Optimal parameter selection for the alternating direction method of multipliers (ADMM): quadratic problems

Abstract

The alternating direction method of multipliers (ADMM) has emerged as a powerful technique for large-scale structured optimization. Despite many recent results on the convergence properties of ADMM, a quantitative characterization of the impact of the algorithm parameters on the convergence times of the method is still lacking. In this paper we find the optimal algorithm parameters that minimize the convergence factor of the ADMM iterates in the context of -regularized minimization and constrained quadratic programming. Numerical examples show that our parameter selection rules significantly outperform existing alternatives in the literature.

I Introduction

The alternating direction method of multipliers is a powerful algorithm for solving structured convex optimization problems. While the ADMM method was introduced for optimization in the 1970’s, its origins can be traced back to techniques for solving elliptic and parabolic partial difference equations developed in the 1950’s (see [1] and references therein). ADMM enjoys the strong convergence properties of the method of multipliers and the decomposability property of dual ascent, and is particularly useful for solving optimization problems that are too large to be handled by generic optimization solvers. The method has found a large number of applications in diverse areas such as compressed sensing [2], regularized estimation [3], image processing [4], machine learning [5], and resource allocation in wireless networks [6]. This broad range of applications has triggered a strong recent interest in developing a better understanding of the theoretical properties of ADMM[7, 8, 9].

Mathematical decomposition is a classical approach for parallelizing numerical optimization algorithms. If the decision problem has a favorable structure, decomposition techniques such as primal and dual decomposition allow to distribute the computations on multiple processors[10, 11]. The processors are coordinated towards optimality by solving a suitable master problem, typically using gradient or subgradient techniques. If problem parameters such as Lipschitz constants and convexity parameters of the cost function are available, the optimal step-size parameters and associated convergence rates are well-known (e.g., [12]). A drawback of the gradient method is that it is sensitive to the choice of the step-size, even to the point where poor parameter selection can lead to algorithm divergence. In contrast, the ADMM technique is surprisingly robust to poorly selected algorithm parameters: under mild conditions, the method is guaranteed to converge for all positive values of its single parameter. Recently, an intense research effort has been devoted to establishing the rate of convergence of the ADMM method. It is now known that if the objective functions are strongly convex and have Lipschitz-continuous gradients, then the iterates produced by the ADMM algorithm converge linearly to the optimum in a certain distance metric e.g. [7]. The application of ADMM to quadratic problems was considered in [9] and it was conjectured that the iterates converge linearly in the neighborhood of the optimal solution. It is important to stress that even when the ADMM method has linear convergence rate, the number of iterations ensuring a desired accuracy, i.e. the convergence time, is heavily affected by the choice of the algorithm parameter. We will show that a poor parameter selection can result in arbitrarily large convergence times for the ADMM algorithm.

The aim of the present paper is to contribute to the understanding of the convergence properties of the ADMM method. Specifically, we derive the algorithm parameters that minimize the convergence factor of the ADMM iterations for two classes of quadratic optimization problems: -regularized quadratic minimization and quadratic programming with linear inequality constraints. In both cases, we establish linear convergence rates and develop techniques to minimize the convergence factors of the ADMM iterates. These techniques allow us to give explicit expressions for the optimal algorithm parameters and the associated convergence factors. We also study over-relaxed ADMM iterations and demonstrate how to jointly choose the ADMM parameter and the over-relaxation parameter to improve the convergence times even further. We have chosen to focus on quadratic problems, since they allow for analytical tractability, yet have vast applications in estimation [13], multi-agent systems [14] and control[15]. Furthermore, many complex problems can be reformulated as or approximated by QPs [16], and optimal ADMM parameters for QP’s can be used as a benchmark for more complex ADMM sub-problems e.g. -regularized problems [1]. To the best of our knowledge, this is one of the first works that addresses the problem of optimal parameter selection for ADMM. A few recent papers have focused on the optimal parameter selection of ADMM algorithm for some variations of distributed convex programming subject to linear equality constraints e.g. [17, 18].

The paper is organized as follows. In Section II, we derive some preliminary results on fixed-point iterations and review the necessary background on the ADMM method. Section III studies -regularized quadratic programming and gives explicit expressions for the jointly optimal step-size and acceleration parameter that minimize the convergence factor. We then shift our focus to the quadratic programming with linear inequality constraints and derive the optimal step-sizes for such problems in Section IV. We also consider two acceleration techniques and discuss inexpensive ways to improve the speed of convergence. Our results are illustrated through numerical examples in Section V. In Section V we perform an extensive Model Predictive Control (MPC) case study and evaluate the performance of ADMM with the proposed parameter selection rules. A comparison with an accelerated ADMM method from the literature is also performed. Final remarks and future directions conclude the paper.

I-A Notation

We denote the set of real numbers with and define the set of positive (nonnegative) real numbers as (). Let be the set of real symmetric matrices of dimension . The set of positive definite (semi-definite) matrices is denoted by (). With and , we symbolize the identity matrix and the identity matrix of a dimension , respectively.

Given a matrix , let be the null-space of and denote the range space of by . We say the nullity of is (of zero dimensional) when only contains . The transpose of is represented by and for with full-column rank we define as the pseudo-inverse of . Given a subspace , denotes the orthogonal projector onto , while denotes the orthogonal complement of .

For a square matrix with an eigenvalue we call the space spanned by all the eigenvectors corresponding to the eigenvalue the -eigenspace of . The -th smallest in modulus eigenvalue is indicated by . The spectral radius of a matrix is denoted by . The vector (matrix) -norm is denoted by and is the Euclidean (spectral) norm of its vector (matrix) argument. Given a subspace and a matrix , denote as the spectral norm of restricted to the subspace .

Given , the diagonal matrix with and for is denoted by . Moreover, denotes the element-wise inequality, corresponds to the element-wise absolute value of , and is the indicator function of the positive orthant defined as for and otherwise.

Consider a sequence converging to a fixed-point . The convergence factor of the converging sequence is defined as

| (1) |

The sequence is said to converge Q-sublinearly if , Q-linearly if , and Q-superlinearly if . Moreover, we say that convergence is R-linear if there is a nonnegative scalar sequence such that for all and converges Q-linearly to [19] 111The letters Q and R stand for quotient and root, respectively.. In this paper, we omit the letter Q while referring the convergence rate.

Given an initial condition such that , we define the -solution time as the smallest iteration count to ensure that holds for all . For linearly converging sequences with the -solution time is given by . If the -solution time is finite for all , we say that the sequence converges in finite time. As for linearly converging sequences , the -solution time is reduced by minimizing .

II Background and preliminaries

This section presents preliminary results on fixed-point iterations and the ADMM method.

II-A Fixed-point iterations

Consider the following iterative process

| (2) |

where and . Assume has eigenvalues at and let be a matrix whose columns span the -eigenspace of so that .

Next we determine the properties of such that, for any given starting point , the iteration in (2) converges to a fixed-point that is the projection of the into the -eigenspace of , i.e.

| (3) |

Proposition 1

The iterations (2) converge to a fixed-point in if and only if

| (4) |

Proof:

The result is an extension of [20, Theorem 1] for the case of -eigenspace of with dimension . The proof is similar to this citation and is therefore omitted. ∎

Proposition 1 shows that when , the fixed-point iteration (2) is guaranteed to converge to a point given by (3) if all the non-unitary eigenvalues of have magnitudes strictly smaller than 1. From (2) one sees that

Hence, the convergence factor of (2) is the modulus of the largest non-unit eigenvalue of .

II-B The ADMM method

The ADMM algorithm solves problems of the form

| (7) |

where and are convex functions, , , , and ; see [1] for a detailed review.

Relevant examples that appear in this form are, e.g. regularized estimation, where is the estimator loss and is the regularization term, and various networked optimization problems, e.g. [21, 1]. The method is based on the augmented Lagrangian

and performs sequential minimization of the and variables followed by a dual variable update:

| (8) | ||||

for some arbitrary , , and . It is often convenient to express the iterations in terms of the scaled dual variable :

| (12) |

ADMM is particularly useful when the - and -minimizations can be carried out efficiently, for example when they admit closed-form expressions. Examples of such problems include linear and quadratic programming, basis pursuit, -regularized minimization, and model fitting problems to name a few (see [1] for a complete discussion). One advantage of the ADMM method is that there is only a single algorithm parameter, , and under rather mild conditions, the method can be shown to converge for all values of the parameter; see [1, 22] and references therein. As discussed in the introduction, this contrasts the gradient method whose iterates diverge if the step-size parameter is chosen too large. However, has a direct impact on the convergence factor of the algorithm, and inadequate tuning of this parameter can render the method slow. The convergence of ADMM is often characterized in terms of the residuals

| (13) | ||||

| (14) |

termed the primal and dual residuals, respectively [1]. One approach for improving the convergence properties of the algorithm is to also account for past iterates when computing the next ones. This technique is called relaxation and amounts to replacing with in the - and -updates [1], yielding

| (15) | ||||

The parameter is called the relaxation parameter. Note that letting for all recovers the original ADMM iterations (12). Empirical studies show that over-relaxation, i.e. letting , is often advantageous and the guideline has been proposed [23].

III Optimal convergence factor for -regularized quadratic minimization

Regularized estimation problems

where are abound in statistics, machine learning, and control. In particular, -regularized estimation where is quadratic and , and sum of norms regularization where is quadratic, , and , have recently received significant attention [24]. In this section we will focus on -regularized estimation, where is quadratic and , i.e.

| (18) |

for , and constant regularization parameter . While these problems can be solved explicitly and do not motivate the ADMM machinery per se, they provide insight into the step-size selection for ADMM and allow us to compare the performance of an optimally tuned ADMM to direct alternatives (see Section V).

III-A Standard ADMM iterations

The standard ADMM iterations are given by

| (22) |

The -update implies that , so the -update can be re-written as

Hence, to study the convergence of (22) one can investigate how the errors associated with or vanish. Inserting the -update into the -update and using the fact that , we find

| (23) |

Let be a fixed-point of (23), i.e. . The dual error then evolves as

| (24) |

A direct analysis of the error dynamics (24) allows us to characterize the convergence of (22):

Theorem 1

For all values of the step-size and regularization parameter , both and in the ADMM iterations (22) converge to , the solution of optimization problem (18). Moreover, converges at linear rate for all . The pair of the optimal constant step-size and convergence factor are given as

| (25) |

Proof:

See appendix for this and the rest of the proofs. ∎

Corollary 1

Remark 1

Note that the convergence factors in Theorem 1 and Corollary 1 are guaranteed for all initial values, and that iterates generated from specific initial values might converge even faster. Furthermore, the results focus on the dual error. For example, in Algorithm (22) with and initial condition , , the -iterates converge in one iteration since . However, the constraint in (18) is not satisfied and a straightforward calculation shows that . Thus, although for , the dual residual decays linearly with a factor of .

Remark 2

The analysis above also applies to the more general case with cost function where . A change of variables is then applied to transform the problem into the form (18) with , , and .

III-B Over-relaxed ADMM iterations

The over-relaxed ADMM iterations for (18) can be found by replacing by in the and -updates of (22). The resulting iterations take the form

| (29) |

The next result demonstrates that in a certain range of it is possible to obtain a guaranteed improvement of the convergence factor compared to the classical iterations (22).

Theorem 2

Consider the -regularized quadratic minimization problem (18) and its associated over-relaxed ADMM iterations (29). For all positive step-sizes and all relaxation parameters , the iterates and converge to the solution of (18). Moreover, the dual variable converges at linear rate and the convergence factor is strictly smaller than that of the classical ADMM algorithm (22) if The jointly optimal step-size, relaxation parameter, and the convergence factor are given by

| (30) |

With these parameters, the ADMM iterations converge in one iteration.

IV Optimal convergence factor for quadratic programming

In this section, we consider a quadratic programming (QP) problem of the form

| (33) |

where , , is full rank and .

IV-A Standard ADMM iterations

The QP-problem (33) can be put on ADMM standard form (7) by introducing a slack vector and putting an infinite penalty on negative components of , i.e.

| (36) |

The associated augmented Lagrangian is

where , which leads to the scaled ADMM iterations

| (40) |

To study the convergence of (40) we rewrite it in an equivalent form with linear time-varying matrix operators. To this end, we introduce a vector of indicator variables such that if and if . From the - and - updates in (40), one observes that , i.e. . Hence, means that at the current iterate, the slack variable in (36) equals zero; i.e., the inequality constraint in (33) is active. We also introduce the variable vector and let so that and . Now, the second and third steps of (40) imply that where and returns the signs of the elements of its vector argument. Hence, (40) becomes

| (44) |

where the -update follows from the observation that

| (47) |

Since the -iterations will be central in our analysis, we will develop them further. Inserting the expression for from the first equation of (44) into the second, we find

| (48) |

Noting that and introducing

| (49) |

we obtain

| (50) |

We now relate and to the primal and dual residuals, and , defined in (13) and (14):

Proposition 2

Consider and the primal and dual residuals of the QP-ADMM algorithm (40) and auxiliary variables and . The following relations hold

| (51) | |||

| (52) |

| (53) | ||||

| (54) |

where

-

(i)

and , if has full column-rank;

-

(ii)

and , if has full row-rank;

-

(iii)

and , if is invertible.

The next theorem guarantees that (50) convergence linearly to zero in the auxiliary residuals (51) which implies R-linear convergence of the ADMM algorithm (40) in terms of the primal and dual residuals. The optimal step-size and the smallest achievable convergence factor are characterized immediately afterwards.

Theorem 3

Theorem 4

Although the convergence result of Theorem 3 holds for all QPs of the form (33), optimality of the step-size choice proposed in Theorem 4 is only established for problems where the constraint matrix has full row-rank or it is invertible. However, as shown next, the convergence factor can be arbitrarily close to when rows of are linearly dependent.

Theorem 5

Define variables

and .

The convergence factor of the residual is lower bounded by

| (56) |

Furthermore, given an arbitrarily small and , we have the following results:

-

(i)

the inequality holds for all if and only if the nullity of is zero;

-

(ii)

when the nullity of is nonzero and , it holds that ;

-

(iii)

when the nullity of is nonzero, , and , it follows that .

The previous result establishes that slow convergence can occur locally for any value of when the nullity of is nonzero and is small. However, as section (ii) of Theorem 5 suggests, in these cases, (55) can still work as a heuristic to reduce the convergence time if is taken as the smallest nonzero eigenvalue of . In Section V, we show numerically that this heuristic performs well with different problem setups.

IV-B Over-relaxed ADMM iterations

Consider the relaxation of (40) obtained by replacing in the - and -updates with . The corresponding relaxed iterations read

| (60) |

In next, we study convergence and optimality properties of these iterations. We observe:

Like the analysis of (40), introduce and with if and otherwise. Adding the second and the third step of (60) yields . Moreover, satisfies and , so (60) can be rewritten as

| (64) |

where . Defining and substituting the expression for in (64) into the expression for yields

| (65) |

As in the previous section, we replace by in (65) and form :

| (66) |

The next theorem characterizes the convergence rate of the relaxed ADMM iterations.

Theorem 6

Next, we restrict our attention to the case where is either invertible or full row-rank to be able to derive the jointly optimal step-size and over-relaxation parameter, as well as an explicit expression for the associated convergence factor. The result shows that the over-relaxed ADMM iterates can yield a significant speed up compared to the standard ADMM iterations.

Theorem 7

Consider the QP (33) and the corresponding relaxed ADMM iterations (60). If the constraint matrix is of full row-rank or invertible then the joint optimal step-size, relaxation parameter and the convergence factor with respect to the residual are

| (68) | ||||

Moreover, when the iterations (66) are over-relaxed; i.e. their iterates have a smaller convergence factor than that of (50).

IV-C Optimal constraint preconditioning

In this section, we consider another technique to improve the convergence of the ADMM method. The approach is based on the observation that the optimal convergence factors and from Theorem 4 and Theorem 7 are monotone increasing in the ratio . This ratio can be decreased –without changing the complexity of the ADMM algorithm (40)– by scaling the equality constraint in (36) by a diagonal matrix , i,e., replacing by . Let , , and . The resulting scaled ADMM iterations are derived by replacing , , and in (40) and (60) by the new variables , , and , respectively. Furthermore, the results of Theorem 4 and Theorem 7 can be applied to the scaled ADMM iterations in terms of new variables. Although these theorems only provide the optimal step-size parameters for the QP when the constraint matrices are invertible or have full row-rank, we use the expressions as heuristics when the constraint matrix has full column-rank. Hence, in the following we consider and to be the largest and smallest nonzero eigenvalues of , respectively and minimize the ratio in order to minimize the convergence factors and . A similar problem was also studied in [25, 26].

Theorem 8

Let be the Choleski factorization of and be a matrix whose columns are orthonormal vectors spanning with being the dimension of and let and be the largest and smallest nonzero eigenvalues of . The diagonal scaling matrix that minimizes the eigenvalue ratio can be obtained by solving the convex problem

| (69) |

and setting .

So far, we characterized the convergence factor of the ADMM algorithm based on general properties of the sequence . However, if we a priori know which constraints will be active during the ADMM iterations, our parameter selection rules (55) and (68) may not be optimal. To illustrate this fact, we will now analyze the two extreme situations where no and all constraints are active in each iteration and derive the associated optimal ADMM parameters.

IV-D Special cases of quadratic programming

The first result deals with the case where the constraints of (33) are never active. This could happen, for example, if we use the constraints to impose upper and lower bounds on the decision variables, and use very loose bounds.

Proposition 3

The next proposition addresses another extreme scenario when the ADMM iterates are operating on the active set of the quadratic program (33).

Proposition 4

It is worthwhile to mention that when (33) is defined so that its constraints are active (inactive) then the () residuals of the ADMM algorithm remain zero for all updates.

V Numerical examples

In this section, we evaluate our parameter selection rules on numerical examples. First, we illustrate the convergence factor of ADMM and gradient algorithms for a family of -regularized quadratic problems. These examples demonstrate that the ADMM method converges faster than the gradient method for certain ranges of the regularization parameter , and slower for other values. Then, we consider QP-problems and compare the performance of the over-relaxed ADMM algorithm with an alternative accelerated ADMM method presented in [27]. The two algorithms are also applied to a Model Predictive Control (MPC) benchmark where QP-problems are solved repeatedly over time for fixed matrices and but varying vectors and .

V-A -regularized quadratic minimization via ADMM

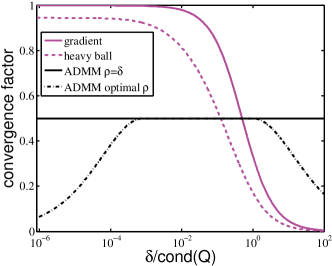

We consider -regularized quadratic minimization problem (1) for a with condition number and for a range of regularization parameters . Fig. 1 shows how the optimal convergence factor of ADMM depends on . The results are shown for two step-size rules: and given in (25). For comparison, the gray and dashed-gray curves show the optimal convergence factor of the gradient method

| with step-size and a multi-step gradient iterations on the form | ||||

This latter algorithm is known as the heavy-ball method and significantly outperforms the standard gradient method on ill-conditioned problems [28]. The algorithm has two parameters: , and . For our problem, since the cost function is quadratic and its Hessian is bounded between and , the optimal step-size for the gradient method is and the optimal parameters for the heavy-ball method are , and [28].

Figure 1 illustrates the convergence properties of the ADMM method under both step-size rules. The optimal step-size rule gives significant speedups of the ADMM for small or large values of the regularization parameter . This phenomena can be intuitively explained based on the interplay of the two parts of the objective function in (18). For extremely small values of , one sees that the -th part of the objective is becoming dominant compared to -th part. Consequently, using the optimal step-size in (25), - is dictated to quickly follow the value of -update. A similar reasoning holds when is large, in which the - has to obey the -update.

It is interesting to observe that ADMM outperforms the gradient and heavy-ball methods for small (an ill-conditioned problem), but actually performs worse as grows large (i.e. when the regularization makes the overall problem well-conditioned). It is noteworthy that the relaxed ADMM method solves the same problem in one step (convergence factor ).

V-B Quadratic programming via ADMM

Next, we evaluate our step-size rules for ADMM-based quadratic programming and compare their performance with that of other accelerated ADMM variants from the literature.

V-B1 Accelerated ADMM

One recent proposal for accelerating the ADMM-iterations is called fast-ADMM [27] and consists of the following iterations

| (77) |

The relaxation parameter in the fast-ADMM method is defined based on the Nesterov’s order-optimal method [12] combined with an innovative restart rule where is given by

| (80) |

where , and for . The restart rule assures that (77) is updated in the descent direction with respect to the primal-dual residuals.

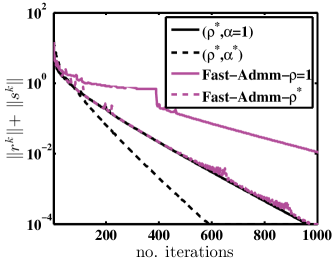

To compare the performance of the over-relaxed ADMM iterations with our proposed parameters to that of fast-ADMM, we conducted several numerical examples. For the first numerical comparison, we generated several instances of (33); Figure 2 shows the results for the two representative examples. In the first case, and with condition number ; constraints are active at the optimal solution. In the second case, and , where the condition number of is . The polyhedral constraints correspond to random box-constraints, of which are active at optimality. We evaluate for four algorithms: the ADMM iterates in (60) with and without over-relaxation and the corresponding tuning rules developed in this paper, and the fast-ADMM iterates (77) with as proposed by [27] and of our paper. The convergence of corresponding algorithms in terms of the summation of primal and dual residuals are depicted in Fig. 2. The plots exhibit a significant improvement of our tuning rules compared to the fast-ADMM algorithm.

To the best of our knowledge, there are currently no results about optimal step-size parameters for the fast-ADMM method. However, based on our numerical investigations, we observed that the performance of fast-ADMM algorithm significantly improved by employing our optimal step-size (as illustrated in 2). In the next section we perform another comparison between three algorithms, using the optimal -value for fast-ADMM obtained by an extensive search.

V-B2 Model Predictive Control

Consider the discrete-time linear system

| (81) |

where is the time index, is the state, is the control input, is a constant reference signal, and , , and are fixed matrices. Model predictive control aims at solving the following optimization problem

| (82) |

where , , and are given, , , and are the state, input, and terminal costs, and the sets and are convex. Suppose that the sets and correspond to component-wise lower and upper bounds, i.e., and . Defining , , , (81) can be rewritten as . The latter relationship can be used to replace for in the optimization problem, yielding the following QP:

| (83) |

where

| (84) |

and and .

Below we illustrate the MPC problem for the quadruple-tank process [29]. The state of the process corresponds to the water levels of all tanks, measured in centimeters. The plant model was linearized at a given operating point and discretized with a sampling period of . The MPC prediction horizon was chosen as . A constant reference signal was used, while the initial condition was varied to obtain a set of MPC problems with different non-empty feasible sets and linear cost terms. In particular, we considered initial states of the form where for . Out of the possible initial values, yields feasible QPs (each with decision variables and inequality constraints). We have made these QPs publically available as a MATLAB formatted binary file [30]. To prevent possible ill-conditioned QP-problems, the constraint matrix and vector were scaled so that each row of has unit-norm.

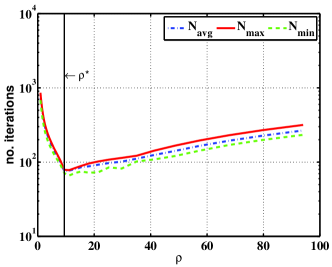

Fig. 3 illustrates the convergence of the ADMM iterations for the QPs as a function of the step-size , scaling matrix , and over-relaxation factor . Since has a non-empty null-space, the step-size was chosen heuristically based on Theorem 4 as , where is the smallest nonzero eigenvalue of . As shown in Fig. 3, our heuristic step-size results in a number of iterations close to the empirical minimum. Moreover, performance is improved by choosing and .

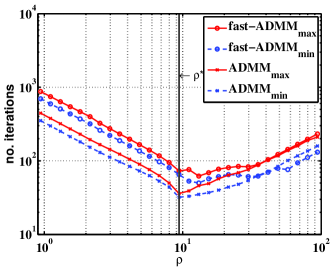

The performance of the Fast-ADMM and ADMM algorithms is compared in Fig. 4 for and . The ADMM algorithm with the optimal over-relaxation factor uniformly outperforms the Fast-ADMM algorithm, even with suboptimal scaling matrix .

V-B3 Local convergence factor

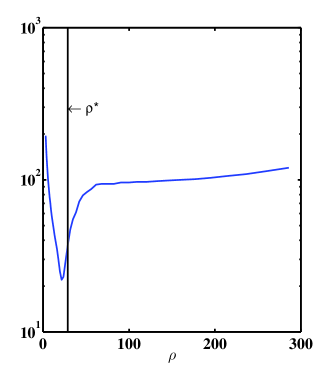

To illustrate our results on the slow local convergence of ADMM, we consider a QP problem of the form (83) with

| (85) | ||||

The ADMM algorithm was applied to the former optimization problem with and . Given that the nullity of is not , the step-size was chosen heuristically based on Theorem 4 as with taken to be the smallest nonzero eigenvalue of . The resulting residuals are shown in Fig. 5, together with the lower bound on the convergence factor evaluated at each time-step. As expected from the results in Theorem 3, the residual is monotonically decreasing. However, as illustrated by , the lower bound on the convergence factor from Theorem 5, the auxiliary residual and the primal-dual residuals show a convergence factor close to over several time-steps. The heuristic step-size rule performs reasonably well as illustrated in the right subplot of Fig. 5.

VI Conclusions and Future Work

We have studied optimal parameter selection for the alternating direction method of multipliers for two classes of quadratic problems: -regularized quadratic minimization and quadratic programming under linear inequality constraints. For both problem classes, we established global convergence of the algorithm at linear rate and provided explicit expressions for the parameters that ensure the smallest possible convergence factors. We also considered iterations accelerated by over-relaxation, characterized the values of the relaxation parameter for which the over-relaxed iterates are guaranteed to improve the convergence times compared to the non-relaxed iterations, and derived jointly optimal step-size and relaxation parameters. We validated the analytical results on numerical examples and demonstrated superior performance of the tuned ADMM algorithms compared to existing methods from the literature. As future work, we plan to extend the analytical results for more general classes of objective functions.

Acknowledgment

The authors would like to thank Pontus Giselsson, Themistoklis Charalambous, Jie Lu, and Chathuranga Weeraddana for their valuable comments and suggestions to this manuscript.

References

- [1] S. Boyd, N. Parikh, E. Chu, B. Peleato, and J. Eckstein, “Distributed optimization and statistical learning via the alternating direction method of multipliers,” Foundations and Trends in Machine Learning, vol. 3 Issue: 1, pp. 1–122, 2011.

- [2] J. Yang and Y. Zhang, “Alternating direction algorithms for -problems in compressive sensing,” SIAM J. Sci. Comput., vol. 33, no. 1, pp. 250–278, 2011.

- [3] B. Wahlberg, S. Boyd, M. Annergren, and Y. Wang, “An ADMM algorithm for a class of total variation regularized estimation problems,” in Proceedings of the16th IFAC Symposium on System Identification, Brussels, Belgium, July 2012, pp. 83–88.

- [4] M. Figueiredo and J. Bioucas-Dias, “Restoration of poissonian images using alternating direction optimization,” IEEE Transactions on Image Processing, vol. 19, no. 12, pp. 3133–3145, 2010.

- [5] P. A. Forero, A. Cano, and G. B. Giannakis, “Consensus-based distributed support vector machines,” J. Mach. Learn. Res., vol. 99, pp. 1663–1707, 2010.

- [6] S. Joshi, M. Codreanu, and M. Latva-aho, “Distributed SINR balancing for MISO downlink systems via the alternating direction method of multipliers,” in Proceedings of 11th International Symposium on Modeling & Optimization in Mobile, Ad Hoc & Wireless Networks (WiOpt), Tsukuba Science City, Japan, May 2013, pp. 318 – 325.

- [7] W. Deng and W. Yin, “On the global and linear convergence of the generalized alternating direction method of multipliers,” Rice University CAAM Technical Report ,TR12-14, 2012., Tech. Rep., 2012.

- [8] M. Hong and Z.-Q. Luo, “On the linear convergence of the alternating direction method of multipliers,” ArXiv e-prints, 2013.

- [9] D. Boley, “Local linear convergence of the alternating direction method of multipliers on quadratic or linear programs,” SIAM Journal on Optimization, vol. 23, no. 4, pp. 2183–2207, 2013.

- [10] L. Lasdon, Optimization theory for large systems. Courier Dover Publications, 1970.

- [11] D. P. Bertsekas and J. N. Tsitsiklis, Parallel and distributed computation: numerical methods. Upper Saddle River, NJ, USA: Prentice-Hall, 1989.

- [12] Y. Nesterov, Introductory Lectures on Convex Optimization: A Basic Course. Springer-Verlag New York, LCC, 2004.

- [13] D. Falcao, F. Wu, and L. Murphy, “Parallel and distributed state estimation,” Power Systems, IEEE Transactions on, vol. 10, no. 2, pp. 724–730, May 1995.

- [14] A. Nedic, A. Ozdaglar, and P. Parrilo, “Constrained consensus and optimization in multi-agent networks,” Automatic Control, IEEE Transactions on, vol. 55, no. 4, pp. 922–938, 2010.

- [15] G. S. B. O’Donoghue and S. Boyd, “A splitting method for optimal control,” IEEE Transactions on Control Systems Technology, vol. 21(6), pp. 2432–2442, 2013.

- [16] S. Boyd and L. Vandenberghe, Convex Optimization. New York, NY, USA: Cambridge University Press, 2004.

- [17] A. Teixeira, E. Ghadimi, I. Shames, H. Sandberg, and M. Johansson, “Optimal scaling of the admm algorithm for distributed quadratic programming,” in Proceedings of the 52nd IEEE Conference on Decision and Control (CDC), Florence, Italy, December 2013.

- [18] W. Shi, Q. Ling, K. Yuan, G. Wu, and W. Yin, “Linearly convergent decentralized consensus optimization with the alternating direction method of multipliers,” in Proceedings of International Conference on Acoustics, Speech, and Signal Processing (ICASSP), Vancouver, Canada, May 2013, pp. 4613 – 4617.

- [19] J. Nocedal and S. J. Wright, Numerical Optimization. Springer New York, 2006.

- [20] L. Xiao and S. Boyd, “Fast linear iterations for distributed averaging,” Systems and Control Letters, vol. 53(1), pp. 65–78, 2004.

- [21] T. Erseghe, D. Zennaro, E. Dall’Anese, and L. Vangelista, “Fast consensus by the alternating direction multipliers method,” IEEE Transactions on Signal Processing, vol. 59, pp. 5523–5537, 2011.

- [22] J. Eckstein, “Augmented lagrangian and alternating direction methods for convex optimization: A tutorial and some illustrative computational results,” RUTCOR Research Report RRR 32-2012, Tech. Rep., December 2012.

- [23] ——, “Parallel alternating direction multiplier decomposition of convex programs,” J. Optim. Theory Appl., vol. 80, no. 1, pp. 39–62, Jan. 1994.

- [24] H. Ohlsson, L. Ljung, and S. Boyd, “Segmentation of ARX-models using sum-of-norms regularization,” Automatica, vol. 46, no. 6, pp. 1107–1111, 2010.

- [25] P. Giselsson, “Improving Fast Dual Ascent for MPC - Part II: The Embedded Case,” ArXiv e-prints, Dec. 2013.

- [26] E. Ghadimi, I. Shames, and M. Johansson, “Multi-step gradient methods for networked optimization,” Signal Processing, IEEE Transactions on, vol. 61, no. 21, pp. 5417–5429, Nov 2013.

- [27] T. Goldstein, B. O’Donoghue, S. Setzer, and R. Baraniuk, “Fast alternating direction optimization methods,” UCLA, Tech. Rep., 2012.

- [28] B. Polyak, Introduction to Optimization. ISBN 0-911575-14-6, 1987.

- [29] K. Johansson, “The quadruple-tank process: a multivariable laboratory process with an adjustable zero,” IEEE Transactions on Control Systems Technology, vol. 8, no. 3, pp. 456–465, 2000.

- [30] [Online]. Available: https://www.dropbox.com/s/x2w74mpbezejbee/MPC_QP_quadtank_170_Np5_SxQ.mat

- [31] R. A. Horn and C. R. Johnson, Matrix Analysis. Cambridge, 1985.

Appendix A Proofs

A-A Proof of Theorem 1

From Proposition 1, the variables and in iterations (22) converge to the optimal values and of (18) if and only if the spectral radius of the matrix in (23) is less than one. To express the eigenvalues of in terms of the eigenvalues of , let be the eigenvalues of sorted in ascending order. Then, the eigenvalues of satisfy

| (86) |

Since , we have for all , which ensures convergence.

To find the optimal step-size parameter and the associated convergence factor , note that, for a fixed , the convergence factor corresponds to the spectral radius of , i.e. . It follows that the optimal pair is given by

| (87) |

From (86), we can see that is monotone decreasing in when and monotone increasing when . Hence, we consider these two cases separately.

When , the largest eigenvalue of is given by and . By the first-order optimality conditions and the explicit expressions in (86) we have

However, this value of is larger than only if . When , the assumption that implies that , so

Since attains it is optimal.

A similar argument applies to . In this case, and when , is the optimal step-size and the associated convergence factor is

For , the requirement that implies the inequalities and that , which leads to being optimal.

A-B Proof of Corollary 1

The proof is a direct consequence of evaluating (86) at for .

A-C Proof of Theorem 2

The -update in (29) implies that , and that the -update in (29) can be written as . Similarly to the analysis of the previous section, inserting the -update into the -update, we find

Consider the fixed-point candidate satisfying and . The -update in (29) converges (and so does the ADMM algorithm) if and only if the spectral radius of the error matrix in the above linear iterations is less than one. The eigenvalues of can be written as

| (88) |

Since and , we see that implies that for all , which completes the first part of the proof.

For a fixed and , we now characterize the values of that ensure that the over-relaxed iterations (29) have a smaller convergence factor and thus a smaller -solution time than the classical ADMM iterates (22), i.e. . From (86) and (88) we have , since and are equivalent up to an affine transformation and they have the same sign of the derivative with respect to . For any given we have

and we conclude that when . Recalling the first part of the proof we conclude that, for given , the over-relaxed iterations converge with a smaller convergence factor than classical ADMM for .

To find , we define

| (89) |

One readily verifies that for . Since zero is the global minimum of we conclude that the pair is optimal. Moreover, for the matrix is a matrix of zeros and thus the algorithm (29) converges in one iteration.

A-D Proof of Proposition 2

For the sake of brevity we derive the expressions only for , as similar computations also apply to . First, since , it holds that . From the equality we then have . The residual can be rewritten as . From (13) and (40) we observe that , so . Decomposing as we then conclude that . We now examine each case separately:

(i) When has full column rank, and . In the light of the dual residual (14) we obtain .

(ii) Note that the nullity of is if is full row-rank. Thus, and . Moreover, since is invertible, .

(iii) When is invertible, the result easily follows.

We now relate the norm of and to the one of . From (51) and (52), we have

where the first inequality is the triangle inequality and the last inequality holds as ’s are positive vectors, .

For the dual residual, it can be verified that in case (i) and (ii) , so

In case (iii), one finds and again the same bound can be achieved (by replacing with in above equality), thus concluding the proof.

A-E Proof of Theorem 3

Note that since is positive and is diagonal with elements in , implies . Hence, it suffices to establish the convergence of . From (50) we have

Furthermore, as s are positive vectors, , which implies

| (90) |

We conclude that if , then and the iterations (50) converge to zero at a linear rate.

To determine for what values of the iterations (50) converge, we characterize the eigenvalues of . By the matrix inversion lemma . From [31, Cor. 2.4.4], is a polynomial function of which implies that is a polynomial function of with . Applying [31, Thm. 1.1.6], the eigenvalues of are given by and thus

| (91) |

If , then and . Hence is guaranteed for all and equality only occurs if has eigenvalues at . If is invertible or has full row-rank, then is invertible and all its eigenvalues are strictly positive, so and (50) is guaranteed to converge linearly. The case when is tall, i.e., is rank deficient, is more challenging since has zero eigenvalues and . To prove convergence in this case, we analyze the -eigenspace of and show that it can be disregarded. From the -iterates given in (44) we have . Multiplying the former equality by from the left on both sides yields . Consider a nonzero vector in . Then we have either or . Having assumed that is full column-rank denies the second hypothesis. In other words, the -eigenspace of corresponds to the stationary points of the algorithm (44). We therefore disregard this eigenspace and the convergence result holds. Finally, the R-linear convergence of the primal and dual residuals follows from the linear convergence rate of and Proposition 2.

A-F Proof of Theorem 4

From the proof of Theorem 3 recall that

Define

where the last equality follows from the definition of in (91). Since and for the case where is either invertible or has full row-rank, for all , we conclude that .

It remains to find that minimizes the convergence factor, i.e.

| (92) |

Since is a monotonically increasing function in , the maximum values of happen for the two extreme eigenvalues and :

| (93) |

Since the left brace of , i.e. is monotone decreasing in and the right brace is monotone increasing, the minimum with respect to happens at the intersection point (55).

A-G Proof of Theorem 5

First we derive the lower bound on the convergence factor and show it is strictly smaller than . From (50) we have By applying the reverse triangle inequality and dividing by , we find

Recalling from (1) that the convergence factor is the maximum over of the left hand-side yields the lower bound (56). Moreover, the inequality follows directly from Theorem 3.

The second part of the proof addresses the cases (i)-(iii) for . Consider case (i) and let . It follows from Theorem 4 that the convergence factor is given by , thus proving the sufficiency of in (i). The necessity follows directly from statement (iii), which is proved later.

Now consider the statement (ii) and suppose is not zero-dimensional. Recall that is the smallest nonzero eigenvalue of and suppose that . Next we show that implies . Since , , and we have

Using the above inequality and we obtain .

The latter inequality allows us to derive an upper-bound on as follows. Recalling (50), we have

| (94) | ||||

Using the inequalities and for , the inequality (94) becomes which concludes the proof of (ii).

As for the third case (iii), note that holds if , as the latter inequality implies that

Supposing that there exists a non-empty set such that and holds for all , we have regardless the choice of .

A-H Proof of Lemma 1

Let denote a fixed-point of (60) and let be the Lagrange multiplier associated with the equality constraint in (36). For the optimization problem (36), the Karush-Kuhn-Tucker (KKT) optimality conditions [12] are

Next we show that the KKT conditions hold for the fixed-point with . From the iterations we have . It follows that is given by . The iteration then yields . Finally, from and the update, we have that and . Thus, .

A-I Proof of Theorem 6

Taking the Euclidean norm of (66) and applying the Cauchy-Schwarz inequality yields

Note that since s are positive vectors we have and thus

| (95) |

Note that and recall from the proof of Theorem 3 that the -eigenspace of can be disregarded. Therefore, . Defining we have

Hence, we conclude that for and , it holds that , which implies that (66) converges linearly to a fixed-point. By Lemma 1 this fixed-point is also a global optimum of (33). Now, denote and . Following the same steps as Proposition 2, it is easily verified that and from which combined with (60) one obtains

We only upper-bound , since an upper bound for was already established in (54). Taking the Euclidean norm of the second equality above and using the triangle inequality

| (96) |

The R-linear convergence of the primal and dual residuals now follows from the linear convergence rate of and the bounds in (54) and (96).

A-J Proof of Theorem 7

Define

| (97) | ||||

Since , it follows that is monotone decreasing in . Thus, is minimized by . To determine

| (98) |

we note that (92) and (98) are equivalent up to an affine transformation, hence we have the same minimizer . It follows from the proof of Theorem 4 that . Using in (LABEL:eqn:QP_Convergencefactor_relaxation) results in the convergence factor (68).

For given , , and , we can now find the range of values of for which (60) have a smaller convergence factor than (40), i.e. for which . By (90) and (95) it holds that

This means that when . Therefore, the iterates produced by the relaxed algorithm (60) have smaller convergence factor than the iterates produced by (40) for all values of the relaxation parameter . This concludes the proof.

A-K Proof of Theorem 8

Note that the non-zero eigenvalues of are the same as the ones of where and is its Choleski factorization [31]. Defining and as the largest and smallest nonzero eigenvalues of , the optimization problem we aim at solving can be formulated as

| (99) |

In the proof we show that the optimization problem (99) is equivalent to (69).

Define . First observe that holds if and only if , which proves the first inequality in the constraint set (69).

To obtain a lower bound on one must disregard the zero eigenvalues of (if they exist). This can be performed by restricting ourselves to the subspace orthogonal to . In fact, letting to be the dimension of the nullity of or simply and denoting as a basis of , we have that if and only if for all . Note that for the case when the nullity of is (), all the eigenvalues of are strictly positive and, hence, one can set . We conclude that if and only if .

Note that can be chosen arbitrarily by scaling , which does not affect the ratio . Without loss of generality, one can suppose and thus the lower bound on corresponds to the last inequality in the constraint set of (69). Observe that the optimization problem now reduces to minimizing . The proof concludes by rewriting (99) as (69), which is a convex problem.

A-L Proof of Proposition 3

Assuming , (65) reduces to . By taking the Euclidean norm of both sides and applying the Cauchy inequality, we find

Since the eigenvalues are , the convergence factor is

It is easy to check that the smallest value of is obtained when and . Since the relaxed ADMM iterations (60) coincide with (40) and consequently .

A-M Proof of Proposition 4

The proof follows similarly to the one of Proposition 3 but with .