A Stochastic Feedback Model for Volatility

Abstract

Financial time series exhibit a number of interesting properties that are difficult to explain with simple models. These properties include fat-tails in the distribution of price fluctuations (or returns) that are slowly removed at longer timescales, strong autocorrelations in absolute returns but zero autocorrelation in returns themselves, and multifractal scaling. Although the underlying cause of these features is unknown, there is growing evidence they originate in the behavior of volatility, i.e., in the behavior of the magnitude of price fluctuations. In this paper, we posit a feedback mechanism for volatility that closely reproduces the non-trivial properties of empirical prices. The model is parsimonious, contains only two parameters that are easily estimated, fits empirical data better than standard models, and can be grounded in a straightforward framework where volatility fluctuations are driven by the estimation error of an exogenous Poisson rate.

pacs:

Financial time series exhibit a number of interesting regularities (or “stylized facts”, as economists call them) that are well-documented in the literatureMandelbrot (1963); Fama (1965); T. Bollerslev, R. F. Engle, and D. B. Nelson in: (1994); Guillaume et al. (1997); Cont (2001); Bouchaud and Potters (2003); Borland et al. (2005). They include fat tails in the distribution of price fluctuations (known as returns in finance) that are slowly removed at longer timescales, strong autocorrelations in absolute returns but zero autocorrelation in returns themselves, multifractal scaling, and a negative correlation between past returns and the future magnitude of returns (known as the leverage effect).

Although there is currently no consensus on the underlying cause of these properties, there is growing evidence they are all rooted in the behavior of volatility, i.e., in the behavior of the magnitude of returnsT. Bollerslev, R. F. Engle, and D. B. Nelson in: (1994). In addition, there is evidence that returns – like earthquakes, turbulent flow, and Barkhausen noise – are driven by strong endogenous, or internal, feedback effectsJ. P. Bouchaud in: (2011).

In this paper, we present a stochastic feedback model for volatility that generates many of the stylized facts of financial time series. The model is motivated by several recent studies that have found the variance of price fluctuations, i.e., the squared volatility, is slowly varying and inverse gamma distributedGerig et al. (2009); Fuentes et al. (2009); Ma and Serota so that returns are well-fit by a Student’s -distribution at short timescalesGerig et al. (2009); Fuentes et al. (2009); Ma and Serota ; Praetz (1972); Blattberg and Gonedes (1974); Peiró (1994); Tsallis et al. (2003); Platen and Rendek (2008); Gu et al. (2008); Gerig (2011). Here we extend these results by modelling the properties of returns over timescales longer than one day. We propose a simple mechanism that generates inverse gamma distributed variances and introduce a feedback parameter that allows the variance to change slowly over time as it does in real price series. As a result, returns are -distributed at daily intervals but slowly approach a Gaussian as timescales are increased to weekly, monthly, and yearly intervals.

Although the results of the model match empirical data very well, we make no strong claim that we have uncovered the mechanism driving real-world volatility fluctuations. Instead, we offer the proposed mechanism as a novel explanation for these fluctuations and leave any conclusions regarding the true mechanism for later analysis. Alternative models that also produce inverse gamma distributed variances (and therefore Student -distributed returns) include the well-known GARCH modelBollerslev (1986); Nelson (1990); T. Bollerslev, R. F. Engle, and D. B. Nelson in: (1994) which can be motivated by the position of stop-loss orders in marketsBorland and Bouchaud (2011) and the Minimal Market ModelE. Platen in: (2001); Platen and Heath (2006) which describes the dynamics of a growth optimal portfolio with deterministic drift.

To begin our analysis, we define the return as the difference in logarithmic price from time to time where is measured in days,

| (1) |

We model daily returns, , as a discrete time stochastic process with a fluctuating variance,

| (2) |

where is the daily average return, is an IID Gaussian random variable, and is the local variance of returns (the square of the daily volatility, ).

We assume that the daily variance of returns, , is determined by a stochastic feedback process so that,

| (3) |

where is the gamma distribution, .

Only two parameters are used in Eq. 3: is the equilibrium inverse variance of the return process and is a feedback parameter. Notice that when , the expected value of is . Deviations from this equilibrium value are removed over a length of time determined by . If is large, the variance requires many iterations to relax back towards , but for small , the relaxation is quick.

The model can be motivated by the following mechanism: suppose that market participants continually observe an exogenous Poisson process that influences how they trade (this process could describe, for example, the arrival of new orders to the market or the arrival of economic news). When they estimate a high rate for the process, they increase their activity in the market and raise market volatility. Likewise, when they estimate a low value for this rate, they decrease their activity and reduce market volatility.

Specifically, assume that detrended intraday returns are uncorrelated, are all of size , and occur at an average daily rate, , that changes from day to day. is influenced by market participants as follows: (1) they observe an exogenous Poisson process with rate parameter , (2) based on the estimated rate of this process, they act in the market such that, on average, price fluctuations occur per exogenous events. Denoting their estimate of the exogenous rate by ,

| (4) |

exogenous events will occur in an amount of time, , making the estimated rate inverse gamma distributed, . The local variance of daily returns is therefore,

| (5) |

Notice that this mechanism produces inverse gamma distributed variances, but these variances are not autocorrelated.

To introduce feedback effects we assume that varies through time so that the sensitivity of the market to exogenous events (measured by ) is high when the local variance is high and low when the local variance is low. The simplest form of this relationship (taking into account that ) is,

| (6) |

The final result is,

| (7) |

The equation can be simplified by introducing the equilibrium inverse variance , defined by the relation . Therefore, . Using this relation and the simplifying assumption that at equilibrium, , so that , we have,

| (8) |

Notice this equation is identical to Eq. 3 with the change of variable . According to the proposed mechanism, is the daily rate of the exogenous process. If is large, the exogenous process has a high daily rate and can be estimated without too much error by market participants. Volatility therefore does not change much day to day and is strongly autocorrelated. If is small, the exogenous process has a low rate and there are large errors in its estimation, which means volatility autocorrelations are less strong.

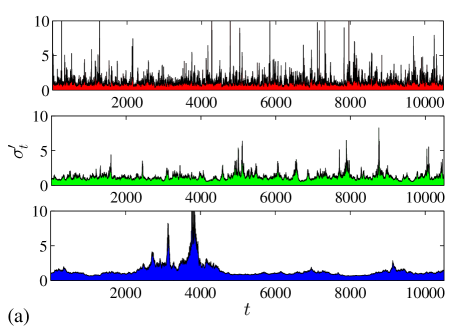

To determine how the parameters of the model affect returns, we simulate the model using different choices of and (each run includes 50 million time steps). only influences the scale of the process and leaves the statistical properties of returns unchanged (a result confirmed in our simulations), so we do not show the results of varying here.

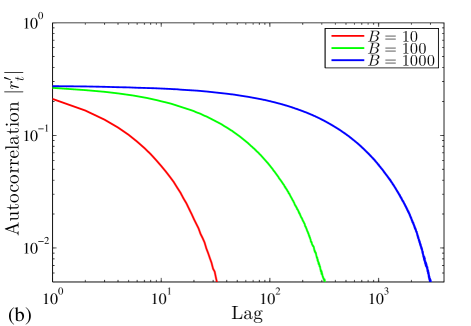

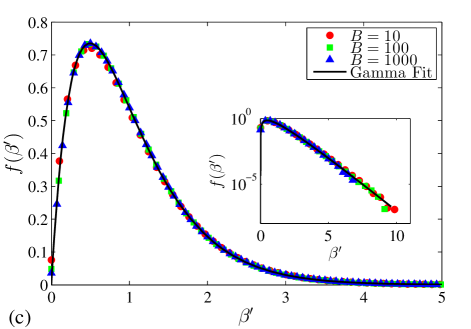

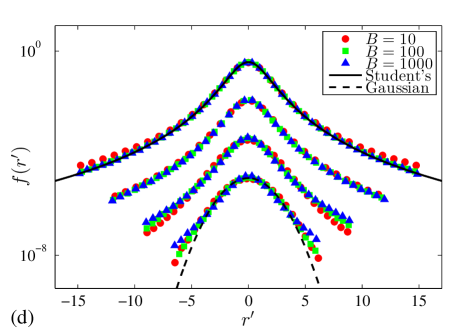

In Fig. 1, we show the properties of the model with different . We set and let respectively. To facilitate the presentation of results, we define the following normalized variables:

| (9) | |||||

| (10) | |||||

| (11) |

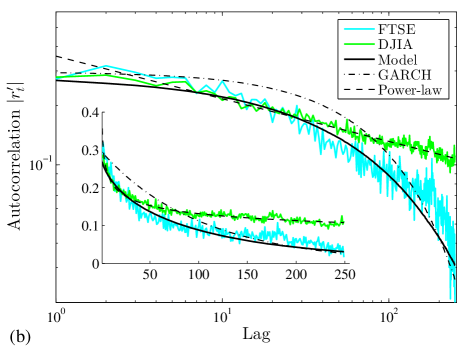

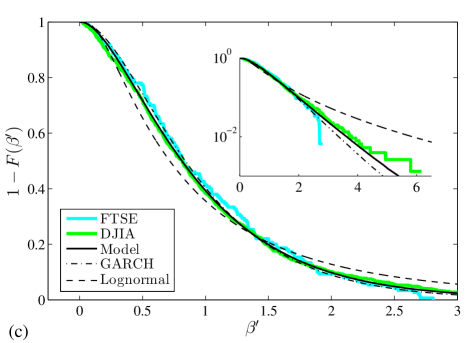

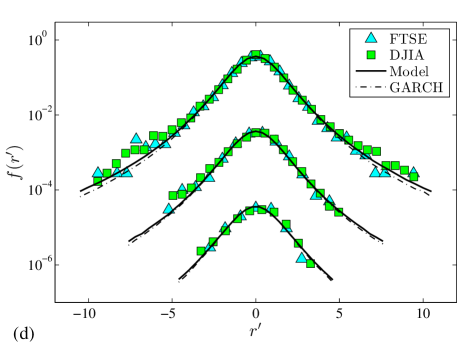

As seen in Figs. 1(a and b), the parameter sets the strength of volatility autocorrelations with larger values of producing stronger autocorrelations. As seen in Fig. 1(c), the distribution of the normalized inverse squared volatility, , is gamma distributed and largely unaffected by (although for , the peak of the distribution is slightly below the others). A gamma distributed should produce -distributed returns for , which is observed in the topmost curves in Fig. 1(d). As increases (moving to the lower curves in Fig. 1(d)), the return distribution adjusts from a Student’s -distribution to a Gaussian, with the speed of adjustment determined by . Higher values of correspond to a slowly varying volatility and therefore to a return distribution that retains its non-Gaussian shape at larger .

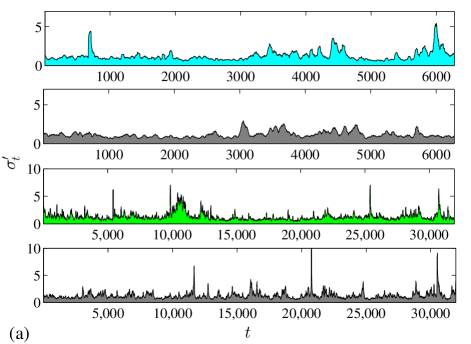

In Fig. 2 we compare the results of the model (, ) with two empirical financial time series: the daily price series of (a) the Dow Jones Industrial Average (DJIA) from May 26, 1896 to September 13, 2013 and (b) the FTSE 100 from January 2, 1985 to December 31, 2009. The DJIA data is from the St. Louis Federal Reserve website and the FTSE data is from finance.yahoo.com. From the price series, daily returns are calculated as in Eq. 1. Squared volatilities are estimated using a rolling window of two months of daily returns (42 trading days),

| (12) |

where is the estimated mean of the daily returns. We have systematically estimated the variance using window sizes from 10 to 100 days for the DJIA dataset. The variance distribution changes as the window size increases, but reaches a steady distribution for sizes larger than 40.

We have found that a good estimate of , is the inverse of the mean inverse variance,

| (13) |

Using this equation, we find for the DJIA data and for the FTSE data.

We estimate for each series by minimizing the sum of the squared difference between and its expected value, i.e., we find the that minimizes , where . Using this method, we find for the DJIA data and for the FTSE data.

Although we obtain a different for the two empirical price series, the values are sufficiently similar that we choose to compare both datasets to the model using the DJIA fit, (see Fig. 2). As in Fig. 1, the plots in Fig. 2 use the renormalizations of Eqs. 9-11 but with the estimated values of the parameters.

To demonstrate how well the model matches data, we compare its predicted results to alternatives. In Fig. 2(b) we compare the autocorrelation function from the model to that of a GARCH(1,1) process and also a power-law fit both calibrated to the DJIA data. The model reproduces the autocorrelation function for both datasets until about 25 lags. For higher lags, it continues to match the FTSE data but for the DJIA it is outperformed by the power-law fit. Care should be taken when drawing conclusions from these results, however, as autocorrelation functions fluctuate considerably and are misleading if the data contains structural breaksGranger and Hyung (2004). Note that the model does not produce long-memory in volatility, i.e., the autocorrelation function of the model is integrable.

For the distribution of the normalized inverse variance, we compare the model’s predictions to that of a GARCH(1,1) process calibrated to each dataset (see caption of Table I for parameters) and also to a gamma, an inverse-gamma (the Heston modelHeston (1993) predicts a gamma distributed variance, i.e., an inverse-gamma distributed inverse variance), and a lognormal fit (which is often assumed in the finance literature: see Andersen et al. (2001) and note that the inverse square of a lognormally distributed variable is also lognormally distributed). We specifically show the GARCH(1,1) prediction for the DJIA data and the lognormal fit for the DJIA data in Fig. 2(c), and we test all of the predictions and fits using a chi-square goodness-of-fit test (see Table I). In agreement with previous resultsGerig et al. (2009); Fuentes et al. (2009), the gamma distribution cannot be rejected for either dataset. The predicted distributions from the model also cannot be rejected for either dataset (the predictions are also not rejected for the unnormalized distributions). The distribution predicted by the GARCH(1,1) process is rejected for the DJIA data but not for the FTSE data (although not shown, the predictions for the unnormalized distributions are both rejected). Both the lognormal and inverse gamma fits are rejected.

Chi-square p-values Gamma Model GARCH Logn InvGam FTSE 0.49 0.19 0.13 0.03* 0.00** DJIA 0.42 0.38 0.00** 0.00** 0.00**

Financial time series have been studied by mathematicians and physicists over many yearsBachelier (1964); Mandelbrot (1963); Mantegna and Stanley (1999); Bouchaud and Potters (2003). Although the dynamics of prices are now well-characterized and understood, it is still unclear why prices exhibit the interesting properties that they do. This lack of understanding is especially troublesome because prices fluctuate in a universal, regular way, i.e., the returns of many different traded items all possess the same non-trival properties. It is therefore quite likely that some simple, robust mechanism underlies price dynamics, even if we have not yet discovered itGerig (2011).

We have presented a simple feedback model for volatility that matches empirical data very well using only two parameters. The model is unlike any other volatility model because our feedback mechanism is embedded in a parameter of the noise term, which is inverse gamma distributed. Although we do not show it here, the model can be connected to the stochastic volatility literature because under certain restrictions, it reduces to the 3/2 stochastic volatility modelPlaten and Heath (2006). Although also not shown, we have found that the model replicates the multifractal structure of returns and can be used to predict volatility better than the standard GARCH(1,1) model. The model does not produce the well-known correlation between negative returns and volatility (known as the leverage effect) nor does it explicitly include feedback effects on multiple timescalesMüller et al. (1997); LeBaron (2001); Zumbach and Lynch (2001); Borland and Bouchaud (2011), but these features could be added without difficulty.

Acknowledgements.

This work was supported by the European Commission FP7 FET-Open Project FOC-II (no. 255987) and a UTS Faculty of Business Research Grant.References

- Mandelbrot (1963) B. Mandelbrot, J. Business 36, 394 (1963).

- Fama (1965) E. F. Fama, J. Business 38, 34 (1965).

- T. Bollerslev, R. F. Engle, and D. B. Nelson in: (1994) T. Bollerslev, R. F. Engle, and D. B. Nelson in:, Handbook of Econometrics, Volume IV (North-Holland, Amsterdam, 1994).

- Guillaume et al. (1997) D. M. Guillaume, M. M. Dacorogna, R. D. Davé, U. A. Müller, R. B. Olsen, and O. V. Pictet, Finance Stochast. 1, 95 (1997).

- Cont (2001) R. Cont, Quant. Finance 1, 223 (2001).

- Bouchaud and Potters (2003) J. P. Bouchaud and M. Potters, Theory of Financial Risks and Derivative Pricing (Cambridge Univ. Press, Cambridge, U.K., 2003), 2nd ed.

- Borland et al. (2005) L. Borland, J.-P. Bouchaud, J.-F. Muzy, and G. Zumbach, Wilmott Magazine pp. 86–96 (2005).

- J. P. Bouchaud in: (2011) J. P. Bouchaud in:, Lessons from the 2008 Crises (Risk Books, London, U.K., 2011).

- Gerig et al. (2009) A. Gerig, J. Vicente, and M. A. Fuentes, Phys. Rev. E 80, 065102 (2009).

- Fuentes et al. (2009) M. A. Fuentes, A. Gerig, and J. Vicente, PLoS ONE 4, e8243 (2009).

- (11) T. Ma and R. A. Serota, e-print arXiv:1305.4173.

- Praetz (1972) P. D. Praetz, J. Business 45, 49 (1972).

- Blattberg and Gonedes (1974) R. C. Blattberg and N. J. Gonedes, J. Business 47, 244 (1974).

- Peiró (1994) A. Peiró, Applied Financial Economics 4, 431 (1994).

- Tsallis et al. (2003) C. Tsallis, C. Anteneodo, L. Borland, and R. Osorio, Physica A 324, 89 (2003).

- Platen and Rendek (2008) E. Platen and R. Rendek, J. Statistical Theory and Practice 2, 233 (2008).

- Gu et al. (2008) G. F. Gu, W. Chen, and W. X. Zhou, Physica A 387, 495 (2008).

- Gerig (2011) A. Gerig, Complexity 17, 9 (2011).

- Bollerslev (1986) T. Bollerslev, J. Econometrics 31, 307 (1986).

- Nelson (1990) D. B. Nelson, J. Econometrics 45, 7 (1990).

- Borland and Bouchaud (2011) L. Borland and J.-P. Bouchaud, J. of Investment Strategies 1, 65 (2011).

- E. Platen in: (2001) E. Platen in:, Mathematical Finance (Birkhauser, Basel, 2001).

- Platen and Heath (2006) E. Platen and D. Heath, A Benchmark Approach to Quantitative Finance (Springer-Verlag, Berlin, 2006).

- Granger and Hyung (2004) C. W. J. Granger and N. Hyung, J. Empirical Finance 11, 399 (2004).

- Heston (1993) S. L. Heston, Rev. Financial Studies 6, 327 (1993).

- Andersen et al. (2001) T. G. Andersen, T. Bollerslev, F. X. Diebold, and H. Ebens, J. Financial Economics 61, 43 (2001).

- Bachelier (1964) L. Bachelier, in The Random Character of Stock Prices, edited by H. Cooper, P. (MIT Press, Cambridge, 1964).

- Mantegna and Stanley (1999) R. N. Mantegna and H. E. Stanley, Introduction to Econophysics: Correlations and Complexity in Finance (Cambridge University Press, Cambridge, 1999).

- Müller et al. (1997) U. A. Müller, M. M. Dacorogna, R. D. Davé, R. B. Olsen, O. V. Pictet, and J. E. Weizsäcker, J. of Empirical Finance 4, 213 (1997).

- LeBaron (2001) B. LeBaron, Quant. Finance 1, 621 (2001).

- Zumbach and Lynch (2001) G. Zumbach and P. Lynch, Physica A 298, 521 (2001).