EXPANSION FOR MOMENTS OF REGRESSION QUANTILES WITH APPLICATIONS TO NONPARAMETRIC TESTING

Enno Mammen

Heidelberg University, Germany

Institut für Angewandte Mathematik,

Universität Heidelberg,

Im Neuenheimer Feld 205,

69120 Heidelberg,

Germany. E-mail address: mammen@math.uni-heidelberg.de.

Ingrid Van Keilegom

KU Leuven, Belgium

ORSTAT, KU Leuven, Naamsestraat 69, 3000 Leuven, Belgium. E-mail address: ingrid.vankeilegom@kuleuven.be.

Kyusang Yu

Konkuk University, Seoul, Korea

Department of Applied Statistics, Konkuk University, Seoul 143-701, Korea, E-mail address:

kyusangu@konkuk.ac.kr

.

Abstract

We discuss nonparametric tests for parametric specifications of regression quantiles. The test is based on the comparison of parametric and nonparametric fits of these quantiles. The nonparametric fit is a Nadaraya-Watson quantile smoothing estimator.

An asymptotic treatment of the test statistic requires the development of new mathematical arguments. An approach that makes only use of plugging in a Bahadur expansion of the nonparametric estimator is not satisfactory. It requires too strong conditions on the dimension and the choice of the bandwidth.

Our alternative mathematical approach requires the calculation of moments of Nadaraya-Watson quantile regression estimators. This calculation is done by application of higher order Edgeworth expansions.

Consider a data set of i.i.d. tuples , where is a one-dimensional response variable and is a -dimensional covariate. For we denote the conditional -quantile of given by .

Thus we can write

(1)

with error variables that fulfill . Here, is the -quantile of the conditional distribution of given . Consider the null hypothesis

(2)

where is a parametric class of regression quantiles, is a compact subset of and . The set can be a singleton , but can also be a closed subset of if a set of quantile functions is checked.

In this paper we aim at studying a test statistic for , and to study its asymptotic properties under the null and the alternative. We will see that this problem is an example of a quantile model where the asymptotics cannot be developed by standard tools of quantile regression. In particular, a direct application of Bahadur expansions requires assumptions that are too restrictive.

Our test statistic is based on kernel smoothing. Let , where is a one-dimensional density function defined on , and let be a -dimensional bandwidth parameter. We assume that all bandwidths are of the same order. For simplicity of notation we further assume that they are identical and by abuse of notation we write . For any and any in the support of , let be the conditional distribution function of , given , and let be the -quantile of given that . Define

where , and and where is an estimator of .

Note that instead of estimating the conditional quantile by the above estimator, we could have considered the alternative estimator

However, the latter estimator has the important drawback that the consideration of responses in a neighborhood of induces a smoothing bias, whereas has no smoothing related bias, since it is based on the errors , whose conditional quantile of order is exactly zero under for all .

We suppose that is a closed subinterval of . We define the following test statistic :

(3)

for some weight function .

For the case that contains only one value we use

(4)

for some weight function . One could also generalize our results to the case that is a finite set. To keep notation simple we omit this case in our mathematical analysis.

Our test is an omnibus test that has power against all types of alternatives. It is based on the comparison of a kernel quantile estimator with the parametric fit. We will show that the test statistic is asymptotically equivalent to a weighted -distance between the nonparametric and the parametric estimator. Similar tests have been used in a series of papers for mean regression. Early references are Härdle and Mammen (1993), González-Manteiga and Cao-Abad (1993), Hjellvik, Yao and Tjøstheim (1998), Zheng (1996) and Fan, Zhang and Zhang (2001). Furthermore recent references are Dette and Sprekelsen (2004), Kreiss, Neumann and Yao (2008), Haag (2008), Leucht (2012), Gao and Hong (2008) and Ait-Sahalia, Fan and Peng (2009). Most of the more recent work concentrates on time series data.

The classical way to carry over results from parametric and nonparametric mean regression to quantile regression is the use of Bahadur expansions. The main point is that asymptotically quantile regression is equivalent to weighted mean regression. This approach has been used in Chaudhuri (1991), Truong (1989), He and Ng (1999), He, Ng and Portnoy (1998) and more recently in Hoderlein and Mammen (2009), Hong (2003), Kong, Linton and Xia (2010), Lee and Lee (2008), El Ghouch and Van Keilegom (2009), Li and Racine (2008), and De Backer, El Ghouch and Van Keilegom (2017). A detailed review of quantile regression can be found in the book by Koenker (2005). Testing procedures in quantile regression were considered in Zheng (1998), Koenker and Machado (1999), Bierens and Ginther (2001), Horowitz and Spokoiny (2002), Koenker and Xiao (2002), and He and Zhu (2003), among others. They all considered tests for the parametric form of the quantile function.

More recently, Rothe and Wied (2013) proposed a test statistic for the hypothesis that the conditional distribution belongs to a certain parametric class.

Tests based on quantiles of the errors have also been considered in Su and White (2012) in the context of testing conditional independence.

Other recent papers are the ones by Volgushev et al. (2013) and Conde-Amboage, Sánchez-Sellero and González-Manteiga (2015), who considered significance tests in quantile regression and developed a test statistic based on marked empirical processes.

In this paper we will discuss how results from mean regression carry over to our case. Whereas elsewhere a first attempt could be based on the application of a Bahadur expansion, we will see that in our setting the accuracy of a direct application of Bahadur expansions is too poor. We will shortly explain this here for the testing problem where contains only one value .

Suppose for simplicity at this stage that the parametric model contains only one value and that

. The Bahadur expansion of is given by

(5)

where is the conditional density of given .

This gives the following approximation for :

One can show that up to a logarithmic factor and are of order and , respectively. This implies that up to a logarithmic factor, the difference is of order . On the other hand as it is also the case in mean regression is equal to the sum of a deterministic term and a random term of order . Thus the above approximation only helps if or equivalently if for sample size going to . E.g. if one applies a bandwidth that leads to rate optimal estimation of twice differentiable functions this assumption would allow only a one-dimensional setting . Also in the case of minimax optimal testing with twice differentiable functions under the alternative (see Ingster (1993) and Guerre and Lavergne (2002)), the optimal bandwidth is only allowed for dimension . In this paper we develop an asymptotic theory for -type quantile tests that works under the assumption that . In the above examples this allows dimensions and . Furthermore, for our asymptotic discussion of the distribution of the test statistic on the hypothesis we only need the assumption that . Thus on the hypothesis, our basic assumptions coincide with conditions needed for the asymptotics of mean regression. We conjecture that also for the alternative the assumption could be weakened but that then the asymptotic mean of the test statistic changes. We will comment on this after the statement of Theorem 2.

In our approach we will make use of the fact that Bahadur expansions of kernel quantile estimators calculated at two different points are asymptotically independent if they are calculated at points that are such that the supports of the kernels do not overlap. Thus the variance of an integral over a Bahadur expansion should be of smaller order than the variance of the Bahadur expansion at a fixed point. The main technical difficulty that will come up when applying this idea is the need to calculate moments of the kernel regression quantiles. We will introduce a method for the expansion of such moments that is based on Edgeworth expansions in a related problem. Our main result gives a bound between the moments of kernel regression quantiles and the moments of its Bahadur approximation.

The paper is organized as follows. In the next section we will state our result on moments of kernel regression quantiles. Our main result on the asymptotics of -type quantile tests is given in Section 3. We will also introduce some kind of wild bootstrap procedure adapted to quantile regression and give a theoretical result on its consistency. In Section 4 we present the results of a simulation study, and we analyze data on Engel curves. The proofs are postponed to the last three sections.

2 Asymptotic moments

In this section we will present an asymptotic result on higher order moments of kernel regression quantiles. This result will be our most important ingredient for getting our result on the asymptotic distribution of our test statistic. In our result the moments of kernel regression quantiles are compared with the moments of their Bahadur approximations. Recall that we are interested in the null hypothesis defined in (2). We suppose that for all ,

(6)

For the case the function lies on the hypothesis. In order to develop our asymptotic theory, we need to work under the following assumptions. In the formulation of the assumptions and in the proofs we use the convention that are generic strictly positive constants that are chosen large enough, that are generic strictly positive constants that are chosen small enough, and that are generic strictly positive constants that are arbitrarily chosen. Using this convention we write for a sequence with large enough and for a sequence with an arbitrarily chosen constant . All these variable names are used for different constants and sequences, even in the same equation.

We will make use of the following assumptions.

(B1)

The support of is a compact convex subset of . The density of is bounded and bounded away from zero on . The function is uniformly absolutely bounded for .

(B2)

The conditional distribution of given allows a density that is twice differentiable with respect to . For this derivative it holds that for , , and . The density also satisfies and

for and , where is the Euclidean norm. Moreover, the functions , and are continuously differentiable with respect to .

(B3)

The bandwidth satisfies and . The kernel is a symmetric, continuously differentiable probability density function with compact support, , say. It fulfills a Lipschitz condition and it is monotone strictly increasing on . It holds that for some where denotes the inverse of .

In our asymptotics, the density and the functions are fixed and do not depend on . The cumulative distribution function of given may depend on . We do not indicate this in our notation.

Assumptions (B1)–(B3) are standard assumptions for the study of smoothing estimators, with the exception of the last assumption in (B3). We now shortly explain why this assumption is needed here. For fixed and , define the random vector with , and where is defined in (12) below. In the proof of the following Theorem 1

we will develop Edgeworth expansions for the distribution of . Typically, the summands of do not fullfil non-lattice type assumptions that are needed for the verification of Edgeworth expansions. But under (B3) a non-lattice assumption can be verified for the conditional distribution of a finite sum of summands of .

For more details we refer to the proof of Theorem 1. The last assumption in (B3) can be easily verified. It just puts a simple bound on the derivative of . E.g., it can be easily checked for the triangle kernel and for all kernels of the form with . In case that is bounded away from zero on bounded intervals of the assumption follows if for some , it holds that for and small enough and that for in a neighborhood of .

We put

(7)

(10)

In the main result of this section we will consider conditional moments of the truncated kernel smoothing quantiles , conditioned on the number of covariables falling into local neighborhoods. Note that, with positive probability, kernel smoothing quantiles are not defined because there is no covariable in the support of the kernel, with positive probability. Thus unconditional moments are not defined. In the following theorem we will condition on local neighborhoods that are designed such that the result can be easily used for the asymptotic analysis of our test statistic in the next section. Note that is the support of the kernel . The theorem could also easily be stated with other local neighborhoods. The conditional moments of the truncated kernel smoothing quantiles will be compared with the conditional moments of the following modified Bahadur expansion, denoted by :

(11)

where is defined such that

(12)

Here denotes the conditional expectation, given that . Furthermore is defined as

where

We have the following asymptotic result for the moments of kernel quantile estimators and their Bahadur approximations.

Theorem 1.

Assume (B1)–(B3). Then, for natural numbers ,

(13)

(14)

uniformly in , and where is the random number of ’s that lie in , and where

. For the second moments of the uncentered estimators and we have that

(15)

Under the additional assumption that we get that

(16)

We can apply the theorem when , in which case and and . Hence, (13) and (14) hold with and replaced by and . In particular, for (16) follows directly from (13).

3 Asymptotic theory

We suppose that there exists an estimator that converges to . Hence, on the hypothesis the true value of is equal to . On the alternative, may depend on the chosen estimator .

In order to develop the asymptotic distribution of and , we need the following additional assumptions.

(B4)

We assume that

for some function . The function is continuous, and the functions , and are continuous with respect to . For and it holds that , and for some and for all and all .

(B5)

For some it holds that

The first assumption in (B4) can be shown under smoothness conditions on the relation . For the case that contains only one single element, this assumption in (B4) would directly follow from (B5) and the assumption that has a derivative that is continuous in . Assumption (B5) states that achieves at least a nearly parametric rate. In the case of linear quantile regression (i.e. ), such an assumption has been shown in Angrist et al (2006). Note that

implies (B5) if is chosen such that . Note that because of

.

We now state our main result on the asymptotic distribution of our test statistics.

Theorem 2.

Assume (B1)-(B5). For the case that make the additional assumption that . Then,

where

and where for any , denotes the -times convolution product of at .

In our theorem for the alternative we make the additional assumption that converges to . This assumption is used in the proof for the treatment of the deterministic term , see Lemma 5. The assumption can be weakened but with another limit for . This would result in a limit theorem for the test statistic with a mean that differs from . We have added a short discussion of this point after the statement of Lemma 5.

We expect that Theorem 2 cannot be used for an accurate calculation of critical values. The asymptotic normality result of

Theorem 2 is based on the fact that kernel smoothers are asymptotically independent if they are calculated at points that differ more than . Thus the convergence is comparable to the convergence of the sum of independent summands. This would motivate a rate of convergence of order . As has been suggested for other goodness-of-fit tests in the literature, also here a way out is to use a bootstrap procedure. We will introduce some kind of wild bootstrap for quantiles in which the Bahadur expansion of is resampled. For the definition of see (5) in Section 2. For the bootstrap, we define

where is an estimator of and are independent random variables with uniform distribution on that are independent of the sample. The bootstrap test statistics are defined as:

and

For proving the consistency of this bootstrap procedure, we do not specify the choice of the estimator that is used in the construction of the bootstrap procedure. We only assume that the estimator is consistent:

(B6)

It holds that

in probability.

The next theorem shows the consistency of the above bootstrap approach.

Theorem 3.

Assume (B1)-(B6). Then,

where denotes the conditional distribution, given the sample. Furthermore, is the Kolmogorov distance, i.e. the sup norm of the difference between the corresponding distribution functions.

Theorem 3 remains to hold if we replace (B1)–(B5) by weaker conditions. We do not pursuit this because we need for consistency of bootstrap that both, Theorem 2 and Theorem 3, hold.

4 Numerical study

In this section, we present the results of our numerical studies. In our first simulation we show that a direct application of the Bahadur representation is not accurate enough for studying the approximation of the distribution of our test statistics and . For this purpose, we compare the differences and . Here is the integrated difference between the quantile regression and its Bahadur representation and is the difference between the test statistic and its approximation based on Bahadur representation. It is clear that . Our point is not that is smaller than but that the ratio is large and that it is decreasing for an increasing bandwidth. This result supports our theory that a direct use of Bahadur expansions only works under very restrictive assumptions on the bandwidth. Table 1 shows the results of and for the one dimensional case. We also simulated a two dimensional model, whose results are shown in Table 2. In the one dimensional model, we set , where has a standard normal distribution. This results in the quantile function , where stands for the quantile of the standard normal distribution. For the two dimensional model, we set , where has a standard normal distribution and we get the quantile function . For the one dimensional model, we generated from the uniform distribution supported on the unit interval . For the two dimensional model we generated from a distribution on the unit square which has uniform marginals but where the joint distribution differs from a uniform distribution. This is done to allow for a dependence between the two regressors. We generated random vectors from a bivariate normal distribution with correlations and 0.8 and then transformed them with their marginal distribution functions. We generated 400 data sets of size 200 and 400 for each model. For the one dimensional model, we used the bandwidths and we used the bandwidths for the two dimensional model. We used the R package quantreg for fitting quantile functions. From Table 1 and Table 2, one can see that the ratio of over is large for small bandwidths and decreases as the bandwidth grows. This observation supports our approach for the asymptotic theory. This implies that when we approximate the test statistic it requires less strict assumptions on the bandwidth if we approximate the integrated function rather than when we approximate the quantile function itself.

Bandwidth

0.05

0.08

0.1

0.12

0.15

0.195

0.116

0.091

0.077

0.059

0.067

0.044

0.037

0.034

0.028

Ratio

2.922

2.653

2.473

2.284

2.073

0.231

0.139

0.110

0.091

0.071

0.124

0.078

0.065

0.056

0.046

Ratio

1.865

1.779

1.687

1.635

1.547

0.196

0.117

0.092

0.077

0.059

0.065

0.044

0.037

0.033

0.029

Ratio

3.028

2.696

2.481

2.305

2.070

0.094

0.057

0.045

0.037

0.029

0.033

0.022

0.019

0.017

0.014

Ratio

2.899

2.536

2.338

2.170

2.027

0.109

0.068

0.054

0.045

0.036

0.058

0.039

0.032

0.028

0.023

Ratio

1.867

1.755

1.684

1.614

1.552

0.094

0.056

0.045

0.037

0.029

0.032

0.022

0.019

0.017

0.015

Ratio

2.959

2.604

2.378

2.192

1.982

Table 1: Difference between two approximations: is the integrated squared approximation error of a quantile estimator by its Bahadur representation and is the approximation error of the test statistic by .

Weak dependence

Strong dependence

Bandwidths

0.125

0.150

0.175

0.200

0.125

0.150

0.175

0.200

0.249

0.139

0.086

0.058

0.153

0.105

0.077

0.059

0.081

0.051

0.036

0.029

0.044

0.037

0.033

0.029

Ratio

3.065

2.716

2.369

1.983

3.445

2.828

2.371

2.024

0.296

0.164

0.102

0.072

0.180

0.126

0.094

0.072

0.142

0.087

0.061

0.048

0.089

0.069

0.056

0.048

Ratio

2.093

1.884

1.667

1.500

2.021

1.832

1.659

1.504

0.247

0.138

0.085

0.058

0.153

0.106

0.077

0.059

0.077

0.047

0.035

0.029

0.045

0.037

0.032

0.029

Ratio

3.221

2.929

2.446

1.990

3.355

2.831

2.378

2.022

0.249

0.139

0.086

0.058

0.074

0.051

0.038

0.029

0.081

0.051

0.036

0.029

0.023

0.019

0.017

0.015

Ratio

3.066

2.716

2.369

1.983

3.273

2.716

2.278

1.958

0.296

0.166

0.102

0.072

0.087

0.061

0.046

0.035

0.142

0.087

0.061

0.048

0.044

0.034

0.028

0.024

Ratio

2.093

1.884

1.667

1.500

1.991

1.785

1.610

1.467

0.247

0.138

0.085

0.058

0.073

0.051

0.037

0.028

0.077

0.047

0.035

0.029

0.022

0.019

0.017

0.015

Ratio

3.221

2.929

2.446

1.990

3.274

2.666

2.230

1.899

Table 2: Difference between two approximations under a two dimensional model: is the integrated squared approximation error of a quantile estimator by its Bahadur representation and is the approximation error of the test statistic by . The left panel in the table is the result for and the right panel shows the result for .

The second simulation study is conducted to show the validity of our bootstrap procedure. We considered four scenarios:

I.

All quantiles are linear:

II.

The median is linear and other quantiles are not linear:

III.

All quantiles are non-linear:

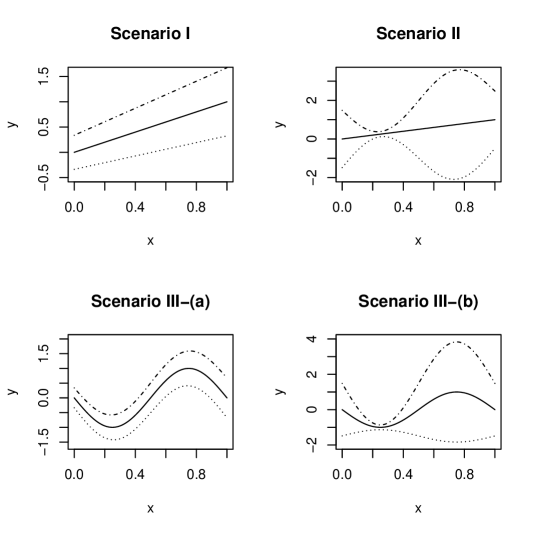

Here , , , and . The covariates are generated from a uniform distribution on the unit interval . We generated 200 samples of size 400. We generated 201 bootstrap samples for each data set. The three scenarios are shown in Figure 1. In the bootstrap procedure, we used a kernel density estimator for estimating the conditional density .

We tried three bandwidths 0.075, 0.100, and 0.125 for the test statistic, and fifteen choices of bandwidths for estimating the conditional density of the error used in the bootstrap procedure. We applied the proposed bootstrap test for testing the linearity of the lower quartile, the median, and the upper quartile functions. We also tested the linearity hypothesis over these three different quantile levels. In our scenarios there are four models under the null hypothesis: all three quantiles in scenario I and the median in scenario II. In Table 3, we report the summary statistics of rejection ratios of 45 different choices of bandwidths. Among 45 different choices of bandwidths, there was no case where the bootstrap test did not keep the significance level of 5% under scenario I. In slightly more than half of the cases the bootstrap test did not keep the significance level in testing the linearity of the median under scenario II. These cases appeared when we used large bandwidths. Concerning the power of the bootstrap test, we observed that almost all choices of the bandwidth showed a power near one under scenario III-(a). One exception is the case with the smallest bandwidths where we observe an empirical power around 0.8. One interesting observation is that the bootstrap test shows a poor power for the lower quartile in scenario III-(b) where the empirical power ranges from 0.045 to 0.27. This is however natural since the function is not so far from a linear function as one can see in Figure 1. We also observed that the median and the upper quartile in scenario III-(b) showed much stronger power. The result of the test based on the test statistic integrated over levels shows a similar result. In this case, only scenario I is in the null hypothesis and there was no case where the empirical size of the bootstrap test is bigger than 5%. The power behavior is also similar. The test showed the strongest power with the bigger bandwidths.

Figure 1: Shape of quantile curves in each scenario. The three curves in each panel represent the , , and quantile curves in each scenario.

Quartile functions

1st Quartile

Median

3rd Quartile

Sum quartiles

Scenario I

Q1

0.005

0.000

0.005

0.000

Med

0.010

0.005

0.010

0.005

Q3

0.010

0.010

0.015

0.010

Scenario II

Q1

0.470

0.030

0.450

0.380

Med

0.575

0.055

0.545

0.550

Q3

0.630

0.105

0.610

0.695

Scenario III (a)

Q1

0.985

1.000

0.995

1.000

Med

1.000

1.000

1.000

1.000

Q3

1.000

1.000

1.000

1.000

Scenario III (b)

Q1

0.065

0.300

0.735

0.545

Med

0.135

0.385

0.865

0.770

Q3

0.155

0.440

0.935

0.895

Table 3: First quartile, median and third quartile (obtained from 45 choices of the bandwidth) of the rejection proportions based on 200 generated samples.

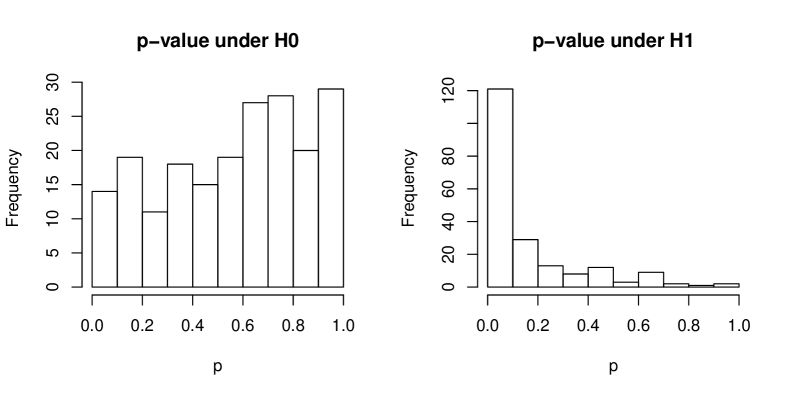

Figure 2 shows the distributions of estimated p-values by using the proposed bootstrap. The plots are based on 200 simulated data sets for scenario II. The left panel shows the distribution of estimated p-values for testing the linearity of the median, which lies in the null and the right panel shows the distribution of estimated p-values for testing the linearity of the upper quartile, which lies in the alternative. The distribution in the left panel is close to the uniform distribution which we expect for the null hypothesis and the right panel shows that the bootstrap p-values are close to zero, which we also expect.

To summarize our observations from this simulation study, in our setting the bootstrap test keeps the level well except for cases where we use too large bandwidths. On the other hand, too small bandwidths lead to relatively poor power. Interesting cases are scenario II and scenario III-(b). Under scenario II, the median is linear but both quartiles are not. The simulation result shows that the bootstrap test keeps the level for the median and has some power for the other quantiles. Under scenario III-(b), the lower quartile is non-linear but close to the null. We observe that here the bootstrap test has stronger power for the median and the upper quartile than for the lower quartile.

Figure 2: The left panel shows the distribution of estimated p-values under the null and the right panel shows the distribution of estimated p-values under the alternative.

In the last simulation study, we compared our test with the test proposed by Zheng (1998). We considered the same four scenarios as in the previous simulation study. In this simulation, we generated 500 data sets of 400 observations. For the bootstrap we generated 501 bootstrap samples. The other simulation settings are the same as in the previous simulation study. To choose the bandwidth for Zheng’s test, we applied the function npregbw in the R-package np, which is based on cross-validation with AIC. For the nonparametric quantile estimator in our procedure, we used the bandwidth proposed in Yu and Jones (1998). The bandwidths for the kernel estimator for the conditional density in the bootstrap procedure were chosen by a rule of thumb using the function bw.nrd in R. The level of the tests was set to . We observe in Table 4 that the level of our test is close to the nominal level. None of the two tests is always more powerful than the other. In the null model both tests keep the level well. In Scenario II, Zheng’s test shows stronger power than the proposed test, whereas in Scenario III(b), the proposed test has higher power.

Quartile functions

1st Quartile

Median

3rd Quartile

Sum quartiles

Scenario I

Zheng

0.006

0.000

0.000

MVY

0.024

0.052

0.048

0.028

Scenario II

Zheng

0.954

0.008

0.950

MVY

0.696

0.002

0.650

0.884

Scenario III (a)

Zheng

0.974

0.994

0.984

MVY

0.994

0.992

0.990

1.000

Scenario III (b)

Zheng

0.034

0.334

0.460

MVY

0.048

0.404

0.992

0.954

Table 4: Rejection proportions based on 500 generated samples.

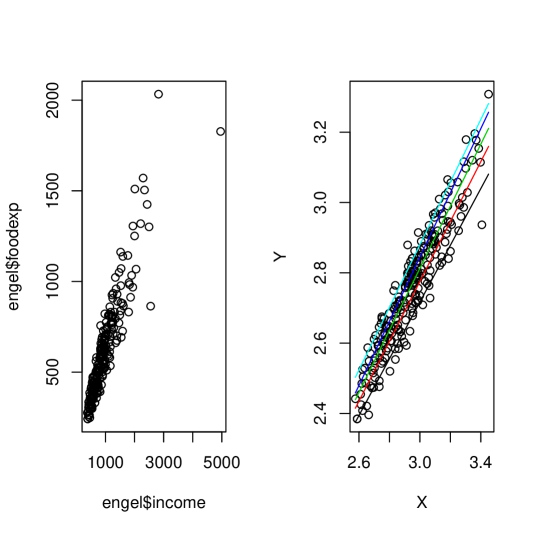

Finally, as an illustrating example, we applied the proposed test to a historic data set of Ernst Engel. The data set was used in Koenker (2005), among many other publications. The data set was first presented by Engel (1857) to support his famous Engel’s law. The data set has two variables, household income and food expenditure and it contains 235 observations. Figure 3 shows the scatter plot of this dataset and the scatter plot of the data after a log transform with base 10. As one can see in Figure 3, there is one outlier. We removed this point from the data. Hence the analysis below is based on 234 observations. We first analyzed the log transformed income versus the log transformed food expenditure. We used five different bandwidths for calculating the test statistic. The bandwidth for the conditional density estimator used in the bootstrap resampling was chosen by a rule of thumb. To obtain the bootstrap distribution, we resampled the data set 1,001 times. We test the linearity of quantiles for 0.1, 0.2, 0.3, 0.4, 0.5, 0.6, 0.7, 0.8, and 0.9. As can be seen from Table 5, the test did not reject linearity of quantiles for any of these values at the significance level 5%. This was the case for all five bandwidth choices.

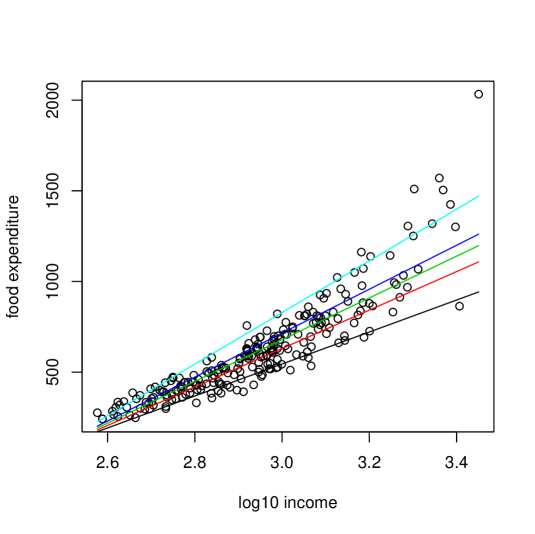

We also used the log transformed income with the original untransformed food expenditure as a further example. Figure 4 shows the scatter plot of this dataset together with 0.1, 0.3, 0.5, 0.7, 0.9 linear quantile fits. The figure shows that high level quantiles deviate from their linear fits. This is also seen by our test, since it rejects the linearity for high level quantiles. The estimated p-values for the conditional quantiles of level or higher are smaller than for every bandwidth we used.

Quantile level

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

Bandwidth

0.050

0.289

0.246

0.629

0.999

0.996

1.000

0.999

1.000

1.000

0.075

0.152

0.383

0.997

0.992

0.993

0.979

1.000

1.000

1.000

0.100

0.105

0.745

0.997

0.964

0.971

0.970

0.999

1.000

0.993

0.125

0.100

0.986

0.988

0.908

0.895

0.992

1.000

1.000

0.963

0.150

0.149

0.996

0.976

0.894

0.843

0.997

0.999

1.000

0.935

Quantile level

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

Bandwidth

0.050

0.305

0.675

0.413

0.135

0.031

0.008

0.012

0.004

0.000

0.075

0.569

0.498

0.268

0.140

0.046

0.027

0.003

0.002

0.000

0.100

0.640

0.324

0.181

0.047

0.015

0.004

0.003

0.001

0.000

0.125

0.531

0.235

0.150

0.034

0.009

0.001

0.002

0.001

0.000

0.150

0.664

0.197

0.088

0.012

0.003

0.002

0.002

0.003

0.000

Table 5: Estimated p-values for testing the linearity of conditional quantiles of Engel’s data. The upper table shows the estimated p-values for testing the linearity of conditional quantiles of as a function of and the lower table shows the estimated p-values for testing the linearity of conditional quantiles of food expenditure as a function of .

Figure 3: The left panel shows the scatter plot of the original Engel data. The right panel shows the scatter plot of log transformed data after removing one influential point. The lines in the right panel represent linear quantile fits of levels 0.1, 0.3, 0.5, 0.7, and 0.9.

Figure 4: The figure shows the scatter plot of log transformed income versus food expenditure after removing one influential point. The lines represent linear quantile fits of level 0.1, 0.3, 0.5, 0.7, and 0.9.

We need to show equations (13)–(15). Claim (15) follows from

(13)–(14) because of . Furthermore, (16) is a direct consequence of (13), see the remark after the statement of the theorem. It remains to show (13)–(14).

It holds that , where we use the shorthand notation . At this point and in the following proofs we will make use of our convention of using the symbols, .

First note that

(17)

Let

uniformly in , because of Assumption (B2). Then, with

we have that

We now argue that an Edgeworth expansion holds for the conditional density of , given , that is of the form

(18)

where, the error term holds uniformly in , and for and constants . Here, we use standard notation used e.g. in Bhattacharya and Rao (1976), p. 53. In particular, denotes the conditional variance of , given that , and

denotes a product of a standard normal density with a polynomial that has coefficients

depending only on the conditional cumulants of of order , given that . Note that and

depend on , , and and that we do not indicate this in our notation. Furthermore, the cumulants and the variance converge to constants depending on , uniformly in and . Note that for the conditional distribution of , given that , converges to the distribution of where and are independent random variables, has a uniform distribution on and is -valued with . This helps to understand that limit theorems hold uniformly. The function is defined as

see Section 7 in in Bhattacharya

and Rao (1976).

In our case expansion (18) follows from Theorem 19.3 in Bhattacharya

and Rao (1976). For this claim we have to verify that their conditions (19.27), (19.29) and (19.30) hold. Our setting is slightly different from theirs, since we consider triangular arrays of independent identically distributed random variables instead of a sequence of independent random variables as is the case in Theorem 19.3 in Bhattacharya and

Rao (1976). But the same proof applies because

in our setting we can verify the following uniform versions of (19.27), (19.29) and (19.30):

(19)

(20)

(21)

with for some . Note that , and depend on .

Claim (19) follows by a direct argument using brute force bounds.

For the proof of (20), we consider the conditional density of given the value of and given that for . For this density evaluated at can be bounded by a constant times by Assumptions (B1) and (B3). This bound holds uniformly over , , and the value of .

We now show that for every , there exists such that the density of can be bounded by a constant times . For simplification of notation we assume for the proof that .

For the proof of the claim, we show first that for we get that the conditional density of is uniformly bounded. This follows by an evaluation of convolution integrals where one uses that . Applied to this gives that the density of is bounded by . Note that the density of is bounded by . For the density of we get the bound . Finally, for it holds that and we have that for , the density of is uniformly bounded. We now use that the -fold convolution of a bounded density with bounded support for some is bounded by . This gives that the density of can be bounded by a constant times if with , . This result can be easily extended to .

From this result now we want to conclude that the conditional density of is uniformly bounded, given the value of and given that for . This follows immediately from the following result. Suppose that has support and a density that is bounded by

then has a density that is bounded by .

For a proof of this result, note that

We now apply the result that for chosen large enough, the conditional density of is bounded, given that for , uniformly over , and . This implies that the square of this conditional density is integrable and by the Fourier Inversion Theorem (see Theorem 4.1 (vi) in Bhattacharya and

Rao (1976)) the same holds for the squared modulus of its Fourier transform. Thus the modulus of the Fourier transform of the conditional density of , given that for , is integrable. This shows (20) for .

For the proof of (21) one applies the Riemann-Lebesgue Lemma (see Theorem 4.1 in Bhattacharya and

Rao (1976)). Consider for simplicity the case where . For one gets that

The right hand side of this equation converges to

This convergence holds uniformly in , , and .

By using these facts we get (21)

from the Riemann-Lebesgue Lemma.

By applying Theorem 19.3 in Bhattacharya and

Rao (1976) with we get that

(22)

uniformly in , and for and constants . Here we have used the fact that terms for in the expansion (18) can be bounded by . We used the following notation

with . It is easy to show that, uniformly in ,

and that

with

Note that . Thus we get that uniformly in ,

(23)

(24)

Note also that with , uniformly in ,

Hence, uniformly in ,

(25)

From (23), (25) and the above calculations it now follows for that with and

uniformly in with constants .

If is chosen with large enough we get that the right hand side of the last equation is equal to . This follows since it can be easily shown that

For the proof of (13) and (14) it remains to show that uniformly in , with constants , and

for

(28)

(29)

It remains to show (28) – (29). For the proof of (28) note that for independent random variables with mean zero, variance 1 and bounded -th absolute moment it holds that

because for one has

where the sum runs over all indices that are such that each value of an index appears exactly two times.

For the proof of (29) one applies that for independent random variables with mean zero, variance 1 and bounded -th absolute moment it holds that

where the sum runs over all indices that are such that one value of an index appears three times and for all other indices each value appears exactly two times.

This concludes the proof of the theorem.

For the proof of Theorem 2 we will use the following corollary of Theorem 1.

For the statement of the corollary we have to define another construction of local neighborhoods. For their definition suppose first that is one-dimensional. Then the support is a compact interval. For arbitrary and for , we can then define

The set of indices of the () that fall inside the interval is denoted by . We write for the number of elements of . An arbitrary belongs to a unique and we define and . Thus is an interval of length , such that lies in the middle subinterval of of length . If the dimension of is larger than one, this partition of the support into small intervals can be generalized in an obvious way.

Corollary 1.

Assume (B1)–(B3). Then, for natural numbers ,

uniformly in , and , where is the random number of ’s that lie in , and where

. For the second moments of the uncentered estimators and we have that

Under the additional assumption that we get that

Proof of Corollary 1. For we have by a simple argument with or that . Note that because of .

Using (13) and

We only prove the statement for . The asymptotic result for follows similarly. We need to introduce a few more notations. With and

we define as in (11) and we put

Note that , and that by Assumption (B4). We also define as in (10).

Let also

with .

The proof of Theorem 2 will make use of the following lemmas.

Lemma 1.

Suppose that the assumptions of Theorem 2 are satisfied. Then,

(30)

(31)

Proof of Lemma 1. As is known for the case where there is no parametric part and where , one has that

with defined as in (5).

For a proof see Theorem 2 in Guerre and Sabbah (2012). By standard smoothing theory we have that (still when )

(32)

This shows (31) when .

We can move from this case to by adding to the observations terms of order . This changes the local quantiles by at most this amount, and hence (31) still holds when .

In the case of we have to add to the observations terms of the order . This shows the first statement of the lemma. ∎

Lemma 2.

Suppose that the assumptions of Theorem 2 are satisfied. Then,

Proof of Lemma 2.

First note that is equal to the quantile estimator we would obtain when we shift all observations in the window around by the amount , and hence we need to show that the distance between this latter estimator (say ) and is uniformly in and .

Next, note that if now in addition we perturb all observations in the window around by adding , the quantile estimator will get perturbed by at most the maximal perturbation of the observations, which is of the order by Assumption (B4).

After these two perturbations, the quantile estimator is now based on instead of . Finally note that if we apply one more perturbation by subtracting for all in the window around , the estimator changes by at most by Assumption (B5). The so-obtained estimator equals , which shows the statement of the lemma.

∎

Lemma 3.

Suppose that the assumptions of Theorem 2 are satisfied. Then,

Suppose that the assumptions of Theorem 2 are satisfied. Then,

and hence,

At this point we needed the additional assumption for the case that . We now shortly outline what happens if we are on the alternative and if this assumption does not hold. Note that for

For the first term on the right hand side we get from Corollary 1 that it is of order . For one can show that it is equal to . For the term one can show that it is equal to for some function that does not depend on the function . This can be done by using the arguments based on Edgeworth expansions that were central in the proof of Theorem 1. This gives that

Suppose now that . Then it holds that and

using Lemma 10 we get that

This implies that the test rejects for large values of . Thus, in this high-dimensional setting the test behaves like a linear test and not like an omnibus test.

Lemma 6.

Suppose the assumptions of Theorem 2 are satisfied. Then,

Proof of Lemma 6. For simplicity of exposition of the argument, let us assume that is one-dimensional. For arbitrary and for , define

Then we can write with (). The terms , and are sums of conditionally independent summands. The summands are uniformly bounded by a term of order . This follows from Lemma 5, from the fact that , see also (32), and from the Bahadur representation for , given in Lemma 3. It now follows that , which implies the statement of the lemma for . For one can use the same approach. ∎

Lemma 7.

Suppose the assumptions of Theorem 2 are satisfied. Then,

Proof of Lemma 7. This is obvious, since , thanks to Assumption (B5) and Lemma 3.

∎

Lemma 8.

Suppose the assumptions of Theorem 2 are satisfied. Then,

uniformly in , and hence the statement of the lemma holds because of (34) and (B5).

∎

Lemma 9.

Suppose the assumptions of Theorem 2 are satisfied. Then,

Proof of Lemma 9.

The statement of the lemma follows from (B5).

∎

Lemma 10.

Suppose the assumptions of Theorem 2 are satisfied. Then,

Proof of Lemma 10. The proof is very similar to the proof of e.g. Proposition 1 in

Härdle and Mammen (1993). Write

where . By writing , we can decompose into . As in Härdle and Mammen (1993), is negligible. Straightforward calculations show that . Indeed,

Next, write with

where

By calculating its mean and variance it can be checked that . Thus for the lemma it remains to check that . For the proof of this claim one can proceed as in Härdle and Mammen (1993) and apply the central limit theorem for U-statistics of de Jong (1987).

For this purpose one has to verify that

, and

. This can be done by straightforward but tedious calculations.

∎

Proof of Theorem 2. The theorem follows immediately from Lemmas 4–10. Lemmas 4–9 imply the negligibility of the terms , .., . Lemma 10 shows the asymptotic normality of .

∎

The theorem can be shown by verification of the conditions of the central limit theorem for U-statistics of de Jong (1987), in the same way as was done in the proof of Lemma 10. The crucial point in the proof is to note that has the same distribution as , and hence the calculations in the proof of Lemma 10 go through in this proof.

Acknowledgments

Research of the first author was prepared within the framework of a subsidy granted to the HSE by the Government of the Russian Federation for the implementation of the Global Competitiveness Program and it was supported by Deutsche Forschungsgemeinschaft

through the Research Training Group RTG 1953. The research of the second author was supported by the European Research Council (2016-2021, Horizon 2020 / ERC grant agreement No. 694409), and by IAP research network

grant nr. P7/06 of the Belgian government (Belgian Science Policy).

References

Ait-Sahalia, Y., Fan, J. and Peng, H. (2009).

Nonparametric transition-based tests for diffusions.

Journal of the American Statistical Association104 1102-1116.

Angrist, J., Chernozhukov, V. and Fernández-Val, I. (2006).

Quantile regression under misspecification, with an application to the U.S. wage structure.

Econometrica74 539-563.

Bhattacharya, R. and Rao, R. (1976). Normal Approximations and Asymptotic Expansions.

John Wiley & Sons, New York.

Bierens, H.J. and Ginther, D. (2001). Integrated conditional moment testing of quantile regression models. Empirical Economics26 307-324.

Chaudhuri, P. (1991). Nonparametric estimates of regression quantiles and their local Bahadur representation. Annals of Statistics19 760-777.

Conde-Amboage, M., Sánchez-Sellero, C. and González-Manteiga, W. (2015). A lack-of-fit test for quantile regression models with high-dimensional covariates. Computational Statistics and Data Analysis88 128-138.

De Backer, M., El Ghouch, A. and Van Keilegom, I. (2017). Semiparametric copula quantile regression for complete or censored data. Electronic Journal of Statistics11 1660-1698.

de Jong, P. (1987). A central limit theorem for generalized quadratic forms. Probability Theory and Related Fields75 261-277.

Dette, H. and Sprekelsen, I. (2004). Some comments on specification tests in nonparametric absolutely regular processes. Journal of Time Series Analysis25 159-172.

El Ghouch, A. and Van Keilegom, I. (2009). Local linear quantile regression with dependent censored data. Statistica Sinica19 1621-1640.

Fan, J., Zhang, C. and Zhang, J. (2001).

Generalized likelihood ratio statistics and Wilks phenomenon.

Annals of Statistics29 153-193.

Gao, J. and Hong, Y. (2008). Central limit theorems for generalized U-statistics with applications in nonparametric specification. Journal of Nonparametric Statistics20 61-76.

González-Manteiga, W. and Cao-Abad, R. (1993).

Testing the hypothesis of a general linear model

using nonparametric regression estimation. Test2 161-188.

Guerre, E. and Lavergne, P. (2002). Optimal minimax rates for nonparametric specification testing in regression models. Econometric Theory18 1139-1171.

Guerre, E. and Sabbah, C. (2012). Uniform bias study and Bahadur representation for local polynomial estimators of the conditional quantile function. Econometric Theory28 87-129.

Haag, B. (2008).

Non-parametric regression tests using dimension reduction techniques. Scandinavian Journal of Statistics35 719-738.

Härdle, W. and Mammen, E. (1993). Testing parametric

versus nonparametric regression. Annals of Statistics21 1926-1947.

He, X. and Ng, P. (1999). Quantile splines with several covariates. Journal of Statistical

Planning and Inference75 343-352.

He, X., Ng, P. and Portnoy, S. (1998). Bivariate quantile smoothing splines. Journal

of the Royal Statistical Society - Series B60 537-550.

He, X. and Zhu, L.-X. (2003).

A lack of fit test for quantile regression.

Journal of the American Statistical Association98 1013-1022.

Hjellvik, V., Yao, Q. and Tjøstheim, D. (1998). Linearity testing using local polynomial

approximation. Journal of Statistical Planning and Inference68 295-321.

Hoderlein, S. and Mammen, E. (2009). Identification and estimation of local average derivatives in non-separable models without monotonicity. Econometrics Journal12 1-25.

Hong, S.Y. (2003). Bahadur representation and its applications for local polynomial estimates in non-parametric M-regression. Journal of Nonparametric Statistics15 237-251.

Horowitz, J.L. and Spokoiny, V.G. (2002).

An adaptive, rate-optimal test of linearity for median regression models.

Journal of the American Statistical Association97 822-835.

Ingster, Y.I. (1993).

Asymptotically minimax hypothesis testing for nonparametric alternatives I, II, III.

Math. Methods of Statistics2 85-114, 171-189, 249-268.

Koenker, R. (2005).

Quantile Regression.

Cambridge University Press.

Koenker, R. and Machado, J.A.F. (1999).

Goodness of fit and related inference processes for quantile regression.

Journal of the American Statistical Association94 1296-1310.

Koenker, R. and Xiao, Z. J. (2002).

Inference on the quantile regression process.

Econometrica70 1583-1612.

Kong, E., Linton, O. and Xia, Y. (2010).

Uniform Bahadur representation for local polynomial estimates of M-regression and its application to the additive model.

Econometric Theory26 1529-1564.

Kreiss, J.P., Neumann, M.H. and Yao, Q. (2008).

Bootstrap tests for simple structures in nonparametric time series regression.

Statistics and its Interface1 367-380.

Lee, K.L. and Lee, E.R. (2008).

Kernel methods for estimating derivatives of conditional quantiles.

Journal of the Korean Statistical Society37 365-373.

Leucht, A. (2012).

Degenerate - and -statistics under weak dependence: Asymptotic theory and bootstrap consistency.

Bernoulli18 552-585.

Li, Q. and Racine, J.S. (2008).

Nonparametric estimation of conditional CDF and quantile functions with mixed categorical and continuous data.

Journal of Business & Economic Statistics26 423-434.

Rothe, C. and Wied, D. (2013).

Misspecification testing in a class of conditional distributional models.

Journal of the American Statistical Association108 314-324.

Su, L. and White, H.L. (2012).

Conditional independence specification testing for dependent processes with local polynomial quantile regression.

Advances in Econometrics29 355-434.

Truong, Y.K. (1989).

Asymptotic properties of kernel estimators based on local medians.

Annals of Statistics 17 606-617.

Volgushev, S., Birke, M., Dette, H. and Neumeyer, N. (2013).

Significance testing in quantile regression.

Electronic Journal of Statistics7 105-145.

Yu, K. and Jones, M. C. (1998).

Local Linear Quantile Regression.

Journal of the American Statistical Association93 228-237.

Zheng, J.X. (1996).

A consistent test of a functional form via nonparametric estimation techniques.

Journal of Econometrics75 263-289.

Zheng, J.X. (1998).

A consistent nonparametric test of parametric models under conditional quantile regressions.

Econometric Theory 14 223-238.