Ruin probability of a discrete-time risk process with proportional reinsurance and investment for exponential and Pareto distributions

Abstract

In this paper a quantitative analysis of the ruin probability in finite time of a discrete risk process with proportional reinsurance and investment of financial surplus is focused on. It is assumed that the total loss on a unit interval has a light-tailed distribution – exponential distribution and a heavy-tailed distribution – Pareto distribution. The ruin probability for finite-horizon 5 and 10 was determined from recurrence equations. Moreover, for exponential distribution the upper bound of ruin probability by Lundberg adjustment coefficient is given. For Pareto distribution the adjustment coefficient does not exist, hence an asymptotic approximation of the ruin probability if an initial capital tends to infinity is given. Obtained numerical results are given as tables and they are illustrated as graphs.

Keywords: discrete time risk process, ruin probability, proportional reinsurance, Lundberg’s inequality, regularly varying tail

1 Introduction

In the risk theory, works concerning the financial surplus of insurance companies in a continuous time have been proceeding for nearly a century. Very advanced models of the classical continuous risk process were established. Although such a model is more natural in the description of reality, the research on the discrete process of financial surplus is considerably more modest. The review of the results concerning the discrete process of financial surplus one can find in the paper [6]. This paper is one of the series of papers which try to bring closer of the classical discrete process of financial surplus to the reality of insurance companies. Namely, the analysis of the investment of financial surplus enhances the security of an insurance company. These problems are considered in the papers [1, 2, 3, 9, 10]. Reinsurance has a considerable influence on increasing the security of an insurance company. The results concerning a discrete risk process with investment and reinsurance can be found in [4, 7].

In this paper we consider the ruin probability in finite time of a discrete risk process with proportional reinsurance and investment of financial surplus. Moreover, we obtain numerical results for particular cases: exponential and Pareto distribution of a total loss and some asymptotic results.

In the paper by Cai and Dickson [3] the ruin probability in a discrete time risk process with a Markov interest model is studied. Recursive equations for the ruin probabilities, generalised Lundberg inequalities and an approximating approach to the recursive equations are given in that paper. Diaspara and Romera [4] introduced a proportional reinsurance in the discrete risk process with an investment.

For any reinsurance, not only proportional, Jasiulewicz [7] obtained recursive equations and Lundberg inequality for the ruin probability in the discrete-time risk process with Markovian chain interest rate model. Moreover, for the proportional reinsurance and the reinsurance of stop-loss an optimal level of retention was considered, assuming the maximisation of Lundberg adjustment coefficient as an optimising criterion.

This paper is a continuation of the research initiated by Jasiulewicz [7]. For the given theoretical results we conduct a detailed quantitative analysis for particular distributions of the total loss in a unit period and proportional reinsurance. We consider the ruin probability for a light-tailed distribution (exponential pdf) and a heavy-tailed distribution (Pareto pdf) taking into account an investment of finance surplus according to a random interest rate. Based on these considerations we give practical conclusions concerning connections between the initial capital level and the reinsurance level. We pointed out the level of reinsurance of a loss in order to set a ruin probability at the level low enough to be accepted by an insurer and vice versa i.e. how high his own capital should be.

The quality of the upper bound of ruin probability in finite time with the use of Lundberg coefficient was illustrated by the example of exponential distribution. We observe that if an insurer and a reinsurer use the same security loading then the adjustment coefficient as a function of the reinsurance level is convex, which considerably improves an upper estimation of the ruin probability. However, if loading of a reinsurer is greater than loading of insurer, the adjustment coefficient is not a convex function, which lowers the quality of an upper estimation. This observation was not taken into account in the numerical examples in Diaspara and Romera [4].

It is known that for heavy-tailed distributions Lundberg adjustment coefficient does not exist. For distributions of that type we give the theorem about the approximation of the ruin probability if the initial capital is sufficiently large. The example of Pareto distribution shows that such an approximation is appropriate and quickly tends to the limit value.

In the paper we assume the expectation of a loss in a unit period as a monetary unit. For that reason we assume that the expected values in both considered distributions are equal to 1. For the assumed values of parameters in Pareto distribution a variance does not exist. To compare numerical results for both distributions we also take such parameters in order to obtain the same geometric means as well as geometric variances.

Concluding, below we list the new elements, ideas and results which are introduced in this article:

-

1.

In the continuous risk process the level of retention is optimal if it minimises the ruin probability which can be determined by maximising an adjustment coefficient relative to the level of retention (see Dickson and Waters [5]). Then we can pose the following natural question: does the discrete risk process hold the same?

-

2.

The upper bound of the ruin probability obtained by Lundberg coefficient in the case of proportional reinsurance is given by Diaspara and Romera [4]. The numerical example for shows that this estimation is reasonable. Is that estimation also good for the more natural case ?

-

3.

In the case of heavy tailed claims we give the approximation of the ruin probability. The question is: is the sequence of approximations is fast convergent for sufficiently large initial capital?

2 Notations and theorems

Further notations, assumptions and theorems 1 and 2 given below come from the paper by Jasiulewicz [7]. In that paper the following notations and assumptions were taken.

-

1.

Let denote the total loss in unit period . The loss is calculated at the end of each period. Let us assume that is a sequence of independent and identically distributed random variables with a common distribution function .

-

2.

The premium is calculated by the expected value principle with the loading factor . Constant premium is paid at the end of every unit period .

-

3.

The insurer’s surplus at the moment is denoted by and is calculated after the payoff. The surplus is invested at the beginning of the period at a random rate .

-

4.

Let us assume that the interest rates follow a time-homogeneous Markov chain. We further assume that for all , the rate takes possible values . For all and all states, the transition probability is denoted by

and the initial distribution is denoted by

-

5.

Suppose that the insurer effects reinsurance and that the amount paid by the insurer when the loss occurs is where a parameter denotes a retention level. The meaning of the parameter will be explained in two examples of the most frequent reinsurancies applied in the insurance practice.

-

(a)

Proportional reinsurance, if a function has the form

where .

-

(b)

Stop loss reinsurance, if a function has the form

where .

The following assumption about is obvious. A part of the loss retained by the insurer is denoted by and its distribution function by . Therefore is a reinsured part of the loss .

-

(a)

-

6.

Le us assume that a reinsurer calculates a premium rate according to the expected value rule with a loading factor , i.e.

We assume that , so an insurer does not earn without risk if he retains only zero value of claims.

-

7.

The premium rate retained by an insurer in a unit period is denoted by and is given by

-

8.

Let denote a financial surplus of an insurer at the end of the unit period after the payment of premium and after the payoff. The process considered in the paper is given by

-

9.

The ultimate ruin probability for this risk process in the finite time is denoted by and is defined by

The ultimate ruin probability in the infinite time is given by

Obviously

The further research is conducted for a proportional reinsurance. The premium rate retained by an insurer is

| (2.1) |

To avoid such an event that the ruin could occur with probability 1 it is assumed that

| (2.2) |

To write the self-contained paper, we give theorems from Jasiulewicz [7] (Theorems 1 and 2), which will be used in the analysis of the ruin probability. In the special case of reinsurance, namely proportional reinsurance, the theorems analogous to Theorems 1 and 2 were given in the paper by Diaspara and Romera [4].

Theorem 1.

Ruin probability of an insurer in finite time is given recursively in the following way:

| (2.3) | ||||

| (2.4) | ||||

Ruin probability in infinite time:

where

| (2.5) |

Proof.

Let , . If , then a ruin will occur in the first period . Therefore

The ruin in first periods can occur in two excluding ways:

-

•

the ruin will occur in the first period or

-

•

the ruin will not occur in the first period but it will occur in next periods.

Since the process is stationary with independent increments then

The probability of the ruin in infinite time is obtained by taking a two-sided limit in the above formula for . ∎

Recurrence formulas for the ruin probability can be presented in a matrix form, which simplifies calculations using several computer programs888In this paper the calculations were made by program Maxima: http://maxima.sourceforge.net/ . .

Theorem 2.

If and there exists a positive constant fulfilling the equation

| (2.6) |

the upper estimation of the ruin probability in finite and infinite time is in the form

| (2.7) |

where

| (2.8) |

Proof.

Whereas the inequality (2.8) follows from the fact that for an inequality occurs. Therefore

From the conversion of this inequality the inequality (2.8) is obtained.

Theorem 1 gives recurrence formulae for the ruin probability and Theorem 2 gives an upper estimation of the ruin probability using Lundberg adjustment coefficient, which exists only for a light-tailed distribution. Therefore one cannot use Theorem 2 to estimate the ruin probability for heavy-tailed distributions. In that case we will use an asymptotic ruin probability in the respect of an initial capital tending to infinity, whereas the total loss has the distribution with a regularly varying tail.

Definition 1.

A distribution on has a regularly varying tail if there exists some constant such that for every is

The class of such distributions is denoted by .

Theorem 3.

Let total loss have cdf for some . If for any fixed there exists a finite positive moment of rank of discounting factor , then for a proportional reinsurance for every and every we have

| (2.13) |

if , where are given recursively

| (2.14) |

with an initial condition for

Proof.

In the paper by Cai and Dickson [3] the above theorem was proved in the case where an insurer does not apply reinsurance but invests the financial surplus. It is sufficient to remark that with proportional reinsurance , if has a distribution with a regularly changing tail with an index , then has also the distribution with a regularly varying tail with an index . This follows from

where , if , because . Therefore our Theorem 3 is fulfilled for by Theorem 5.1 from the paper Cai and Dickson [3]. Our proof repeats the arguments given in Theorem 5.1 from that paper if we substitute with . ∎

In the next sections we will consider particular cases if the total loss in the unit period has an exponential distribution with mean 1, i.e. and has Pareto distribution with the same mean: , , , . In Section 3 we give analytical formulae only for the cases , (i.e. financial surplus is not invested) and small values of the parameter . To determine these formulae we use the program Maxima assigned to symbolic calculations.

Numerical results will be presented for the case and for selected values of the parameters , , , and .

3 Ruin probability

Calculations of values of function given by Theorem 1 were conducted for , and . We considered the cases

-

•

for ,

-

•

for , with transition matrix

The values and were taken. For from (2.5) we obtain the formula

The condition (2.2) is fulfilled for .

3.1 Exponential distribution

Let us assume that has the exponential distribution with mean 1. Hence has the distribution function

| (3.1) |

for and , .

The explicit formulae for function for are too complicated to present. We take and .

| (3.2) | ||||

| (3.5) |

Formulae for for obtained from Maxima were used to verify the correctness of numerical algorithms which are used for greater and .

| 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | 1.0 | |||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 5 | 1 | 0.0087 | 0.0385 | 0.0776 | 0.1164 | 0.1512 | 0.1814 | 0.2073 | 0.2299 | 0.2494 | |

| 2 | 0.0001 | 0.0029 | 0.0119 | 0.0271 | 0.0460 | 0.0665 | 0.0871 | 0.1074 | 0.1265 | ||

| 3 | 0.0000 | 0.0002 | 0.0017 | 0.0060 | 0.0134 | 0.0236 | 0.0357 | 0.0491 | 0.0630 | ||

| 4 | 0.0000 | 0.0000 | 0.0002 | 0.0013 | 0.0038 | 0.0081 | 0.0143 | 0.0220 | 0.0308 | ||

| 5 | 0.0000 | 0.0000 | 0.0000 | 0.0003 | 0.0010 | 0.0027 | 0.0056 | 0.0096 | 0.0148 | ||

| 1 | 0.0046 | 0.0256 | 0.0580 | 0.0934 | 0.1267 | 0.1568 | 0.1832 | 0.2067 | 0.2271 | ||

| 2 | 0.0001 | 0.0015 | 0.0077 | 0.0196 | 0.0357 | 0.0542 | 0.0734 | 0.0927 | 0.1113 | ||

| 3 | 0.0000 | 0.0001 | 0.0010 | 0.0040 | 0.0098 | 0.0183 | 0.0288 | 0.0409 | 0.0539 | ||

| 4 | 0.0000 | 0.0000 | 0.0001 | 0.0008 | 0.0026 | 0.0061 | 0.0111 | 0.0178 | 0.0257 | ||

| 5 | 0.0000 | 0.0000 | 0.0000 | 0.0002 | 0.0007 | 0.0020 | 0.0042 | 0.0076 | 0.0121 | ||

| 10 | 1 | 0.0112 | 0.0493 | 0.0978 | 0.1448 | 0.1856 | 0.2203 | 0.2494 | 0.2749 | 0.2964 | |

| 2 | 0.0003 | 0.0049 | 0.0190 | 0.0411 | 0.0669 | 0.0936 | 0.1193 | 0.1442 | 0.1669 | ||

| 3 | 0.0000 | 0.0005 | 0.0035 | 0.0113 | 0.0236 | 0.0391 | 0.0564 | 0.0748 | 0.0932 | ||

| 4 | 0.0000 | 0.0000 | 0.0006 | 0.0030 | 0.0081 | 0.0160 | 0.0262 | 0.0383 | 0.0515 | ||

| 5 | 0.0000 | 0.0000 | 0.0001 | 0.0008 | 0.0027 | 0.0064 | 0.0119 | 0.0193 | 0.0281 | ||

| 1 | 0.0049 | 0.0282 | 0.0654 | 0.1064 | 0.1452 | 0.1800 | 0.2103 | 0.2372 | 0.2605 | ||

| 2 | 0.0001 | 0.0020 | 0.0101 | 0.0256 | 0.0462 | 0.0695 | 0.0932 | 0.1168 | 0.1392 | ||

| 3 | 0.0000 | 0.0001 | 0.0015 | 0.0061 | 0.0146 | 0.0267 | 0.0411 | 0.0574 | 0.0742 | ||

| 4 | 0.0000 | 0.0000 | 0.0002 | 0.0014 | 0.0046 | 0.0101 | 0.0180 | 0.0280 | 0.0393 | ||

| 5 | 0.0000 | 0.0000 | 0.0000 | 0.0003 | 0.0014 | 0.0038 | 0.0078 | 0.0135 | 0.0206 | ||

From Table 1 we obtain the following conclusions.

-

•

If the initial capital grows, the part of the insurer’s retained loss also grows with the constant level of risk of the company bankruptcy for any time horizon .

-

•

If the initial invention rate grows then the level of retention also grows with the constant ruin probability for any time horizon .

-

•

If time horizon grows, then the ruin probability grows for every fixed and interest rate . The greater , the smaller ruin probability.

| Initial capital | 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|---|

| 0.3289 | 0.6188 | 0.9062 | 1.0000 | 1.0000 | ||

| 0.3752 | 0.6775 | 0.9700 | 1.0000 | 1.0000 | ||

| 0.3005 | 0.5339 | 0.7626 | 0.9876 | 1.0000 | ||

| 0.3585 | 0.6160 | 0.8549 | 1.0000 | 1.0000 | ||

Table 2 implies that with initial capital and interest rate for every the ruin probability does not exceed for time horizon and . This means that without using an insurance the insurer is exposed to bankruptcy with a small probability not exceeding .

In Table 2 the number 1 means that without reinsurance an insurer will have the level of bankruptcy below .

We calculate the parameter from Equation (2.8) for defined by (3.1):

| (3.6) |

We calculate the integral under assumption that :

After substitution to (3.6) we have

Hence

| (3.7) |

For the parameter the adjustment coefficient is the positive solution of Equation (2.6). Since the moment generating function has the form

where , then Equation (2.6) has the form

from which we determine .

Based on Theorem 2, the upper estimation of the ruin probability has the form

| (3.8) |

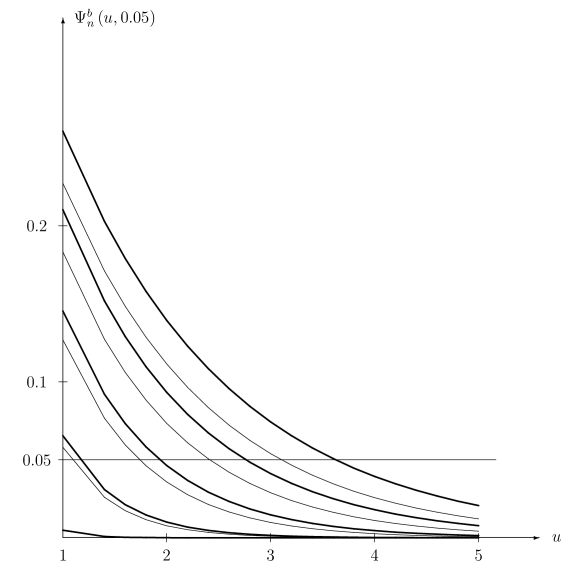

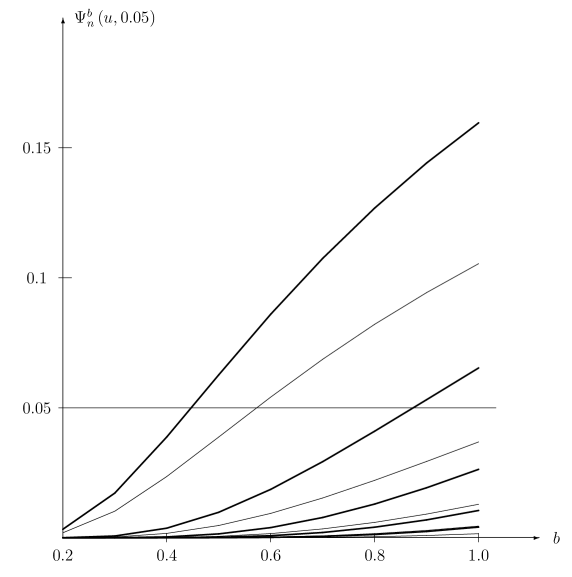

Let us denote the right-hand-side of the inequality (3.8) by . Figure 1 depictes graphs of for an exponential distribution for and , for each one for and for . In Figure 2 graphs of for and were depicted, for and for . Graphs for are almost the same so we omit them. The differences are easy to observe in Table 1.

3.2 Pareto distribution

We assume that the total loss has Pareto distribution with the distribution function

| (3.9) |

for . The random variable has the expectation

for and a variance

for .

We assume that . Hence the parameter must be in the form

The loss retained by insurer has cdf

| (3.10) |

for .

In the numerical calculations we assume similarly to the paper by Palmowski [8]. In this paper it was show that the greatest losses which came out at the end of eighties and nineties of XX century have Pareto distribution with the parameter approximately equal to 1.24138. With such a value of the variance is infinite.

From (2.5) we have

The function can be set by (2.3) in explicit form only for , and .

| (3.11) |

The cases need numerical integrations. Let us consider the case . In this case it is necessary to calculate the integral

Substituting we come to the problem of the calculation of the integral

where is the hypergeometric function.

| 0.2 | 0.3 | 0.4 | 0.5 | 0.6 | 0.7 | 0.8 | 0.9 | 1.0 | |||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 5 | 1 | 0.0471 | 0.0663 | 0.0818 | 0.0945 | 0.1050 | 0.1156 | 0.1214 | 0.1280 | 0.1337 | |

| 2 | 0.0255 | 0.0384 | 0.0499 | 0.0602 | 0.0693 | 0.0787 | 0.0846 | 0.0912 | 0.0972 | ||

| 3 | 0.0169 | 0.0263 | 0.0352 | 0.0434 | 0.0510 | 0.0590 | 0.0644 | 0.0704 | 0.0759 | ||

| 4 | 0.0124 | 0.0197 | 0.0267 | 0.0335 | 0.0399 | 0.0468 | 0.0515 | 0.0569 | 0.0618 | ||

| 5 | 0.0097 | 0.0156 | 0.0214 | 0.0270 | 0.0325 | 0.0384 | 0.0427 | 0.0474 | 0.0519 | ||

| 1 | 0.0421 | 0.0603 | 0.0754 | 0.0880 | 0.0986 | 0.1092 | 0.1154 | 0.1222 | 0.1281 | ||

| 2 | 0.0234 | 0.0356 | 0.0466 | 0.0566 | 0.0655 | 0.0748 | 0.0807 | 0.0873 | 0.0933 | ||

| 3 | 0.0158 | 0.0247 | 0.0332 | 0.0411 | 0.0485 | 0.0563 | 0.0617 | 0.0676 | 0.0730 | ||

| 4 | 0.0118 | 0.0187 | 0.0254 | 0.0320 | 0.0382 | 0.0448 | 0.0495 | 0.0548 | 0.0597 | ||

| 5 | 0.0092 | 0.0148 | 0.0204 | 0.0259 | 0.0312 | 0.0370 | 0.0411 | 0.0458 | 0.0502 | ||

| 10 | 1 | 0.0685 | 0.0947 | 0.1150 | 0.1312 | 0.1442 | 0.1599 | 0.1640 | 0.1718 | 0.1785 | |

| 2 | 0.0405 | 0.0599 | 0.0765 | 0.0907 | 0.1029 | 0.1175 | 0.1226 | 0.1309 | 0.1382 | ||

| 3 | 0.0282 | 0.0432 | 0.0568 | 0.0690 | 0.0798 | 0.0929 | 0.0980 | 0.1060 | 0.1131 | ||

| 4 | 0.0213 | 0.0334 | 0.0448 | 0.0552 | 0.0648 | 0.0765 | 0.0814 | 0.0888 | 0.0956 | ||

| 5 | 0.0170 | 0.0270 | 0.0367 | 0.0458 | 0.0542 | 0.0647 | 0.0694 | 0.0762 | 0.0826 | ||

| 1 | 0.0582 | 0.0829 | 0.1028 | 0.1191 | 0.1325 | 0.1480 | 0.1532 | 0.1615 | 0.1687 | ||

| 2 | 0.0354 | 0.0533 | 0.0691 | 0.0829 | 0.0949 | 0.1091 | 0.1148 | 0.1232 | 0.1307 | ||

| 3 | 0.0252 | 0.0391 | 0.0519 | 0.0635 | 0.0740 | 0.0866 | 0.0921 | 0.1000 | 0.1072 | ||

| 4 | 0.0194 | 0.0306 | 0.0413 | 0.0513 | 0.0605 | 0.0717 | 0.0768 | 0.0841 | 0.0908 | ||

| 5 | 0.0156 | 0.0250 | 0.0341 | 0.0427 | 0.0509 | 0.0609 | 0.0656 | 0.0723 | 0.0786 | ||

| Initial capital | 1 | 2 | 3 | 4 | 5 | |

|---|---|---|---|---|---|---|

| 0.2190 | 0.4052 | 0.5907 | 0.7696 | 0.9621 | ||

| 0.2468 | 0.4379 | 0.6209 | 0.8133 | 0.9996 | ||

| lack | 0.2567 | 0.3582 | 0.4588 | 0.5588 | ||

| lack | 0.2884 | 0.3933 | 0.4958 | 0.5974 | ||

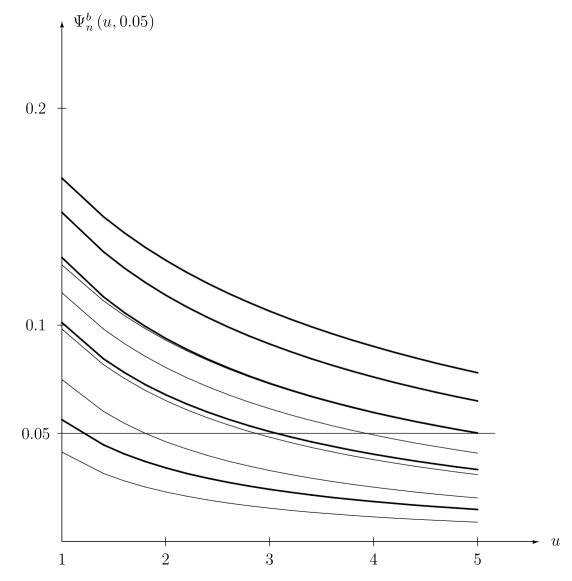

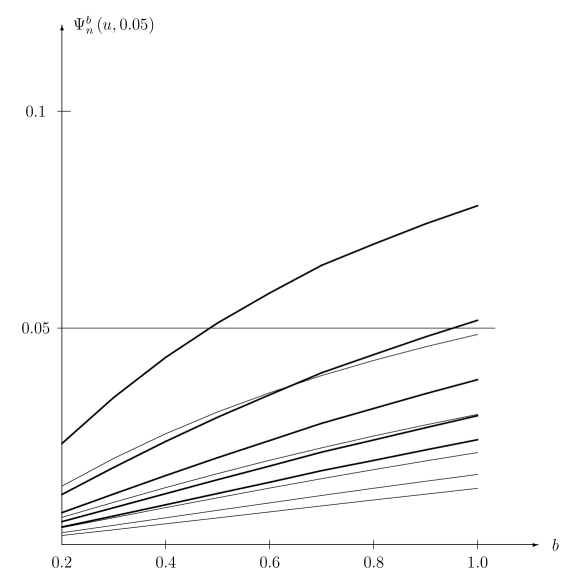

Table 3 gives the same conclusion as for exponential distribution. Word “lack” in Table 4 means that for any level of retention with initial capital , the ruin probability exceeds both for a five-years-time horizon and for a ten-year-time horizon. In Figure 3 graphs of for and for Pareto distribution were depicted for . In Figure 4 graphs of for and , for and . Graphs for are almost the same so we omit them. The differences are easy to observe in Table 3.

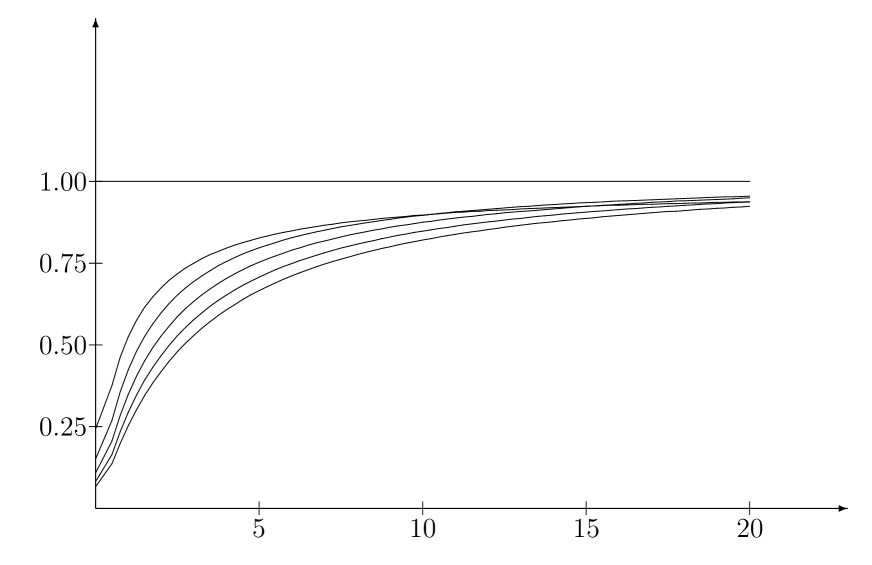

Taking an advantage from Theorem 3 we will present the results concerning an approximation of ruin probability for Pareto distribution. In Figure 5 the ratio

for , and was depicted.

4 Conclusions

In the continuous risk process the optimal level of retention can be determined by maximising of an adjustment coefficient relative to the level of retention. In the discrete risk process the above statement is not true.

For the fixed initial capital the probability of ruin is an increasing function of the retention level . Therefore the probability of the ruin is minimal if the retention level is minimal. It means that an insurer retains only very low losses which causes very low income and is very unfavourable for him. It seems that the right approach relies on fixing an acceptable level of the ruin probability, and appropriately to this probability, determining the retention level.

If loading of a reinsurer is greater than loading of an insurer (), the adjustment coefficient is not a convex function, which lowers the quality of upper estimation. Basing on our numerical examples we conclude that such an upper bound is very imprecise, and basically it is worthless. For the heavy tailed claims we give the theorem about the approximation of the ruin probability if the initial capital is sufficiently large. The example of Pareto distribution shows that such an approximation is appropriate and quickly tends to the limit value.

Acknowledgements

The research by Helena Jasiulewicz was supported by a grant from the National Science Centre, Poland.

References

- [1] CAI, J., Discrete time risk models under rates of interest. Prob. Eng. Inf. Sci. 16, 309–324 (2002)

- [2] CAI, J., Ruin probabilities with dependent rates of interest. J. Appl. Prob. 39, 312–323 (2002)

- [3] CAI, J., DICKSON, D.C.M., Ruin probabilities with a Markov chain interest model. Insurance Math. Econom. 35, 513–525 (2004)

- [4] DIASPARRA, M.A., ROMERA, R., Bounds for the the ruin probability of a discrete-time risk process. J. Appl. Probab. 46, 99–112 (2009)

- [5] DICKSON, D.C.M., WATERS, H.R., Reinsurance and ruin. Insurance Math. Econom. 19, 61–80 (1996)

- [6] JASIULEWICZ, H., Discrete-time financial surplus models for insurance companies. Annals of the Collegium of Economic Analysis 21, 225–255 (2010)

- [7] JASIULEWICZ, H., Discrete risk process with reinsurance and random interest rate. Annals of the Collegium of Economic Analysis 31, 11–26 (2013). (in polish)

- [8] PALMOWSKI, Z., Approximations of ruin probability of insurance company in diffusion Cox model. Research Papers of Wrocław University of Economics 1108, 34–64 (2006). (in polish)

- [9] TANG, Q., TSITSIASHVILI, G., Precise estimates for the ruin probability in finite horizon in a discrete-time model with heavy-tailed insurance and financial risk. Stochastic Processes Appl. 108, 299–325 (2003)

- [10] YANG, H., Non-exponential bounds for ruin probability with interest effect included. Scand. Actuarial J. 99, 66–79 (1999)