Copula-type Estimators for Flexible Multivariate Density Modeling using Mixtures

Abstract

Copulas are popular as models for multivariate dependence because they allow the marginal densities and the joint dependence to be modeled separately. However, they usually require that the transformation from uniform marginals to the marginals of the joint dependence structure is known. This can only be done for a restricted set of copulas, e.g. a normal copula. Our article introduces copula-type estimators for flexible multivariate density estimation which also allow the marginal densities to be modeled separately from the joint dependence, as in copula modeling, but overcomes the lack of flexibility of most popular copula estimators. An iterative scheme is proposed for estimating copula-type estimators and its usefulness is demonstrated through simulation and real examples. The joint dependence is is modeled by mixture of normals and mixture of normals factor analyzers models, and mixture of and mixture of factor analyzers models. We develop efficient Variational Bayes algorithms for fitting these in which model selection is performed automatically. Based on these mixture models, we construct four classes of copula-type densities which are far more flexible than current popular copula densities, and outperform them in simulation and several real data sets.

Keywords. Mixtures of factor analyzers; Mixtures of normals; Mixtures of ; Mixtures of -factor analyzers; Variational Bayes.

1 Introduction

Multivariate density estimation is a fundamental problem in statistics and related fields. One of the common approaches to multivariate density estimation is mixture modeling, which estimates the multivariate density of interest by a multivariate mixture of densities such as a multivariate mixture of normal densities or a multivariate mixture of densities (Titterington et al.,, 1985; McLachlan and Peel,, 2000). Mixture models provide an automatic method for estimating the density of non-standard and high-dimensional data. In principle, with sufficient data relative to the dimension of the multivariate data, a mixture model can fit a data set arbitrarily well and capture most of its features. In practice, however, transforming the marginals can greatly facilitate obtaining statistically efficient estimates of a target multivariate density. This can be done informally by taking known transformations of the marginals, for example by taking logs, or more formally, as we have done, by estimating the marginals flexibly and then transforming.

A drawback in using mixture models is that we do not have much flexibility in modeling the marginals, because all of the implied marginals are restricted to some particular form. For example, if the multivariate density of interest is estimated by a multivariate mixture of normals then the marginals of the target are estimated by the implied univariate mixture of normals. These implied marginals may not even be close to the best models for the target marginals, which can be a kernel density, a univariate mixture of or some parametric form. Furthermore, Giordani et al., (2012) observe that implicit estimation of marginals is in some cases less efficient than direct estimation, even when the true model is used to fit the joint distribution. They conjecture that the large number of parameters in the joint model that need to be estimated makes the estimation practically less efficient, while direct estimation of the marginals does not deteriorate with the dimension.

Copula modeling is a widely used approach to multivariate density estimation (Joe,, 1997; Nelsen,, 1999). This approach is flexible in the sense that it allows one to model the marginals and the joint dependence separately. Because of computational reasons, the joint dependence is often estimated by a mathematically convenient model such as a multivariate normal or a multivariate distribution. Such conveniently parametric copula models may not be appropriate for modeling data sets that have a complex joint dependence structure. For example, different areas in the domain of the data may have different dependence structures (see the motivating example in Section 2 and the Iris data in Section 3). In such cases, a multivariate mixture model will capture the joint dependence of the data better than a simple model such as a normal or a model. It is therefore desirable to use flexible models such as multivariate mixture models to estimate the joint dependence.

This article proposes a new class of multivariate density estimators called copula-type estimators which have the motivation of using flexible models for estimating complex joint dependence structure, while preserving the possibility offered by copulas of modeling the marginal distributions separately. Except in some special cases, copula-type estimators are not copula estimators, although they still allow the marginals to be separately estimated. The construction of copula-type estimators allows us to estimate them using an iterative scheme. The construction also covers many popular copula estimators found in the literature. The article focuses on a class of copula-type estimators using multivariate mixture models to capture the joint dependence of the target density. In particular, four copula-type estimators are considered: a copula-type estimator based on a multivariate mixture of normals, a copula-type estimator based on a multivariate mixture of , a copula-type estimator based on a mixture of factor analyzers and a copula-type estimator based on a mixture of -factor analyzers. These four copula-type estimators allow us to achieve flexibility, efficiency and robustness in multivariate density estimation. Their estimation is based on efficient Variational Bayes algorithms for fitting mixture models, in which model selection (and factor selection) is automatically incorporated. See, e.g., Ormerod and Wand, (2009) for an introduction to the Variational Bayes method. We believe that our algorithm for fitting mixtures of mixtures of and -factor analyzers is the first method in the literature which is able to do parameter estimation and component and factor selection simultaneously and automatically.

2 The copula-type model

2.1 Copula modeling

Suppose that we are given a data set of realizations of a random vector , and we wish to estimate the distribution of . We will denote random variables by upper-case letters, their realizations by lower-case letters, and write vector variables in bold. We write for a general multivariate argument and for a particular realization. We restrict the discussion in this paper to continuous marginals.

In copula modeling, one often assumes that inherits the joint dependence structure from another continuous random vector . Let be the joint cumulative distribution function (cdf) of and , , be its marginal cdf’s. Write the corresponding probability density functions (pdf’s) as and . The joint dependence of is assumed to be constructed from as follows. First, let , . Each has a uniform distribution on while their joint dependence is induced from that of , i.e. the cdf of can be written as

| (1) |

This function is referred to as a copula function or a copula (induced by ). This way of constructing a copula is known as the inverse method (Nelsen,, 1999).

Given univariate (continuous) cdf’s , let , . Then each random variable admits as its cdf while their joint dependence is induced from that of the vector , i.e. the cdf of can be expressed in terms of as

| (2) |

We refer to (or its pdf ) as a copula cdf, which can be though of as an approximation to the true cdf of . It is easy to see that the th marginal cdf of is . Figure 1 demonstrates this and relationship diagrammatically. The three random vectors , and have different marginals but the same joint dependence structure in the sense that their cdf’s can be written in terms of the copula .

Two examples of popular copulas are the normal and copulas. In the normal copula is assumed to be the cdf of a multivariate normal distribution , with is assumed to be the cdf of a multivariate distribution with the degrees of freedom and is a scale matrix with diagonal entries 1. For both the normal and copulas the scale matrix is a correlation matrix.

Inference in copula modeling consists of two problems. The first is how to estimate the marginal cdf’s and the second is how to select and estimate an appropriate copula , or equivalently . This section focuses on the second problem, i.e. on estimating an appropriate joint dependence structure. We assume for now that the marginal cdf’s are known; marginal estimation is discussed in Section 2.5. By making the transformation , , , we obtain a data set in the -space and the problem reduces to reconstructing the source of dependence structure in based on . It is worth emphasizing that the data contain all information we have about the joint dependence of (or ).

The main problem with many current approaches for fitting joint dependence using copulas is that if an inappropriate choice of copula is made, then the transformed data in the -space may be harder to model than the original data . The following discussion and example consider this issue. Suppose that we wish to estimate the joint dependence in by a multivariate cdf , where is assumed known up to some parameters that need to be estimated from the data. For example, may be a multivariate normal cdf whose mean is and whose covariance matrix is a correlation matrix that needs to be estimated from the data. We further assume that the marginal cdf’s of are fully known. This is the case, for example, in the normal copula or the copula with fixed degrees of freedom. Then a simple method for estimating is as follows: first, transform the data to a data set in the -space via , , ; then, fit to . For example, in fitting a normal copula we first make the transformation with the standard normal cdf and then fit a multivariate normal distribution (with a correlation matrix) to this -space data set. The idea (hope) is that the transformed data are easier to model than . However, in some cases cannot be fitted well by . The main problem with copulas is that with an inappropriate choice of , the transformed data may be harder to model than the original data . This is illustrated in the example below.

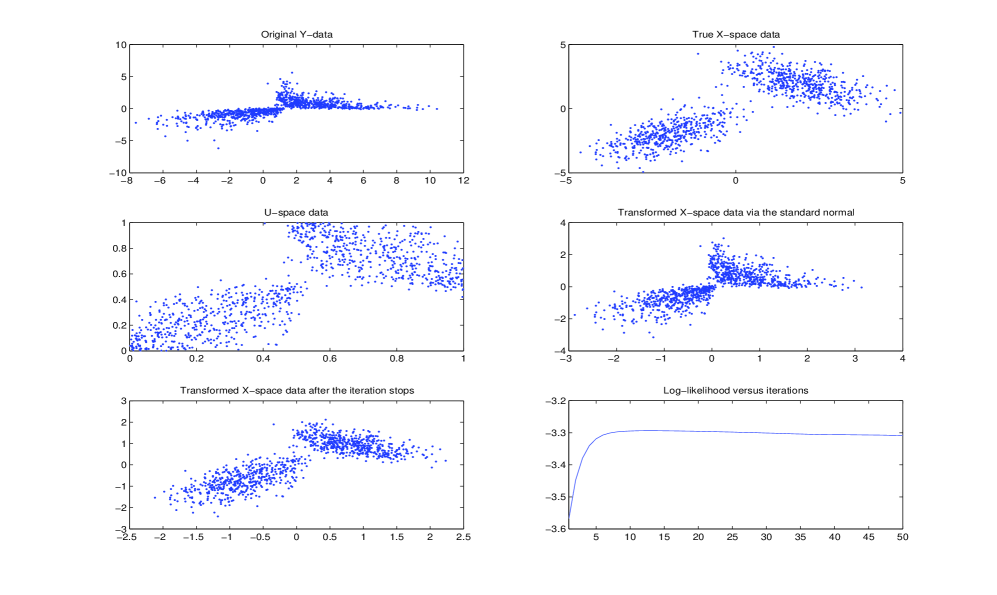

A motivating example. We construct a two-dimensional vector whose joint dependence is induced from another vector as in Figure 1. is distributed as a multivariate mixture of two normals with density

| (3) |

where

and and .

The panels in the first row of Figure 2 show 1000 realizations from the vectors and respectively. The left panel of the middle row plots the data obtained via , which contain all information about the joint dependence of (and ). If we use a normal copula to model the dependence structure in , we need to fit a bivariate normal distribution to the data shown in the right panel of the middle row, which are obtained via . Clearly a multivariate normal density does not provide a good fit to this data set and it is necessary to have a more flexible model than a multivariate normal distribution to capture the joint dependence.

The example above motivates the use of flexible models to estimate the joint dependence. Suppose that belongs to some class of multivariate cdf’s, such as the cdf’s of multivariate mixtures of normals, with unknown parameter vector . From (2), the pdf of is

| (4) |

where . It is possible, in principle, to estimate by maximum likelihood or by its posterior mode based on the pdf (4). However, when is a complex cdf such as a mixture cdf, optimization over is computationally very difficult, for two reasons. First, we cannot in general compute the gradient of the likelihood analytically because the pdf (4) has deeply embedded in the inverse transformations . Second, this is a high-dimensional optimization problem with the complex constraints that the scale correlation matrices in the mixture need to be positive definite. For example, suppose that is the cdf of a mixture of normals; then the dimension of is , which can be thousands for even a moderate ; here, we have components, probability parameters, mean parameters and correlation parameters. We note that we tried black box optimization in Matlab for a two dimensional () problems, but the optimization algorithm repeatedly failed to converge.

In the next section we propose a class of copula-type (CT) estimators which estimate the marginals from as well as flexibly estimating the dependence structure.

2.2 Copula-type estimators

We now describe a framework for constructing flexible multivariate density estimators, which allows using complex and flexible models for estimating the joint dependence structure. Note that we are assuming that the marginal cdf’s are given or separately estimated, so that we start with the transformed data and wish to capture the joint dependence of .

Our estimator for the distribution of interest is constructed as follows. Suppose that univariate cdf’s are an initial guess of the marginal cdf’s , . Recall that is the cdf of and are its marginal cdf’s, is unknown and we wish to estimate . Let be the data set in the -space obtained by transforming . Now fit a multivariate cdf to . For example, can be the cdf of an univariate mixture of normals and the cdf of a multivariate mixture of normals. Let

| (5) |

We note that is selected from the class of cdf’s corresponding to mixture of normals, mixture of factor analyzers, mixtures of and mixture of analyzers. That is, is specified up to class, e.g. mixture of normals, with the parameters, number of components and number of factors unknown and to be estimated form the data.

The following result provides an explicit expression for the estimator.

Proposition 1.

The cdf of the estimator for the distribution of is

| (6) |

The pdf of the estimator is

| (7) |

its th marginal pdf is

with and , , , density functions with respect to , , , respectively.

We note that equation (5) is not necessarily a copula. It is also important to note that in (7) is a valid multivariate density for any , and . To see this, using the equality that , we can prove that . This justifies the stopping criterion used in the iterative scheme in Section 2.3.

The following result guarantees that under some conditions the marginals of the estimator converge to the true marginals . We say that a fitting method is reliable if the resulting estimator converges in total variation norm to the underlying density that generates the data , i.e.

as the sample size increases.

Proposition 2 (Marginal consistency).

Suppose that the method for fitting to is reliable. Then converges in total variation to the true marginal , , as the sample size increases.

The proofs of the two propositions are in Appendix A.

We call the function in (5) a copula-type function, and refer to (6) or (7) as a copula-type estimator. This is because has a similar form as the copula function in (1), and under some conditions (see below) a copula-type function becomes a copula function.

This approach to multivariate density estimation is flexible for the following reasons.

-

•

It allows us to use complex and principled models such as multivariate mixture models to estimate the joint dependence.

-

•

With appropriate choices of the and , the framework covers some popular copulas in the literature. For example, with , and a correlation matrix we obtain the normal copula model; with , and a scale matrix with diagonal entries 1 we obtain the copula model. Note that in these two cases, , . More generally, a copula-type function is a copula function if admits ’s as its marginal cdf’s.

-

•

If , then is fit directly to the original data, i.e. no marginal adaptation is used. Then copula-type modeling reduces to the usual multivariate modeling, such as multivariate mixture modeling.

We note that unless , copula-type estimators are not true copula estimators because the marginal pdf’s of a copula-type estimator are not exactly the separately estimated marginal pdf’s . In order for a copula-type estimator to be a copula estimator it is necessary to impose the constraint . However, imposing this constraint usually makes the estimation of very difficult, especially when complex models are used to estimate the joint dependence. Furthermore, this constraint need not lead to better performance; see the remarks at the end of Section 2.3. Finally, Proposition 2 guarantees that in large samples a copula-type estimator converges to an exact copula estimator if the model for is sufficiently flexible.

2.3 Iterative scheme

In general, we should choose the univariate cdf such that the transformed data look as if they can be effectively fitted by the candidate set of multivariate distributions . In our case, this means that the transformed data can be parsimoniously fitted by a multivariate mixture of normals or a multivariate mixture of . This is difficult if the are only chosen once. We propose an iterative scheme which is useful for estimating the and in general. Assume that belongs to some family of multivariate cdf’s such as multivariate normal mixture cdf’s: with the parameters. We start with some initial univariate cdf’s , fit to to get an estimate of and then repeat the procedure with set to .

-

1.

Start with some initial univariate cdf’s .

-

2.

Transform the data to via , , .

-

3.

Fit to to get an estimate of .

-

4.

Set with the th marginal cdf of . Go back to Step 2.

We suggest stopping the iteration if the log-likelihood

does not improve any further. The iteration uses Variational Bayes at each iteration to choose the parameters, as well as choosing automatically the number of components and number of factors. Note that is a valid density. We observe that the log-likelihood often increases in the first few iterations and then decreases; see the last panel in Figure 2. A possible choice for the initial marginal distributions is the standard normal cdf . When is the cdf of a multivariate mixture of normals or a multivariate mixture of , we suggest selecting the as the implied marginals of the multivariate mixture distribution estimated from the original data . We found that the resulting estimates are insensitive to the initial distribution taken and show the usefulness of this scheme through numerical examples.

A motivating example (continued). We now apply the iterative scheme to estimate the joint dependence in with and a multivariate mixture of two normals. The procedure stops after 13 iterations when the log-likelihood is maximized. The bottom right panel in Figure 2 plots the log-likelihood values vs iterations number. The bottom left panel shows the transformed data after the iterative scheme stops. Clearly, the joint dependence structure of this estimated is similar to that of the true distribution . In fact, the two component correlation matrices of are and , which are close to the true matrices and .

Remark 1. A different, but related, estimator constructed within our framework is

| (8) |

with obtained after the iteration above has terminated, i.e. we use the copula induced by to construct the estimator. The estimator (8) is a copula estimator as its marginals are equal to . However, our experiments show that the copula-type estimator (7) usually has a slightly better performance in terms of the log predictive density score (see Section 3) than the copula estimator (8). We conjecture that this is because the expression (7) takes into account the actual marginal transformations of the data , while (8) uses only the estimated joint dependence.

Remark 2. The proposed method can be easily extended to the case where the marginals depend on covariates . Assume that are observations from a multivariate distribution , whose joint dependence is independent of . Let , , , where is the th marginal cdf. We can now use the iterative scheme to estimate the and . The pdf of the estimator is expressed as

with . Extension to the case where the distribution functions and depend on covariates is more difficult and is left for future research.

2.4 Copula-type estimators based on mixtures

This paper considers in particular four copula-type distributions using multivariate mixture models to estimate the joint dependence.

The first copula-type estimator uses a multivariate mixture of normals to model the joint dependence and is denoted by CT-MN. See, e.g., Titterington et al., (1985) and McLachlan and Peel, (2000) for an introduction to mixture models.

A mixture of normals model may be over-parameterized when modeling high-dimensional data as the number of model parameters increases at least quadratically with the dimension. This is because the number of parameters in each component increases quadratically and the number of components is also likely to increase with dimension. Parameter estimation is typically less efficient statistically if the number of observations is small relative to the number of parameters. In such cases, it is desirable to reduce the number of parameters. The mixture of factor analyzers model introduced in Ghahramani and Hinton, (1997) provides an effective way to parsimoniously model high-dimensional data, and inherits the advantages of flexibility from mixture modeling and dimensionality reduction from the factor representation. The second copula-type estimator is based on a mixture of factor analyzers and is denoted by CT-MFA.

Krupskii and Joe, (2013) propose a general one component factor copula model which they propose to estimate by maximum likelihood. However, they do not address the two main issues in our article, i.e. the estimation of a copula of a mixture and how to make the marginals in that copula consistent with the joint distribution.

The third copula-type estimator uses a multivariate mixture of to model the joint dependence and is denoted as CT-M. The heavy tails of distributions can make this estimator successful when modeling data with outliers or atypical observations. See, e.g., Peel and McLachlan, (2000) for a discussion of the multivariate mixture of model. The fourth copula-type uses a mixture of -factor analyzers to estimate the joint dependence, and we denote it by CT-MFA.

We note that our component and factor selection approach will indicate if a simpler normal or t copula or a factor version of these models is sufficient to fit the data. We can also use cross-validation log predictive score (LPDS – see the definition in Section 3) to make a similar assessment.

Appendix B presents more details on mixture modeling and how to fit a mixture model to the data using Variational Bayes methods.

2.5 Estimation of marginals

Estimating the marginal densities of is typically much easier than estimating the joint dependence structure. There are a number of efficient approaches for estimating a univariate density, for example parametric estimation, kernel density estimation and univariate mixture estimation. Given a class of univariate density estimators, the best estimator can be selected using cross validation LPDS (see Section 3). In the examples below, we consider for the class a kernel density estimator, a univariate mixture of normals estimator, a univariate mixture of estimator, an implied univariate mixture of normals estimator (i.e. the univariate density estimator for the marginal implied from the multivariate mixture of normals for the joint) and an implied univariate mixture of estimator. When fitting univariate mixtures to the marginals, the number of components is selected by Variational Bayes for the real examples. For the simulated example, we used the true model that generated the data as the best model for the marginals because we wished to focus on how well the joint density was being estimated.

3 Examples

A common measure for the performance of a density estimator is the log predictive density score (LPDS) (see, e.g., Good,, 1952; Geisser,, 1980). Let be a test data set that is independent of the training set . Suppose that is a density estimator based on . The LPDS of the estimator is defined by

with the number of observations in . The smaller the LPDS the better the estimator.

For the real examples considered in this section we use the cross-validated LPDS. Suppose that the data set is split into roughly equal parts , the -fold cross-validated LPDS is defined as

When computing this cross-validated LPDS, the marginal models are fixed at the best models which have been already selected (again, by cross-validated LPDS for each marginal). That is, the models for the marginals and the copula model for the joint are specified up to class with the parameters (including the number of components and number of factors) estimated from each data set . We take or as recommended by Hastie et al., (2009), pp. 241-244.

Giordani et al., (2012) propose a class of multivariate density estimators to improve on standard multivariate estimators. They do so by allowing the user to adjust any initial multivariate estimator by the best fitting density for each marginal. Giordani et al., (2012) introduce two marginally adjusted estimators using the mixture of normals and mixture of factor analyzers models for the initial estimators. These estimators are denoted by MAMN and MAMFA. A total of 12 estimators are considered below for comparison. The first six are mixture-based estimators including a multivariate mixture of normals (MN), a multivariate mixture of (M), a mixture of factor analyzers (MFA), a mixture of -factor analyzers (MFA), and two marginally adjusted estimators, MAMN and MAMFA. The others are copula-based estimators including a normal copula (NC), a copula (C), CT-MN, CT-M, CT-MFA and CT-MFA.

3.1 Simulated Example

We consider the data generating process as in the motivating example in Section 2. Given a dimension , a training data set of size is generated from (3), where and are vectors of size , , with and , and for all . A test data set of 1000 realizations is then generated in the same manner to compute the log predictive density scores. For each and combination, we compute the 12 density estimators based on , their LPDS based on , CPU times, and replicate this computation for 50 replications. Tables 1 and 2 summarize the LPDS and CPU times averaged over the replications for various and .

We draw the following conclusions. 1) The copula-type estimators perform best, except for the CT-M when and . We conjecture that estimating the CT-M in the large- small- case is challenging because of a very large number of parameters that need to be estimated. We observe that the CT-M works well when is large enough. 2) Dimension reduction via the factor analyzers models is useful when is large. 3) The marginally adjusted estimators, MAMN and MAMFA, always outperform their initial estimators, MN and MFA. 4) The normal and copulas work poorly. This is not surprising as the joint dependence of the data has a mixture structure. 5) The copula-type estimators are more time consuming than the others, principally because in the variational Bayes algorithms, components (and factor) selection takes place every iteration. The code is written in Matlab and run on an Intel Core 16 i7 3.2GHz desktop.

| MN | M | MFA | MFA | MAMN | MAMFA | NC | C | CT-MN | CT-M | CT-MFA | CT-MFA | ||

| 5 | 200 | 5.01 | 4.96 | 5.17 | 4.97 | 4.94 | 5.15 | 5.62 | 5.62 | 4.45 | 4.33 | 4.66 | 4.34 |

| (0.07) | (0.06) | (0.06) | (0.04) | (0.08) | (0.06) | (0.04) | (0.04) | (0.09) | (0.08) | (0.09) | (0.08) | ||

| 500 | 4.84 | 4.80 | 5.05 | 4.85 | 4.78 | 5.03 | 5.53 | 5.53 | 4.19 | 4.15 | 4.35 | 4.19 | |

| (0.06) | (0.06) | (0.06) | (0.06) | (0.05) | (0.05) | (0.07) | (0.07) | (0.08) | (0.06) | (0.16) | (0.07) | ||

| 10 | 200 | 9.27 | 9.31 | 9.36 | 9.09 | 9.11 | 9.26 | 10.47 | 10.47 | 8.03 | 8.09 | 8.14 | 7.90 |

| (0.16) | (0.12) | (0.19) | (0.13) | (0.15) | (0.24) | (0.15) | (0.15) | (0.16) | (0.19) | (0.46) | (0.18) | ||

| 500 | 8.85 | 8.80 | 9.03 | 8.80 | 8.73 | 8.97 | 10.22 | 10.22 | 7.74 | 7.44 | 7.65 | 7.47 | |

| (0.11) | (0.12) | (0.13) | (0.10) | (0.11) | (0.12) | (0.04) | (0.04) | (0.20) | (0.10) | (0.19) | (0.08) | ||

| 40 | 200 | 52.36 | 43.17 | 36.42 | 36.25 | 51.28 | 35.41 | 41.42 | 41.42 | 45.40 | 78.12 | 31.06 | 30.94 |

| (1.52) | (0.10) | (0.36) | (0.32) | (1.44) | (0.27) | (0.01) | (0.01) | (0.41) | (1.29) | (0.05) | (0.17) | ||

| 500 | 35.90 | 40.52 | 34.44 | 34.32 | 35.18 | 33.56 | 38.55 | 38.55 | 30.02 | 67.15 | 28.69 | 28.68 | |

| (0.12) | (0.03) | (0.08) | (0.05) | (0.13) | (0.11) | (0.16) | (0.17) | (0.10) | (2.50) | (0.13) | (0.09) | ||

| 1000 | 33.94 | 35.19 | 33.64 | 33.58 | 33.39 | 32.87 | 38.18 | 38.18 | 29.62 | 31.75 | 27.95 | 28.00 | |

| (0.31) | (0.25) | (0.15) | (0.13) | (0.29) | (0.12) | (0.19) | (0.19) | (0.23) | (1.28) | (0.18) | (0.13) |

| MN | M | MFA | MFA | MAMN | MAMFA | NC | C | CT-MN | CT-M | CT-MFA | CT-MFA | ||

| 5 | 200 | 0.03 | 0.18 | 1.39 | 6 | 0.16 | 1.53 | 0.01 | 0.14 | 17 | 42 | 102 | 140 |

| 500 | 0.09 | 0.29 | 12 | 20 | 0.21 | 12 | 0.04 | 0.34 | 40 | 214 | 456 | 429 | |

| 10 | 200 | 0.02 | 0.29 | 3.30 | 8 | 0.25 | 3.53 | 0.02 | 0.20 | 43 | 145 | 83 | 251 |

| 500 | 0.06 | 0.35 | 30 | 43 | 0.31 | 30.8 | 0.02 | 0.60 | 81 | 381 | 604 | 967 | |

| 40 | 200 | 0.03 | 0.47 | 8.46 | 13 | 0.65 | 9.08 | 0.02 | 0.55 | 43 | 65 | 103 | 278 |

| 500 | 0.12 | 1.60 | 51 | 61 | 1.06 | 52 | 0.03 | 2.05 | 184 | 424 | 421 | 1148 | |

| 1000 | 0.24 | 5.14 | 91 | 112 | 2.07 | 98 | 0.08 | 3.81 | 201 | 724 | 672 | 1634 |

3.2 Iris data

This data set (Fisher,, 1936) consists of observations of the lengths and widths of the sepals and petals of 150 Iris plants. We are interested in estimating the joint density of these four variables. For visualization purposes, we first consider the density estimation problem in 2 dimensions, and estimate the joint density of the sepal width and the petal length. The first row in Figure 3 shows the original -data and the -space data, respectively. We use the univariate mixture of model to estimate the marginals: a univariate mixture with two components is selected for the sepal width and an univariate model is selected for the petal length. The lower-left panel in Figure 3 shows the transformed -space data via when the normal copula is used. If a normal copula is used then it is necessary to fit a bivariate normal to this data. Clearly, it is unreasonable to do so. The last panel shows the -space data (after the iterative scheme stops) when we use the CT-MN model. A multivariate mixture of two normals is selected by the iterative scheme to estimate the dependence structure. This mixture model seems to fit this data set well, visually showing that the CT-MN model captures the joint dependence structure in the data better than the normal copula model. Indeed, the 10-fold cross-validation LPDS values of CT-MN and NC are and , respectively.

| Estimators | MN | M | MFA | MFA | MAMN | MAMFA |

|---|---|---|---|---|---|---|

| LPDS | ||||||

| Estimators | NC | C | CT-MN | CT-M | CT-MFA | CT-MFA |

| LPDS |

We now consider estimating the joint density of all four variables, and demonstrate the performance of various estimators using the LPDS criterion. The best estimator for the first marginal is the implied mixture of normals, and for the last three marginals the directly-estimated mixtures of . Table 3 summarizes the 10-fold cross-validation LPDS values of these estimators. We draw the following conclusions. 1) CT-M performs the best. 2) The copula-type estimators outperform the normal and copula estimators. 3) Dimension reduction via the factor analyzers models does not help, probably because of the small dimension. The improvement of the mixture-based copula-type estimators over the mixture estimators shows that it is important to estimate the marginals separately. The improvement of the copula-type estimators over the normal and copula estimators shows that it is important to have flexibility in estimating the joint dependence.

3.3 Plasmodium gene expression data

Malaria is an infectious disease caused by the parasitic protozoan genus plasmodium. This data set consists of the relative expression level of parasite genes taken at several time points of the life cycle of parasites. The original data set consisting of the expression level of 4221 genes taken at 46 time points is further processed by Jasra et al., (2007) using K-means clustering and principal component analysis to reduce the number of observations from 4221 to 1000 and the number of variables from 46 to 6. We use the processed data to demonstrate our proposed estimators.

The best estimators for the first three marginals are kernel densities and for the last three are a mixture of , a kernel density and a mixture of normals, respectively. Table 4 summarizes the 5-fold cross validated LPDS values. Typically we have the same conclusions as in the previous example: 1) the CT-M outperforms the others; 2) the copula-type estimators work better than the parametric copulas; and 3) dimension reduction does not help in this low-dimensional example.

| Estimators | MN | M | MFA | MFA | MAMN | MAMFA |

|---|---|---|---|---|---|---|

| LPDS | ||||||

| Estimators | NC | C | CT-MN | CT-M | CT-MFA | CT-MFA |

| LPDS |

3.4 Wine data set

This data set consists of 13 chemical constituents found in 178 samples of wines in a region of Italy. The data set and detailed information on it is available at the UC Irvine Machine Learning Repository http://archive.ics.uci.edu/ml/datasets/Wine. The small number of observations relative to the number of variables in this data set shows the usefulness of dimension reduction via the factor representation. The best models for the marginals vary between a kernel density and a directly-estimated mixture of (details not shown). Table 5 summarizes the multivariate model fitting results. The best estimator is the CT-MFA. In general, dimension reduction improve the performance, e.g. the CT-MFA is better than the CT-MN, the CT-MFA is better than the CT-M. The NC and C work almost as well as the CT-MN and CT-M respectively. This is because the CT-MN and CT-M estimators reduce to the NC and C estimators respectively when the joint dependence does not have a mixture structure.

| Estimators | MN | M | MFA | MFA | MAMN | MAMFA |

|---|---|---|---|---|---|---|

| LPDS | ||||||

| Estimators | NC | C | CT-MN | CT-M | CT-MFA | CT-MFA |

| LPDS |

4 Conclusion

The article introduces copula-type estimators for flexible multivariate density estimation which we believe improve on current popular copula estimators. The new estimators allow the marginal densities to be modeled separately from the joint dependence, as in all copula estimators, but have the ability to model complex joint dependence structures. In particular, the joint dependence in the copula-type estimators that we propose is modeled by mixture models. The mixtures are fitted by Variational Bayes algorithms which automatically incorporate the model selection problem. An iterative scheme is proposed for estimating copula-type estimators and its usefulness is demonstrated through examples.

A practical issue is determining when a mixture-based copula-type estimator is needed for a given data set. As can be seen from the examples, a mixture-based copula-type estimator works well when the underlying joint dependence has a mixture structure. Such an estimator can be obtained by the Variational Bayes fitting algorithm in our paper, i.e. if the multivariate mixture estimated by the iterative scheme has more than one component then it is likely that the underlying joint dependence has a mixture structure. In our experience, if the underlying joint dependence does not have a mixture structure, then the estimated multivariate mixture will have only one component and the resulting copula-type estimator will be very similar to the corresponding normal or copula estimator.

In practice, it is necessary to select an estimator among the four mixture-based copula-type estimators proposed in the article. In our experience, the CT-M often works well in small dimensions and the CT-MFA is the best in high dimensions. However, we suggest fitting all four estimators to the data and then selecting the best estimator using some criterion such as the log predictive density score.

An alternative approach is to use marginally adjusted estimators (Giordani et al.,, 2012) which try to improve on standard multivariate estimators such as a mixture of multivariate normals, by modifying such estimators to take account of the best fitting marginal densities. We believe that the copula-type and the marginal adaptation approaches complement each other, in the sense that marginal adaptation attempts to correct deficiencies in standard multivariate estimators and copula-type estimation attempts to make the popular copula models more flexible. The practitioner may use both approaches and choose the best performing one, by some criterion such as the log predictive score.

We note, however, that if we wish to incorporate dependence on the covariates in the marginals, then it is easier to do so using the copula type estimators than the marginally adjusted estimators because of the need to estimate the normalizing constants in the marginally adjusted estimators.

Acknowledgment

The authors would like to thank the referees for insightful comments which helped to improve the presentation and content of the paper. The research of Minh-Ngoc Tran, Xiuyan Mun and Robert Kohn was partially supported by Australian Research Council grant DP0667069. We thank Professor Ajay Jasra for the genome data.

Appendix A

Proof of Proposition 1.

Without loss of generality, assume that . By construction, , and . The distribution of is

Taking derivatives with respect to and , we obtain the density function of

with .

Now noting that , the density of the first marginal is

∎

Proof of Proposition 2.

By construction, the data are realizations of a random vector obtained by the transformation with uniformly distributed on , . Therefore are the marginal pdf’s of . Denote by be the joint pdf of , we have that

Noting that , by the second result in Proposition 1,

when the sample size inncreases, because the fitting method is reliable. ∎

Appendix B: Variational Bayes algorithms for fitting mixture models

Using Variational Bayes for fitting mixture models has proven useful and efficient. See, e.g., Ormerod and Wand, (2009) for an introduction to Variational Bayes. Giordani et al., (2012) develop efficient Variational Bayes algorithms for fitting a multivariate mixture of normals and a mixture of factor analyzers in which the number of components and the number of factors in each component are automatically selected. We present here Variational Bayes algorithms for fitting a multivariate mixture of and a mixture of -factor analyzers, in which the model selection problem is also automatically incorporated.

Fitting a mixture of

The density of the mixture of model is of the form

| (9) |

where denotes the density of a -variate distribution with location , scale matrix and degrees of freedom . The mean of this distribution is if , and its variance matrix is if . The key to our Variational Bayes fitting approach is the expression of distributions as scale mixtures of normals (Andrews and Mallows,, 1974). The distribution of can be expressed hierarchically as

Using this result, the model (9) can be written as

with and latent variables. Here . For now we consider the degrees of freedom as fixed hyperparameters. This will be relaxed below. The model parameters are . We consider the following decomposition

| (10) |

with the conjugate priors

where , , and are hyperparamters. Note that at the moment the degrees of freedom are also considered as hyperparameters. From the decomposition (10) (cf. Ormerod and Wand,, 2009), the optimal Variational Bayes posteriors are

where denotes expectation with respect to the Variational Bayes posterior , i.e., . In the above

and , , and . Let be the lower bound on .

Estimating the degrees of freedom is challenging in both Bayesian and frequentist approaches. In our setting, the optimal Variational Bayes posterior of does not have any standard form. We proceed as follow. Let be a prior on . We use a point mass distribution for the Variational Bayes posterior of , i.e., with the Dirac delta distribution. The lower bound on is

| (11) |

With the lower bound on , the lower bound on is

| (12) |

This needs to be optimized with respect to . We will use the notation instead of in what follows.

It is well known in Bayesian fitting of distributions that an improper prior on the degrees of freedom leads to an improper posterior, while in frequentist fitting the MLE may not converge because of the non-regularity of the likelihood. A truncated prior is commonly used. We follow Lin et al., (2004) and use the uniform prior on , with some sufficiently large , say . Then maximizing (12) is equivalent to maximizing the following function in

| (13) |

subject to , . This is somewhat similar to the M-step update of the degrees of freedom in the EM algorithm of Peel and McLachlan, (2000). However, Peel and McLachlan, (2000) did not impose any constraint on , which may cause divergence of the solution. For simplicity, we consider to be integer.

Given an initial number of components , the Variational Bayes algorithm sequentially updates the parameters , , , , and until some stopping rule is met. Often, this iterative scheme stops when the lower bound (12) is not improved any further, or when the updates are stable in the sense that the difference of main parameters and in two successive iterations is smaller than a tolerance value. We refer to this update procedure as the standard Variational Bayes algorithm.

To select , we start with a reasonably large value of and remove redundant components on the basis of maximizing the lower bound as follows. After the standard Variational Bayes procedure has converged, we try removing the components with smallest and actually remove these components if the final optimized lower bound is improved. That is, unlike the existing algorithms in which components with the posterior probabilities smaller than a specific threshold value are eliminated (Corduneanu and Bishop,, 2001; McGrory and Titterington,, 2007), we first rank components for elimination and eliminate plausible components until the lower bound is not improved any further. We found that our strategy quickly and efficiently eliminates redundant components, while not requiring any specific threshold value which may be hard to determine. We will refer to this algorithm for determining as the Elimination Variational Bayes (EVB). It might be desirable to include split steps which split poorly-fitted components. However, implementation of split steps is difficult in the mixture context because it is not clear how to initialize new components optimally.

Fitting a mixture of -factor analyzers

The density of a mixture of -factor analyzers is (9) with the scale matrices having factor representation . This model is first considered in McLachlan et al., (2007) who develop an EM algorithm for fitting. Model selection in fitting this model consists of selecting the number of components and the number of factors in each component. Therefore the number of models in the model space is huge, which makes the model selection problem challenging when using model selection criteria such as AIC or BIC because one needs to search over the whole model space. To reduce the model space, McLachlan et al., (2007) consider the same number of factors for all components. We relax this assumption here and develop below a Variational Bayes algorithm for fitting the model in which and are automatically determined. We believe this is the first algorithm in the literature for fitting the (full) mixture of -factor analyzers model which is able to do parameter estimation and model selection simultaneously and automatically.

The model can be written as

with , , latent variables. Following McLachlan et al., (2007) we assume , which helps avoid spikes or near singularities in the likelihood. We consider the following priors on the model parameters

with and put gamma priors on and . The form of the prior plays a key role in determining the local dimensions : a very small value of suggests that the factor of the component should be removed. This approach is introduced in Ghahramani and Beal, (2000) for mixtures of (normal) factor analyzers.

The Variational Bayes optimal posteriors for the parameters are as follows

where

The expectation terms are given by

and

Similar to the reasoning in the previous section, the degrees of freedom are estimated by maximizing

subject to , .

Our standard Variational Bayes algorithm sequentially updates the parameters , , , , , , , , , , , , , and until the difference of main parameters and in two successive iterations is smaller than a tolerance value. Other stopping rules can be used as well.

We now present our strategy for determining the local dimensions . We remove the factor of the component if the posterior mean of is smaller than a threshold . Note that the mean of is . Because the unit of these means depends on that of the data , we found it necessary to standardize the data such that the columns of have standard deviations of 1; this makes the analysis more stable and facilitates the choice of . After fitting, it is straightforward to write the resulting density back in the original units. From our experience, is a good choice. To select , we follow the same elimination Variational Bayes strategy as in the previous section.

In summary, our strategy for model selection in fitting the MFA model is as follows.

-

•

Step 1: Start with a reasonably large value of and with the initial number of factors - the largest value allowed for the number of factors in factor analysis.

-

•

Step 2: After the standard Variational Bayes procedure has converged, remove factors with .

-

•

Step 3: Remove redundant components via the EVB algorithm.

-

•

Step 4: Repeat steps 2 and 3 until the lower bound is not improved any further.

References

- Andrews and Mallows, (1974) Andrews, D. and Mallows, C. (1974). Scale mixtures of normal distributions. Journal of the Royl Statistical Series, Series B, 36:99–102.

- Corduneanu and Bishop, (2001) Corduneanu, A. and Bishop, C. (2001). Variational Bayesian model selection for mixture distributions. In Jaakkola, T. and Richardson, T., editors, Artifcial Intelligence and Statistics, volume 14, pages 27–34. Morgan Kaufmann.

- Fisher, (1936) Fisher, R. (1936). The use of multiple measurements in taxonomic problems. Annual Eugenics, 7, Part II:179–188.

- Geisser, (1980) Geisser, S. (1980). Discussion of “Sampling and Bayes inference in scientific modelling and 10 robustness” by G.E.P. Box. Journal of the Royal Statistical Society, Series A, 143:416–417.

- Ghahramani and Beal, (2000) Ghahramani, Z. and Beal, M. J. (2000). Variational inference for Bayesian mixtures of factor analyzers. In S. A. Solla, T. K. L. and Muller, K., editors, NIPS, volume 12, pages 449–455. MIT Press.

- Ghahramani and Hinton, (1997) Ghahramani, Z. and Hinton, G. (1997). The EM algorithm for mixtures of factor analyzers. Technical report, Dept. of Computer Science, University of Toronto.

- Giordani et al., (2012) Giordani, P., Mun, X., Tran, M.-N., and Kohn, R. (2012). Flexible multivariate density estimation with marginal adaptation. Journal of Computational and Graphical Statistics. to appear.

- Good, (1952) Good, I. (1952). Rational decisions. J. R. Stat. Soc. B, 14:107–114.

- Hastie et al., (2009) Hastie, T. J., Tibshirani, R. J., and Friedman, J. H. (2009). The elements of statistical learning : data mining, inference, and prediction. Springer series in statistics. New York, N.Y. Springer, second edition.

- Jasra et al., (2007) Jasra, A., Stephens, D., and Holmes, C. (2007). Population-based reversible jump Markov chain Monte Carlo. Biometrika, 97(4):787 – 807.

- Joe, (1997) Joe, H. (1997). Multivariate models and dependence concepts. Chapman & Hall, London.

- Krupskii and Joe, (2013) Krupskii, P. and Joe, H. (2013). Factor models for multivariate data. Journal of Multivariate Analysis. To appear.

- Lin et al., (2004) Lin, T. I., Lee, J. C., and Ni, H. F. (2004). Bayesian analysis of mixture modelling using the multivariate distribution. Statistics and Computing, 14:119–130.

- McGrory and Titterington, (2007) McGrory, C. A. and Titterington (2007). Variational approximations in Bayesian model selection for finite mixture distributions. Computaional Statistics and Data Analysis, 51:5352–5367.

- McLachlan and Peel, (2000) McLachlan, G. and Peel, D. (2000). Finite Mixture Models. John Wiley and Sons, New York.

- McLachlan et al., (2007) McLachlan, G. J., Bean, R. W., and Jones, L. B. (2007). Extension of the mixture of factor analyzers model to incorporate the multivariate -distribution. Computational Statistics & Data Analysis, 51:5327 5338.

- Nelsen, (1999) Nelsen, R. (1999). An Introduction to Copulas. Springer-Verlag, New York.

- Ormerod and Wand, (2009) Ormerod, J. T. and Wand, M. P. (2009). Explaining variational approximation. The American Statistician, 64(2):140–153.

- Peel and McLachlan, (2000) Peel, D. and McLachlan, G. J. (2000). Robust mixture modelling using the distribution. Statistics and Computing, 10:339–348.

- Titterington et al., (1985) Titterington, D. M., Smith, A. F. M., and Makov, U. E. (1985). Statistical Analysis of Finite Mixture Distributions. John Wiley & Sons.