Consistency of the maximum likelihood estimate for Non-homogeneous Markov-switching models

Abstract

Many nonlinear time series models have been proposed in the last decades. Among them, the models with regime switchings provide a class of versatile and interpretable models which have received a particular attention in the literature. In this paper, we consider a large family of such models which generalize the well known Markov-switching AutoRegressive (MS-AR) by allowing non-homogeneous switching and encompass Threshold AutoRegressive (TAR) models and prove the consistency of the maximum likelihood estimator under general conditions. We show that these conditions apply to specific but representative models with non-homogeneous Markov switchings. The famous MacKenzie River lynx dataset is used to illustrate one of these models.

Keywords: Markov-switching autoregressive process, non-homogeneous hidden Markov process, maximum likelihood, consistency, stability, lynx data

Introduction

Recent decades have seen extensive interest in time series models with regime switchings. One of the most influential paper in this field is the one by Hamilton in 1989 (see [13]) where Markov-Switching AutoRegressive (MS-AR) models were introduced. It became one of the most popular nonlinear time series model. MS-AR models combine several autoregressive models to describe the evolution of the observed process at different periods of time, the transition between these autoregressive models being controlled by a hidden Markov chain . In most applications, it is assumed that is an homogeneous Markov chain. In this work, we relax this assumption and let the evolution of depend on lagged values of and exogenous covariates.

More formally, we assume that takes its values in a compact metric space endowed with a finite Borel measure and that takes its values in a complete separable metric space endowed with a non-negative Borel -finite measure and we set . It will be useful to denote , (and to use analogous notations , ) for integer and . The Non-Homogeneous Markov-Switching AutoRegressive (NHMS-AR) model of order considered in this work is characterized by Hypothesis 1 below.

Hypothesis 1.

The sequence is a Markov process of order with values in such that, for some parameter belonging to some subset of ,

-

•

the conditional distribution of (wrt ) given the values of and only depends on and and this conditional distribution has a probability density function (pdf) denoted

with respect to .

-

•

the conditional distribution of given the values of and only depends on and and this conditional distribution has a pdf

with respect to .

Let us write for the conditional pdf (with respect to ) of given . Hypothesis 1 implies that

The various conditional independence assumptions of Hypothesis 1 are summarized by the directed acyclic graph (DAG) below when .

This defines a general family of models which encompasses the most usual models with regime switchings.

-

•

When does not dependent on , the evolution of the hidden Markov chain is homogeneous and independent of the observed process and we retrieve the usual MS-AR models. If we further assume that does not depend of , we obtain the Hidden Markov Models (HMMs).

-

•

When does not dependent on and is parametrized using indicator functions, we obtain the Threshold AutoRegressive (TAR) models which is an other important family of models with regime switching in the literature (see e.g. [24]).

HMMs, MS-AR and TAR models have been used in many fields of applications and their theoretical properties have been extensively studied (see e.g. [24], [10] and [5]).

Models with non-homogeneous Markov switchings have also been considered in the literature. In particular, they have been used to describe breaks associated with events such as financial crises or abrupt changes in government policy in econometric time series (see [16] and references therein). They are also popular for meteorological applications (see e.g. [15], [4], [26], [2]) with the regimes describing the so-called ”weather types”. The most usual method procedure to fit such models consists in computing the Maximum Likelihood Estimates (MLE). It is indeed relatively straightforward to adapt the standard numerical estimation which are available for the homogeneous models, such as the forward-backward recursions or the EM algorithm, to the non-homogeneous models (see e.g. [7], [16], [15]). However, we could not find any theoretical results on the asymptotic properties of the MLE for these models and this paper aims at filling this gap.

The paper is organized as follows. In Section 1, we give general conditions ensuring the consistency of the MLE. They include conditions on the ergodicity of the model and the identifiability of the parameters. In Sections 2 and 3, we show that these general conditions apply to various specific but representative NHMS-AR models. Some results are proven in the appendices.

1 A general consistency result of MLE for NHMS-AR models

We aim at estimating the true parameter of a NHMS-AR process for which only the component is observed. For that we consider the Maximum Likelihood Estimator (MLE) which is defined as the maximizer of for a fixed with

where is the conditional pdf of given evaluated at , i.e.

Observe that is a random variable depending on (which is observed).

Before stating our main result, we introduce quickly some notations (see beginning of Appendix A for further details).

Let be the transition operator of the -order Markov process , being seen as an operator acting on

the set of complex-valued bounded measurable functions on (or on some other complex Banach space)

and let be its adjoint operator. We set .

We identify with the canonical Markov chain. We suppose that, for every , there exists a

stationary probability for the Markov chain with transition operator (i.e. is an invariant probability measure for ) with pdf with respect to .

We then write for the probability measure corresponding to this invariant probability.

For every and any integer , we write for the pdf of with

respect to given .

The question of consistency of the MLE has been studied by many authors in the context of usual HMMs (see e.g. [20, 19, 8]) and MS-AR models (see [9] and references therein). The aim of this section is to state consistency results of MLE for general NHMS-AR. The proof of the following theorem is a careful adaptation of the proof of [9, Thm. 1 & 5]. This proof is given in appendix A.

Theorem 2.

Assume that is compact, that is ergodic, that there exists an invariant probability measure for every , that is absolutely continuous with respect to for every , that and are continuous in . Assume also that the following conditions hold true

| (1) |

| (2) |

| (3) |

| (4) |

| (5) |

Then, for every , the limit values of are -almost surely contained in .

If, moreover, is positive Harris recurrent and aperiodic, then, for every and every initial probability , the limit values of are almost surely contained in .

Our hypotheses are close to those of [9]. Let us point out the main differences. First, in [9] does not depend on . Second, (3) and (4) are slightly weaker than

assumed in [9]. This is illustrated below in Section 3 where the parametrization of uses Gamma pdf which may not be bounded close to the origin depending on the values of the parameters. The results given in [9] do not apply directly to this model whereas we will show that (3) applies (see also [1]). Third, to prove the result in the stationary case, we replace Harris recurrence by (5) which is equivalent to each one of the two following properties

-

•

for any initial measure on , we have , where stands for the total variation norm,

-

•

for any initial measure on , we have , with the set of probability measures on .

Remark 3.

Observe that, if and if exists for every , then the pdf of satisfies (-a.e.). In this case, is absolutely continuous with respect to for every .

Observe also that the ergodicity of the dynamical system is satisfied as soon as the transition operator is strongly ergodic with respect some Banach space satisfying general assumptions (see for example [14, Proposition 2.2]).

2 NHMS-AR model with linear autoregressive models

2.1 A NHMS-AR model for MacKenzie River lynx data

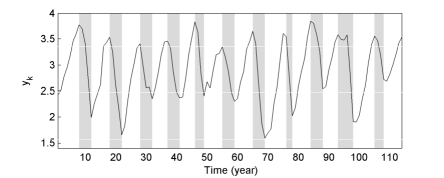

In this section we introduce a particular NHMS-AR model and discuss the results obtained when fitting this model to the the time series of annual number of Canadian lynx trapped in the Mackenzie River district of northwest Canada from 1821 to 1934. This time series is a benchmark dataset to test nonlinear time series model (see e.g. [24], [10]). In order to facilitate the comparison with the other works on this time series, we analyze the data at the logarithm scale with the base 10 shown on Figure 1. This time series exhibits periodic fluctuations (it may be due to the competition between several species, predator-prey interaction,…) with asymmetric cycles (increasing phase are slower than decreasing phase) which makes it challenging to model.

In [24], it was proposed to fit a SETAR(2) model to this time series. The fitted model is the following

| (6) |

The two regimes have a nice biological interpretation in terms of prey-predator interaction, with the upper regime () corresponding to a population decrease whereas the population tends to increase in the lower regime.

The NHMS-AR model defined below has been fitted to this time series.

Hypothesis 4.

We assume that (endowed with the counting measure), (endowed with the Lebesgue measure) and satisfies

with an iid sequence of standard Gaussian random variables, with and for every and every

| (7) |

where stands for the Gaussian pdf with mean and standard deviation .

The transition probabilities of are parametrized using the logistic function as follows when

| (8) |

with a positive integer and the unknown parameters for .

The unknown parameter corresponds to

We write for the set of such parameters satisfying, for every , and (this last constraint is added in order to ensure that (1) holds).

Although very simple, this model encompasses the homogeneous Gaussian MS-AR model when and the SETAR(2) model as a limit case. Indeed, if is fixed for , , , and then

Both models have been extensively studied in the literature.

In practice, we have used the EM algorithm to compute the MLE. The recursions of this algorithm are relatively similar to the ones of the MS-AR model (see [18], [7]). To facilitate the comparison with the SETAR(2) model (6), we have also considered AR models of order and a lag for the transition probabilities. The fitted model is the following

| (9) |

with

| (10) |

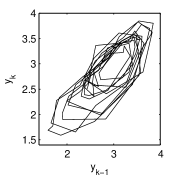

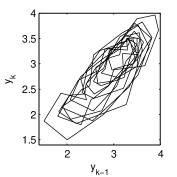

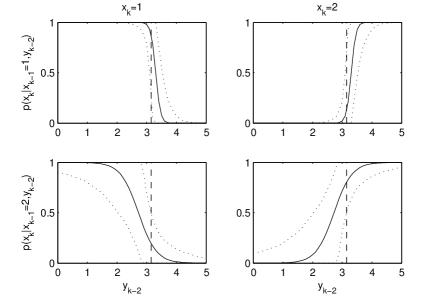

where the italic values in parenthesis below the parameter values correspond to 95% confidence intervals computed using parametric bootstrap (see e.g. [25]). These values reflect the finite sample properties of the estimates. The estimate of and are not given because they are very close to . It means that these technical parameters have no practical importance and can be fixed equal to an arbitrary small value (here we used the machine epsilon ). There are small differences between the AR coefficients (6) and (9) but the dynamics inside the regimes of the SETAR(2) and NHMS-AR models are broadly similar. The models differ mainly in the mechanism used to govern the switchings between the two regimes. For the SETAR model the regime is a deterministic function of a lagged value of the observed process. The NHMS-AR model can be seen as a fuzzy extension of the SETAR model where the regime has its own Markovian evolution influenced by the lagged value of the observed process. This is illustrated on Figure 2 which shows the transition probabilities (10) and the threshold of the SETAR(2) model. According to this figure, it seems reasonable to model the transition from regime 1 to regime 2 by a step function at the level but the values of for which the transition from regime 2 to regime 1 occurs seem to be more variable and the step function approximation less realistic.

The asymmetries in the cycle imply that the system spends less time in the second regime (decreasing phase) than in the first one. It may explain the larger confidence intervals in the second regime compared to the first one (see (9)). Figure 2 shows that there is an important sampling variability in the estimate of the transition kernel of the hidden process. This is probably due to the low number of transitions among regimes (see Figure 1) which makes it difficult to estimate the associated parameters. A similar behavior has been observed when fitting the model to other time series.

Table 1 gives the AIC and BIC values defined as

and is the likelihood of the data, is the number of parameters and is the number of observations. The values for the NHMS-AR and SETAR models are relatively similar. The NHMS-AR models has a slightly better AIC value but BIC selects the SETAR model. As expected, these two models clearly outperform the homogeneous MS-AR which does not include information on the past values in the switching mechanism.

| AIC | BIC | npar | |

|---|---|---|---|

| SETAR () | -28.33 | -3.70 | 9 |

| MS-AR () | -0.2063 | 27.15 | 10 |

| NHMS-AR () | -30.83 | 2.00 | 12 |

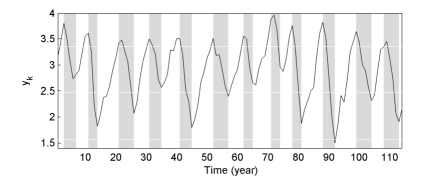

The simulated sequence shown on Figure 1 exhibits a similar cyclical behavior than the data. A more systematic validation was performed but the results are hard to analyze because of the low amount of data available. The model can be generalized in several ways to handle regimes or include covariates, for example through a linear function in the logistic term (see e.g. [7]). Other link functions, such as the probit model used in [16] or a Gaussian kernel (see (17)), or non-linear autoregressive models could also be considered. Such models have been developed for various environmental data including temperature and wind time series. The fitted models generally provide an accurate description of the distributional properties of these time series and accurate short-term forecasts. This will be the subject of a forthcoming paper.

2.2 Properties of the Markov chain

In this section, we discuss the recurrent and ergodic properties of the model introduced in the previous section. It is a key step to prove the consistence of the MLE (see Theorem 2). Various authors have studied the ergodicity of MS-AR ([28], [27], [11]) and TAR ([6], [3]) models. A classical approach to prove the ergodicity of a non-linear time series consists in establishing a drift condition. Here we will use a strict drift condition. Let be some norm on . For any , we consider the set . Recall that is here the product of the counting measure on and of the Lebesgue measure on .

Proposition 5.

Assume Hypothesis 4.

The Markov chain is -irreducible (with ).

Let . The set is -small and -small with and equivalent to . Hence, the markov chain is aperiodic.

Proof.

The -irreducibility comes from the positivity of . Let us prove that is -small with and

Indeed is uniformly bounded from below by some , are uniformly bounded from above by some and from below by some and, for every , we have

So

The proof of the -smallness of (with equivalent to ) uses the same ideas. ∎

Now, to obtain the other properties related to the ergodicity of the process for practical applications (including the practical example given in Section 2.1), we can use the following strict drift property.

Hypothesis 6.

There exist three real numbers , and such that, for every ,

| (11) |

Recall that this property has several classical consequences (see [22, Chapters 11 and 15] for more details). Hypothesis 6 (combined with the irreducibility and aperiodicity coming from Hypothesis 4) implies in particular

-

•

the existence of a (unique) stationary measure admitting a moment of order 2;

-

•

the -geometric ergodicity with and so the ergodicity of the Markov chain (see for example [14, Proposition 2.2] for this last point);

-

•

the positive Harris recurrence.

We end this section with some comments on (11). Let us write

for the companion matrix associated to the AR model in regime ,

There exist such that, for every , we have

where denotes abusively the matrix norm associated to the vector norm. We deduce the following.

Remark 7.

The strict drift condition (11) is satisfied when there exists such that for all and all

| (12) |

This is true in particular if

| (13) |

The model fitted to the lynx data in the previous section satisfies condition (13) for the matrix norm defined as

with the matrix containing the eigenvectors of the companion matrix for the second regime and the infinity norm. This condition implies that all the regimes are stable. However, it is also possible to construct models which satisfy (12) with some unstable regimes if the instability is controlled by the dynamics of .

2.3 Consistency of MLE

The results given in this section generalize the results given in [12, 17] for homogeneous MS-AR models with linear Gaussian autoregressive models.

Corollary 9.

Proof.

This corollary is a direct consequence of Theorem 2 and of the previous section. As already noticed in section 1, the invariant measure has a positive pdf with respect to . As seen in the previous section, the Markov chain is aperiodic positive Harris recurrent (which implies (5)) and the stationary process is square integrable, which implies (2) and (3). In this example, is bounded from above and so (4) holds. ∎

Remark 10.

In the sequel, we explicit the limit set under the supplementary condition

| (14) |

that the dynamics in the two regimes are distinct. Note that this condition is not sufficient in order to ensure identifiability. First, it can be easily seen that the homogeneous MS-AR model can be written in many different ways using the parametrization (8). It led us to add one of the following constraints on the parameters

| (15) |

which does not include the homogeneous model as a particular case or

| (16) |

in order to solve this problem. A practical motivation for (16) is given in Section 2.1. Let be the set of satisfying (15) and let be the set of satisfying (16). Then, a permutation of the two states also leads different parameters values but to the same model. This problem can be solved by ordering the regimes or by allowing a permutation of the states as discussed below.

Proposition 11 (Identifiability).

Let and belong to (resp. ) with and

the parameters associated with the regime .

Assume that satisfies (14). Then if and only if and define the same model up to a permutation of indices, i.e. there exists a permutation of such that

Theorem 12.

3 Non-homogeneous Hidden Markov Models with exogenous variables

3.1 Model

When using NHMS-AR models in practice, it is often assumed that the evolution of depends not only on lagged values of the process of interest but also on strictly exogenous variables. In order to handle such situation, we will denote with the time series of covariates and the output time series to be modeled. Besides Hypothesis 1, various supplementary conditional independence assumptions can be made for specific applications. For example, in [15] it is assumed that the switching probabilities of only depend on the exogenous covariates

that the evolution of is independent of and and that is conditionally independent of and given

This model, which dependence structure is summarized by the DAG below when is often referred as Non-Homogeneous Hidden Markov Models (NHMMs) in the literature.

In this section, we consider a typical example of NHMM with finite hidden state space and strictly exogenous variables and show that the theoretical results proven in this paper apply to this model. We focus on a model initially introduced in [4] for downscaling rainfall. It is an extension of the model proposed in [15] (see also [26] for more recent references). The results given in this section can be adapted to other NHMM with finite hidden state space such as the one proposed in [7] which is widely used in econometrics. The model is described more precisely hereafter.

Hypothesis 13.

Let be a positive integer and be a positive definite symmetric matrix. We suppose that (endowed with the counting measure on ) and that the observed process has two components . For every time , is a vector of large scale atmospheric variables (covariates) and is the daily accumulation of rainfall measured at meteorological stations (output time series) with the value corresponding to dry days. The model aims at describing the conditional distribution of given . For this, we assume that

| (17) |

with , and (3.1) holds with respect to , where is the Lebesgue measure on and where is the sum of the Dirac measure and of the Lebesgue measure on . We observe that is a Markov chain which transition kernel depends neither on the current weather type nor on the unknown parameter (typically is the output of an atmospheric model and is considered as an input to the Markov switching model) and that the conditional distribution of given and only depends on as in usual HMMs. Finally the rainfall at the different locations is assumed to be conditionally independent given the weather type

and the rainfall at the different locations is given by the product of Bernoulli and Gamma variables

| (18) |

where , , and denotes the pdf of a Gamma distribution with parameters , :

The parameter corresponds to

We write for the set of such parameters satisfying, for every and every ,

The conditions and come from [15]. These conditions are not restrictive. Indeed, is unchanged if we replace by and by (with ).

Observe that the fact that, if for every , then is an homogeneous Markov chain and does not plays any role in the dynamics of .

3.2 Properties of the Markov chain

We start by recalling a classical result ensuring (5) in the context of HMM (a proof of this result is given in Appendix D for completeness).

Lemma 14 (HMM).

Fix . Assume that does not depend on , is a Markov chain with transition kernel admitting an invariant pdf (wrt ) such that

Assume moreover that (this means that we can take with ). Then there exists an invariant measure with pdf (wrt ) given by and

Moreover, if and if is an aperiodic positive Harris recurrent Markov chain, then the Markov chain is positive Harris recurrent and aperiodic.

Due to this lemma, assumption (5) holds true and is aperiodic positive Harris recurrent as soon as is aperiodic positive Harris recurrent.

The ergodicity of will also follow from the ergodicity of .

3.3 Consistency of MLE

Corollary 15.

Assume Hypothesis 13. Assume that is a compact subset of and that, for every , the transition kernel of the Markov chain admits an invariant pdf (wrt ) such that

| (19) |

Assume moreover that is compact, that

| (20) |

and that

| (21) |

Then, for every , on a set of probability one (for ), the limit values of the sequence of random variables are -almost surely contained in .

If, moreover, is aperiodic and positive Harris recurrent then this result holds true for any initial probability distribution.

Proof.

Due to the previous section, we know that (19) implies (5) and that the aperiodicity and positive Harris recurrence of implies the positive Harris recurrence of .

The fact that is a compact subset of directly implies (1).

Now according to (21), (2) and (3) will follow from the fact that, for every and every ,

Now we observe that if , then

where and are the minimal and maximal possible values of (for , and in the compact set ). Analogously, let us write , for the minimal and maximal possible values of and , for the minimal and maximal possible values of . Since, all this quantities are positive and finite, due to the expression of , to prove (2) and (3), it is enough to prove that

Now we will add an assumption on to ensure the identifiability of the parameter. If we assume for every and every , then identifiability follows easily if we assume moreover that

| (22) |

But, if we do not assume , (22) does not ensure identifiability anymore. We give now an explicit counter-example.

Remark 16.

Assume . We consider two models and associated to and respectively, with

and

-

•

, , , , , , ,

-

•

, , , , , , , , , .

For model (under the stationary measure), is an iid sequence on with and the distribution of given is whereas the distribution of taken is Hence, for the model , the are iid with distribution

| (23) |

For model (under the stationary measure), is an iid sequence on with and the distribution of given is whereas the distribution of taken is . Hence, for the model , the are iid with distribution (23).

Observe that the distribution of under the stationary measure is the same for models and .

The next result (proved in appendix C) states that the following condition ensures identifiability

| (24) |

Proposition 17.

Then if and only and are equal up to a permutation of indices, i.e. there exists a permutation of such that, for every and every , we have , , , , .

Theorem 18.

Assume Hypothesis 13. Assume that is a compact subset of and that, for every , the transition kernel of the Markov chain admits an invariant pdf (wrt ) satisfying (19). Assume that satisfies (24). Assume moreover that is compact, that (20) and (21) hold true. Then, for every , on a set of probability one (for ), the limit values of the sequence of random variables are equal to up to a permutation of indices.

If, moreover, is aperiodic and positive Harris recurrent then this result holds true for any initial probability distribution.

4 Conclusions

In this work, we have extended the consistency result of [9] to the non-homogeneous case and we have relaxed some other of their assumptions (namely on ). We have illustrated our results by two specific but representative models for which we gave general conditions ensuring the consistency of the maximum likelihood estimator. Our results opens perspectives in different directions: theoretical results (such as the asymptotic normality of the MLE), applied statistics (namely the study of other non-homogeneous switching Markov models and their applications), but also the development of a R package to make easier the practical use of these flexible models.

Appendix A Consistency : proof of Theorem 2

As usual, we define the associated transition operator as an operator acting on the set of bounded measurable functions of (it may also act on other Banach spaces ) by

We denote by the adjoint operator of defined on the dual space of (if acts on ) by

For every integer , the measure corresponds to the distribution of if is the Markov chain with transition operator such that the distribution of is .

If has a pdf with respect to , then is also absolutely continuous with respect to and its pdf, written , is given by

Observe that, due to the particular form of , for every integer and every , the measure (where is the Dirac measure at ) is absolutely continuous with respect to ; its pdf is given by

More generally, for every initial measure and every , is absolutely continuous with respect to and its pdf is given by

| (25) |

We suppose that, for every , there exists an invariant probability measure for . Observe that, due to (25), admits a pdf with respect to .

We identify with the canonical Markov chain defined on by , , being the shift (). We endow with its Borel -algebra . We denote by the probability measure on associated to the invariant measure and by the corresponding expectation. The ergodicity of is equivalent to the ergodicity of .

We now follow and adapt the proof of [9, Thm. 1] (see Lemmas 26 and 27). We do not give all the details of the proofs when they are a direct rewriting of [9]. First, we consider the stationary case. Let be the full shift on . For every , we identify with and with , where and .

A.1 Likelihood and stationary likelihood

We start by recalling a classical fact in the context of Markov chains (and the proof of which is direct).

Fact 19.

Let and belong to with . Under , conditionally to , is a (possibly nonhomogeneous) Markov chain. Moreover, under , the conditional pdf (wrt ) of given is given by

| (26) |

with

| (27) |

and

| (28) |

Using (1), (2) and (3), we observe that the quantities appearing in this fact are well-defined. Due to Fact 19, the quantity is equal to

with . Therefore

| (29) |

From this last inequality (since ), we directly get the following (from [21]).

Corollary 20.

Observe that the log-likelihood satisfies

with

Let us now define the stationary log-likelihood by

with

and

Lemma 21.

(as [9, Lem. 2]) We have

| (30) |

A.2 Asymptotic behavior of the log-likelihood

The idea is to approximate by To this end, we define, for any , any and any , the following quantities

With these notations, we have

| (32) |

Lemma 22.

Proof.

Due to (33), we get that, -a.s., is a (uniform in ) Cauchy sequence and so converges uniformly in to some .

Due to (35), (1), (2) and (3), is uniformly bounded in . Therefore is in . Let us write

Since is ergodic, from the Birkhoff-Khinchine ergodic theorem, we have

| (36) |

Now, due to (33) and (34) applied with , we obtain

| (37) |

Corollary 23.

Still following [9], we have the next lemma insuring the continuity of .

Lemma 24.

(as [9, Lemma 4]) For all ,

Proof.

Lemma 25.

(as [9, Prop. 2]) We have

Lemma 25 can be deduced exactly as in the proof of [9, Prop. 2]. We do not rewrite the proof, but mention that it uses (30), the compacity of , the continuity of , (37), the ergodicity of and Lemma 24.

Lemma 26.

(as [9, Lemma 5]) For every , we have

Proof.

Let us write and . As in the proof of [9, Lemma 5], we observe that, by stationarity, it is enough to prove that

and we write

with

with

and with

Let us write

We have

On the one hand, due to (5), converges to 0 as goes to infinity, for -almost every (and this quantity is bounded by 1). On the other hand, on , we have

with

and

Therefore, by the Lebesgue dominated convergence theorem, we obtain

Of course, this convergence also holds in -probability. Now, since, for every , is a real valued random variable (see (4)) with the same distribution as , we obtain the result. ∎

Lemma 27.

([9, Lem. 6 & 7, Prop. 3]) For every , . Furthermore

Elements of the proof.

We do not rewrite the proof of this lemma, the reader can follow the proofs of [9, Lem. 6-7, Prop. 3] (using Lemma 26 and Kullback-Leibler divergence functions). The only adaptations to make concern the proof of [9, Lem. 7] which, due to our slightly weaker hypothesis (4), are the following facts. Following the proof of Lemma 26, observe that, due to (1), (28) and (27), on , is between

and

with . Therefore we have

which enables the adaptation of the proof of [9, Lem. 7]. ∎

Proof of Theorem 2.

Let . We know that, -almost surely, converges uniformly to which admits a maximum . Since is continuous on and since is compact, is well defined. Moreover, the limit values of are contained in

Assume now that is aperiodic and positive Harris recurrent, following the proof of [9, Thm. 5], we have almost surely for any initial measure and we conclude as above. ∎

Appendix B Identifiability for the Gaussian model: proof of Proposition 11

Assume that . In particular, we have

and thus

for -almost every . Since (the invariant pdf satisfies and the transition pdf satisfies by construction), this last equality also holds for Lebesgue almost every . According to [23], finite mixtures of Gaussian distribution are identifiable. Due to (7), this implies in particular that if

with , and , then there exists a permutation such that and . Therefore, since for every and for Lebesgue almost every , (since ), for Lebesgue almost every there exists a permutation of such that,

Recall that we have assumed (for the first model)

which implies

for Lebesgue almost every . Since the set of permutations of is finite, there exists a positive Lebesgue measure subset of on which the permutation is the same permutation . From this, we deduce that, for all and ,

and

If and are in then for and looking at the asymptotic behavior of the terms which appear in (B) when permits to show that , . We can then easily deduce that and and thus that .

If and are in , then we directly obtain that and then that .∎

Appendix C Identifiability for the Rainfall model: proof of Proposition 17

Assume that . First, we use the fact that

| (39) |

to prove that

Using (39) on the set , we conclude that there exists a permutation of such that, for every and every , we have

| (40) |

and

Now, for every , we use (39) on the set . Due to (40) and since satisfies (24), we obtain

From which, we conclude

| (41) |

Now it remains to prove that . To this hand, as for the AR model (see Appendix B), we use the fact that

| (42) |

and obtain that

This implies that

| (43) |

with and . From (43), we obtain that

and so that, for every ,

| (44) |

and

| (45) |

Finally, it comes from (44) that (using ) and so . So (45) becomes

which implies that (due to ).∎

Appendix D Proof of Lemma 14

Let be any probability pdf wrt . We have

with . Now, since , we obtain that

Therefore

Now, let us assume that and that is an aperiodic positive Harris recurrent Markov chain. We will use the notations of [22].

Since is positive, it is -irreducible (with ). Due to the hypothesis on , this implies the -irreducibility of (with ).

Moreover is positive since it admits an invariant probability measure (due to the first point of this result).

The fact that is aperiodic means that, for every -small set such that for , the greatest common divisor of the set defined as follows is equal to 1:

Now, let be a -small set for with , then for every and every , we have . Moreover is equal to

Since does not depend on , we obtain

and so is -small with and . Moreover . Indeed, if is -small with , then is -small with with ; and conversely, if is -small with , then is -small with and with . Therefore is also aperiodic.

Finally, the Harris recurrence property of follows from the Harris-recurrence of and from .∎

References

- [1] P. Ailliot. Some theoretical results on markov-switching autoregressive models with gamma innovations. Comptes Rendus de l’Acad mie des sciences, Series I, 343:271 274, 2006.

- [2] P. Ailliot and V. Monbet. Markov-switching autoregressive models for wind time series. Environmental Modelling and Software, 30:92–101, 2012.

- [3] H.Z. An and F.C. Huang. The geometrical ergodicity of nonlinear autoregressive models. Statistica Sinica, 6:943–956, 1996.

- [4] E. Bellone, J.P. Hughes, and P. Guttorp. A hidden markov model for downscaling synoptic atmospheric patterns to precipitation amounts. Climate Research, 15:1–12, 2000.

- [5] O. Cappé, E. Moulines, and Rydén T. Inference in hidden Markov models. Springer-Verlag, New York, 2005.

- [6] R. Chen and R.S. Tsay. On the ergodicity of tar(1) processes. Annals of Applied Probability, 1:613–634, 1991.

- [7] F. Diebold, J-H Lee, and G. Weinbach. Regime Switching with Time-Varying Transition Probabilities. Oxford: Oxford University Press, 1994.

- [8] R. Douc and C. Matias. Asymptotics of the maximum-likelihood estimator for general hidden Markov models. Bernoulli, 7(3):381–420, 2001.

- [9] R. Douc, E. Moulines, and T. Ryd n. Asymptotic properties of the maximum likelihood estimator in autoregressive models with markov regime. Annals of Statistics, 32:2254–2304, 2004.

- [10] J. Fan and Q.. Yao. Nonlinear Time Series: Nonparametric and Parametric Methods. Springer, New York., 2003.

- [11] C. Francq and M. Roussignol. Ergodicity of autoregressive processes with markov switching and consistency of the maximum-likelihood estimator. Statistics, 27:1 –38, 1998.

- [12] C. Francq and M. Roussignol. Ergodicity of autoregressive processes with markov-switching and consistency of the maximum-likelihood estimator. Statistics, 32(2):151–173, 1998.

- [13] J.D. Hamilton. A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica, 57:357–384, 1989.

- [14] L. Hervé and F. Pène. The nagaev-guivarc’h method via the keller-liverani theorem. Bulletin de la Société Mathématique de France 138, 138:415–489, 2010.

- [15] J.P Hughes, P. Guttorp, and S.P. Charles. A non-homogeneous hidden markov model for precipitation occurrence. Journal of the Royal Statistical Society: Series C (Applied Statistics), 48(1):15–30, 1999.

- [16] C. Kim, J. Piger, and R. Startz. Estimation of markov regime-switching regression models with endogenous switching. Journal of Econometrics, 143:263–273, 2008.

- [17] V. Krishnamurthy and T. Ryden. Consistent estimation of linear and non-linear autoregressive models with markov regime. Journal of time series analysis, 19(3):291–307, 1998.

- [18] H.M. Krolzig. Markov-Switching vector autoregressions: modelling, statistical inference, and application to business cycle analysis, volume 454. Springer Berlin, 1997.

- [19] F. Le Gland and L. Mevel. Exponential forgetting and geometric ergodicity in hidden Markov models. Mathematics of Control, Signals, and Systems, 13:63–93, 2000.

- [20] B. Leroux. Maximum-likelihood estimation for hidden Markov models. Stochastic Processes and their Applications, 40:127–143, 1992.

- [21] T. Lindvall. Lectures on the coupling method. Corrected reprint of the 1992 original. Dover Publications, Inc., Mineola, NY, 2002.

- [22] S.P. Meyn, R.L Tweedie, and P.W. Glynn. Markov chains and stochastic stability, volume 2. Cambridge University Press Cambridge, 2009.

- [23] H. Teicher. Identifiability of finite mixtures. Annals of mathematical statistics, 34:1265–1269, 1963.

- [24] H. Tong. Non-Linear Time Series: A Dynamical System Approach. Oxford University Press, Oxford, U.K., 1990.

- [25] I. Visser, M.E.J. Raijmakers, and P. Molenaar. Confidence intervals for hidden markov model parameters. British journal of mathematical and statistical psychology, 53(2):317–327, 2000.

- [26] M. Vrac and P. Naveau. Stochastic downscaling of precipitation: From dry events to heavy rainfalls. Water resources research, 43:W07402, 2007.

- [27] J.F. Yao. On square-integrability of an ar process with markov switching. Statistics & Probability letters, 52:265–270, 2001.

- [28] J.F. Yao and J.G. Attali. On stability of nonlinear ar processes with markov switching. Advances in Applied Probability, 32:394–407, 2000.