We define the set of points where there exists only one outward normal vector denoted , i.e.

| (3.2) |

Equivalently, is the set of the boundary points where there is a tangent hyperplane, see [18] for details.

In the sequel, we shall sometimes use the following technical assumption on the couple .

For any and any , the -local martingale defined by

for , is an -martingale.

We refer to Remark 3.3 for a discussion on relevant cases when is satisfied.

Finally, for any , we associate to a family of vectors such that and is an orthonormal basis of . We denote by the new matrix basis i.e. , . Observe that is an orthogonal matrix.

When it is clear from context, we shall omit the ’’ in the above notations, for the reader’s convenience.

Theorem 3.1

Let us consider the two conditions:

-

(i)

For any payoff function satisfying and any , the super-replicating price and strategy of under -constraint coincides with the exact replicating price and unconstrained strategy of the facelifted claim .

-

(ii)

The following holds true:

(3.3) for all .

Under , we have that (i) implies to (ii). Moreover, if and hold then implies .

In order to alleviate the presentation of the paper, the proof of this theorem is postponed to Section 5. Considering first regular payoff functions which are stable under the facelifting procedure, the unconstrained hedging strategy of interprets as the solution of a linear BSDE (or PDE) with terminal condition . We introduce in Section 4 the notion of first order viability for the corresponding BSDE which ensures that the solution of the BSDE is valued at any time in , for any bounded terminal payoff function of the form lying in . We then establish in Theorem 4.2 that Condition (ii) above is necessary and sufficient for this newly introduced first order viability property. The extension of this property to payoff functions satisfying is done via a regularization argument presented in Section 5.

Remark 3.2

The previous property extends also naturally to American options, under additional regularity assumptions. See Remark 4.5 (ii) below for a sketch of proof.

Remark 3.3

Let us exhibit interesting cases where holds.

(i) The Black and Scholes model.

Suppose that the volatility function is given by

| (3.4) |

where is an invertible matrix of . As detailed in Example 5 below, Condition (3.3) imposes that is a vector of the canonical basis, for any . Denoting then the outward normal vector of interest, the relation for any together with (3.4) imply via a direct computation that the local martingale rewrites

for all . Therefore, Assumption is satisfied.

(ii) The elliptic volatility model.

Suppose that there exists two constants and such that

| (3.5) |

Observe that and Assumption (H) holds. Using (3.5), we compute

Since is and bounded, we deduce that the term above is bounded, and using Novikov condition that, holds.

We conclude this section with the following Remark discussing equivalent writing of condition (3.3).

Remark 3.4

(i) An equivalent coordinate-free formulation of condition (3.3) is the following:

| (3.6) |

Indeed, fixing , observe that the family of elements of , given by

is a basis of . Moreover, it is straightforward to show that the family is a basis of . Thus the relation

implies that (3.3) and (3.6) are equivalent.

(ii) Condition (3.3) can also be rewritten fully in the new basis , for a fixed . Let us define

, then (3.3) simply reads

for all . If we define , then the above condition states that there is no dependency upon the first component of of the quadratic covariations of the other components.

3.3 Financial applications

We now present financial applications of the main result of the paper. We also precise the form of the necessary and sufficient condition (3.3) for relevant convex constraints and model dynamics in the field of mathematical finance. We successively consider the cases of illiquid assets, short sell prohibition and restrictions on the total number of positions taken on the financial market.

Then, we look towards the model dynamics satisfying the viability property for any possible closed convex constraints set. Although it is always the case in dimension , it appears that this condition is very restrictive in greater dimension. Finally, for the multidimensional Black Scholes model, we show that super-replicating an option with Delta constraint is equivalent to replicating the corresponding facelifted payoff if and only if the set of constraints is given by an hypercube , recalling (3.1).

Example 1: Non-tradable asset.

In dimension 2, we consider the case where Asset is illiquid and thus cannot be traded. The corresponding convex set is the ordinate axis . This convex set does not satisfy Assumption since it has an empty interior, but Remark 4.3 below justifies that Theorem 3.1 is also valid for hyperplanes. The only outward normal vectors to are and which lead to the same Condition (3.3), which rewrites

| (3.7) |

This necessary and sufficient condition indicates that the quadratic variation of the second asset does not depend on the first one. Observe that the condition derived by [5] for classical viability property rewrites: . This condition is stronger than (3.7) as expected.

Example 2: No short sell.

Consider a market with two assets where short selling Asset is prohibited i.e. . Up to their sign, this convex set shares the exact same outward normal vectors with the one considered in the previous example. The main observation here is that Condition (3.3) is only related to the border of so that convex sets with similar borders share the same viability property. Therefore the prohibition of short selling asset is also related to Condition (3.7). Moreover, since the corresponding convex sets share the same unit outward normal vectors, we emphasize that restricting to portfolios such that for some leads to the same condition (3.7) derived here when .

Similarly, if short selling any of the two assets is prohibited, super-replication reduces to hedging the facelifted claim payoff whenever the stock model satisfies

| and | (3.8) |

In dimension , when the subset of assets cannot be short sold, the necessary and sufficient Condition (3.3) rewrites as a constraint on quadratic covariations and takes the following form:

Example 3: Bound on the number of shares.

We now consider the case where the investor faces a constant upper bound on the total number of possible positions he or she can take on the financial market. In dimension , this corresponds to the consideration of the lozenge convex set . Up to their directions, there are two outward normal vectors for the convex set : namely and . Thus, the condition (3.3) rewrites as

Observe that this condition is the one given by (3.8), but simply written in a different orthonormal basis.

Example 4: Model with unconditional viability property.

Clearly, Condition (3.3) is always satisfied if the volatility function is constant. Therefore, the replication property (i) of Theorem 3.1 is valid for any closed convex set in the particular case where the assets’ price is a multidimensional Brownian motion, i.e. in the Bachelier model.

Moreover, in dimension 1, Proposition 3.1 states that any model satisfies this property.

We now show that this unconditional viability property may lead to strong restriction on the model in dimension greater than .

To this end, we identify the models with separate dynamics and invertible volatility matrix satisfying the unconditional viability property in dimension 2.

Namely, the model has the form

For any outward normal vectors , Condition (3.3) rewrites

Hence, a model satisfies the replication property for any closed convex set if and only if

Since the volatility function is invertible, this condition is equivalent to the relation

| and |

Then, the volatility function reads

for some and .

The invertibility condition on imposes and invertible. Necessarily, the class of model with separate dynamics and invertible volatility matrix satisfying an unconditional viability property is the class of Bachelier models.

Example 5: The multidimensional Black Scholes model.

We assume that the dynamics of the stocks are given by

with is invertible.

1. If the property is satisfied for a given convex set , then is an hypercube.

Indeed, Remark 3.4 (i) yields

Since and belong to , this rewrites

| (3.10) |

If we define by

we easily check that . Then using (3.10), we get

which gives since is invertible. Using a similar argument, we prove that for , which shows that must be a vector of the canonical basis .

2. If , we can apply Proposition 3.2 to obtain the first-order viability, when the terminal condition is smooth enough. For the general case, we apply our main result. Indeed, Remark 3.3 implies that holds for the couple . The assumptions of Theorem 3.1 (ii) are thus satisfied. Setting, w.l.o.g , we get that Condition (3.3) holds since it rewrites in this case

4 First order viability for the PDE

In this section, we introduce a new notion of viability for linear PDEs. Namely, the constrained super-replication problems considered in this paper entails to find out whether a hedging strategy with terminal value in will always do so on the time interval . Since the hedging strategy rewrites as the gradient of a function of solving the linear PDE , we want to know if the gradient of the solution of this PDE lies in on as soon as it does so at time . This leads to the notion of first order viability property for the PDE , presented in Section 4.1. This notion interprets also in terms of viability for linear BSDEs associated to the subclass of gradient type terminal functions. We verify in Section 4.2 that the PDE is first order viable for a closed convex set with non empty interior whenever it is first order viable for almost all its tangent half-spaces. Specializing then our study on first order viability for half-spaces, we provide in Section 4.3 a geometric condition indicating whether or not the PDE is first order viable for a given half-space. This finally allows us to verify in Section 4.4 that the PDE is first order viable for a closed convex set if and only if the structural condition (3.3) on the couple is satisfied.

4.1 First order viability: PDE and BSDE viewpoints

For any , the price function of the European option with terminal payoff function and maturity is given by:

This function interprets as the unique viscosity solution of the parabolic PDE

| (4.1) |

in the class of continuous functions with polynomial growth, see e.g. [17]. Moreover, by Theorem 3.1444An uniform ellipticity condition for appears in the statement of this theorem but this assumption is not used in the proof and indeed not required. in [14], we deduce that is on .

We now introduce the notion of first order viability.

Definition 4.1

The PDE is first order viable for a given set (or -first order viable) if and only if, for any function s.t.

the function defined by (4.1) satisfies

Remark 4.1

Contrary to the classical definition of viability, which requires the function to take value in , our definition deals with the first derivative of which has to be valued in .

The first order viability property for the PDE also has a direct interpretation in terms of linear BSDE solution. Indeed, as detailed in the next proposition, admits a BSDE representation, for any and .

For , we denote by the set of -adapted continuous processes valued in and by the set of -predictable processes valued in such that

Proposition 4.1

Let be in . For , we consider the process solution of the BSDE

| (4.2) |

where is defined by

| (4.3) |

Then we have

Moreover, under , we have that , for some symetric matrix valued process .

Observe that the first order viability for the PDE can be directly rewritten in terms of (zero-order) viability property for the linear BSDE (4.2) on a subclass of gradient payoff functions.

Corollary 4.1

The PDE is first order viable for a given set if and only if, for any such that belongs to , the part of the solution of the BSDE (4.2) belongs a.s. to , for any .

Proof of Proposition 4.1. Fix and . Let be the solution to the following BSDE with no driver:

Such a solution exists and is unique since and . We consider the inverse of the tangent process as well as the tangent process of , see e.g. [14]. They have the following dynamics

From e.g. Theorem 3.1 in [14], we know that

| (4.4) |

Recalling that the process is solution to the markovian linear BSDE (4.2) with continuous coefficient function, we have that for some continuous function , see e.g. Theorem 4.1 in [12]. Observe also that is deterministic. Applying Itô’s formula, we compute using the dynamics of and that

| (4.5) |

Setting in the above equation and using (4.4), we obtain that .

We deduce that , for any .

When the volatility matrix is smooth, one can show, using Feynman-Kac formula, that is a classical solution of a linear PDE and then . In the general case, one uses a regularization procedure (see e.g. the proof of Proposition 3.3 in [3]) and the stability property of (linear) BSDEs (see e.g. Proposition 2.1 in [12]) to show that is the limit of symetric matrix and thus symetric itself.

The rest of the section is dedicated to the proof of a necessary and sufficient condition for the first order viability property to hold. It is important to observe that the only possible terminal conditions for the linear BSDE (4.2) are of the form . Hence the viability characterization for BSDEs derived in [5] does not apply directly here since it requires the consideration of any terminal condition of the form , with a continuous function. In the next section, we adapt the arguments developed in [5] using a geometric approach.

4.2 First order viability and half-space decomposition

In this section, we prove that the first order viability for a closed convex set satisfying , is characterized by the first order viability of a well chosen collection of half-spaces supporting , i.e. such that and . For this purpose, we first rewrite as the intersection of the corresponding half-spaces and then discuss the related first order viability properties.

For , we denote by the radius of the largest closed ball included in which is tangent to at point i.e.

The set of points of with corresponds to a subset of points where the convex surface presents some regularity. We denote this subset by , namely,

In particular, observe that for any point in , there exists a unique outward normal vector so that where is defined in (3.2). For , we denote by the unique outward normal vector and by the half-space tangent to at point containing , i.e.

Lemma 4.1

Any convex set satisfying rewrites

| (4.6) |

Proof. The proof divides in two steps.

Step 1: Theorem 18.8 in [18] states that if and only if

| (4.7) |

Let be a dense subset of . It is obvious that implies

| (4.8) |

We are going to verify the converse implication, showing that (4.8) implies (4.7).

For this to be true, we only need to find for any fixed an approximating sequence of points in s.t. and .

Let first observe that for , since is a dense subset of , there exists

an approximating sequence of points in converging to .

Since is compact, we have that, up to a subsequence still denoted , converges to some unit vector . Moreover, we compute

This implies that for any , so that is an outward normal vector for at . Since , we get and (4.8) holds.

Step 2: Let be the unit closed ball and set for , with . Hence . For , one observes that if and , then . McMullen [15] shows that has a zero -lebesgue measure, for any . Since , this implies that is dense in . Combined with Step 1, this concludes the proof of the lemma.

We now observe that the first order viability property for the convex set relates to the first order viability property for every half-space , . This nice property allows us to restrict our upcoming argumentation to the consideration of viability property for half-spaces.

Proposition 4.2

Let be in force. Then, the PDE is first order viable for the closed convex set if and only if it is first order viable for every half-space , for .

The proof of this proposition requires the following lemma, which states the homothetic stability of the first order viability property.

Lemma 4.2

The PDE is first order viable for a closed set if and only if it is first order viable for every closed set with and .

Proof. We fix a set and choose and . We suppose that the PDE is first order viable for and simply need to verify that it is also first order viable for . Let such that is valued in and define the function by

The gradient of directly satisfies

Since the PDE is viable for we deduce that is valued in . Moreover, we easily check that the function solves the PDE

| (4.9) |

From uniqueness of the solution to (4.9), we get

Since is valued in , we deduce that is valued in . The arbitrariness of indicates that is first order viable for and concludes the proof.

We now to turn to the proof of Proposition 4.2.

Proof of Proposition 4.2. The proof divides in two steps, corresponding to each implication.

Step 1: Assume that the PDE is first order viable for any , with . We deduce from this viability property and the representation of given in Lemma 4.1 that, for any with valued , is valued in every , . Using again the representation of given in Lemma 4.1, we conclude that is first order viable.

Step 2: Assume that the PDE is first order viable for .

We intend to prove that it is also first order viable for any with . Up to considering according to Lemma 4.2, we suppose that .

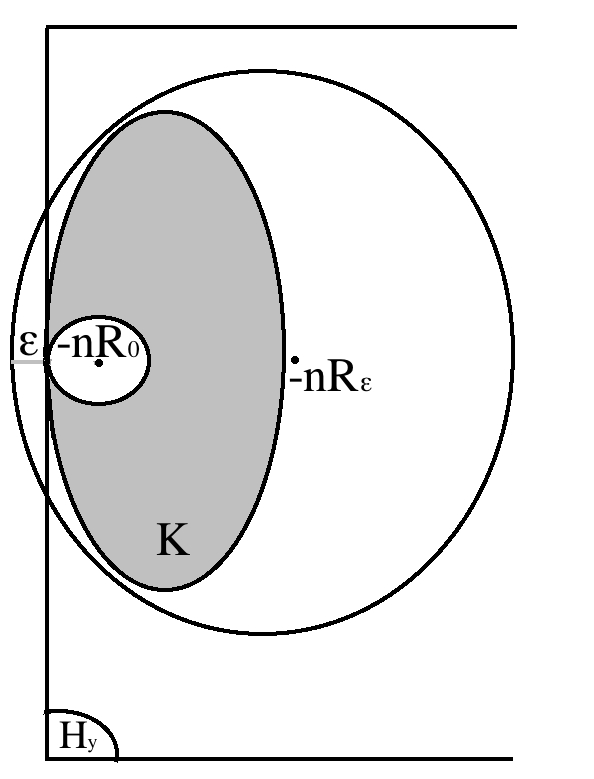

By definition of and denoting by the outward normal vector to at point , there exists such that the ball is tangent to at . We pick with valued in . We choose any arbitrary and intend to prove that is valued in .

Since is bounded, there exists such that is valued in , as shown on Figure 1. Therefore, we deduce that

Since the PDE is first order viable for , Lemma 4.2 indicates that it is also first order viable for and therefore is valued in . But, since the half-space is convex cone, we have

Thus is valued in , for any . Hence, is also valued in . Therefore, the PDE is first order viable for any hyperplane , with .

4.3 First order viability property for half-spaces

The aim of this section is to prove the following result.

Theorem 4.1

If the PDE is first order viable for the half-space with normal unit vector then

| (4.10) |

Moreover, whenever and hold, the converse is valid.

The proof of this theorem is done in two steps below, proving each assertion separately, namely Proposition 4.3 and Proposition 4.4. The proofs follow ideas developed in [5] for (zero-order) viability properties on BSDEs, but are much simpler due to the consideration of half-spaces.

Remark 4.2

(i) The condition has a natural geometric interpretation. For a given terminal condition in , it indicates that the -component of the solution of the BSDE (4.2) with generator is pushed inside the half-space whenever it comes near its boundary. This condition takes the form in our context since given in (4.3) is linear with respect to its second variable.

(ii) Assume holds true. The BSDE (4.2) satisfies the classical (zero-order) viability property for the half-space if and only if

This condition is the one given in [5] adapted to our context, it is stronger than (4.10). It is important to observe that the restriction to terminal conditions of the form translates into the only consideration of symetric matrices .

Before proving Theorem 4.1, we state that Condition (4.10) and Condition (3.3) for half-spaces with outward normal vector , are the same.

Lemma 4.3

Proof. Recall that denotes the new basis orthogonal matrix associated to . We introduce the family of elements of , given by

This family is a basis of . Moreover, it is straightforward to show that the family is a basis of . If we assume that

| (4.12) |

it is then clear that Condition (4.10) is equivalent to Condition (4.11).

The following computations prove (4.12):

We now proceed with the proof of the necessary part of Theorem 4.1.

Proposition 4.3

If the PDE is first order viable for a half-space with unit outward normal vector , then Condition (4.10) holds for .

In order to derive this proposition, we use the following technical lemma whose proof is given in the Appendix, see Section 6.3.

Lemma 4.4

Let such that . If the PDE is first order viable for a half-space with unit outward normal vector , then belongs to where is the solution on of the BSDE (4.2) associated to the terminal condition .

Proof of Proposition 4.3.

Using Lemma 4.2, we can assume w.l.o.g. that .

In order to verify that Condition (4.10) holds for the vector , we pick any and such that . Since one can choose either or and the map is linear, we only need to check that

| (4.13) |

We pick and denote by solution on of the SDE (2.1) starting in at time and by the solution on of the BSDE (4.2) associated to the terminal condition . We deduce from that so that . This implies that

Since the PDE is first order viable for the half-space , Lemma 4.4 indicates that belongs to and thus

| (4.14) |

Let us define the process on by

Since , we compute directly

| (4.15) |

In particular, observe that (4.13) is satisfied as soon as is non-positive for small enough.

Besides, and are solutions on of BSDEs with the same terminal condition and respective drivers and . The stability property for BSDE, see for e.g. Prop 4.1 in [5], reads

where is a non-negative constant, which may change from line to line and does not depend on .

The Cauchy Schwartz inequality together with the Lipschitz property of the driver with respect to its second variable leads to

| (4.16) | |||||

where the last inequality follows from classical estimates on the forward diffusion on , and is given by

Observe from the Markov property of the process that rewrites

Since , the function given in (4.3) is continuous and bounded. Therefore, the continuity of the process together with the dominated convergence theorem ensures that goes to as does so. Thus, we deduce from (4.16) that

Up to a subsequence, this implies that and share a.s. the same limit. Therefore (4.14) together with (4.15) provide

which concludes the proof.

Remark 4.3

Observe that the same line of arguments indicates that (4.10) is satisfied for a given vector as soon as the PDE is first order-viable for an hyperplane with outward normal vector . One simply needs to work with conditions of the form instead of in the above proof.

Moreover, observe that rewrites with a half-space with outward normal vector , and (4.10) is automatically satisfied for as soon as it is valid for . Therefore, Proposition 4.4 below indicates that the PDE is first order-viable for both half spaces and whenever (4.10) holds for . Thus this condition is also necessary and sufficient in order to ensure that the PDE is first order viable for any hyperplane with outward normal vector .

Proposition 4.4

Suppose that Condition (4.10) holds for the vector . Then, under and , the PDE is first order viable for any half-space with outward normal vector .

Proof. Without loss of generality, we assume that , recalling Lemma 4.2.

Let be a function in with gradient valued in .

Let and denote the respective solutions of the SDE (2.1) and the BSDE (4.2) associated to any fixed starting point in and terminal condition . We intend to prove that is valued in on . The first order viability of for is then a direct consequence of Corollary 4.1.

Using Proposition 4.1, we have, for

| (4.17) |

where is valued in . Recalling the proof of Lemma 4.3, we write and observe that .

Moreover, since , we get from (4.17) that

| (4.18) |

for all , recalling (4.12).

Using Condition (4.10) in its equivalent form (4.11), we obtain

| (4.19) |

for . Defining the vector valued process s.t. , , we compute

| (4.20) |

Using the definition of , we notice that

Therefore, we can apply Girsanov Theorem under , and we know that there exists an equivalent probability measure , under which the process is a Brownian motion. Taking the expectation under this new probability measure in (4.20), we obtain

which concludes the proof.

4.4 First order viability for general convex sets

As established in Proposition 4.2, the first order viability of a closed convex set with non empty interior is characterized by the first order viability of supporting half-spaces tangent to at points . We shall verify in this section that it is also characterized in terms of first order viability on the largest class of supporting hyper-spaces associated to any . More importantly, we derived in Theorem 4.1 a necessary and sufficient analytical condition ensuring the PDE to be first order viable for a given half-space. Combining these observations provides therefore a similar condition for any closed convex set with non empty interior.

Theorem 4.2

Let be in force. If the PDE is first order viable for the convex set , then the condition (3.3), which rewrites equivalently

| (4.21) |

is satisfied. Besides, whenever and hold, the converse is valid.

Proof. The proof is performed in several steps.

Step 1: (4.21) implies the first order viability property.

We assume in this step that (4.21) is satisfied and holds. Then, for any , Theorem 4.1 indicates that the PDE is first order viable for the supporting half-space . In particular, it is first order viable for any half-space with and Proposition 4.2 implies that it is first order viable for the convex .

Step 2: The first order viability property implies (4.21).

Assume that the PDE is first order viable for . Proposition 4.2 indicates that this is also true for any half-space with and Theorem 4.1 implies that

It remains to check that this relation is also valid for a given .

Let be in . As observed in the proof of Lemma 4.1, is the limit of a sequence of points lying in s.t. . Fix now some satisfying . Then there exists a sequence in such that for any and . Indeed, since , there exists s.t. and where is a diagonal matrix with . The matrix corresponds to the new basis matrix from the canonical basis to an orthonormal basis . Then consider the basis obtained by applying the Gram-Schmidt orthonormalization procedure to the basis and denote by the new basis matrix for for . Since the Gram-Schmidt orthonormalization procedure is continuous, we get that . Then define the sequence in by

From the definition of the basis and since we have for all . Moreover, since , we have .

Now, since and , we get

for any . Letting go to infinity, we obtain and (4.21) holds also for such that .

Remark 4.5

(i) As observed in Remark 4.4, Condition (3.3) also ensures that, if the first component of the solution to the BSDE (4.2) lies in at a given stopping time valued in , remains in on . Therefore Condition (3.3) is necessary and sufficient to ensure that the BSDE (4.2) satisfies the first order viability property for on any random time interval , with stopping time smaller than .

(ii) Consider for example an American option whose exercise payoff is on . We assume that with valued in . We denote by the optimal stopping time. Under some regularity assumptions, it is known that the Delta of the option at time is , where the terminal condition in (4.2) is now random and given by , see e.g. [10] Theorem 2.3 and the references therein. One can then apply (i) above to conclude that Theorem 3.1 holds true for American Option, under strengthened regularity assumption.

5 Proof of Theorem 3.1

In this Section we prove the main result of this paper, i.e. Theorem 3.1, using the results of Section 4 together with some regularization arguments. We prove each implication separately.

5.1 (i) (ii)

Let be any function in such that is valued in . Our goal is to show that is valued in when (i) holds true ( is not necessarily bounded from below). If this is the case, then the PDE is first-order viable and the statement is a straightforward consequence of Theorem 4.2.

We now construct an approximating sequence of functions s.t. satisfies

and , as .

To this end, we introduce, for ,

where is the facelift operator on associated to the convex set . We then define the sequence by for all . We notice that is lower bounded and for all , and all . We compute that and since , . Thus satisfies . Moreover, we have and , as , for all . Using the representation of Proposition 4.1 and usual stability arguments for BSDEs (see e.g. Proposition 2.1 in [12]), we obtain that , as . Under (i), we have that takes its values in and so does .

5.2 (ii) (i)

Step 1: Replication strategy for .

Let fix . Under , is bounded from below. Hence, Lemma 6.1 (v) ensures that is also bounded from below. Using the martingale representation Theorem, we have

which allows us to define the replicating financial strategy for by

Since and is a continuous process, this strategy is obviously admissible.

Step 2: Viability of the replication strategy of .

We now prove that the replicating strategy is admissible.

The main difficulty relies here in the lack of regularity of the payoff function under assumption . We therefore use an approximation argument and proceed in two substeps.

Substep 2.a: Regularization of .

Under , we consider the Lipschitz-regularization of given in Lemma 6.2. We introduce the sequence given by

Using , Lemma 6.2 and the dominated convergence theorem, we easily obtain

and thus in .

Defining the process

we directly deduce that up to a subsequence

| (5.1) |

Substep 2.b: Regularization of .

Fix and let be a compactly supported smooth probability density function on .

We define the sequences of function and from to by

and

for any . Let us introduce given by the martingale representation Theorem

As in the previous step, we define the sequence of processes . We observe that, up to a subsequence, a.e. on as goes to . Besides, Theorem 3.1 in [14] directly implies that

| (5.2) |

Now, since is a bounded Lipschitz function, combining Rademacher Theorem with Lemma 6.3 (i) we have , for almost every , which means

We also observe that, since is Lipschitz cotinuous, we have from the dominated convergence theorem

Now, since is closed and convex, we obtain

| (5.3) |

Applying Theorem 4.2, we deduce that and thus are valued in , recalling (5.2).

Substep 2.c: Viability of the replicating strategy of .

For any , since a.e. as goes to infinity, the closeness of implies that is valued in a.e.

A similar argument yields that is also valued in , recalling Step 1.

Since is an admissible strategy, we conclude that .

6 Appendix

6.1 Facelift properties

The first lemma collects some useful properties of the facelift transform. Lemma 6.2 is an approximation result and Lemma 6.3 is a (minimal) PDE characterisation of the facelift.

Lemma 6.1

(i) If h is lower semi-continuous, then is also l.s.c..

(ii) If for all , then , for all .

(iii) If and with a given constant then .

(iv) .

(v) and .

Proof. Property (i) holds true since is the point wise supremum of l.s.c. functions. Properties (ii)-(iii)-(iv) are obvious consequences of the Definition 2.2 of the facelift transform. Property (v) follows from the fact that and the following computation

for any .

Lemma 6.2

Assume that is lower semi-continuous and bounded from below by , for some .

Then, there exists an increasing sequence of

bounded Lipschitz function, uniformly bounded from below by converging to and such that

.

Proof. We define the sequence of functions by

for . It is clear that the sequence is nondecreasing, that and is -Lipschitz continuous for all .

We now prove that converges pointwise to . Fix some . Since is l.s.c and bounded from below there exists a sequence in such that

| (6.1) |

Since is bounded from below by , we deduce

so that . Together with (6.1) and the lower semi continuity of , this yields

Thus, as , for all .

Define now the sequence of functions by

Since is Lipschitz continuous and bounded from below, is bounded and Lipschitz continuous, for all . Moreover, since is nondecreasing and converges pointwise to , we also get that is nondecreasing and converges pointwise to .

It remains to prove the convergence of to . For any , we simply observe that

Lemma 6.3

Let be a lower semi-continuous function from to .

(i) Assume that is locally bounded, then is a viscosity super-solution of

| (6.2) |

(ii) Let be a differentiable super-solution of (6.2), then

In particular, if is differentiable and , then .

Proof. Step 1: Proof of (i).

We first recall that, since is l.s.c continuous, is also l.s.c, see Lemma 6.1. Let and a test function such

that

| (6.3) |

Observe that Lemma (6.1) (v) implies , so that

Using (6.3), we deduce

In particular, for where and with , we obtain

Letting goes to yields . Since is arbitrarily chosen in , this yields .

Step 2: Proof of (ii).

Let be a differentiable supersolution of (6.2). We then have

Fix now . We get from the previous inequality

Therefore, we compute

Taking the supremum over , we obtain .

Suppose now that is differentiable and . Since we already know that , we conclude .

6.2 Proof of Corollary 2.1

For sake of clarity, let us define by

Recall also the definition of and in the proof of Theorem 3.1, Section 5.2, Step 1 and Substep 2.a and the fact that

| and |

for .

From the left-hand equality of the above statement and Proposition 2.1, we deduce that is a viscosity super-solution of

| (6.6) |

Since is Lipschitz continuous, it is also well known (see e.g. [16]) that is a viscosity solution of (6.6), for any .

The PDE (6.6) satisfies the assumptions of Theorem 4.4.5 in [17], which provides a strong comparison theorem for viscosity solutions with polynomial growth. Since the functions and have linear growth, this yields

for any . The proof is concluded letting go to infinity.

6.3 Proof of Lemma 4.4

We fix . We first notice that, since , the terminal condition can be written under the form with defined by

However, we cannot directly conclude from the -first order viability of that belongs to , since the terminal payoff function does not belong to . We therefore construct a sequence valued in approximating .

Since , we can write with and two elements of which are respectively non-negative and non-positive and satisfy .

For all , define the function by

where the function is defined by

and is defined by

for all . We then easily check that

for all . Therefore we get from the dominated convergence theorem that

| (6.7) |

Observe that and is valued in , for all . Since the PDE is first order viable for , we deduce from Proposition 4.1 that

| (6.8) |

where is the solution on of the BSDE (4.2) associated to the terminal condition .

We get from (6.7) and classical estimates on BSDEs that

Since is closed, (6.8) together with the previous convergence imply that is valued in .

References

- [1] Bensoussan A., N. Touzi and J. Menaldi (2005), Penalty approximation and analytical characterization of the problem of super-replication under portfolio constraints, Asymptotic Analysis, 41, 311-330.

- [2] Bouchard B. (2010) Portfolio management under risk contraints. Lectures given at MITACS-PIMS-UBC Summer School in Risk Management and Risk Sharing. http://arxiv.org/abs/1307.0230

- [3] Bouchard, B. and J.-F. Chassagneux (2008) Discrete-time approximation for continuously and discretely reflected BSDEs. Stochastic Processes and their Applications, 118(4), 2269-2293.

- [4] Broadie M., J. Cvitanic and M. Soner (1998), Optimal replication of contingent claims under portfolio constraints, Review of Financial Studies, 11(1), 59-79.

- [5] Buckdahn R., Quincampoix M. and A. Rascanu (2000), Viability property for a backward stochastic differential equation and application to partial differential equations, Probab. Theory. Relat. Fields, 116, 485-504.

- [6] Cheridito, P., H.M. Soner and N. Touzi (2005) The multi-dimensional super-replication problem under gamma constraints Annales de l’Institut Henri Poincaré (C), 22, 632-666.

- [7] Cvitanic J. and I. Karatzas (1993), Hedging Contingent Claims with Constrained Portfolios, The Annals of Applied Probability, 3(3), 652-681.

- [8] Cvitanic J., I. Karatzas and M. Soner (1998), Backward Stochastic Differential Equations with Constraints on the Gains-Process, The Annals of Probability, 26(4), 1522-1551.

- [9] Cvitanic J., H. Pham and N. Touzi (1999), Super-Replication in Stochastic Volatility Models under Portfolio Constraints, Journal of Applied Probability, 36(2), 523-545.

- [10] Gobet E. (2004) Revisiting the Greeks for European and American options, Proceedings of the "International Symposium on Stochastic Processes and Mathematical Finance" at Ritsumeikan University, Kusatsu, Japan, March 2003. Edited by J. Akahori, S. Ogawa, S. Watanabe. World Scientific, pp.53-71.

- [11] El Karoui N., M. Jeanblanc, S. Shreve (1998), Robustnes of the Black Scholes formula Mathematical finance, 8(2), 93-126.

- [12] El Karoui N., S. Peng, M.C. Quenez (1997), Backward Stochastic Differential Equation in finance Mathematical finance, 7(1), 1-71.

- [13] Karatzas I. and S. Kou (1996), On the pricing of contingent claims under constraints, The Annals of Applied Probability, 6(2), 321-369.

- [14] Ma, J. and J. Zhang (2002) Representation theorems for backward stochastic differential equations. The Annals of Applied Probability, 12(4), 1390-1418.

- [15] McMullen P. (1974), On the inner parallel body of a convex body, Israel Journal of Mathematics, 19(3), 217-219.

- [16] Pardoux E. and S. Peng (1992), Backward stochastic differential equations and quasilinear parabolic partial differential equations, Lecture Notes in Control and Information Sciences, 172, 200-217.

- [17] Pham H. (2009), Continuous-time Stochastic Control and Optimization with Financial Applications, Stochastic Modeling and Applied Probability, Springer, 61.

- [18] Rockafellar R. (1996), Convex Analysis, Cambridge university press.

- [19] Soner M. and N. Touzi (2003), The problem of super-replication under constraints, Paris-Princeton Lectures on Mathematical Finance, Lecture Notes in Mathematics, 1814, 133-172.