A Dynamic Learning Algorithm for Online Matching

Problems with Concave Returns

\ARTICLEAUTHORS\AUTHOR

Xiao Alison Chen \AFFDepartment of

Industrial and Systems Engineering, University of Minnesota, MN, USA

chen2847@umn.edu\AUTHORZizhuo

Wang \AFFDepartment of Industrial and Systems Engineering,

University of Minnesota, MN, USA

zwang@umn.edu

\ABSTRACT

We consider an online matching problem with concave

returns. This problem is a generalization of the traditional online

matching problem and has vast applications in online advertising. In

this work, we propose a dynamic learning algorithm that achieves

near-optimal performance for this problem when the inputs arrive in

a random order and satisfy certain conditions. The key idea of our

algorithm is to learn the input data pattern dynamically: we solve a

sequence of carefully chosen partial allocation problems and use

their optimal solutions to assist with the future decisions. Our

analysis belongs to the primal-dual paradigm; however, the absence

of linearity of the objective function and the dynamic feature of

the algorithm makes our analysis quite unique. We also show through

numerical experiments that our algorithm performs well for test

data.

\KEYWORDSonline algorithms; primal-dual; dynamic price update;

random permutation model; Adwords problem

1 Introduction

In traditional optimization models, inputs are usually assumed to be

known and efficient algorithms are sought to find the optimal

solutions. However, in many practical cases, data does not reveal

itself at the beginning. Instead, it comes in an online fashion. For

example, in many revenue management problems, customers arrive

sequentially and each time a customer arrives, the decision maker

has to make some irrevocable decisions (e.g., what product to sell,

at what prices) for this customer without knowing any of the future

inputs. Such a regime is often called online optimization.

Online optimization has gained much attention in the research

community in the past few decades due to its applicability in many

practical problems, and much effort has been directed toward

understanding the quality of solutions that can be obtained under

such settings. For an overview of the online optimization literature

and its recent developments, we refer the readers to

Borodin and El-Yaniv (1998), Buchbinder and Naor (2009) and Devanur (2011).

In this paper, we consider a special type of online optimization

problem - an online matching problem. Online matching problems are

considered as fundamental problems in online optimization theory and

have important applications in the online advertisement allocation

problems. For a review of online matching problems, we refer the

readers to Mehta (2012).

In the problem we study, there is an underlying weighted bipartite

graph with weights for each edge . The vertices in arrive sequentially in some order, and

whenever a vertex arrives, the set of weights is

revealed for all , . The decision maker then has

to match to one of its neighbors , and a value of

will be obtained from this matching. In our problem, the decision

maker’s gain from each vertex is a function of the total matched

value to this vertex, and his goal is to maximize the total gain

from

all vertices. Mathematically, the problem can be formulated as follows

(assume , , and let for ):

(1)

where denotes the fraction of vertex that is matched to

vertex .111We allow fractional allocations in our model.

However, our proposed algorithms output integer solutions. Thus all

our results hold if one confines to integer solutions. In

(1), the coefficient is revealed only when vertex arrives, and an

irrevocable decision has to be made

before observing the next input. For each , is a

nondecreasing concave function with . In this paper, we

assume that s are continuously differentiable.

As mentioned earlier, online matching problems have a very important

application in the online advertisement allocation problem, which we

will later refer to as the Adwords problem. In the Adwords problem,

there are advertisers (which we also call the bidders). A

sequence of keywords are searched during a fixed time horizon.

Based on the relevance of the keyword, the th bidder would bid a

certain amount to show his advertisement on the result page

of the th keyword. The search engine’s decision is to allocate

each keyword to one of the bidders (we only consider a single

allocation in this paper). Note that each allocation decision can

only depend on the information earlier in the arrival sequence but

not on any future data. As pointed out in Devanur and Jain (2012),

there are several practical motivations for considering a concave

function of the matched bids in the Adwords problem. Among them are

convex penalty costs for under-delivery in search engine-advertiser

contracts, the concavity of the click-through rate in the number of

allocated bids observed in empirical data and fairness

considerations. In each of the situations mentioned above, one can

write the objective as a concave function. We refer the readers to

Devanur and Jain (2012) for a more thorough review of the

motivations for this problem. It is worth noting that there is a

special case of this problem where . In

this case, one can view that the bidder has a budget and the

revenue from each bidder is bounded by .

One important question when studying online algorithms is the

assumptions on the input data. In this work, we adopt a random

permutation model. More precisely, we assume:

1.

The total number of arrivals is known a priori.

2.

The weights can be adversarially

chosen. However, the order that arrives is uniformly distributed

over all the permutations.

The random permutation model has been adopted in much recent

literature in the study of online matching problems, see, e.g.,

Devanur and Hayes (2009), Feldman et al. (2010), Agrawal et al. (2014), etc. It is equivalent to

saying that a set of is arbitrarily chosen

beforehand (unknown to the decision maker). Then the arrivals

are drawn randomly without replacement

from . The random permutation model is an intermediate

path between using a worst-case analysis and assuming each input

data is drawn independently and identically distributed (i.i.d.)

from a certain distribution. On one hand, compared to the worst-case

analysis (see, e.g., Mehta et al. 2005, Buchbinder et al. 2007, Feldman et al. 2009, Devanur and Jain 2012), the random permutation model is practically

reasonable yet much less conservative. On the other hand, the random

permutation model is much less restrictive than assuming the inputs

are drawn i.i.d. from a certain distribution

(Devanur 2011). Also, the assumption of the knowledge of

is necessary for any online algorithm to achieve near-optimal

performance (see Devanur and Hayes 2009). Therefore, for large problems

with relatively stationary inputs, the random permutation model is a

good approximation and the study of such models is of practical

interest. Next we define the performance measure of an algorithm

under the random permutation model:

Definition 1(-competitiveness)

Let OPT be the optimal value for the offline problem

(1). An online algorithm is called

-competitive in the random permutation model if the expected

value of the online solutions by using is at least times the

optimal value of (1), that is

where the expectation is taken over uniformly random permutations

of , and is the th

decision made by algorithm when the inputs arrive in order

.

In Devanur and Jain (2012), the authors propose an algorithm for the

online matching problem with concave returns that has a constant

competitive ratio under the worst-case model (the constant

depends on the forms of each ). They also show that a

constant competitive ratio is the best possible result under

that model. In this paper, we propose an algorithm under the random

permutation model, which achieves near-optimal performance

under some conditions on the input.

Our main result is stated as follows:

Theorem 1

Fix . There exists an algorithm (Algorithm

DLA) that is competitive for the online matching

problem with concave returns s under the random

permutation model if

(2)

where , , and

is a constant that only depends on each

and .

In condition (2), can be viewed as the

average bid value of a bidder over time. Given that each bidder is

at least interested in some fractions of the keywords, this average

will go to a certain constant as becomes large. Also, can

be viewed as the ratio between the value of the smallest non-zero

bid and the highest bid. In practice, this is often bounded below by

a constant by enforcing a reserve price and a maximum price for any

single bid. The exact functional form of is somewhat

complicated, and is given in Proposition 1.

Just to give an example, if we choose (),

then . Therefore,

condition (2) can be viewed as simply requiring the

total number of inputs is large, which is often the case in

practice. For example, in the Adwords problem, is the number of

keyword searches in a certain period, and for instance, Google

receives more than billion searches per day. Even if we focus on

a specific category, the number can still be in the millions. Thus,

this condition is reasonable. We note that most learning algorithms

in the literature make similar requirements, see Devanur and Hayes (2009), Agrawal et al. (2014), and Molinaro and Ravi (2014). Furthermore, as we will show in our

numerical tests, our algorithm performs well even for problems with

sizes that are significantly smaller than the condition requires,

which validates the potential usefulness of our algorithm.

To propose an algorithm that achieves near-optimal performance, the

main idea is to utilize the observed data in the allocation process.

In particular, since the input data arrives in a random order, using

the past input data and projecting it into the future should present

a good approximation for the problem. To mathematically capture this

idea, we use a primal-dual approach. We obtain the dual optimal

solutions to suitably constructed optimization problems and use them

to assist with future allocations. We first propose a one-time

learning algorithm (OLA, see Section 2) that only solves

an optimization problem once at time . By carefully

examining this algorithm, we prove that it achieves near-optimal

performance when the inputs satisfy certain conditions. However, the

conditions are stronger than those stated in Theorem 1.

To improve our algorithm, we further propose a dynamic learning

algorithm (DLA, see Section 3). The dynamic learning

algorithm makes better use of the observed data and updates the dual

solution at a geometric pace, that is, at time ,

, and so on. We show that these

resolvings can lift the performance of the algorithm and thus prove

Theorem 1. As one will see in the proof of the DLA, the

choice of the resolving points perfectly balances the trade-off

between exploration and exploitation, which are the main

trade-offs in such types of learning algorithms.

It is worth mentioning that a similar kind of dynamic learning

algorithm has been proposed in Agrawal et al. (2014) and further studied in

Wang (2012) and Molinaro and Ravi (2014). However, those works

only focus on linear objectives. In our analysis, the nonlinearity

of the objective function presents a non-trivial hurdle since one

can no longer simply analyze the revenue generated in each time

segment and add them together. In this paper, we successfully work

around this hurdle by a convex duality argument. We believe that our

analysis is a non-trivial extension of the previous work. Moreover, the

problem solved has important applications.

The remainder of the paper is organized as follows. In Section

2, we start with a one-time learning algorithm and prove

that it achieves near-optimal performance under some mild conditions

on the input. The one-time learning algorithm is easy to understand

and shows important insights for designing this class of learning

algorithms. However, it only achieves a weaker performance than what

is stated in Theorem 1. In Section 3, we

propose a dynamic learning algorithm which makes better use of the

data and has a stronger performance. Some numerical test results of

our algorithm are presented in Section 4, which

validate the strength of our algorithm. Section 5

concludes this paper.

2 One-Time Learning Algorithm

We first rewrite the offline problem

(1) as follows:

(3)

We define the following dual problem:

(4)

Let the optimal value of (3) be and the optimal

value of (4) be . In Devanur and Jain (2012), the

authors proved the weak duality between (3) and

(4). In the following lemma, we prove that in fact the

strong duality holds. The proof of the lemma is relegated to the

Appendix.

Lemma 1

. Furthermore, the objective value of any feasible

solution to (4) is an upper bound of .

Before we describe our algorithm, we define the following partial

optimization problem:

(5)

Now we define the one-time learning algorithm as follows:

Algorithm 1 One-Time Learning Algorithm

(OLA)

1.

During the first arrivals, no allocation is made.

2.

After observing the first arrivals,

solve () and denote the optimal solutions by

and .

3.

For any dimensional vector , define

(8)

Here, ties among are broken arbitrarily. For the

th to the th arrival, the allocation rule

is used.

Now we provide some intuition for the algorithm. The idea of the

algorithm is to use the first inputs to learn an

approximate and then use it to make all the future

allocations based on the complementarity conditions between the

primal and dual problems ((3) and (4)). Here

is solved from () which projects the

allocation in the first inputs to the entire problem.

The decision rule in (8) can be explained as choosing the

with the highest product of the nominal bid value and the

marginal contribution rate to the total projected reward

. Note that a similar idea has been used to

construct algorithms for an online matching problem with linear

objective functions (see e.g., Devanur and Hayes 2009, Agrawal et al. 2014, Molinaro and Ravi 2014). However, the analyses of those algorithms all depend

on the linearity of the objective function which we do not possess

in this problem. Instead, an analysis with the use of concavity is

required in our analysis, making it quite different from those in

the prior literature. In the following, we assume without loss of

generality that (we can always scale the

inputs to make this hold). We also make a technical assumption as

follows:

Assumption 1

The inputs of the problem are in a general position. That is,

for any vector , there are at most

terms among , , that are

not singleton sets.

The assumption says that we only need to break ties in (8) no

more than times. This assumption is not necessarily true for all

inputs. However, as pointed out by Devanur and Hayes (2009) and Agrawal et al. (2014),

one can always perturb by adding a random variable

taking uniform distribution on for some very

small . By doing so the assumption holds with probability one

and the effect to the solution can be made arbitrarily small. Given

this assumption and by the complementarity conditions, we have the

following lemma, whose proof is in the Appendix.

Lemma 2

We first prove the following proposition about the performance of

the OLA, which relies on a condition of the solution to ().

Proposition 1

For any given , if , then the

OLA is a -competitive algorithm.

Before we prove Proposition 1, we define

some notation.

•

We define the optimal offline solution to (3) by with optimal value OPT.

•

Define , note that normally does not equal

.

We show the following lemma:

Lemma 3

For any given , if ,

then with probability ,

(9)

Proof. The proof will proceed as follows: For any

fixed , we define that a random sample (the first

arrivals) is bad for this if

and only if is the optimal solution to (5)

for this , but , or ,

for some . First, we show that the probability of a bad

sample is small for every fixed (satisfying

)

and . Then, we take a union bound over all distinct

and s to prove the lemma.

To start with, we fix and . Define . By Lemma 2 and

the condition on , we have

Therefore, the probability of bad

is bounded by the sum of the following two terms ():

(10)

For the first term, we first define and we have

Then we have

Here the second inequality follows from the Hoeffding-Bernstein’s

inequality for sampling without replacement, see Lemma 8 in

the Appendix. Similarly, we can get the same result for the second

term in (10), which is also bounded by .

Therefore, the probability of a bad sample is bounded by

for fixed and .

Next, we take a union bound over all distinct s.

We call and distinct if and only

if they result in different allocations, i.e., for some , . Denote

. For each , by the definition in

(8), the allocation is uniquely defined by the signs of the

following terms:

There are such terms for each . Therefore, the entire

allocation profiles for all the arrivals can be determined by

the signs of no more than differences. Now we find out how

many different allocation profiles can arise by choosing different

s. By Orlik and Terao (1992), the total number of different profiles for

the differences can not exceed .

Therefore, the number of distinct s is no more than

. Now we take a union bound over all

distinct s and , and Lemma

3

follows.

Next we show that the OLA achieves a near-optimal solution under the

condition in Proposition 1. We first

construct a feasible solution to (4):

By Lemma 1,

is an upper bound of OPT. Thus, we have

where the last equality is because by the allocation rule

(8):

Proposition 1 shows that the OLA is

near-optimal under some conditions on . However,

is essentially an output of the algorithm. Although such

types of conditions are not uncommon in the study of online

algorithms (e.g., in the result of Devanur and Hayes 2009, Feldman et al. 2010), it is quite undesirable. In the following, we

address this problem by providing a set of sufficient conditions

which only depend on the input parameters (i.e., , , s

and s). We show that our algorithm achieves near-optimal

performance under these conditions. We start with the following

lemma.

Lemma 4

For any , suppose the following condition holds:

(11)

where , and is such that

Then with probability , , for all .

The proof of Lemma 4 is relegated to the

Appendix (it is proved together with Lemma

7). Now combining Proposition

1 and Lemma 4, we have

the following result for the OLA:

Proposition 2

Fix any . Suppose

(12)

where , and is such that

(13)

with . Then the OLA

is -competitive under the random permutation model.

Here we give some comments on the definition of . The

definition of basically ensures that we rule out the

possibility that one receives nearly all the allocation while

some others receive almost none. Note that such always

exists and is finite if for

all . In practice, this is usually true as there is usually a

upper bound on the possible reward from each bidder . In

particular, if for all and

, then one can choose

where denotes the inverse function of .

For example, if one chooses (), then one can

further choose .

Therefore, in most practical situations, one can view as

a constant. Finally, we want to remark that the conditions in Lemma

4 (or Proposition 2) are only one

set of sufficient conditions which have the nice feature of only

depending on the problem inputs. In practice, one can always resort

to the condition in Proposition 1 () if they

are more favorable. In addition, as we will show in our numerical

tests in Section 4, our algorithm performs quite

well even if some of the conditions in Lemma 4

are not satisfied. Therefore, the applicability of our algorithm

could be well beyond what the conditions require.

3 Dynamic Learning Algorithm

In the previous section, we introduced the OLA

that can achieve near-optimal performance. While the OLA illustrates

the ideas of our approach and requires solving a convex

optimization problem only once, the conditions it requires to achieve

near-optimality are stricter than what we claim in Theorem

1. In this section, we propose an enhanced algorithm

that lessens the conditions and thus improves the OLA.

The main idea for the enhancement is the following: In the one-time

learning algorithm, we only solve a partial optimization problem

once. However, it is possible that there is some error for that

solution due to the random order of arrival. If we could modify the

solution as we gather more data, we might be able to improve the

performance of the algorithm. In the following, we introduce a

dynamic learning algorithm based on this idea, which updates the

allocation policy every time the history doubles; that is, it

computes a new at time and uses it to perform the matching for the next

time period. We define the

following problem:

We further define to be the optimal solution to

().

We define the dynamic learning algorithm as follows:

Algorithm 2 Dynamic Learning Algorithm (DLA)

1.

During the first arrivals, no allocation is made.

2.

For , for , set for all ,

where .

In the following, without loss of generality, we assume that is an integer (otherwise one can just choose a

smaller and prove the same result). Define , , and define . We first prove the following proposition:

Proposition 3

If for all , , then the DLA is

-competitive under the random permutation model.

Before we proceed to the proof, we first define some more notation.

We define:

Note that in these definitions, is the

allocated values for in the period to

using , which is the actual allocation in that period.

is the allocation for in all periods if

is used. is the actual allocation for

during the entire algorithm. We first prove the following lemma

bounding the differences between , and

.

Lemma 5

If , then with probability

, for all ,

(14)

and

(15)

Lemma 5 shows that with high probability,

, and are

close to each other. In particular, when is small, the factor

is relatively loose while as

increases, the factor becomes tight. The proof of Lemma

5 is similar to that of Lemma 3

and is relegated to the Appendix.

The next lemma gives a bound on the revenue obtained by the DLA.

Lemma 6

If for

all and , then with probability ,

The proof of Lemma 6 can be found in the

Appendix.

Finally, we prove Proposition 3. We bound the

objective value of the actual allocation. Note that the actual

allocation for each can be written as

where . By the property of concave

functions, we have

Similar to Lemma 4, we have the following

conditions on the input parameters such that with high probability,

the conditions in Proposition 3 hold.

Lemma 7

For any , suppose the following condition holds:

(16)

where , and is such that

Then with probability , , for all

.

The proof of Lemma 7 is given in the

Appendix. Finally, we combine Proposition 3 and

Lemma 7, and Theorem 1

follows.

The same remark after Lemma 4 applies here. In

particular, the conditions in Lemma 7 is

only one set of sufficient conditions for our algorithm to achieve

the target performance. However, one may also use the conditions in

Proposition 3 if they turn out to hold in practice.

In the next section, we show that the DLA works well even if the

conditions in Lemma 7 are not satisfied.

4 Numerical Experiments

In this section, we report some numerical test

results for our algorithms (both the OLA and the DLA). The objective

is to validate the strength of our approaches and investigate the

relationship between the performance of our algorithms and the input

parameters.

In our numerical tests, we consider the Adwords problem. We assume

there are advertisers (bidders), keywords arriving

sequentially, and is the amount bidder would like to

pay to display his advertisement on keyword search . We introduce

a base problem in which we set , and with . The bidding values are generated in

the following way:

1.

Assume there are categories of keywords. For each

category , there is a base valuation of bidder , denoted by

, which is generated according to the following distribution:

where denotes a uniformly distributed random variable

on .

2.

For each arriving keyword,

we first randomly choose a category. The probability for each

category , denoted by , is randomly chosen on the simplex

. Then if

category is chosen, the final bid value for bidder will be

.

Although the way is chosen seems arbitrary, we believe it

reflects some major features of the bid values in practice. In the

Adwords problem, each bidder is interested in certain categories of

keywords. For example, a sport product company is interested in

keywords related to sports. The s represent such

interest levels. Then the bidder ’s actual bid on such a keyword

is the base value multiplied by a random number,

which reflects some level of idiosyncrasies of each keyword arrival.

We also tested other ways to generate , and the test results

are similar. We will report those test results in the end of this

section.

To evaluate the performance of our algorithms, we introduce the

notion of Relative Loss (RL) defined as follows:

In the numerical experiment, there is one key parameter we need to

set in both of our algorithms: . In Theorem

1 and Proposition 1, we gave

sufficient conditions on the inputs such that the algorithms will

have expected RL less than . However, the theoretical

results are asymptotic and thus may not represent the best practical

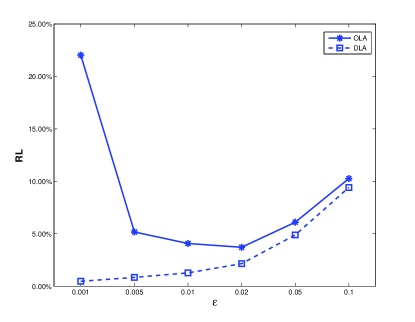

choice of . In Table 1 and Figure 1,

we first test both our OLA and DLA with different choices of

. We have the following observations from Table

1 and Figure 1 (each

number in Table 1 is the average of

independent runs, the standard deviations of the results are

insignificant compared to the average value):

•

For the DLA, choosing a smaller improves its

performance. There are two reasons for that. First, choosing a smaller

reduces the loss due to ignoring the first

bids. Second, it increases the number of price updates

which help the decision maker to refine the decision

policy and achieve better performance. Therefore one should

choose a smaller in the DLA.

•

For the OLA, the optimal choice of is more subtle.

There are two countervailing forces when one chooses a smaller

. On one hand, by choosing a smaller , the loss

due to the failure to allocate any bid during period to

becomes smaller, which benefits the algorithm. On the

other hand, if is too small, the learned price may not be

accurate enough which may lead to poor allocation in the remaining

periods. In the test example, the optimal choice is .

•

The DLA outperforms the OLA for all choices of .

0.001

0.005

0.01

0.02

0.05

0.10

OLA

22.02%

5.17%

4.07%

3.71%

6.10%

10.26%

DLA

0.47%

0.84%

1.27%

2.15%

4.89%

9.41%

Table 1: Performance of the OLA and the DLA for Different Choices of

Figure 1: Performance of the OLA and the DLA for Different Choices of

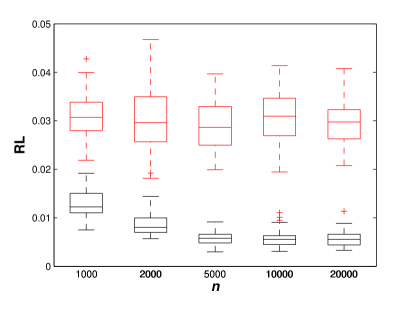

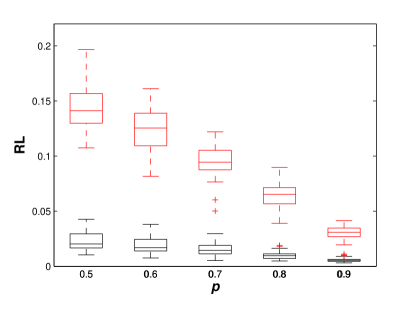

Next we focus ourselves on the DLA. As shown in Table

1, we prefer to choose a smaller in

the DLA. In the following experiments, we will choose . Next we compare the performance of the DLA to a myopic

allocation method which simply allocates each incoming keyword to

the bidder with the highest value. We also study the impact

of the two parameters, and , on the performance of our

algorithm. We generate instances of the input and

compare the average performance. The results of the average RL are

shown in Table 2 (the standard deviations are shown

in the parentheses) as well as in Figures 2(a) and

2(b).

1,000

2,000

5,000

10,000

20,000

DLA

1.29% (0.29%)

0.87% (0.26%)

0.58% (0.12%)

0.57% (0.17%)

0.57% (0.16%)

Myopic

3.07% (0.47%)

3.03% (0.61%)

2.90% (0.49%)

3.11% (0.54%)

2.96% (0.47%)

0.5

0.6

0.7

0.8

0.9

DLA

2.30% (0.82%)

1.87% (0.67%)

1.55% (0.56%)

0.99 % (0.34%)

0.57% (0.17%)

Myopic

14.38% (2.01%)

12.46% (1.81%)

9.46% (1.38%)

6.51% (1.05%)

3.11% (0.54%)

Table 2: Performance of the DLA and the Myopic

Policy

(a)Different Problem Sizes

(b)Different s

Figure 2: Performance of the DLA (the Bottom Ones) and the Myopic

Policy (the Top Ones)

From Table 2, we can see that the DLA consistently

performs better than the myopic approach. In particular, the

performance of the DLA gradually improves when increases, while

the performance of the myopic approach seems to be insensitive to

the size of the problem. Moreover, even for small values of ,

the performance of the DLA is still very good. This means that the

DLA works well even for problems whose size is much smaller than

what Theorem 1 requires. For the parameter , we can

see that both the DLA and the myopic algorithm deteriorate when

decreases, but the DLA deteriorates much slower. Finally, we comment

that these results are computed when we ignore the first bids. In practice, one does not need to do that and the

performance of the DLA would be even better.

Finally, we repeat the above test for different setups of the

inputs. We fix the parameters , and with in the base problem and generate s in the

following ways:

1.

follows a normal distribution (truncated at and ). The parameters of

each normal distribution (mean and standard deviation

) are randomly generated from a uniform distribution on .

2.

follows a Beta distribution. The parameters of the Beta

distribution are generated from a uniform distribution on .

3.

follows a

mixed normal and Beta distribution. That is, with probability ,

follows a truncated normal distribution with mean and

standard deviation , and with probability ,

follows a Beta distribution with .

Next, we compare the performance of the DLA (choose ) and the myopic algorithm. For each case, we generate 100

instances of the input and compare the average RL. The

results are shown in Table 3.

Case 1

1,000

2,000

5,000

10,000

20,000

DLA

1.56% (0.33%)

0.84% (0.18%)

0.36% (0.07%)

0.21% (0.05%)

0.14% (0.03%)

Myopic

1.45% (0.45%)

1.37% (0.47%)

1.42% (0.45%)

1.41% (0.48%)

1.31% (0.47%)

0.5

0.6

0.7

0.8

0.9

DLA

0.20% (0.04%)

0.22% (0.06%)

0.22% (0.05%)

0.21% (0.03%)

0.21% (0.05%)

Myopic

9.10% (2.01%)

7.98% (2.00%)

5.71% (1.32%)

3.38% (0.96%)

1.44% (0.46%)

Case 2

1,000

2,000

5,000

10,000

20,000

DLA

1.19% (0.24%)

0.61% (0.12%)

0.25% (0.08%)

0.13% (0.07%)

0.12% (0.08%)

Myopic

13.91% (2.07%)

13.66% (2.48%)

13.90% (2.07%)

13.78% (1.97%)

13.62% (2.12%)

0.5

0.6

0.7

0.8

0.9

DLA

0.20% (0.16%)

0.29% (0.20%)

0.21% (0.12%)

0.17% (0.11%)

0.13% (0.07%)

Myopic

40.57% (6.50%)

38.30% (5.98%)

32.45% (4.71%)

24.67% (3.26%)

13.46% (2.07%)

Case 3

1,000

2,000

5,000

10,000

20,000

DLA

1.50% (0.31%)

0.89% (0.34%)

0.35% (0.07%)

0.21% (0.06%)

0.14% (0.01%)

Myopic

10.84% (2.50%)

11.22% (2.64%)

11.30% (2.44%)

10.91% (2.54%)

11.07% (2.85%)

0.5

0.6

0.7

0.8

0.9

DLA

0.21% (0.12%)

0.22% (0.12%)

0.15% (0.45%)

0.15% (0.35%)

0.21% (0.06%)

Myopic

37.00% (7.43%)

34.02% (6.82%)

30.22% (5.89%)

20.72% (4.70%)

10.91% (2.54%)

Table 3: Performance of the DLA and the Myopic Policy

From Table 3, we can see that the DLA outperforms

the myopic approach under all the above three setups. The RL of the

DLA decreases as the problem size grows, while the RL of the myopic

policy is not sensitive to . Also, as changes, the

performance of the DLA is rather stable, while the performance of

the myopic algorithm varies a lot. The overall trend of the DLA and

the myopic algorithm resembles that in the experiment in the

beginning of this section. Finally, we observe that the DLA seems

robust toward various problem setups, while the myopic approach does

not.

5 Conclusion

In this paper, we propose a dynamic learning

algorithm for an online matching problem with concave returns. We

show that our algorithm achieves near-optimal performance when the

data arrives in a random order and satisfies some conditions. The

analysis is primal-dual based, however, the nonlinear objective

function requires us to work around nontrivial hurdles that do not

exist in previous work. Numerical experiment results show that our

algorithm works well in test problems.

6 Acknowledgement

We thank the anonymous referees for their insightful comments. The

research of both authors is supported by National Science Foundation

under research grant CMMI-1434541.

References

Agrawal et al. (2014)

Agrawal, S., Z. Wang, Y. Ye. 2014.

A dynamic near-optimal algorithm for online linear programming.

Operations Research62(4) 876–890.

Borodin and El-Yaniv (1998)

Borodin, A., R. El-Yaniv. 1998.

Online computation and competitive analysis.

Cambridge University Press.

Buchbinder et al. (2007)

Buchbinder, N., K. Jain, J. Naor. 2007.

Online primal-dual algorithms for maximizing ad-auctions revenue.

ESA’07: Proceedings of the 15th Annual European Symposium on

Algorithms. 253–264.

Buchbinder and Naor (2009)

Buchbinder, N., J. Naor. 2009.

Online primal-dual algorithms for covering and packing.

Mathematics of Operations Research34(2) 270–286.

Devanur (2011)

Devanur, N. 2011.

Online algorithms with stochastic input.

SIGecom Exch.10(2) 40–49.

Devanur and Hayes (2009)

Devanur, N., T. Hayes. 2009.

The adwords problem: Online keyword matching with budgeted bidders

under random permutations.

EC’09: Proceedings of the 10th ACM Conference on Electronic

Commerce. 71–78.

Devanur and Jain (2012)

Devanur, N., K. Jain. 2012.

Online matching with concave returns.

STOC’12: Proceedings of the 44th Annual Symposium on Theory of

Computing. 137–144.

Feldman et al. (2010)

Feldman, J., M. Henzinger, N. Korula, V. Mirrokni, C. Stein. 2010.

Online stochastic packing applied to display ad allocation.

ESA’10: Proceedings of the 18th Annual European Symposium on

Algorithms: Part I. 182–194.

Feldman et al. (2009)

Feldman, J., N. Korula, V. Mirrokni, S. Muthukrishnan, M. Pal. 2009.

Online ad assignment with free disposal.

WINE’09: Proceedings of the 5th International Workshop on

Internet and Network Economics. 374–385.

Mehta (2012)

Mehta, A. 2012.

Online matching and ad allocation.

Foundations and Trends in Theoretical Computer Sciences8(4) 265–368.

Mehta et al. (2005)

Mehta, A., A. Saberi, U. Vazirani, V. Vazirani. 2005.

Adwords and generalized on-line matching.

FOCS’05: Proceedings of the 46th Annual IEEE Symposium on

Foundations of Computer Science. 264–273.

Molinaro and Ravi (2014)

Molinaro, M., R. Ravi. 2014.

Geometry of online packing linear programs.

Mathematics of Operations Research39(1) 46–59.

Orlik and Terao (1992)

Orlik, P., H. Terao. 1992.

Arrangement of hyperplanes.

Grundlehren der Mathematischen Wissenschaften [Fundamental Principles

of Mathematical Sciences], Springer-Verlag, Berlin.

van der Vaart and Wellner (1996)

van der Vaart, A., J. Wellner. 1996.

Weak convergence and empirical processes: with applications to

statistics (Springer Series in Statistics).

Springer.

Wang (2012)

Wang, Z. 2012.

Dynamic learning mechanism in revenue management problems.

Ph.D. thesis, Stanford University, Palo Alto.

{APPENDIX}

In our proofs, we will frequently use the following

Hoeffding-Bernstein’s Inequality for sampling without replacement:

Lemma 8(Theorem 2.14.19 in

van der Vaart and Wellner 1996:)

Let be random

samples without replacement from real numbers .

Then for every ,

where , , and .

Proof of Lemma 1. We first

write down the Lagrangian dual of (3). By associating

to the first set of constraints and to the second set of

constraints, the Lagrangian dual of (3) is:

(18)

Since the primal problem is convex and only has linear constraints,

Slater’s condition holds, thus the strong duality theorem holds and

(3) and (18) have the same optimal

value. Next we show that (4) and (18) are

equivalent. To show this, assume the range of on

is or (by the assumption that

s are continuously differentiable, it must be either one

of these two forms). Now we argue that the optimal must be

within in (18). First we must have

, otherwise the term goes to infinity as increases

and it cannot be the optimal solution to (18). On

the other hand, if , the optimal must be , and

one can always set and achieves a smaller value of the

objective function. Therefore, at optimality.

Now if at optimality, one can always find one

such that , and that must be the

optimal solution to

(the optimal solution must be attainable in this case). Therefore,

each feasible solution of (18) will correspond to

a feasible solution of (4) and vice versa. The only case

left now is when at optimality. In this case,

. Also, we

know that , therefore,

there exists a sequence of feasible solution of (4) such

that the limit of the objective value equals the objective obtained

when in (18). Therefore, the lemma is

proved.

Proof of Lemma 2. To prove

this lemma, it suffices to show that for each fixed ,

and (recall that is the optimal solution to (5)) differ

by no more than terms. If this is true, then note that

and

, the lemma holds.

To show that and differ by no

more than terms, we first construct the dual problem of

(5) (according to (4)):

By Lemma 2.1, strong duality holds and thus any optimal solution

should satisfy the complementarity conditions. Among them we should

have .

Therefore, if there is no tie when we defined , we must have . By

Assumption 1, there are no more than

ties. Thus, Lemma 2 is proved.

Proof of Lemma 5.

We first prove (14). The

idea is similar to the proof of the one-time learning case. For any

fixed , we define that a random sample (a sequence

of arrival) is bad if and only if is the

optimal solution to () but does not

satisfy (14) for some . First, we show that the

probability of a bad sample is small for any fixed and

fixed . Then we take a union bound over all distinct

s and s to show the result.

Fix and . We define . By Lemma 2 and the assumption on

, we have

Therefore, the probability of a bad sample is bounded by

the following two terms:

(19)

For the first term, we have

Here the second inequality follows from Lemma 8, and the

third inequality is due to the condition of .

Similarly, we can get the bound for the second term in

(S6.Ex40). Therefore, the probability of a bad sample is

bounded by .

Now we take union bound over all distinct and

. Similar to the proof of Lemma 3, we call

s to be distinct if they result in different

allocations. As argued earlier, there are no more than

distinct s. Therefore, we know that with probability

, (14) holds.

Next we prove (15). The idea is similar. Fix

and . We define . Applying Lemma 8, we get

Proof of Lemma 4 and Lemma

7. First, we note that Lemma

7 implies Lemma 4

(except for the constant part, which can be strengthened easily by

only considering one in the following proof). Therefore, it

suffices to prove Lemma 7.

We first prove for each , with probability , . Then we take a union

bound to prove Lemma 7. To show that for

each , with probability ,

, first we show that with probability

, for all . To see this, we use Lemma 8, we

have for any ,

where the last inequality is due to condition (16).

Next we show that given , there cannot exist an such that in the optimal solution to the partial program (). We prove by contradiction. Let . If there exists

such that in the optimal solution, then we argue

that there must exist such that

1.

, and

2.

There exists such that and .

Here these two conditions mean that there must exist a keyword

such that we allocated it (at least partially) to bidder whose

total allocation had already exceeded when we could have

allocated it to bidder whose final allocation is less than .

To see this, we note that we have proved with probability

, . However, by the definition of , ,

thus we also have . Therefore, combined with the assumption that , there must exist at least s

between and such that but , i.e., .

Next we show that among , there exists at least one

such that while for some

. We define . We have

(21)

Here the second inequality is because . However, we also

have

(22)

This is because s are increasing, thus each must equal at optimality. Then, by taking the difference

between (21) and (22), we have that

The last inequality is by the definition of and that for all . Therefore, there exists such

that the bid is allocated to some with .

We denote such by .

Finally, we consider another allocation that increases the

allocation of to while decreasing the allocation to .

The local change of the objective function at this point is:

where the first inequality is due to the concavity of s

and the last inequality is due to condition (16).

However, this contradicts the assumption that the solution is

optimal. Thus, Lemma 7 is proved.