On moment indeterminacy of the Benini income distribution

Abstract

The Benini distribution is a lognormal-like distribution generalizing the Pareto distribution. Like the Pareto and the lognormal distributions it was originally proposed for modeling economic size distributions, notably the size distribution of personal income. This paper explores a probabilistic property of the Benini distribution, showing that it is not determined by the sequence of its moments although all the moments are finite. It also provides explicit examples of distributions possessing the same set of moments. Related distributions are briefly explored.

Keywords: Benini distribution, characterization of distributions, income distribution, moment problem, statistical distributions, Stieltjes class.

AMS 2010 Mathematics Subject Classification: Primary 60E05, Secondary 62E10, 44A60.

JEL Classification: C46, C02.

1 Introduction

In the late 19th century, the eminent Italian economist Vilfredo Pareto observed that empirical income distributions are well described by a straight line on a doubly logarithmic plot (Pareto, 1895, 1896, 1897). Specifically, with denoting the survival function of an income distribution with c.d.f. , Pareto observed that, to a good degree of approximation,

| (1.1) |

The distribution implied by this equation is called the Pareto distribution.

Not much later, the Italian statistician and demographer Rodolfo Benini found that a second-order polynomial

| (1.2) |

sometimes provides a markedly better fit (Benini, 1905, 1906). The distribution implied by this equation is called the Benini distribution.

The present paper is concerned with a probabilistic property of the Benini distribution, namely whether it is possible to characterize this distribution in terms of its moments. The moment problem asks, for a given distribution with finite moments of all orders , whether or not is uniquely determined by the sequence of its moments. See, for example, Shohat and Tamarkin (1950) for analytical or Stoyanov (2013, Sec. 11) for probabilistic aspects of the moment problem. If a distribution is uniquely determined by the sequence of its moments it is called moment-determinate, otherwise it is called moment-indeterminate. Cases where the support of the distribution is the positive half-axis or an unbounded subset thereof are called Stieltjes-type moment problems. The Benini distribution thus poses a Stieltjes-type moment problem. It is shown below that the Benini moment problem is indeterminate. Drawing on a classical example going back to Stieltjes (1894/1895) explicit examples of distributions possessing the same set of moments are constructed. Certain generalizations of the Benini distribution are briefly explored, all of which are moment-indeterminate.

2 The Benini distribution

Pareto’s observation (1.1) leads to a distribution of the form

where . Benini’s observation (1.2) leads to a distribution of the form

| (2.1) |

where , with . Setting gives the Pareto distribution.

For parsimony, Benini (1905) often worked with the special case where , i.e. with

Here is a scale and is a shape parameter. This distribution will be denoted as Ben(). For the purposes of the present paper the scale parameter is immaterial. The object under study is, therefore, the distribution with

| (2.3) |

It may be worth noting that the Benini distributions are stochastically ordered w.r.t. . Specifically, it follows directly from (2.3) that

| (2.4) |

hence is larger than under this condition in the sense of the usual stochastic order, often called first-order stochastic dominance in economics.

Noting further that the c.d.f. of a Weibull distribution is , , , it follows that eq. (2.3) describes a log-Weibull distribution with . The Weibull distribution with is also known (up to scale) as the Rayleigh distribution, especially in physics, and so the Benini distribution may be seen as the log-Rayleigh distribution. It may also be seen as a log-chi distribution with two degrees of freedom (again up to scale); i.e., the logarithm of a Benini random variable follows the distribution of the square root of a chi-square random variable with two degrees of freedom.

The density implied by (2.3) is

| (2.5) |

and hence is similar to the density of the more familiar lognormal distribution. The lognormal distribution is perhaps the most widely known example of a distribution that is not determined by its moments, although all its moments are finite (Heyde, 1963). The similarity of the lognormal and the Benini densities now suggests that the Benini distribution might also possess this somewhat pathological property. The remainder of the present paper explores this issue.

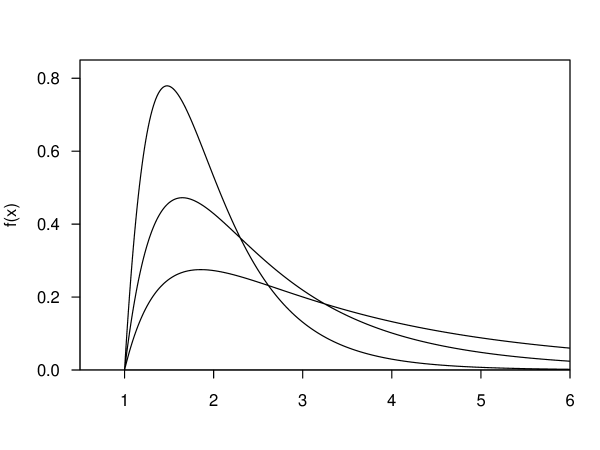

Figure 1 depicts some two-parameter Benini densities, showing that distributions with smaller values of are associated with heavier tails, as indicated by (2.4).

From a modeling point of view, the significance of the Benini distribution lies in the fact that it generalizes the Pareto distribution while itself being ‘lognormal-like’. It thus enables to discriminate between these two widely used distributions, at least approximately. Further details on the Benini distribution, including an independent rediscovery in actuarial science motivated by failure rate considerations (Shpilberg, 1977), may be found in Kleiber and Kotz (2003, Ch. 7.1). The appendix of Kleiber and Kotz (2003) also provides a brief biography of Rodolfo Benini.

3 The Benini distribution and the moment problem

The following proposition provides two basic properties of the Benini distribution that are relevant in the context of the moment problem.

Proposition 1.

-

(a)

The moments , , of the Benini distribution Ben() are given by

(3.1) (3.2) Here, is a parabolic cylinder function and denotes the error function.

-

(b)

The moment generating function (m.g.f.) of the Benini distribution does not exist.

Proof. (a) We have

using Gradshteyn and Ryzhik (2007), no. 3.462, eq. 1. This proves (3.1). The alternative representation (3.2) is established via the relation (Olver et al., 2010, § 12.7.5)

where is the complementary error function, together with and .

(b) The defining integral is

Now the leading term in

is the linear term, hence for all .

The representation (3.2) can also be obtained using Mathematica (Wolfram Research, Inc., 2013), version 9.0.1.0.

As an illustration, Table 1 provides the first four moments of selected Benini distributions, namely those from Figure 1. These moments are rather large, especially for small values of .

| 1.98 | 4.48 | 11.81 | 37.20 | |

| 2.73 | 9.88 | 50.59 | 387.19 | |

| 4.48 | 37.20 | 677.00 | 29888.67 |

Proposition 1 showed that the Benini distribution has moments of all orders, but no m.g.f. Distributions possessing these properties are candidates for moment indeterminacy, although these facts alone are not conclusive. Unfortunately, no tractable necessary and sufficient condition for moment indeterminacy is currently known.

For exploring determinacy, the Carleman criterion (e.g. Stoyanov, 2013, Sec. 11) sometimes provides an answer. In a Stieltjes-type problem, the condition

implies that the underlying distribution is characterized by its moments.

However, Proposition 1 indicates that the moments of the Benini distribution grow rather rapidly. In view of , for , it follows from (3.2) that

Using the ratio test this further implies that

| (3.3) |

So the Carleman condition cannot establish determinacy here.

This suggests to explore indeterminacy instead. Indeed, Theorem 2 shows that all Benini distributions are moment-indeterminate. Two proofs are given, one utilizing a converse to the Carleman criterion due to Pakes (2001) and the other utilizing the Krein criterion (Stoyanov, 2000, 2013).

Theorem 2.

The Benini distribution is moment-indeterminate for any .

Proof 1. Pakes (2001, Th. 3) showed that if there exists such that for , the condition together with the convexity of the function on the interval implies moment indeterminacy. was shown in (3.3). For the Benini distribution, the function

is easily seen to be convex on the interval in view of .

Proof 2. In the case of a Stieltjes-type moment problem, the Krein criterion requires, for a strictly positive density and some , that the logarithmic integral

| (3.4) |

is finite. For the Benini distribution this integral is, choosing ,

This quantity is finite for all .

4 A Stieltjes class for the Benini distribution

The methods used in the proof of Theorem 2 only establish existence of further distributions possessing the same set of moments as the Benini distribution. It is known from Berg and Christensen (1981) that if a distribution is moment-indeterminate, then there exist infinitely many continuous and also infinitely many discrete distributions possessing the same moments. It is, therefore, of interest to find explicit examples of such objects.

A Stieltjes class (Stoyanov, 2004) corresponding to a moment-indeterminate distribution with density is a set

where is a perturbation function satisfying for all . If and , then is called a two-sided Stieltjes class. Counterexamples to moment determinacy in the literature are typically of this type. It is also possible to have one-sided Stieltjes classes, for which only needs to be bounded from below, and . The following Theorem provides a one-sided Stieltjes class for the Benini distribution.

Theorem 3.

The distributions with densities , ,

all have the same moments as the Benini distribution with density . Here is a normalizing constant defined in the proof.

Proof. Consider the (unscaled) perturbation

This perturbation has the following properties:

(P1). .

(P2). Basic properties of the sine function imply that on the interval .

(P3). On the interval , the function is continuous, with and . Hence is bounded there.

Let and set . It follows from (P1)–(P3) that is unbounded from above and bounded from below, specifically . By construction, . The moments of the corresponding random variable with density , , are further given by

It remains to show that . Now

in view of

| (4.1) |

for all . In particular, .

Note that Theorem 3 provides a further proof of the moment indeterminacy of the Benini distribution.

Apart from the shifted argument, the perturbation employed here draws on the pioneering work of Stieltjes (1894/1895). In modern terminology, Stieltjes showed that the relation (4.1) leads to a family of distributions whose moments coincide with those of a certain generalized gamma distribution, implying that the latter is moment-indeterminate.

Stieltjes (1894/1895) has a further, and more widely known, example of a distribution that is not determined by its moments, the lognormal distribution. The counterexample he provides for that distribution employs the perturbation

| (4.2) |

which was further developed by Heyde (1963). It can also lead to a Stieltjes class for the Benini distribution. However, note that in view of the exponential term common to both the lognormal and the Benini densities, the perturbation based on (4.2) only works for small values of , otherwise the resulting ratio diverges for . Methods outlined by Stoyanov and Tolmatz (2005) may help to construct Stieltjes classes based on (4.2) and the lognormal density that cover the entire range of the shape parameter , at the price of somewhat greater analytical complexity.

5 Related distributions

It is natural to augment Pareto’s equation (1.1) by higher-order terms going beyond the second-order term proposed by Benini (1905). Not surprisingly, curves of the form

| (5.1) |

soon began to appear in the subsequent Italian-language literature on economic statistics; see, e.g., Bresciani Turroni (1914) and Mortara (1917) for some early contributions. Somewhat later, the Austrian statistician Winkler (1950) independently also experimented with polynomials in . Specifically, he fitted a quadratic—i.e., the three-parameter Benini distribution (2.1)—to the U.S. income distribution of 1919.

Dropping a scale parameter, i.e. setting , eq. (5.1) gives the c.d.f.

| (5.2) |

where , with corresponding density

| (5.3) |

Using the Krein criterion it is not difficult to see that these generalized Benini distributions are moment-indeterminate, provided as otherwise not all moments exist.

A further generalization of the Benini distribution proceeds along different lines. In section 2 it was noted that the Benini distribution may be seen as the log-Rayleigh distribution, up to scale. It is then natural to consider the log-Weibull family, with c.d.f.

where , and corresponding density

References

- Benini (1905) Benini, R. (1905): “I diagrammi a scala logaritmica (a proposito della graduazione per valore delle successioni ereditarie in Italia, Francia e Inghilterra),” Giornale degli Economisti, Serie II, 16, 222–231.

- Benini (1906) ——— (1906): Principii di Statistica Metodologica, Torino: Unione Tipografica–Editrice Torinese.

- Berg and Christensen (1981) Berg, C. and J. P. R. Christensen (1981): “Density Questions in the Classical Theory of Moments,” Annales de l’Institut Fourier, 31, 99–114.

- Bresciani Turroni (1914) Bresciani Turroni, C. (1914): “Osservazioni critiche sul “Metodo di Wolf” per lo studio della distribuzione dei redditi,” Giornale degli Economisti e Rivista di Statistica, Serie IV, 25, 382–394.

- Gradshteyn and Ryzhik (2007) Gradshteyn, I. S. and I. M. Ryzhik (2007): Tables of Integrals, Series and Products, Amsterdam: Academic Press, 7th ed.

- Heyde (1963) Heyde, C. C. (1963): “On a Property of the Lognormal Distribution,” Journal of the Royal Statistical Society, Series B, 25, 392–393.

- Kleiber and Kotz (2003) Kleiber, C. and S. Kotz (2003): Statistical Size Distributions in Economics and Actuarial Sciences, Hoboken, NJ: John Wiley & Sons.

- Mortara (1917) Mortara, G. (1917): Elementi di Statistica, Rome: Athenaeum.

- Olver et al. (2010) Olver, F. W. J., D. W. Lozier, R. F. Boisvert, and C. W. Clark, eds. (2010): NIST Handbook of Mathematical Functions, Cambridge: Cambridge University Press.

- Pakes (2001) Pakes, A. G. (2001): “Remarks on Converse Carleman and Krein Criteria for the Classical Moment Problem,” Journal of the Australian Mathematical Society, 71, 81–104.

- Pareto (1895) Pareto, V. (1895): “La legge della domanda,” Giornale degli Economisti, 10, 59–68, English translation in Rivista di Politica Economica, 87 (1997), 691–700.

- Pareto (1896) ——— (1896): “La courbe de la répartition de la richesse,” in Recueil publié par la Faculté de Droit à l’occasion de l’Exposition Nationale Suisse, Genève 1896, Lausanne: Ch. Viret-Genton, 373–387, English translation in Rivista di Politica Economica, 87 (1997), 645–660.

- Pareto (1897) ——— (1897): Cours d’économie politique, Lausanne: Ed. Rouge.

- Shohat and Tamarkin (1950) Shohat, J. A. and J. D. Tamarkin (1950): The Problem of Moments, Providence, RI: American Mathematical Society, revised ed.

- Shpilberg (1977) Shpilberg, D. C. (1977): “The Probability Distribution of Fire Loss Amount,” Journal of Risk and Insurance, 44, 103–115.

- Stieltjes (1894/1895) Stieltjes, T. J. (1894/1895): “Recherches sur les fractions continues,” Annales de la Faculté des Sciences de Toulouse, 8/9, 1–122, 1–47.

- Stoyanov (2000) Stoyanov, J. (2000): “Krein Condition in Probabilistic Moment Problems,” Bernoulli, 6, 939–949.

- Stoyanov (2004) ——— (2004): “Stieltjes Classes for Moment-Indeterminate Probability Distributions,” Journal of Applied Probability, 41A, 281–294.

- Stoyanov (2013) ——— (2013): Counterexamples in Probability, New York: Dover Publications, 3rd ed.

- Stoyanov and Tolmatz (2005) Stoyanov, J. and L. Tolmatz (2005): “Methods for Constructing Stieltjes Classes for M-Indeterminate Probability Distributions,” Applied Mathematics and Computation, 165, 669–685.

- Winkler (1950) Winkler, W. (1950): “The Corrected Pareto Law and its Economic Meaning,” Bulletin of the International Statistical Institute, 32, 441–449.

- Wolfram Research, Inc. (2013) Wolfram Research, Inc. (2013): Mathematica, Version 9.0.1.0, Champaign, IL.