Online Convex Optimization in

Dynamic Environments

Abstract

High-velocity streams of high-dimensional data pose significant “big data” analysis challenges across a range of applications and settings. Online learning and online convex programming play a significant role in the rapid recovery of important or anomalous information from these large datastreams. While recent advances in online learning have led to novel and rapidly converging algorithms, these methods are unable to adapt to nonstationary environments arising in real-world problems. This paper describes a dynamic mirror descent framework which addresses this challenge, yielding low theoretical regret bounds and accurate, adaptive, and computationally efficient algorithms which are applicable to broad classes of problems. The methods are capable of learning and adapting to an underlying and possibly time-varying dynamical model. Empirical results in the context of dynamic texture analysis, solar flare detection, sequential compressed sensing of a dynamic scene, traffic surveillance,tracking self-exciting point processes and network behavior in the Enron email corpus support the core theoretical findings.

1 Introduction

Modern sensors are collecting very high-dimensional data at unprecedented rates, often from platforms with limited processing power. These large datasets allow scientists and analysts to consider richer physical models with larger numbers of variables, and thereby have the potential to provide new insights into the underlying complex phenomena. For example, the Large Hadron Collider (LHC) at CERN “generates so much data that scientists must discard the overwhelming majority of it – hoping hard they’ve not thrown away anything useful.” [2] Typical NASA missions collect hundreds of terabytes of data every hour [3]: the Solar Data Observatory generates 1.5 terabytes of data daily [4], and the upcoming Square Kilometer Array (SKA, [5]) is projected to generate an exabyte of data daily, “more than twice the information sent around the internet on a daily basis and 100 times more information than the LHC produces” [6]. In these and a variety of other science and engineering settings, there is a pressing need to recover relevant or anomalous information accurately and efficiently from a high-dimensional, high-velocity data stream.

Rigorous analysis of such data poses major issues, however. First, we are faced with the notorious “curse of dimensionality”, which states that the number of observations required for accurate inference in a stationary environment grows exponentially with the dimensionality of each observation. This requirement is often unsatisfied even in so-called “big data” settings, as the underlying environment varies over time in many applications. Furthermore, any viable method for processing massive data must be able to scale well to high data dimensions with limited memory and computational resources. Finally, in a variety of large-scale streaming data problems, ranging from motion imagery formation to network analysis, the underlying environment is dynamic yet predictable, but many general-purpose and computationally efficient methods for processing streaming data lack a principaled mechanism for incorporating dynamical models. Thus a fundamental mathematical and statistical challenge is accurate and efficient tracking of dynamic environments with high-dimensional streaming data.

Classical stochastic gradient descent methods, including the least mean squares (LMS) or recursive least squares (RLS) algorithms do not have a natural mechanism for incorporating dynamics. Classical stochastic filtering methods such as Kalman or particle filters or Bayesian updates [7] readily exploit dynamical models for effective prediction and tracking performance. However, these methods are also limited in their applicability because (a) they typically assume an accurate, fully known dynamical model and (b) they rely on strong assumptions regarding a generative model of the observations. Some techniques have been proposed to learn the dynamics [8, 9], but the underlying model still places heavy restrictions on the nature of the data. Performance analysis of these methods usually does not address the impact of “model mismatch”, where the generative models are incorrectly specified.

A contrasting class of prediction methods, receiving widespread recent attention within the machine learning community, is based on an “individual sequence” or “universal prediction” [10] perspective; these strive to perform provably well on any individual observation sequence without assuming a generative model of the data.

Online convex programming provides a variety of tools for sequential universal prediction [11, 12, 13, 14]. Here, a Forecaster measures its predictive performance according to a convex loss function, and with each new observation it computes the negative gradient of the loss and shifts its prediction in that direction. Stochastic gradient descent methods stem from similar principles and have been studied for decades, but recent technical breakthroughs allow these approaches to be understood without strong stochastic assumptions on the data, even in adversarial settings, leading to more efficient and rapidly converging algorithms in many settings.

This paper describes a novel framework for prediction in the individual sequence setting which incorporates dynamical models – effectively a novel combination of state updating from stochastic filter theory and online convex optimization from universal prediction. We establish tracking regret bounds for our proposed algorithm, Dynamic Mirror Descent (DMD), which characterize how well we perform relative to some alternative approach (e.g., a computationally intractable batch algorithm) operating on the same data to generate its own predictions, called a “comparator sequence.” Our novel regret bounds scale with the deviation of this comparator sequence from a dynamical model. These bounds simplify to previously shown bounds when there are no dynamics. In addition, we describe methods based on DMD for adapting to the best dynamical model from either a finite or parametric class of candidate models. In these settings, we establish tracking regret bounds which scale with the deviation of a comparator sequence from the best sequence of dynamical models.

While our methods and theory apply in a broad range of settings, we are particularly interested in the setting where the dimensionality of the parameter to be estimated is very high. In this regime, the incorporation of both dynamical models and sparsity regularization plays a key role. With this in mind, we focus on a class of methods which incorporate regularization as well as dynamical modeling. The role of regularization, particularly sparsity regularization, is increasingly well understood in batch settings and has resulted in significant gains in ill-posed and data-starved settings [15, 16, 17, 18]. More recent work has examined the role of sparsity in online methods such as recursive least squares (RLS) algorithms, but do not account for dynamic environments [19].

1.1 Organization of paper and main contributions

The remainder of this paper is structured as follows. In Section 2, we formulate the problem and introduce notation used throughout the paper, and Section 3 introduces the Dynamic Mirror Descent (DMD) method, and gives brief comparison to existing methods. along with novel tracking regret bounds. This section also describes the application of data-dependent dynamical models and their connection to recent work on online learning with predictable sequences. DMD uses only a single series of dynamical models, but we can use it to choose among a family of candidate dynamical models. This is described for finite families in Section 4 using a fixed share algorithm, and for parametric families in Section 5. Section 6 shows experimental results of our methods in a variety of contexts ranging from imaging to self-exciting point processes. Finally, Section 7 makes concluding remarks while proofs are relegated to Section A.

2 Problem formulation

The problem of sequential prediction is posed as an iterative game between a Forecaster and the Environment. At every time point, , the Forecaster generates a prediction from a bounded, closed, convex set . After the Forecaster makes a prediction, the Environment reveals the loss function where is a convex function which maps the space to the real number line. We will assume that the loss function is the composition of a convex function from the Environment and a convex regularization function which does not change over time. Frequently the loss function, will measure the accuracy of a prediction compared to some new data point where is the domain of possible observations. The regularization function promotes low-dimensional structure (such as sparsity) within the predictions. We additionally assume that we can compute a subgradient of or at any point , which we denote and . Thus the Forecaster incurs the loss .

The goal of the Forecaster is to create a sequence of predictions that has a low cumulative loss . Because the loss functions are being revealed sequentially, the prediction at each time can only be a function of all previously revealed losses to ensure causality. Thus, the task facing the Forecaster is to create a new prediction, , based on the previous prediction and the new loss function , with the goal of minimizing loss at the next time step. We characterize the efficacy of relative to a comparator sequence using a concept called regret, which measures the difference of the total accumulated loss of the Forecaster with the total accumulated loss of the comparator:

Definition 1 (Regret)

The regret of with respect to a comparator is

Notice that this definition of regret is very general and simply measures the performance of an algorithm versus an arbitrary sequence . We are particularly interested in comparators which correspond to the output of a batch algorithm (with access to all the data simultaneously) that is too computationally complex or memory-intensive for practical big data analysis problems. In this sense, regret encapsulates how much one regrets working in an online setting as opposed to a batch setting with full knowledge of past and future observations.

Much of the online learning literature is focused on algorithms with guaranteed sublinear regret (e.g., ) in the special case where the comparator is constrained so that . Unfortunately, this is a highly unrealistic constraint in most practical streaming big data settings. The parameters could correspond to frames in a video or the weights of edges in a dynamic network and by nature are highly variable.

This paper focuses more generally on arbitrary comparator sequences and shows how the regret scales as a function of the temporal variability in that comparator. This idea is typically referred to as “tracking” or “shifting” regret [20, 21], which is closely-related to “adaptive” regret [22, 23]. Existing methods guarantee sublinear regret for all which do not vary at all over time, or which change only at a few discrete points in time, or which only vary extremely slowly over time; generally, these regret bounds depend linearly on a variation term of the form

sublinear regret is only possible for comparator sequences for which this variation is small. In contrast, the proposed methods in this paper guarantee sublinear regret for different classes of that allow quite large temporal variability.

3 Dynamic Mirror Descent

To begin, we propose a simple modification to the “mirror descent” online learning paradigm. Specifcally, we incorporate a dynamical model at each time ; this approach is called dynamic mirror descent (DMD). For now, we assume is fixed and known. For example,

-

•

Streaming observations correspond to (potentially distorted) frames in a video sequence, corresponds to a set of wavelet coefficients for that frame, and corresponds to a video motion model at time .

-

•

Streaming observations correspond to interactions within a social network, corresponds the likelihood of each pair of people interacting at time , and captures diurnal patterns and social network evolution models.

-

•

Streaming observations correspond to the price of stocks, parameterizes a probability distribution governing stock prices, and captures underlying autoregressive behavior and side information derived from other financial instruments.

In all of these settings, it is possible to posit a dynamical model based on prior knowledge of the application, akin to developing a state space model for stochastic filters.

| (1a) | ||||

| (1b) | ||||

The DMD algorithm is presented in Algorithm 1. In this algorithm denotes an arbitrary subgradient of at , is the Bregman divergence [24, 25] which measures the distance between and , and is a step size parameter.

We may compare the DMD approach with classical online learning methods [11, 22, 13, 12] and more recent reguarlized formulations [26, 27, 28]. For instance, mirror descent (MD, [11, 12]) sets

| (2) |

and Composite Objective Mirror Descent (COMID111The COMID formulation is helpful when the regularization function promotes sparsity in , and helps ensure that is indeed sparse., [26]) sets

| (3) |

Specifically, note that if is the identity operator for all , so that for all and , then DMD corresponds exactly to COMID.

Methods like MD and COMID have sublinear regret bounds only for comparators with small , such as when for some and all . In contrast, our method is an algorithm which incorporates a dynamical model, denoted , and admits a tracking regret bound of the form (shown in the next section).

By including in the process, we effectively search for a predictor which (a) attempts to minimize the loss and (b) which adheres to the dynamical model . The DMD approach effectively includes dynamics into the COMID framework.222Rather than considering COMID, we might have used other online optimization algorithms, such as the Regularized Dual Averaging (RDA) method [27], which has been shown to achieve similar performance with more regularized solutions. However, to the best of our knowledge, no tracking or shifting regret bounds have been derived for dual averaging methods (regularized or otherwise). Recent results on the equivalence of COMID and RDA [29] suggest that the bounds derived here might also hold for a variant of RDA, but proving this remains an open problem.

The important feature of Alg. 1 is Equation 1b, where the predetermined function is incorporated in the learning process. The main intuition is that instead of believing the next loss function is well approximated by all the previous loss functions as in MD and COMID, we are instead assuming the loss functions will be well predicted by the trajectory encoded by the functions . This results in changing the class of comparators which lead to sublinear regret bounds. MD and COMID have sublinear regret when the comparator is static or changes very slowly. However, as we will show, DMD yields sublinear regret when the comparator evolves according to the functions or only deviates from these functions by a small amount, meaning is small. Thus, while the class of that has low regret may be the same size as with MD or COMID, the classes contain very different comparator sequences. In later sections we will address how to learn the sequence from the data. Additionally, we make no assumption about whether the data actually follow these dynamics, but instead we derive a regret bound which scales with how well the comparator evolves according to these functions.

3.1 Tracking regret of DMD

Our main result uses the following assumptions:

-

•

Let denote a continuously differentiable function that is -strongly convex for some parameter and some norm

-

•

The Bregman Divergence used in our algorithm is defined as . Because is -strongly convex we have

(4) Additionally, the definition of the Bregman Divergence implies the following relationship: for all

(5) -

•

For all the functions and are Lipschitz with constants and respectively, such that and for all . The function used in these assumptions is the dual to the norm that is strongly convex with respect to.

-

•

There exists a constant such that for all .

-

•

For all , the transformation has a maximum distortion factor such that for all . When for all , we say that satisfies the contractive property.

Theorem 2 (Tracking regret of dynamic mirror descent)

Let be a dynamical model such that for with respect to the Bregman divergence used in 1. Let the sequence be generated using Alg. 1 using a non-increasing series , with a convex, Lipschitz function on a closed, convex, bounded set , and let be an arbitrary sequence in . Then

where measures variations or deviations of the comparator sequence from the sequence of dynamical models . If or , then for some independent of ,

This bound scales with the comparator sequence’s deviation from the sequence of dynamical models – a stark contrast to previous tracking regret bounds which are only sublinear for comparators which change slowly with time or at a small number of distinct time instances. Note that when corresponds to an identity operator, the bound in Theorem 2 corresponds to existing tracking or shifting regret bounds [14, 21].

It is intuitively satisfying that this measure of variation, , appears in the tracking regret bound. First, if the comparator sequence evolves approximately like , this variation term will be very small, leading to low regret. This fact holds whether is part of the generative model for the observations or not. Secondly, we can get a dynamic analog of static regret, where we enforce . This is equivalent to saying that the batch comparator is fitting the best single trajectory using instead of the best single point. Using this, we would recover a bound analogous to a static regret bound in a stationary setting.

The condition that is similar to requiring that be a contractive mapping. This restriction is important; without it, any poor prediction made at one time step could be exacerbated by repeated application of the dynamics. For instance, linear dynamic models with all eigenvalues less than or equal to unity satisfy this condition with respect to the squared Bregman Divergence, similar in spirit to restrictions made in more classical adaptive filtering work such as [30]. Notice also that if in for all , then Theorem 2 gives a novel, previously unknown tracking regret bound for COMID.

3.2 Data-dependent dynamics

An interesting example of dynamical models is the class of data-dependent dynamical models. In this regime the state of the system at a given time is not only a function of the previous state, but also the actual observations. One key example of this scenario arises in self-exciting point processes, where the state of the system is directly related to the previous observations. Our algorithm can account for such models since the function is time varying, and therefore can implicitly depend on all data up to time , i.e. . Our regret bounds therefore scale with how well the comparator series matches these data dependent dynamics:

Notice now that the data plays a part in the regret bounds, whereas before we only measured the variation of the comparator. Data-dependent regret bounds are not new. Concurrent related work considers online algorithms where the data sequence is described by a “predictable process” [31]. The basic idea of that paper is that if one has a sequence of functions which predict based on , then the output of a standard online optimization routine should be combined with the predictor generated by to yield tighter regret bounds that scale with . However, [31] only works with static regret (i.e., regret with respect to a static comparator) and their regret has a variation term that expresses the deviation of the input data from the underlying process. In contrast, our tracking regret bounds scale with the deviation of a comparator sequence from a prediction model.

4 Prediction with a finite family of dynamical models

DMD in the previous section uses a single sequence of dynamical models. In practice, however, we may not know the best dynamical model to use, or the best model may change over time in nonstationary environments. To address this challenge, we assume a finite set of candidate dynamical models at every time , and describe a procedure which uses this collection to adapt to nonstationarities in the environment. In particular we establish tracking regret bounds which scale not with the deviation of a comparator from a single dynamical model, but with how it deviates from a series of different dynamical models on different time intervals with at most switches. These switches define different time segments with time points . We can bound the regret associated with the best dynamical model on each time segment and then bound the overall regret using a Prediction with Experts Advice algorithm.

Our dynamic fixed share (DFS) estimate is presented in Algorithm 2. Let denote the output of Equation 1b at time using dynamical models ; we choose by using the Fixed Share forecaster on these outputs.333There are many algorithms from the Prediction with Expert Advice literature which can be used to form a single prediction from the predictions created by the set of dynamical models. We use the Fixed Share algorithm [32] as a means to combine estimates with different dynamics; however, other methods could be used with various tradeoffs. One of the primary drawbacks of the Fixed Share algorithm is that an upper bound on the number of switches must be known a priori. However, this method has a simple implementation and tracking regret bounds. One common alternative to Fixed Share allows the switching parameter ( in Alg. 2) to decrease to zero as the algorithm runs [33, 34]. This has the benefit of not requiring knowledge about the number of switches, but comes at the price of higher regret. Alternative expert advice algorithms exist which decrease the regret but increase the computational complexity. For a thorough treatment of existing methods see [35]. In Fixed Share, each expert (here, each sequence of candidate dynamical models) is assigned a weight that is inversely proportional to its cumulative loss at that point yet with some weight shared amongst all the experts. Here there is amount of weight divided evenly amongst experts so that an expert with previously high loss quickly regain enough weight to become the leader [32, 21]. In this update, is how much of the weight is shared amongst the experts. Notice each expert “donates” a fraction of it’s weight which is then replaced by . For experts which large weights this will cause some weight to be lost, but ensures that a minimum weight of is attained for each expert. Sharing weight allows fast switching between experts.

Theorem 3 (Tracking regret of DFS algorithm)

Assume all the candidate dynamic sequences are contractive such that for for all and with respect to the Bregman divergence in Alg 1. Then for some , the dynamic fixed share algorithm in Algorithm 2 with parameter set equal to , and or with a convex, Lipschitz function on a closed, bounded, convex set , has tracking regret

where

measures the deviation of the sequence from the best sequence of dynamical models with at most switches (where does not depend on ).

The choice of is important, as low values of will have low regret but for a smaller class of comparators, comparators with a small number of switches. Oppositely, larger values of will have low regret for a larger class of comparators, but there is an overhead to be paid in the constant terms. Note that the family of comparator sequences for which scales sublinearly in is significantly larger than the set of comparators yielding sublinear regret for MD. This is because for any fixed , thus this approach yields a lower variation term than using a fixed dynamical model. However, we incur some loss by not knowing the optimal number of switches or when the optimal switching times are.

5 Parametric dynamical models

Rather than having a finite family of dynamical models, as we did in Section 4, we may consider a parametric family of dynamical models, where the parameter of is allowed to vary across a closed, bounded, convex domain, denoted . In other words, we consider . In this context we would like to jointly predict both and .

We consider two approaches. First, in Section 5.1 we consider tracking only a finite subset of the possible model parameters, in a manner similar to when we had a finite collection of possible dynamical models, which provide a “covering” of the parameter space. In this case, the overall regret and computational complexity both depend on the resolution of the covering set. Second, in Section 5.2, we consider a special family of additive dynamical models; in this setting, we can efficiently learn the optimal dynamics.

5.1 Covering the set of dynamical models

In this section we show that by tracking a subset which appropriately covers the entire space of candidate models, we can bound the overall regret, as well as bound the number of parameter values we have to track, and the inherent tradeoff between the two. We propose to choose a finite collection of parameters from a closed, convex set and perform DFS (Alg. 2) on this collection. We specifically consider the case where the true dynamical model is unchanging in time and use DFS with . (Fixed share with amounts to the Exponentially Weighted Averaging Forecaster [36, 22, 14].) In the below, for any , let

Theorem 4 (Covering sets of dynamics parameter space)

Let and denote a covering set for with cardinality , such that for every , there is some such that . Define candidate dynamical models as for and assume they are all contractive with respect to the Bregman Divergence used in Alg. 1. If for some for all , then for some constant , the Alg 2 with yields a tracking regret bounded by

Intuitively, we know that if we set to be very small we will have good performance because any possible parameter value would have to be close to a candidate dynamic; however, we would need to choose many candidates. Conversely, if we run DFS on only a few candidate models, it will be computationally much more efficient but our total regret will grow due to parameter mismatch.

Corollary 5

Assume , and let be given. Let and ; let correspond to an -dimensional grid with grid points over . Then

Additionally, the total number of grid points is upper bounded by

Under the assumptions of Theorem 4, with this set and using the fact that norms are equivalent on finite-dimensional vectors (i.e., there’s a finite such that for any for any norm), we get the following bound on regret for some constant .

Here we have an explicit tradeoff between regret and computationally accuracy controlled by , since the computational complexity is linear in .

We can further control the tradeoff between computation complexity and performance by allowing to vary in time. This could be done by using the doubling trick, setting temporary time horizons, and then refining the grid once the temporary time horizon is reached using a slightly different experts algorithm which could account for the changing number of experts as in [37].

5.2 Additive dynamics in exponential families

The approach described above for generating a covering set of dynamical models may be effective when the dimension of parameters is small; however, in higher dimensions, this approach can require significant computational resources. In this section, we consider an alternative approach that only requires the computation of predictions for a single dynamical model. We will see that in some settings, the prediction produced by Dynamic Mirror Descent (DMD) and a certain set of parameters for the dynamic model can quickly be converted to the prediction for a different set of parameters. While the method described in this section is efficient and admits strong regrets bounds, it is applicable only for loss functions derived from exponential families.

The basics of exponential families are described in [38, 39], and Mirror Descent in this setting is explored in [40, 41]. We assume some which is a measurable function of the data, and let , , denote its components:

We use the specific loss function

| (6a) | |||

| where | |||

| (6b) | |||

for a sufficient statistic and , known as the log-partition function, ensures that integrates to a constant independent of . Furthermore, as in [40, 41], we use the Bregman divergence corresponding to the Kullback-Leibler divergence between two members of the exponential family:

In our analysis we will be using the Legendre–Fenchel dual of [42, 43]:

Let denote the image of under the gradient mapping i.e. . An important fact is that the gradient mappings and are inverses of one another [12, 14, 44]:

Following [14], we may refer to the points in as the primal points and to their images under as the dual points. For simplicity of notation, in the sequel we will write , , , etc.

Additionally, we will use a dynamical model that takes on a specific form:

| (7) |

for , , , and . and are considered known. This dynamical model encompasses some important scenarios. For instance if the log-partition function is the regular function, this model includes all dynamics in the form of , which is akin to an autoregressive moving average model as in Section 6.5. These types of models could also be used to push estimates towards a known temporal structure, e.g. a diurnal pattern with unknown amplitude as in Section 6.6. Additionally, could encode additional side information. Using these dynamics, we let denote the output of DMD (Alg. 1) at time and be its dual. Under all these conditions, we have the following Lemma.

Lemma 6

For any , let be the duals of the initial prediction for DMD and . Additionally assume that the minimizer of equation 1a is a point in for any parameter . Then the DMD prediction under a dynamical model parameterized by can be calculated directly from the DMD prediction under a dynamical model parameterized by for as

From Lemma 6, we see that the prediction for dynamical model can be computed simply from the prediction using parameters and the value . This is a significant computational gain compared to DFS, where we had to keep track of predictions for each candidate dynamical model individually and therefore needed to bound the number of experts for tractability.

Algorithm 3 leverages Lemma 6 to simultaneously track both and the best dynamical model parameter . In this algorithm, is the function defined as

The basic idea is the following: we use Stochastic Gradient Descent to compute an estimate of the best dynamical model parameter, compute the DMD prediction associated with that parameter, and then use DMD to update that prediction for the next round.

Theorem 7

Assume that the observation space is bounded. Let be a bounded, convex set satisfying the following properties for a given constant :

-

•

For all ,

-

•

For all ,

-

•

Let denote the objective function in (1a). For every and , the solution to occurs where .

If the assumptions of Lemma 6 hold, and is contractive for all with respect to the Bregman Divergence induced by , the loss function is of the form (6) and is convex in , and or , then the regret for any comparator sequence associated with Algorithm 3 for dynamical models of the form (7) is

for some constant .

The condition that is convex is a sufficient condition to ensure that is convex, which we need in order to search for the optimal value of . While this may not hold true for all exponential family distributions, it holds for many common choices such as Gaussian, Poisson, Binomial, Exponential and many others. Theorem 7 shows that Algorithm 3 allows us to simultaneously track predictions and dynamics, and we perform nearly as well as if we knew the best dynamical models for the entire sequence in hindsight. While this approach is only applicable for specific forms of the loss functions and dynamical models, those forms arise in a wide variety of practical problems. Additionally, this methods allows for a much larger class of comparators which would yield sublinear regret. In fact, we now have an algorithm with sublinear regret for any class of comparators which has a low variation term for any value .

6 Experiments and results

As mentioned in the introduction, many online learning problems can benefit from the incorporation of dynamical models. In this section, we describe how the ideas described and analyzed in this paper might be applied to many different settings.

6.1 DMD experiment: dynamic textures with missing data

As mentioned in the introduction, sensors such as the Solar Data Observatory are generating data at unprecedented rates. Heliophysicists have physical models of solar dynamics, and often wish to identify portions of the incoming data which are inconsistent with their models. This “data thinning” process is an essential element of many big data analysis problems. We simulate an analogus situation in this section.

In particular, we consider a datastream corresponding to a dynamic texture [45][46] , where spatio-temporal dynamics within motion imagery are modeled using an autoregressive process. In this experiment, we consider a setting where “normal” autoregressive parameters are known, and we use these within DMD to track a scene from noisy image sequences with missing elements. (Missing elements arise in our motivating solar astronomy application, for instance, when cosmic rays interfere with the imaging detector array.) As suggested by our theory, the tracking will fail and generate very large losses when the posited dynamical model is inaccurate.

More specifically, the idea of dynamic textures is that a low dimensional, auto-regressive model can be used to simulate a video which replicates a moving texture such as flowing water, swirling fog, solar plasma flows, or rising smoke. This process is modeled in the following way:

In the above, denotes the true underlying parameters of the system, and the observations. The matrix is the autoregressive parameters of the system, which will be unique for the type of texture desired, the average background intensity, is the sensing matrix which is usually a tall matrix, and and encode the strength of the driving and observation noises respectively. Using the toolbox developed in [47] and samples of a 220 by 320 pixel ocean scene [46], we learned two sets of parameters , one representing the water flowing when the data is played forward, and the other when played backwards, as well as corresponding parameters and . Parameters and data were then generated using these parameters, with the parameters and on and and the parameters on the rest of according to the above equations. Finally, every observation is corrupted by 50% missing values, chosen uniformly at random at every time point.

The parameters , , and were then used to define our (imperfect) dynamical model for DMD, , and a loss function , where is a linear operator accounting for the missing data. Note that and are not reflected in these choices despite playing a role in generating the data; our theoretical results hold regardless. We use so the Bregman Divergence is the usual squared Euclidean distance, and we perform no regularization (). We set , and ran 100 different trials comparing the DMD method to regular Mirror Descent (MD) to see the advantage of accounting for underlying dynamics. The results are shown in Figure 1.

There are a few important observations about this procedure. The first is that by incorporating the dynamic model, we produce an estimate which visually looks like the dynamic texture of interest, instead of the Mirror Descent prediction, which looks like a single snapshot of the water. Second, we can recover a good representation of the scene with a large amount of missing data, due to the autoregressive parameters being of a much lower dimension than the data itself. Finally, because we are using the dynamics of forward moving water, when the true data starts moving backward, a change that is imperceptible visually, the loss spikes, alerting us of the abnormal behavior.

6.2 DMD experiment: solar flare detection with missing data

We use DMD in order to detect solar flares in image sequences from the Solar Data Observatory, in the presence of missing data and camera jitter. Solar flares represent temporally short, and spatially localized bursts of activity of the solar scene, but can be hard to detect when there is larger motion, and only partial observations. By explicitly accounting for camera jitter, we can do a better job of predicting what the scene should look like, and therefore quickly observe when and where in the scene solar flares occur.

In order to run DMD we choose an loss function on the values of observed pixels

where is a function that preserves the value of the true scene at the observed locations and sets the value to 0 otherwise. We use Euclidean distance as our Bregman Divergence. The dynamical model, accounts for the camera jitter at time . For our experiment we chose to be a random pixel shift one pixel up, down, left or right. This scheme is run where each pixel is missing uniformly at random with probability 0.5. These results shown in Figure 2.

We can see in the loss plots that accounting for camera jitter with DMD explicitly we are less likely to get erroneous spikes in the loss function. This is important, because after the initial learning time, we can threshold the loss to detect anomalies as in [41], which would correspond to solar flares in this setting. However, if we don’t explicitly account for the camera jitter, the Mirror Descent loss plot has spikes that are of the same magnitude as the spikes corresponding to a solar flare, and therefore thresholding would lead to either many false positives or missed detections.

6.3 DFS experiment: compressive video reconstruction

There is increasing interest in using “big data” analysis techniques in applications like high-throughput microscopy, where scientists wish to image large collections of specimens. This work is facilitated by the development of novel microscopes, such as the recent fluorescence microscope based on structured illumination and compressed sensing principles [48]. However, measurements in such systems are acquired sequentially, posing significant challenges when imaging live specimens.

Knowledge of underlying motion in compressed sensing image sequences can allow for faster, more accurate reconstruction [49, 50, 51]. By accounting for the underlying motion in the image sequence, we can have an accurate prediction of the scene before receiving compressed measurements, and when the measurements are noisy and the number of observations is far less than the number of pixels of the scene, these predictions allow both fast and accurate reconstructions. If the dynamics are not accounted for, and previous observations are used as prior knowledge, the reconstruction could end up creating artifacts such as motion blur or overfitting to noise. There has been significant recent interest in using models of temporal structure to improve time series estimation from compressed sensing observations [52, 53]; the associated algorithms, however, are typically batch methods poorly suited to large quantities of streaming data. In this section we demonstrate that DMD helps bridge this gap.

In this section, we simulate fluorescence microscopy data generated by the system in [48] while imaging a paramecium moving in a 2-dimensional plane; the frame is denoted (a image stored as a length- vector) which takes values between 0 and 1. The corresponding observation is where is a matrix with each element drawn iid from and corresponds to measurement noise with with . This model coincides with several compressed sensing architectures [54, 48].

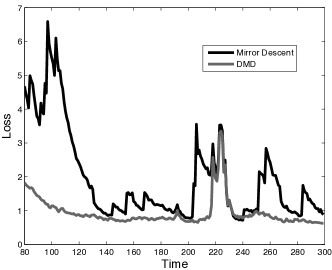

Our loss function uses and , where is a tuning parameter. We construct a family of dynamical models, where shifts the (unvectorized) frame, , one pixel in a direction corresponding to an angle of as well as a “dynamic” corresponding to no motion. (With the zero motion model, DMD reduces to COMID.) The true video sequence uses different dynamical models over (upward motion) and (motion to the right). Finally, we use so the Bregman Divergence is the usual squared Euclidean distance. The DMD sub-algorithms use and the DFS forecaster uses and is set as in Theorem 3. The experiment was then run 100 times.

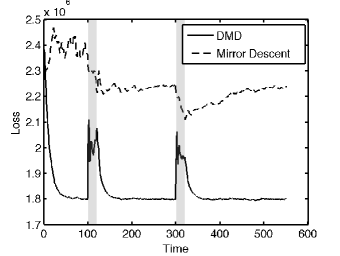

6.4 DFS experiment: downsampled traffic surveillance reconstruction

The DFS framework can also be used to reconstruct and predict traffic surveillance data by incorporating the approximately known traffic patterns into the estimation procedure. For a traffic scene with moving objects, one frame will only be informative for the next frame if the motion of the objects are incorporated into the prediction scheme and thus DFS can be used to improve the prediction process for this type of data. We used the Highway I video from the ATON shadow detection database (http://cvrr.ucsd.edu/aton/shadow/index.html) which contains 440 frames of 240 320 pixel images. The foreground of this video was then extracted using the inexact Augmented Lagrangian Multiplier method of [55]. This models the ability of a surveillance camera to do on-board pre-processing of data to remove long term background information and only transmit relevant, transient information. From here the image is blurred by a Gaussian kernel with width defined by , downsampled by a factor of 4 in both directions (for an overall downsampling factor of 16), and finally Gaussian white noise is added. The overall process can be described as follows:

where encodes the blurring operation and the downsampling, of the vectorized frame . The convolution is normalized such that to ensure signal strength is maintained. The white noise has standard deviation of 20. The Gaussian noise leads intuitively to using an data fit function and because we are estimating foreground objects with background removed we use regularization to induce sparsity. Combining these leads to the following loss function:

where is the dimension of and is the parameter which controls the relative amount of sparsity in the solution.

In order to implement DFS, we need a collection of feasible dynamics which can describe the data. The video shows cars moving generally from the top of the screen to the bottom at a relatively constant speed, so 5 different dynamical models are postulated which are simple row shifts of 10, 14, 18, 22 and 26 pixels respectively. One slightly more complicated dynamical model is also used which is based on a Block Matching Algorithm. For this dynamical model, a training set of the first 20 frames of the full data was used. The idea behind the Block Matching Algorithm is that for every block in a given frame, a search is done over the entire previous frame for the block which best matches. For our purposes, we define the values of a block in the image after applications of the dynamics, , to the be the values of the block in which most consistently predicted the block of interest in the original training set. This process is defined below, where represents the 240 320 images, and the subscripts denote the 8 8 block starting at location .

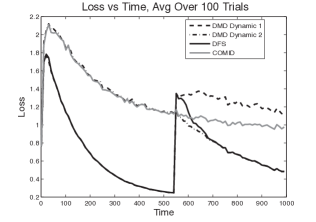

This map was then smoothed slightly to ensure that objects in one frame remained intact after the application of the dynamics and not distorted. This procedure produced a dynamical model which mostly showed downward motion, similar to the pixel shifts, but allowed for some horizontal motion as well as allowing slightly different velocities in different regions of the image. Overall this brings the number of candidate dynamical models to

Using this setup, DFS is implemented for the frames with and . The results are shown in Figure 5. We immediately see that COMID which does not account for dynamics performs very poorly and is easily outperformed even by the very simple pixel shift models (DMD Dynamic 1 in the plots corresponds to pixel shift of 18). Additionally we see that the block matching dynamic (DMD Dynamic 2) performs even better, and that the DFS algorithm quickly hones in on this dynamic model and follows it very closely.

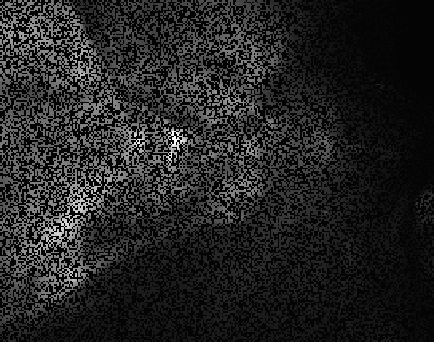

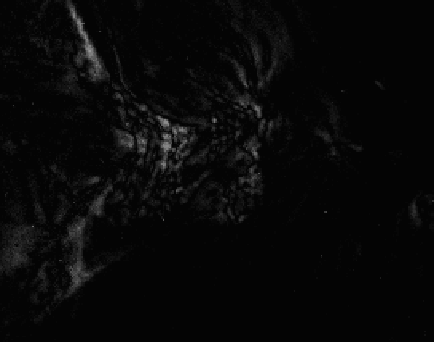

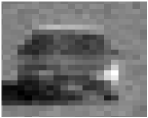

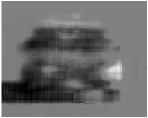

In addition to the loss plots, we can observe actual reconstructions to see how close DFS comes to approximating the true image. An example of one segment of one prediction is shown in Figure 6. We see how the DFS procedure effectively upsamples, deblurs and denoises the data. By incorporating the dynamics, we can much more effectively find the details in the image that is not possible by using just COMID. Additionally, we have revealed details unobservable in the raw data. For instance, notice the lighter shade object inside the car in The lighter shade is visible in the DFS reconstruction, while it is impossible to see in the data. Additionally, details such as shape and edges on the headlights and license plate are much clearer in the DFS reconstruction compared to the data.

6.5 DMD with parametric additive dynamics

We look at self-exciting point processes on connected networks [56, 57]. Here we assume there is an underlying rate for nodes in a network which dictate how likely each node is to participate in an action. Then, based on which nodes act, it will increase other nodes likelihood to act in a dynamic fashion. For example, in a social network a node could correspond to a person and an action could correspond to crime [58]. In a biological neural network, a node could correspond to a neuron and an action could correspond to a neural spike [59].

We simulate observations of a such a self-exciting point process in the following way:

For our experiments represents the average number of actions each of 100 nodes will make during time interval , and reflects the unknown underlying network structure which encodes how much an event by a one node will increase the likelihood of an event by another node in future time intervals. Here we assume is a known parameter between zero and one, is a underlying base event rate.

Our goal is to track the event rates and the network model simultaneously; Algorithm 3 is applied with

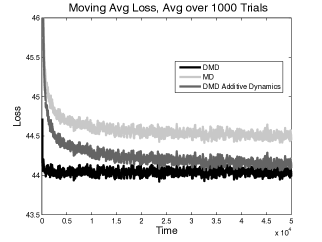

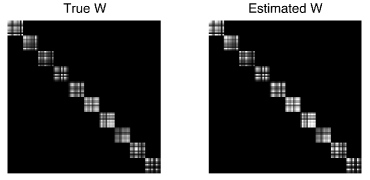

We generated data according to this model for for 1000 different trials, using and generated such that it is all zeros except on each distinct block along the diagonal, elements are chosen to be for a vector with elements chosen uniformly at random. The matrix is then normalized so that its spectral norm is for stability. Using this generated data we ran DMD with known (Alg. 1), MD, and DMD with additive dynamics (Alg. 3) to learn the dynamic rates. The step size parameters were set as and . The results are shown for DMD with the matrix known in advance, MD and Alg. 3 in Figure 7.

We again see several important characteristics in these plots. The first is that by incorporating knowledge of the dynamics, we incur significantly less loss than standard Mirror Descent. Secondly, we see that even without knowing what the values of the matrix , we can learn it simultaneously with the rate vectors from streaming data, and the resulting accurate estimate leads to low loss in the estimates of the rates.

6.6 DMD with parametric additive dynamics experiment - Enron email corpus

For our final set of experiments, we analyzed the Enron email corpus[60]. The goal of analyzing this dataset is to be able to read in the emails in a streaming fashion, and be able to detect anomalous moments, and determine if they align with important known events in the company’s history. In order to do this, the approximately 500,000 emails were combined into 1 hour time bins for each of the 150 given employees, from December 16th 2000 until January 1st 2003. For each employee for each hour, we receive an indicator saying whether that employee sent or received an email at that specific hour.

We model the indicator values as a Bernoulli random variable for each employee for each hour, and want to learn the probability that each employee will send or receive an email at a given time. Given an estimate and the actual observations at time , we have the following loss function

which can be rewritten as

under the transformation . This formulation gives us the primal () and dual () variables and loss functions necessary for DMD with parametric additive dynamics algorithm described in Alg. 3.

In order to use Alg. 3 on this data set we need to postulate a sequence of dynamics, and this dataset lends itself to several possibilities. The first possibility is to search for possible relationships in the network that might effect a person’s likelihood to send or receive and email. For this we consider the following dynamic model:

This dynamic model might look a little bit strange at first, but when used in Alg. 3 we are left with the overall update equation of the form

where we can search for over the space . This update equation shows that we not only update our estimate of an individual’s likelihood of sending or receiving an email based on their previous history, but also the history of people they might be associated with in the network. For instance, if someone is working closely with another employee, they will be more likely to respond quickly to that person’s email as opposed to someone who works in another department.

The next two dynamical models attempt to incorporate the weekly cycles in email sending behavior. The first dynamical model incorporates a weighted average over each employee’s behavior at corresponding hours in previous weeks to predict their behavior at the current moment, and the second model incorporates a weighted average of the entire company’s behavior in previous weeks. The first model uses the following function:

where corresponds to the amount of time backwards we wish to look, in this case hours, and is how many of these periods back we wish to look. This leads to the total update equation

where we can use Alg 3 to search for optimal values of over the dimensional simplex. A similar dynamical model leads to the final update equation

which uses the same mechanism for incorporating weekly patterns, but considers the company-wide information from the previous weeks, instead of the employee specific information. Once again our algorithm allows us to use this update equation while searching for optimal values of over the dimensional simplex. For our experiments, we considered =20.

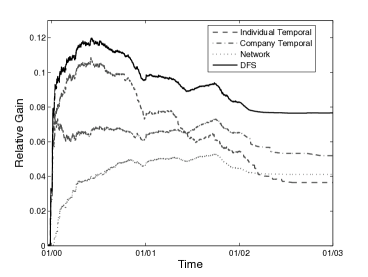

Using this loss function and dynamical models, Alg. 3 was used to predict each employees probability of sending or receiving an email for every hour in the given time range. The DMD step size was set as , where is the total number of hours observed. Additionally, the step sizes were set at for the network dynamics, and for the temporal behavior dynamics. In addition to these three models, we also used Alg. 2 to assign weights to each of these methods, and regular Mirror Descent, to create one combined prediction. We compared the performance of each of these methods to Mirror Descent, and calculated the relative gain through time as , where corresponds to the prediction made by Mirror Descent. These results are shown in Figure 8.

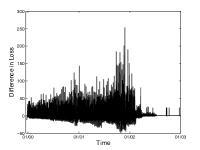

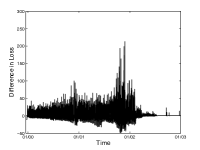

Immediately we see that all of the proposed dynamic models improve the our predictive power compared to Mirror Descent. Including individual employees weekly email behavior has the biggest single impact, followed by the company’s weekly behavior, and finally the network dynamics. When all three are combined using fixed share, we attain a performance boost of about 8% in the end, and 12% at its peak. Additionally, our method can more accurately detect anomalies. One heuristic for determining anomalies would be to compare a method’s instantaneous loss to the average loss for the preceding week. High spikes would then correspond to anomalous moments. This value is shown in Figure 9 for Mirror Descent and our DFS method. We see that our method does a better job of finding the spikes in December 2000 and December 2001, corresponding to true anomalies, as the spikes stick out more from the noise around them. In December 2000 energy commodity trading became deregulated in California [61] and in December 2001 Enron filed for Chapter 11 [62].

7 Conclusions and future directions

Processing high-velocity streams of high-dimensional data is a central challenge to big data analysis. Scientists and engineers continue to develop sensors capable of generating large quantities of data, but often only a small fraction of that data is carefully examined or analyzed. Fast algorithms for sifting through such data can help analysts track dynamic environments and identify important subsets of the data which are inconsistent with past observations.

In this paper we have proposed a novel online optimization method, called Dynamic Mirror Descent (DMD), which incorporates dynamical models into the prediction process and yields low regret bounds for broad classes of comparator sequences. The proposed methods are applicable for a wide variety of observation models, noise distributions, and dynamical models. There is no assumption within our analysis that there is a “true” known underlying dynamical model, or that the best dynamical model is unchanging with time. The proposed Dynamic Fixed Share (DFS) algorithm adaptively selects the most promising dynamical model from a family of candidates at each time step. Additionally we show methods which learn in parametric families of dynamical models. In experiments DMD shows strong tracking behavior even when underlying dynamical models are switching, in such applications as dynamic texture analysis, compressive video, and self-exciting point process analysis.

Appendix A Proofs

A.1 Proof of Theorem 2

The proof of Theorem 2 shares some ideas with the tracking regret bounds of [13], but uses properties of the Bregman Divergence to eliminate some terms, while additionally incorporating dynamics. We employ the following lemma.

Lemma 8

Let the sequence be as in Alg. 1, and let be an arbitrary sequence in ; then

Proof of Lemma 8: The optimality condition of (1a) implies

| (8) |

The proof has a similar structure to that in [26]

| (9a) | ||||

| (9b) | ||||

| (9c) | ||||

| (9d) | ||||

| (9e) | ||||

| (9f) | ||||

where (9c) follows from the convexity of and , (9e) follows from the optimality condition in (1a), and (9f) follows from (5). Each of these terms can be bounded individually, and then recombined to complete the proof.

| (10a) | ||||

| (10b) | ||||

| (10c) | ||||

| (10d) | ||||

| (10e) | ||||

| (10f) | ||||

| (10g) | ||||

where (10b) is due to the convexity of and (10c) is from the Cauchy-Schwarz inequality. Additionally, (10f) is due to (4) and (10g) uses Young’s Inequality [63, Prob 9.1] which states . Combining these inequalities with (9) gives the lemma as it is stated.

The proof of the theorem concludes by summing the bounds of Lemma 8 over time. Denote and . Remember, we have assumed that .

A.2 Proof of Theorem 3

The tracking regret can be decomposed as:

| (11) |

where the minimization in the second term of and first term of is with respect to sequences of dynamical models with at most switches, such that . In (11), corresponds to the tracking regret of our algorithm relative to the best sequence of dynamical models within the DMD framework, and is the regret of that sequence relative to the best comparator in the class . We use Corollary 3 of [21] to bound , using and . A slight modification to their proof needs to be considered, because their losses are bounded between . In our case, we assume our loss function is convex, and Lipschitz on a bounded, closed, convex set . Therefore, we can say there exists a value such that . This value can be easily incorporated into the proofs and bounds of [21] to give

where with respect to the natural logarithm. can be bounded using Lemma 8 on each time interval and summing over the intervals, yielding

A.3 Proof of Theorem 4

Let to be the dynamical parameter in our candidate covering set, which minimizes the cumulative loss, as the dynamical parameter in the entire space, which minimizes total loss, and to be the parameter in closest to . Formally, we use the following definitions:

We decompose the regret in the following way:

To bound we use the bounds of [14, Corr 2.2] for the Exponentially Weighted Average Forecaster, which requires . Similarly to the proof of Theorem 3, the bound needs to be adjusted to account for the fact that our loss function, instead of being bounded by instead has arbitrary bounds . Because, is a convex function with a Lipschitz gradient defined on a bounded, closed, convex set, these bounds are finite, and incorporating them into the proof of [14] is not difficult, yielding

The term is upper bounded by by the definitions of and . Finally, the bound on is just the DMD regret bound (Theorem 2) with respect to :

We now use the Lipschitz assumption on to show the bound with respect to . Notice the variation term can be separated.

This shows we get a regret bound which scales like the variation from the best possible parameter , in the set . Setting gives the result.

A.4 Proof of Lemma 6

The proof is by induction, and we assume without loss of generality that . Assume that ; this is trivially true for since and by construction. If we use DMD with for , applying (1) in this setting yields

Notice that we must assume that must lie on the interior of the set such that we can set the gradient to 0 to find the minimizer of equation 1a without projecting back onto the set.

A.5 Proof of Theorem 7

References

- [1] E. Hall and R. Willett, “Dynamical models and tracking regret in online convex programming,” in Proc. International Conference on Machine Learning (ICML), 2013.

- [2] E. Dumbill, “What is big data? An introduction to the big data landscape,” 2012. http://strata.oreilly.com/2012/01/what-is-big-data.html.

- [3] W. Clavin, “Managing the deluge of ‘big data’ from space,” 2013. http://www.jpl.nasa.gov/news/news.php?release=2013-299.

- [4] J. Matson, “Nasa readies a satellite to probe the sun–inside and out,” Scientific American, 2010. http://www.scientificamerican.com/article/solar-dynamics-observatory-sdo/.

- [5] P. E. Dewdney, P. J. Hall, R. T. Schlilzzi, and T. J. L. W. Lazio, “The square kilometre array,” Proceedings of the IEEE, vol. 97, no. 8, 2009.

- [6] J. Marlow, “What to do with 1,000,000,000,000,000,000 bytes of astronomical data per day,” 2012. Wired, http://www.wired.com/2012/04/what-to-do-with-1000000000000000000-bytes-of-astronomical-data-per-day/.

- [7] A. Bain and D. Crisan, Fundamentals of Stochastic Filtering. Springer, 2009.

- [8] L. Xie, Y. C. Soh, and C. E. de Souza, “Robust Kalman filtering for uncertain discrete-time systems,” IEEE Trans. Autom. Control, vol. 39, pp. 1310–1314, 1994.

- [9] Y. Theodor and U. Shaked, “Robust discrete-time minimum-variance filtering,” IEEE Trans. Sig. Proc., vol. 44(2), pp. 181–189, 1996.

- [10] N. Merhav and M. Feder, “Universal prediction,” IEEE Trans. Info. Th., vol. 44, pp. 2124–2147, October 1998.

- [11] A. S. Nemirovsky and D. B. Yudin, Problem complexity and method efficiency in optimization. New York: John Wiley & Sons, 1983.

- [12] A. Beck and M. Teboulle, “Mirror descent and nonlinear projected subgradient methods for convex programming,” Operations Research Letters, vol. 31, pp. 167–175, 2003.

- [13] M. Zinkevich, “Online convex programming and generalized infinitesimal gradient descent,” in Proc. Int. Conf. on Machine Learning (ICML), pp. 928–936, 2003.

- [14] N. Cesa-Bianchi and G. Lugosi, Prediction, Learning and Games. New York: Cambridge University Press, 2006.

- [15] O. Banerjee, L. El Ghaoui, and A. d’Aspremont, “Model selection through sparse maximum likelihood estimation for multivariate Gaussian or binary data,” J. Mach. Learn. Res., vol. 9, pp. 485–516, 2008.

- [16] P. Ravikumar, M. J. Wainwright, and J. D. Lafferty, “High-dimenstional Ising model selection using -regularized logistic regression,” Annals of Statistics, vol. 38, pp. 1287–1319, 2010.

- [17] E. Candès, J. Romberg, and T. Tao, “Stable signal recovery from incomplete and inaccurate measurements,” Communications on Pure and Applied Mathematics, vol. 59, no. 8, pp. 1207–1223, 2006.

- [18] M. Belkin and P. Niyogi, “Laplacian eigenmaps for dimensionality reduction and data representation,” Neural Comput., vol. 15, pp. 1373–1396, June 2003.

- [19] D. Angelosante, J. A. Bazerque, and G. B. Giannakis, “Online adaptive estimation of sparse signals: Where rls meets the 11-norm,” IEEE Transactions on Signal Processing, vol. 58, no. 7, pp. 3436–3447, 2010.

- [20] M. Herbster and M. K. Warmuth, “Tracking the best linear predictor,” Journal of Machine Learning Research, vol. 35, no. 3, pp. 281–309, 2001.

- [21] N. Cesa-Bianchi, P. Gaillard, G. Lugosi, and G. Stoltz, “A new look at shifting regret.” arXiv:1202.3323, 2012.

- [22] N. Littlestone and M. K. Warmuth, “The weighted majority algorithm,” Inf. Comput., vol. 108, no. 2, pp. 212–261, 1994.

- [23] E. Hazan and C. Seshadhri, “Efficient learning algorithms for changing environments,” in Proc. Int. Conf on Machine Learning (ICML), pp. 393–400, 2009.

- [24] L. M. Bregman, “The relaxation method of finding the common points of convex sets and its application to the solution of problems in convex programming,” Comput. Mathematics and Math. Phys., vol. 7, pp. 200–217, 1967.

- [25] Y. Censor and S. A. Zenios, Parallel Optimization: Theory, Algorithms and Applications. Oxford, UK: Oxford Univ. Press, 1997.

- [26] J. Duchi, S. Shalev-Shwartz, Y. Singer, and A. Tewari, “Composite objective mirror descent,” in Conf. on Learning Theory (COLT), 2010.

- [27] L. Xiao, “Dual averaging methods for regularized stochastic learning and online optimization,” J. Mach. Learn. Res., vol. 11, pp. 2543–2596, 2010.

- [28] J. Langford, L. Li, and T. Zhang, “Sparse online learning via truncated gradient,” J. Mach. Learn. Res., vol. 10, pp. 777–801, 2009.

- [29] B. McMahan, “A unified view of regularized dual averaging and mirror descent with implicit updates.” arXiv:1009.3240v2, 2011.

- [30] S. Haykin, Adaptive Filter Theory. New Jersey: Prentice-Hall, 2002.

- [31] A. Rakhlin and K. Sridharan, “Online learning with predictable sequences.” arXiv:1208.3728, 2012.

- [32] M. Herbster and M. K. Warmuth, “Tracking the best expert,” Machine Learning, vol. 32, pp. 151–178, 1998.

- [33] W. Koolen and S. de Rooij, “Combining expert advice efficiently,” in Proceedgins of the 21st Annual Conference on Learning Theory (COLT 2008), pp. 275–286, 2008.

- [34] D. Adamskiy, W. M. Koolen, A. Chernov, and V. Vovk, “A closer look at adaptive regret,” in Proceedings of the 23rd international conference on Algorithmic Learning Theory, ALT’12, pp. 290–304, 2012.

- [35] A. Gyorgy, T. Linder, and G. Lugosi, “Efficient tracking of large classes of experts,” IEEE Transaction on Information Theory, vol. 58, pp. 6709–6725, November 2012.

- [36] V. Vovk, “Aggregating algorithms,” Conf. on Learning Theory (COLT), 1990.

- [37] C. Shalizi, A. Jacobs, K. Klikner, and A. Clauset, “Adapting to non-stationarity with growing expert ensembles.” arXiv:1103:0949, 2011.

- [38] S. Amari and H. Nagaoka, Methods of Information Geometry. Providence: American Mathematical Society, 2000.

- [39] M. J. Wainwright and M. I. Jordan, “Graphical models, exponential families, and variational inference,” Foundations and Trends in Machine Learning, vol. 1, pp. 1–305, December 2008.

- [40] K. S. Azoury and M. K. Warmuth, “Relative loss bounds for on-line density estimation with the exponential family of distributions,” Machine Learning, vol. 43, pp. 211–246, 2001.

- [41] M. Raginsky, R. Willett, C. Horn, J. Silva, and R. Marcia, “Sequential anomaly detection in the presence of noise and limited feedback,” IEEE Transactions on Information Theory, vol. 58, no. 8, pp. 5544–5562, 2012.

- [42] J.-B. Hiriart-Urruty and C. Lemaréchal, Fundamentals of Convex Analysis. Berlin: Springer, 2001.

- [43] S. Boyd and L. Vandenberghe, Convex Optimization. Cambridge, UK: Cambrdige Univ. Press, 2004.

- [44] A. Nemirovski, A. Juditsky, G. Lan, and A. Shapiro, “Robust stochastic approximation approach to stochastic programming,” SIAM J. Optim., vol. 19, no. 4, pp. 1574–1609, 2009.

- [45] M. Szummer and R. W. Picard, “Temporal texture modeling,” in Proceedings of International Conference on Image Processing (ICIP), 1996.

- [46] G. Doretto, A. Chiuso, Y. Wu, and S. Soatto, “Dynamic textures,” International Journal of Computer Vision, vol. 51, no. 2, pp. 91–109, 2003.

- [47] A. Ravichandran, R. Chaudhry, and R. Vidal, “Dynamic texture toolbox,” 2011. http://www.vision.jhu.edu.

- [48] V. Studer, J. Bobin, M. Chahid, H. S. Mousavi, E. Candes, and M. Dahan, “Compressive fluorescence microscopy for biological and hyperspectral imaging,” Proceedings of the National Academy of Sciences, vol. 109, no. 26, pp. E1679–E1687, 2012.

- [49] R. Marcia and R. Willett, “Compressive coded aperture video reconstruction,” in Proc. European Signal Processing Conference EUSIPCO, 2008.

- [50] J. Y. Park and M. B. Wakin, “A multiscale framework for compressive sensing of video,” in Picture Coding Symposium (PCS), (Chicago, IL), May 2009.

- [51] A. C. Sankaranarayanan, C. Studer, and R. G. Baraniuk, “CS-MUVI: video compressive sensing for spatial-multiplexing cameras,” in 2012 IEEE International Conference on Computational Photography (ICCP), pp. 1–10, Apr. 2012.

- [52] D. Angelosante, G. B. Giannakis, and E. Grossi, “Compressed sensing of time-varying signals,” in Intl. Conf. on Dig. Sig. Proc., 2009.

- [53] N. Vaswani and W. Lu, “Modified-CS: Modifying compressive sensing for problems with partially known support,” IEEE Trans. Sig. Proc., vol. 58, pp. 4595–4607, 2010.

- [54] M. F. Duarte, M. A. Davenport, D. Takhar, J. N. Laska, T. Sun, K. F. Kelly, and R. G. Baraniuk, “Single pixel imaging via compressive sampling,” IEEE Sig. Proc. Mag., vol. 25, no. 2, pp. 83–91, 2008.

- [55] Z. Lin, M. Chen, and Y. Ma, “The augmented lagrange multiplier method for exact recovery of corrupted low-rank matrices.” arXiv:1009:5055, 2010.

- [56] C. Blundell, K. A. Heller, and J. M. Beck, “Modelling reciprocating relationships with hawkes processes,” in Proc. NIPS, 2012.

- [57] S. W. Linderman and R. P. Adams, “Discovering latent network structure in point process data.” arXiv:1402.0914, 2014.

- [58] A. Stomakhin, M. B. Short, and A. L. Bertozzi, “Reconstruction of missing data in social networks based on temporal patterns of interactions,” Inverse Problems, vol. 27, no. 11, p. 115013, 2011.

- [59] E. N. Brown, R. E. Kass, and P. P. Mitra, “Multiple neural spike train data analysis: state-of-the-art and future challenges,” Nature neuroscience, vol. 7, no. 5, pp. 456–461, 2004.

- [60] B. Klimt and Y. Yang, “The Enron corpus: a new dataset for e-mail classification research,” in Proceedings of the European Conference on Machine Learning (ECML), pp. 217–226, 2004.

- [61] “http://www.pbs.org/wgbh/pages/frontline/shows/blackout/california/timeline.html.” Retrieved June 3, 2010.

- [62] R. Smith and J. Emswhwiller, “Enron faces collapse as dynegy bolts and stock price, credit standing dive,” The Wall Street Journal, 2001.

- [63] J. M. Steele, The Cauchy-Schwarz master class : an introduction to the art of mathematical inequalities. Cambridge, New York, NY, Port Melbourne: Cambridge University Press, 2010.