On the probability density function of baskets

Abstract.

The state price density of a basket, even under uncorrelated Black–Scholes dynamics, does not allow for a closed form density. (This may be rephrased as statement on the sum of lognormals and is especially annoying for such are used most frequently in Financial and Actuarial Mathematics.) In this note we discuss short time and small volatility expansions, respectively. The method works for general multi-factor models with correlations and leads to the analysis of a system of ordinary (Hamiltonian) differential equations. Surprisingly perhaps, even in two asset Black–Scholes situation (with its flat geometry), the expansion can degenerate at a critical (basket) strike level; a phenomena which seems to have gone unnoticed in the literature to date. Explicit computations relate this to a phase transition from a unique to more than one “most-likely” paths (along which the diffusion, if suitably conditioned, concentrates in the afore-mentioned regimes). This also provides a (quantifiable) understanding of how precisely a presently out-of-money basket option may still end up in-the-money.

Key words and phrases:

Sums of lognormals, focality, pricing of butterfly spreads on baskets1. Introduction

As is well known, the sum of independent log-normal variable does not admit a closed-form density. And yet, there are countless applications in Finance and Actuarial Mathematics where such sums play a crucial role, consider for instance the law of a Black–Scholes basket at time , i.e. the weighted average of geometric Brownian motions.

As a consequence, there is a natural interest in approximations and expansions, see e.g. [14] and the references therein. This article contains a detailed investigation in small volatility and short time regimes. Forthcoming work of A. Gulisashvili and P. Tankov [23] deals with tail asymptotics. Our methods are not restricted to the geometric Brownian motion case: in principle, each Black–Scholes component could be replaced by the asset price in a stochastic volatility model, such as the the Stein–Stein model [38], with full correlation between all assets and their volatilities. In the end, explicit solutions only depend on the analytical tractability of a system of ordinary differential equations. If such tractability is not given, one can still proceed with numerical ODE solvers.

As a matter of fact, our aim here is not to push the generality in which our methods work: one can and should expect involved answers in complicated models. Rather, our main – and somewhat surprising – insight is that unexpected phenomena are already present in the simplest possible setting: to this end, our first focus will be on the case of independent Black–Scholes assets, without drift and correlation, with unit spot and unit volatility). To be more specific, if denotes the fair value of an (out-of-money) call option on the basket struck at , one naturally expects, for a small maturity ,

And yet, while true for most strikes, it fails for ; in fact,

To the best of our knowledge, and despite the seeming triviality of the situation (two independent Black–Scholes assets!), the existence of a “special” strike level , at which the value of a basket option (here: butterfly spread111Extensions to spreads and vanilla options are possible and will be discussed elsewhere.) has a “special” decay behavior, as maturity approaches , seems to be new. There are different proofs of this fact; the most elementary argument – based on the analysis of a convolution integral – is given in Section 2. However, this approach – while telling us what happens – does not tell us how it happens.

The main contribution of this note is precisely a good understanding of the latter. In fact, there is clear picture that comes with . For and conditional on the option to expire on the money, there is a unique “most likely” path around which the underlying asset price process will concentrate as maturity approaches . For , however, this ceases to be true: there will be two distinct (here: equally likely) paths around which concentration occurs. What underlies this interpretation is that large deviation theorynot only characterizes the probability of unlikely events (such as expiration in-the-money, if presently out-of-the-money, as time to maturity goes to zero) but also the mechanism via which these events can occur. Such understanding was already crucial in previous works on baskets aiming at quantification of basket (implied vol) skew relative to its components, starting with [1, 2]. As a matter of fact, the analysis in these papers relied on the statement that “generically there is a unique arrival point [of a unique energy minimizing path] on the (basket-strike) arrival manifold”. The situation, however, even in the Black–Scholes model, is more involved. And indeed, we shall establish existence of a critical strike , at which one sees the phase-transition from one to two energy minimizing, “most likely”, paths.222It can be shown that, sufficiently close to the arrival manifold, there is in fact a unique energy minimizing paths. The (near-the-money) analysis of [1, 2] is then justified. And this information will have meaning to traders (as long as they believe in a diffusion model as maturity approaches , which may or may not be a good idea …) as it tells them the possible scenarios in which an out-of-the money basket option may still expire in the money.

Let us conclude this introduction with a few technical notes. We view the evolution of the basket price – even in the Black-Scholes model – as a stochastic volatility evolution model; by which we mean (as opposed to a local vol evolution where ). This should explain why the methods developed in Part I of [10, 11] for the analysis of stochastic volatility models (then used in Part II, [11], to solve the concrete smile problem (shape of the wings) for the correlated Stein–Stein model), are also adequate for the analysis of baskets. In a sense, the present note may well be viewed as Part III in this sequence of papers.

Acknowledgment: Martin Forde kindly informed us about some misleading formulations in a previous version. P.K.F. has received partial funding from the European Research Council under the European Union’s Seventh Framework Program (FP7/2007-2013) / ERC grant agreement nr. 258237.

2. Computations based on saddle-point method

In terms of a standard -dimensional Wiener process ,

Write for the probability density function of ; i.e. for . Of course, it is given by some -dimensional convolution integral, explicit asymptotic expansions are – in principle – possible with the saddle point method. It will be enough for our purposes to illustrate the method in the afore-mentioned simplest possible setting:

In other words, . We claim that for some constant

| (1a) | when , | ||||

| (1b) | when , | ||||

with

and

with

| (2) |

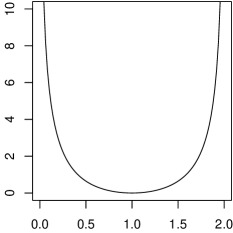

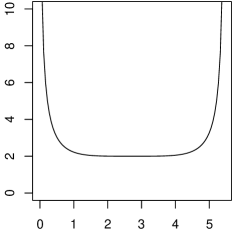

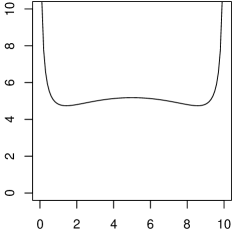

Note that for we can explicitly solve this minimization problem and obtain with corresponding minimizer , corresponding to the single local extremum of . For , we have two global minima, which cannot be given in closed form, and hence can only be computed numerically.

(A) For there is a unique global minimum at which is non-degenerate in the sense that

(B) For there is a unique global minimum at which is degenerate in the sense that

(C) For , gives a local maximum. There are two symmetric global minimizers, which are not given in closed form.

The stock price has a log-normal distribution with parameters and , where the density of the log-normal distribution is given by

| (3) |

Obviously, the density of the sum of these two independent log-normal random variables satisfies

| (4) |

Using our special parameters, the integrand is of the form

In order to apply the Laplace approximation to (4), we compute the minimizer for , which is found by the first order condition

| (5) |

Clearly, this equation is solved by choosing — which is the unique global minimizer iff and a local maximizer otherwise, in which case we have two global minima . Assuming , we can check degeneracy of that minimum directly by computing

and

| (6) |

With more work one can see that also the global minima , in the case , are non-degenerate. Hence, whenever a standard Laplace method leads to the expansion (1a). In the remainder of this section, we consider the degenerate case and establish (1b).

Choosing and, correspondingly, , we obtain the Taylor expansion , with and , we obtain the Laplace approximation

where we used

Thus, we arrive at (1b).

3. Large Deviations approach

Our main tool here are novel marginal density expansions in small-noise regime [10]. This was used in order to compute the large-strike behavior of implied volatility in the correlated Stein–Stein model; [38, 22].333Similar investigations have recently been conducted in the Heston model; [26, 21] and the references therein.

In fact, the technical assumptions of [10] were satisfied in the analysis of the Stein–Stein model whereas in the (seemingly) trivial case of two IID Black-Scholes assets, the technical assumptions of [10] are indeed violated for a critical strike . The necessity of this condition is then highlighted by the fact, as was seen in the previous section,

The computation of can be achieved either via a geometric construction borrowed from Riemannian geometry, which relies on the Weingarten map, or by some (fairly) elementary analysis of a system of Hamiltonian ODEs. In fact, the Hamiltonian point of view extends naturally when one introduces correlation, local and even stochastic volatility. Explicit answers then depend on the analytical tractability of these (boundary value) ODE problems. (Of course, the numerical solution of such problems is well-known.)

In the following, we review [10]. Consider a -dimensional diffusion given by the stochastic differential equation

| (7) |

and where ) is an -dimensional Brownian motion. Unless otherwise stated, we assume and to be smooth, bounded with bounded derivatives of all orders. Set and assume that, for every multi-index , the drift vector fields converges to in the sense444If (7) is understood in Stratonovich sense, so that is replaced by , the drift vector field is changed to . In particular, is also the limit of in the sense of (8) .

| (8) |

We shall also assume that

| (9) |

and

| (10) |

Theorem 1.

(Small noise) Let be the solution process to

Assume in the sense of (8), (9), and as in the sense of (10). Assume non-degeneracy of in the sense that is strictly positive definite everywhere in space. 555This may be relaxed to a weak Hoermander condition with an explicit controllability condition. Fix and let be the the space of all , the Cameron-Martin space of absolutely continuous paths with derivatives in , s.t. the solution to

satisfies . In a neighborhood of , assume smoothness of666If smoothness of the energy can be shown and need not be assumed; [10]. Note also that in our application to tail asymptotics, with -scaling, , the energy must be linear resp. quadratic (by scaling) and hence smooth.

Assume also (i) there are only finitely many minimizers, i.e. where

(ii) is non-focal for in the sense of [10]. (We shall review below how to check this.) Then there exists such that

admits a density with expansion

where denotes the gradient of .

Here is the projection, , of the solution to the following (ordinary) differential equation

| (11) | |||||

Remark 2 (Localization).

The assumptions on the coefficients in theorem 1 (smooth, bounded with bounded derivatives of all orders) are typical in this context (cf. Ben Arous [5, 6] for instance) but rarely met in practical examples from finance. This difficulty can be resolved by a suitable localization. For instance, as detailed in [10], an estimate of the form

| (12) |

with will allow to bypass the boundedness assumptions.

3.1. Short time asymptotics

The reduction of short time expansions to small noise expansions by Brownian scaling is classical. In the present context, we have the following statement, taken from [10, Sec. 2.1].

Corollary 3.

(Short time) Consider , started at , with -bounded vector fields which are non-degenerate in the sense that is strictly positive definite everywhere in space. Fix and assume (i),(ii) as in theorem 1. Let be the density of . Then

where is the sub-Riemannian distance, based on , from the point to the affine subspace .

3.2. Computational aspects

We present here the mechanics of the actual computations, in the spirit of the Pontryagin maximum principle (e.g. [37]). For details we refer to [10].

-

•

The Hamiltonian. Based on the SDE (7), with diffusion vector fields and drift vector field (in the limit) we define the Hamiltonian

Remark the driving Brownian motions were assumed to be independent. Many stochastic models, notably in finance, are written in terms of correlated Brownian motions, i.e. with a non-trivial correlation matrix , where . The Hamiltonian then becomes

(13) -

•

The Hamiltonian ODEs. The following system of ordinary differential equations,

(14) gives rise to a solution flow, denoted by , so that

is the unique solution to the above ODE with initial data . Our standing (regularity) assumption are more than enough to guarantee uniqueness and local ODE existence. As in [8, p.37], the vector field is complete, i.e., one has global existence. It can be useful to start the flow backwards with time- terminal data, say ; we then write

for the unique solution to (14) with given time- terminal data. Of course,

-

•

Solving the Hamiltonian ODEs as boundary value problem. Given the target manifold , the analysis in [10] requires solving the Hamiltonian ODEs (14) with mixed initial -, terminal - and transversality conditions,

(15) Note that this is a -dimensional system of ordinary differential equations, subject to conditions. In general, boundary problems for such ODEs may have more than one, exactly one or no solution. In the present setting, there will always be one or more than one solution. After all, we know by [10] that there exists at least one minimizing control and that can be reconstructed via the solution of the Hamiltonian ODEs, as explained in the following step.

-

•

Finding the minimizing controls. The Hamiltonian ODEs, as boundary value problem, are effectively first order conditions (for minimality) and thus yield candidates for the minimizing control , given by

(16) Each such candidate is indeed admissible in the sense but may fail to be a minimizer. We thus compute the energy for each candidate and identify those (“”) with minimal energy. The procedure via Hamiltonian flows also yields a unique . If – as in our case – the energy is equal to , otherwise the formula is slightly more complicated.

-

•

Checking non-focality. By definition [10], is non-focal for along in the sense that, with ,

is non-degenerate (as matrix; here we think of and recall that denotes the projection from onto ; in coordinates ). Note that in the point-point setting, is fixed and only perturbations of the arrival ”velocity” - without restrictions, i.e. without transversality condition - are considered. Non-degeneracy of the resulting map should then be called non-conjugacy (between two points; here: and ). In the absence of the drift vector field , this is consistent with the usual meaning of non-conjugacy; after identifying tangent- and cotangent-space is precisely the differential of the exponential map.

-

•

The explicit marginal density expansion. We then have

with . The second-order exponential constant then requires the solution of a finitely many ( ) auxiliary ODEs, cf. theorem 1.

4. Analysis of the Black–Scholes basket

For a general multi-dimensional Black-Scholes model, we have a Hamiltonian

with . While the corresponding Hamiltonian ODEs can be solved in closed form, the boundary conditions lead to systems of non-linear equations, which we cannot solve explicitly any more. While numerical solutions are, of course, possible, we restrict ourselves to the extremely simple setting of Section 2, in order to keep maximal tractability.

Consequently, we have the Hamiltonian . The solutions of the Hamiltonian ODEs started at satisfy

| (17) |

which can be easily seen from the observation that is constant along solutions of the Hamiltonian ODEs together with symmetry between and . This immediately implies that the inverse flow is given by

| (18) |

Now we introduce the boundary conditions. Note that, contrary to Theorem 1, we now project to the linear subspace . Thus, the terminal condition on translates into – we need to end at the target manifold –, whereas the transversality condition translates to being orthogonal to the target manifold. Evaluating these conditions at , we get

It is a pleasant exercise to check that solving for and then leads exactly to the first order condition (5) encountered in Section 2. With identical arguments, assuming from here on (and disregarding the case where closed form computations are not available), we find that the optimal configuration must satisfy . Inserting this value into the first two components of (17), we obtain the equation

This implies that . Moreover, we see that the minimizing control satisfies

| (19) |

see (16), implying that the minimal energy is given by

| (20) |

Regarding focality, we have to check that the matrix:

| (21) |

is non-degenerate when evaluated at the optimal configuration . A simple calculation shows that

implying that

and we can conclude that

which is zero if and only if . We summarize the results of this calculation as follows:

- •

- •

Remark 4.

It is immediate to use this analysis to deal also with the case of non-unit (but identical) spots by scaling the Black-Scholes dynamics accordingly, i.e., by replacing with . Hence, in this case focality happens when , i.e., when .

5. Extensions: correlation, local and stochastic vol

5.1. Analysis of the Black–Scholes basket, small noise

In section 4 we analyzed the density of a simple Black–Scholes basket with dynamics

As explained in Section 3 the analysis is really based on a small noise (small vol) expansion of

run til time . Consider now a situation with small rates, also of order . In other words,

and then as before. We still assume . A look at Theorem 1 (now we cannot use Corollary 3) reveals that the entire leading order computation remains unchanged (at least at unit time and with trivial changes otherwise). The resulting (now: small noise) density expansion of is more involved and takes the form

| (22) |

Here is given in closed form, cf. (20), so that is also explicitly known. Furthermore, under similar restrictions on as before, is (still) given by (19), so that

Thus, the ODE for (see Theorem 1) is given by

which has the solution

implying that . Thus, the second exponential term has the form given above.

5.2. Basket analysis under local, stochastic vol etc.

One can immediately write down the Hamiltonian associated to, say two, or assets, each of which is governed by local vol dynamics or stochastic vol, based on additional factors. In general, however, one will be stuck with the analysis of the resulting boundary value problem for the Hamiltonian ODEs; numerical (e.g. shooting) methods will have to be used. In some models, including the Stein–Stein model, we believe (due to the analysis carried out in [11]) that, in special cases, closed form answers are possible but we will not pursue this here. Instead, we continue with a few more computation in the Black–Scholes case for assets.

5.3. Multi-variate Black-Scholes models

In the multi-variate case of a general, -dimensional Black Scholes model with correlation matrix , the Hamiltonian has the form

Thus, the Hamiltonian ODEs have the form

Consequently, it is again easy to see that , implying that . The Hamiltonian flow has the form

| (23) |

Using again that for any , we obtain the inverse Hamiltonian flow

| (24) |

The boundary conditions – at – are now given by

| (25a) | |||

| (25b) | |||

| (25c) | |||

Indeed, the transversality condition (25c) says that the final momentum is orthogonal to the surface , whose tangent space is spanned by the collection of vectors , , with the standard basis of . The equations (25) are certainly not difficult to solve numerically, but an explicit solution is not available, neither in the general case nor in the case of uncorrelated assets.

Remark 6.

The main point of this calculation is that while explicit solutions are no longer possible in a general Black-Scholes model, the phenomenon (1) potentially appears in all Black-Scholes models. Moreover, we stress that the non-focality conditions are easily checked numerically.

Remark 7.

Note that the discretely monitored Asian option can be considered as a special case of a basket option on correlated assets. Indeed, let us consider an option on

For each individual we have, for fixed , the equality in law

for and . In law, the vector corresponds to the marginal distribution of an -dimensional Brownian motion at time with correlation , . Thus, the Asian option corresponds to an option on the basket with , as above and a correlation matrix with maturity . Moreover, the asymptotic expansion of the price of the Asian option as corresponds to the short-time asymptotics of the basket.

Remark 8.

As in the two-dimensional case, the boundary conditions can be solved explicitly in the fully symmetric case, when and, say, . For suitable the optimal configuration is

Introducing

we obtain (for the case of uncorrelated assets)

where , , with

In the symmetric case, we can evaluate at the optimal configuration and obtain

whose determinant can be seen to be

Thus, the non-focality condition fails if and only if . Moreover, we obtain the energy

6. A geometric approach to focality

In this final section we take a more geometrical look at the non-focality condition appearing in Section 3.2. Consider the Black Scholes model

We change parameters , by

where denotes the correlation matrix of and its Cholesky factorization. Obviously, . In terms of the -coordinates we have

The advantage of using the chart is that the corresponding Riemannian metric tensor is the usual Euclidean metric tensor. Thus, we simply have

and the geodesics are straight lines as seen from the -chart. Note furthermore that is transformed to .

The payoff function of the option is given by . We normalize and . The strike surface , which is (a sub-set of) a hyperplane in coordinates is, however, transformed to a much more complicated submanifold in coordinates. Re-phrasing the equation in -coordinates and solving for gives

with , which implies – using that and are lower-triangular matrices –

For sake of clarity, let us introduce the notation . A parametrization of the strike surface is then given by the map with

and

Note that by the change of coordinates, we are implicitly assuming that for all . Moreover, the standard basis of the tangent space to at is given by the columns of the Jacobi matrix of evaluated at , more precisely we have

for and . Consequently, the normal vector field to at is given by

where is a normalization factor guaranteeing that , i.e.,

The Weingarten map or shape operator is defined by

, see [13]. In other words, for , we interpret as a map in and is the directional derivative of that map. We study the Weingarten map since it gives us the curvature of the surface . Indeed, the eigenvalues of the linear map are called principal curvatures of . Then the focal points of at are given by

In order to compute the eigenvalues of the shape operator, we need to compute the representation of in the standard basis . Let us denote this matrix by , then we obviously have

The principal curvatures are, thus, the eigenvalues of the -dimensional matrix .

Since the calculations become too complicated in the general case, we now again concentrate on the case of two uncorrelated assets, i.e., and . In this case, we have

Thus, the Weingarten map is given by

where for

is the curvature of the curve in . We see that if and only if , i.e., at the boundary of the surface . Otherwise, is negative.

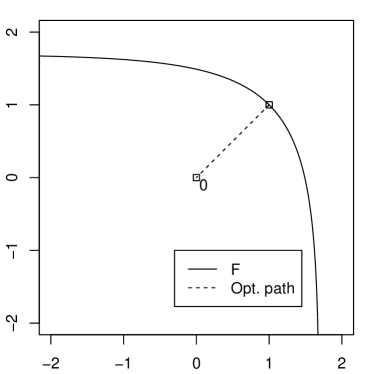

Here, both components of are positive on . Consequently, for any there is precisely one focal point , which is given by

Denoting and re-introducing the short-cut notation , , (noting that ) we can express as

In the current setting, let be the optimal configuration in -coordinates, i.e., the point on with smallest Euclidean norm. Then the non-focality condition of Theorem 1 is satisfied, if is not a focal point to , see the discussion in the proof of [10, Prop. 6].

Remark 9.

As both components of the normal vector are non-negative on and the curvature is negative, can only be a focal point if has a non-empty intersection with the positive quadrant. Inserting into the parametrization of , we see that this can only be the case if . In other words: if the option is in the money, then the non-focality condition is always satisfied (in the two-dimensional, uncorrelated case).

Let us again use the parameters of Section 2, i.e., , . Then we consider , which translates into . Inserting into the formulas for the focal points, we obtain

So, is focal to the optimal configuration, if and only if

and we recover, once more, the results of Section 2 and Section 4 – recall that corresponds to in -coordinates.

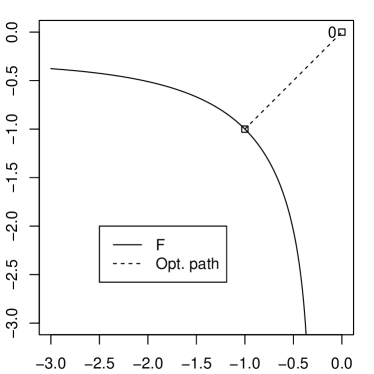

(A) The dashed line depicts the optimal path between the spot price ( in the -chart) and the optimal configuration.

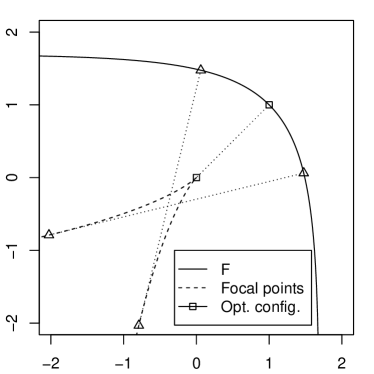

(B) Dotted lines connect some selected points on the manifold with the corresponding focal points. Points marked with a triangle visualize the construction of the focal points. We see that is, indeed, focal to the optimal configuration.

(A) The dashed line depicts the optimal path between the spot price ( in the -chart) and the optimal configuration.

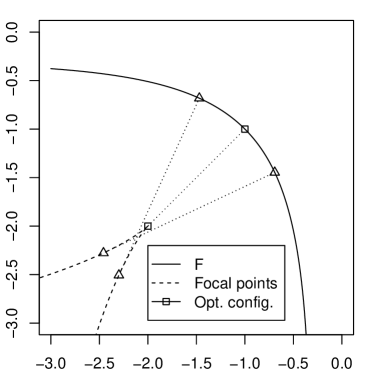

(B) Dotted lines connect some selected points on the manifold with the corresponding focal points. Points marked with a triangle visualize the construction of the focal points. This example illustrates the fact that the non-focality condition always holds when the basket option is in the money.

In Figure 2 and 3 the focal points are visualized for two different configurations of two uncorrelated baskets. We plot the surface as a submanifold of . We have seen above that for any there is precisely one focal point . Hence, we additionally plot the surface – more precisely, part of this surface. In Figure 2 we show the case constructed above where the non-focality condition is violated. In Figure 3 the option is ITM. As explained above, in the ITM case the manifold does not intersect the positive quadrant, implying that the non-focality condition is satisfied.

References

- [1] M. Avellaneda, D. Boyer-Olson, J.Busca, P. Friz: Application of large deviation methods to the pricing of index options in finance, Comptes Rendus de l’Académie des Sciences - Series I - Mathematique (2003).

- [2] M. Avellaneda, D. Boyer-Olson, J.Busca, P. Friz: Reconstructing volatility, RISK (2004).

- [3] C. Bayer and P. Laurence, Asymptotics beats Monte-Carlo: the case of correlated local vol baskets. Forthcoming in Communications on Pure and Applied Mathematics.

- [4] Benaim, Friz: Regular Variation and Smile Asymptotics, Math. Finance Vol. 19 no 1. (2009), 1-12

- [5] G. Ben Arous. Développement asymptotique du noyau de la chaleur hypoelliptique hors du cut-locus. Annales Scientifiques de l’Ecole Normale Supérieure, 4 (21): 307-331, 1988.

- [6] G. Ben Arous. Methods de Laplace et de la phase stationnaire sur l’espace de Wiener. Stochastics, 25: 125-153, 1988.

- [7] H. Berestycki, J. Busca, and I. Florent. Computing the implied volatility in stochastic volatility models. Communications on Pure and Applied Mathematics, 57(10):1352-1373, 2004.

- [8] J.M. Bismut. Malliavin Calculus and Large Deviations. 1984

- [9] S. de Marco, P.K. Friz. Varadhan’s formula for projected diffusion and local volatility. Preprint 2013.

- [10] J.D. Deuschel, P.K. Friz, A. Jacquier, S. Violante. Marginal density expansions for diffusions and stochastic volatility, part I: Theoretical Foundations. Communications on Pure and Applied Mathematics, to appear.

- [11] J.D. Deuschel, P.K. Friz, A. Jacquier, S. Violante. Marginal density expansions for diffusions and stochastic volatility, part II: Applications. Communications on Pure and Applied Mathematics, to appear.

- [12] J.D. Deuschel and D.W. Stroock. Large Deviations. Volume 342 of AMS/Chelsea Series. 2000

- [13] M.P. do Carmo. Differential geometry of curves and surfaces. Prentice-Hall, 1976.

- [14] D. Dufresne, The log-normal approximation in financial and other computations, Advances in Applied Probability 36, pgs 747-773, 2004.

- [15] M. Freidlin and A.D. Wentzell. Random perturbations of dynamical systems. Grundlehren der Mathematischen Wissenschaften (Second edition ed.). New York: Springer-Verlag, 1998.

- [16] P. Friz, S. Gerhold, A. Gulisashvili and S. Sturm. Refined implied volatility expansions in the Heston model. Quant. Finance, Volume 11, Issue 8, 1151-1164, 2011.

- [17] K. Gao and R. Lee. Asymptotics of implied volatility to arbitrary order. Preprint available at http://ssrn.com/abstract=1768383, 2011.

- [18] Gatheral, Jim; The Volatilty Surface. Wiley Finance, 2006.

- [19] Gatheral, Jim; Further Developments in Volatility Derivatives Modeling. Presentation 2008. Available on www.math.nyu.edu/fellows_fin…/gatheral/FurtherVolDerivatives2008.pdf

- [20] Gatheral, Jim; Hsu, Elton P.; Laurence, Peter; Ouyang, Cheng; Wang, Tai-Ho. Asymptotics of Implied Vol in Local Vol Models. Math. Finance, Volume 22, Issue 4, pages 591–620, October 2012.

- [21] A. Gulisashvili. Analytically tractable stochastic stock price models, Springer finance, Springer London 2012.

- [22] A. Gulisashvili and E. Stein. Asymptotic Behavior of the Stock Price Distribution Density and Implied Volatility in Stochastic Volatility Models, Applied Mathematics & Optimization, Volume 61, Number 3, 287-315, DOI: 10.1007/s00245-009-9085-x

- [23] A. Gulisashvili and P. Tankov. Tail behavior of sums and differences of log-normal random variables, Preprint 2013.

- [24] Patrick Hagan, Andrew Lesniewski, and Diana Woodward; Probability Distribution in the SABR Model of Stochastic Volatility. Forthcoming in these Proceedings.

- [25] Henry-Labordère P, Analysis, geometry and modeling in finance, Chapman and Hill/CRC, 2008.

- [26] Heston S. 1993. A closed-form solution for options with stochastic volatility, with application to bond and currency options. Review of Financial Studies 6, 327–343.

- [27] Shigeo Kusuoka and Yasufumi Osajima: A remark on the asymptotic expansion of density function of Wiener functionals. UTMS Preprint 2007-18.

- [28] Roger Lee. The Moment Formula for Implied Volatility at Extreme Strikes, Mathematical Finance, vol 14 issue 3 (July 2004), 469-480.

- [29] P.L. Lions and M. Musiela. Correlations and bounds for stochastic volatility models. Ann. I.H. Poincaré, 24, 2007, 1-16.

- [30] Alex Lipton and Artur Sepp, Stochastic volatility models and Kelvin waves. 2008, J. Phys. A: Math. Theor. 41.

- [31] S A Molchanov, ”Diffusion processes and Riemannian geometry”, Russ. Math. Surv., 1975, 30 (1), 1–63.

- [32] R. Montgomery. A Tour of SubRiemannian Geometries, their Geodesics and Applications, Volume 91 of Mathematical Surveys and Monographs. American Mathematical Society, Providence, RI, 2002.

- [33] Osajima, Yasufumi, General Asymptotics of Wiener Functionals and Application to Mathematical Finance (July 25, 2007). Available at SSRN: http://ssrn.com/abstract=1019587

- [34] Huyen Pham, Large deviations in Finance, 2010, Third SMAI European Summer School in Financial Mathematics.

- [35] V. Piterbarg, Markovian projection method for volatility calibration; RISK (2007).

- [36] Sakai, T.: Riemannian Geometry, AMS, 1992.

- [37] Seierstad, A. and Sydsaeter, K.: Optimal Control Theory with Economic Applications. (Advanced Textbooks in Economics, 24). North- Holland Amsterdam, 1987

- [38] Stein, E. M., and J. C. Stein, 1991, “Stock Price Distributions with Stochastic Volatility: An Analytic Approach,” Review of Financial Studies, 4, 727-752.

- [39] Takanobu S. Watanabe S.: Asymptotic expansion formulas of the Schilder type for a class of conditional Wiener functional integration. In Asymptotics problems in probability theory: Wiener functionals and asymptotics . K.D. Elworthy N. Ikeda edit. Pitman. Res. Notes. Math. Series. 284 (1993), 194-241.

- [40] Varadhan, S. R. S., On the behavior of the fundamental solution of the heat equation with variable coefficients. Communications on Pure and Applied Mathematics, 20: 431–455. 1967