Assessing Financial Model Risk

Abstract

Model risk has a huge impact on any risk measurement procedure and its quantification is therefore a crucial step. In this paper, we introduce three quantitative measures of model risk when choosing a particular reference model within a given class: the absolute measure of model risk, the relative measure of model risk and the local measure of model risk. Each of the measures has a specific purpose and so allows for flexibility. We illustrate the various notions by studying some relevant examples, so as to emphasize the practicability and tractability of our approach.

1 Introduction

The specification of a model is a crucial step when measuring financial risks to which a portfolio is exposed. Common methodologies, such as Delta-Normal or simulation methods, are based on the choice of a particular model for the risk factors. Even when using historical methods, we implicitly rely on the empirical distribution as the reference model. However, it is observed that the final risk figure is often quite sensitive to the choice of the model. The hazard of working with a potentially not well-suited model is referred to as model risk. The study of the impact of model risk and its quantification is an important step in the whole risk measurement procedure. In particular, in the aftermath of the recent financial crisis, understanding model uncertainty when assessing the regulatory capital requirements for financial institutions seems to be crucial. The main goal of this paper is precisely to propose some ways to quantify model risk when measuring financial risks for regulatory purposes. We stress that our objective is not to measure risk in the presence of model uncertainty, but to quantify model risk itself.

The question of the impact of model risk has received increasing attention in recent years. In particular, the significance of minimum risk portfolios has been questioned when studying the problem of optimal asset allocation: several authors (among them El Ghaoui et al. 2003, Natarajan et al. 2008, Chen et al. 2010, Zymler et al. 2013) have recently considered this issue from a robust optimization perspective.

Our approach to assessing model risk is very general. It is based on the specification of a set of alternative models (or distributions) around a reference one. Note that Kerkhof et al. (2010) propose measuring model risk in a similar setting by computing the worst-case risk measure over a tolerance set of models. Our approach differs, however, as we introduce different measures of model risk, based on both the worst- and best-case risk measures, in order to serve different purposes.

Examples of the set of alternative models we can consider include parametric or non-parametric families of distributions, or small perturbations of a given distribution. If we believe in a parametric model, we can consider all distributions within the family whose parameters are in the confidence intervals derived from the data. By doing this, we are accounting only for the estimation risk (see Kerkhof et al. 2010). If, on the other hand, we completely believe in some estimated quantities (for instance, mean and variance), without relying on confidence intervals, we can consider all possible distributions of any form which are in accordance with those quantities (for instance, they have the same mean and variance). We can also consider those distributions which are not too far from a reference one, according to some statistical distance (the uniform distance, for instance), or all joint distributions that have the same marginals as the reference one. This latter example leads to the relevant problem of aggregation of risks in a portfolio (see Embrechts et al 2013). We could even specify different pricing models if the portfolio contains derivatives.

Note that the scope of our approach is very wide, going beyond issues pertaining just to statistical estimation. Furthermore, the assessment of model risk should not be confused with the analysis of statistical robustness of a risk measurement procedure (as in Cont et al. 2010), even though the two concepts are related. Indeed, the reference distribution is an input in our approach, while in Cont et al. (2010) it is the result of a statistical estimation process which is part of the definition of robustness itself.

In order to assess model risk, we introduce three different measures: the absolute measure of model risk, the relative measure of model risk and the local measure of model risk. Our aim is to provide a quantitative measure of the model risk we are exposed to in choosing a particular reference model within a given class when working with a specific risk measure. All three measures are pure numbers, independent from the reference currency. They take non-negative values and vanish precisely when there is no model risk. Each of the measures we propose has a specific purpose: whilst the absolute measure is cardinal and gives a quantitative assessment of model risk, both the relative measure and the local measure are ordinal and allow for comparison of different situations, which may have different scales. If we consider different possible models as references, the use of the relative measure is probably the more natural measure to use as it will give a clear ranking between the alternatives. When the reference model is almost certain, the local measure becomes an obvious choice as it focuses on the very local properties around the reference model.

In addition, we obtain explicit and closed-form formulae in some interesting situations when considering either the Value-at-Risk or the Expected Shortfall as reference risk measure and alternative sets of distributions based on fixed moments or small perturbations based on some standard statistical distances.

2 A motivating example

In this section, we start by looking at the Basel multiplier, introduced by the Basel Committee as an ingredient in the assessment of the capital requirements for financial institutions. As we will see, this multiplier is closely related to probabilistic bounds giving some upper limit to classical risk measures such as the Value-at-Risk and the Expected Shortfall. These preliminary remarks will motivate our approach when introducing some measures for model risk in the next section.

2.1 The Basel multiplier

Within the Basel framework, financial institutions are allowed to use internal models to assess the capital requirement due to market risk. The capital charge is actually the sum of six terms taking into account different facets of market risk. The term that measures risk in usual conditions is given by the following formula:

| (1) |

where is the portfolio’s Value-at-Risk (of order and with a -day horizon) computed today, while is the figure we obtained days ago.

The constant is called the multiplier and it is assigned to each institution by the regulator, which periodically revises it. Its minimum value is , but it can be increased up to in the event that the risk measurement system provides poor back-testing performances. Given the magnitude of , it is apparent that in normal conditions the second term is the leading one in the maximum appearing in (1).

2.2 Chebishev bounds and the multiplier

Stahl (1997) offered a simple theoretical justification for the multiplier to be chosen in the range . Here, we briefly summarize his argument. Let be the random variable (r.v.) describing the Profits-and-Losses of a portfolio due to market risk. If the time-horizon is short, it is usually assumed that , so that

where is the variance of and is standard, i.e. it has zero mean and unit variance. While is a matter of estimation, depends on the assumption we make about the type of the distribution of (normal, Student-t, etc.).

An application of the Chebishev inequality to yields

| (2) |

Recalling the definition of , it readily follows , or

| (3) |

The right hand side of the above inequality thus provides an upper bound for the VaR of a random variable having mean and variance . It can be compared with the VaR we obtain by using the delta-normal method, which is very commonly employed in practice. According to this method, is normally distributed and therefore

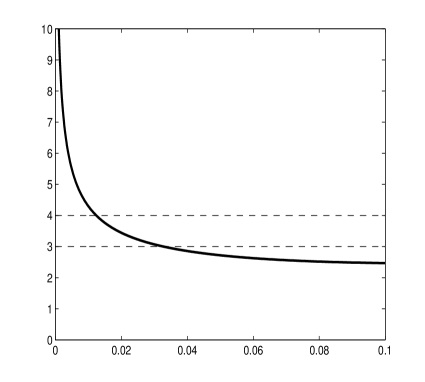

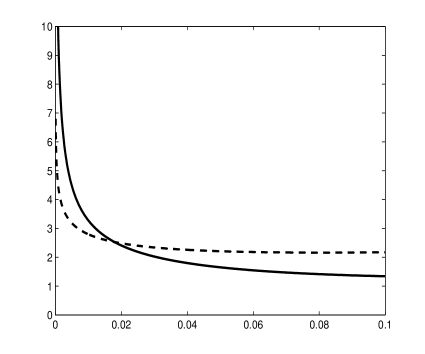

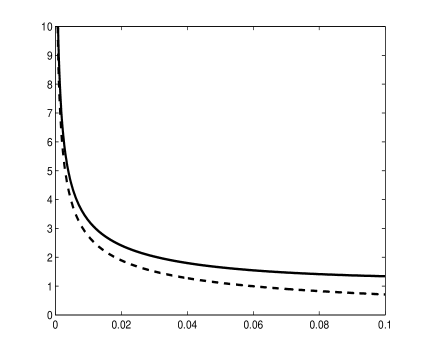

where is the quantile of a standard normal. The graph of the ratio

| (4) |

is reported below (see Figure 1, left). We can see that for usual values of (i.e. from to ), the ratio broadly lies in the interval . Therefore, if the VaR computed under normal assumptions is multiplied by , we obtain an upper bound for the worst possible VaR compatible with partial information (mean and variance) we have.

We can then extend this argument to the Expected Shortfall.333Also see Leippold and Vanini (2002) Indeed, by integrating inequality (3), we obtain

| (5) |

The upper bound has to be compared with the Expected Shortfall under normal assumptions, which is

where is the density of a standard normal. From the graph of the ratio

(see Figure 1, right) we see that a proper multiplier for the Expected Shortfall would be in the range .

The second inequality in (2) is sharp, i.e. it cannot be improved for any . However, the first inequality is certainly not sharp and this means that the upper bounds for VaR and Expected Shortfall that we derived above are not optimal ones.

2.3 Cantelli bounds and improvement of the multiplier

Better results for the bounds can be achieved by using the Cantelli inequality which concentrates on a single tail. A possible version of this inequality states that for a standard r.v. , the following inequality holds true:

| (6) |

From (6) it readily follows that

| (7) |

for any random variable having mean and variance . We see that this latter bound improves on (3). Nevertheless, the ratio between this bound and the VaR computed under normal assumptions broadly remains between and .

2.4 Sharp bounds and significance of the multiplier

It is well known that the Cantelli inequality provides a sharp upper bound on the tail probability.444See for instance Billingsley (1995), Section 5. To put it another way, the following holds true:

This means that is a sharp upper bound on for standard (see also Lemma 4.2 below). By contrast, the bound (8), being an integral of sharp bounds, is not necessarily sharp. Indeed, we will recall later that the sharp bound is, in this case, .

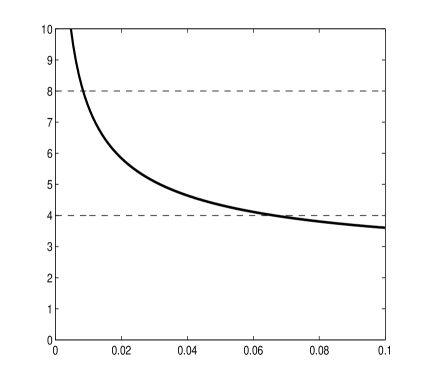

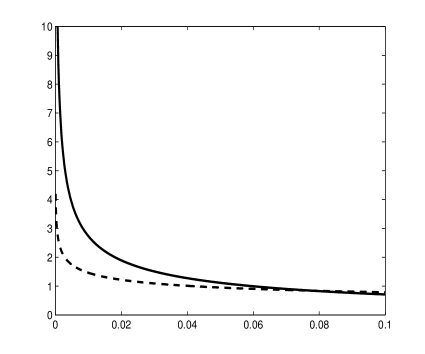

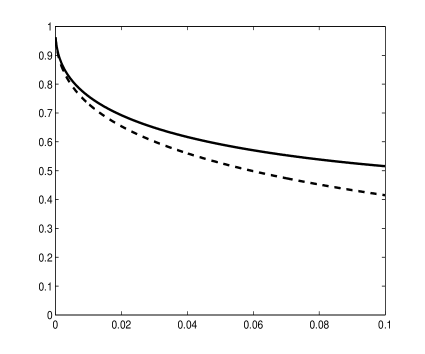

We can plot the ratio between the sharp upper bound and the risk measure computed under Gaussian hypotheses and compare it with the ratio we obtained before, using the Chebishev bounds. The results are in Figure 2. We can notice that for the Expected Shortfall, the actual ratio (i.e. the one based on the sharp bound) is much lower than the ratio based on the Chebishev bound and the actual multiplier should be in the range for the Expected Shortfall as well. This also means that assessing the impact of model uncertainty using Chebishev bounds can give us misleading answers regarding the Expected Shortfall.

Therefore, it becomes apparent that an accurate analysis and understanding of the sharp bounds for the considered risk measure is essential in the assessment of model risk. Any other bounds may lead to an inaccurate assessment of the model risk and as a consequence to potential errors in any associated decision process. For that reason, in this paper we introduce different measures of model risk based on sharp bounds (both lower and upper bounds). The explicit computation of those bounds will then be a crucial step.

3 Absolute and relative measures of model risk

In this section, we introduce two different notions of measures of model risk. We will work with a given risk measure, a given reference model and a set of alternative models. Our aim is to provide a quantitative measure of the model risk we are exposed to in choosing this particular reference model within a given class when working with a specific risk measure. Two measures are introduced: the absolute measure of model risk provides a cardinal measure whilst the relative measure of model risk is ordinal and allows for comparison between various situations.

3.1 Notation

We first introduce some basic notation and assumptions to be used here and in the sequel to this paper. A probability space is given and we assume it to be atomless.555This ensures, for any distribution , the existence of a r.v. distributed as . For any r.v. defined on , let be the associated distribution function, i.e. , and

be the (lower) quantile of order . We will write if and if . In this paper, a risk measure is a map , defined on some space of r.v. and satisfying the following properties

-

•

law invariance: whenever

-

•

positive homogeneity: for any

-

•

translation invariance: for any

We remark that, for fixed , both the Value-at-Risk

and the Expected Shortfall

satisfy these assumptions. We stress that Value-at-Risk is defined over all random variables, while the Expected Shortfall requires an integrability condition on the left tail of . More generally any law-invariant coherent risk measure falls in our framework, a chief example being the class of spectral risk measures (see Acerbi 2002). In view of the law invariance property, we can alternatively regard a risk measure as a functional directly defined on a suitable set of distributions. Indeed, with a slight abuse of notation, we can set for .

3.2 Definitions

We now introduce two measures of model risk. Both measures are associated to a risk measure , a r.v. , to act as a reference distribution hypothesis, and a set of r.v., to act as alternative distribution hypotheses. In this paper, we do not discuss the selection procedure for the reference distribution, and refer to Alexander and Sarabia (2012), where some specific criteria are reviewed. We assume that . We also assume that both quantities

are finite and that . Clearly, the inequalities hold true. Finally, we assume that : this is not a restrictive hypothesis as the measured risk of financial positions is usually positive. We are ready to give the two definitions of model risk.

Definition 3.1

The absolute measure of model risk associated to , and is666For the sake of simplicity, we drop the obvious dependence on .

The relative measure of model risk is

The absolute measure is a concept which in a sense generalizes the Basel multiplier: indeed, by multiplying by we reach the maximum risk that is attainable within . So, if we interpret as a set of possible departures from the reference model , then quantifies how bad the worst possible case is. Plainly, with (i.e. no model risk) if and only if has already a worst-case distribution, i.e. .

It is apparent that, for given and , the larger is the greater is, as is increasing in . This justifies the qualifier absolute that we give to , even though it comes in the form of a ratio.

By contrast, has a relative behaviour. Indeed, the difference is divided by the whole range . As a consequence, it is immediately seen that

We observe or precisely when (no model risk) or (full model risk). In other words, it focuses on the relative position of within the range and not only on the position with respect to the supremum. In the next section, we will also see that need not be increasing in , thus providing a relative assessment of model risk.

Remark 3.2

Using the previous notation, the measure of model risk introduced in Kerkhof et al (2010) is

We note that this measure is also non-negative and vanishes precisely when there is no model risk. However, it is expressed in terms of a given currency and depends on the scale of the risk . Since , the absolute measure proposed here is a unit-less version of , normalized by the size of the risk. We think that this normalization allows us to use also as a comparison tool between different situations.

Remark 3.3

In the different context of derivative pricing, Cont (2006) proposed a measure of model risk which is based on the computation of extremal prices using a set of pricing measures. The obtained measure is formally similar to our definitions.

3.3 Properties

In the next proposition, we collect some basic properties of the two measures of model risk previously introduced. For any we define

Proposition 3.4

For any and it holds

and

Proof.

The proof is trivial once we observe that for and

and .

For given and , consider the set

where the first two moments are fixed. The standardized version of is defined by

Setting and in Proposition 3.4 we immediately obtain

Corollary 3.5

If and , then

where . In particular

In what follows we shall be mainly interested in measuring model risk with respect to , or some subsets. In view of the last result, we will concentrate on the particular case , provided we standardize the reference r.v. .

Next, we observe that, for fixed and , the relative measure of model risk comes in the form

| (9) |

where is positive. If is a convex map, as is the case with the Expected Shortfall, or more generally with the class of (law-invariant) convex risk measures, then is concave.777Provided, of course, a certain convex combination of two r.v. in remains in . So, for instance, if , and are in and , then

Such an inequality can be partly explained by the fact that the model risk associated with is due both to the model risk of the marginals and to the model risk of the joint distribution.

Thanks to (9), we see that other possible properties for (like monotonicity, continuity, etc.) are inherited from similar properties of the risk measure. Subadditivity, a property which is fulfilled by all coherent risk measures, is an exception. Indeed, if we know that , and that we can only conclude that

and subadditivity is ensured only if the last term in the right hand side is sufficiently small.

4 Some examples

In this section, we illustrate both measures of model risk and study the following example: we consider a r.v. with a reference distribution in the set , which corresponds to the set of all r.v. with mean and standard deviation , and we estimate both measures of model risk for two measures of risk, namely VaR and Expected Shortfall. Without any loss of generality, as previously discussed, we can restrict our attention to the particular case where the set of r.v. is .

Before focusing on our examples, we give a preliminary result on extremal quantiles on a general set that will be useful for the rest of the paper.

4.1 Preliminary result on extremal quantiles

Let be a general set of r.v. and and the extremal functions on defined, for any , as:

Note that , and that both and are non-decreasing functions888Note that both and are not necessarily càdlàg. However the set of points on which they are not càdlàg is at most countable. We will refer to them as the maximal function and the minimal function respectively. Note also that these functions are not necessarily distribution functions as it may happen that and/or .

Remark 4.1

If and are indeed distribution functions, they are extremal in the sense of the first order stochastic dominance (denoted ). This means that

and that if and are two distribution functions satisfying , , then and .

The following result on extremal quantiles will be very useful in the rest of the paper.

Lemma 4.2

Assume that . If and are invertible functions,999Except, respectively, on the sets and . then for any it holds

| (10) |

If both and are distribution functions, then (10) holds true for any .

Proof.

We prove the result for the infimum only, as a similar argument leads to the result for the supremum. If , then by assumption is well defined.

Let us assume by contradiction that . Then for any we have , hence for , by the very definition of quantile. It follows that for , but this is in contrast with the fact that, by assumption, is strictly increasing.

If instead we assume that , then there exists some such that . As is strictly increasing, we have

However, by definition of quantile, it always holds and we have reached a contradiction. We then conclude that .

Remark 4.3

The following example underlines the importance of the invertibility of and in Lemma 4.2. Without this assumption the equalities in (10) need not hold even if we replace or by the generalized inverses (i.e. the quantile functions). Fix and consider the sequence of r.v. where takes the value with probability and the value with probability . It is easy to check that

If , we have even though for any . So, (10) does not hold in this case.

4.2 Model risk for VaR

Following Section 4 in Royden (1953) and Chapter 3, Section 4 in Hürlimann (2008), using classical Chebyshev-Markov inequalities, the extremal functions on are distributions and are given as follows:

These extremal distributions are often called, respectively, maximal and minimal Chebyshev-Markov distributions for . Note, however, that both extremal distributions and are not in . In fact, the mean of is negative, the mean of is positive and both variances are infinite.

From Lemma 4.2, as both and are invertible, the following identities prevail for the extremum quantiles (see for instance Hürlimann 2002, Theorem 3.1, or Bertsimas et al. 2004, Theorem 2):

As a straightforward consequence of the extremal quantiles, the following result holds true:

Proposition 4.4

The absolute measure of model risk for at is:

The relative measure of model risk for at is:

This result will be illustrated later in Subsection 4.4.

Remark 4.5

Note that and . Therefore, in the class , some distributions are acceptable, meaning that they have negative risk, while others are not. In the case of , when , if , then all distributions are acceptable. When , if , then all distributions are non-acceptable.

Remark 4.6

As pointed out by Hürlimann (2008) (Chapter 4, Section 3), knowledge of the skewness does not improve the Chebyshev extremal distributions when considering distributions over . Therefore, if :

where and denotes the skewness of .

4.3 Model risk for Expected Shortfall

Adopting a similar approach for the Expected Shortfall is not so easy since the Lemma 4.2 gives a result on the extremal quantiles, but not on the extremal Expected Shortfalls. However, a recent result by Bertsimas et al. (2004) (Theorem 2) using arguments from convex analysis gives the following identities for the extremal Expected Shortfalls on the set :

| (11) | ||||

| (12) |

To our knowledge, similar results for a general set have not been obtained.

As a straightforward consequence, the following result on model risk holds true:

Proposition 4.7

The absolute measure of model risk for at is:

The relative measure of model risk for at is:

This result will be illustrated later in Subsection 4.4.

Remark 4.8

As mentioned earlier, we cannot use Lemma 4.2 to obtain the Extremal Shortfalls. However, we may wonder whether the Extremal Shortfalls in (11) are obtained as Expected Shortfalls of some extremal distributions. Since the Expected Shortfall is monotone with respect to the stop-loss order (see for instance Bäuerle and Müller (2006)), we look at the extremal distributions for the stop-loss order on the set . Following Hürlimann (2002), we use the fact that the stop-loss transform for a distribution is defined as:

By simple calculation, we have:

Such a relationship also holds true for the extremal stop-loss distributions (see for instance Equation (1.3) in Hürlimann (2002)):

where

and the same holds true for the infimum.

Therefore, in order to get the extremal stop-loss distributions, we first need to obtain the extremal stop-loss transforms. For the maximum stop-loss transform, we refer to Theorem 2 in Jansen et al. (1986) and obtain:

For the minimum stop-loss transform, we refer to Table 5.2 Section 5., Chapter 3 in Hürlimann (2008):

Finally, we obtain the extremal stop-loss distributions:

We finally obtain, using Equation (11) that:

and

Note that using the extremal distributions and for the first-order stochastic dominance will give us some bounds which are not sharp as discussed earlier in Subsection 2.3 (in particular Equation (8)).

4.4 Illustration

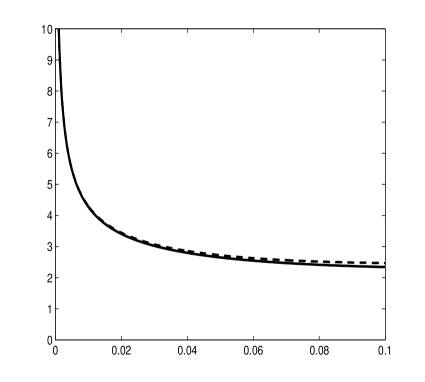

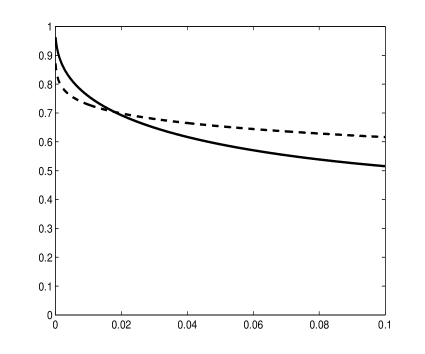

We numerically compute both measures of model risk for standard (i.e. in ) r.v. following the normal or Student-t distribution. We are especially interested in the dependence of the measures on the order of the Value at Risk or the Expected Shortfall. This dependence is depicted in Figures 3 and 4.

It is natural to expect that using a reference fat-tailed distribution (Student-t) yields lower model risk than starting with a normal one. While for the Expected Shortfall this is true for any practical101010Precisely, for . See Figures 3 (right) and 4 (right). value of , for the Value-at-Risk this holds only for small enough ().

We can also notice that the relative measure of model risk, for both VaR and Expected Shortfall and for both distributions, goes to as . In other words, as we go further in the (left) tails, any given distribution departs more and more from the worst case. We think this is a general behaviour, although we offer no proof for this claim.

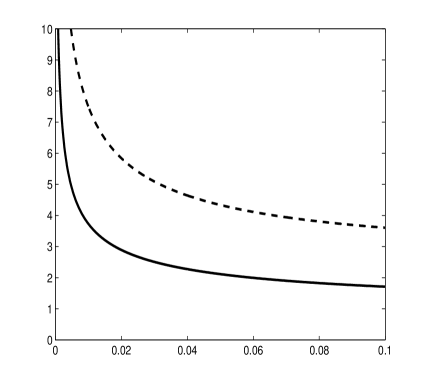

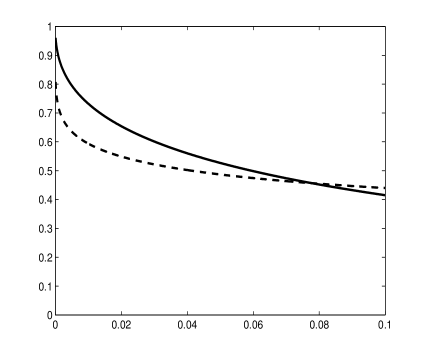

The graphs in Figure 5 compare the absolute (left) and relative (right) measure of model risk for VaR and Expected Shortfall, using a normal reference distribution. We see that in both cases the Expected Shortfall has a lower level of model risk. By taking a Student-t as the reference distribution we obtain a similar behaviour. This is probably at odds with what we would expect: indeed, it is often said that Expected Shortfall is more sensitive to the model choice than VaR as the former depends on the whole left tail.111111See also the related discussion on statistical robustness in Cont et al. (2010). Instead, at least with respect to our two measures of model risk, the opposite proves true.

5 Local measure of model risk

In this section we introduce a local measure of model risk, by taking the limit of the relative measure on a family of perturbation sets that shrink to the singleton . This measure attempts to assess model risk for infinitesimal perturbations.

5.1 The definition

Let be a family of sets, each one contained in and such that

This means that whenever and . Below, we will see some examples based on distances and on mixtures.

Definition 5.1

The local measure of model risk associated to , and the family is

provided the limit exists.

The limit defining is evidently in the form ; however, if it exists, then it is in the interval as for any . The local measure describes the relative position of with respect to the worst and best cases for infinitesimal perturbations.

5.2 An example based on distances

In what follows, we will consider the case for some , so that is the set of all r.v. and we will make no reference at it in the definition of . As a first example of computation of the local model risk, consider the family of sets defined by:

| (13) |

where is some given distance between distributions. It can immediately be recognized that such a family satisfies the assumptions stated above. In particular, we can consider the Kolmogorov (or uniform) distance

or the Lévy distance

Proposition 5.2

Proof.

If it can immediately be seen that

| (14) |

From now on, let , so that

By assumption, is invertible and therefore both and are invertible; an immediate computation shows that

We can then apply Lemma 4.2, obtaining

and therefore

as . Finally, if is the density of , by applying de l’Hôpital’s rule we have

In the case we start by observing that and and then proceed similarly as above.

This result is quite natural as the set of perturbations is in a sense asymptotically symmetrical around . Therefore the relative measure of model risk converges to . However, we stress that this is true only in the limit and not for a fixed .

5.3 An example based on mixtures

Let be the distribution of ; for define

| (15) |

The set collects all (r.v. distributed as) mixtures between and a distribution of a standard r.v. , for which the alternative distribution () is not weighted too much. It is worth noting that for any : indeed, both the mean and the variance are affine functions of the distributions.

Remark 5.3

We stress that is in general not the distribution of , even if we assume and to be independent. Rather, it is the distribution of , where is an event of probability , independent from both and , and denotes its indicator function.

Proposition 5.4

Proof.

The maximal function for is

where we have used in deriving the last equality. Since both and are invertible (the former by assumption), too is invertible and therefore, applying Lemma 4.2, we have

| (16) |

Using a similar argument, we find that

| (17) |

where . As a consequence, the local measure of model risk is

| (18) |

If we set , then, by definition

Differentiating (in ) both sides, we obtain

where is the density of . Setting and observing that , so that , we readily obtain121212A similar proof can also be found in Barrieu and Ravanelli (2013)

In a very similar way, we can prove that satisfies

Applying de l’Hôpital’s rule to (18) and simplifying the result we obtain

As by assumption, we have

and we reach the final result as an immediate computation.

Remark 5.5

As an illustration we compute the local measure of model risk when is standard normal or Student-t (see Figure 6). Consistent with the observations we made in the last section, regarding the relative measure, we see that starting with a fat-tailed reference distribution yields a lower local measure with respect to a normal distribution only when is small enough.

6 Conclusion

The study of the impact of model risk and its quantification is an essential part of the whole risk measurement procedure. In this paper, we introduce three quantitative measures of the model risk when choosing a particular reference model within a given class: the absolute measure of model risk, the relative measure of model risk and the local measure of model risk. Each of the measures we propose has a specific purpose and so allows for flexibility in their use. We obtain explicit formulae in some interesting cases, in order to emphasize the practicability and tractability of our approach. However, our contribution is not limited to the study of these particular examples and our measures of model risk can be applied to more general settings.

References

- [1] Acerbi, C. 2002. Spectral measures of risk: a coherent representation of subjective risk aversion. Journal of Banking & Finance 26(7) 1505-1518

- [2] Alexander, C., J.M. Sarabia. 2012. Quantile uncertainty and Value-at-Risk model risk. Risk Analysis 32(8) 1293-1308.

- [3] Barrieu, P., C. Ravanelli. 2013. Robust capital requirements under model risk. Working paper, FINRISK.

- [4] Bäuerle, N., A. Müller. 2006. Stochastic orders and risk measures: Consistency and Bounds. Insurance: Mathematics and Economics 38 132-148.

- [5] Berstimas, D., G.J. Lauprete, A. Samarov. 2004. Shortfall as a risk measure: properties, optimization and applications. J. of Econ. Dyn. Con. 28 1353-1381.

- [6] Billingsley, P. 1995. Probability and measure. (3rd ed.). John Wiley & Sons.

- [7] Chen, W., M. Sim, J. Sun, C.P. Teo. 2010. From CVaR to uncertainty set: Implications in joint chance constrained optimization. Operations Research 58 (2) 470-485.

- [8] Cont, R. 2006. Model uncertainty and its impact on the pricing of derivative instruments Mathematical finance 16(3) 519-547.

- [9] Cont, R., R. Deguest, G. Scandolo. 2010. Robustness and sensitivity analysis of risk measurement procedures. Quantitative Finance 10(6) 593 606.

- [10] El Ghaoui, L., M. Oks, F. Oustry. 2003. Worst-case value-at-risk and robust portfolio optimization: a conic programming approach. Operations Research 51(4) 543-556.

- [11] Embrechts, P., G. Puccetti, L. Rüschendorf. 2013. Model uncertainty and VaR aggregation. Journal of Banking and Finance (to appear).

- [12] Hürlimann, W. 2002. Analytical bounds for two Value-At-Risk functionals. ASTIN Bulletin 32(2) 235-265.

- [13] Hürlimann, W. 2008. Extremal moment methods and stochastic orders. Boletin de la Associacion Matematica Venezolana 15(2) 153-301.

- [14] Jansen, K., J. Haezendonck, M.J. Goovaerts. 1986. Analytical upper bounds on stop-loss premiums in case of known moments up to the fourth order. Insurance: Mathematics and Economics 5 315-334.

- [15] Kerkhof, J., B. Melenberg, H. Schumacher. 2010. Model risk and capital reserves. Journal of Banking and Finance 34 267-279.

- [16] Leippold, M., P. Vanini. 2002. Half as many cheers: the multiplier reviewed. The Wilmott Magazine 2 251-274.

- [17] Natarajan, K., D. Pachamanova, M. Sim. 2008. Incorporating asymmetric distributional information in robust value-at-risk optimization. Management Science 54(3) 573-585.

- [18] Royden, H.L. 1953. Bounds on a distribution function when its first moments are given. The Annals of Mathematical Statistics 24(3) 361-376.

- [19] Stahl, G. 1997. Three cheers. Risk Magazine 10(5) 67-69.

- [20] Zymler, S., D. Kuhn, B. Rustem. 2013. Worst-case Value-at-Risk of nonlinear portfolios, Management Science 59(1) 172-188.