The dimension of the St. Petersburg game

Abstract.

Let be the total gain in repeated St. Petersburg games. It is known that converges in distribution to a random element along subsequences of the form with and . We determine the Hausdorff and box-counting dimension of the range and the graph for almost all sample paths of the stochastic process . The results are compared to the fractal dimension of the corresponding limiting objects when gains are given by a deterministic sequence initiated by Hugo Steinhaus.

Key words and phrases:

St. Petersburg game, semistable process, sample path, semi-selfsimilarity, range, graph, Hausdorff dimension, Steinhaus sequence, iterated function system, self-affine set2010 Mathematics Subject Classification:

Primary 60G17; Secondary 28A78, 28A80, 60G18, 60G22, 60G52.1. Introduction

The famous St. Petersburg game is easily formulated as a simple coin tossing game. The player’s gain in a single game can be expressed by means of the stopping time of repeated independent tosses of a fair coin until it first lands heads. For a sequence of gains in independent St. Petersburg games the partial sum denotes the total gain in the first games. To find a fair entrance fee for playing the game is commonly called the St. Petersburg problem, frequently raised to the status of a paradox. Since the expectation is infinite, a fair premium cannot be constructed by the help of the usual law of large numbers. We refer to Jorland [21] and Dutka [10] for the history of the St. Petersburg game and for early solutions of the 300 year old problem.

The first step towards a mathematically satisfactory solution has been achieved by Feller [16, 17] who showed that a time-dependent premium can fulfill a certain weak law of large numbers

where denotes logarithm to the base . However, Feller’s result does not tell if the game is dis- or advantageous for the player, i.e. if is likely to be negative or positive. This question can only be answered by a weak limit theorem and the first theorem of this kind has been shown by Martin-Löf [24] for the subsequence

The limit is infinitely divisible with characteristic function , where

and the Lévy measure is concentrated on with for . Hence is a semistable random variable and the corresponding Lévy process with is a (non-strictly) semistable Lévy process fulfilling the semi-selfsimilarity condition

For details on semistable random variables and Lévy processes we refer to the monographs [26, 30]. The nature of semistability is that there exists in general a continuum of possible limit distributions. For the St. Petersburg game the possible limit distributions have been characterized by Csörgő and Dodunekova [5] who proved that for any subsequence with

we have

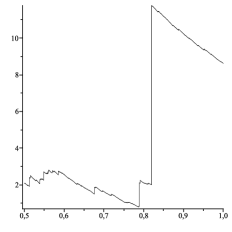

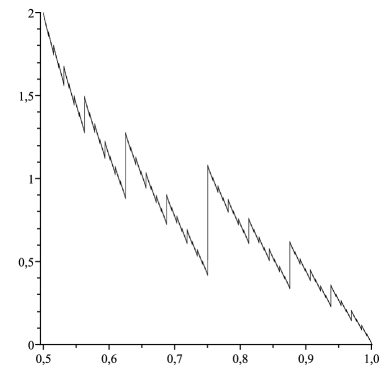

The object of our study are local fluctuations of the sample paths of the stochastic process consisting of all the possible weak limits of normalized total gains in repeated St. Petersburg games. Figure 1 shows typical (approximative) sample paths of generated by simulated St. Petersburg games.

Note that the sample paths do only have upward jumps due to the fact that the Lévy measure is concentrated on .

The main goal of our paper is to determine the Hausdorff dimension of the range and the graph of the stochastic process encoding all the possible distributional limits of St. Petersburg games. For an arbitrary subset the -dimensional Hausdorff measure is defined as

where denotes the diameter of a set . It can now be shown that there exists a unique value so that for all and for all . This critical value is called the Hausdorff dimension of . Specifically, we have

For details on the Hausdorff dimension we refer to [14, 25].

An alternative fractal dimension is the so called box-counting dimension (see, e.g., [14]). For this purpose let be the smallest number of closed balls of radius that cover the set . The lower and the upper box-counting dimensions of an arbitrary set are now defined as

and the box-counting dimension of is given by

provided that this limit exists. The different fractal dimensions are related as follows:

| (1.1) |

Note that there are plenty of sets where these inequalities are strict.

In Section 2 we will determine the Hausdorff and box-counting dimension of the range and the graph for almost all sample paths of the stochastic process . Additionally, in Section 3 we will also consider a deterministic sequence introduced by Steinhaus [31] which is called the “Steinhaus sequence” according to [7]. The Steinhaus sequence is defined by if for some and . Alternatively, as in Vardi [34], one can define to be twice the highest power of dividing . The Steinhaus sequence is explicitly given by

and has relative frequencies for . The sequence has been considered as time-dependent entrance fees for repeated St. Petersburg games in [31, 7] and has been proven to be a sequence of nearly asymptotically fair premiums in a certain sense. For details we refer to [7]. In contrast to [31, 7] we will consider the Steinhaus sequence as a sequence of possible gains in repeated St. Petersburg games. Again, we will determine the Hausdorff and box-counting dimension of the range and the graph of the specific sample path of resulting as a limiting object of the Steinhaus sequence. To do so, we will employ results for iterated function systems as presented in [15].

2. Hausdorff dimension of the St. Petersburg game

2.1. Hausdorff dimension of the range

In this section we evaluate the Hausdorff dimension of the range of the stochastic process . We employ common techniques used to calculate Hausdorff dimensions of selfsimilar Lévy processes (see [35, 27, 23]) and adapt them to our situation. Note that the given process is neither a Lévy process nor does it have the selfsimilarity property of a semistable process. The result is stated in the theorem below.

Theorem 2.1.

We have almost surely.

Note that Theorem 2.1 together with (1.1) yields almost surely. Since is a process on it is obvious that almost surely. For the proof of Theorem 2.1 it is hence sufficient to prove the following lemma.

Lemma 2.2.

We have almost surely.

Proof.

As mentioned above we can write

where is a semistable Lévy process. To prove the proposition we will apply Frostman’s theorem [22, 25] with the probability measure , where denotes Lebesgue measure. For this purpose let and note that is an admissible measure for Frostman’s lemma, i.e.

By Frostman’s theorem it is now sufficient to show that

| (2.1) |

For let be a Lebesgue density of chosen from the class by Proposition 2.8.1 in [30]. Then we have as in Lemma 2.2 of [23]. By symmetry of the integrand we get

where in the last equality we substituted . Now we write as with and . This leads us to

Using the substitutions and we get

where denotes the set . We now estimate the two integrals separately. First,

and secondly,

This leads us to

Taken all together, we obtain

since . This concludes our proof. ∎

2.2. Hausdorff dimension of the graph

In this section we show that the dimension result for the range of the stochastic process also holds for its graph . We will split the proof into two parts, first verifying as an upper bound and secondly as a lower bound for the Hausdorff dimension of the graph.

We first calculate the upper bound for the Hausdorff dimension of the graph of the semistable Lévy process and later on transfer the result to the process . As is not strictly semistable we can’t use the dimension results of [23], without modifying it according to our situation. Note that for the strictly stable (symmetric) Cauchy process on it is known that the Hausdorff dimension of the range coincides with those of an asymmetric (non-strictly) stable Cauchy process; see [2, 19, 32].

Theorem 2.3.

Let . Then almost surely

Let denote the sojourn time of the Lévy process up to time in the closed ball with radius centered at the origin. To prove Theorem 2.3 we need the following lemma.

Lemma 2.4.

Let be the stochastic process from above. There exists a positive and finite constant such that for all and we have

Proof.

Fix and let , to be specified later, so that

for some . We have

The probability from above can be estimated from below by

if we choose large enough so that for all . As is a Lévy process, we can assume that it has càdlàg paths and thus both and are random variables. Hence we can choose from above small enough (i.e., even bigger) so that we have

Note that does not depend on . It follows that

which concludes the proof. ∎

Proof of Theorem 2.3.

Let be a fixed constant. A family of cubes of side in is called -nested if no ball of radius in can intersect more than cubes of . For any let be the number of cubes hit by the Lévy process at some time . Then a famous covering lemma of Pruitt and Taylor [29, Lemma 6.1] states that

Lemma 2.4 now enables us to construct a covering of whose expected -dimensional Hausdorff measure is finite for every . The arguments are in complete analogy to the proof of part (i) of Lemma 3.4 in [23] and thus omitted. ∎

In order to transfer the result of Theorem 2.3 to the process we can now write all elements as

It can easily be shown that for a fixed constant the function

is bi-Lipschitz. Since is a Lévy process, it can be assumed that all paths are cádlág and hence that for all fixed there exists a constant such that

This means that for and all we have

by Lemma 1.8 in [11]. Since we have shown in Theorem 2.3 that almost surely, we have thus proven the following upper bound.

Theorem 2.5.

We have almost surely.

To prove the lower bound for the Hausdorff dimension of the graph we can use the same technique as for the lower bound in case of the range of .

Theorem 2.6.

We have almost surely.

With similar techniques it is also possible to proof the following dimension result for the box-counting dimension of the graph of the St. Petersburg process .

Theorem 2.7.

We have almost surely.

Proof.

The lower bound follows directly from the almost sure inequalities

For the upper bound it is now sufficient to verify almost surely. With similar arguments as in the proof of Theorem 2.3 we can show that almost surely; see also the proof of Lemma 3.5 in [27]. With the bi-Lipschitz invariance of the upper box-counting dimension (see section 3.2 in [14]) the proof concludes. ∎

Remark 2.8.

If one prefers to flip an unfair coin this naturally leads to so called generalized St. Petersburg games as treated in [6, 18, 28]. Let be the probability of the coin falling heads and let . Then a gain of in a single St. Petersburg game results in the limit theorem

in distribution, whenever

where is a semistable Lévy process with the semi-selfsimilarity property

We emphasize that with the above techniques our Theorems 2.1, 2.5, 2.6 and 2.7 also hold for the process in this generalized situation when replacing the interval by .

3. Hausdorff dimension of the Steinhaus sequence

Recall the definition of the Steinhaus sequence given in the Introduction. The asymptotic properties of have been analyzed in full detail by Csörgő and Simons [7]. Let and then by Theorem 3.3 in [7] we have for any

| (3.1) |

where the function is defined by

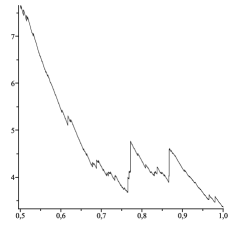

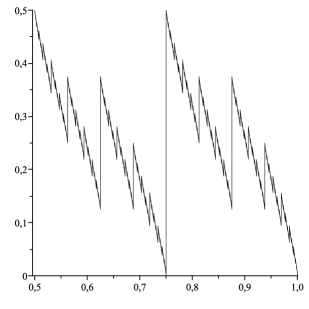

and the sequence is given by the dyadic expansion of with the convention that for infinitely many . By Theorem 3.1 in [7] the function is càdlàg with and has jumps precisely at the dyadic rationals in . All these jumps are upward and the largest jump occurs from to . The graph of seems to inhere fractal properties as can be seen in Figure 2 below, a replication of Figure 1 in [7].

It follows directly from (3.1) that the sequence of total gains satisfies the asymptotic property of Feller

| (3.2) |

as ; see [7]. Moreover, for any sequence with we get from (3.1)

where denotes the set of accumulation points. Hence we may consider the function as the corresponding limiting sample path of . Note that (3.2) shows that the Steinhaus sequence is an exceptional sequence of gains when considering almost sure limit behavior, since Feller’s law of large numbers does not hold in an almost sure sense. According to classical results in [3, 1, 8] it is known that

| (3.3) |

More precisely, by Corollary 1 in [34] we have almost surely, but there is a version of the strong law of large numbers by [9] when neglecting the largest gain

A comparison of (3.2) and (3.3) shows that the Steinhaus sequence belongs to an exceptional nullset concerning almost sure limit behavior of the total gain in repeated St. Petersburg games. We will now show that the Steinhaus sequence is not exceptional concerning the local fluctuations of the limiting sample paths measured by the Hausdorff or box-counting dimension.

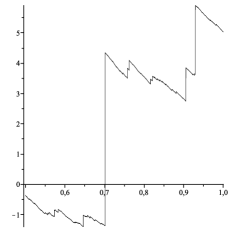

It follows directly from the above stated properties of given in Theorem 3.1 of [7] that the range is equal to the interval and hence by Theorem 1.12 in [11]. This shows that coincides with the Hausdorff dimension of the range of a typical sample path of . Clearly, by (1.1) we also have . A look at Figure 2 suggests that it is merely the graph and not the range of that should inhere fractal properties. In the sequel we will argue that also the graph is typical concerning the almost sure dimension properties of the sample graph of . To this aim we will again apply the bi-Lipschitz function from Section 2 whose inverse is given by with . Applied to the graph of we get for any

and by bi-Lipschitz invariance we have

| (3.4) |

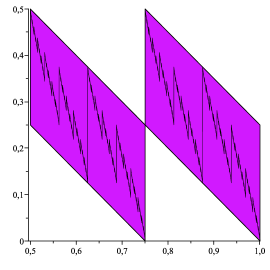

The same equality holds for upper and lower box-counting dimensions; e.g., see [14]. The image is illustrated in Figure 3 and shows perfect selfsimilarity. To see this, we may write with .

Lemma 3.1.

Let be the function from above. Then for any we have

Proof.

For the dyadic expansion of we necessarily have . Consequently,

| and | ||||

It follows that

This shows and furthermore we get

concluding the proof. ∎

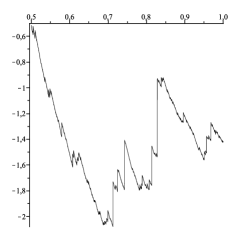

Let be the affine contractions given by

Then it follows from Lemma 3.1 that for any

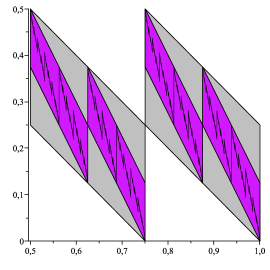

These contraction properties are illustrated in Figure 4 and show that the image can be generated by an iterated function system.

By Hutchinson [20] there exists a unique non-empty compact set , called the attractor, such that which fulfills

Our construction shows that for with dyadic expansion we have and

as , where for and . Since we required for infinitely many , the only limit points missing are those with for all but finitely many . For these we have

for a dyadic rational . The above arguments show that is the closure of and since the dyadic rationals are countable, by elementary properties of the Hausdorff dimension and (3.4) we get

| (3.5) |

The same equality holds for upper and lower box-counting dimensions; e.g., see [14].

A common way to calculate the fractal dimension of the self-affine invariant set is by means of the singular value function. For on overview of such methods we refer to [15]. The linear part of both affine mappings and is equal to the linear contraction with associated matrix

By induction one easily calculates for

and the singular values of are the positive roots of the eigenvalues of which calculate as

| (3.6) |

These determine the singular value function of for given by

Now the affinity dimension of is defined by

| (3.7) |

and the special form of the singular values in (3.6) shows that .

Since the union is disjoint, by Proposition 2 in [13] we get a lower bound for the Hausdorff dimension of

| (3.8) |

Again, by induction one easily calculates for

and the singular values of are

which shows that by (3.8). Since by [12] we have

altogether the above calculations show:

Theorem 3.2.

We have

This shows that the graph of , being the limiting object of the Steinhaus sequence (considered as a possible sequence of total gains in repeated St. Petersburg games), is not exceptional concerning the Hausdorff or box-counting dimension of the sample graph calculated in Section 2.

References

- [1] Adler, A. (1990) Generalized one-sided laws of the iterated logarithm for random variables barely with or without finite mean. J. Theoret. Probab. 3 587–597.

- [2] Blumenthal, R.M.; and Getoor, R.K. (1960) A dimension theorem for sample functions of stable processes. Illinois J. Math. 4 370–375.

- [3] Chow, Y.S.; and Robbins, H. (1961) On sums of independent random variables with infinite moments and “fair” games. Proc. Nat. Acad. Sci. USA 47 330–335.

- [4] Csörgő, S. (2010) Probabilistic approach to limit theorems for the St. Petersburg game. Acta Sci. Math. (Szeged) 76 233–350.

- [5] Csörgő, S.; and Dodunekova, R. (1991) Limit theorems for the Petersburg game. In: M.G. Hahn et al. (Eds.) Sums, Trimmed Sums and Extremes. Progress in Probability, Vol. 23, Birkhäuser, Boston, pp. 285–315.

- [6] Csörgő, S.; and Kevei, P. (2008) Merging asymptotic expansions for cooperative gamblers in generalized St. Petersburg games. Acta Math. Hungar. 121 119–156.

- [7] Csörgő, S.; and Simons, G. (1993) On Steinhaus’ resolution of the St. Petersburg paradox. Probab. Math. Statist. 14 157–172.

- [8] Csörgő, S.; and Simons, G. (1996) A strong law of large numbers for trimmed sums, with applications to generalized St. Petersburg games. Statist. Probab. Lett. 26 65–73.

- [9] Csörgő, S.; and Simons, G. (2007) St. Petersburg games with the largest gains withheld. Statist. Probab. Lett. 77 1185–1189.

- [10] Dutka, J. (1988) On the St. Petersburg paradox. Arch. Hist. Exact Sci. 39 13–39.

- [11] Falconer, K.J. (1985) The Geometry of Fractal Sets. Cambridge University Press, Cambridge.

- [12] Falconer, K.J. (1988) The Hausdorff dimension of self-affine fractals. Math. Proc. Cambridge Philos. Soc. 103 339–350.

- [13] Falconer, K.J. (1992) The dimension of self-affine fractals II. Math. Proc. Cambridge Philos. Soc. 111 169–179.

- [14] Falconer, K.J. (2003) Fractal Geometry – Mathematical Foundations and Applications. 2nd Ed., Wiley, New York.

- [15] Falconer, K.J. (2013) Dimension of self-affine sets: A survey. In: J. Barral and S. Seuret (Eds.) Further Developments in Fractals and Related Fields. Trends in Mathematics, Vol. 13, Birkhäuser, Basel, pp. 115–134.

- [16] Feller, W. (1945) Note on the law of large numbers and “fair” games. Ann. Math. Statist. 16 301–304.

- [17] Feller, W. (1968) An Introduction to Probability Theory and Its Applications, Vol. 1. 3rd Ed., Wiley, New York.

- [18] Gut, A. (2011) limit theorems for a generalized St. Petersburg game. J. Appl. Probab. 47 752–760. Correction (2013) http://www2.math.uu.se/~allan/86correction.pdf

- [19] Hawkes,, J. (1970) Measure function properties of the asymmetric Cauchy process. Mathematika 17 68–78.

- [20] Hutchinson, J.E. (1981) Fractals and self-similarity. Indiana Univ. Math. J. 30 713–747.

- [21] Jorland, G. (1987) The Saint Petersburg paradox 1713–1937. In: L. Krüger et al. (Eds.) The Probabilistic Revolution, Vol. 1: Ideas in History. MIT Press, Cambridge Ma., pp. 157–190.

- [22] Kahane, J.-P. (1985) Some Random Series of Functions. 2nd Ed., Cambridge University Press, Cambridge.

- [23] Kern, P.; and Wedrich, L. (2013) The Hausdorff dimension of operator semistable Lévy processes. J. Theoret. Probab. (to appear).

- [24] Martin-Löf, A. (1985) A limit theorem which clarifies the “Petersburg paradox”. J. Appl. Probab. 22 634–643.

- [25] Mattila, P. (1995) Geometry of Sets and Measures in Euclidean Spaces. Cambridge University Press, Cambridge.

- [26] Meerschaert, M.M.; and Scheffler, H.-P. (2001) Limit Distributions for Sums of Independent Random Vectors. Wiley, New York.

- [27] Meerschaert, M.M.; and Xiao, Y. (2005) Dimension results for sample paths of operator stable Lévy processes. Stochastic Process. Appl. 115 55–75.

- [28] Pap, G. (2011) The accuracy of merging approximations in generalized St. Petersburg games. J. Theoret. Probab. 24 240–270.

- [29] Pruitt, W.E.; and Taylor, S.J. (1969) Sample path properties of processes with stable components. Z. Wahrsch. verw. Geb. 12 267–289.

- [30] Sato, K. (1999) Lévy Processes and Infinitely Divisible Distributions. Cambridge University Press, Cambridge.

- [31] Steinhaus, H. (1949) The so-called Petersburg paradox. Colloq. Math. 2 56–58.

- [32] Taylor, S.J. (1967) Sample path properties of a transient stable process. J. Math. Mech. 16 1229–1246.

- [33] Vardi, I. (1995) The limiting distribution of the St. Petersburg game. Proc. Amer. Math. Soc. 123 2875–2882.

- [34] Vardi, I. (1997) The St. Petersburg game and continued fractions. C. R. Acad. Sci. Paris Sér. I Math. 324 913–918.

- [35] Xiao, Y. (2004) Random fractals and Markov processes. In: M.L. Lapidus et al. (Eds.) Fractal Geometry and Applications: A Jubilee of Benoit Mandelbrot, AMS, Providence, pp. 261–338.