Effective measure of endogeneity for the Autoregressive Conditional Duration point processes via mapping to the self-excited Hawkes process

Abstract

In order to disentangle the internal dynamics from exogenous factors within the Autoregressive Conditional Duration (ACD) model, we present an effective measure of endogeneity. Inspired from the Hawkes model, this measure is defined as the average fraction of events that are triggered due to internal feedback mechanisms within the total population. We provide a direct comparison of the Hawkes and ACD models based on numerical simulations and show that our effective measure of endogeneity for the ACD can be mapped onto the “branching ratio” of the Hawkes model.

I Introduction

An outstanding challenge in socio-economic systems is to disentangle the internal dynamics from the exogenous influence. It is obvious that any non-trivial system is both subject to external shocks as well as to internal organizational forces and feedback loops. In absence of external influences, many natural and social systems would regress or die, however the internal mechanisms are of no less importance and can either stabilize or destabilize the system. These systems are continuously subjected to external shocks, forces, noises and stimulations; they propagate and process these inputs in a self-reflexive way. The stability (or criticality) of these dynamics is characterized by the relative strength of self-reinforcing mechanisms.

For instance, the brain development and performance is given by both external stimuli and endogenous collective and interactive wiring between neurons. The normal regime of brain dynamics corresponds to asynchronous firing of neurons with relatively low coupling between individual neurons. However as the coupling strength increases, the internal feedback loops starts playing an increasingly important role in the dynamics, and the system moves towards the tipping point at which abnormal synchronous “neuronal avalanches” result in an epileptic seizure Shorvon et al. (1012). As another example, financial systems are known to be driven by exogenous idiosyncratic news that are digested by investors and complemented with quasi-rational (sometimes self-referential) behavior. Correlated over-expectations (herding) of investors correspond to the bubble phase that pushes the system towards criticality, where the crash may result as a bifurcation towards a distressed regime Sornette (2003).

In physical systems at thermodynamic equilibrium, the so-called fluctuation-dissipation theorem relates quantitatively the response of the system to an exogenous (and instantaneous) shock to the correlation structure of the spontaneous endogenous fluctuations Stratonovich (1992). In out-of-equilibrium systems, the existence of such relation is still an open question Ruelle (2004). In a given observation set, it seems in general hopeless to separate the contributions resulting from external perturbations and internal fluctuations and responses. However, one would like to understand the interplay between endogeneity and exogeneity (the ‘endo-exo’ problem, for short) in order to characterize the reaction of a given system to external influences, to quantify its resilience, and explain its dynamics. Using the class of self-exciting conditional Poisson (Hawkes) processes Hawkes (1971a, b), some progress has recently been made in this direction Sornette et al. (2004); Deschâtres & Sornette (2005); Sornette (2006); Crane & Sornette (2008).

In the modeling of complex point processes in natural and socio-economic systems, the Hawkes process Hawkes (1971b, a) has become the gold standard due to its simple construction and flexibility. Nowadays, it is being successfully used for modeling sequences of triggered earthquakes Ogata (1988); genomic events along DNA Reynaud-Bouret & Schbath (2010); brain seizures Sornette & Osorio (2010); Osorio et al. (2014); spread of violence Lewis et al. (2012) and crime Mohler et al. (2011) across some regions; extreme events in financial series Embrechts et al. (2011) and probabilities of credit defaults Errais et al. (2010). In financial applications, the Hawkes processes are most actively used for modeling high frequency fluctuations of financial prices (see for instance Bowsher (2007); Bauwens & Hautsch (2009); Filimonov & Sornette (2012a); Bacry et al. (2013)), however applications to lower frequency data, such as daily, are also possible (see A).

Being closely related to branching processes Harris (2002), the Hawkes model combines, in a natural and parsimonious way, exogenous influences with self-excited dynamics. It accounts simultaneously for the co-existence and interplay between the exogenous impact on the system and the endogenous mechanism where past events contribute to the probability of occurrence of future events. Moreover, using the mapping of the Hawkes process onto a branching structure, it is possible to construct a representation of the sequence of events according to a branching structure, with each event leading to a whole tree of offspring.

The linear construction of the Hawkes model allows one to separate exogenous events and develop a single parameter, the so-called “branching ratio” that directly measures the level of endogeneity in the system. The branching ratio can be interpreted as the fraction of endogenous events within the whole population of events Helmstetter & Sornette (2003); Filimonov & Sornette (2012a). The branching ratio provides a simple and illuminating characterization of the system, in particular with respect to its fragility and susceptibility to shocks. For , on average, the proportion of events arrive to the system externally, while the proportion of events can be traced back to the influence of past dynamics. As approaches from below, the system becomes “critical”, in the sense that its activity is mostly endogenous or self-fulfilling. More precisely, its activity becomes hyperbolically sensitive to external influences. The regime corresponds to the occurrence of an unbounded explosion of activity nucleated by just a few external events (e.g., news) with non-zero probability. In any realistic case, when present, this explosion will be observable in finite time. Not only does the Hawkes model provide this valuable parameter , but it also amenable to an easy and transparent estimation by maximum likelihood Ogata (1978); Ozaki (1979) without requiring stochastic declustering Zhuang et al. (2002); Marsan & Lengline (2008), which is essential in the branching processes’ framework but has several limitations Sornette & Utkin (2009).

However, the Hawkes model is not the only model that describes self-excitation in point processes. In particular, the Autoregressive Conditional Duration (ACD) model Engle & Russell (1997, 1998) and the Autoregressive Conditional Intensity (ACI) model Russell (1999) have been introduced and successfully used in econometric applications. A similar concept was used in the so-called Autoregressive Conditional Hazard (ACH) model Hamilton & Jorda (2002). These processes were designed to mimic properties of the famous Autoregressive Conditional Heteroskedasticity (ARCH) model Engle (1982) and Generalized Autoregressive Conditional Heteroskedasticity (GARCH) model Bollerslev (1986) that successfully account for volatility clustering and self-excitation in price time series. Some other modifications of ACD models such as Fractionally Integrated ACD (FIACD) Jasiak (1998) or Augmented ACD (AACD) Fernandes & Grammig (2006) were introduced to account for additional effects (such as long memory) or to increase the flexibility of the model (for a more detailed review, see Bauwens & Hautsch (2009) and references therein).

In general, all approaches to modeling self-excited point processes can be separated into the classes of Duration-based (represented by the ACD model and its derivations) and Intensity-based approaches (Hawkes, ACH, ACI, and so on), which define a stochastic expression for inter-event durations and intensity respectively. Of all the models, as discussed above, the Hawkes process dominates by far in the class of intensity-based model, and the ACD model – a direct offspring of the GARCH-family – is the most used duration-based model.

Despite belonging to different classes, both models describe the same phenomena and exhibit similar mathematical properties. In this article, we aim to establish a link between the ACD and Hawkes models. We show that, despite the fact that the ACD model cannot be directly mapped onto a branching structure, and thus the branching ratio for this model cannot be derived, it is possible to introduce a parameter that serves as an effective degree of endogeneity in the ACD model. We show that this parameter shares important properties with the branching ratio in the framework of the Hawkes model. Namely, both and characterize stationarity properties of the models, and provide an effective transformation of the exogenous excitation of the system onto its total activity. By numerical simulations, we show that there exists a monotonous relationship between the parameter of the ACD model and the branching ratio of the corresponding Hawkes model. In particular, the purely exogenous case () and the critical state () are exactly mapped to the corresponding values and . We validate our results by goodness-of-fit tests and show that our findings are robust with respect to the specification of the memory kernel of the Hawkes model.

The article is structured as follows. In section II, we introduce the Hawkes and ACD models and briefly discuss their properties. Section III introduces the branching ratio and relates it to the measure of endogeneity within the framework of the Hawkes model. In section IV, we discuss similarities between the Hawkes and ACD models, and identify a parameter in the ACD model that can be treated as an effective degree of endogeneity. We support our thesis with extensive numerical simulations and goodness-of-fit tests. In section V, we conclude.

II Models of self-excited point processes

Let us define a univariate point process of event times ( for ) with the counting process , and the duration process of inter-event times . Properties of the point process are usually described with the (unconditional) intensity process and conditional intensity process , which is adapted to the natural filtration representing the history of the process.

The well-known Poisson point process is defined as the point process whose conditional intensity does not depend on the history of the process and is constant:

| (1) |

The non-homogenous Poisson process extends expression (1) to account for time-dependence of both conditional and unconditional intensity functions: . Both homogeneous and non-homogeneous Poisson processes are completely memoryless, which means that the durations are independent from each other and are completely determined by the exogenous parameter (function) .

The Self-excited Hawkes process and Autoregressive Conditional Durations (ACD) model, which are described in this article, extend the concept of the Poisson point processes by adding path dependence and non-trivial correlation structures. These models represent two different approaches in modelling point processes with memory: the so called intensity-based and duration-based approaches. As follows from their names, the first approach focuses on models for the conditional intensity function and the second considers models of the durations . For example, in the context of the intensity-based approach, the Poisson process is defined by equation (1). In the context of the duration-based approach, the Poisson process is defined as the point process whose durations are independent and identically distributed (iid) random variables with exponential probability distribution function .

II.1 Hawkes Model

The linear Hawkes process Hawkes (1971b, a), which belongs to the class of intensity-based models, has its conditional intensity being a stochastic process of the following general form:

| (2) |

where is the background intensity, which is a deterministic function of time that accounts for the intensity of arrival of exogenous events (not dependent on history). A deterministic kernel function , which should satisfy causality ( for ), models the endogenous feedback mechanism (memory of the process). Given that each event arrives instantaneously, the differential of the counting process can be represented in the form of a sum of delta-functions , allowing (2) to be rewritten in the following form:

| (3) |

It can be shown (and we will discuss this point in the following section) that the stationarity of the process (3) requires that

| (4) |

The shape of the kernel function defines the correlation properties of the process. In particular, the geophysical applications of the Hawkes model, or more precisely of its spatio-temporal extension called the Epidemic-Type Aftershock sequence (ETAS) Vere-Jones & Ozaki (1982); Vere-Jones (1970); Ogata (1988), assume in general a power law time-dependence of the kernel :

| (5) |

that describes the modified Omori-Utsu law of aftershock rates Utsu (1961); Utsu & Ogata (1995). Financial applications Hewlett (2006); Bowsher (2007); Cont (2011); Filimonov & Sornette (2012a) traditionally use an exponential kernel

| (6) |

which has been originally suggested by Hawkes (1971b) and ensures Markovian properties of the model Oakes (1975). In both cases, a Heaviside function ensures the validity of the causality principle. The stationarity condition (4) requires for the power law kernel and for the exponential kernel.

In the present work, we focus on the Hawkes model with an exponential kernel (6) and background intensity that does not depend on time: . We introduce a new dimensionless parameter, , which will be discussed in detail later, which allows us to write the final expression for the conditional intensity as follows:

| (7) |

Then, the stationarity condition reads . In order to check the robustness of the results presented below, in particular with respect to the choice of the memory kernel, we have also considered a power law kernel (5) with time-independent background intensity . Similarly to the exponential kernel, the integral from to of the memory kernel defines the dimensionless parameter , which allows us to rewrite the Hawkes model with power law kernel as:

| (8) |

Again, the stationarity condition reads .

II.2 Autoregressive Conditional Durations (ACD) Model

The class of Autoregressive Conditional Durations (ACD) models has been introduced by Engle & Russell (1997, 1998) in the field of econometrics to model financial data at the transaction level. The ACD model applies the ideas of the Autoregressive Conditional Heteroskedasticity (ARCH) Engle (1982) model, which separates the dynamics of a stationary random process into a multiplicative random error term and a dynamical variance that regresses the past values of the process. In the spirit of the ARCH, the ACD model is represented by the duration process in the form

| (9) |

where defines an iid random non-negative variable with unit mean , and the function is the conditional expected duration: . Here, represents the set of parameters of the model. From expression (9), one can simply derive the conditional intensity of the process Engle & Russell (1998):

| (10) |

where represents the intensity function of the noise term, . Assuming to be iid exponentially distributed, one can call this model (9) an Exponential ACD model.

The conditional expected duration of the ACD(,) model, where denotes the order of the model, is defined as an autoregressive function of the past observed durations and the conditional durations themselves:

| (11) |

where , and are parameters of the model that constitute the set . The stationarity condition for the ACD model has the form Engle & Russell (1998):

| (12) |

III The Branching ratio as a measure of endogeneity in the Hawkes model

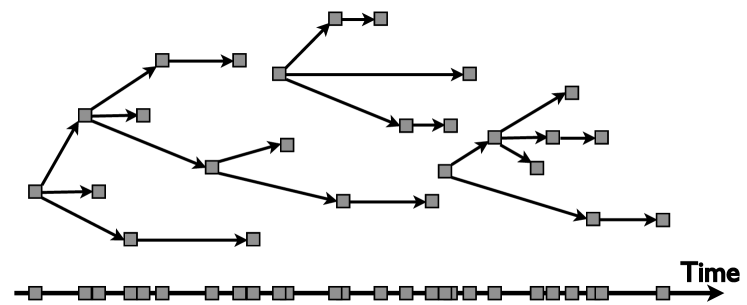

The linear structure of the Hawkes process (3) with identical functional form of summands , that depend only on arrival time of a single event , allows one to consider it as a cluster process in which the random process of cluster centers is the Poisson process with rate . All clusters associated with centers are mutually independent by construction and can be considered as a generalized branching process Hawkes & Oakes (1974), illustrated in figure 1.

[Insert Figure 1 here]

In this context, each event can be either an immigrant or a descendant. The rate of immigration is determined by the background intensity and results in an exogenous random process. Once an immigrant event occurs, it generates a whole cluster of events. Namely, a zeroth-order event (which we will call the mother event) can trigger one or more first-order events (daughter events). Each of these daughters, in turn, may trigger several second-order events (the grand-daughters of the initial mother), and so on. All first-, second- and higher-order events form a cluster and are called descendants (or aftershocks) and represent endogenously driven events that appear due to internal feedback mechanisms in the system. It should be noted that this mapping of the Hawkes process (3) onto the branching structure (figure 1) is possible due to the linearity of the model, and is not valid for nonlinear self-excited point processes, such as the class of nonlinear mutually excited point processes Brémaud & Massoulié (1996), of which the Multifractal stress activation model Sornette & Ouillon (2005) is a particular implementation.

The crucial parameter of the branching process is the branching ratio (), which is defined as the average number of daughter events per mother event. Depending on the branching ratio, there are three regimes: (i) sub-critical (), (ii) critical () and (iii) super-critical or explosive (). Starting from a single mother event (or immigrant) at time , the process dies out with probability in the sub-critical and critical regimes and has a finite probability to explode to an infinite number of events in the super-critical regime. The critical regime for separates the two main regimes and is characterized by power law statistics of the number of events and in the number of generations before extinction Saichev et al. (2005). For , the process is stationary in the presence of a Poissonian or more generally stationary flux of immigrants.

Being the parameter that describes the clustering structure of the branching process, the branching ratio defines the relative proportion of exogenous events (immigrants) and endogenous events (descendants or aftershocks). Moreover, in the sub-critical regime, in the case of a constant background intensity (), the branching ratio is exactly equal to the fraction of the average number of descendants in the whole population Helmstetter & Sornette (2003); Filimonov & Sornette (2012a). In other words, the branching ratio is equal to the proportion of the average number of endogenously generated events among all events and can be considered as an effective measure of endogeneity of the system.

To see this, let us count separately the rates of exogenous and endogenous events. The rate of exogenous immigrants (zeroth-order events) is equal to the background activity rate: . Each immigrant independently gives birth, on average, to daughters and thus the rate of first-order events is equal to . In turn, each first-order event produces, on average, second-order events, whose rate is equal to . Continuing this process ad infinitum and summing over all generations, we obtain the rate of all endogenous descendants:

| (15) |

which is finite for . The global rate is the sum of the rates of immigrants and descendants and equal to

| (16) |

And the proportion of descendants (endogenously driven events) in the whole system is equal to the branching ratio:

| (17) |

Calibrating on the data therefore provides a direct quantitative estimate of the degree of endogeneity.

In the framework of the Hawkes model (3) with , the branching ratio is easily defined via the kernel :

| (18) |

For the exponential parametrization (6), the branching ratio, , is equal to a dimensionless parameter previously introduced. The Hawkes framework provides a convenient way of estimating the branching ratio, , from the observations , using the Maximum Likelihood method, which benefits from the fact that the log-likelihood function is known for Hawkes processes Ogata (1978); Ozaki (1979). The calibration of the model and estimation of the branching ratio can then be performed with the numerical maximization of Log-Likelihood function in the parameter space for the exponential kernel (6) and for the power law model (5). Despite being a relatively straightforward calibration procedure, special care should be taken with respect to data processing, choice of the kernel, robustness of numerical methods and stationarity tests as discussed in details in Filimonov & Sornette (2013).

IV The Effective degree of endogeneity in the Autoregressive Conditional Durations (ACD) model

IV.1 Formal similarities between the ACD and Hawkes models

Note that the ACD(,) and Hawkes models operate on different variables with inverse dimensions: duration for the ACD(,) model and conditional intensity for the Hawkes model, which is of the order of the inverse of the duration . As a consequence, equations (21) and (16) apply to different statistics (average durations and average rate ). Moreover, the ACD model cannot be exactly mapped onto a branching structure whereas the Hawkes process can.

Indeed, the branching structure requires that the conditional probability for an event to occur within the infinitely small interval (which is the conditional intensity) should be decomposed into a sum of (1) a (deterministic or stochastic) function of time that represents the immigration intensity and (2) the contributions from each past event that satisfy the following conditions: (i) these contributions should depend only on and be independent from all other events ; (ii) these contributions should exhibit identical structure for all events; and (iii) they should satisfy the causality principle. Thus, in its general form, a conditional Poisson process that can be mapped on (multiple) branching structures if it is described by the following conditional intensity:

| (19) |

where is some deterministic function, and is a unit step (Heaviside function). In the context of autoregressive models (such as ACD), the expected waiting time at a given time is defined as a regressive sum of past durations, which means that the contribution of each event to the intensity at time depends on all the events that happened after it (). This violates the first principle for a branching processes of the independence of distinct branches. For the ACD model, the analysis is also complicated by the structure of the conditional intensity function (10), where past history is influencing the intensity both in a multiplicative way and with a shift in the baseline intensity . One should note that autoregressive intensity models (such as ACI) in general also do not have a branching structure representation due to the problem discussed above.

Despite the differences in their definition and the impossibility of developing an exact mapping onto a branching structure, the ACD model shares many similarities with the Hawkes model and their point processes exhibit similar degrees of clustering. In particular, for the ACD defined by expression (11), the combined parameter,

| (20) |

plays a similar role to the parameter of the Hawkes process with an exponential kernel (7). The similarities start with the stationarity conditions (4) and (12), which require for the Hawkes model and for the ACD, but go much deeper than the simple idea of “effective distance” to a non-stationary regime.

As we have seen in the previous section, defines the effective degree of endogeneity (17) that translates the exogenous rate into the total rate . Similarly, let us study the role of endogenous feedback in the ACD model. For , the ACD(0,0) model (9),(11) reduces to a simple Poisson process with durations having an average value of , which can be considered as the exogenous factor. When and , there is an amplification of the average durations. Considering the average of eq. (11) in the stationary regime ( and ), and taking into account eq. (9), we obtain the following expression for the mean duration in the stationary regime:

| (21) |

Equations (21) and (16) share the same functional dependence, with a divergence when the corresponding control parameters and approach .

IV.2 Empirical dependence of the effective branching ratio as a function of for the ACD(,) process

In order to quantify the similarities between the ACD and Hawkes models outlined in the previous section, we have performed the following numerical study. We simulated realizations of the ACD(1,1) process and calibrated the Hawkes model to it. The traditional way of fitting the Hawkes model uses the maximum likelihood method Ozaki (1979), which is asymptotically normal and asymptotically efficient Ogata (1978). We have used the R package “PtProcess” Harte (2010), which provides a convenient framework for Hawkes models (3) with arbitrary kernel and background intensity . Then, we maximized the likelihood function using a Newton-type non-linear maximization Schnabel et al. (1986); Dennis & Schnabel (1987). The B reports a study of the finite sample bias and efficiency of the Hawkes maximum likelihood estimator. We find that the estimation error of the branching ratio (without model error) measured with the 90% quantile ranges does not exceed for all values .

More precisely, we want to quantify similarities between control parameters of the model ACD(,) and of the exponential Hawkes model. For this, we have simulated realizations of the ACD process and estimated the parameter from these realizations. The parameter of the ACD(,) (11) model defines the time scale. Without loss of generality, we let , which accounts for a linear transformation of time in equations (9) and (11). For the sake of simplicity, we present our results for the ACD(1,1) model, for which the dimensionless parameter reduces to . However, our findings are robust to the choice of the order of the ACD model and can be easily generalized to the case of . The parameters and were chosen so that spanned at 40 equidistant points. For each of the 40 values of , we have generated 100 realizations of the corresponding exponential ACD(1,1) process. Each realization of 3500 events was generated by a recursive algorithm using eq. (13). In order to minimize the impact of edge effects that can bias the estimation of the branching ratio Filimonov & Sornette (2013), the first 500 points of each realization were discarded. Then, the Hawkes model (7) was calibrated on these synthetic datasets.

For each calibration, we have performed a goodness-of-fit test based on residual analysis Ogata (1988), which consists of studying the so-called residual process defined as the nonparametric transformation of the initial time-series into

| (22) |

where is the conditional intensity of the Hawkes process (7) estimated with the maximum likelihood method. Under the null hypothesis that the data has been generated by the Hawkes process (7), the residual process should be Poisson with unit intensity Papangelou (1972). Visual analysis involves studying the cusum plot or Q-Q plot and may be complemented with rigorous statistical tests. Under the null hypothesis (Poisson statistics of the residual process ), the inter-event times in the residual process, , should be exponentially distributed with CDF . Thus, the random variables should be uniformly distributed in . We have performed rigorous Kolmogorov-Smirnov tests for uniformity and provided the corresponding p-values.

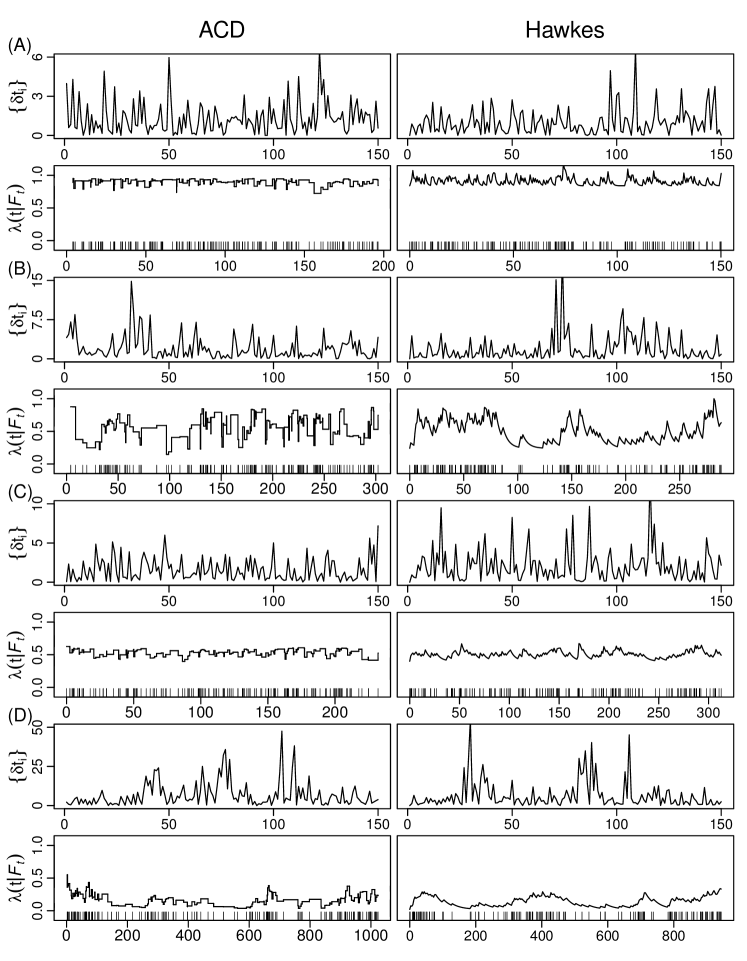

We start with a visual comparison of realizations generated with the two models. Figure 2 presents a comparison of the conditional intensities and durations for (i) simulations of the ACD(1,1) process and, (ii) simulations of the Hawkes process with parameters calibrated to the corresponding ACD process realization. Visual similarities are striking for all four ACD-Hawkes pairs: Total, average, and maximum durations are similar. Moreover, bursts of short and long durations are of similar length. The conditional intensities fluctuate in a similar range and show qualitatively similar clustering of events, although the ACD conditional intensity is constant between events while the Hawkes decays exponentially. Quantitatively, the distributions of durations also show a large degree of similarity.

[Insert Figure 2 here]

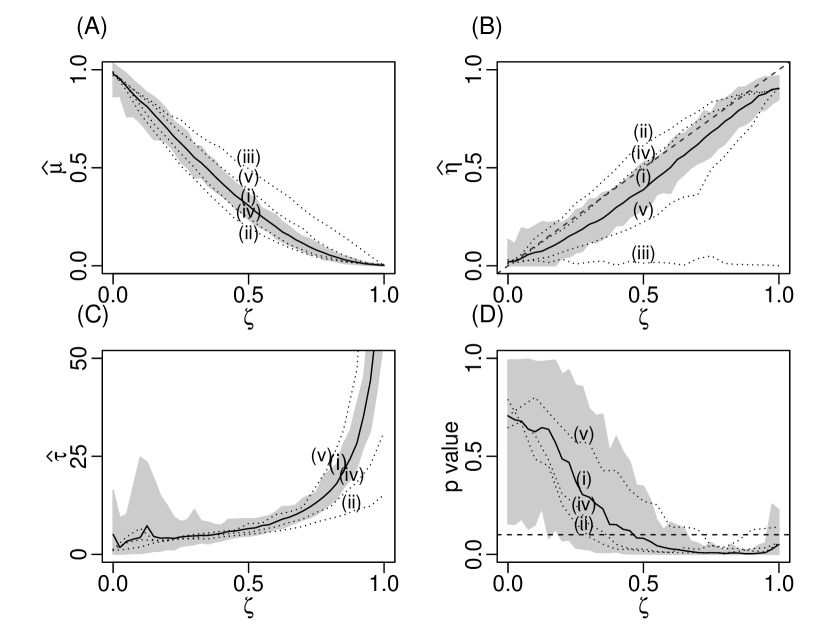

Figure 2 also reveals one important property of the ACD model. Despite the fact that many statistical properties (such as average durations (21)) are defined by the control parameter , and have different impacts on the effective degree of endogeneity . For instance, case (B) , and case(C) both have the same but for (B) and for (C). The smaller endogeneity found in case (C) is compensated by a higher rate of exogenous events ( for (C) compared with for (B)), resulting in a “flatter” conditional intensity for (C).

In order to explore this effect in simulations of the ACD model, for each value of , we considered different relations between and : (i) , (ii) , (iii) , (iv) and (v) . Figure 3 presents the results of the fitting of the Hawkes model on realizations of the ACD(1,1) model in these five cases. The first striking observation is the existence of two fundamentally different behaviors observed for (case (iii)) versus (cases (i),(ii),(iv),(v)). For , the estimated effective branching ratio is for all values of the control parameter , as shown in Figure 3(B). This diagnoses a completely exogenous dynamics of the ACD process, which is indeed the expected diagnostic given that, for , eq. (9) and (13) reduce to

| (23) |

for which the dynamics of the conditional durations is purely deterministic and independent of the realized durations , while the later are entirely driven by the random term .

[Insert Figure 3 here]

For , we find similar non-trivial results. Figure 3(B) shows the effective branching ratio as a monotonously increasing function of for all combinations of and . In cases (ii) () and (iv) (), the dependence of on is almost linear for and respectively and, for higher values of , the convexity increases. In case (i) (), depends linearly on for with a very good approximation. Finally, in case (v) (), the curvature of is significant over the range of . Remarkably, all four dependencies converge to the same value for .

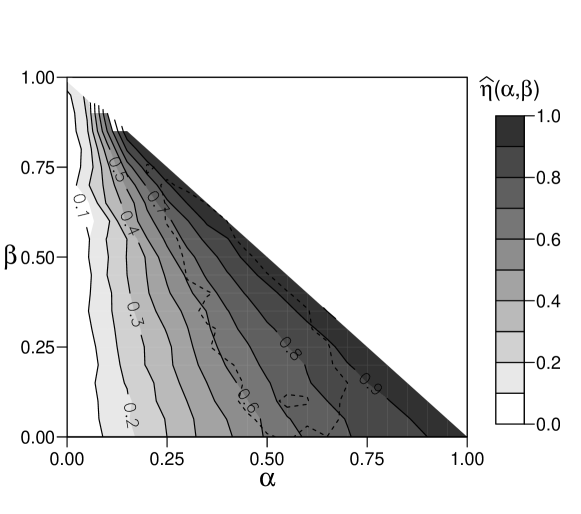

Figure 4 presents the dependence of the effective branching ratio on the control parameter after correction of the bias in estimation due to finite size effects presented in the B and summarized in figure 7). All dependencies of as a function of converge to the critical value .

[Insert Figure 4 here]

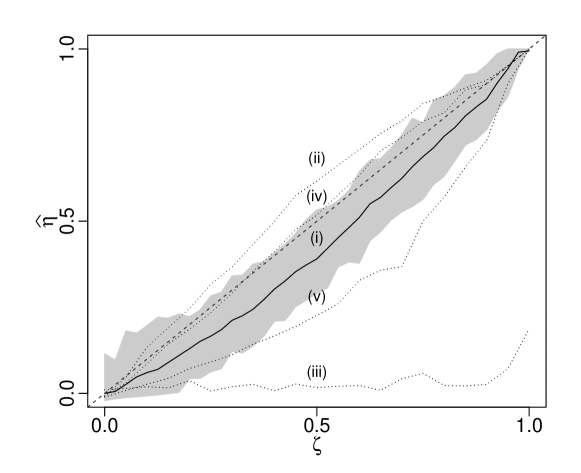

Figure 5 generalizes figure 3(B) by presenting the dependence of the effective branching ratio (corrected for the finite sample bias determined in the B) on the parameters and separately. As expected, the impact of a change of is much larger than that of . There is a region, delineated by the dashed line, within which the Hawkes model is rejected at the 5% level for the Kolmogorov-Smirnov test. For most combinations of and such that , the Hawkes model is rejected. Interestingly, the Hawkes model is not rejected in the case where is kept significantly larger than , and it is only rejected in a small interval in the extreme opposite case where . The model is often not rejected for large values of .

IV.3 Differences between the ACD and Hawkes models

Despite similarities, the Hawkes and ACD models exhibit some important differences. Figure 3A shows that the effective background rate estimated by the Hawkes model is a decreasing function of the control parameter . This is an indirect consequence of the dependence of the expected duration on given by expression (21). In contrast to the Hawkes model (2), for which the background rate completely describes the exogenous impact on the system, the parameter of the ACD model (11) is not the only factor embodying the exogenous activity and there is no strict decoupling between the exogenous driver and endogenous level as occurs for the parameters and of the Hawkes model. In other words, in contrast to the Hawkes model, the ACD in its classical form (11) does not provide a clean distinction between exogenous and endogenous activities.

Another difference between the Hawkes and ACD models can be observed in figure 3(D), which presents a residual analysis of the calibration of realizations of the ACD process by the Hawkes model using the Kolmogorov-Smirnov test. The null hypothesis that the realizations of the ACD process are generated by the Hawkes model is rejected at the 5% confidence level for in case (i) (). For case (ii) () and (iv) (), the null hypothesis is rejected for even lower . However, for case (v) (), the null cannot be rejected for almost all values of the control parameter , except for a small interval around .

IV.4 Influence of the memory kernel of the calibrating Hawkes process

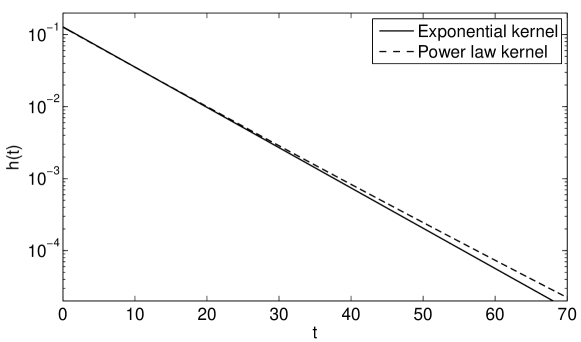

Finally, we need to discuss the choice of the kernel in the specification of the Hawkes model (3) used in the calibration of the realizations generated with the ACG process. The use of the exponential kernel (6) is a priori justified by the short memory of the ACD(,) process. Indeed, the autocorrelation function of the ACD(,) model decays exponentially Bauwens & Hautsch (2009), and the same can be shown explicitly for the GARCH(,) model Zakoian & Francq (2010). The choice of a short-memory exponential kernel for the Hawkes model ensures Markovian properties with a fast decaying autocorrelation function of the durations Oakes (1975). High p-values of the goodness-of-fit tests for parameters (see figure 3) confirm the good mapping between the exponential ACD(1,1) and Hawkes processes with an exponential kernel.

In order to further validate the selection of the exponential kernel of the Hawkes process, we have compared the calibrations of realizations generated with the ACG process with the Hawkes model with the exponential kernel (6) and with the power law kernel (5). Since these models have a different number of parameters ( and respectively), we compare them using the Akaike information criterion (AIC) Akaike (1974). The AIC is by far the most popular model comparison criterion used in the point process literature Guttorp & Thorarinsdottir (2012). The AIC penalizes complex models by discounting the likelihood function by the number of parameters of the model. Specifically, the AIC suggests selecting the model with a minimum value, where .

[Insert Table 1 here]

Table 1 gives the results for the realizations presented in figure 2. In terms of likelihood, the exponential and power law kernels give practically identical values (). Penalizing model complexity with the AIC widens the gap, and the exponential kernel with one fewer parameters is selected under the AIC.

Notwithstanding their apparent strong difference, the estimated background intensities () and branching ratios () are almost the same for both memory kernels. This can explained by the fact that the parameters and estimated for the power law kernel (5) are such that the later remains very close to an exponential kernel over a large time interval, as illustrated by figure 6 for case C (, ), which presents a direct comparison between the exponential kernel ) and the power law kernel . The corresponding ML estimates of their parameters are respectively , and . The large value of the estimated exponent (of the order of 100) implies a fast decay, similar to an exponential function. Correlatively, the large value of the constant implies the absence of the hyperbolic range (or “long tail”) as well. The almost perfect coincidence is observed for up to times , over which the kernels decay by a factor of almost 50. For for which the relative difference between the two kernels exceed 20%, the absolute values of is less than so that the contribution of time scales beyond to the total intensity (7),(8) becomes insignificant.

[Insert Figure 6 here]

V Conclusion

The present article positions itself within the neoclassical financial literature that investigates the nature of the mechanisms that drive financial prices. The benchmark, called the “Efficient Market Hypothesis” (EMH) Fama (1991, 1970); Samuelson (1965, 1973), holds that markets only reacts to external inputs (information flow) and almost instantaneously reflect these inputs in the price dynamics. This purely exogenous view on price formation has been contradicted by many empirical observations (see for instance the original works Shiller (1981); Cutler et al. (1987) and more recent Fair (2002); Sornette et al. (2003); Joulin et al. (2008)), which show that only a minor fraction of price movements can be explained by relevant news releases. This implies a significant role for internal feedback mechanisms. Using the framework of Hawkes processes, two of us Filimonov & Sornette (2012a); Filimonov et al. (2014) have used the corresponding branching ratio to provide what is, to the best of our knowledge, the first quantitative estimate of the degree of endogeneity in financial markets. This degree of endogeneity is measured as the proportion of price moves resulting from endogenous interactions among the total number of all price moves (including both endogenous interactions and exogenous news). These works provided a solid counter-example of short-term “inefficiency” of financial markets, which was complemented with the similar confirmation from longer time scales Hardiman et al. (2013). The later work, though, is subjected to a number of numerical biases, as shown in Filimonov & Sornette (2013), and triggered an ongoing discussion about the nature of long-range memory and criticality.

In this context, the present article expands the quantification of endogeneity to the class of Autoregressive Conditional Duration (ACD) point processes. This is done by the introduction of the composite parameter (20) associated with the parameters and , which control the dependence of the conditional expectated duration between events as a function of past realized duration and past conditional expected duration. We have shown that the parameter can be mapped onto the branching ratio that directly measures the level of endogeneity within the framework of the Hawkes self-excited conditional Poisson model. This result leads to a novel interpretation of the various studies that analyzed high-frequency financial data with the ACD model.

An important conclusion derives from our mapping of the ACD onto the Hawkes process. Both original works Russell (1999); Engle & Russell (1998); Engle (2000) as well as more recent studies reviewed in Refs. Pacurar (2008); Engle & Russell (2009) have reported estimated parameters and that combine to extremely large values of , often larger than , and up to . From the perspective offered by the present work and in particular from the mapping of onto , these empirical findings provide strong support to the hypothesis of a dominant endogenous or “reflexive” Soros (1987) component in the dynamics of financial markets.

The present work offers itself to a natural extension beyond point processes to the class of discrete time processes. There are several successful models of self-excitation within a discrete time framework, such as AR (auto-regressive), ARMA (auto-regressive moving average) Hamilton (1994) and GARCH models Bollerslev (1986) and their siblings, as well as the recently introduced Self-Excited Multifractal (SEMF) model Filimonov & Sornette (2011), that extends Quasi-Multifractal models Saichev & Sornette (2006); Saichev & Filimonov (2008) by introducing explicit feedback mechanism. However, until now, there has been no framework that provides a direct quantification and estimation of the degree of endogeneity present in a given time series. As discussed above, the ACD(,) model in fact belongs to the class of GARCH(,) models, though not with normally distributed innovations but instead with iid distributed innovations with a Poisson distribution. By extension, this suggests a direct application of our present findings to GARCH models. This correspondence will benefit from the elaborate toolbox of calibration methods and the detailed accumulated knowledge of the statistical properties of GARCH models Mikosch et al. (2009); Zakoian & Francq (2010).

Appendix A Financial applications of the Hawkes and ACD models

Both Hawkes and ACD-type models belong to a class of point processes and describe stochastic arrival times of events of some kind. Since the key variable of these models is the arrival time, selection of what defines an event is extremely important both for numerical analysis and for the diagnostic of the exogenous and endogenous mechanisms. In Filimonov et al. (2014), a number of endogenous mechanisms that exist in financial markets are listed — ranging from high frequency trading to behavioural herding at longer time scales. These mechanisms operate on different time scales, and have different magnitudes. Thus, the appropriate events must be defined to capture (and hopefully isolate) the dynamics of the mechanism of interest. Below, we present a non-exhaustive review of modern financial applications of Hawkes and ACD models.

As discussed in the introduction, high-frequency applications of Hawkes and ACD models are by far dominant in modern financial econometrics (see also Hautsch (2012)). In the context of the description of the order-book formation process, events can be naturally defined as a sequence of individual transactions Engle & Russell (1998); Engle (2000); Hewlett (2006) or quotes Engle & Russell (1997), or more detailed as a set of mutually-exciting processes of submission and cancellation of limit orders and submission of market orders Large (2007); Abergel & Jedidi (2011); Toke (2011); Jedidi & Abergel (2013). On the aggregate level, the last transaction price change can serve as a proxy for cross-excitation between different markets Bacry et al. (2011, 2013). Following the modern literature on price impacts (see Bouchaud et al. (2009) and references therein), Filimonov & Sornette (2012a) and Filimonov et al. (2014) suggested mid-quote price as a better proxy for price movements and mid-quote price changes were used for the estimation of the endogeneity of the price dynamics. In Bowsher (2007) and Bacry & Muzy (2013), the co-excitation between market orders and mid-price changes was used to model market impact.

However, applications of self-excited point processes are not limited to microstructure events (that can be defined only using complete order flow or level-1 tick data). In case of regularly-spaced discrete time time series (such as minutely, hourly or daily price dynamics), events can be defined as some kind of “extremes” in the dynamics. The most standard way (see for instance Chavez-Demoulin et al. (2005); Embrechts et al. (2011) with respect to applications to daily data) defines events using the “peak-over-threshold” concept: for a given dynamics of financial returns, one selects those returns that fall outside a selected quantile range (for example 10%–90%). The resulting irregularly-spaced point process can then be calibrated using the Hawkes or ACD model. A more accurate approach should account for potential changes of regime and volatility clustering, and thus should use local extreme detection methods, such as the realized bi-power variation Barndorff-Nielsen & Shephard (2004) (Bormetti et al. (2013) apply this method to model co-jumps in time-series of 1-minute returns).

Another interesting, but not yet explored application of point process models, involves detecting regime (or trend) changes in price dynamics and defining a point process using turning points. The simplest way is to define a local minima and maxima at a fixed time-scale in the discrete time series, and use these extrema to construct a point process. More accurate trend detection would involve local volatility estimation, such as method of drawup and drawdown detection (consecutive positive or negative price changes) discussed in Johansen & Sornette (2001). However, one needs to be warned that: (i) most trend detection methods are not causal and require information about the future price dynamics, thus they are not well-suited for forecasting purposes; and (ii) all these methods are based on conditional statistics that should be treated carefully in order to avoid spurious phenomena even in featureless processes Filimonov & Sornette (2012b). A general recommendation is to always consider one or several well-known processes (such as the uncorrelated random walk) and apply first the new method to these known processes to check if the event defining procedure might not introduce some spurious endogeneity.

Finally, in modeling both micro- and macro-structure of financial time series, the magnitude of events (size of orders, size and sign of price changes or jumps) can be relevant. In this case, a marked Hawkes model may be considered in which the size of the event determines its expected number of offspring, such as in the ETAS model for earthquakes for which the marks are the earthquake magnitudes Vere-Jones & Ozaki (1982); Vere-Jones (1970); Ogata (1988).

Appendix B Finite sample bias of the Hawkes maximum likelihood estimator

In order to optimize the calibration of the Hawkes model on the ACD(,), we study the finite sample bias and efficiency of the Hawkes maximum likelihood estimator. For this, we have simulated realizations of the Hawkes process with a modified thinning procedure Lewis & Shedler (1979); Ogata (1981) implemented in the same “PtProcess” package Harte (2010), and afterwards we have calibrated the Hawkes model on this synthetic data. It should be noted that simulation (and fitting Engle & Russell (1998)) of the ACD model is computationally easier than for the Hawkes model. Indeed, simulation of the Hawkes process with the thinning algorithm has complexity of (with possibility to reduce to Møller & Rasmussen (2005, 2006)), compared with complexity of only for the ACD(,) model.

[Insert Figure 7 here]

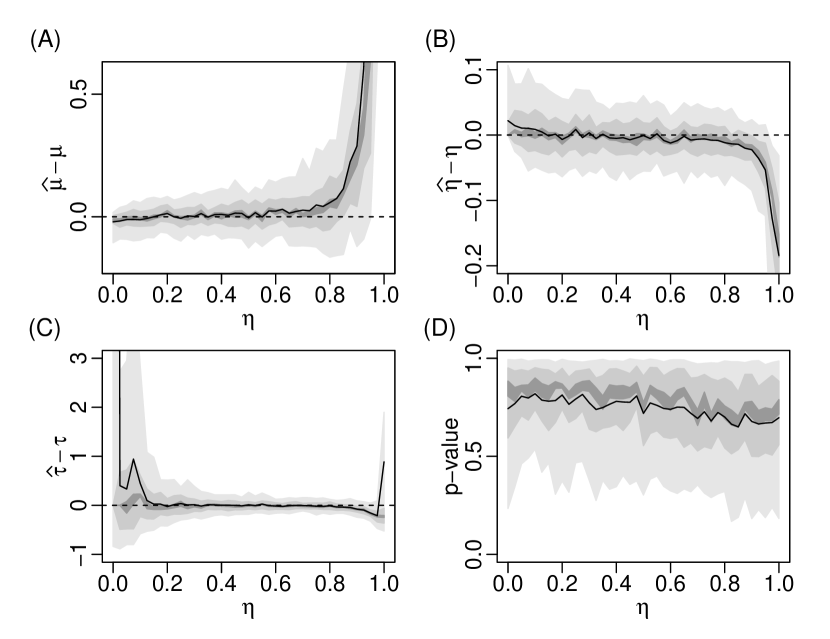

We swept the parameter in the range , fixing other parameters to and . We generated 100 realizations of the Hawkes process of size 3500 each. To reduce the edge effects of the thinning algorithm, we discarded the first 500 points of each realization and afterwards calibrated the parameters of the Hawkes model on these realizations of length 3000. Figure 7 illustrates the bias and efficiency of the maximum likelihood estimator in our framework. The definition of the Hawkes model (3) requires the kernel to be always positive. This implies , so the estimation of is expected to have positive bias for small values, as seen in figure 7. On the other hand, when approaches the critical value of 1 from below, the memory of the system increases dramatically and, for critical state of , the memory becomes infinite. Thus, for a realization of limited length, the finite size will play a very important role and will result in a systematic negative bias for . This reasoning is supported by the evidence presented in figure 7, where one observes large systematic bias for . For values of the branching ratio not too close to or , the bias is very small for almost all reasonable realization lengths (longer than 200 to 400 points). We also find that the bias for close to strongly depends on the realization length. Finally, figure 7 illustrates the high efficiency of the maximum likelihood estimator: for values of , the estimation error measured with the 90% quantile ranges does not exceed .

References

- Abergel & Jedidi (2011) Abergel, F., & Jedidi, A. (2011). A Mathematical Approach to Order Book Modelling. In Econophysics of Order-Driven Markets, (pp. 93–107). Springer Verlag.

- Akaike (1974) Akaike, H. (1974). A new look at the statistical model identification. IEEE Transactions on Automatic Control, 19(6), 716–723.

- Bacry et al. (2011) Bacry, E., Delattre, S., Hoffmann, M., & Muzy, J.-F. (2011). Modeling microstructure noise using Hawkes processes. Proceedings of the ICASSP 2011, (pp. 5740–5743).

- Bacry et al. (2013) Bacry, E., Delattre, S., Hoffmann, M., & Muzy, J.-F. (2013). Modeling microstructure noise with mutually exciting point processes. Quantitative Finance, 13(1), 65–77.

- Bacry & Muzy (2013) Bacry, E., & Muzy, J.-F. (2013). Hawkes model for price and trades high-frequency dynamics.

- Barndorff-Nielsen & Shephard (2004) Barndorff-Nielsen, O., & Shephard, N. (2004). Power and bipower variation with stochastic volatility and jumps. Journal of Financial Econometrics, 2(1), 1.

- Bauwens & Hautsch (2009) Bauwens, L., & Hautsch, N. (2009). Modelling Financial High Frequency Data Using Point Processes. In T. Mikosch, J.-P. Kreiß, R. A. Davis, & T. G. Andersen (Eds.) Handbook of Financial Time Series, (pp. 953–979). Springer.

- Bollerslev (1986) Bollerslev, T. (1986). Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics, 31(3), 307–327.

- Bormetti et al. (2013) Bormetti, G., Calcagnile, L. M., Treccani, M., Corsi, F., Marmi, S., & Lillo, F. (2013). Modelling systemic cojumps with Hawkes factor models.

- Bouchaud et al. (2009) Bouchaud, J.-P., Farmer, J. D., & Lillo, F. (2009). How markets slowly digest changes in supply and demand. In Handbook of Financial Markets: Dynamics and Evolution, (pp. 57–160). Amsterdam: North Holland.

- Bowsher (2007) Bowsher, C. G. (2007). Modelling security market events in continuous time: Intensity based, multivariate point process models. Journal of Econometrics, 141(2), 876–912.

- Brémaud & Massoulié (1996) Brémaud, P., & Massoulié, L. (1996). Stability of nonlinear Hawkes processes. The Annals of Probability, 24(3), 1563–1588.

- Chavez-Demoulin et al. (2005) Chavez-Demoulin, V., Davison, A. C., & McNeil, A. J. (2005). Estimating value-at-risk: a point process approach. Quantitative Finance, 5(2), 227–234.

- Cont (2011) Cont, R. (2011). Statistical Modeling of High Frequency Financial Data: Facts, Models and Challenges. IEEE Signal Processing, 28(5), 16–25.

- Crane & Sornette (2008) Crane, R., & Sornette, D. (2008). Robust dynamic classes revealed by measuring the response function of a social system. Proceedings of the National Academy of Sciences of the United States of America, 105(41), 15649–15653.

- Cutler et al. (1987) Cutler, D. M., Poterba, J. M., & Summers, L. H. (1987). What moves stock prices? Journal of Portfolio Management, 15(3), 4–12.

- Dennis & Schnabel (1987) Dennis, J. E., & Schnabel, R. B. (1987). Numerical Methods for Unconstrained Optimization and Nonlinear Equations, vol. 16 of Classics in Applied Mathematics. Society for Industrial Mathematics.

- Deschâtres & Sornette (2005) Deschâtres, F., & Sornette, D. (2005). Dynamics of book sales: Endogenous versus exogenous shocks in complex networks. Physical Review E, 72(1), 016112.

- Embrechts et al. (2011) Embrechts, P., Liniger, T., & Lu, L. (2011). Multivariate Hawkes Processes: an Application to Financial Data. J. Appl. Probab., 48A, 367–378.

- Engle (1982) Engle, R. F. (1982). Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation. Econometrica: Journal of the Econometric Society, 50(4), 987–1007.

- Engle (2000) Engle, R. F. (2000). The Econometrics of Ultra-High-Frequency Data. Econometrica: Journal of the Econometric Society, 68(1), 1–22.

- Engle & Russell (1997) Engle, R. F., & Russell, J. R. (1997). Forecasting the frequency of changes in quoted foreign exchange prices with the autoregressive conditional duration model. Journal of Empirical Finance, 4(2-3), 187–212.

- Engle & Russell (1998) Engle, R. F., & Russell, J. R. (1998). Autoregressive Conditional Duration: A New Model for Irregularly Spaced Transaction Data. Econometrica: Journal of the Econometric Society, 66(5), 1127–1162.

- Engle & Russell (2009) Engle, R. F., & Russell, J. R. (2009). Analysis of High Frequency Financial Data. In Handbook of Financial Econometrics, (pp. 383–426). North Holland.

- Errais et al. (2010) Errais, E., Giesecke, K., & Goldberg, L. R. (2010). Affine Point Processes and Portfolio Credit Risk. SIAM Journal on Financial Mathematics, 1(1), 642.

- Fair (2002) Fair, R. C. (2002). Events That Shook the Market. Journal of Business, 75(4), 713–731.

- Fama (1970) Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance, 25(2), 383–417.

- Fama (1991) Fama, E. F. (1991). Efficient capital markets: II. Journal of Finance, 46(5), 1575–1617.

- Fernandes & Grammig (2006) Fernandes, M., & Grammig, J. (2006). A family of autoregressive conditional duration models. Journal of Econometrics, 130(1), 1–23.

- Filimonov et al. (2014) Filimonov, V., Bicchetti, D., Maystre, N., & Sornette, D. (2014). Quantification of the High Level of Endogeneity and of Structural Regime Shifts in Commodity Markets. Journal of International Money and Finance, 42, 174–192.

- Filimonov & Sornette (2011) Filimonov, V., & Sornette, D. (2011). Self-excited multifractal dynamics. Europhysics Letters, 94(4), 46003.

- Filimonov & Sornette (2012a) Filimonov, V., & Sornette, D. (2012a). Quantifying reflexivity in financial markets: Toward a prediction of flash crashes. Physical Review E, 85(5), 056108.

- Filimonov & Sornette (2012b) Filimonov, V., & Sornette, D. (2012b). Spurious trend switching phenomena in financial markets. The European Physical Journal B - Condensed Matter and Complex Systems, 85(5), 155.

- Filimonov & Sornette (2013) Filimonov, V., & Sornette, D. (2013). Apparent criticality and calibration issues in the Hawkes self-excited point process model: application to high-frequency financial data. Swiss Finance Institute Research Paper No. 13-60.

- Guttorp & Thorarinsdottir (2012) Guttorp, P., & Thorarinsdottir, T. L. (2012). Bayesian Inference for Non-Markovian Point Processes. In E. Porcu, J. M. Montero, & M. Schlather (Eds.) Advances and Challenges in Space-time Modelling of Natural Events, (pp. 79–102). Berlin, Heidelberg: Springer Berlin Heidelberg.

- Hamilton (1994) Hamilton, J. D. (1994). Time Series Analysis. Princeton University Press.

- Hamilton & Jorda (2002) Hamilton, J. D., & Jorda, O. (2002). A Model for the Federal Funds Rate Target. Journal of Political Economy, 110, 1135–1167.

- Hardiman et al. (2013) Hardiman, S. J., Bercot, N., & Bouchaud, J.-P. (2013). Critical reflexivity in financial markets: a Hawkes process analysis. The European Physical Journal B - Condensed Matter and Complex Systems, 86(10), 442.

- Harris (2002) Harris, T. E. (2002). The Theory of Branching Processes. Dover Phoenix Editions.

- Harte (2010) Harte, D. (2010). PtProcess: An R package for modelling marked point processes indexed by time. Journal of Statistical Software, 35(8), 1–32.

- Hautsch (2012) Hautsch, N. (2012). Econometrics of Financial High-Frequency Data. Berlin, Heidelberg: Springer Berlin Heidelberg.

- Hawkes (1971a) Hawkes, A. G. (1971a). Point Spectra of Some Mutually Exciting Point Processes. Journal of the Royal Statistical Society. Series B (Methodological), 33(3), 438–443.

- Hawkes (1971b) Hawkes, A. G. (1971b). Spectra of some self-exciting and mutually exciting point processes. Biometrika, 58(1), 83–90.

- Hawkes & Oakes (1974) Hawkes, A. G., & Oakes, D. (1974). A Cluster Process Representation of a Self-Exciting Process. Journal of Applied Probability, 11(3), 493–503.

- Helmstetter & Sornette (2003) Helmstetter, A., & Sornette, D. (2003). Importance of direct and indirect triggered seismicity in the ETAS model of seismicity. Geophysical Research Letters, 30(11), 1576.

- Hewlett (2006) Hewlett, P. (2006). Clustering of order arrivals, price impact and trade path optimisation. In Workshop on Financial Modeling with Jump processes, Ecole Polytechnique.

- Jasiak (1998) Jasiak, J. (1998). Persistence in intratrade durations. Financial Analysts Journal, 19, 166–195.

- Jedidi & Abergel (2013) Jedidi, A., & Abergel, F. (2013). On the Stability and Price Scaling Limit of a Hawkes Process-Based Order Book Model.

- Johansen & Sornette (2001) Johansen, A., & Sornette, D. (2001). Large stock market price drawdowns are outliers. Journal of Risk, 4(2), 69–110.

- Joulin et al. (2008) Joulin, A., Lefevre, A., Grunberg, D., & Bouchaud, J.-P. (2008). Stock price jumps: news and volume play a minor role. Wilmott Magazine, Sep/Oct, 46.

- Large (2007) Large, J. (2007). Measuring the resiliency of an electronic limit order book. Journal of Financial Markets, 10(1), 1–25.

- Lewis et al. (2012) Lewis, E., Mohler, G. O., Brantingham, P. J., & Bertozzi, A. L. (2012). Self-exciting point process models of civilian deaths in Iraq. Security Journal, 25, 244–264.

- Lewis & Shedler (1979) Lewis, P. A. W., & Shedler, G. S. (1979). Simulation of nonhomogeneous poisson processes by thinning. Naval Research Logistics Quarterly, 26(3), 403–413.

- Marsan & Lengline (2008) Marsan, D., & Lengline, O. (2008). Extending Earthquakes’ Reach Through Cascading. Science, 319(5866), 1076–1079.

- Mikosch et al. (2009) Mikosch, T., Kreiß, J.-P., Davis, R. A., & Andersen, T. G. (Eds.) (2009). Handbook of Financial Time Series. Springer, 1 ed.

- Mohler et al. (2011) Mohler, G. O., Short, M. B., Brantingham, P. J., Tita, G. E., & Schoenberg, F. P. (2011). Self-Exciting Point Process Modeling of Crime. Journal of the American Statistical Association, 106(493), 100–108.

- Møller & Rasmussen (2005) Møller, J., & Rasmussen, J. G. (2005). Perfect simulation of Hawkes processes. Advances in applied probability, 37(3), 629–646.

- Møller & Rasmussen (2006) Møller, J., & Rasmussen, J. G. (2006). Approximate Simulation of Hawkes Processes. Methodology and Computing in Applied Probability, 8(1), 53–64.

- Oakes (1975) Oakes, D. (1975). The Markovian Self-Exciting Process. Applied Probability Trust, 12(1), 69–77.

- Ogata (1978) Ogata, Y. (1978). The asymptotic behaviour of maximum likelihood estimators for stationary point processes. Annals of the Institute of Statistical Mathematics, 30(1), 243–261.

- Ogata (1981) Ogata, Y. (1981). On Lewis’ simulation method for point processes. IEEE Transactions on Information Theory, 27(1), 23–31.

- Ogata (1988) Ogata, Y. (1988). Statistical models for earthquake occurrences and residual analysis for point processes. Journal of the American Statistical Association, 83(401), 9–27.

- Osorio et al. (2014) Osorio, I., Lyubushin A. & Sornette D. (2014). Self-exciting component of brain activity. working paper.

- Ozaki (1979) Ozaki, T. (1979). Maximum likelihood estimation of Hawkes’ self-exciting point processes. Annals of the Institute of Statistical Mathematics, 31(1), 145–155.

- Pacurar (2008) Pacurar, M. (2008). Autoregressive Conditional Duration (ACD) Models in Finance: A Survey of the Theoretical and Empirical Literature. Journal of Economic Surveys, 22(4), 711–751.

- Papangelou (1972) Papangelou, F. (1972). Integrability of Expected Increments of Point Processes and a Related Random Change of Scale. Transactions of the American Mathematical Society, 165, 483–506.

- Reynaud-Bouret & Schbath (2010) Reynaud-Bouret, P., & Schbath, S. (2010). Adaptive estimation for Hawkes processes; application to genome analysis. The Annals of Statistics, 38(5), 2781–2822.

- Ruelle (2004) Ruelle, D. (2004). Conversations on nonequilibrium physics with an extraterrestrial. Physics Today, 57(5), 48–53.

- Russell (1999) Russell, J. R. (1999). Econometric Modeling of Multivariate Irregularly-Spaced High-Frequency Data. Working Paper, University of Chicago, (pp. 1–40).

- Saichev & Filimonov (2008) Saichev, A., & Filimonov, V. (2008). Numerical Simulation of the Realizations and Spectra of a Quasi-Multifractal Diffusion Process . JETP Letters, 87(9), 506–510.

- Saichev et al. (2005) Saichev, A., Helmstetter, A., & Sornette, D. (2005). Anomalous Scaling of Offspring and Generation Numbers in Branching Processes. Pure and Applied Geophysics, 162, 1113–1134.

- Saichev & Sornette (2006) Saichev, A., & Sornette, D. (2006). Generic multifractality in exponentials of long memory processes. Physical Review E, 74(1), 011111+.

- Samuelson (1965) Samuelson, P. A. (1965). Proof That Properly Anticipated Prices Fluctuate Randomly. Industrial Management Review, 6, 41–49.

- Samuelson (1973) Samuelson, P. A. (1973). Proof That Properly Discounted Present Values of Assets Vibrate Randomly. The Bell Journal of Economics and Management Science, 4(2), 369–374.

- Schnabel et al. (1986) Schnabel, R. B., Koonatz, J. E., & Weiss, B. E. (1986). A modular system of algorithms for unconstrained minimization. ACM Transactions on Mathematical Software, 11(4), 419–440.

- Shiller (1981) Shiller, R. J. (1981). Do Stock Prices Move Too Much to be Justified by Subsequent Changes in Dividends? The American Economic Review, 71(3), 421–436.

- Shorvon et al. (1012) Shorvon, S., Guerrini, R., Cook, M., & Lhatoo, S. (Eds.) (1012). Oxford Textbook of Epilepsy and Epileptic Seizures. Oxford Textbooks in Clinical Neurology. OUP Oxford.

- Sornette (2003) Sornette, D. (2003). Why Stock Markets Crash: Critical Events in Complex Financial Systems. Princeton University Press.

- Sornette (2006) Sornette, D. (2006). Endogenous versus Exogenous Origins of Crises. In S. Albeverio, V. Jentsch, & H. Kantz (Eds.) Extreme events in nature and society, (pp. 95–119). Berlin, Heidelberg: Springer Berlin Heidelberg.

- Sornette et al. (2004) Sornette, D., Deschâtres, F., Gilbert, T., & Ageon, Y. (2004). Endogenous Versus Exogenous Shocks in Complex Networks: An Empirical Test Using Book Sale Rankings. Physical Review Letters, 93(22), 228701.

- Sornette et al. (2003) Sornette, D., Malevergne, Y., & Muzy, J.-F. (2003). What causes crashes? Risk, 16(2), 67–71.

- Sornette & Osorio (2010) Sornette, D., & Osorio I. (2010). Prediction In Epilepsy: The Intersection of Neurosciences, Biology, Mathematics, Physics and Engineering, (pp. 203–237). CRC Press, Taylor & Francis Group.

- Sornette & Ouillon (2005) Sornette, D., & Ouillon, G. (2005). Multifractal Scaling of Thermally Activated Rupture Processes. Physical Review Letters, 94(3), 038501+.

- Sornette & Utkin (2009) Sornette, D., & Utkin, S. (2009). Limits of declustering methods for disentangling exogenous from endogenous events in time series with foreshocks, main shocks, and aftershocks. Physical Review E, 79(6), 061110.

- Soros (1987) Soros, G. (1987). The Alchemy of Finance: Reading the Mind of the Market. NY: John Wiley & Sons.

- Stratonovich (1992) Stratonovich, R. L. (1992). Nonlinear Nonequilibrium Thermodynamics I: Linear and Nonlinear Fluctuation-Dissipation Theorems. Springer-Verlag.

- Toke (2011) Toke, I. M. (2011). “Market making” in an order book model and its impact on the spread. In Econophysics of Order-Driven Markets, (pp. 49–64). Springer Verlag.

- Utsu (1961) Utsu, T. (1961). A statistical study of the occurrence of aftershocks. Geophysical Magazine, 30, 521–605.

- Utsu & Ogata (1995) Utsu, T., & Ogata, Y. (1995). The centenary of the Omori formula for a decay law of aftershock activity. Journal of Physics of the Earth, 41(1), 1–33.

- Vere-Jones (1970) Vere-Jones, D. (1970). Stochastic Models for Earthquake Occurrence. Journal of the Royal Statistical Society. Series B (Methodological), 32(1), 1–62.

- Vere-Jones & Ozaki (1982) Vere-Jones, D., & Ozaki, T. (1982). Some examples of statistical estimation applied to earthquake data I. Cyclic Poisson and self-exciting models. Annals of the Institute of Statistical Mathematics, 34(1), 189–207.

- Zakoian & Francq (2010) Zakoian, J.-M., & Francq, C. (2010). GARCH Models: Structure, Statistical Inference and Financial Applications. Oxford: Wiley-Blackwell.

- Zhuang et al. (2002) Zhuang, J., Ogata, Y., & Vere-Jones, D. (2002). Stochastic declustering of space-time earthquake occurrences. Journal of the American Statistical Association, 97(458), 369–380.

A 0.05 0.05 (0.84, 0.07, 4.3) (0.83, 0.10, 262.77, 73.13) 692.0 694.8 B 0.38 0.13 (0.24, 0.52, 5.6) (0.21, 0.54, 501.14, 113.41) 986.8 990.8 C 0.13 0.38 (0.38, 0.22, 7.9) (0.36, 0.23, 816.41, 105.17) 1023.6 1026.6 D 0.45 0.45 (0.02, 0.83, 28.4) (0.01, 0.87, 203.91, 7.70) 1806.0 1811.0