Making Mean-Variance Hedging Implementable

in a Partially Observable Market

-with supplementary contents for stochastic interest rates-111

All the contents expressed in this research are solely those of the authors and do not represent any views or

opinions of any institutions. The authors are not responsible or liable in any manner for any losses and/or damages caused by the use of any contents in this research.

Masaaki Fujii222Graduate School of Economics, The University of Tokyo. e-mail: mfujii@e.u-tokyo.ac.jp,

Akihiko Takahashi333Graduate School of Economics, The University of Tokyo. e-mail: akihikot@e.u-tokyo.ac.jp

(

First version: June 14, 2013, This version: November 15, 2013)

Abstract

The mean-variance hedging (MVH) problem is studied in a partially observable

market where the drift processes can only be inferred through the observation of asset

or index processes. Although most of the literatures treat the MVH

problem by the duality method, here we study a system consisting of three BSDEs

derived by Mania and Tevzadze (2003) and Mania et.al.(2008) and try to provide

more explicit expressions directly implementable by practitioners. Under the Bayesian

and Kalman-Bucy frameworks, we find that a relevant BSDE can yield a semi-closed

solution via a simple set of ODEs which allow a quick numerical evaluation. This

renders remaining problems equivalent to solving European contingent claims

under a new forward measure, and it is straightforward to obtain a forward looking non-sequential Monte Carlo simulation

scheme. We also give a special example where the hedging

position is available in a semi-closed form.

For more generic setups, we provide explicit expressions of

approximate hedging portfolio by an asymptotic expansion.

These analytic expressions not only allow the hedgers to update the hedging positions

in real time but also make a direct analysis of the terminal distribution of the hedged

portfolio feasible by standard Monte Carlo simulation.

We have added a brief note on a stochastic short rate and Interest-Rate Futures

to the original version accepted by Quantitative Finance for publication.

Since the last financial crisis, there are market-wide efforts for

standardization of financial products so that they can be traded through

security exchanges or central counterparties.

This is expected to make them more liquid, transparent,

remote from counterparty credit risks, and in particular significantly

reduces the regulatory cost for financial firms.

For these products, an

idealistic situation for electronic trading is emerging and

many financial firms are heavily investing to setup sophisticated e-trading systems

to maintain their profitability for coming years.

At first sight,

it might appear that it leads the financial market closer to the ideal “complete” environment.

However, on the other hand, remaining uncleared

OTC contracts are going to be severely penalized in terms of regulatory cost

so that it gives financial firms a strong incentive to walk away from them.

This inevitably makes a part of security universe less liquid and costlier to trade,

and can make practitioners reluctant to use them even if they were the most efficient

hedging instruments before the crisis.

The last crisis also created another complication by

pushing all the practitioners into a new pricing regime for the collateralized contracts.

Growing recognition of the critical importance of

the choice of collateral and its funding cost makes it impossible to perfectly

hedge even a very simple cash flow unless one has an easy access to the

relevant collateral assets or there exist very liquid basis markets.

Considering the above situation, we naturally expect that there

is a growing need of systematic hedging method allowing

investors to flexibly choose the hedging instruments

based on their own regulatory and accessibility conditions.

Mean-variance hedging (MVH) is a one possible approach to this problem.

MVH has been studied by many authors through duality method and there exist vast literatures on

the related issues. See, as recent works, Laurent & Pham (1999) [12],

Pham (2001) [18] and references therein 444

See also Pham & Quenez (2001) [19] as an application of duality

for the utility maximization in a partially observable market..

Although the mathematical understanding of the MVH problem has been greatly progressed

by those adopting the duality,

more practical issues related to the actual implementation of a hedging program

have not attracted much attention so far and there exist only a few special examples

reported with explicit expressions.

In this paper, we try to make a progress in that direction

by studying the system of equations derived by Mania, Tevzadze and

their co-authors.

In Mania & Tevzadze (2003) [13], the authors

studied a minimizing problem of a convex cost function

and showed that the optimal value function follows

a backward stochastic partial differential equation (BSPDE).

They have used the flow dynamics of the value function derived from the Itô-Ventzell formula

combined with a martingale property of the optimal value function to obtain a

BSPDE as a sufficient condition for the optimality.

For the MVH problem, they showed that the BSPDE can be decomposed into

three backward stochastic differential equations (BSDEs).

The technique is extended for a partial information setup by Mania et.al.(2008) [15],

for utility maximization by Mania & Santacroce (2010) [16],

and for MVH problem with general semimartingales by

Jeanblanc et.al. (2012) [7].

In the following, we consider the MVH problem in a partially observable market

where the drift processes can only be inferred through the observation

of stock or any index processes driven by Brownian motions possibly

with stochastic volatilities.

Under the Bayesian and Kalman-Bucy frameworks,

we find that a relevant BSDE yields an semi-closed solution

via a simple set of ODEs allowing a quick numerical evaluation.

This renders remaining problems equivalent to

solving European contingent claims, and it is

straightforward to obtain a forward looking

Monte Carlo simulation scheme using a simple particle method [4].

As far as the optimal hedging positions are concerned, it is also pointed out that

one only needs the standard simulations for the terminal liability and its

Delta sensitivities against the state processes under a certain forward measure.

We also provide explicit expressions for a solvable case and approximate

hedging portfolio for more generic setups by an asymptotic expansion method.

These explicit forms allow the hedgers to update the hedging positions in real time,

and also make the direct analysis of the terminal distribution of

the hedged portfolio feasible by standard Monte Carlo simulation.

We also provide several numerical examples to demonstrate our procedures.

2 The Market Setup

Let be a complete probability space equipped with

a filtration , where is a fixed time horizon.

We consider a financial market

with a risk-less asset, tradable stocks or indexes , and

non-tradable indexes or otherwise

state processes relevant for stochastic volatilities .

For simplicity, we assume that the interest rate is zero in the main body of the paper.

In Section 10, we shall discuss possible extensions with a stochastic interest rate,

which can be relevant if the hedging target is sensitive to a change of the yield curve.

Using a vector notation of and , we write the dynamics of the underlyings as

(2.1)

(2.2)

Here, are independent -Brownian motions with

dimension and .

and are -adapted market price-of-risk (MPR) processes

for and .

, and

are assumed to be known smooth functions

taking values in ,

and .

We assume all of them satisfy the technical conditions to allow

unique strong solutions for and .

We denote the available information set for the investor by

a sub--field .

We assume that is the -augmentation of filtration

generated by the processes of all the stocks and a subset

which are continuously observable assets or indexes but not tradable by the investor by

regulatory or some other reasons.

Although and can be

observed continuously, we assume that the investor cannot identify their drifts and Brownian

shocks independently, which is most likely the case in the real financial market.

Thus, neither nor is -adapted.

Through the observation

of quadratic covariation of and ,

we can recover the values of , and at each time.

We assume the maps are constructed in such a way that they allow to

fix the values of all the remaining uniquely from the values of at every time .

Thus, under the above construction, the whole elements of are in fact -adapted.

Let us further assume and are always nonsingular and thus

(2.3)

(2.4)

are actually -adapted processes.

3 Linear Filtering

From the expressions and and the fact that

both of are observable, we have a linear observation system

for the MPR processes. If we further assume that the MPRs

are either constants or linear Gaussian processes in , then

the system becomes a well-known Bayesian or Kalman-Bucy filtering model.

See a textbook written by Bain & Crisan (2008) [1] for

the details of stochastic filtering.

Let us denote

(3.1)

for notational simplicity, and then we put

(3.2)

For linear filtering models we discuss below, is actually shown to be

a true -martingale. We can then define a new measure by

(3.3)

then, it is easy to check

(3.4)

is a -dimensional -Brownian motion.

By (2.1) and (2.2), one can see that is actually the

augmented filtration generated by (See Ref. [19] for details.).

-martingale gives the inverse relation between the measures

(3.5)

We denote the expectation of the MPRs conditional on by

(3.6)

By Kallianpur-Striebel formula, it is given by

(3.7)

where is the expectation under measure.

This equation can be explicitly solvable for a Bayesian and also for

a linear Gaussian model.

Note that the processes defined by

(3.8)

(3.9)

are called innovation processes and they are -Brownian motions.

3.1 A Bayesian model

In this section, we consider a Bayesian model in which the MPR is assumed to be

-measurable with a known prior distribution.

The constant vector

(3.10)

denotes a value of the MPR.

For a concrete calculation, let us assume that has a prior Gaussian distribution

with the mean and its covariance denoted by a positive

definite symmetric matrix . Let us denote the corresponding density function by .

In this setup, one has

(3.11)

and hence

(3.12)

This yields

(3.13)

For a Gaussian prior distribution, can be evaluated explicitly.

One can show that

(3.14)

Using a new positive definite symmetric matrix defined by

(3.15)

and , one obtains

(3.16)

Then, simple calculation gives

(3.17)

As a result, the conditional expectation of the MPR is given by

(3.18)

Using a simple fact

(3.19)

one can easily confirm that

(3.20)

Thus, the dynamics of can be written as

(3.21)

i.e.,

(3.22)

where we have used a shorthand notation

(3.23)

Thus, we can see that is a Gaussian martingale process in .

3.2 A Kalman-Bucy model

In this model, we assume (or, “signal”) follows a linear Gaussian process in :

(3.24)

where and are constants.

denotes -dimensional -Brownian motions independent of .

The MPR is assumed to have a prior Gaussian distribution with mean and covariance matrix .

The observation is made through

(3.25)

In this case, we have a well-known result that

(3.26)

where is a deterministic function given as a solution of

the following ODE:

(3.27)

with the initial condition .

We assume that is positive definite for all .

In the remainder of the paper, we provide the detailed calculations only for

this Kalman-Bucy model. For Bayesian case, one can get the equivalent results by simply putting

and using the relevant given in (3.15) in

the corresponding formulas.

Kalman-Bucy scheme still works in the same way with time-dependent deterministic coefficients

. The equations (3.26) and (3.27) hold true by simply replacing the

constants with the corresponding time-dependent functions. All the discussions in the paper can be also

extended straightforwardly to this case.

However, throughout this paper, we treat the constant-coefficients case only.

This is for simplicity and also for the practical difficulty to estimate the time-dependent functions

using the market data in reality.

Remark

Let us comment on the differences from the related work Pham (2001) [18], in which

the author has also worked on MVH problem under Bayesian and Kalman-Bucy frameworks.

In the paper, the author considered the setup where the market observables are

the tradable stocks only, of which the volatility function is assumed to be

independent of the non-tradable indexes.

In addition, the hedging target at the maturity was assumed to be given by

a function of and , where is -measurable and

independent of under the measure . In our notations, it also means that

is independent of and that is absent.

In the current paper, we do not make these simplifying assumptions and deal with practically

more relevant situations.

4 A System of BSDEs for Mean-Variance Hedging

Since we are assuming that the interest

rate is zero,

the dynamics of wealth with the initial capital at is given by

(4.1)

where is a portfolio strategy. Here,

denotes a set of -dimensional -predictable processes satisfying

appropriate integrability conditions.

Our problem is to solve

(4.2)

In this paper, we suppose is some -measurable (and hence the investor can

exactly know the terminal liability) square integrable random variable, that is .

Mania & Tevzadze [13, 15] proved (using more general setup) that

a solution of the above problem is given by

(4.3)

where and are the solutions of the following BSDEs:

(4.4)

(4.5)

(4.6)

with some positive constant such that under the

existence of equivalent martingale measures and with some mild conditions.

Here, all the are -adapted processes with

appropriate dimensionality.

The corresponding optimal wealth process is given by

(4.7)

Using the relationship

(4.8)

one can easily read off the optimal hedging position from (4.7) as

(4.9)

In our setup with Brownian motions, derivation of the above BSDEs is quite straightforward by

using Itô-Ventzell formula and the martingale property of for the optimal strategy.

The main ideas are briefly explained in Appendix A.

The detailed explanation on Itô-Ventzell formula is available, for example, in the section 3.3 of a textbook [11]

as a generalized Itô formula. It is quite interesting to see there exists a direct link between the

BSPDE and the usual HJB equation.

See discussions given in Mania & Tevzadze (2008) [14] for this point.

5 Solving by ODEs

We now try to solve for our Kalman-Bucy filtering model.

Firstly, using the fact that , we transform and as follows:

(5.1)

Simple calculation gives a quadratic growth BSDE

(5.2)

The only ingredient of the BSDE is and it has a linear Gaussian form.

Unfortunately, the proof for the existence as well as the

uniqueness of the quadratic growth BSDE (5.2) seems unknown at the moment. This is, in particular,

due to the existence of unbounded MPR processes in its driver.

In the case of the bounded MPR processes, we can borrow the proof given in Kobylanski (2000) [9],

or by directly treating the BSDE of as done in Kohlmann & Tang (2002) [10].

As we shall see below, we can at least confirm its existence by checking

the existence of a bounded solution for the Riccati ordinary differential equation numerically

for the relevant interval .

Let us suppose that the solution has the following

form:

(5.3)

where are deterministic functions taking values in ,

and . We can take as a symmetric form.

Then, simple application of Itô formula gives

and () are () matrices

obtained by restricting to the first (last ) rows of ,

and is the diagonal matrix which has for the first elements

and for all the others.

On the other hand, the dynamics of in (3.26) and Itô formula

yield

(5.7)

Matching the coefficients of and a remaining constant term respectively,

and using the fact that , one obtains

the following ODEs 555Put and use the corresponding for

our first Bayesian model.:

(5.8)

(5.9)

(5.10)

with terminal conditions .

The ODEs can be solved sequentially in order.

Due to the quadratic form, the existence of is not guaranteed

and it possibly blows up in finite time.

The sufficient conditions for a bounded solution have been intensively studied for this type of

Riccati matrix differential equations. See, for example, Kalman (1960) [8],

Jacobson (1970) [6] and references therein.

In our setting, it requires negative semidefinite, which does not hold in general unfortunately.

However, it is still clear that stays finite in a certain interval around .

As long as has a realistic size, the non-blow-up interval seems

wide enough for practical applications in finance.

In any case, the behavior of can be

easily checked numerically.

Once we confirm the boundedness of (and hence also for )

for the relevant interval , we can see that the (5.3) actually

satisfies the BSDE by the standard application of Itô formula. It then

guarantees the existence of the solution for the BSDE (5.2).

In fact, this technique for a quadratic BSDE was already discussed in Schroder & Skiadas (1999) [20]

in the application to a recursive utility, but to the best of our knowledge, it is the first time

as the application to the MVH problem in Mania & Tevzadze approach.

Remark:

It is instructive to apply the perturbative solution technique of FBSDEs proposed by

Fujii & Takahashi (2012) [3] to (5.2).

One can confirm that the has a quadratic form of and

have a linear form of at an arbitrary order of the perturbative expansion.

This is actually how we have noticed the existence of a quadratic-form solution.

6 as a simple forward expectation of

Since the BSDE for is linear

(6.1)

with , it is clear that we have

(6.2)

Here, the measure is defined by

(6.3)

where

(6.4)

By the result of the previous section, is a linear Gaussian process

and hence the above measure change can be justified, for example, by Lemma 3.9 in [1].

Now, let us evaluate

(6.5)

The argument of has a quadratic Gaussian form and is given by

(6.6)

where and are deterministic

functions defined as

(6.7)

(6.8)

One may notice that the problem is equivalent to the pricing of the zero-coupon bond in

a quadratic Gaussian short rate model, and we in fact borrow the same technique below.

Let us focus on the Kalman-Bucy model. The result for the Bayesian model

can be obtained by the simple parameter replacement as before.

In the measure , the MPR follows

(6.9)

where

(6.10)

and is the -Brownian motion which is related to

by Girsanov’s theorem as

(6.11)

Let us suppose is

given in the following form 666The argument is omitted in for

notational simplicity.:

(6.12)

with deterministic functions taking values in

, .

From (6.6), one sees that the dynamics of is given by

Therefore, one can see that the solution of is given by the form (6.12)

if and only if solve the following ODEs:

(6.15)

(6.16)

(6.17)

with the terminal conditions .

Numerical evaluation can be easily performed in order.

The solutions of the ODEs have the same problem for their existence due to the quadratic term of as in the

case for . For this equation, the non-blow-up conditions

are satisfied once is positive semidefinite (see, [8, 6].),

which is always possible when is sufficiently small. When the condition is not satisfied,

the existence of the solution is dependent on the maturity, in general.

In the remainder, let us suppose that there exists a finite solution for in

for a given parameter set, which can be checked numerically in any case.

If there exists a solution for , we can define a very useful forward measure by

(6.18)

under which standard Brownian motion is given by the relation

(6.19)

by Girsanov’s theorem.

Using this measure, one can now express in a very simple fashion:

(6.20)

Once we obtained and , the optimal capital that achieves the smallest

hedging error at the initial time is given by

(6.21)

7 Monte Carlo Method

In this section, we consider how to evaluate

and by Monte Carlo simulation. Although is not necessary for the

specification of the optimal hedging position by Eq.(4.9), it is needed to obtain the

optimal value function .

For notational simplicity, let us put

(7.1)

(7.2)

then, the relevant dynamics under can be written as

(7.3)

In the forward measure , it becomes

(7.4)

where and are deterministic functions given below:

(7.5)

(7.6)

Similarly, the dynamics of in is given by

(7.7)

with deterministic functions :

(7.8)

(7.9)

In the remainder, we consider a situation where the terminal liability is given

by some function of , i.e.,

(7.10)

7.1 Evaluation of

Of course, the evaluation of

(7.11)

can be performed by simply running under

in standard simulation.

For the evaluation of , we need to introduce the three stochastic flows,

.

They are associated with the sensitivity of the values and at certain

future time against the small changes of their initial values at time .

The first one is defined as, for ,

(7.12)

and is actually given as the solution of the following ODE:

(7.13)

Here, the notation emphasizes that started from the value at time .

The next two quantities are similarly defined as

(7.14)

The three arguments indicate that stated from at time but its future value

also depends on the value of at time .

One can show that they follow the SDEs

(7.15)

(7.16)

with initial conditions and , respectively.

In the above equations, and also in the reminder of the paper, we will often use the so-called Einstein convention which assumes

the summation of the duplicated indexes.

For example, (7.15) should be understood to involve .

Using the above stochastic flows, one obtains

(7.17)

Thus, the simulation of those stochastic flows alongside of the original underlyings

provides us the wanted quantity.

Remark: Calculation of from Delta sensitivity

In the previous formulation, we have introduced the stochastic flows.

This complication is not avoidable in order to make a one-shot Monte Carlo

simulation possible for the evaluation of which will be explained in the next section.

However, if one only needs the hedging position at time (and if the dimension is not too large),

we can take a much simpler approach.

As one can imagine from the definitions of the stochastic flows,

the second line of (7.17) can also be estimated by the usual “Delta”

sensitivity of the terminal liability:

(7.18)

Thus, the required simulations to obtain are only those for the estimations of

the terminal liability and its Delta sensitivities against the underlyings

in measure.

7.2 Evaluation of

Let us define, for and ,

(7.19)

We also put

(7.20)

for a lighter notation. Then, it is easy to confirm that

(7.21)

Note that the Radon-Nikodym derivative between and conditional on is given by

(7.22)

where and are the deterministic functions defined as

(7.23)

(7.24)

Then the inverse relation is given by

(7.25)

Since follows a linear BSDE, it is easy to see that satisfies

(7.26)

Changing the measure to , one can express it as

(7.27)

Unfortunately, the naive evaluation of the above expression requires sequential Monte Carlo

simulations and seems numerically too burdensome to be useful in practice.

However, there is a nice way called a particle method

to compress convoluted expectations.

The method describes a physical system where multiple copies of particles

are created at random interaction times following Poisson law. After the creation,

the particles belonging to a common specie follow the same probability law but are driven by

independent Brownian motions. This idea was introduced by

McKean (1975) [17] to solve a certain type of semilinear PDE

and has been applied to various research areas since then.

For the current problem (7.27), let us introduce a deterministic intensity and

denote the corresponding random interaction time by .

Then, can be represented by

(7.28)

Here, the underlyings (or “particles”) belong to either the group or , and

they follow the SDEs having the same form (7.4), (7.7),

(7.15) and (7.1)

respectively, but driven by two independent -dimensional Brownian motions

and .

This particle representation

allows a one-shot non-sequential Monte Carlo simulation.

See Fujii & Takahashi (2012) [4] for the details of the particle method as a

solution technique for BSDEs, and also

Fujii et.al.(2012) [5] as a concrete application to the pricing of American options.

As long as there exist solutions for and , the explained procedures

allow us to obtain the solutions for the three BSDEs given in Sec. 4 under a quite general setup.

However, it may be tough to update the hedging positions in timely manner in a volatile market,

and in addition, it seems almost impossible

to analyze the terminal distribution of the hedged portfolio,

which may be important for financial firms from a risk-management perspective,

by simulating (4.7) in the current approach.

In the remainder of the paper, we give an explicitly solvable example and then

an asymptotic expansion method to answer this issue.

8 A simple solvable example

In this section, we consider a solvable

case where the terminal liability depends only on a non-tradable index

(8.1)

Let us suppose that where

is a -dimensional constant vector.

Then from (7.4), the index’s dynamics under can be written as

(8.2)

In order to get , it is enough to evaluate

(8.3)

Since it has an affine structure, one can evaluate the above expectation by the same

method used for the evaluation of .

One can show that

(8.4)

can be written by the deterministic functions (, ) and

as

(8.5)

where solve the following ODEs:

(8.6)

(8.7)

with terminal conditions .

Now, from the above arguments, one obtains

(8.8)

A simple application of Itô formula gives

(8.9)

Once we calculate and store all the relevant deterministic functions, it is straightforward to

evaluate from

(8.10)

by standard Monte Carlo simulation.

8.1 A numerical test using the solvable example

Let us provide an interesting numerical example which tests

the consistency of our procedures.

In this solvable example, we can directly run the optimal

wealth process given in .

Thus, it is possible to compare , which is obtained by

the ODEs and a standard Monte Carlo simulation for (8.10),

with directly obtained by running

the simulation for and .

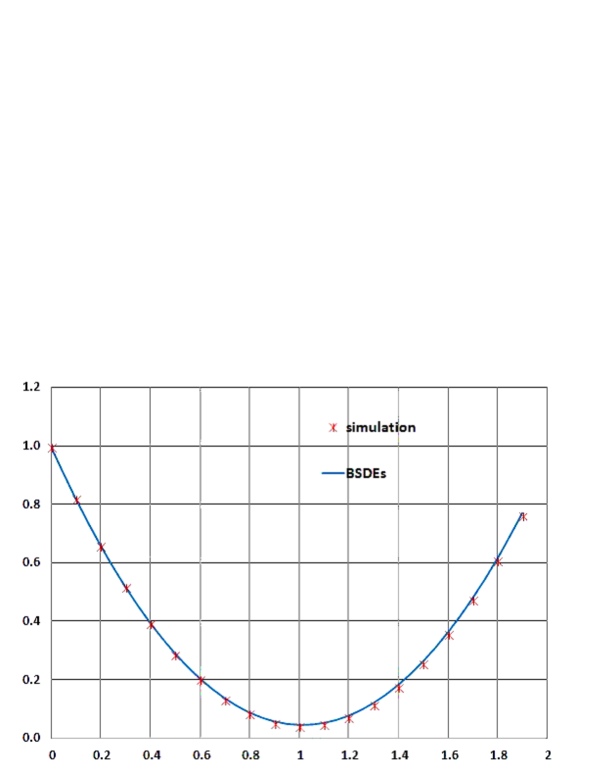

Figure 1: Comparison of and direct simulation of .

The solid line is based on the quadratic form of and marks are those obtained from the

direct simulation of the wealth.

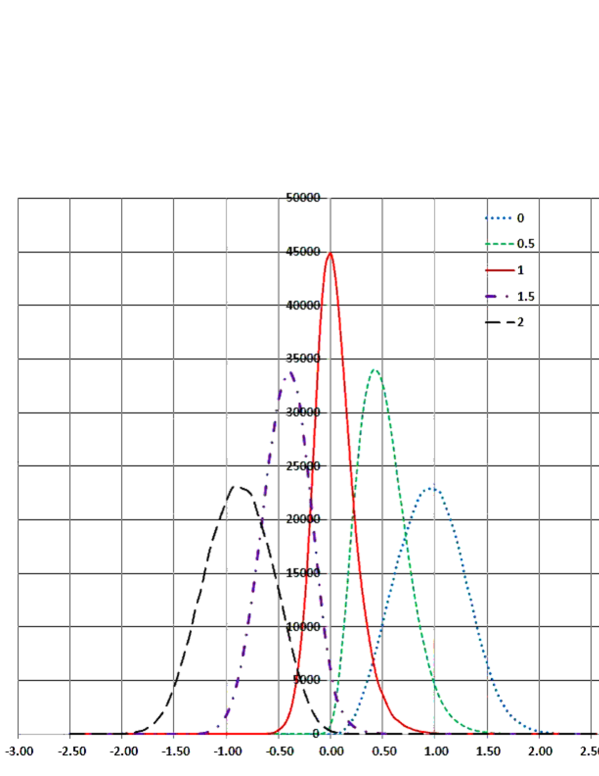

The horizontal axis denotes the size of the initial capital . Figure 2: The terminal distribution of

for the five choices of the initial capital . The graphs are obtained by

connecting the histograms after sampling paths.

Let us use the following parameters with : 777

Here, we put in (3.24). But the choice is free and

what only matters for the dynamics of is .

(8.11)

and

(8.12)

with the initial value .

For , we have obtained by numerically solving ODEs,

and after paths with step size .

The standard error for simulation is about .

In Fig. 1, we have compared the quadratic form of

to the results of direct simulation of hedged portfolio with various initial capitals

with the same number of paths and step size for the evaluation of .

The standard error for the portfolio simulation is less than .

One can see that the prediction of the BSDEs matches very well with the result of the

direct simulation of the hedged portfolio.

One can also study the terminal distribution of the hedged portfolio: .

In Fig. 2, we have plotted the terminal distribution of

for the five choices of the initial capital .

The graphs are obtained by connecting the histograms after sampling scenarios with

the same parameters used to obtain Fig. 1. One can see distributions of the

hedged portfolios change consistently with the result of Fig. 1

and achieves the smallest variance at scenario among the five choices.

9 An asymptotic expansion method

Although it is impossible to obtain a closed-form solution for

(9.1)

in general, its evaluation is clearly equivalent to solving a European contingent claim.

Thus, one can borrow various techniques developed for the pricing of financial derivatives

from the vast existing literatures. Here, we adopt an asymptotic expansion method

to obtain explicit approximate expressions.

See, for example, [22, 21, 23] and references therein for the details of the method.

In those works, the terminal probability distribution of the underlying process is estimated,

which is then applied to a generic payoff function to price an interested contingent claim.

In this article, however, we adopt a slightly simplified approach in which

the asymptotic expansion is directly applied to the terminal payoff by assuming

is a smooth function of . If necessary, we can also apply the original method in [22, 21, 23]

to the current problem, but the resultant formula and required calculation would

be more involved. We also assume the time-homogeneous volatility

structure without explicit dependence on for simplicity.

9.1 Approximation scheme

Firstly, let us introduce an auxiliary parameter and -dependent processes:

(9.2)

(9.3)

where

(9.4)

is a deterministic function 888In theory, there is no need to expand by introducing

since it already has a linear dynamics. However, if one treats exactly,

the calculations associated with become hugely involved due to the presence of in its drift process

most likely with only a minor improvement of accuracy..

The idea behind this setup is to assume

(9.5)

have small enough sizes relative to . Then, the auxiliary parameter is introduced to

count the order of those small quantities appearing in the expansion.

Since contains , the

remaining small term is extracted as in

(9.4).

Suppose, we have expanded the -dependent process as a power series of in the following form:

(9.6)

where

(9.7)

Since the term contains the -th order

products of small quantities in (9.5), the higher order terms in (9.6)

can be naturally neglected for the approximation purpose. Putting at the end of

calculation provides an approximate valuation for the original process .

In the current work, we will provide the formula for up to the third order contribution.

The accuracy of approximation is, of course, determined by the size of the quantities given in

(9.5) 999More precisely speaking, we need to consider the effect of

time-integration together..

As we can see in the numerical examples provided later in the paper,

the scheme seems to work well with realistic parameters,

at least for relatively short maturities.

9.2 Asymptotic expansions of the underlying processes

Let us consider the expansion of for under

the given condition at .

Obviously, we have

(9.8)

(9.9)

with the conventions that and .

Assuming is smooth enough, one can easily derive

(9.10)

(9.11)

(9.12)

(9.13)

with initial conditions for . Similarly, for , one obtains

(9.14)

(9.15)

(9.16)

with for .

9.2.1 Approximation of

Under the assumption that is smooth enough, one can

expand it as

(9.17)

(9.18)

(9.19)

Since is already available as a solution of the ODEs,

one only needs the expectations of and their cross products

to obtain an analytic expression of .

This is actually calculable because all the have linear dynamics

thanks to the way we have introduced in (9.2) and (9.3).

Once this is done,

can be easily derived by the simple application of Itô formula.

Let us put

(9.20)

and a shorthand notation of a time integration, such as

(9.21)

to lighten the expressions. From the application of Itô formula,

we can obtain all the necessary expectations as follows:

(9.22)

Although the expressions are rather lengthy for higher order corrections, there is an

important feature making our method useful. As one can see from the above result,

the stochastic variable are separated from all the necessary time integrations.

Thus, one can carry out the required integrations beforehand and store them in the memory,

which then makes possible to use in the simulation with only the usual

update of underlying state processes . As we shall see next,

this property continues to hold for .

9.2.2 Approximation of

We now try to expand

(9.23)

as

(9.24)

up to the -third order corrections.

Since the expansion for

(9.25)

is already obtained, one only needs a simple application of Itô formula.

Since it increases -order by , we only need up to the 2nd order corrections

of , and also there is no -th order contribution to .

By extracting the coefficients (as row vector) of the -dimensional

Brownian motion from the SDEs of the following conditional expectations,

(9.26)

one obtains

(9.27)

(9.28)

(9.29)

respectively.

Using this result, one can show that the expansion is finally given by

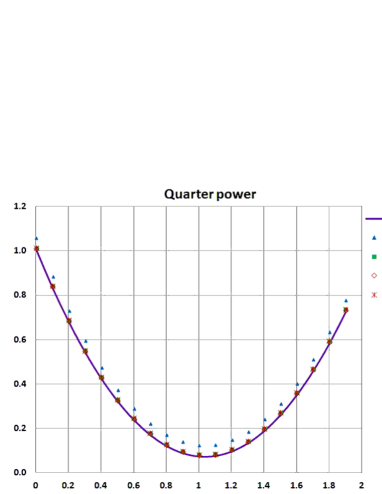

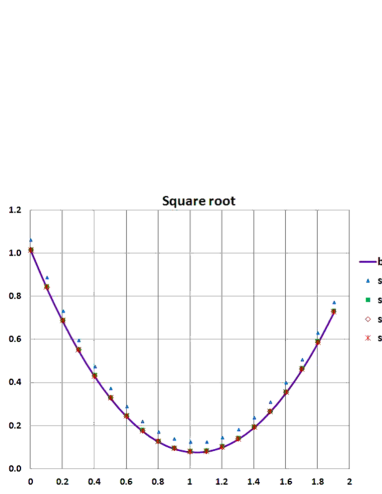

9.3 Numerical Examples

As a simple application of the asymptotic expansion,

let us consider

for its volatility term. Here, is some constant, and

is a constant vector.

In this case, many cross terms vanish in the asymptotic expansion and

one obtains rather simple formulas.

The results of the asymptotic expansion for this model are summarized in Appendix B.

0.87206

0.89560

0.90216

0.90409

0.9052

1.0095

1.0116

1.0088

0.87206

0.89560

0.90224

0.90596

0.9106

1.0142

1.0164

1.0160

Table 1:

The numerical results for for and models.

is calculated based on the asymptotic expansion including all the

contribution up to the -th order. is obtained by running simulation for (8.10) with the corresponding order of approximation for .

Figure 3: Comparison of and direct simulation of with each approximation order of .

The solid line is based on the quadratic form of and the other symbols are those obtained from the

direct simulation of wealth with each approximation order.

The horizontal axis denotes the size of the initial capital .

We have studied and cases for yr maturity.

For the remaining parameters and also are those

we have used in Sec. 8.1.

We have also set for both of the models.

is independent from the model of and we have obtained by

numerically solving the ODEs.

In Table 1, we have listed the numerical results for and .

There, the results of are based on the asymptotic expansion

including all the contribution up to the -th order, and are

calculated by simulating (8.10) with

the corresponding order of approximation for .

The number of simulation paths and step size are the same as those used in Sec. 8.1.

The standard error of simulation is around for both of the models.

In Fig. 3, we have done the same consistency test as in Sec. 8.1,

where we have compared the quadratic form of and direct simulation of .

The solid line corresponds to the prediction of using the 3rd order approximation,

and the other symbols denote the results of direct simulation of

using each order of approximation of .

One can confirm the consistency of our approximation and also

that even the 1st order approximation realizes the most part of

the hedging benefit of the variance reduction.

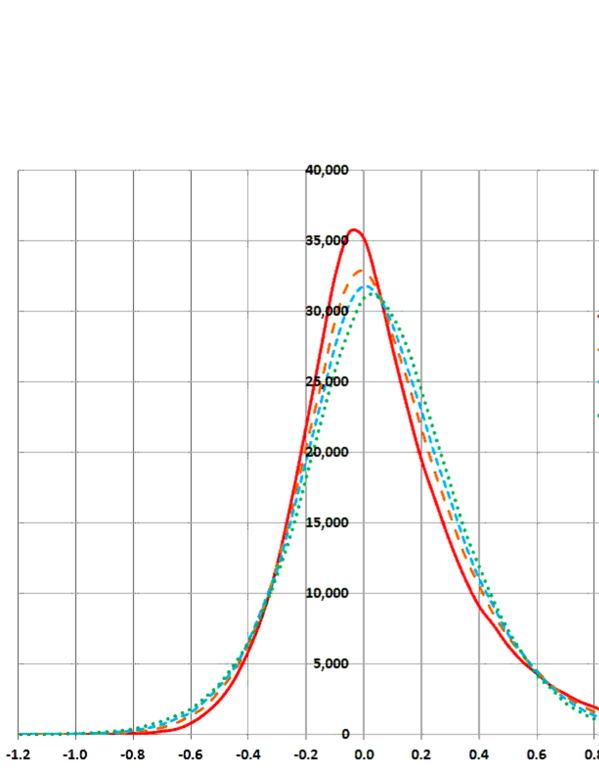

Figure 4: The comparison of the terminal distribution with the initial capital

using the third order asymptotic expansion. The graphs are obtained by connecting the histograms

after sampling paths.

It might be surprising that these results are very close between the two choices of ,

but in fact, this result is naturally expected.

Actually, one can easily confirm that should have exactly the same

value with arbitrary in the current setup. Furthermore, the common and the initial value of

indicate that every model with has almost the same variance for relatively short maturities,

which naturally leads to the similar variance for the hedging error.

However, as can be seen from Fig. 4, there appears a difference in

the distribution of the hedged portfolio. There, we have compared

the terminal distribution with the initial capital

for four models of .

The graphs of distribution were obtained by connecting the histogram after sampling 400,000

paths. These difference may become important for financial firms from a risk-management perspective.

10 An extension to stochastic interest rates

10.1 Interest-Rate Futures

Before concluding the paper, we discuss how to handle the situation with

stochastic interest rates.

Although the effect of discounting is not relevant unless we work on very long term

contracts, the sensitivity of the terminal liability against the change of the forward

curve of interest rate indexes, such as LIBORs, can be quite

significant 101010Note that, in the collateralized era after the Lehman default,

LIBORs are not directly related to the discounting rate of the contract.

For cash-collateralized contracts, the corresponding overnight rate is typically

used as the collateral rate and hence as the discounting rate..

For this point, we emphasize that our method can be directly applied to

a futures market, such as Eurodollar futures provided by CME Group in the following way:

Let us introduce the -dimensional “base” futures prices

as

(10.1)

under . Here, and

are assumed to satisfy the same conditions defined in Section 2.

Using the base futures prices, we assume that the dynamics of the “true” futures prices

is given by

(10.2)

Here, denote the set of maturities of the futures contracts.

We consider as the number of tradable futures at the exchange at any point of time , whose

underlying’s maturities are the smallest of larger than .

It is easy to check that, at any point of time , are

observable, and hence it is possible to adopt the linear filtering scheme in the same way

as we did for the equity market.

One should notice that the Brownian motions and the corresponding MPRs are not

associated with contracts with fixed maturities but rather with the first rolling contracts.

This setup seems natural since the investor’s perception of risk is typically associated with the

time-to-maturity rather than a specific timing of the maturity.

The dynamics of the wealth by taking a position on the tradable set of can be

equally written by that of the first rolling set of contracts, :

(10.3)

Note here that there is no outright cash required to enter and/or exit a futures contract.

From the expression (10.2), the position on the tradable futures

can be directly read from that on at arbitrary point of time.

Neglecting the discounting effect,

it is now clear that one can handle the futures and equity markets completely in

parallel.

10.2 Stochastic Short Rate

Lastly, we would like to mention the fact that introducing a simple stochastic short-rate

process is not difficult as long as it is perfectly observable.

Suppose for example, the money-market account on is tradable in addition to the

stocks.

In this case, the wealth-dynamics is given by

(10.4)

with the modified dynamics of

(10.5)

under .

Using the above wealth dynamics, the Itô-Ventzell formula yields

(10.6)

(10.7)

where the BSDE for is unchanged.

Thus, it only induces additional linear terms to the drivers of and , respectively.

If the short rate process itself is Gaussian, then one can

apply the same technique based on the new state processes .

In the case of a quadratic Gaussian model where

(10.8)

with some deterministic functions

and -dimensional perfectly observable Gaussian process , one can use

instead.

For these models, adding zero coupon bonds as tradable risky assets is also straightforward.

Although it is unrealistic to assume that the short rate is perfectly observable,

it is still very tightly controlled by the central bank in most of the developed countries.

As long as we work in a relatively short time-horizon, fixing its drift term

based on the forward guidance provided by the central bank 111111One must assume that the guidance is provided

in the physical measure., and allocating all the remaining small daily changes to the

Brownian motion would be a reasonable approximation.

11 Conclusions

In this article, we have studied the mean-variance hedging (MVH) problem in a partially observable market

by studying a set of three BSDEs derived by Mania & Tevzadze [13].

Under the Bayesian and Kalman-Bucy frameworks,

we have found that one of these BSDEs yields a semi-closed solution

via a simple set of ODEs which allow a quick numerical evaluation.

We have proposed a Monte Carlo scheme using a particle method

to solve the remaining two BSDEs without nested simulations.

As far as the optimal hedging positions are concerned, it is also pointed out that

one only needs the standard simulations for the terminal liability and its

Delta sensitivities against the state processes under a new measure

.

We gave a special example where the hedging position is available in a semi-closed form

and presented an interesting consistency test by directly simulating the optimal

portfolio.

For more general situations, we have provided explicit expressions of the approximate

hedging portfolio by an asymptotic expansion method and demonstrated the procedures

by several numerical examples.

It would be interesting future works to apply the obtained asymptotic expansion formula to

more involved situations where the payoff function is non-linear or dependent on

both and .

Although the simplifying assumptions on the MPR dynamics in are

very restrictive, generalization to a non-linear dynamics remains as a very challenging

issue of the non-linear filtering problem with infinite degrees of freedom.

It may be worth considering to use a similar asymptotic expansion technique (see, for example,

Fujii (2013) [2].) for this problem.

If the MPR process is perfectly observable, then, in principle, we can take its non-linear effects

into account perturbatively by the method proposed in [3].

Appendix A Derivation of BSDEs

In this section, for interested readers, we briefly explain the main ideas of Mania & Tevzadze leading to the system of BSDEs.

Since defined by (4.2) given the initial capital at

is a -adapted semimartingale in general,

using the “representation theorem” (see, Lemma 4.1 of [19]),

one can decompose it as

(A.1)

with an appropriate -adapted triple .

Then, recalling

and assuming appropriate conditions for the use of Itô-Ventzell formula [11],

one obtains

(A.2)

Here, we have written as for simplicity.

It is easy to see should be a -martingale for the optimal strategy

(and submartingale otherwise). Then, one obtains

(A.3)

as a drift condition.

Assuming the which makes the first term zero is admissible and hence corresponding to , one obtains

(A.4)

Substituting the above result into (A.1) yields a BSPDE

(A.5)

The optimal wealth dynamics can also be read as

(A.6)

Since is given by the orthogonal projection of

on the closed subspace of stochastic integrals,

the optimal strategy is linear with

respect to the initial capital .

Thus, one may suppose the following decomposition holds.

(See Theorem 1.4 of [7] and Theorem 4.1 of [13] for the detail.)

(A.7)

where do not depend on .

This decomposition needs to hold for arbitrary .

Then, inserting back to (A.5) leads to the

desired set of BSDEs. Economic meanings of are explained in [13].

Appendix B Asymptotic expansion formulas for the model in Sec. 9.3

Firstly, let us put

(B.1)

with the convention that

(B.2)

From the results in Sec. 9.2.1 and 9.2.2,

one obtains

(B.3)

Using the above results, one can show can be expanded as

(B.4)

It is also straightforward to obtain

(B.5)

with the definitions of

Acknowledgement

This research is partially supported by Center for Advanced Research in Finance (CARF).

References

[1]

Bain, A., Crisan, D., 2008. Fundamentals of Stochastic Filtering. New York.

Springer.

[2]

Fujii, M., 2013, “Momentum-space approach to asymptotic expansion for stochastic filtering,”

forthcoming in Annals of the Institute of Statistical Mathematics.

[3]

Fujii, M. and Takahashi, A., 2012, “Analytical approximation for non-linear FBSDEs with

perturbation scheme,” International Journal of Theoretical and Applied Finance, Vol. 15, No. 5,

1250034 (24).

[4]

Fujii, M. and Takahashi, A., 2012, gPerturbative Expansion Technique for Non-Linear FBSDEs with Interacting Particle Method, h CARF working paper series, CARF-F-278.

Available at SSRN: http://ssrn.com/abstract=1999137 .

[5]

Fujii, M., Sato, S. and Takahashi, A., 2012, “An FBSDE Approach to American Option Pricing with an Interacting

Particle Method,” CARF working paper series, CARF-F-302.

Available at SSRN: http://ssrn.com/abstract=2180696 .

[6]

Jacobson, D.H., 1970, “New conditions for boundedness of the solution of a matrix Riccati differential

equation,” Journal of Differential Equations 8, 258-263.

[7]

Jeanblanc, M., Mania, M., Santacroce, M.,

and Schweizer, M., 2012, “Mean-variance hedging via stochastic control and BSDEs for general

semimartingales,” The Annals of Applied Probability, Vol. 22, No. 6,

2388-2428.

[8]

Kalman, R.E., 1960, “Contributions on the Theory of Optimal Control,” Bol. Soc. Mat.

Mexicana, Vol. 5, 102-119.

[9]

Kobylanski, M., 2000, “Backward stochastic differential equations and partial differential equations

with quadratic growth,” The Annals of Probability, 28, 558-602.

[10]

Kohlmann, M. and Tang, S., 2002, “Global adapted solution of one-dimensional

backward stochastic Riccati equations, with application to the

mean-variance hedging,” Stochastic Processes and their Applications 97, 255-288.

[11]

Kunita, H., 1990, “Stochastic flows and stochastic differential equations,”

Cambridge studies in advanced mathematics 24, Cambridge University Press, UK.

[12]

Laurent, J. P. and Pham, H., 1999,

”Dynamic programming and mean-variance hedging,” Finance Stochastics, 3, 83-110.

[13]

Mania, M. and Tevzadze, R., 2003,“Backward Stochastic PDE and

Imperfect Hedging,” International Journal of Theoretical and

Applied Finance Vol. 6, No. 7 663-692.

[14]

Mania, M., and Tevzadze, R., 2008,“Backward Stochastic PDEs related to the Utility Maximization Problem,”

arXiv:0806.0240.

[15]

Mania, M., Tevzadze, R. and Toronjadze, T.,

2008,“Mean-Variance Hedging under Partial Information,”

SIAM J. Control Optim., Vol.47, No. 5, pp. 2381-2409.

[16]

Mania, M. and Santacroce, M., 2010,“Exponential utility maximization

under partial information,” Finance and Stochastics, 14: 419-448.

[17]

McKean, H., P., 1975, “Application of Brownian Motion to the Equation of Kolmogorov-

Petrovskii-Piskunov, h Communications on Pure and Applied Mathematics, Vol.

XXVIII, 323-331.

[18]

Pham, H. , 2001, “Mean-variance hedging for partially observed drift

processes,” International Journal of Theoretical and Applied Finance,

Vol.4, No. 2, 263-284.

[19]

Pham, H. and Quenez, M. C. 2001,

“Optimal Portfolio in Partially Observed Stochastic Volatility Models,”

The annals of applied probability, Vol. 11, No. 1, 210-238.

[20]

Schroder, M. and Skiadas, C., 1999, “Optimal Consumption and Portfolio Selection

with Stochastic Differential Utility,” Journal of Economic Theory 89, 68-126.

[21]

Kunitomo, N. and Takahashi, A. (2003).

”On Validity of the Asymptotic Expansion Approach

in Contingent Claim Analysis,”

Annals of Applied Probability, 13, No.3, 914-952.

[22]

Takahashi, A., (1999). An Asymptotic Expansion Approach to Pricing Contingent Claims. Asia-Pacific Financial

Markets, Vol. 6, 115-151.

[23]

Takahashi, A., Takehara, K. and Toda, M., 2012, “A General Computation Scheme for a High-Order Asymptotic Expansion Method”

International Journal of Theoretical and Applied Finance Vol. 15, No. 6, 1250044 (25).