False Discovery Rate Control under Archimedean Copula

Abstract

We are considered with the false discovery rate (FDR) of the linear step-up test considered by Benjamini and Hochberg (1995). It is well known that controls the FDR at level if the joint distribution of -values is multivariate totally positive of order . In this, denotes the total number of hypotheses, the number of true null hypotheses, and the nominal FDR level. Under the assumption of an Archimedean -value copula with completely monotone generator, we derive a sharper upper bound for the FDR of as well as a non-trivial lower bound. Application of the sharper upper bound to parametric subclasses of Archimedean -value copulae allows us to increase the power of by pre-estimating the copula parameter and adjusting . Based on the lower bound, a sufficient condition is obtained under which the FDR of is exactly equal to , as in the case of stochastically independent -values. Finally, we deal with high-dimensional multiple test problems with exchangeable test statistics by drawing a connection between infinite sequences of exchangeable -values and Archimedean copulae with completely monotone generators. Our theoretical results are applied to important copula families, including Clayton copulae and Gumbel copulae.

keywords:

[class=AMS]keywords:

and

1 Introduction

Control of the false discovery rate (FDR) has become a standard type I error criterion in large-scale multiple hypotheses testing. When the number of hypotheses to be tested simultaneously is of order , as it is prevalent in many modern applications from the life sciences like genetic association analyses, gene expression studies, functional magnetic resonance imaging, or brain-computer interfacing, it is typically infeasible to model or to estimate the full joint distribution of the data. Hence, one is interested in generic procedures that control the FDR under no or only qualitative assumptions regarding this joint distribution. The still by far most popular multiple test for FDR control, the linear step-up test (say) considered in the seminal work by Benjamini and Hochberg (1995), operates on marginal -values . As shown by Benjamini and Yekutieli (2001) and Sarkar (2002), is generically FDR-controlling over the class of models that lead to positive dependency among the random -values in the sense of positive regression dependency on subsets (PRDS), including -value distributions which are multivariate totally positive of order (MTP2). Under the PRDS assumption, the FDR of is upper-bounded by , where denotes the number of true null hypotheses and the nominal FDR level.

In this work, we extend these findings by deriving a sharper upper bound for the FDR of in the case that the dependency structure among can be expressed by an Archimedean copula. Our respective contributions are threefold. First, we quantify the magnitude of conservativity (non-exhaustion of the FDR level ) of in various copula models as a function of the copula parameter . This allows for a gain in power in practice by pre-estimating and adjusting the nominal value of . Second, we demonstrate by computer simulations that the proposed upper bound leads to a robust procedure in the sense that the variance of this bound over repeated Monte Carlo simulations is much smaller than the corresponding variance of the false discovery proportion (FDP) of . This makes the utilization of our upper bound an attractive choice in practice, addressing the issue that the FDP is typically not well concentrated around its mean, the FDR, if -values are dependent. As a by-product, we directly obtain that the FDR of is bounded by under the assumption of an Archimedean -value copula, without explicitly relying on the MTP2 property (which is fulfilled in the class of Archimedean -value copulae with completely monotone generator functions, cf. Müller and Scarsini (2005)). Let us point out already here that the FDR criterion is only suitable if the number of tests is large. In this case, the restriction to completely monotone generators is essentially void, because every copula generator is necessarily -monotone. Third, in an asymptotic setting (), we show that the class of Archimedean -value copulae with completely monotone generators includes certain models with -values or test statistics, respectively, which are exchangeable under null hypotheses, -exchangeable for short. Such -exchangeable test statistics occur naturally in many multiple test problems, for instance in many-to-one comparisons or if test statistics are given by jointly Studentized means (cf. Finner, Dickhaus and Roters (2007)).

In addition, we also derive and discuss a lower FDR bound for in terms of the generator of an Archimedean -value copula. Application of this lower bound leads to sufficient conditions under which the FDR of is exactly equal to , at least asymptotically as tends to infinity and converges to a fixed value. Hence, if the latter conditions are fulfilled, the FDR behaviour of is under dependency the same as in the case of jointly stochastically independent -values.

The paper is organized as follows. In Section 2, we set up the necessary notation, define our class of statistical models for , and recall properties and results around the FDR. Our main contributions are presented in Section 3, dealing with FDR control of under the assumption of an Archimedean copula. Special parametric copula families are studied in Section 4, where we quantify the realized FDR of as a function of . Section 5 outlines methods for pre-estimation of . We conclude with a discussion in Section 6. Lengthy proofs are deferred to Section 7.

2 Notation and preliminaries

All multiple test procedures considered in this work depend on the data only via (realized) marginal -values and their ordered values . Hence, it suffices to model the distribution of the random vector of -values and we consider statistical models of the form . In this, we assume that is the (main) parameter of statistical interest and we identify the null hypotheses with non-empty subsets of , with corresponding alternatives . The null hypothesis is called true if and false otherwise. We let denote the index set of true hypotheses and the number of true nulls. Without loss of generality, we will assume throughout the work. Analogously, we define , and . The intersection hypothesis will be referred to as the global (null) hypothesis.

The parameter is the copula parameter of the joint distribution of , thus representing the dependency structure among . Its parameter space may be of infinite dimension. In particular, in Section 3 we will consider the class of all Archimedean copulas which can be indexed by the generator function . However, we sometimes restrict our attention to parametric subclasses, for instance the class of Clayton copulae which can be indexed by a one-dimensional copula parameter . In any case, we will assume that is a nuisance parameter in the sense that it does not depend on and that the marginal distribution of each is invariant with respect to . Therefore, to simplify notation, we will write instead of if marginal -value distributions are concerned. Throughout the work, the -values are assumed to be valid in the sense that

A (non-randomized) multiple test operating on -values is a measurable mapping the components of which have the usual interpretation of a statistical test for versus , . For fixed , we let denote the (random) number of false rejections (type I errors) of and the total number of rejections. The FDR under of is then defined by

| (1) |

and is said to control the FDR at level if . The random variable is referred to as the false discovery proportion of , for short. Notice that, although the trueness of the null hypotheses is determined by alone, the FDR depends on and , because the dependency structure among the -values typically influences the distribution of when regarded as a statistic with values in .

The linear step-up test , also referred to as Benjamini-Hochberg test or the FDR procedure in the literature, rejects exactly hypotheses , where the bracketed indices correspond to the order of the -values and for linearly increasing critical values . If does not exist, no hypothesis is rejected. The sharpest characterization of FDR control of that we are aware of so far is given in the following theorem.

Theorem 2.1 (Finner, Dickhaus and Roters (2009)).

Consider the following assumptions.

- (D1)

-

: is non-increasing in .

- (D2)

-

.

- (I1)

-

: The -values are independent and identically distributed (iid).

- (I2)

-

: The random vectors and are stochastically independent.

Then, the following two assertions hold true.

| (2) | |||||

| (3) |

The crucial assumption (D1) is fulfilled for multivariate distributions of which are positively regression dependent on the subset (PRDS on ) in the sense of Benjamini and Yekutieli (2001). In particular, if the joint distribution of is MTP2, then (D1) holds true.

To mention also a negative result, Guo and Rao (2008) have shown that there exists a multivariate distribution of such that the FDR of is equal to , showing that is not generically FDR-controlling over all possible joint distributions of . The main purpose of the present work (Section 3) is to derive a sharper upper bound on the right-hand side of (2), assuming that is the space of completely monotone generator functions of Archimedean copulae.

3 FDR control under Archimedean Copula

In this section, it is assumed that the joint distribution of is given by an Archimedean copula such that

| (4) |

where the function is the so-called copula generator and takes the role of in our general setup. In (4) and throughout the work, denotes the cumulative distribution function (cdf) of the variate . The generator fully determines the type of the Archimedean copula; see, e.g. Nelsen (2006). A necessary and sufficient condition under which a function with and can be used as a copula generator is that is an -altering function, that is, for , cf. Müller and Scarsini (2005). Throughout the present work, we impose a slightly stronger assumption on . Namely, we assume that is completely monotone, i. e. for all . If is large as it is usual in applications of the FDR criterion, the distinction between the class of completely monotone functions and the class of -altering functions becomes negligible.

A very useful property of an Archimedean copula with completely monotone generator is the stochastic representation of . Namely, there exists a sequence of jointly independent and identically UNI-distributed random variables such that (cf. Marshall and Olkin (1988), Section 5)

| (5) |

where the symbol denotes equality in distribution. The random variable with Laplace transform is independent of , and its distribution is determined by only. Throughout the remainder, and refer to the distribution of , for ease of presentation. The stochastic representation (5) shows that the type of the Archimedean copula can equivalently be expressed in terms of the random variable . Moreover, the -values are conditionally independent given . This second property allows us to establish the following sharper upper bound for the FDR of .

Theorem 3.1 (Upper FDR bound).

Let be as in (5) and let consist of the remaining p-values obtained by dropping from so that . The random set is then given by

| (6) |

For a given value we define the function by with for . This function transforms, for fixed , realizations of into realizations of given in (5). Let denote the image of the set under for given and let . Then it holds

where

| (7) | |||||

with

| (8) |

and denoting the indicator function of the set .

Noticing that is always non-negative, we obtain the following result as a straightforward corollary of Theorem 3.1.

Corollary 3.1.

Let the copula of be an Archimedean copula, where is continuously distributed on for . Then it holds that

| (9) |

where denotes the set of all completely monotone generator functions of Archimedean copulae.

The result of Corollary 3.1 is in line with the findings obtained by Benjamini and Yekutieli (2001) and Sarkar (2002) that we have recalled in Section 1. Namely, Müller and Scarsini (2005) pointed out that an Archimedean copula possesses the MTP2 property if the copula generator is completely monotone and, hence, the FDR is controlled by in this case.

From the practical point of view, it is problematic that depends on the (main) parameter of statistical interest. In practice, one will therefore often only be able to work with . Since for all , the latter -free upper bound will typically still yield an improvement over the ”classical” upper bound. The issue of minimization of over is closely related to the challenging task of determining least favorable parameter configurations (LFCs) for the FDR. So-called Dirac-uniform configurations are least favorable (provide upper FDR bounds) for under independence assumptions and are assumed to be generally least favorable for also in models with dependent -values, at least for large values of (cf., e. g., Finner, Dickhaus and Roters (2007), Blanchard et al. (2013)). Troendle (2000) motivated the consideration of Dirac-uniform configurations from the point of view of consistency of marginal tests with respect to the sample size. Furthermore, the expectations in (7) can in general not be calculated analytically. However, they can easily be approximated by means of computer simulations. Namely, the approximation is performed by generating random numbers which behave like independent realizations of , which completely specifies the type of the Archimedean copula, evaluating the functions at the generated values and replacing the theoretical expectation of by the arithmetic mean of the resulting values of the integrand in (7). Under Dirac-uniform configurations, evaluation of can efficiently be performed by means of recursive formulas for the joint cdf of the order statistics of . We discuss these points in detail in Section 4.

Next, we discuss a lower bound for the FDR of under the assumption of an Archimedean copula.

Theorem 3.2 (Lower FDR bound).

Let the copula of be an Archimedean copula with generator function , where is continuously distributed on for . Then it holds that

| (10) |

where

| (11) |

From the assertion of Theorem 3.2 we conclude that the lower bound for the FDR of under the assumption of an Archimedean copula crucially depends on the extreme points of the function , given by

| (12) |

for . If for all the minimum of is always attained for the same index (say), then and together with Theorem 3.1 we get . This follows directly from the identity

However, the latter holds true only in some specific cases. To obtain a more explicit constant in the general case, we notice that, due to the analytic properties of , there exists a point such that for and for . The point is obtained as the solution of

which leads to

| (13) |

Next, we analyze the function for given . For its derivative with respect to , it holds that

Setting this expression to zero, we get that any extreme point of satisfies

| (14) |

Let be a solution of (14). Then, the second derivative of at is given by

| (15) |

Substituting (14) with in (15), we obtain

and application of the Cauchy-Schwarz inequality leads to

This proves that if is an extreme point of . Thus, any such is a maximum and the minimum in (11) is attained at for as well as at for . This allows for a more explicit characterization of the lower bound.

Lemma 3.1.

If the integral in (16) cannot be calculated analytically, then it can easily be approximated via a Monte Carlo simulation by using the expression on the right-hand side of (17) and replacing the theoretical expectation by its pseudo-sample analogue.

Lemma 3.1 possesses several interesting applications. We consider the quantity itself. It holds that , where

| (18) |

with

because

| (19) |

However, both of the integrals in (19) can be bounded by different values. To see this, we study the behavior of the function . It holds that

Since is a non-increasing function, we get that there exists a unique minimum of at

Consequently, we get

Corollary 3.2.

Under the assumptions of Theorem 3.2, the following two assertions hold true.

-

(a)

If from (13) does not lie in the support of , i. e., if or , then and, consequently, .

-

(b)

Assume that exists. If is such that or as , then

Part (b) of Corollary 3.2 motivates a deeper consideration of asymptotic or high-dimensional multiple tests, i. e., the case of , under our general setup. This approach has already been discussed widely in previous literature. For instance, it was called ”asymptotic multiple test” by Genovese and Wasserman (2002). The case was also considered by Finner and Roters (1998), Storey (2002), Genovese and Wasserman (2004), Finner, Dickhaus and Roters (2007, 2009), Jin and Cai (2007), Sun and Cai (2007), and Cai and Jin (2010), among others.

Very interesting connections can be drawn between Archimedean -value copulae and infinite sequences of -exchangeable -values. More precisely, let us assume an infinite sequence of -values which are absolutely continuous and uniformly distributed on under the respective null hypothesis . Furthermore, we let denote the cdf. of under and assume that are exchangeable random variables, entailing that , themselves are exchangeable under the global hypothesis . Sequences of -exchangeable -values have already been investigated by Finner and Roters (1998) and Finner, Dickhaus and Roters (2007) in special settings. Moreover, the assumption of exchangeability is also pivotal in other areas of statistics, let us mention Bayesian analysis and validity of permutation tests. The problem of exchangeability in population genetics has been discussed by Kingman (1978).

For ease of notation, let for . Because is an exchangeable sequence of random variables, it exists a random variable with distribution function such that the joint distribution of is for any fixed given by

| (20) |

see Olshen (1974) and equation (3.1) of Kingman (1978). Moreover, assuming that with probability , we obtain for any from Marshall and Olkin (1988), p. 834, that

where denotes the Laplace transform of , i. e., .

Theorem 3.3 establishes a connection between the finite-dimensional marginal distributions of -exchangeable -value sequences and Archimedean copulae.

Theorem 3.3.

Assume that the elements in the infinite sequence are absolutely continuous and -exchangeable. Furthermore, let the following two assumptions be valid.

-

(i)

The random variable from (20) takes values in with probability .

-

(ii)

It holds

(21)

Then, for any ,

is a copula of , where .

Corollary 3.3.

Under the assumptions of Theorem 3.3, it holds:

-

a)

Any -dimensional marginal distribution of the sequence possesses the MTP2 property, .

-

b)

The linear step-up test , applied to , controls the FDR at level .

4 Examples: Parametric copula families

In this section, we apply the theoretical results of Section 3 to several parametric families of Archimedean copulas.

4.1 Independence Copula

4.2 Clayton Copula

The generator of the Clayton copula is given by

| (22) |

leading to and to the probability density function (pdf)

| (23) |

of , where denotes Euler’s gamma function and the pdf of the gamma distribution with shape parameter and scale parameter . For the Clayton copula, is given by

| (24) |

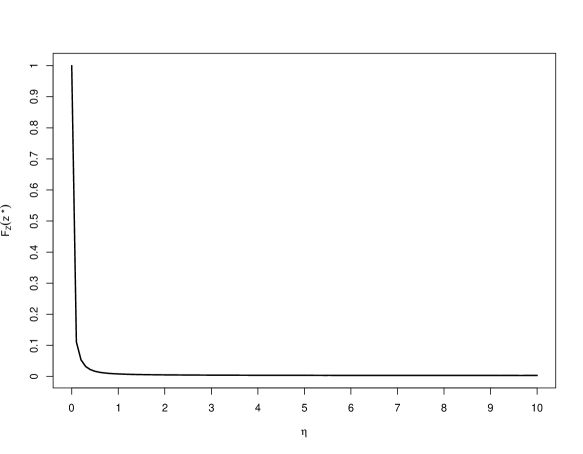

In Figure 1, we plot as a function of for and . It is worth mentioning that the Clayton copula converges to the independence copula for . In this case we get and tends to the Dirac delta function concentrated in . As a result, we observe that as and the FDR of approaches . As increases, steeply decreases and takes values very close to zero for large values of . Consequently, it is expected that the FDR of is close to for large values of , too. For of moderate size, however, the FDR of can be much smaller than . This is shown in Figure 2 below and discussed in detail there.

The quantity for the Clayton copula is calculated by

| (25) | |||||

where

and, similarly,

Hence, from Theorem 3.2 we get for all that

Next, we consider the sharper upper bound for the FDR in the case of Clayton copulae in detail. As outlined in the discussion around Theorem 3.1, a so-called Dirac-uniform configuration (cf., e. g., Blanchard et al. (2013) and references therein) is assumed for in case of . Namely, the -values are assumed to be -almost surely equal to . Under assumptions (I1)-(I2) from Theorem 2.1, Dirac-uniform configurations are least favorable (provide upper bounds) for the FDR of , see Benjamini and Yekutieli (2001). In the case of dependent -values, such general results are yet lacking, but it is assumed that Dirac-uniform configurations yield upper FDR bounds for also under dependency, at least for large (cf., e. g., Finner, Dickhaus and Roters (2007)).

Under a Dirac-uniform configuration, the sharper upper bound for the FDR of is expressed by (see Theorem 3.1)

| (26) | |||||

where is given in (8) and the random set the probability of which is given by can under Dirac-uniform configurations equivalently be expressed as

The last equality follows from the fact that , …, almost surely correspond to -values associated with true null hypotheses, i. e.,

Moreover, since each of the , …, is obtained by the same isotonic transformation from the corresponding element in the sequence , …, , we get that , …, is an increasing sequence of independent and identically UNI-distributed random variables. Hence, the probabilities for can be calculated recursively, for instance by making use of Bolshev’s recursion (see, e. g., Shorack and Wellner (1986), p. 366).

In general, Bolshev’s recursion is defined in the following way. Let be real constants and let be the order statistics of independent and identically UNI-distributed random variables. We let . Then, the probability is calculated recursively by

| (27) |

Application of (27) with and

for as well as numerical integration with respect to the distribution of over lead to a numerical approximation of the sharper upper bound for the FDR of under Dirac-uniform configurations.

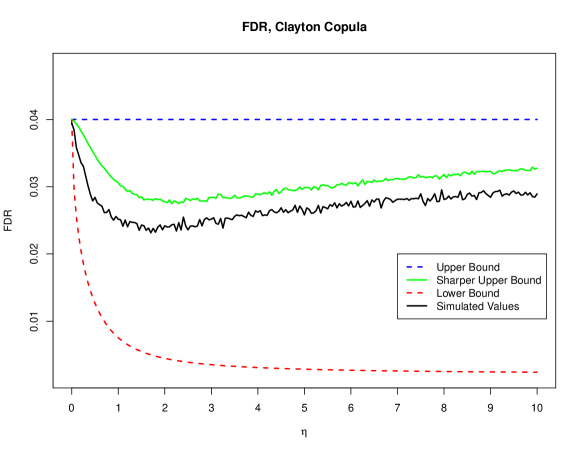

In Figure 2 we present the lower bound (dashed red line), the upper bound (dashed blue line), the sharper upper bound (solid green line), and the simulated values of the FDR of (solid black line) as a function of the parameter of a Clayton copula. We put , , and . The -values which correspond to the false null hypotheses have been set to zero. The simulated values are obtained by using independent repetitions. We observe that the FDR of starts at for and decreases to a minimum of approximately at . This value is much smaller than the nominal level , offering some room for improvement of for a broad range of values of . After reaching its minimum, the FDR of increases and tends to as increases. This behavior of the FDR of is as expected from the values of , as discussed around Figure 1.

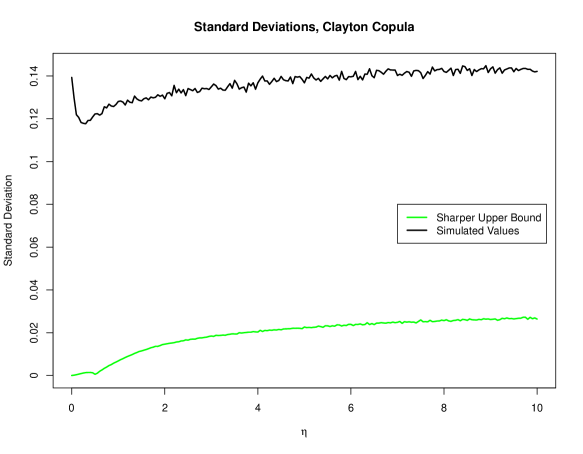

In contrast to the ”classical” upper bound, the sharper upper bound reproduces the behavior of the simulated FDR values very well. It provides a good approximation of the true values of the FDR of for all considered values of . In particular, it is much smaller than the ”classical” upper bound for moderate values of . Consequently, application of the sharper upper bound can be used to improve the power of the multiple testing procedure by adjusting the nominal value of depending on . If is unknown, we propose techniques for pre-estimating it in Section 5. It is also remarkable that the difference between the sharper upper bound and the corresponding simulated FDR-values is not large. In contrast, the empirical standard deviations of the sharper upper bound (over repeated simulations) are about five times smaller than the corresponding ones for the simulated values of the FDP of (see Figure 3). While these standard deviations are always smaller than for the sharper upper bound, they are around for almost all of the considered values of in case of the simulated FDP-values. Finally, we note that the lower bound seems not to be informative in this particular model class. It is close to zero even for moderate values of .

4.3 Gumbel Copula

The generator of the Gumbel copula is given by

| (28) |

which leads to and a stochastic representation

| (29) |

for , where the random variable has a stable distribution with index of stability and unit skewness. The cdf of is given by (cf. Chambers, Mallows and Stuck (1976), p. 341)

Although (29) in connection with characterizes the distribution of completely, the integral representation of may induce numerical issues with respect to implementation. Somewhat more convenient from this perspective is the following result. Namely, Kanter (1975) obtained a stochastic representation of , given by

| (30) |

where and are stochastically independent, is standard exponentially distributed and . We used (30) for simulating and, consequently, .

For the Gumbel copula we get

| (31) |

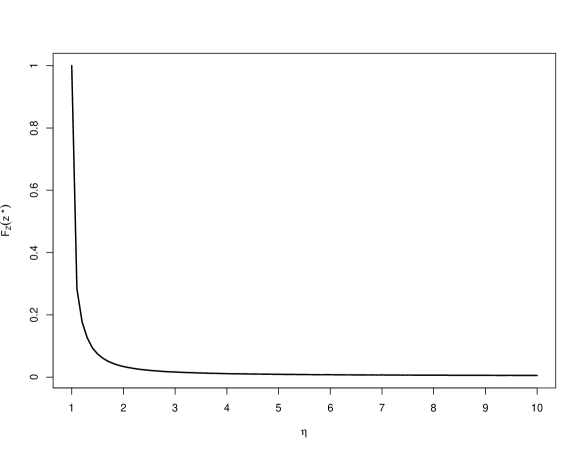

In Figure 4, we plot as a function of for and . A similar behavior as in the case of the Clayton copula is present. If then the Gumbel copula coincides with the independence copula. Hence, and, consequently, the FDR of is equal to in this case. As increases, decreases and it approaches for larger values of . Hence, tends to as becomes considerably large. For moderate values of , can again be much smaller than , in analogy to the situation in models with Clayton copulae.

Recall from (17) that

| (32) |

where . For the Gumbel copula, we obtain

The expectation in (32) cannot be calculated analytically. However, it can easily be approximated with Monte Carlo simulations by applying the stochastic representations (29) and (30) for any fixed . This leads to a numerical value on the left-hand side of the chain of inequalities

| (33) |

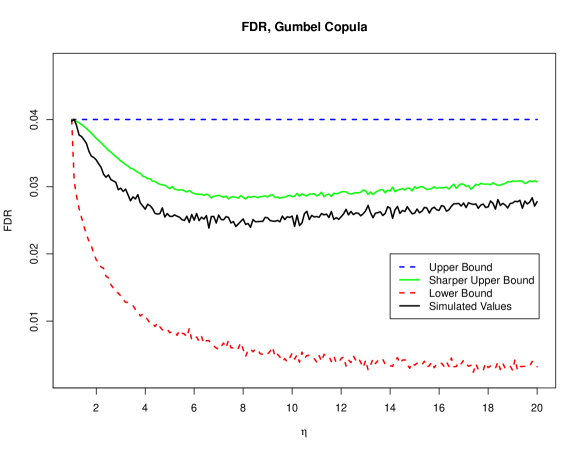

The sharper upper bound from Theorem 3.1 can be calculated by using Bolshev’s recursion similarly to the discussion around (27), but here with as in (28). Figure 5 displays the lower bound (dashed red line), the upper bound (dashed blue line), the sharper upper bound (solid green line), and simulated values of (solid black line) as functions of . Again, we chose , , and . The -values corresponding to the false null hypotheses were all set to zero, as in the case of Clayton copulae. The simulated values were obtained by generating independent pseudo realizations of .

Similarly to the case of the Clayton copula, the curve of simulated FDR values has a -shape. It starts at and drops to its minimum of approximately for values of around . For such values of , the black curve is considerably below the classical upper bound of . In contrast, the sharper upper bound gives a much tighter approximation of the simulated FDR values in such cases and reproduces the -shape over the entire range of values for the parameter of the Gumbel copula. As a result, its application can be used to improve power by adjusting the nominal value of and thereby increasing the probability to detect false null hypotheses. Moreover, as in the case of Clayton copulae, the empirical standard deviations of the sharper upper bound are much smaller than those of the simulated values of the FDP (see Figure 6). The lower bound from (33) (corresponding to the dashed red curve in Figure 5) has been obtained by approximating the expectation in (32) via simulations. As in the case of the Clayton copula, the lower bound is not too informative for the model class that we have considered here (Dirac-uniform configurations).

5 Empirical copula calibration

In the previous section we studied the influence of the copula parameter on the FDR of under several parametric families of Archimedean copulae. It turned out that adapting to the degree of dependency in the data by adjusting the nominal value of based on the sharper upper bound from Theorem 3.1 is a promising idea, because the unadjusted procedure may lead to a considerable non-exhaustion of , cf. Figures 2 and 5. Due to the decision rule of a step-up test, this also entails suboptimal power properties of when applied ”as is” to models with Archimedean -value copulae.

In practice, however, often the copula parameter itself is an unknown quantity. Hence, the outlined adaptation of typically requires some kind of pre-estimation of before multiple testing is performed. Although this is not in the main focus of the present work, we therefore outline possibilities for estimating and for quantifying the uncertainty of the estimation in this section.

One class of procedures relies on resampling, namely via the parametric bootstrap or via permutation techniques if correspond to marginal two-sample problems. Pollard and van der Laan (2004) provided an extensive comparison of both approaches and argued that the permutation method reproduces the correct null distribution only under some conditions. However, if these conditions are met, the permutation approach is often superior to bootstrapping (see also Westfall and Young (1993) and Meinshausen, Maathuis and Bühlmann (2011)). Furthermore, it is essential to keep in mind that both bootstrap and permutation-based methods estimate the distribution of the vector under the global null hypothesis . Hence, the assumption that does not depend on is an essential prerequisite for the applicability of such resampling methods for estimating . Notice that the latter assumption is an informal description of the ”subset pivotality” condition introduced by Westfall and Young (1993). The resampling methods developed by Dudoit and van der Laan (2008) can dispense with subset pivotality in special model classes, but for the particular task of estimating the copula parameter this assumption seems indispensable.

Estimation of and uncertainty quantification of the estimation based on resampling is generally performed by applying a suitable estimator to the re- (pseudo) samples. In the context of Archimedean copulae the two most widely applied estimation procedures are the maximum likelihood method (see, e. g. Joe (2005), Hofert, Mächler and McNeil (2012)) and the method of moments (referred to as ”realized copula” approach by Fengler and Okhrin (2012)).

Hofert, Mächler and McNeil (2012) considered the estimation of the parameter of an Archimedean copula with known margins by the maximum likelihood approach. To this end, they derived analytic expressions for the derivatives of the copula generator for several families of Archimedean copulae, as well as formulas for the corresponding score functions. Using these results and assuming a regular model, an elliptical asymptotic confidence region for the copula parameter can be obtained by applying general limit theorems for maximum likelihood estimators (see Hofert, Mächler and McNeil (2012) for details and the calculations for different types of Archimedean copulae).

In the context of the method of moments, Kendall’s tau is often considered. For a bivariate Archimedean copula with generator of marginally UNI-distributed variates and , it is given by

| (34) | |||||

cf. McNeil and Nešlehová (2009).

The right-hand side of (34) can analytically be calculated for some families of Archimedean copulae. For instance, for a Clayton copula with parameter it is given by , while it is equal to for a Gumbel copula with parameter (see Nelsen (2006), p. 163-164). Based on such moment equations, Fengler and Okhrin (2012) suggested the ”realized copula” method for empirical calibration of a one-dimensional parameter of an -variate Archimedean copula. The method considers all distinct pairs of the underlying random variables, replaces the population versions of by the corresponding sample analogues, and finally aggregates the resulting estimates in an appropriate manner. More specifically, consider the functions for and define , where is the sample estimator of Kendall’s tau (see, e. g., Nelsen (2006), Section 5.1.1). The resulting estimator for is then obtained by

| (35) |

for an appropriate weight matrix . An application of the realized copula method to resampled -values generated by permutations in the context of multiple testing for differential gene expression has been demonstrated by Dickhaus and Gierl (2013). Multivariate extensions of Kendall’s tau and central limit theorems for the sample versions have been derived by Genest, Nešlehová and Ben Ghorbal (2011). These results can be used for uncertainty quantification of the moment estimation of by constructing asymptotic confidence regions.

6 Discussion

We have derive a sharper upper bound for the FDR of in models with Archimedean copulae. This bound can be used to prove that controls the FDR for this type of multivariate -value distributions, a result which is in line with the findings of Benjamini and Yekutieli (2001) and Sarkar (2002). Since certain models with -exchangeable -values fall into this class at least asymptotically (see Theorem 3.3), our findings complement those of Finner, Dickhaus and Roters (2007) who investigated infinite sequences of -exchangeable -values in Gaussian models. While our general results in Section 3 qualitatively extend the theory, our results in Section 4 regarding Clayton and Gumbel copulae are quantitatively very much in line with the findings for Gaussian and -copulae reported by Finner, Dickhaus and Roters (2007). Namely, over a broad class of models with dependent -values, the FDR of as a function of the dependency parameter has a -shape and becomes smallest for medium strength of dependency among the -values. This behavior can be exploited by adjusting in order to adapt to . We have presented an explicit adaptation scheme based on the upper bound from Theorem 3.1. To the best of our knowledge, this kind of adaptation is novel to FDR theory.

It is beyond the scope of the present work to investigate which parametric class of copulae is appropriate for which kind of real-life application. Relatedly, the problem of model misspecification (i. e., quantification of the approximation error if the true model does not belong to the class with Archimedean -value copulae and is approximated by the (in some suitable norm) closest member of this class) could not be addressed here, but is a challenging topic for future research. One particularly interesting issue in this direction is FDR control for finite sequences of -exchangeable -values.

Finally, we would like to mention that the empirical variance of the false discovery proportion was large in all our simulations, implying that the random variable was not well concentrated around its expected value . This is a known effect for models with dependent -values (see, e. g., Finner, Dickhaus and Roters (2007), Delattre and Roquain (2011), Blanchard et al. (2013)) and provokes the question if FDR control is a suitable criterion under dependency at all. Maybe more stringent in dependent models is control of the false discovery exceedance rate, meaning to design a multiple test ensuring that , for user-defined parameters and . In any case, practitioners should be (made) aware of the fact that controlling the FDR with does not necessarily imply that the FDP for their particular experiment is small, at least if dependencies among have to be assumed as it is typically the case in applications. In contrast, the empirical standard deviations of our proposed sharper upper bound are about five times smaller than the empirical standard deviations of the simulated values of the FDP of . This provides an additional (robustness) argument for the application of the results presented in Theorem 3.1 in practice.

7 Proofs

Proof of Theorem 3.1

Following Benjamini and Yekutieli (2001), an analytic expression for the FDR of is given by

| (36) |

where denotes the event that hypotheses are rejected one of which is (a true null hypothesis) and is the event that hypotheses additionally to are rejected. It holds that are disjoint and that .

Let for denote the event that the number of rejected null hypotheses is at most . In terms of introduced in Theorem 3.1, the random set is given by

| (37) |

Next, we prove that

To this end, we consider the function introduced in Theorem 3.1, which transforms a possible realization of the original -values into a realization of for , where and are as in (5). Because each component of this multivariate transformation is a monotonically increasing function which fully covers the interval , the resulting transformation bijectively transforms the set into itself. Let and denote the images of the sets and under for given . Then

-

(a)

are disjoint, i. e., for ,

-

(b)

,

-

(c)

.

Statements (a) - (c) follow directly from the facts that each is a monotonically increasing function and T is a one-to-one transformation with image equal to . Moreover, we obtain

| (39) |

where is the -dimensional vector obtained from by deleting . The last equality shows that for and, hence, that , given by , is an increasing function in .

Returning to (7), we obtain

| (40) | |||||

Next, we analyze the difference under the last integral. It holds that

The last expression is nonnegative if and only if

Hence, for with given in (8), the function under the integral in (40) is positive and for it is negative. Application of this result leads to

Proof of Theorem 3.2

Straightforward calculation yields

where the random events and are defined in the proof of Theorem 3.1. Moreover, making use of the notation introduced in the proof of Theorem 3.1, we can express by

where the latter inequality follows from for all and the fact that each is a true null hypothesis.

Now, it holds that

This completes the proof of the theorem.∎

Proof of Theorem 3.3

Acknowledgments

This research is partly supported by the Deutsche Forschungsgemeinschaft via the Research Unit FOR 1735 ”Structural Inference in Statistics: Adaptation and Efficiency”.

References

- Benjamini and Hochberg (1995) {barticle}[author] \bauthor\bsnmBenjamini, \bfnmY.\binitsY. and \bauthor\bsnmHochberg, \bfnmY.\binitsY. (\byear1995). \btitleControlling the false discovery rate: A practical and powerful approach to multiple testing. \bjournalJ. R. Stat. Soc. Ser. B Stat. Methodol. \bvolume57 \bpages289-300. \endbibitem

- Benjamini and Yekutieli (2001) {barticle}[author] \bauthor\bsnmBenjamini, \bfnmYoav\binitsY. and \bauthor\bsnmYekutieli, \bfnmDaniel\binitsD. (\byear2001). \btitleThe control of the false discovery rate in multiple testing under dependency. \bjournalAnn. Stat. \bvolume29 \bpages1165-1188. \endbibitem

- Blanchard et al. (2013) {barticle}[author] \bauthor\bsnmBlanchard, \bfnmG.\binitsG., \bauthor\bsnmDickhaus, \bfnmT.\binitsT., \bauthor\bsnmRoquain, \bfnmE.\binitsE. and \bauthor\bsnmVillers, \bfnmF.\binitsF. (\byear2013). \btitleOn least favorable configurations for step-up-down tests. \bjournalStatistica Sinica, forthcoming. \endbibitem

- Cai and Jin (2010) {barticle}[author] \bauthor\bsnmCai, \bfnmT. Tony\binitsT. T. and \bauthor\bsnmJin, \bfnmJiashun\binitsJ. (\byear2010). \btitleOptimal rates of convergence for estimating the null density and proportion of nonnull effects in large-scale multiple testing. \bjournalAnn. Stat. \bvolume38 \bpages100-145. \bdoi10.1214/09-AOS696 \endbibitem

- Chambers, Mallows and Stuck (1976) {barticle}[author] \bauthor\bsnmChambers, \bfnmJ. M.\binitsJ. M., \bauthor\bsnmMallows, \bfnmC. L.\binitsC. L. and \bauthor\bsnmStuck, \bfnmB. W.\binitsB. W. (\byear1976). \btitleA method for simulating stable random variables. \bjournalJ. Am. Stat. Assoc. \bvolume71 \bpages340-344. \bdoi10.2307/2285309 \endbibitem

- Delattre and Roquain (2011) {barticle}[author] \bauthor\bsnmDelattre, \bfnmS.\binitsS. and \bauthor\bsnmRoquain, \bfnmE.\binitsE. (\byear2011). \btitleOn the false discovery proportion convergence under Gaussian equi-correlation. \bjournalStat. Probab. Lett. \bvolume81 \bpages111-115. \bdoi10.1016/j.spl.2010.09.025 \endbibitem

- Dickhaus and Gierl (2013) {binproceedings}[author] \bauthor\bsnmDickhaus, \bfnmThorsten\binitsT. and \bauthor\bsnmGierl, \bfnmJakob\binitsJ. (\byear2013). \btitleSimultaneous test procedures in terms of p-value copulae. \bseriesProceedings on the 2nd Annual International Conference on Computational Mathematics, Computational Geometry & Statistics (CMCGS 2013) \bvolume2 \bpages75-80. \bpublisherGlobal Science and Technology Forum (GSTF). \endbibitem

- Dudoit and van der Laan (2008) {bbook}[author] \bauthor\bsnmDudoit, \bfnmSandine\binitsS. and \bauthor\bparticlevan der \bsnmLaan, \bfnmMark J.\binitsM. J. (\byear2008). \btitleMultiple testing procedures with applications to genomics. \bpublisherSpringer Series in Statistics. New York, NY: Springer. \endbibitem

- Fengler and Okhrin (2012) {btechreport}[author] \bauthor\bsnmFengler, \bfnmMatthias R.\binitsM. R. and \bauthor\bsnmOkhrin, \bfnmOstap\binitsO. (\byear2012). \btitleRealized Copula \btypeSFB 649 Discussion Paper No. \bnumber2012-034, \bpublisherSonderforschungsbereich 649, Humboldt-Universität zu Berlin, Germany. \bnoteavailable at http://sfb649.wiwi.hu-berlin.de/papers/pdf/SFB649DP2012-034.pdf. \endbibitem

- Finner, Dickhaus and Roters (2007) {barticle}[author] \bauthor\bsnmFinner, \bfnmH.\binitsH., \bauthor\bsnmDickhaus, \bfnmT.\binitsT. and \bauthor\bsnmRoters, \bfnmM.\binitsM. (\byear2007). \btitleDependency and false discovery rate: Asymptotics. \bjournalAnn. Stat., \bvolume35 \bpages1432-1455. \endbibitem

- Finner, Dickhaus and Roters (2009) {barticle}[author] \bauthor\bsnmFinner, \bfnmHelmut\binitsH., \bauthor\bsnmDickhaus, \bfnmThorsten\binitsT. and \bauthor\bsnmRoters, \bfnmMarkus\binitsM. (\byear2009). \btitleOn the false discovery rate and an asymptotically optimal rejection curve. \bjournalAnn. Stat. \bvolume37 \bpages596-618. \bdoi10.1214/07-AOS569 \endbibitem

- Finner and Roters (1998) {barticle}[author] \bauthor\bsnmFinner, \bfnmH.\binitsH. and \bauthor\bsnmRoters, \bfnmM.\binitsM. (\byear1998). \btitleAsymptotic comparison of step-down and step-up multiple test procedures based on exchangeable test statistics. \bjournalAnn. Stat. \bvolume26 \bpages505-524. \bdoi10.1214/aos/1028144847 \endbibitem

- Genest, Nešlehová and Ben Ghorbal (2011) {barticle}[author] \bauthor\bsnmGenest, \bfnmChristian\binitsC., \bauthor\bsnmNešlehová, \bfnmJohanna\binitsJ. and \bauthor\bsnmBen Ghorbal, \bfnmNoomen\binitsN. (\byear2011). \btitleEstimators based on Kendall’s tau in multivariate copula models. \bjournalAust. N. Z. J. Stat. \bvolume53 \bpages157-177. \bdoi10.1111/j.1467-842X.2011.00622.x \endbibitem

- Genovese and Wasserman (2002) {barticle}[author] \bauthor\bsnmGenovese, \bfnmChristopher\binitsC. and \bauthor\bsnmWasserman, \bfnmLarry\binitsL. (\byear2002). \btitleOperating characteristics and extensions of the false discovery rate procedure. \bjournalJ. R. Stat. Soc., Ser. B, Stat. Methodol. \bvolume64 \bpages499-517. \endbibitem

- Genovese and Wasserman (2004) {barticle}[author] \bauthor\bsnmGenovese, \bfnmChristopher\binitsC. and \bauthor\bsnmWasserman, \bfnmLarry\binitsL. (\byear2004). \btitleA stochastic process approach to false discovery control. \bjournalAnn. Stat. \bvolume32 \bpages1035-1061. \bdoi10.1214/009053604000000283 \endbibitem

- Guo and Rao (2008) {barticle}[author] \bauthor\bsnmGuo, \bfnmWenge\binitsW. and \bauthor\bsnmRao, \bfnmM. Bhaskara\binitsM. B. (\byear2008). \btitleOn control of the false discovery rate under no assumption of dependency. \bjournalJ. Stat. Plann. Inference \bvolume138 \bpages3176-3188. \bdoi10.1016/j.jspi.2008.01.003 \endbibitem

- Hofert, Mächler and McNeil (2012) {barticle}[author] \bauthor\bsnmHofert, \bfnmMarius\binitsM., \bauthor\bsnmMächler, \bfnmMartin\binitsM. and \bauthor\bsnmMcNeil, \bfnmAlexander J.\binitsA. J. (\byear2012). \btitleLikelihood inference for Archimedean copulas in high dimensions under known margins. \bjournalJ. Multivariate Anal. \bvolume110 \bpages133-150. \bdoi10.1016/j.jmva.2012.02.019 \endbibitem

- Jin and Cai (2007) {barticle}[author] \bauthor\bsnmJin, \bfnmJiashun\binitsJ. and \bauthor\bsnmCai, \bfnmT. Tony\binitsT. T. (\byear2007). \btitleEstimating the null and the proportion of nonnull effects in large-scale multiple comparisons. \bjournalJ. Am. Stat. Assoc. \bvolume102 \bpages495-506. \bdoi10.1198/016214507000000167 \endbibitem

- Joe (2005) {barticle}[author] \bauthor\bsnmJoe, \bfnmHarry\binitsH. (\byear2005). \btitleAsymptotic efficiency of the two-stage estimation method for copula-based models. \bjournalJ. Multivariate Anal. \bvolume94 \bpages401-419. \bdoi10.1016/j.jmva.2004.06.003 \endbibitem

- Kanter (1975) {barticle}[author] \bauthor\bsnmKanter, \bfnmMarek\binitsM. (\byear1975). \btitleStable densities under change of scale and total variation inequalities. \bjournalAnn. Probab. \bvolume3 \bpages697-707. \bdoi10.1214/aop/1176996309 \endbibitem

- Kingman (1978) {barticle}[author] \bauthor\bsnmKingman, \bfnmJ. F. C.\binitsJ. F. C. (\byear1978). \btitleUses of exchangeability. \bjournalAnn. Probab. \bvolume6 \bpages183-197. \bdoi10.1214/aop/1176995566 \endbibitem

- Marshall and Olkin (1988) {barticle}[author] \bauthor\bsnmMarshall, \bfnmAlbert W.\binitsA. W. and \bauthor\bsnmOlkin, \bfnmIngram\binitsI. (\byear1988). \btitleFamilies of multivariate distributions. \bjournalJ. Am. Stat. Assoc. \bvolume83 \bpages834-841. \bdoi10.2307/2289314 \endbibitem

- McNeil and Nešlehová (2009) {barticle}[author] \bauthor\bsnmMcNeil, \bfnmAlexander J.\binitsA. J. and \bauthor\bsnmNešlehová, \bfnmJohanna\binitsJ. (\byear2009). \btitleMultivariate Archimedean copulas, -monotone functions and -norm symmetric distributions. \bjournalAnn. Stat. \bvolume37 \bpages3059-3097. \bdoi10.1214/07-AOS556 \endbibitem

- Meinshausen, Maathuis and Bühlmann (2011) {barticle}[author] \bauthor\bsnmMeinshausen, \bfnmNicolai\binitsN., \bauthor\bsnmMaathuis, \bfnmMarloes H.\binitsM. H. and \bauthor\bsnmBühlmann, \bfnmPeter\binitsP. (\byear2011). \btitleAsymptotic optimality of the Westfall-Young permutation procedure for multiple testing under dependence. \bjournalAnn. Stat. \bvolume39 \bpages3369-3391. \bdoi10.1214/11-AOS946 \endbibitem

- Müller and Scarsini (2005) {barticle}[author] \bauthor\bsnmMüller, \bfnmAlfred\binitsA. and \bauthor\bsnmScarsini, \bfnmMarco\binitsM. (\byear2005). \btitleArchimedean copulae and positive dependence. \bjournalJ. Multivariate Anal. \bvolume93 \bpages434-445. \bdoi10.1016/j.jmva.2004.04.003 \endbibitem

- Nelsen (2006) {bbook}[author] \bauthor\bsnmNelsen, \bfnmRoger B.\binitsR. B. (\byear2006). \btitleAn introduction to copulas. 2nd ed. \bpublisherSpringer Series in Statistics. New York, NY: Springer. \endbibitem

- Olshen (1974) {barticle}[author] \bauthor\bsnmOlshen, \bfnmRichard\binitsR. (\byear1974). \btitleA note on exchangeable sequences. \bjournalZ. Wahrscheinlichkeitstheor. Verw. Geb. \bvolume28 \bpages317–321. \bdoi10.1007/BF00532949 \endbibitem

- Pollard and van der Laan (2004) {barticle}[author] \bauthor\bsnmPollard, \bfnmKatherine S.\binitsK. S. and \bauthor\bparticlevan der \bsnmLaan, \bfnmMark J.\binitsM. J. (\byear2004). \btitleChoice of a null distribution in resampling-based multiple testing. \bjournalJ. Stat. Plann. Inference \bvolume125 \bpages85-100. \bdoi10.1016/j.jspi.2003.07.019 \endbibitem

- Sarkar (2002) {barticle}[author] \bauthor\bsnmSarkar, \bfnmSanat K.\binitsS. K. (\byear2002). \btitleSome results on false discovery rate in stepwise multiple testing procedures. \bjournalAnn. Stat. \bvolume30 \bpages239-257. \endbibitem

- Shorack and Wellner (1986) {bbook}[author] \bauthor\bsnmShorack, \bfnmGalen R.\binitsG. R. and \bauthor\bsnmWellner, \bfnmJon A.\binitsJ. A. (\byear1986). \btitleEmpirical processes with applications to statistics. \bseriesWiley Series in Probability and Mathematical Statistics: Probability and Mathematical Statistics. \bpublisherJohn Wiley & Sons Inc., \baddressNew York. \bmrnumber838963 (88e:60002) \endbibitem

- Storey (2002) {barticle}[author] \bauthor\bsnmStorey, \bfnmJohn D.\binitsJ. D. (\byear2002). \btitleA direct approach to false discovery rates. \bjournalJ. R. Stat. Soc., Ser. B, Stat. Methodol. \bvolume64 \bpages479-498. \endbibitem

- Sun and Cai (2007) {barticle}[author] \bauthor\bsnmSun, \bfnmWenguang\binitsW. and \bauthor\bsnmCai, \bfnmT. Tony\binitsT. T. (\byear2007). \btitleOracle and adaptive compound decision rules for false discovery rate control. \bjournalJ. Am. Stat. Assoc. \bvolume102 \bpages901-912. \bdoi10.1198/016214507000000545 \endbibitem

- Troendle (2000) {barticle}[author] \bauthor\bsnmTroendle, \bfnmJ. F.\binitsJ. F. (\byear2000). \btitleStepwise normal theory multiple test procedures controlling the false discovery rate. \bjournalJournal of Statistical Planning and Inference \bvolume84 \bpages139-158. \bdoi10.1016/S0378-3758(99)00145-7 \endbibitem

- Westfall and Young (1993) {bbook}[author] \bauthor\bsnmWestfall, \bfnmPeter H.\binitsP. H. and \bauthor\bsnmYoung, \bfnmS. Stanley\binitsS. S. (\byear1993). \btitleResampling-based multiple testing: examples and methods for p-value adjustment. \bpublisherWiley Series in Probability and Mathematical Statistics. Applied Probability and Statistics. Wiley, New York. \endbibitem