The Effect of Growth on Equality in Models of the Economy

Abstract

We investigate the relation between economic growth and equality in a modified version of the agent-based asset exchange model (AEM). The modified model is a driven system that for a range of parameter space is effectively ergodic in the limit of an infinite system. We find that the belief that “a rising tide lifts all boats” does not always apply, but the effect of growth on the wealth distribution depends on the nature of the growth. In particular, we find that the rate of growth, the way the growth is distributed, and the percentage of wealth exchange determine the degree of equality. We find strong numerical evidence that there is a phase transition in the modified model, and for a part of parameter space the modified AEM acts like a geometric random walk.

It is a wildly held belief that economic growth benefits all members of society review ; gud ; jfk . The purpose of this work is to test this idea in a simple model economy. Economies are complex systems which have many influences that are difficult to include in simple models review . However, if the question is one of a statistical nature about the economy as a whole (macroeconomics), and if we obtain the same behavior in different models, we can have some confidence that the models suggest something meaningful about real economies.

In the original version of the asset exchange model (AEM) an equal amount of wealth is initially distributed to agents boghos . A pair of agents is then chosen at random and a fraction of the wealth of the poorer agent is transferred from the loser of a coin flip to the winner with probability 1/2. The total wealth is fixed, where is the wealth of the th agent at time boghos ; angle ; krapiv . After many time steps, the wealth is concentrated among increasingly fewer individuals, culminating as in a single agent holding a fraction of the wealth which approaches one boghos ; angle ; ispo ; krapiv .

In this work the AEM is modified so that after exchanges (one unit of time) an amount is added to the system resulting in exponential growth with . To distribute the growth to the agents we calculate the quantity

| (1) |

where the sum is over the agents and the parameter . The increase in wealth due to the growth is assigned to the th agent as

| (2) |

For the increase in wealth generated by the growth is distributed equally. As increases, the allocation of the increased wealth is weighted more heavily toward the agents with greater wealth at time . Three parameters determine the wealth distribution in our modified asset exchange model (MAEM): , , and . In this work we focus primarily on the effect of different values of .

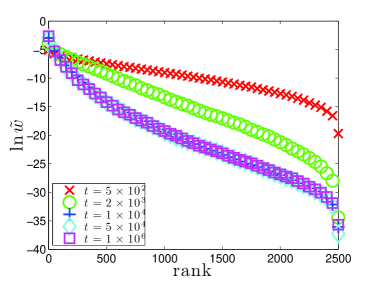

In Fig. 1 we plot the distribution of the rescaled wealth for agents as a function of the rank of their wealth for , , and at different times. After an initial transient the distributions collapse onto a single curve indicating that the wealth distribution rescaled by the total wealth reaches a steady state, which we refer to as a rescaled steady state. During the transient the wealth disparity between rich and poor agents grows until the rescaled steady state is established. Once the rescaled steady state is reached, the form of the distribution (and the ratio of the wealth between rich and poor ranks) remains fixed, while the wealth in every rank grows as . Hence for a rising tide does raise all boats.

As for fixed , the rescaled steady state takes longer to establish, and the wealth distribution is less equal; i.e., the wealthiest have a greater share of the total wealth when the rescaled steady state is reached.

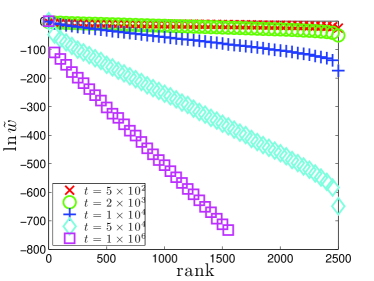

In Fig. 2 we plot the wealth distribution as a function of rank for , , and . No steady state is reached in the rescaled distribution. As wealth is added to the system, it is transferred to the wealthy via the exchange mechanism so inequality continues to grow.

For there is no rescaled steady state, and the wealth added by growth goes to the wealthiest agents while the wealth of the remaining agents declines with time. This behavior implies that there is a phase transition at . However, the behavior of the system as a function of is complicated.

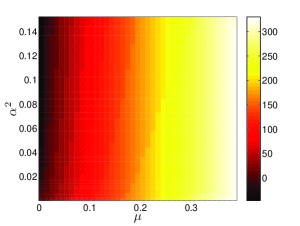

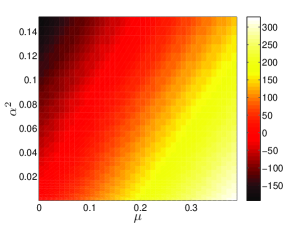

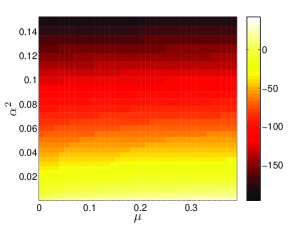

In Fig. 3 we plot the average wealth of the poorest 1% of the agents (out of a total of 2500) at for different values of , , and . For the average wealth of the poorest agents in the rescaled steady state is weakly dependent on but depends strongly on . For there is no rescaled steady state, but the average wealth of the poorest 1% depends strongly on and depends weakly on . For there is a boundary at where . For the wealth of the poorest increases with , while for the wealth of the poorest decreases with . This behavior is similar to the geometric random walk ole , for which there is a boundary between growth and decay for the wealth of the poorer agents (members of an ensemble) at ; is the amplitude of the random noise and, as in this work governs the geometric growth. Similar to the MAEM, the poorer agents’ wealth in the geometric random walk grows for and decays for .

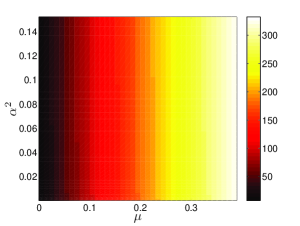

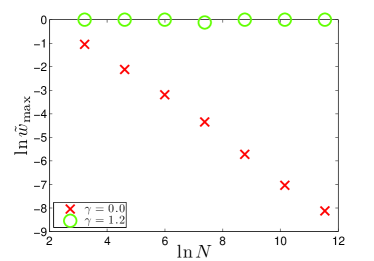

The behavior of the poorest differs from the evolution of the richest as can be seen by comparing Figs. 3 and 4. For the richest there is no sign of a boundary and the growth weakly depends on for all . A phase transition at for the wealthiest is found by looking at the rescaled wealth of the richest agent for as . For this rescaled wealth goes to zero as , and for it goes to a nonzero constant (see Fig. 5).

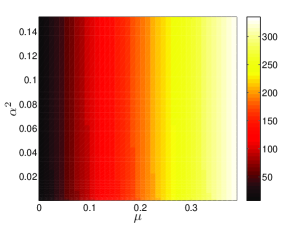

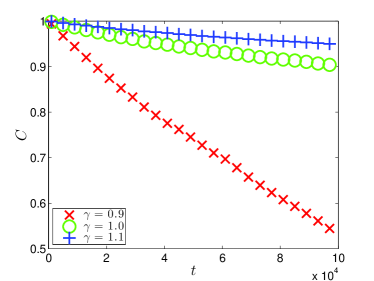

An important property is economic mobility. To determine the mobility we measure the Pearson correlation function pearson of the rank in the steady state.

| (3) |

where is the rank of the th agent and is the ensemble average of the rank. As can be seen from Fig. 6, as for , which indicates that the rank of the agents as is not correlated with their rank at . Hence, there is nonzero mobility in the MAEM for . For approaches a constant, indicating that there is a strong correlation of the rank at different times. Hence, there is a lack of mobility for .

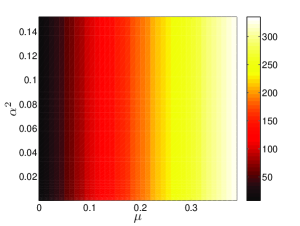

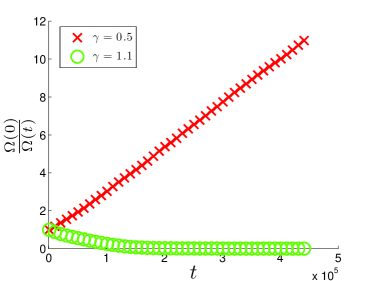

For the nonzero mobility suggests that the system is ergodic in the sense that the time averaged rescaled wealth of each agent equals the ensemble average of the rescaled wealth. This equality is known as effective ergodicity tm . To test the MAEM for effective ergodicity we use the rescaled wealth of the th agent, , to define a wealth metric as tm

| (4) |

where

| (5) |

and

| (6) |

If the system is effectively ergodic, tm . From Fig. 7 we see that the dependence of indicates effective ergodicity for and the absence of effective ergodicity for . We conclude from the -dependence of and that the system is ergodic for but not for .

Our numerical results suggest that the effect of adding growth to the AEM is to produce two “phases.” For the system does not reach a rescaled steady state, and in the limit the wealthiest agent has a finite fraction of the total wealth as . The system is not ergodic in the sense explained above and has some of the characteristics of the geometric random walk which is not ergodic ole ; ole-bill . For the system is effectively ergodic and reaches a rescaled steady state. The wealthiest agent has a zero fraction of the total wealth as . For the system has another transition at , and its behavior is similar to the geometric random walk.

The nature of these phases and the transitions is not well understood. For example, the time required for the system to reach a rescaled steady state as diverges as with , suggesting a critical point kang-et . However, the fraction of wealth possessed by the richest agent jumps from 0 to at . This finite discontinuity suggests that the transition is first-order.

It is very interesting that the MAEM is a driven system that might, for some range of parameter space, be treated by equilibrium methods in the limit of an infinite system. In this way it is similar to a driven dissipative system used to model earthquake faults rundle . The latter model is ergodic and can be described by a Boltzmann distribution in the infinite stress transfer limit. Among the several challenges this work presents is to better understand how exchange mechanisms in the limit results in ergodicity in driven systems and how to identify the “thermodynamic” control parameters as well as quantities such as the order parameter and the nature of the phase transitions.

The economic implications of the MAEM are also quite interesting. Our results suggest that there exists a transition or tipping point. As increases, the benefits of growth are weighted more toward the wealthy, and wealth inequality increases. However, as long as , the wealth of all ranks grows at the same rate once the rescaled steady state is reached. If the benefits of growth are skewed too much toward the wealthy (), the poor and middle rank agents no longer benefit from the growth, and the richest agent eventually accrues all the wealth.

There is some controversy as to whether economic systems are in equilibrium or even exhibit effective ergodicity ole ; ole-bill ; yak . As discussed in Refs. ole ; ole-bill , the geometric random walk is not ergodic, and hence equilibrium methods do not apply. However, one of the phases of the MAEM is effectively ergodic and might be described by an equilibrium approach. Because there is no reason to believe that parameters such as are temporal constants in real economies, the MAEM suggests that the applicability of equilibrium methods may be situational and vary with time.

We acknowledge useful conversations with O. Peters, J. I .Ogren and A. Gabel.

References

- (1) A. Chakraborti, I. M. Toke, M. Patriarca, and F. Abergel, Quant. Finance 11, 1013 (2011).

- (2) E. Gudreis, “Unequal America,” Harvard Magazine, July-August (2008).

- (3) John F. Kennedy, “Remarks in Heber Springs Arkansas at the dedication of the Greers Ferry Dam,” The American Presidency Project.

- (4) B. Boghosian, arXiv:1212.6300 (2012).

- (5) J. Angle, J. Math. Sociology 18, 27 (1993).

- (6) P. L. Krapivsky and S. Redner, Science and Culture 76, 424 (2010).

- (7) S. Ispolatov, P. L. Krapivsky, and S. Redner, J. Eur. Phys. B 2, 267 (1998).

- (8) O. Peters, Quant. Finance 11, 1593 (2011).

- (9) J. L. Rodgers and W. A. Nicewander, Amer. Stat. 42, 59 (1988).

- (10) O. Peters and W. Klein, Phys. Rev. Lett. 110, 100603 (2013).

- (11) D. Thirumalai and R. D. Mountain, Phys. Rev. A 42, 4574 (1990) and Phys. Rev. E 47, 479 (1993).

- (12) V. M. Yakovenko and J. B. Roser Jr., Rev. Mod. Phys. 81, 1703 (2009).

- (13) N. Lubbers, K. Liu, W. Klein, J. Tobochnik, B. Boghosian, and H. Gould, manuscript in preparation.

- (14) J. B. Rundle, W. Klein, S. Gross and D. L. Turcotte, Phys. Rev. Lett. 75, 1658 (1995).