Asymptotics for Fixed Transaction Costs111The authors thank Bruno Bouchard, Jan Kallsen, Ludovic Moreau, Mathieu Rosenbaum, and Peter Tankov for fruitful discussions, and Martin Forde for pertinent remarks on an earlier version. Moreover, they are grateful to two anonymous referees for numerous constructive comments.

Abstract

An investor with constant relative risk aversion trades a safe and several risky assets with constant investment opportunities. For a small fixed transaction cost, levied on each trade regardless of its size, we explicitly determine the leading-order corrections to the frictionless value function and optimal policy.

Mathematics Subject Classification: (2010) 91G10, 91G80, 91B28, 35K55, 60H30.

JEL Classification: G11.

Keywords: fixed transaction costs, optimal investment and consumption, homogenization, viscosity solutions, asymptotic expansions.

1 Introduction

Market frictions play a key role in portfolio choice, “drastically reducing the frequency and volume of trade” [9]. These imperfections manifest themselves in various forms. Trading costs proportional to the traded volume affect all investors in the form of bid-ask spreads. In addition, fixed costs, levied on each trade regardless of its size, also play a key role for small investors.

Proportional transaction costs have received most of the attention in the literature. On the one hand, this is due to their central importance for investors of all sizes. On the other hand, this stems from their relative analytical tractability: by their very definition, proportional costs are “scale invariant”, in that their effect scales with the number of shares traded. With constant relative or absolute risk aversion and a constant investment opportunity set, this leads to a no-trade region of constant width around the frictionless target position [31, 9, 11, 12, 41]. Investors remain inactive while their holdings lie inside this region, and engage in the minimal amount of trading to return to its boundaries once these are breached. The trading boundaries can be determined numerically by solving a free boundary problem [11]. In the limit for small costs, the no-trade region and the corresponding utility loss can be determined explicitly at the leading order, cf. Shreve and Soner [41], Whalley and Wilmott [43], Janeček and Shreve [22], as well as many more recent studies [6, 18, 42, 37, 7]. Extensions to more general preferences and stochastic opportunity sets have been studied numerically by Balduzzi, Lynch, and Tan [29, 3, 30]. Corresponding formal asymptotics have been determined by Goodman and Ostrov [19], Martin [32], Kallsen and Muhle-Karbe [25, 24] as well as Soner and Touzi [42]. The last study, [42], also contains a rigorous convergence proof for general utilities, which is extended to several risky assets by Possamaï, Soner, and Touzi [37].

Proportional costs lead to infinitely many small transactions. In contrast, fixed costs only allow for a finite number of trades over finite time intervals. However, the optimal policy again corresponds to a no-trade region. In this setting, trades of all sizes are penalized equally, therefore rebalancing takes place by a bulk trade to the optimal frictionless target inside the no-trade region [13]. These “simple” policies involving only finitely many trades are appealing from a practical point of view. However, fixed costs destroy the favorable scaling properties that usually allow to reduce the dimensionality of the problem for utilities with constant relative or absolute risk aversion. In particular, the boundaries of the no-trade region are no longer constant, even in the simplest settings with constant investment opportunities as well as constant absolute or relative risk aversion. Accordingly, the literature analyzing the impact of fixed trading costs is much more limited than for proportional costs: on the one hand, there are a number of numerical studies [40, 27], which iteratively solve the dynamic programming equations. On the other hand, Korn [26] as well as Lo, Mamaysky, and Wang [28] have obtained formal asymptotic results for investors with constant absolute risk aversion. For small costs, these authors find that constant trading boundaries are optimal at the leading order. Thus, these models are tractable but do not allow us to study how the impact of fixed trading costs depends on the size of the investor under consideration. The same applies to the “quasi-fixed” costs proposed by Morton and Pliska [33], and analyzed in the small-cost limit by Atkinson and Wilmott [2]. In their model, each trade – regardless of its size – incurs a cost proportional to the investors’ current wealth, leading to a scale-invariant model where investors of all sizes are affected by the “quasi-fixed” costs to the same extent. Similarly, the asymptotically efficient discretization rules developed by Fukasawa [16, 17] as well as Rosenbaum and Tankov [39] also do not take into account that the effect of fixed trading costs should depend on the “size” of the investor under consideration.222Indeed, these schemes asymptotically correspond to constant absolute risk version, cf. [17] for more details.

The present study helps to overcome these limitations by providing rigorous asymptotic expansions for investors with constant relative risk aversion.333For our formal derivations, we consider general utilities like in recent independent work of Alcala and Fahim [1]. In the standard infinite-horizon consumption model with constant investment opportunities, we obtain explicit formulas for the leading-order welfare effect of small fixed costs and a corresponding almost-optimal trading policy. These shed new light on the differences and similarities compared to proportional transaction costs.

A universal theme is that, as for proportional transaction costs [22, 32, 25, 24], the crucial statistic of the optimal frictionless policy turns out to be its “portfolio gamma”, which trades off the local variabilities of the strategy and the market (cf. (2.6)). The latter is also crucial in the asymptotic analysis of finely discretized trading strategies [44, 5, 21, 16, 17, 39]. Therefore, it appears to be an appealingly robust proxy for the sensitivity of trading strategies to small frictions.

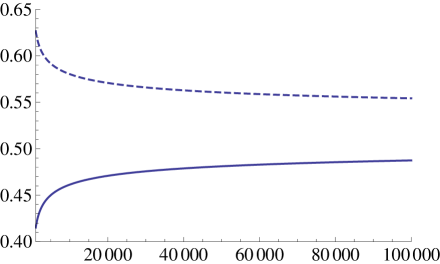

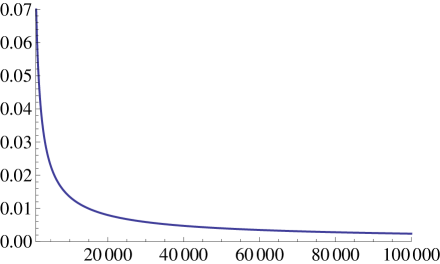

A fundamental departure from the corresponding results for proportional transaction costs is that the effect of small fixed costs is inversely proportional to investors’ wealth. That is, doubling the fixed cost has the same effect on investors’ welfare and trading boundaries as halving their wealth.444Here, both quantities are measured in relative terms, as is customary for investors with constant relative risk aversion. That is, trading boundaries are parametrized by the fractions of wealth held in the risky asset, and the welfare effect is described by the relative certainty equivalent loss, i.e., the fraction of the initial endowment the investor would be willing to give up to trade without frictions. This explains and quantifies to what extent fixed costs can be neglected by large institutional entities, yet play a key role for small private investors. For example, for typical market parameters (cf. Figure 1), a fixed transaction cost of $1 per trade leads to trading boundaries of 45% and 59% around the frictionless Merton proportion of 52% if the investor’s wealth is $5000. If wealth increases to $100000, however, the trading boundaries narrow to 49% and 55%, respectively. Our results also show that, asymptotically for small costs, fixed transaction costs are equivalent – both in terms of the no-trade region and the corresponding welfare loss – to a suitable “equivalent proportional cost”. Since the effect of the fixed costs varies with investors’ wealth, this equivalent proportional cost is not constant, but decreases with the investors’ wealth level. For example, with typical market parameters (cf. Figure 1) a $1 fixed cost corresponds to a proportional cost of 2.3% if the investor’s wealth is $5000, but to only 0.24% if wealth is $100000. In a similar spirit, our results are also formally linked to those of Atkinson and Wilmott [2]: their trading costs, taken to be a constant fraction of the investors’ current wealth, formally lead to the same results as substituting a stochastic fixed cost proportional to current wealth into our formulas.

A second novelty is that our results readily extend to a multivariate setting with several risky assets. This is in contrast to the models with proportional transaction costs, where optimal no-trade regions for several risky assets can only be determined numerically by solving a multidimensional nonlinear free-boundary problem, even in the limit for small costs [37]. With small fixed costs, the optimal no-trade region with several risky assets turns out to be an ellipsoid centered around the frictionless target, whose precise shape is easily determined even in high dimensions by the solution of a matrix-valued algebraic Riccati equation. This is again in line with the quasi-fixed costs studied by Atkinson and Wilmott [2], up to rescaling the transaction cost by current wealth. Qualitatively, the shape of our ellipsoid resembles the one for the parallelogram-like regions computed numerically for proportional transaction costs by Muthuraman and Kumar [34] as well as by Possamaï, Soner, and Touzi [37]. On a quantitative level, however, we find that the shape of the ellipsoid is much more robust with respect to correlation among the risky assets.

Finally, the present study provides the first rigorous proofs for asymptotics with small fixed costs, complementing earlier partially heuristic results [26, 28, 1], rigorous analyses of the related problem of optimal discretization [16, 17, 39], and rigorous asymptotics with proportional costs (see [41, 22, 6, 18, 42, 37, 7]). As for proportional costs [42], our approach is based on the theories of viscosity solutions and homogenization, in particular, the weak-limits technique of Barles and Perthame [4] as well as Evans [14]. However, substantial new difficulties have to be overcome because i) the value function is not concave, ii) the usual dimensionality reduction techniques fail even in the simplest models, iii) the set of controls is not scale invariant, and iv) the dynamic programming equation involves a non-local operator here. In order not to drown these new features in further technicalities, we leave for future research the extension to more general preferences as well as asset price and cost dynamics as in [42, 25, 24] for proportional costs, and also the analysis of the joint impact of proportional and fixed costs.555Cf. [26, 1] for corresponding formal asymptotics.

The remainder of the article is organized as follows: the model, the main results, and their implications are presented in Section 2. Subsequently, we derive the results in an informal manner. This is done in some detail, to explain the general procedure that is likely to be applicable for a number of related problems. In particular, we explain how to come up with the scaling in powers of by heuristic arguments as in [22, 38] and discuss how to use homogenization techniques to derive the corrector equations describing the first-order approximations of the exact solution. Section 4 then makes these formal arguments rigorous by providing a convergence proof. Some technical estimates are deferred to Appendix A. Finally, Appendix B presents a self-contained proof of the weak dynamic programming principle, in the spirit of Bouchard and Touzi [8], which in turn leads to the viscosity solution property of the value function for the problem at hand.

Throughout, denotes the transpose of a vector or matrix , , and we write for the identity matrix on . For a vector , represents the diagonal matrix with diagonal elements .

2 Model and Main Results

2.1 Market, Trading Strategies, and Wealth Dynamics

Consider a financial market consisting of a safe asset earning a constant interest rate , and risky assets with expected excess returns and invertible infinitesimal covariance matrix :

for a -dimensional standard Brownian motion defined on a filtered probability space . Each trade incurs a fixed transaction cost , regardless of its size or the number of assets involved. As a result, portfolios can only be rebalanced finitely many times, and trading strategies can be described by pairs , where the trading times are a sequence of stopping times increasing towards infinity, and the -measurable, -valued random variables collected in describe the transfers at each trading time. More specifically, represents the monetary amount transferred from the safe to the -th risky asset at time . Each trade is assumed to be self-financing, and the fixed costs are deducted from the safe asset account. Thus, the safe and risky positions evolve as

for each trade at time . The investor also consumes from the safe account at some rate . Hence, starting from an initial position , the wealth dynamics corresponding to a consumption-investment strategy are given by

We write for the solution of the above equation. The solvency region

is the set of positions with nonnegative liquidation value. A strategy starting from the initial position is called admissible if it remains solvent at all times: , for all , -a.s. The set of all admissible strategies is denoted by

2.2 Preferences

In the above market with constant investment opportunities and fixed transaction costs , an investor with constant relative risk aversion , i.e., with a utility function of either logarithmic or power type,

and impatience rate trades to maximize the expected utility from consumption over an infinite horizon, starting from an initial endowment of in the safe and in the risky assets, respectively:666By convention, the value of the integral is set to minus infinity if its negative part is infinite.

| (2.1) |

Theorem 2.1.

The value function of the problem with fixed costs is a (possibly) discontinuous viscosity solution of the Dynamic Programming Equation (3.7) in the domain

For our asymptotic results, it suffices to obtain this result for rather than the full solvency region . This is because any fixed initial allocation with will satisfy for sufficiently small .

For the definition of a discontinuous viscosity solution, we refer the reader to [10, 15, 23, 36]. Øksendal and Sulem [36] study existence and uniqueness for one risky asset and power utility with risk aversion under the additional assumption , a sufficient condition for the finiteness of the frictionless value function. The proof of the Theorem 2.1 is given in Appendix B by establishing a weak dynamic programming principle in the spirit of Bouchard and Touzi [8]. We believe that, in analogy to corresponding results for proportional costs [41], the above theorem as well as a comparison result hold in the entire solvency region for all utility functions whenever the transaction cost value function is finite. However, this extension is not needed here.

2.3 Main Results

Let us first collect the necessary inputs from the frictionless version of the problem (cf., e.g., [15]): denote by

the optimal frictionless target weights, i.e., the Merton proportions, in the risky assets. Write

for the frictionless optimal consumption rate and let

| (2.2) |

be the value function for the frictionless counterpart of (2.1) with initial wealth . The latter is finite provided that , which we assume throughout. Moreover, we also suppose that the matrix

| (2.3) |

is invertible.

Remark 2.2.

Our main results are the leading-order corrections for small fixed transaction costs ; their interpretation as well as connections to the literature are discussed in Section 2.4 below.

Theorem 2.3 (Expansion of the Value Function).

For all solvent initial endowments with , we have

that is,

locally uniformly as . Here,

for a constant determined by the corrector equations from Definition 3.1. For a single risky asset ():

see Section 3.6 for the multivariate case. This determines the leading-order relative certainty equivalent loss, i.e., the fraction of her initial endowment the investor would give up to trade the risky asset without transaction costs, as follows:

| (2.4) |

The leading-order optimal performance from Theorem 2.3 is achieved by the following “almost optimal policy”:

Theorem 2.4 (Almost Optimal Policy).

Fix a solvent initial portfolio allocation. Define the no-trade region

for the ellipsoid from Section 3.6. Consider the strategy which consumes at the frictionless Merton rate, does not trade while the current position lies in the above no-trade region, and jumps to the frictionless Merton proportion once its boundaries are breached. Then, for any , the utility obtained from following this strategy until wealth falls to level , and then switching to a leading-order optimal strategy for (2.1), is optimal at the leading order (cf. Section 4.5 for more details).

For a single risky asset, the above no-trade region simplifies to the following interval around the frictionless Merton proportion:

| (2.5) |

Remark 2.5.

Unlike for proportional transaction costs, trading only after leaving the above asymptotic no-trade region is not admissible for any given fixed cost . This is because wealth can fall below the level needed to perform a final liquidating trade. Hence, the above region is only “locally” optimal, in that one needs to switch to the unknown optimal policy after wealth falls below a given threshold.

2.4 Interpretations and Implications

In this section, we discuss a number of interpretations and implications of our main results. We first focus on the simplest case of one safe and one risky asset, before turning to several correlated securities.

Small Frictions and Portfolio Gammas

The transactions of the optimal policies for proportional and fixed costs are radically different. For proportional costs, there is an infinite number of small trades of “local-time type”, whereas fixed costs lead to finitely many bulk trades. Nevertheless, the respective no-trade regions – that indicate when trading is initiated – turn out to be determined by exactly the statistics summarizing the market and preference parameters.

Indeed, just as for proportional transaction costs [22], the width of the leading-order optimal no-trade region in (2.5) is determined by a power of rescaled by the investor’s risk tolerance . This term quantifies the sensitivity of the current risky weight with respect to changes in the price of the risky asset, cf. [22, Remark 4]. Compared to the corresponding formula for proportional transaction costs in [22], it enters through its quartic rather than cubic root, and is multiplied by a different constant. Nevertheless, most qualitative features remain the same: the leading-order no-trade region vanishes if a full safe or risky investment is optimal in the absence of frictions ( or , respectively) and the effect on optimal strategies increases significantly in the presence of leverage (, compare [18]).

As in [32, 25, 24] for proportional costs, the no-trade region can also be interpreted in terms of the activities of the frictionless optimizer and the market as follows. Let be the frictionless optimal strategy for current wealth , expressed in terms of the number of shares held in the risky asset. Then, the frictionless wealth dynamics and Itô’s formula yield

As a result, the maximal deviations (2.5) from the frictionless target can be rewritten in numbers of risky shares as

Our formal results from Section 3.5 suggest that an analogous result remains valid also for more general preferences. Then, the frictionless target (cf. Section 3.1) is no longer constant, and Itô’s formula yields

so that the maximal deviations (3.18) from the frictionless target can be written as

| (2.6) |

in terms of numbers of risky shares. Up to changing the power and the constant, this is the same formula as for proportional transaction costs [25, 32, 24]: the width of the no trade region is determined by the transaction cost, times the (squared) portfolio gamma , times the risk-tolerance of the indirect utility function of the frictionless problem. The portfolio gamma also is the key driver in the analysis of finely discretized trading strategies [44, 5, 21, 16, 17, 39]. Hence, it appears to be an appealingly robust measure for the sensitivity of trading strategies to small frictions.

Wealth Dependence and Equivalent Proportional Costs

A fundamental departure from the corresponding results for proportional transaction costs is that the impact of fixed costs depends on investors’ wealth. Indeed, the fixed cost is normalized by the investors’ current wealth, both in the asymptotically optimal trading boundaries (2.5) and in the leading-order relative welfare loss (2.4), see Figure 1 for an illustration. This makes precise to what extent fixed costs can indeed be neglected for large institutional traders, but play a key role for small private investors: ceteris paribus, doubling the investors’ wealth reduces the impact of fixed trading costs in exactly the same way as halving the costs themselves. As a result, a constant fixed cost leads to a no-trade region that fluctuates with the investors’ wealth. In contrast, for proportional transaction costs, this only happens if these evolve stochastically. The formal results of Kallsen and Muhle-Karbe [24] shed more light on this connection. It turns out that a constant fixed cost is equivalent – both in terms of the associated no-trade region and the corresponding welfare loss – to a random and time-varying proportional cost given by

for current total wealth .777To see this, formally let the time horizon tend to infinity in [24, Sections 4.1 and 4.2] and insert the explicit formulas for the optimal consumption rate and risky weight. This immediately yields that the leading-order no-trade regions coincide; for the corresponding welfare effects this follows after integrating. Note that this formula is independent of the impatience parameter , and only depends on the market parameters () through the Merton proportion . This relation clearly shows that a fixed cost corresponds to a larger proportional cost if rebalancing trades are small because i) the investors’ wealth is small or ii) the no-trade region is narrow because the frictionless optimal position is close to a full safe or risky position ( or ). In contrast, for large investors and a frictionless position sufficiently far away from full risky or safe investment, the effect of fixed costs becomes negligible (cf. Figure 1 for an illustration). For sufficiently high risk aversion , the equivalent proportional cost is increasing in risk aversion (as higher risk aversion leads to smaller trades), in line with the numerical findings of Liu [27] for exponential utility. Here, however, one can additionally assess the impact of changing wealth over time endogenously, rather than by having to vary the investors’ risk aversion.

Our asymptotic formulas for fixed costs also allow to relate these to the fixed fraction of current wealth charged per transaction in the model of Morton and Pliska [33]. Their “quasi-fixed” costs are scale-invariant, in that they lead to constant trading boundaries around the Merton proportion , whose asymptotics have been derived by Atkinson and Wilmott [2]. Formally, these trading boundaries coincide with ours if the ratio of their time-varying trading cost and our fixed fee is given by the investors’ current wealth.

Multiple Stocks

For multiple stocks, Theorem 2.4 shows that it is approximately optimal to keep the portfolio weight in an ellipsoid around the frictionless Merton position . Whereas nonlinear free-boundary problems have to be solved to determine the optimal no-trade region for proportional costs even if these are small [37], the asymptotically optimal no-trade ellipsoid with fixed costs is determined by a matrix-valued algebraic Riccati equation, which is readily evaluated numerically even in high dimensions (see Section 3.6 for more details). Qualitatively, this is again in analogy to the asymptotic results of Atkinson and Wilmott [2] for the Merton and Pliska model [2] but – as for a single risky asset – the trading boundary varies with investors’ wealth for the fixed costs considered here.

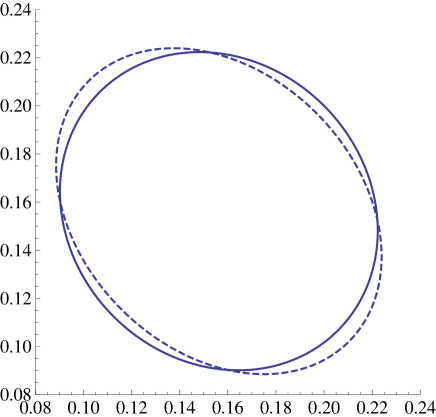

To shed some light on the quantitative features of the solution, Figure 2 depicts the no-trade ellipsoid for two identical risky assets with varying degrees of correlation.888To facilitate comparison, we use the same market parameters and risk aversion as in Muthuraman and Kumar [34]. The fixed cost and the current wealth are chosen so that the one dimensional no-trade region for each asset corresponds to the one for their 1% proportional cost. Qualitatively, correlation deforms the shape of the no-trade region similarly as in Muthuraman and Kumar [34, Figure 6.8] for proportional costs: in the space of risky asset weights, the no-trade region shrinks in the direction but widens in the -direction because investors use the positively correlated assets as partial substitutes for one another.

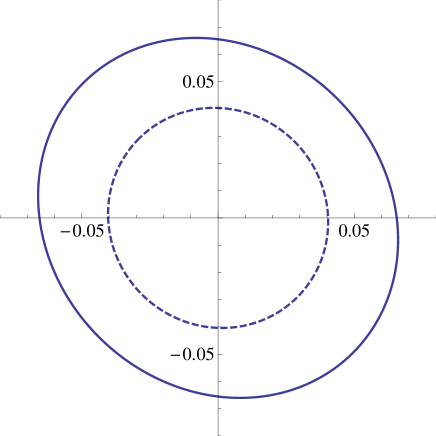

On a quantitative level, however, the impact of correlation turns out to be considerably less pronounced for fixed costs. This is because whenever any trade happens all stocks can be traded with no extra cost, weakening the incentive to use substitutes for hedging. Also notice that the no-trade region is not rotationally symmetric even for two identical uncorrelated stocks. This is in contrast to the results for exponential utilities, for which the investor’s maximization problem factorizes into a number of independent subproblems [27]. Note, however, that as risk aversion rises the optimal no-trade region for uncorrelated identical stocks quickly becomes more and more symmetric, in line with the high risk aversion asymptotics linking power utilities to their exponential counterparts.999Compare Nutz [35] for a general frictionless setting, as well as Guasoni and Muhle-Karbe [20] for a model with proportional transaction costs. A similar result for fixed costs is more difficult to formulate, because the investor’s wealth does not factor out of the trading policy in this case. This is illustrated in Figure 3.

3 Heuristic Derivation of the Solution

In this section, we explain how to use the homogenization approach to determine the small-cost asymptotics on an informal level. The derivations are similar to the ones for proportional costs [42].

Since this entails few additional difficulties on a formal level, we consider general utilities defined on the positive half-line in this section. For the rigorous convergence proofs in Section 4, we focus on utilities with constant relative risk aversion in order not to drown the arguments in technicalities.

3.1 The Frictionless Problem

The starting point for the present asymptotic analysis is the solution of the frictionless version of the problem at hand. Since trades are costless in this setting, the corresponding value function does not depend separately on the positions in the safe and the risky assets, but only on total wealth . As is well known (cf., e.g., [15, Chapter X]), the frictionless value function solves the dynamic programming equation

| (3.1) |

where

| (3.2) |

and the corresponding optimal consumption rate and optimal risky positions are given by

| (3.3) |

and

| (3.4) |

For power or logarithmic utilities with constant relative risk aversion , this leads to the explicit formulas from Section 2.3 because the value function is homothetic in this case: (if ) resp. (if ).

3.2 The Frictional Dynamic Programing Equation

For the convenience of the reader, we now recall how to heuristically derive the dynamic programming equation with fixed trading costs. We start from the ansatz that the value function for our infinite horizon problem with constant model parameters should only depend on the positions in each of the assets. Evaluated along the positions corresponding to any admissible policy , Itô’s formula in turn yields

| (3.5) |

where

By the martingale optimality principle of stochastic control, the utility

obtained by applying an arbitrary policy until some intermediate time and then trading optimally should always lead to a supermartingle, and to a martingale if the optimizer is used all along. Between trades – in the policy’s “no-trade region” – this means that the absolutely continuous drift should be nonpositive, and zero for the optimizer. After taking into account (3.5), using integration by parts, and canceling the common factor , this leads to

| (3.6) |

By definition, the value function can only be decreased by admissible bulk trades at any time:

and this inequality should become an equality for the optimal transaction once the boundaries of the no-trade region are breached. Combining this with (3.6) and switching the sign yields the dynamic programming equation:

| (3.7) |

where is the convex dual of the utility function , the differential operator is defined as

and denotes the non-local intervention operator

3.3 Identifying the Correct Scalings

The next step is to determine heuristically how the optimal no-trade region around the frictionless solution and the corresponding utility loss should scale with a small transaction cost . This can be done by adapting the heuristic argument in [22, 38]. Indeed, the welfare effect of any trading cost is composed of two parts, namely the direct costs incurred due to actual trades and the displacement loss due to having to deviate from the frictionless optimum. Since the frictionless value function is locally quadratic around its maximum, Taylor’s theorem suggests that the displacement effect should be of order for any small cost that only causes a small displacement . Where the various cost structures differ is in the losses due to actual trades. Proportional transaction costs lead to trading of local-time type, which scales with the inverse of the width of the no-trade region [22, Section 3]. This leads to a total welfare loss proportional to

for some constant . Minimizing this expression leads to a no-trade region with width of order and a corresponding welfare loss of order . In contrast, trades of all sizes are penalized alike by fixed costs. This leads to a bulk trade to the optimal frictionless position, and therefore a transaction cost of , whenever the boundaries of the no-trade region are reached. On the short time-interval before leaving a narrow no-trade region, any diffusion resembles a Brownian motion at the leading order. Hence, the first exit time can be approximated by the one of a Brownian motion from the interval , which scales with . After the subsequent jump to the midpoint of the no-trade region, this procedure is repeated, so that the number of trades approximately scales with . As a result, the total welfare loss due to small fixed costs is proportional to

for some constant . Minimizing this expression in then leads to an optimal no-trade region of order and a corresponding welfare loss of order .

3.4 Derivation of the Corrector Equations

In view of the above considerations, we expect the leading-order utility loss due to small transaction costs to be of order , whereas the deviations of the optimal policy from its frictionless counterpart should be of order . This motivates the following ansatz for the asymptotic expansion of the transaction cost value function:

| (3.8) |

Here, is the frictionless value function from Section 3.1, the functions and are to be calculated, and we change variables from the safe and risky positions to total wealth

and the deviations

of the risky positions from their frictionless targets, normalized to be of order as . The function is included, even though it only contributes at the higher order itself, because its second derivatives with respect to the -variables are of order .

To determine and , insert the postulated expansion (3.8) into the Dynamic Programming Equation (3.7). This leads to two separate equations in the no-trade and trade region, respectively.

No-Trade Region

To ease notation, we illustrate the calculations for the case of a single risky asset (), and merely state the multi-dimensional results at the end.101010The full multi-dimensional derivation can be found in [42]. In the no-trade region, the calculations are identical. In the no-trade region, we have to expand the elliptic operator from (3.7) in powers of . To this end, Taylor expansion, (3.3), and yield

Moreover, also taking into account that , it follows that

for the differential operator from (3.2). The -terms in this expression vanish by definition (3.4) of the frictionless optimal weight; the same holds for the -terms by the frictionless Dynamic Programming Equation (3.1). Satisfying the elliptic part of equation (3.7) between bulk trades – at the leading order – is therefore tantamount to

| (3.9) |

Trade Region

Now, turn to the second part of the frictional Dynamic Programming Equation (3.7), which should vanish when a bulk trade becomes optimal outside the no-trade region. Suppose that and . Then, inserting the expansion for yields

where the infimum is over deviations attainable from the current position by a single trade. Taylor expansion yields

If where only depends on ,111111This will turn out to be consistent with the results of our calculations below; see Sections 3.5 and 3.6. this simplifies to

In the ansatz (3.8), the function is multiplied by a higher-order term. Therefore, its value at a particular point is irrelevant at the leading order and we may assume . As a result, we expect , because a zero deviation from the frictionless position should lead to the smallest utility loss. Consequently, the leading-order dynamic programming equation outside the no-trade region reads as

| (3.10) |

Note that this derivation remains valid for several risky assets.

Corrector Equations

Together with (3.9), (3.10) shows that – at the leading order – the Dynamic Programming Equation (3.7) can be written as

| (3.11) |

where we set

| (3.12) |

To solve (3.11), first treat the -variable as constant and solve (3.11) as a function of only:

for some that only depends on but not on . Then, take as given and solve for the function of :

If both of these “corrector equations” are satisfied, (3.11) evidently holds as well. For several risky assets, the corresponding analogues read as follows:

Definition 3.1 (Corrector Equations).

For a given , the first corrector equation for the unknown pair is

| (3.13) |

together with the normalization , where

The second corrector equation uses the function from the first corrector equation and is a simple linear equation for the function :

| (3.14) |

where – defined in (3.12) and (3.2) – is the infinitesimal generator of the optimal wealth process for the frictionless problem.

Remark 3.2.

As for proportional costs [42, Remark 3.3], the first corrector equation is the dynamic programming equation of an ergodic control problem. Indeed, for fixed and for an increasing sequence of stopping times and impulses , one defines the cost functional by

where the state process is given by

with a -dimensional standard Brownian motion .

The structure of the above problem implies that the optimal strategy is decreed through a region enclosing the origin. The optimal stopping times are the hitting times of to the boundary of . When hits , it is optimal to move it to the origin. Hence, the optimal stopping times are the hitting times of of the boundary of and , so that for each Put differently, the region provides the asymptotic shape of the no-trade region. In the power and log utility case, it is an ellipsoid as in Figure 2.

The function is the optimal value,

Then, the Feynman-Kac formula, for the linear equation for implies

where is the optimal wealth process for the frictionless Merton problem with initial value .

3.5 Solution in One Dimension

If there is only a single risky asset (), the asymptotically optimal no-trade region is an interval . The first corrector equation can then be readily solved explicitly by imposing smooth pasting at the boundaries, similarly as for proportional transaction costs [42]. Matching values and first derivatives across the trading boundaries leads to two conditions for a symmetric function , in addition to the actual optimality equation in the interior of the no-trade region. Thus, the lowest order polynomials in capable of fulfilling these requirements are of order four. Since we have imposed , this motivates the ansatz

Inside the no-trade region, inserting this ansatz into the first corrector equation (3.13) gives

where as in Definition 3.1 above. Since this equation should be satisfied for any value of , comparison of coefficients yields

| (3.15) |

Next, the smooth pasting condition at the trading boundary implies

| (3.16) |

Finally, the value matching conditions at give

and in turn

| (3.17) |

In view of (3.16) and (3.15), the optimal trading boundaries are therefore determined as

| (3.18) |

For utilities with constant relative risk aversion , the optimal frictionless risky position is , so that that the corresponding trading boundaries are given by

For the maximal deviations of the risky weight from the frictionless target, this yields the formulas from Theorem 2.4:

With constant relative risk aversion, the homotheticity of the value function (2.2) and (3.17) imply that the second corrector equation simplifies to

which is solved by

This is the formula from Theorem 2.3.

3.6 Solution in Higher Dimensions

Let us now turn to the solution of the corrector equations for multiple risky assets. To ease the already heavy notation, we restrict ourselves to utilities with constant relative risk aversion here. Then, we can rescale the corrector equation to obtain a version which is independent of the wealth variable . Indeed, let

so that, setting

we obtain

for some constant and a function to be determined. We also introduce the matrices

Then, a direct computation shows

We use the notation to rewrite the corrector equation. The resulting rescaled equation is for the pair , with independent variable

| (3.19) |

together with the normalization Following Atkinson and Wilmott [2], we postulate a solution of the form

for a symmetric matrix to be computed. Then,

Hence:

provided that and solves the algebraic Ricatti equation

| (3.20) |

Remarkably, this is exactly equation (3.7) obtained by Atkinson and Wilmott [2] in their asymptotic analysis of the Morton and Pliska model [33] with trading costs equal to a constant fraction of the investors’ current wealth. Atkinson and Wilmott [2] argue that one may take to be the identity without any loss of generality by transforming to a coordinate system in which the second order operator is the Laplacian. For the convenience of the reader, we provide this transformation here: since is symmetric positive definite by Assumption (2.3), there is a unitary matrix for which

where denote the eigenvalues of . Setting

Equation (3.20) becomes

| (3.21) |

Using that and have the same eigenvectors, Atkinson and Wilmott (see (3.8-3.11) in [2]) obtain simple algebraic equations for the eigenvalues of , thus determining up to the above coordinate transformation. In summary, given positive definite, there exists a positive definite solution of (3.20). Then, the following function solves the corrector equation (3.13):

where is the following ellipsoid around zero:

Reverting to the original variables, it follows that the asymptotically optimal no-trade region should be given by

in accordance with Theorem 2.4.

Remark 3.3.

For each define

so that, given, one has if and only if .

4 Proofs

In the sequel, we turn the above heuristics into rigorous proofs of our main results, Theorems 2.3 and 2.4, using the general methodology developed by Barles and Perthame [4] and Evans [14] in the context of viscosity solutions. To ease notation by avoiding fractional powers, we write

and, with a slight abuse of notation, use sub- or superscript to refer to objects pertaining to the transaction cost problem. For instance, refers to , to et cetera.

To establish the expansion of the value function asserted in Theorem 2.3, we need to show that

is locally uniformly bounded from above as . To this end, define the relaxed semi-limits

| (4.1) |

Their existence is guaranteed by the straightforward lower bound , as well as the locally uniform upper bound provided in Theorem 4.1. Establishing the latter involves the explicit construction of a particular trading strategy and is addressed first. We then show in Sections 4.2 and 4.3 that the relaxed semi-limits are viscosity sub- and super-solutions, respectively, of the Second Corrector Equation (3.14). Combined with the Comparison Theorem 4.12 for the second corrector equation provided in Section 4.4, this in turn yields that . Since the opposite inequality is satisfied by definition, it follows that is the unique solution of the Second Corrector Equation (3.14). As a consequence, locally uniformly, verifying the asymptotic expansion of the value function. With the latter at hand, we can in turn verify that the policy from Theorem 2.4 is indeed almost optimal for small costs (cf. Section 4.5).

4.1 Existence of the Relaxed Semi-Limits

Locally uniform upper bound of

In this section we show that is locally uniformly bounded from above as :

Theorem 4.1.

Given any with , there exists and such that

| (4.2) |

Theorem 4.1 is an immediate corollary of Theorem 4.6 below. To prove the latter, we construct an investment-consumption policy which gives rise to a suitable upper bound. The construction necessitates some technical estimates. The reader can simply read the definition of the strategy and proceed directly to the proof of Theorem 4.6 in order to view the thread of the argument.

Strategy up to a Stopping Time

Given an initial portfolio allocation , use the trading strategy from Theorem 2.4, corresponding to the no-trade region , from time until a stopping time to be defined below. More specifically, let , where is the -th time the portfolio process hits the boundary of the no-trade region. The corresponding reallocations are chosen so that, after taking into account transaction costs, the portfolio process is at the frictionless Merton proportions:

Until , the investor consumes the optimal frictionless proportion of her current wealth,

so that her wealth process is governed the following stochastic differential equations until time :

| (4.3) |

The stopping time must be chosen so that the investor’s position remains solvent at all times, , -almost surely. Therefore, we use the first time the investor’s wealth falls below some threshold, which needs to be large enough to permit the execution of a final liquidating bulk trade.

At Time and Beyond

Define to be the exit time of the portfolio process from the set

Within the above policy is used and the portfolio process follows (4.1). At time the investor liquidates all risky assets, leading to a safe position of least . Afterwards, she consumes at half the interest rate, thereby remaining solvent forever. The resulting portfolio process satisfies the following deterministic integral equation with stochastic initial data:

| (4.4) |

Let be the portfolio process produced by concatenating the controlled stochastic process (4.1) and the deterministic process (4.4) at time .

Remark 4.2.

For any , the optimal value must be greater than or equal to the utility obtained from the immediate liquidation of all risky assets and then running the deterministic policy (4.4). Since the latter can be computed explicitly, this provides a crude lower bound for .

To see this, suppose the investor’s wealth after the liquidating trade at time is given by . Then, . For power utilities (), this yields the lower bound

The corresponding result for logarithmic utility () is

| (4.5) |

Constructing a Candidate Lower Bound

For given , define the function

We now establish a series of technical lemmata. These will be used in the proof of Theorem 4.6 to verify that – asymptotically – is dominated by the value function in the no-trade region for an appropriate choice of the parameters and .

Lemma 4.3.

Let be given. There exists independent of such that for all we have

Proof. We only consider power utilities (); the case of logarithmic utility can be treated similarly. First, notice that since the term is always negative it can be ignored. Write , for some Using the estimates from Remark 4.2, the goal is to find a sufficiently large so that

for all This follows by observing that one can take

| (4.6) |

for a large enough positive constant which only depends on the model and preference parameters () but is independent of and .

Lemma 4.4.

There exists such that, for all sufficiently large, there is such that

Proof. Recall that, by definition, the corrector satisfies as well as for

First consider the case of power utility. Taylor expansion and evaluation at yields

| (4.7) |

where the points are determined by the Taylor remainders of and , respectively, and satisfy Considering expression (4.1) as a function of , the dominant term is of the order Since where only depends on the model parameters (), the term also contributes at the order . Consequently, choosing

| (4.8) |

ensures that the leading-order coefficient is positive, independent of . For sufficiently large , the assertion follows.

In the case of logarithmic utility (), the argument is the same because the expressions involved are all power type functions. The same choice (4.8) of works as well.

Lemma 4.5.

Proof. We consider only the power utility case as the argument also works mutatis mutandis for logarithmic utility. To ease notation, we write instead of . Throughout the proof, satisfies Decompose

We analyze the asymptotic properties in of each of the terms and :

Here, we used that if is sufficiently large. The estimates in Remark A.2, and the fact that is of order (cf. Equation (4.6)) give

where . Hence, this term is positive for sufficiently large . Finally, by Remark A.2, we have

again for all sufficiently large . In summary:

for sufficiently large . Equivalently, there exists some such that, for all and :

This completes the proof.

We now have all the ingredients to prove the main result of this section, which in turn yields Theorem 4.1.

Theorem 4.6.

Proof. Let be given and let be large enough so that all the previous lemmata are applicable. Without loss of generality, we may assume , since we are proving an asymptotic result.

Step 1: Let be the controlled portfolio process with dynamics (4.1), (4.4), which starts from the initial allocation and switches to deterministic consumption at half the interest rate at the first time the total wealth falls to level . As before, write

Recall that and are given by (4.6) and (4.8), respectively. Itô’s formula yields

Observe that the summation is at most countable and that, in view of Lemma 4.4, each summand satisfies

Together with Lemma 4.5, this yields

| (4.11) |

Step 2: For any with let be the strategy of (4.4), i.e., liquidation of all risky assets and then deterministic consumption at half the risk-free rate ad infinitum. According to Remark 4.2 and the proof of Lemma 4.3,

where

Let be a localizing sequence of stopping times for the local martingale term in (4.11) and set . Assume for the moment that the family is uniformly integrable, and therefore it converges in expectation to its pointwise limit. Then, the same applies to the integral of the term in (4.11) by the dominated convergence theorem. Taking expectations in (4.11), sending and using these observations together with Lemmas 4.3 and 4.5 shows

As were arbitrary, the assertion (4.9) follows.

Step 3: All that remains to show is that is uniformly integrable. Since the functions and domains are explicit, one can check that there is a constant , independent of such that

Hence, it is sufficient to show that is uniformly integrable. This will follow, for instance, if it is uniformly bounded in for some The interesting case is ; otherwise is bounded on the domain under consideration because the wealth process is bounded away from zero and the Merton value function is negative. We just show the power utility case; a similar argument applies for logarithmic utility.

Let denote the same controlled wealth process, however, obtained by not deducting transaction costs or consumption. Evidently, almost surely, for any stopping time . Moreover, for any , we have

where When , the drift term is maximized at the Merton proportion, , and moreover, by the finiteness criterion for the frictionless value function:

Taking and for sufficiently small , the drift term is maximized at a vector arbitrarily close to , for which

| (4.12) |

As a consequence:

Taking expectations, passing to the limit over a localizing sequence of stopping times for the local martingale term, and applying Fatou’s lemma, we obtain

Hence, the family is uniformly bounded in and thus uniformly integrable as claimed.

We conclude this section by establishing that the relaxed semi-limits only depend on total wealth and can be realized by restricting to limits on the Merton line.

Lemma 4.7.

For any , we have

Proof. Given , where without loss of generality, we observe that

| (4.13) |

Therefore,

and

| (4.14) |

Let be chosen so that we have Setting and using the previous observations, it follows that

Taking as on both sides yields

where The proof for is similar.

Remark 4.8.

For later use, observe that

where are the lower and upper semi-continuous envelopes of , respectively. Moreover, (4.14) extends to the envelopes as follows:

| (4.15) | ||||

4.2 Viscosity Sub-Solution Property

Theorem 4.9.

The function is a viscosity sub-solution of the Second Corrector Equation (3.14).

Proof. Let so that

To prove the assertion, we have to show

Step 1: By Theorem 4.6, there exist , depending on so that

| (4.16) |

The radius can taken small enough that does not intersect the line By Lemma 4.7, can be achieved along a sequence on the Merton line, i.e.,

Observe that

and

Due to the strict maximality of at , each can be taken to be a maximizer of on For and set

with to be chosen later.

Step 2: Now, we use the function to touch from below near . Set

Consider any point . We have

| (4.17) |

Thus, can be chosen large enough to ensure that (4.2) is positive for all sufficiently small when .

Next, we show that when and (recall the definition of in Remark 3.3). To this end, observe that by Taylor expansion, (4.15), and the maximizer property of , we have

for all sufficiently small . Using , we deduce that attains a local minimum at some point with and for all sufficiently small.

Step 3: Now, we derive some limiting identities. Since, according to the previous argument, is uniformly bounded in , there is a convergent subsequence where and . Then,

by construction. Moreover:

So in fact, the inequalities must all be equalities. The strict maximality property of at in turn gives and . Having chosen a particular subsequence, we may, without loss of generality, write instead of . Using that is a super-solution of the Dynamic Programming Equation (3.7), one obtains

As , we have

Step 4: Combining the above limits with yields the inequality

Finally, letting and using the local boundedness of (cf. Proposition A.3) produces the desired inequality:

4.3 Viscosity Super-Solution Property

Theorem 4.10.

is a viscosity super-solution of the Second Corrector Equation (3.14).

Proof. Let be such that

To prove the assertion, we have to show

Step 1: As before, we start by constructing the test function. Recall that

where denotes the upper-semicontinuous envelope of the transaction cost value function . By definition of the relaxed semi-limit and Lemma 4.7, there exists a sequence on the Merton line so that

Set

and

We localize by choosing such that does not intersect the line Define

where is chosen so large that

Then, for all we have

| (4.18) |

and, by construction,

Step 2: A priori, there is no reason that the supremum in (4.18) should be achieved at any particular point, let alone that a maximizing sequence should converge as we send to zero. As a way out, we perturb the original test function to complete the localization. To this end, fix and let be a maximizing sequence of . (Keep in mind that this sequence depends on .) Set

and

where

Notice that as . The modified test function is taken to be

so that

By construction, each has a maximizer, say Observe that the rate of decay of with respect to can be taken to be as fast as we wish, simply by choosing large enough. We will find it convenient to take which can always be accomplished by relabeling, if necessary.

For any selection , it turns out that is the unique subsequential limit of as . Indeed, note that since , it contains a convergent subsequence. If is the limit of such a subsequence, then

which implies that

By the strict minimality of at we must have

Step 3: Next, we show that any sequence of maximizers of where as , satisfying is asymptotically contained in the no-trade region, that is,

for all sufficiently large . To see this, suppose by way of contradiction that instead

| (4.19) |

for some Such a point exists by the upper-semicontinuity and the boundedness of at fixed wealths. Using the fact that is a maximizer of on , one deduces that

for all sufficiently large because . This contradicts (4.19).

By the sub-solution property of at for which we now write , one obtains the differential inequality

Step 4: We claim that is uniformly bounded in . Expanding the above differential inequality into powers of leads to

We proceed to estimate each term. To this end, let denote a sufficiently large generic constant. By Proposition A.3, we have

and

as well as

Finally,

We therefore conclude that

Recalling that , it follows that the dominant term is non-negative and therefore must be uniformly bounded in . Hence, along some subsequence we have and Sending gives

Finally, let . Together with the -estimates on (cf. Proposition A.3), it follows that the trace term disappears from the inequality. This yields

thereby completing the proof.

4.4 Comparison for the Second Corrector Equation

A straightforward computation shows that for some constant If the Merton value function is finite, i.e. , one readily verifies that . Moreover, since the matrix from (2.3) is assumed to be invertible, the diffusion coefficient in (3.19) is positive definite, so that As a consequence,

Remark 4.11.

In view of the explicit locally uniform upper bound (4.10) for from Theorem 4.6, the relaxed semi-limits satisfy the growth constraint

| (4.20) |

We therefore prove that the second corrector equation satisfies a comparison theorem in the class of non-negative functions satisfying this growth condition:

Theorem 4.12.

Let be positive and satisfy the growth constraint (4.20). If

is satisfied in the viscosity sense, then

where .

Proof. We just prove that the sub-solution is dominated by ; the second part of the assertion follows along the same lines. Let be a sub-solution to satisfying the growth condition (4.20). We need to distinguish two cases:

Case 1: Suppose Set

where

Then, for all sufficiently small we have for all To see this, suppose on the contrary that, at some point, . Then, due to the growth restriction on , will have a global maximum at some and

However, by construction,

Therefore, everywhere. For , this gives

Case 2: Now suppose Set instead

The proof then follows along the same lines as in the first case.

4.5 Proof of the Main Results

We now conclude by proving the main results of the paper.

Expansion of the Value Function

Proof of Theorem 2.3. We have shown in Theorem 4.1 that the relaxed semi-limits and of (4.1) exist, are functions of wealth only by Lemma 4.7 and, by Theorem 4.6, satisfy the growth condition

In view of Theorems 4.9 and 4.10,

holds in the viscosity sense. As a result, Theorem 4.12 gives

The opposite inequality evidently holds by definition, therefore

| (4.21) |

The locally uniform convergence claimed in Theorem 2.3 then follows directly from (4.21) and the definitions of

Almost Optimal Policy

With the asymptotic expansion from Theorem 2.3 at hand, we can now show that the policy from Theorem 2.4 is almost optimal for small costs. To this end, fix an initial allocation and a threshold . Consider the policy from Theorem 2.4. If wealth falls below the threshold, another strategy is pursued (see Remark 2.5). More precisely, we choose controls such that i) where is the first time the wealth process falls below level , and ii) is -optimal on for each realization of . The main technical concern is whether this can be done measurably, but this will follow from a construction similar to the one performed in the proof of the weak dynamic programming principle (B.2).

Let be the corresponding expected discounted utility from consumption:

Then we have:

Theorem 4.13.

There exists such that, for all :

That is, the policy from Theorem 2.4 is optimal at the leading order .

Proof. Step 1: Set

for some sufficiently large to be chosen later. Itô’s formula yields

Step 2: We show that there are a sufficiently large and a sufficiently small such that, for all ,

Expanding a typical summand, where and , we find that

can be achieved for sufficiently small , uniformly in , provided that is chosen large enough. (Here, the points come from the Taylor remainders of and , respectively.)

Step 3: Next, establish that, for a suitable , we have

for all and for all Expanding the elliptic operator applied to , we obtain

for sufficiently large , where is positive for and negative for , thanks to the pointwise estimates on the remainder terms (cf. Remark A.2) and the fact that is proportional to The argument for logarithmic utility is similar. The inequality therefore holds for all sufficiently small and for all

Step 4: We now choose an appropriate control to use after time Define the set

and, for each point , choose such that

We also define, for each , the set

By construction we have

and by compactness there is a finite sub-cover, say for some .

Now, define a mapping which assigns to each point one of the neighborhoods in the subcover to which it belongs:

and set

By the monotonicity of the value function,

| (4.22) |

Also, since is smooth, each is open. Finally, define the following control :

Step 5: Piecing together the above estimates, and proceeding as in the proof of Theorem 4.6 to get rid of the local martingale term, we obtain

where we have used in the last step that is positive for ,121212For logarithmic utility (), this follows similarly by additionally exploiting the estimate (4.5). and where

The convergence results from Theorem 2.3 imply that as Since

it follows that the proposed policy is indeed optimal at the leading order .

Appendix

Appendix A Pointwise Estimates

Proposition A.1.

There exists such that, for and , we have

Remark A.2.

Proposition A.1 yields the expansion

where the remainder term satisfies the bound

In particular,

We can also expand

with the following bound on the remainder:

Proof. This follows from tedious but straightforward computations, since all the functions and domains involved are known explicitly (compare [42, Section 4.2] for a similar calculation).

Proposition A.3.

Let be given and consider , for some Then, given any for which each restriction has compact support, there exists a independent of so that

| (A.1) |

and

| (A.2) |

Proof. This again follows from a tedious but straightforward calculation.

Appendix B Proof of Theorem 2.1

In this section we prove that for each fixed the value function is a viscosity solution of the corresponding Dynamic Programming Equation (3.7) on the domain

As observed by Bouchard and Touzi [8], a “weak version” of the dynamic programming principle is sufficient to derive the viscosity property via standard arguments (see for instance Chapter 7, in particular Theorem VII.7.1, in [15]). Rather than checking the abstract hypotheses of [8], we present, for the convenience of the reader, a direct proof of the weak dynamic programming principle in our specific setting, using the techniques of [8].

To this end, fix , , let denote the ball of radius centered at , and set

Take sufficiently small so that . For any investment-consumption policy , define as the exit time of the corresponding state process from . (Following standard convention, our notation does not explicitly show the dependence of on .) It is then clear that

The following weak version of the DPP is introduced in [8]:

Let be a smooth and bounded function on , satisfying

Then, we have

| (B.1) |

The restriction to bounded test functions is possible since by (4.13), is bounded on .

Conversely, let be a smooth function bounded on , satisfying

Then, we have

| (B.2) |

We start with the proof of (B.1). For any policy , let be its restriction to the (stochastic) interval . Then, , -a.s. Therefore,

holds by definition of the value function and because lies in the set where dominates by definition. As a result, for any ,

By taking the supremum over all policies , we arrive at (B.1).

To prove (B.2), set to be the right hand side of (B.2), that is:

For any we can choose satisfying

| (B.3) |

We have already argued that . Our next step is to construct a countable open cover of . For every point , set

By the monotonicity of the value function,

| (B.4) |

Also, since is smooth, each is open and

Hence, by the Lindelöf covering lemma, we can extract a countable subcover

Now, define a mapping which assigns to each point one of the neighborhoods in the subcover to which it belongs:

and set

By definition, these constructions imply

| (B.5) |

As a final step, for each positive integer , we choose a control so that

| (B.6) |

By monotonicity, for every . We now define a composite strategy , which follows the policy satisfying (B.3) until the corresponding state process leaves at time . It then switches to the policy corresponding to the index which the state process is assigned by the mapping :

This construction ensures . Hence, it follows from the definitions of the value function and , (B.6) and (which holds for by definition of ), as well as (B.5) and (B.3) that

Since was arbitrary, this establishes (B.2) and thereby completes the proof.

References

- [1] J. V. Alcala and A. Fahim. Balancing small fixed and proportional transaction cost in trading strategies. Preprint, 2013.

- [2] C. Atkinson and P. Wilmott. Portfolio management with transaction costs: an asymptotic analysis of the Morton and Pliska model. Math. Finance, 5(4):357–367, 1995.

- [3] P. Balduzzi and A. Lynch. Transaction costs and predictability: some utility cost calculations. J. Financ. Econom., 52(1):47–78, 1999.

- [4] G. Barles and B. Perthame. Discontinuous solutions of deterministic optimal stopping time problems. RAIRO Modél. Math. Anal. Numér., 21(4):557–579, 1987.

- [5] D. Bertsimas, L. Kogan, and A. W. Lo. When is time continuous? J. Financ. Econom., 55(2):173–204, 2000.

- [6] M. Bichuch. Asymptotic analysis for optimal investment in finite time with transaction costs. SIAM J. Financial Math., 3(1):433–458, 2011.

- [7] M. Bichuch and S. E. Shreve. Utility maximization trading two futures with transaction costs. SIAM J. Financial Math., 4(1):26–85, 2013.

- [8] B. Bouchard and N. Touzi. Weak dynamic programming principle for viscosity solutions. SIAM J. Control Optim., 49(3):948–962, 2011.

- [9] G. Constantinides. Capital market equilibrium with transaction costs. J. Polit. Econ., 94(4):842–862, 1986.

- [10] M. G. Crandall, H. Ishii, and P.-L. Lions. User’s guide to viscosity solutions of second order partial differential equations. Bull. Amer. Math. Soc., 27(1):1–67, 1992.

- [11] M. H. A. Davis and A. R. Norman. Portfolio selection with transaction costs. Math. Oper. Res., 15(4):676–713, 1990.

- [12] B. Dumas and E. Luciano. An exact solution to a dynamic portfolio choice problem under transaction costs. J. Finance, 46(2):577–595, 1991.

- [13] J. F. Eastham and K. J. Hastings. Optimal impulse control of portfolios. Math. Oper. Res., 13(4):588–605, 1988.

- [14] L. C. Evans. The perturbed test function method for viscosity solutions of nonlinear PDE. Proc. Roy. Soc. Edinburgh Sect. A, 111(3-4):359–375, 1989.

- [15] W. H. Fleming and H. M. Soner. Controlled Markov processes and viscosity solutions. Springer, New York, second edition, 2006.

- [16] M. Fukasawa. Asymptotically efficient discrete hedging. In Stochastic Analysis with Financial Applications, pages 331–346. Springer, 2011.

- [17] M. Fukasawa. Efficient discretization of stochastic integrals. Finance Stoch., to appear, 2013.

- [18] S. Gerhold, P. Guasoni, J. Muhle-Karbe, and W. Schachermayer. Transaction costs, trading volume, and the liquidity premium. Finance Stoch., to appear, 2013.

- [19] J. Goodman and D. N. Ostrov. Balancing small transaction costs with loss of optimal allocation in dynamic stock trading strategies. SIAM J. Appl. Math., 70(6):1977–1998, 2010.

- [20] P. Guasoni and J. Muhle-Karbe. Long horizons, high risk aversion, and endogeneous spreads. Math. Finance, to appear, 2013.

- [21] T. Hayashi and P. A. Mykland. Evaluating hedging errors: an asymptotic approach. Math. Finance, 15(2):309–343, 2005.

- [22] K. Janeček and S. E. Shreve. Asymptotic analysis for optimal investment and consumption with transaction costs. Finance Stoch., 8(2):181–206, 2004.

- [23] Y. M. Kabanov and M. M. Safarian. Markets with transaction costs. Springer, Berlin, 2009.

- [24] J. Kallsen and J. Muhle-Karbe. The general structure of optimal investment and consumption with small transaction costs. Preprint, 2013.

- [25] J. Kallsen and J. Muhle-Karbe. Option pricing and hedging with small transaction costs. Math. Finance, to appear, 2013.

- [26] R. Korn. Portfolio optimisation with strictly positive transaction costs and impulse control. Finance Stoch., 2(2):85–114, 1998.

- [27] H. Liu. Optimal consumption and investment with transaction costs and multiple risky assets. J. Finance, 59(1):289–338, 2004.

- [28] A. W. Lo, H. Mamaysky, and J. Wang. Asset prices and trading volume under fixed transaction costs. J. Polit. Econ., 112(5):1054–1090, 2004.

- [29] A. Lynch and P. Balduzzi. Predictability and transaction costs: the impact on rebalancing rules and behavior. J. Finance, 55(5):2285–2310, 2000.

- [30] A. Lynch and S. Tan. Explaining the magnitude of liquidity premia: the roles of return predictability, wealth shocks, and state dependent transaction costs. J. Finance, 66(4):1329–1368, 2011.

- [31] M. Magill and G. Constantinides. Portfolio selection with transaction costs. J. Econom. Theory, 13:245–263, 1976.

- [32] R. Martin. Optimal multifactor trading under proportional transaction costs. Preprint, 2012.

- [33] A. R. Morton and S. R. Pliska. Optimal portfolio management with fixed transaction costs. Math. Finance, 5(4):337–356, 1995.

- [34] K. Muthuraman and S. Kumar. Multidimensional portfolio optimization with proportional transaction costs. Math. Finance, 16(2):301–335, 2006.

- [35] M. Nutz. Risk aversion asymptotics for power utility maximization. Probab. Theory Relat. Fields, 152(3–4):703–749, 2012.

- [36] B. Øksendal and A. Sulem. Optimal consumption and portfolio with both fixed and proportional transaction costs. SIAM J. Control Optim., 40(6):1765–1790, 2002.

- [37] D. Possamaï, H. M. Soner, and N. Touzi. Homogenization and asymptotics for small transaction costs: the multidimensional case. Preprint, 2012.

- [38] L. C. G. Rogers. Why is the effect of proportional transaction costs ? In Mathematics of Finance, pages 303–308. Amer. Math. Soc., Providence, RI, 2004.

- [39] M. Rosenbaum and P. Tankov. Asymptotically optimal discretization of hedging strategies with jumps. Ann. Appl. Probab., to appear, 2013.

- [40] M. Schroder. Optimal portfolio selection with fixed transaction costs: numerical solutions. Preprint, 1995.

- [41] S. E. Shreve and H. M. Soner. Optimal investment and consumption with transaction costs. Ann. Appl. Probab., 4(3):609–692, 1994.

- [42] H. M. Soner and N. Touzi. Homogenization and asymptotics for small transaction costs. SIAM J. Control Optim., 51(3):2893–2921, 2013.

- [43] A. E. Whalley and P. Wilmott. An asymptotic analysis of an optimal hedging model for option pricing with transaction costs. Math. Finance, 7(3):307–324, 1997.

- [44] R. Zhang. Couverture approchée des options Européennes. PhD thesis, Ecole Nationale des Ponts et Chaussées, 1999.