abbr

The cluster graphical lasso for improved estimation of Gaussian graphical models

Abstract

We consider the task of estimating a Gaussian graphical model in the high-dimensional setting. The graphical lasso, which involves maximizing the Gaussian log likelihood subject to an penalty, is a well-studied approach for this task. We begin by introducing a surprising connection between the graphical lasso and hierarchical clustering: the graphical lasso in effect performs a two-step procedure, in which (1) single linkage hierarchical clustering is performed on the variables in order to identify connected components, and then (2) an -penalized log likelihood is maximized on the subset of variables within each connected component. In other words, the graphical lasso determines the connected components of the estimated network via single linkage clustering. Unfortunately, single linkage clustering is known to perform poorly in certain settings. Therefore, we propose the cluster graphical lasso, which involves clustering the features using an alternative to single linkage clustering, and then performing the graphical lasso on the subset of variables within each cluster. We establish model selection consistency for this technique, and demonstrate its improved performance relative to the graphical lasso in a simulation study, as well as in applications to an equities data set, a university webpage data set, and a gene expression data set.

1 Introduction

Graphical models have been extensively used in various domains, including modeling of gene regulatory networks and social interaction networks. A graph consists of a set of nodes, corresponding to random variables, as well as a set of edges joining pairs of nodes. In a conditional independence graph, the absence of an edge between a pair of nodes indicates a pair of variables that are conditionally independent given the rest of the variables in the data set, and the presence of an edge indicates a pair of conditionally dependent nodes. Hence, graphical models can be used to compactly represent complex joint distributions using a set of local relationships specified by a graph. Throughout the rest of the text, we will focus on Gaussian graphical models.

Let be a matrix where is the number of observations and is the number of features; the rows of are denoted as . Assume that where is a covariance matrix. Under this simple model, there is an equivalence between a zero in the inverse covariance matrix and a pair of conditionally independent variables [MKB79]. More precisely, for some if and only if the th and th features are conditionally independent given the other variables.

Let denote the empirical covariance matrix of , defined as . A natural way to estimate is via maximum likelihood. This approach involves maximizing

with respect to , where is an optimization variable; the solution serves as an estimate for . However, in high dimensional settings where , is singular and is not invertible. Furthermore, even if is invertible, typically contains no elements that are exactly equal to zero. This corresponds to a graph in which the nodes are fully connected to each other; such a graph does not provide useful information. To overcome these problems, \citeasnounYuanLin07 proposed to maximize the penalized log likelihood

| (1) |

with respect to , penalizing only the off-diagonal elements of . A number of algorithms have been proposed to solve (1) \citeaffixedSparseInv,YuanLin07,Rothman08,YuanGlasso08,Scheinberg10among others. Note that some authors have considered a slight modification to (1) in which the diagonal elements of are also penalized. We refer to the maximizer of (1) as the graphical lasso solution; it serves as an estimate for . When the nonnegative tuning parameter is sufficiently large, the estimate will be sparse, with some elements exactly equal to zero. These zero elements correspond to pairs of variables that are estimated to be conditionally independent.

WittenFriedman11 and \citeasnounMazumderHastie11 presented the following result:

Theorem 1.

The connected components of the graphical lasso solution with tuning parameter are the same as the connected components of the undirected graph corresponding to the adjacency matrix , defined as

Here is an indicator variable that equals 1 if , and equals 0 otherwise. For instance, consider a partition of the features into two disjoint sets, and . Theorem 1 indicates that if for all and all , then the features in and are in two separated connected components of the graphical lasso solution. Theorem 1 reveals that solving problem (1) boils down to two steps:

-

1.

Identify the connected components of the undirected graph with adjacency matrix .

-

2.

Perform graphical lasso with parameter on each connected component separately.

In this paper, we will show that identifying the connected components in the graphical lasso solution – that is, Step 1 of the two-step procedure described above – is equivalent to performing single linkage hierarchical clustering (SLC) on the basis of a similarity matrix given by the absolute value of the elements of the empirical covariance matrix . However, we know that SLC tends to produce trailing clusters in which individual features are merged one at a time, especially if the data are noisy and the clusters are not clearly separated [ElemStatLearn]. In addition, the two steps of the graphical lasso algorithm are based on the same tuning parameter, , which can be suboptimal. Motivated by the connection between the graphical lasso solution and single linkage clustering, we therefore propose a new alternative to the graphical lasso. We will first perform clustering of the variables using an alternative to single linkage clustering, and then perform the graphical lasso on the subset of variables within each cluster. Our approach decouples the cutoff for the clustering step from the tuning parameter used for the graphical lasso problem. This results in improved detection of the connected components in high dimensional Gaussian graphical models, leading to more accurate network estimates. Based on this new approach, we also propose a new method for choosing the tuning parameter for the graphical lasso problem on the subset of variables in each cluster, which results in consistent identification of the connected components in the graph.

The rest of the paper is organized as follows. In Section 2, we establish a connection between the graphical lasso and single linkage clustering. In Section 3, we present our proposal for cluster graphical lasso, a modification of the graphical lasso that involves discovery of the connected components via an alternative to SLC. We prove model selection consistency of our procedure in Section 4. Simulation results are in Section LABEL:simulation, and Section LABEL:realdata contains an application of cluster graphical lasso to an equities data set, a webpage data set, and a gene expression data set. The Discussion is in Section LABEL:discussion.

2 Graphical lasso and single linkage clustering

We assume that the columns of have been standardized to have mean zero and variance one. Let denote the matrix whose elements take the form where is the th column of .

Theorem 2.

Let denote the clusters that result from performing single linkage hierarchical clustering (SLC) using similarity matrix , and cutting the resulting dendrogram at a height of . Let denote the connected components of the graphical lasso solution with tuning parameter . Then, , and there exists a permutation such that for .

Theorem 2, which is proven in the Appendix, establishes a surprising connection between two seemingly unrelated techniques: the graphical lasso and SLC. The connected components of the graphical lasso solution are identical to the clusters obtained by performing SLC based on the similarity matrix .

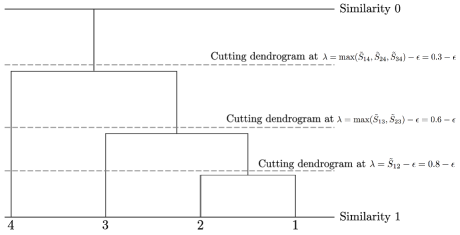

Theorem 2 refers to cutting a dendrogram that results from performing SLC using a similarity matrix. This concept is made clear in Figure 1. In this example, is given by

| (2) |

For instance, cutting the dendrogram at a height of results in three clusters, , , and . Theorem 2 further indicates that these are the same as the connected components that result from applying the graphical lasso to with tuning parameter .

3 The cluster graphical lasso

3.1 A simple alternative to SLC

Motivated by Theorem 2, as well as by the fact that the clusters identified by SLC tend to have an undesirable chain structure [ElemStatLearn], we now explore an alternative approach, in which we perform clustering before applying the graphical lasso to the set of features within each cluster.

The cluster graphical lasso (CGL) is presented in Algorithm 1.

-

1.

Let be the clusters obtained by performing a clustering method of choice based on the similarity matrix . The th cluster contains features.

-

2.

For :

-

(a)

Let be the empirical covariance matrix for the features in the th cluster. Here, is a matrix.

-

(b)

Solve the graphical lasso problem (1) using the covariance matrix with a given value of . Let denote the graphical lasso estimate.

-

(a)

-

3.

Combine the resulting graphical lasso estimates into a matrix that is block diagonal with blocks .

We partition the features into clusters based on , and then perform the graphical lasso estimation procedure on the subset of variables within each cluster. Provided that the true network has several connected components, and that the clustering technique that we use in Step 1 is better than SLC, we expect CGL to outperform graphical lasso.

Furthermore, we note that by Theorem 2, the usual graphical lasso is a special case of Algorithm 1, in which the clusters in Step 1 are obtained by cutting the SLC dendrogram at a height , and in which in Step 2(a).

The advantage of CGL over the graphical lasso is two-fold.

-

1.

As mentioned earlier, SLC often performs poorly, often resulting in estimated graphs with one large connected component, and many very small ones. Therefore, identifying the connected components using a better clustering procedure may yield improved results.

-

2.

As revealed by Theorems 1 and 2, the graphical lasso effectively couples two operations using a single tuning parameter : identification of the connected components in the network estimate, and identification of the edge set within each connected component. Therefore, in order for the graphical lasso to yield a solution with many connected components, each connected component must typically be extremely sparse. CGL allows for these two operations to be decoupled, often to advantage.

3.2 Interpretation of CGL as a penalized log likelihood problem

Consider the optimization problem

| (3) |

where

By inspection, the solution to this problem is the CGL network estimate. In other words, the CGL procedure amounts to solving a penalized log likelihood problem in which we impose an arbitrarily large penalty on if the th and th features are in different clusters. In contrast, if in (3), then this amounts to the graphical lasso optimization problem (1).

3.3 Tuning parameter selection

CGL involves several tuning parameters: the number of clusters and the sparsity parameters . It is well-known that selecting tuning parameters in unsupervised settings is a challenging problem \citeaffixedMC85,Gordon96,TWH2000,ElemStatLearn,StabilitySelectionfor an overview and several past proposals, see e.g.. Algorithm 2 outlines an approach for selecting . It involves leaving out random elements from the matrix and performing clustering. The clusters obtained are then used to impute the left-out elements, and the corresponding mean squared error is computed. Roughly speaking, the optimal is that for which the mean squared error is smallest. This is related to past approaches in the literature for performing tuning parameter selection in the unsupervised setting by recasting the unsupervised problem as a supervised one \citeaffixedWold1978,OwenPerry2008,WittenHastieTibs09see e.g.. The numerical investigation in Section LABEL:simulation indicates that our algorithm results in reasonable estimates of the number of connected components, and that the performance of CGL is not very sensitive to the value of .

In Corollary LABEL:chooselambdacorr, we propose a choice of that guarantees consistent recovery of the connected components.

-

1.

Repeat the following procedure times:

-

(a)

Let be a set that contains elements of the form , where is drawn randomly from . Augment the set such that if , then . We refer to as a set of missing elements.

-

(b)

Construct a matrix, , for which the elements in are removed and are replaced by taking the average of the corresponding row and column means of the non-missing elements in :

(4) where and is the cardinality of .

-

(c)

For each value of under consideration:

-

i.

Perform the clustering method of choice based on the similarity matrix . Let denote the clusters obtained.

-

ii.

Construct a matrix in which each element is imputed using the block structure of based on the clusters obtained:

(5) -

iii.

Calculate the mean squared error as follows:

(6)

-

i.

-

(a)

-

2.

For each value of that was considered in Step 1(c), calculate , the mean of quantity (6) over the iterations, as well as , its standard error.

-

3.

Identify the set . Select the smallest value in this set.

4 Consistency of cluster graphical lasso

In this section, we establish that CGL consistently recovers the connected components of the underlying graph, as well as its edge set. A number of authors have shown consistency of the graphical lasso solution for different matrix norms [Rothman08, LamFan2009, CaietalJASA11]. \citeasnounLamFan2009 further showed that under certain conditions, the graphical lasso solution is sparsistent, i.e., zero entries of the inverse covariance matrix are correctly estimated with probability tending to one. \citeasnounLamFan2009 also showed that there is no choice of that can simultaneously achieve the optimal rate of sparsistency and consistency for estimating , unless the number of non-zero elements in the off-diagonal entries is no larger than . In a more recent work, \citeasnounRavikumar2011 studied the graphical lasso estimator under a variety of tail conditions, and established that the procedure correctly identifies the structure of the graph, if an incoherence assumption holds on the Hessian of the inverse covariance matrix, and if the minimum non-zero entry of the inverse covariance matrix is sufficiently large. We will restate these conditions more precisely in Theorem LABEL:thm:CGLconsistency.

Here, we focus on model selection consistency of CGL, in the setting where the inverse covariance matrix is block diagonal. To establish the model selection consistency of CGL, we need to show that (i) CGL correctly identifies the connected components of the graph, and (ii) it correctly identifies the set of edges (i.e. the set of non-zero values of the inverse covariance matrix) within each of the connected components. More specifically, we first show that CGL with clusters obtained from performing SLC, average linkage hierarchical clustering (ALC), or complete linkage hierarchical clustering (CLC) based on consistently identifies the connected components of the graph. Next, we adapt the results of \citeasnounRavikumar2011 on model selection consistency of graphical lasso in order to establish the rates of convergence of the CGL estimate.

As we will show below, our results highlight the potential advantages of CGL in the settings where the underlying inverse covariance matrix is block diagonal (i.e. the graph consists of multiple connected components). As a byproduct, we also address the problem of determining the appropriate set of tuning parameters for penalized estimation of the inverse covariance matrix in high dimensions: given knowledge of , the number of connected components in the graph, we suggest a choice of for CGL that leads to consistent identification of the connected components in the underlying network. In the context of the graphical lasso, \citeasnounBanerjee have suggested a choice of such that the probability of adding edges between two disconnected components is bounded by , given by

| (7) |

where denotes the percentile of the Student’s t-distribution with degrees of freedom, and is the empirical variance of the th variable. The proposal of \citeasnounBanerjee is based on an earlier result by \citeasnounMB2006, who suggested a similar choice of for estimating the edge set of the graph using the neighborhood selection approach. Note that (7) is fundamentally different from our proposal, as this choice of does not guarantee that each connected component is not broken into several distinct connected components. In fact, empirical studies have found that the choice of in (7) may result in an estimated graph that is too sparse [Shojaieetal2012].

Before we continue, we summarize some notation that will be used in Sections 4.1 and LABEL:modelselection. Let be a matrix; the rows of are denoted as , where and is a block diagonal covariance matrix with blocks. We let be the feature set corresponding to the th block. (In previous sections, denoted a set of estimated clusters; in this section only, are the true and in practice unknown clusters.) Also, let denote a set of estimated clusters obtained from performing SLC, ALC, or CLC. In what follows, we use the terms clusters and connected components interchangeably. Let be the absolute empirical covariance matrix. Proofs of what follows are provided in the Appendix.

4.1 Consistent recovery of the connected components

We now present some results on the recovery of the connected components of by SLC, ALC, or CLC, as well as its implications for the CGL procedure.