Abstract

We study the fair strike of a discrete variance swap for a general time-homogeneous stochastic volatility model. In the special cases of Heston, Hull-White and Schöbel-Zhu stochastic volatility models we give simple explicit expressions (improving Broadie and Jain \citeyearBJ08 in the case of the Heston model). We give conditions on parameters under which the fair strike of a discrete variance swap is higher or lower than that of the continuous variance swap. The interest rate and the correlation between the underlying price and its volatility are key elements in this analysis. We derive asymptotics for the discrete variance swaps and compare our results with those of Broadie and Jain \citeyearBJ08, Jarrow et al. \citeyearJ12 and Keller-Ressel and Griessler \citeyearKG12.

Key-words: Discrete Variance swap, Heston model, Hull-White model, Schöbel-Zhu model.

1 Introduction

A variance swap is a derivative contract that pays at a fixed maturity the difference between a given level (fixed leg) and a realized level of variance over the swap’s life (floating leg). Nowadays, variance swaps on stock indices are broadly used and highly liquid. Less standardized variance swaps could be linked to other types of underlying stocks such as currencies or commodities. They can be useful for hedging volatility risk exposure or for taking positions on future realized volatility. For example, Carr and Lee \citeyearCL07 price options on realized variance and realized volatility by using variance swaps as pricing and hedging instruments. See Carr and Lee \citeyearCL for a history of volatility derivatives. As noted by Jarrow et al. \citeyearJ12, most academic studies focus on continuously sampled variance and volatility swaps. However, existing volatility derivatives tend to be based on the realized variance computed from the discretely sampled log stock price and continuously sampled derivatives prices may only be used as approximations. As pointed out in Sepp \citeyearS, some care is needed to replace the discrete realized variance by the continuous quadratic variation. By standard probability arguments, the discretely sampled realized variance converges to the quadratic variation of the log stock price in probability. However, this does not guarantee that it converges in expectation. Jarrow et al. \citeyearJ12 provide sufficient conditions such that the convergence in expectation happens when the stock is modeled by a general semi-martingale, and concrete examples where this convergence fails.

In this paper we study discretely sampled variance swaps in a general time-homogeneous model for stochastic volatility. For discretely sampled variance swaps, it is difficult to use the elegant and model-free approach of Dupire \citeyearD93 and Neuberger \citeyearN94, who independently proved that the fair strike for a continuously sampled variance swap on any underlying price process with continuous path is simply two units of the forward price of the log contract. Building on these results, Carr and Madan \citeyearCM published an explicit expression to obtain this forward price from option prices (by synthesizing a forward contract with vanilla options). The Dupire-Neuberger theory was recently extended by Carr, Lee and Wu \citeyearCLW11 to the case when the underlying stock price is driven by a time-changed Lévy process (thus allowing jumps in the path of the underlying stock price). In this paper, we adopt a parametric approach that allows us to derive explicit closed-form expressions and asymptotic behaviors with respect to key parameters such as the maturity of the contract, the risk-free rate, the sampling frequency, the volatility of the variance process, or the correlation between the underlying stock and its volatility. This is in line with the work of Broadie and Jain \citeyearBJ08 in which the Heston model and the Merton jump diffusion model are considered. See also Itkin and Carr \citeyearIC who study discretely sampled variance swaps in the 3/2 stochastic volatility model.

Our main contributions are as follows. We give an expression of the fair strike of the discretely sampled variance swap and derive its sensitivity to the interest rate in a general time-homogeneous stochastic volatility model. In the case of the (correlated) Heston \citeyearH model, the (correlated) Hull-White \citeyearHW model, and the (correlated) Schöbel-Zhu \citeyearSZ99 model, we obtain simple explicit closed-form formulas for the respective fair strikes of continuously and discretely sampled variance swaps. In the Heston model, our formula simplifies the results of Broadie and Jain \citeyearBJ08 and is easy to analyze. Consequently, we are able to give asymptotic behaviors with respect to key parameters of the model and to the sampling frequency. In particular, we provide explicit conditions under which the fair strike of the discretely sampled variance swap is less valuable than that of the continuously sampled variance swap for high sampling frequencies, although the contrary is commonly observed in the literature (see Bühler \citeyearB for example). Thus the “convex-order conjecture" formulated by Keller-Ressel and Griessler \citeyearKG12 may not hold for stochastic volatility models with correlation. We discuss practical implications and illustrate the risk to underestimate or overestimate prices of discretely sampled variance swaps when using a model for the corresponding continuously sampled ones with numerical examples.

The paper is organized as follows. Section 2 deals with the general time-homogeneous stochastic volatility model. Sections 3, 4 and 5 provide formulas for the fair strike of a discrete variance swap in the Heston, the Hull-White and the Schöbel-Zhu models. Section 6 contains asymptotics for the Heston, the Hull-White and the Schöbel-Zhu models and discusses the “convex-order conjecture". A numerical analysis is given in Section 7.

2 Pricing Discrete Variance Swaps in a Time-homogeneous Stochastic Volatility Model

In this section, we consider the problem of pricing a discrete variance swap under the following general time-homogeneous stochastic volatility model , where the stock price and its volatility can possibly be correlated. We assume a constant risk-free rate , and that under a risk-neutral probability measure Q

|

|

|

(1) |

where , with , standard correlated Brownian motions. The state space of the stochastic variance process is . Assume that are Borel functions satisfying the following Engelbert-Schmidt conditions,

.

Here denotes the class of locally integrable functions, i.e. the functions that are integrable on compact subsets of . Under the above conditions, the SDE (1) for has a unique in law weak solution that possibly exits its state space (see Theorem , page 341, Karatzas and Shreve \citeyearKS91). Assume that is differentiable at all .

In particular, this general model includes the Heston, the Hull-White, the Schöbel-Zhu, the and the Stein-Stein models as special cases. In what follows, we study discretely and continuously sampled variance swaps with maturity . In a variance swap, one counterparty agrees to pay at a fixed maturity a notional amount times the difference between a fixed level and a realized level of variance over the swap’s life. If it is continuously sampled, the realized variance corresponds to the quadratic variation of the underlying log price. When it is discretely sampled, it is the sum of the squared increments of the log price. Define their respective fair strikes as follows.

Definition 2.1.

The fair strike of the discrete variance swap associated with the partition of the time interval is defined as

|

|

|

|

(2) |

where the underlying stock price follows the time-homogeneous stochastic volatility model (1) and where the exponent refers to the model .

Definition 2.2.

The fair strike of the continuous variance swap is defined as

|

|

|

|

(3) |

where follows the time-homogeneous stochastic volatility model (1).

In popular stochastic volatility models, , so that . The derivation of the fair strike of a discrete variance swap in the time-homogeneous stochastic volatility model (1) is based on the following proposition.

Proposition 2.1.

Under the dynamics (1) for the stochastic volatility model , define

|

|

|

For all and , assume that

|

|

|

|

|

|

(4) |

Define for ,

|

,

|

,

|

|

,

|

,

|

|

|

|

|

|

|

|

|

|

|

(5) |

Proof. See Appendix A.

Proposition 2.1 gives the key equation in the analysis of discrete variance swaps. Observe that the final expression (5) only depends on covariances of functionals of . Thus we can derive closed-form formulas for the fair strike of discrete variance swaps in those stochastic volatility models in which the terms from Proposition 2.1 can be computed in closed-form.

In the rest of the paper, we provide three examples to apply this formula.

From now on, for simplicity, we consider the equi-distant sampling scheme in (2). Under this scheme, and , for .

Remark 2.1.

From (5) it is clear that the fair strike of a discrete variance swap only depends on the risk-free rate up to the second order, as there is no higher order terms of . Interestingly, the second order coefficient of this expansion is model-independent whereas the first order coefficient is directly related to the strike of the corresponding continuously-sampled variance swap. Assume a constant sampling period , the fair strike of the discrete variance swap can be expressed as

|

|

|

|

(6) |

where does not depend on . Its sensitivity to the risk-free rate is equal to

|

|

|

(7) |

so that the minimum of as a function of is attained when the risk-free rate takes the value given by

|

|

|

The next proposition deals with the special case when the risk-free rate and the correlation coefficient are both equal to 0.

Proposition 2.2.

(Fair strike when and )

In the special case when the constant risk-free rate is 0, and the underlying stock price is not correlated to its volatility, we observe that

|

|

|

Proof. Using Proposition 2.1 when and , we obtain

|

|

|

|

We then add up the expectations of the squares of the log increments (as in (2)) and find that the fair strike of the discrete variance swap is always larger than the fair strike of the continuous variance swap given in (3).

Proposition 2.2 has already appeared in the literature in specific models. See for example Corollary of Carr, Lee and Wu \citeyearCLW11, where this result is proved in the more general setting of time-changed Lévy processes with independent time changes. However, we will see in the remainder of this paper that Proposition 2.2 may not hold under more general assumptions, namely when the dynamic of the stock price is correlated to the one of the volatility.

3 Fair Strike of the Discrete Variance Swap in the Heston model

Assume that we work under the Heston stochastic volatility model with the following dynamics

|

|

|

(8) |

where . It is a special case of the general model (1), where we choose

|

|

|

|

(9) |

Using (29) in Lemma A.1 in the Appendix with and , the stock price is

|

|

|

|

(10) |

where and is such that .

Using Proposition 2.1 for the time-homogeneous stochastic volatility model, we then derive a closed-form expression for the fair strike of a discrete variance swap and compare it with the fair strike of a continuous variance swap.

Proposition 3.1.

(Fair Strikes in the Heston Model)

In the Heston stochastic volatility model (8),

the fair strike (2) of the discrete variance swap is

|

|

|

|

|

|

(11) |

|

|

|

|

|

|

where and . The fair strike of the continuous variance swap is

|

|

|

|

(12) |

Proof. See Appendix B for the proof of (11). The formula (12) for the fair strike of a continuous variance swap is already well-known and can be found for example in Broadie and Jain \citeyearBJ08, formula , page 772.

Proposition 3.1 provides an explicit formula for the fair strike of a discrete variance swap as a function of model parameters. This formula simplifies the expressions obtained by Broadie and Jain \citeyearBJ08 in equations (A-29) and (A-30), page 793, where several sums from 0 to are involved and can actually be computed explicitly as shown by the expression (11) above. We verified that our formula agrees with numerical examples presented in Table 5 (column ‘SV’) on page 782 of Broadie and Jain \citeyearBJ08.

Contrary to what is stated in the introduction of the paper by Zhu and Lian \citeyearZL, the techniques of Broadie and Jain \citeyearBJ08 can easily be extended to other types of payoffs. The following proposition gives explicit expressions for the volatility derivative considered by Zhu and Lian \citeyearZL.

Proposition 3.2.

For the following set of dates with , denote , and assume , and . Then the fair price of a discrete variance swap with payoff is equal to

|

|

|

|

where we define , for . Then for , we have

|

|

|

where

|

|

|

|

with the following auxiliary functions

|

|

|

|

|

|

|

|

|

|

Proof.

See Appendix C.

Remark 3.1.

The formula in the above Proposition 3.2 is consistent with the one obtained in equation (2.34) by Zhu and Lian \citeyearZL. In particular, we are able to reproduce all numerical results but one presented in Table , page of Zhu and Lian \citeyearZL using their set of parameters: , , , , , , and (all numbers match except the case when we get 263.2 instead of 267.6).

Proposition 3.2 gives a formula for pricing the variance swap with payoff , but it is straightforward to extend its proof to the following payoff , with an arbitrary integer power .

6 Asymptotics

In the time-homogeneous stochastic volatility model, this section presents asymptotics for the fair strikes of discrete variance swaps in the Heston, the Hull-White and the Schöbel-Zhu models based on the explicit expressions derived in the previous sections 3, 4 and 5.

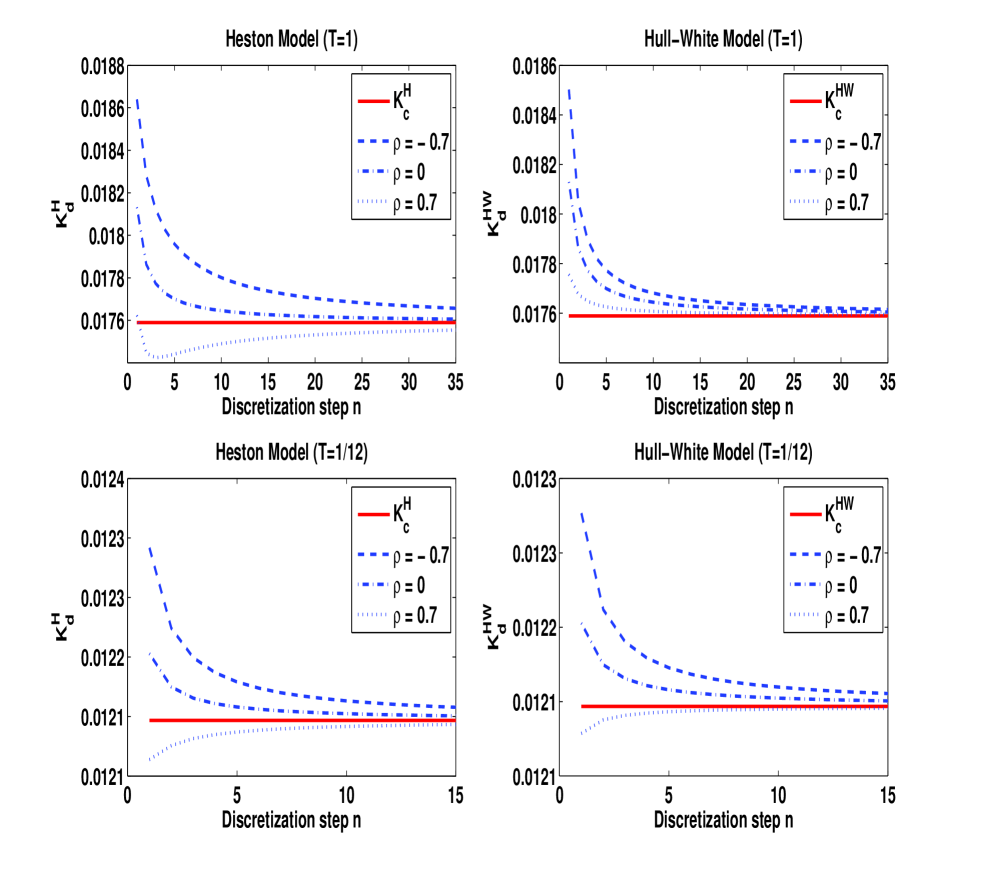

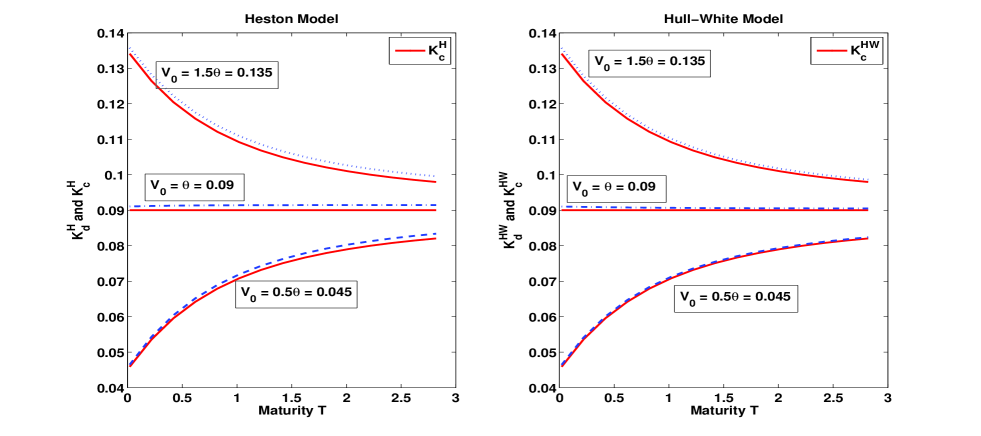

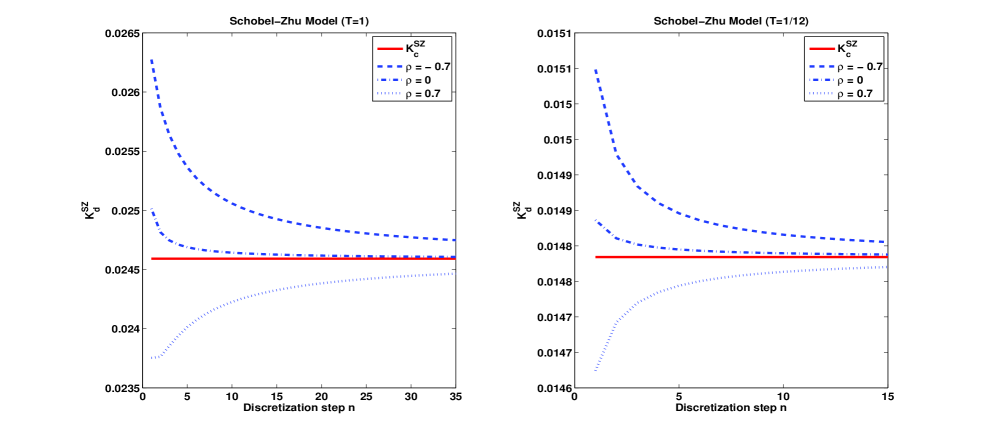

The expansions as functions of the number of sampling periods are given in Propositions 6.1, 6.4 and 6.7 (respectively for the Heston, Hull-White and Schöbel-Zhu models). In the Heston model, our results are consistent with Proposition 4.2 of Broadie and Jain \citeyearBJ08, in which it is proved that . The expansion below is more precise in that at least the first leading term in the expansion is given explicitly. See also Theorem 3.8 of Jarrow et al. \citeyearJ12 in a more general context. In particular, Jarrow et al. \citeyearJ12 give a sufficient condition for the convergence of the fair strike of a discrete variance swap to that of a continuously monitored variance swap. In our setting, which is in the absence of jumps, their sufficient condition reduces to . This latter condition is obviously satisfied in the three examples considered in this paper (the Heston, the Hull-White and the Schöbel-Zhu models).

Expansions as a function of the maturity (for small maturities) are also given in order to complement results of

Keller-Ressel and Muhle-Karbe \citeyearKM12 (see for example Corollary which gives qualitative properties of the discretization gap as the maturity ).

6.1 Heston Model

We first expand the fair strike of the discrete variance swap with respect to the number of sampling periods .

Proposition 6.1.

(Expansion of the fair strike w.r.t. )

In the Heston model, the expansion of the fair strike of a discrete variance swap, , is given by

|

|

|

|

(20) |

where

|

|

|

with

|

|

|

Proof. This proposition is a straightforward expansion from (11) in Proposition 3.1.

We know that from (6) in Remark 2.1. It is thus clear that contains all the terms in the risk-free rate and thus that all the higher terms in the expansion (20) with respect to are independent of the risk-free rate.

Remark 6.1.

The first term in the expansion (20), , is a linear function of . Observe that the coefficient in front of , is negative, so that is always a decreasing function of . We have that

|

|

|

where

Proposition 6.2.

(Expansion of the fair strike for small maturity)

In the Heston model, can be expanded when as

|

|

|

(21) |

where

|

|

|

|

|

|

|

|

Note also that

and thus

|

|

|

Proof. This proposition is a straightforward expansion from (11) in Proposition 3.1.

Proposition 6.2 is consistent with Corollary 2.7 [b] on page of Keller-Ressel and Muhle-Karbe \citeyearKM12, where it is clear that the limit of is when .

Notice that in the case , in the Heston model, is non-negative and decreasing in as the maturity goes to 0. However, this property cannot be generalized to all correlation levels as it depends on the sign of .

Proposition 6.3.

(Expression of the fair strike w.r.t. )

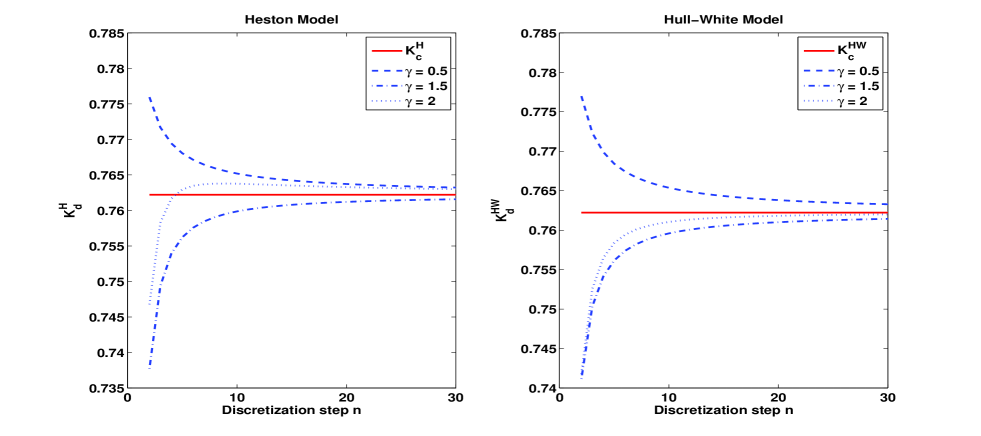

In the Heston model, is a quadratic function of :

|

|

|

(22) |

where

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Proposition 6.3 shows that the discrete fair strike in the Heston model is a quadratic function of the volatility of variance . From Figure 6, we observe that the discrete fair strikes evolve in a parabolic shape as varies.

6.2 Hull-White Model

Proposition 6.4.

(Expansion of w.r.t. )

In the Hull-White model, the expansion of the fair strike of the discrete variance swap, , is given by

|

|

|

(23) |

where

|

|

|

|

|

|

|

|

|

|

|

|

Proof. This proposition is a straightforward expansion from (15) in Proposition 4.1.

Observe that where is independent of .

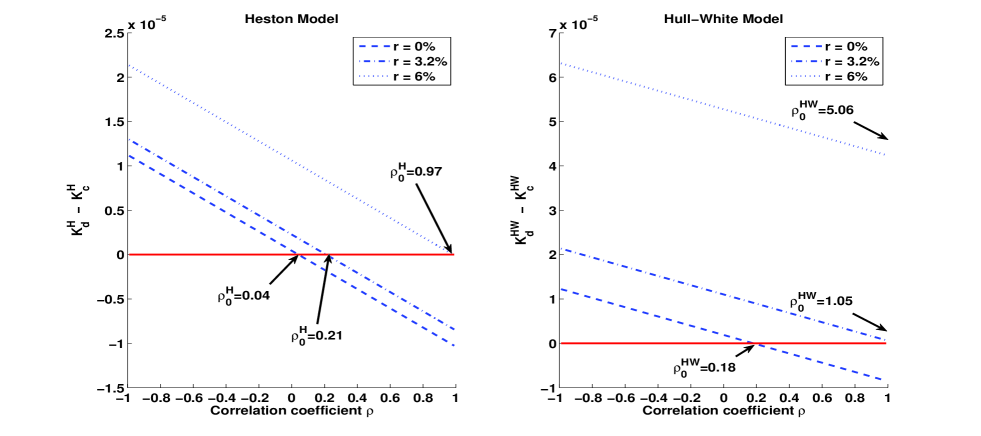

If we neglect higher order terms in the expansion (23), we observe that the position of the fair strike of the discrete variance swap with respect to the fair strike of the continuous variance swap is driven by the sign of and we have the following observation.

Remark 6.2.

The first term in the expansion (23), , is a linear function of .

|

|

|

where

can take values strictly larger than 1 as it appears clearly in the right panel of Figure 4. In this latter case, the fair strike of the discrete variance swap is larger than the fair strike of the continuous variance swap for all levels of correlation and for sufficiently high values of . The minimum value of as a function of is obtained when . After replacing by in the expression of , can easily be shown to be positive.

Proposition 6.5.

(Expansion of for small maturity)

In the Hull-White model, can be expanded when as

|

|

|

(24) |

where

|

|

|

|

|

|

|

|

|

|

|

|

Note also that

and thus

|

|

|

Proof. This proposition is a straightforward expansion from (15) in Proposition 4.1.

Note that the expansion for small maturities in the Hull White model is similar to the one in the Heston model given in Proposition 6.2.

Proposition 6.6.

(Expansion of w.r.t. )

In the Hull-White model, the fair strike of a discrete variance swap, , verifies

|

|

|

(25) |

where

|

|

|

|

|

|

|

|

The expansion of the fair strike in the Hull-White model with respect to the volatility of volatility is very different from the one in the Heston model as it is not a quadratic function of , and it also involves higher order terms of .

6.3 Schöbel-Zhu Model

We first expand the fair strike of the discrete variance swap with respect to the number of sampling periods . The following result is similar to Proposition 6.1 and 6.4. In particular we find that the first term in the expansion is also linear in and has a similar behaviour as in the Heston and Hull-White model.

Proposition 6.7.

(Expansion of w.r.t. )

In the Schöbel-Zhu model, the expansion of the fair strike of the discrete variance swap, , is given by

|

|

|

|

(26) |

where

|

|

|

|

(27) |

with

|

|

|

and

|

|

|

where

|

|

|

Proof. This proposition is a straightforward expansion from the formula of in Proposition 5.1. Note that although the formula of does not have a simple form, its asymptotic expansion can be easily computed with Maple for instance.

Remark 6.3.

Similarly as in the Heston and the Hull-White models, the first term in the expansion (26), , is a linear function of , but the sign of its slope is not clear in general.

Proposition 6.8.

(Expansion of the fair strike for small maturity)

In the Schöbel-Zhu model, can be expanded when as

|

|

|

(28) |

where

|

|

|

Note also that

and thus,

|

|

|

Proof. This proposition is a straightforward expansion from the formula of in Proposition 5.1.

Note that the form of the expansion is similar for the three models under study (compare Propositions 6.2, 6.5 and 6.8). We find that the difference between the discrete and the continuous strikes has a first term involving the product of by a function of the initial variance value and the volatility of the variance process, and respectively in the Heston, in the Hull-White and in the Schöbel-Zhu model. See for example footnote 9 where the dynamics of the variance is derived in the Schöbel-Zhu model.

6.4 Discussion on the convex-order conjecture

As motivated in Keller-Ressel and Griessler \citeyearKG12, it is of interest to study the systematic bias for fixed and when using the quadratic variation to approximate the realized variance. Bühler \citeyearB and Keller-Ressel and Muhle-Karbe \citeyearKM12 show numerical evidence of this bias (see also Section 7 for further evidence in the Heston and the Hull-White models). Keller-Ressel and Griessler \citeyearKG12 propose the following “convex-order conjecture”:

|

|

|

where is convex, refers to the partition of in division points and . is the discrete realized variance () and is the continuous quadratic variation ( in our setting).

When and the correlation can be positive, the conjecture is violated, see for example Figure 1 to 4 where can be below . When , the process has conditionally independent increments and satisfies other assumptions in Keller-Ressel and Griessler \citeyearKG12. Proposition 2.2 ensures that , which is consistent with their results.

Appendix A Proof of Proposition 2.1

Using It’s lemma and Cholesky decomposition, (1) becomes

|

|

|

|

|

|

|

|

|

|

where and are two standard independent Brownian motions.

Proposition 2.1 is then a direct application of the following lemma (see Lemma of Bernard and Cui \citeyearBC11 for its proof).

Lemma A.1.

Under the model given in (1), we have

|

|

|

(29) |

where

and

Now from equation (29) in Lemma A.1, we compute the following key elements in the fair strike of the discrete variance swap. Assume that the time interval is , then

|

|

|

|

|

|

|

|

Then we can compute

|

|

|

|

|

|

(30) |

where and

|

|

|

|

Using the above expressions for and in (30), we obtain

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(31) |

By It’s lemma, defined in Lemma A.1 verifies

Integrating the above SDE from to , we have

|

|

|

|

Thus

|

|

|

|

(32) |

Rearrange (31) and use (32) to simplify the terms, and we obtain

|

|

|

(33) |

Now we apply Fubini’s theorem and partial integration to further simplify (33). Note that , Q-a.s., then by Fubini’s theorem for non-negative measurable functions, .

Similarly we have for any and any ,

If for any and any , then we have .

If for any and any , then we have

|

|

|

If for all , then we have

|

|

|

|

|

|

Thus we finally have proved (5) from Proposition 2.1. This completes the proof.

Appendix B Proof of Proposition 3.1

Proof. We apply Proposition 2.1 to the Heston stochastic volatility model. We first compute and , then we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(34) |

Furthermore, for all

|

|

|

(35) |

and for all

|

|

|

|

|

|

|

|

(36) |

In particular, this formula holds for and gives . These formulas already appear in Broadie and Jain \citeyearBJ08 (formula (A-15)). To compute , (35) and (36) are the only expressions needed, and they should then be integrated and summed.

We have computed all terms in (34) with the help of Maple and also have simplified the final expression given by Maple. It turns out that in the case of the Heston model, all terms can be computed explicitly and the final simplified expression for (34) does not require any sums or integrals. We finally obtain an explicit formula for as a function of the parameters of the model. This completes the proof.

Appendix C Proof of Proposition 3.2

Proof. Denote the log stock price without drift as , and . Denote , . We have that . Thus the goal is to calculate the second moment , and note that it is closely linked to the moment generating function of the log stock price . Recall the following formulation of the moment generating function from Albrecher et al. \citeyearA

|

|

|

|

|

|

|

|

(37) |

where the auxiliary functions are given by

|

|

|

|

We first separate out the case of and . For the first case, we have

|

|

|

|

(38) |

For the second case, with , we have

|

|

|

|

|

|

|

|

|

|

|

|

(39) |

We first define , and . Then from Theorem in Hurd and Kuznetsov \citeyearHK08, we have

|

|

|

|

(40) |

Combine equations (39) and (40), for , we finally have

|

|

|

(41) |

where . Using the definition of , we can factor out from (41) and finally we have

|

|

|

(42) |

When , we have and since as , we use L’Hôpital’s rule

|

|

|

|

Thus is a special case of the formula in (42) when .

From Theorem in Hurd and Kuznetsov \citeyearHK08, equation (37) and consequently the above (39), (40) are well-defined if . Note that the formula (42) involves the case. A sufficient condition for to hold is (since is equivalent to ).

Then the final formula for the discrete fair strike follows by summing the above terms . This completes the proof.

Appendix D Proof of Proposition 4.1

Proof. For the Hull-White model, from Proposition 2.1, we first compute and , then we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

with .

We now compute the following covariance terms that are useful in the simplification of the fair strike . In the Hull-White model, the stochastic variance process follows a geometric Brownian motion. Thus we have

.

Note that

|

|

|

which will be useful below for , and .

|

|

|

The fair strike for the continuous variance swap is straightforward and is equal to

Similarly

|

|

|

|

and for , we have the following results

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(43) |

After some tedious calculations with the help of Maple, we can obtain an explicit formula as the one appearing in Proposition 4.1. This completes the proof.

Appendix E Proof of Proposition 5.1

Proof. For the Schöbel-Zhu model, from the key equation in Proposition 2.1, we have

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(45) |

|

|

|

|

|

|

|

|

|

|

and .

We compute the following two terms in (E) by expanding the products out. For

|

|

|

|

|

|

|

|

|

|

|

|

and for

|

|

|

|

|

|

|

|

|

|

|

|

It is clear from the above expressions of for that they are all functions of , , , , , and . We now compute these seven expressions.

Lemma E.1.

For the Ornstein-Uhlenbeck process , introduce the auxiliary deterministic functions , and , then

|

|

|

|

(46) |

|

|

|

|

(47) |

|

|

|

|

(48) |

|

|

|

|

(49) |

For

|

|

|

|

|

|

|

|

|

|

|

|

(50) |

For

|

|

|

|

|

|

|

|

(51) |

For

|

|

|

|

(52) |

Proof. The stochastic variance process follows

|

|

|

|

On page 120 of Jeanblanc, Yor and Chesney \citeyearJYC09, one finds that the exact solution of the above SDE is

|

|

|

|

We can compute

|

|

|

|

(53) |

|

|

|

|

(54) |

and the higher moments can also be computed

|

|

|

|

(55) |

|

|

|

|

(56) |

|

|

|

|

(57) |

For , , and

|

|

|

|

|

|

|

|

|

|

|

|

Now we can compute the continuous fair strike as

|

|

|

|

|

|

|

|

(58) |

For

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

In the above expressions, the moments , , and are already calculated in (53), (55), (56), and (57). Then we can substitute the corresponding inputs into equation (E), sum up the terms, and obtain . This completes the proof.