22email: sitabhra@imsc.res.in 33institutetext: Uday Kovur 44institutetext: Department of Physics, Birla Institute of Technology & Science, Pilani 333031, India.

Uncovering the network structure of the world currency market: Cross-correlations in the fluctuations of daily exchange rates

Abstract

The cross-correlations between the exchange rate fluctuations of 74 currencies over the period 1995-2012 are analyzed in this paper. The eigenvalue distribution of the cross-correlation matrix exhibits a bulk which approximately matches the bounds predicted from random matrices constructed using mutually uncorrelated time-series. However, a few large eigenvalues deviating from the bulk contain important information about the global market mode as well as important clusters of strongly interacting currencies. We reconstruct the network structure of the world currency market by using two different graph representation techniques, after filtering out the effects of global or market-wide signals on the one hand and random effects on the other. The two networks reveal complementary insights about the major motive forces of the global economy, including the identification of a group of potentially fast growing economies whose development trajectory may affect the global economy in the future as profoundly as the rise of India and China has affected it in the past decades.

1 Introduction

At whatever scale one studies economic phenomena, we can find complex systems, comprising relatively large number of mutually interacting elements often connected to each other in non-trivial topologies, at work. The components can be individual traders, firms, banks, markets or countries, but however complicated the behavior of the individual agents in the system, an even richer collective behavior is manifested at the scale of the entire group of interacting agents. Explaining the emergence of such systems-level phenomena which may be qualitatively different from the properties exhibited by the individual components is one of the key goals of many physicists working on socio-economic questions, an enterprise that is often referred to as econophysics Sinha11 . An important step in this direction will be to identify features of economic systems that are universal, in the sense of occurring at many different scales, suggesting that their existence is not contingent upon the particular conditions prevailing in a specific situation. This will help econophysicists to focus on phenomena that are not just the outcome of a series of historical accidents and which can therefore be potentially explained by generalizable mechanisms.

Market dynamics has been identified by many physicists as a particular area of economics that has the potential for yielding several such universal features. In particular, one can mention the identification of scale-invariant distributions in price fluctuations, the trading volume and number of trades Gabaix03 ; Farmer05 in equities markets (but see also Ref. Vikram11a ). However, in order to get an understanding of how qualitatively new features emerge at the level of the collective dynamics of the entire market, one needs to understand the nature and structure of interactions between the agents. While several studies on the networks underlying equities markets (e.g., Ref. Sinha07 ) have been done, we need to compare between markets of different kinds in order to distinguish those features that are particular to specific systems and those which are universal. With this aim, we undertake a detailed investigation of the world currency market in this article. While several previous studies have looked at the cross-correlations between the foreign exchange rates of different currencies (e.g., see Refs. Ausloos01 ; Mizuno06 ; Drozdz07 ), our results reveal several novel insights and unexpected features of the network of interactions between the currencies that we reconstruct from the cross-correlations data. The period of the preceding sixteen years we have chosen for our study has seen remarkable transformations in the world economy with the emergence of new economic powerhouses such as China and India, but it has also shown how our world is vulnerable to massive system-spanning crises (such as that of 2007-08). The study of networks in the global currency market provides an important perspective with which to view the positive as well negative impacts of globalization. It has been argued that globalization is neither a completely new phenomenon in world history nor are its effects always beneficial to the economy Jennings11 . We hope that by investigating the collective dynamics of the international trade in currencies in order to identify the major motive forces of the world economy, one can potentially understand the long-term trends and prospects of globalization.

2 The World Currency Market

The foreign exchange (FX) market, representing the entire global decentralized trading of various currencies, is the largest financial market in the world with an average daily trading volume estimated in 2010 to be US Dollars BIS10 . A typical trade in the FX market consists of a pair of agents exchanging a certain amount of a particular currency for a mutually agreed amount of another currency. The ratio of the amounts of the two currencies changing hands specify the corresponding exchange rate for the pair of currencies concerned. Thus the exchange rates determine the value of a currency with respect to another (the numeraire). The modern FX market characterized by a large number of currencies having floating exchange rates which continuously fluctuate over time date from the 1970s. The varying rates reflect the changing demand and supply for the currencies, and are thought to be directly influenced by the trade deficit/surplus of the corresponding countries Sarkar06 as well as macroeconomic variables such as changes in growth of the gross domestic product, interest rates, etc. However, international events can often trigger large perturbations in the FX market and it is possible that sudden changes in the exchange rates of a certain group of currencies can spread over time, eventually affecting a much larger number of currencies. Our article aims at uncovering the network of interactions between the different currencies of the FX market along which perturbations can propagate in the world currency market.

Description of the data set. We have considered the daily exchange rate of currencies in terms of US Dollars (i.e., the base currency) publicly available from the website of the financial services provider company, Oanda Corporation oanda . We have chosen the US Dollar as the numeraire as it is currently the primary reserve currency of the world and is most widely used in international transactions. The daily rates are computed as the average of all exchange rates (taken as the midpoint of the bid and ask rates) quoted during a 24-hour period prior to the day of posting the rate. For cross-correlation analysis, we have focused on the price data of currencies from October 23, 1995 to April 30, 2012, which corresponds to working days. The choice of currencies was governed by our decision to only include those which either follow a free float or a managed float exchange rate regime. We have thus avoided currencies such as the Chinese yuan whose rate of exchange is pegged against another currency so that the value of currency does not vary appreciably in time (resulting in trivial cross-correlations). We have also excluded countries having a dollarized economy such as Panama, Ecuador Vietnam or Zimbabwe, that use a foreign currency - in majority of cases, the US Dollar - instead of or alongside the domestic currency, as this introduces strong artifacts in the cross-correlations. The period of observation was chosen so as to maximize the volume of available data. Using the MSCI Market Classification Framework MSCI we have divided the countries to which the currencies belong into three categories: developed, emerging and frontier markets. This classification is based on a number of criteria including market accessibility, size and liquidity of the market and the sustainability of economic development. While many of the OECD countries belong to the developed category, the rapidly growing economies of Asia, Africa and Latin America (such as the BRICS group comprising Brazil, Russia, India, China and South Africa) are in the emerging category with the frontier markets category being populated by the remainder. The individual currencies, along with the above economic classification of the corresponding countries and the geographical regions to which they belong are given in Table 1.

| Currency code | Currency name | Type of market | Geographical region | |

|---|---|---|---|---|

| 1 | CAD | Canadian Dollar | Developed | Americas |

| 2 | DKK | Danish Krone | Developed | Europe and Middle-East |

| 3 | EUR | Euro | Developed | Europe and Middle-East |

| 4 | ILS | Israeli New Shekel | Developed | Europe and Middle East |

| 5 | ISK | Iceland Krona | Developed | Europe and Middle-East |

| 6 | NOK | Norwegian Kroner | Developed | Europe and Middle-East |

| 7 | SEK | Swedish Krona | Developed | Europe and Middle-East |

| 8 | CHF | Swiss Franc | Developed | Europe and Middle-East |

| 9 | GBP | Great Britain Pound | Developed | Europe and Middle-East |

| 10 | AUD | Australian Dollar | Developed | Asia-Pacific |

| 11 | HKD | Hong Kong Dollar | Developed | Asia-Pacific |

| 12 | JPY | Japanese Yen | Developed | Asia-Pacific |

| 13 | NZD | New Zealand Dollar | Developed | Asia-Pacific |

| 14 | SGD | Singapore Dollar | Developed | Asia-Pacific |

| 15 | BOB | Bolivian Boliviano | Emerging | Americas |

| 16 | BRL | Brazilian Real | Emerging | Americas |

| 17 | CLP | Chilean Peso | Emerging | Americas |

| 18 | COP | Colombian Peso | Emerging | Americas |

| 19 | DOP | Dominican Republic Peso | Emerging | Americas |

| 20 | MXN | Mexican Peso | Emerging | Americas |

| 21 | PEN | Peruvian Nuevo Sol | Emerging | Americas |

| 22 | VEB | Venezuelan Bolivar | Emerging | Americas |

| 23 | ALL | Albanian Lek | Emerging | Europe, Middle-East and Africa |

| 24 | DZD | Algerian Dinar | Emerging | Europe, Middle-East and Africa |

| 25 | CVE | Cape Verde Escudo | Emerging | Europe, Middle-East and Africa |

| 26 | CZK | Czech Koruna | Emerging | Europe, Middle-East and Africa |

| 27 | EGP | Egyptian Pound | Emerging | Europe, Middle-East and Africa |

| 28 | ETB | Ethiopian Birr | Emerging | Europe, Middle-East and Africa |

| 29 | HUF | Hungarian Forint | Emerging | Europe, Middle-East and Africa |

| 30 | MUR | Mauritius Rupee | Emerging | Europe, Middle-East and Africa |

| 31 | MAD | Moroccan Dirham | Emerging | Europe, Middle-East and Africa |

| 32 | PLN | Polish Zloty | Emerging | Europe, Middle-East and Africa |

| 33 | RUB | Russian Rouble | Emerging | Europe, Middle-East and Africa |

| 34 | ZAR | South African Rand | Emerging | Europe, Middle-East and Africa |

| 35 | TZS | Tanzanian Shilling | Emerging | Europe, Middle-East and Africa |

| 36 | TRY | Turkish Lira | Emerging | Europe, Middle-East and Africa |

| 37 | INR | Indian Rupee | Emerging | Asia |

| 38 | IDR | Indonesian Rupiah | Emerging | Asia |

| 39 | KRW | South Korean Won | Emerging | Asia |

| 40 | PHP | Philippine Peso | Emerging | Asia |

| 41 | PGK | Papua New Guinea Kina | Emerging | Asia |

| 42 | TWD | Taiwan Dollar | Emerging | Asia |

| 43 | THB | Thai Baht | Emerging | Asia |

| 44 | GTQ | Guatemalan Quetzal | Frontier | Americas |

| 45 | HNL | Honduran Lempira | Frontier | Americas |

| 46 | JMD | Jamaican Dollar | Frontier | Americas |

| 47 | PYG | Paraguay Guarani | Frontier | Americas |

| 48 | TTD | Trinidad Tobago Dollar | Frontier | Americas |

| 49 | HRK | Croatian Kuna | Frontier | Europe and CIS |

| 50 | KZT | Kazakhstan Tenge | Frontier | Europe and CIS |

| Currency code | Currency name | Type of economy | Geographical region | |

|---|---|---|---|---|

| 51 | LVL | Latvian Lats | Frontier | Europe and CIS |

| 52 | BWP | Botswana Pula | Frontier | Middle-East and Africa |

| 53 | KMF | Comoros Franc | Frontier | Middle-East and Africa |

| 54 | GMD | Gambian Dalasi | Frontier | Middle-East and Africa |

| 55 | GHC | Ghanaian Cedi | Frontier | Middle-East and Africa |

| 56 | GNF | Guinea Franc | Frontier | Middle-East and Africa |

| 57 | KES | Kenyan Shilling | Frontier | Middle-East and Africa |

| 58 | KWD | Kuwaiti Dinar | Frontier | Middle-East and Africa |

| 59 | MWK | Malawi Kwacha | Frontier | Middle-East and Africa |

| 60 | MRO | Mauritanian Ouguiya | Frontier | Middle-East and Africa |

| 61 | MZM | Mozambique Metical | Frontier | Middle-East and Africa |

| 62 | NGN | Nigerian Naira | Frontier | Middle-East and Africa |

| 63 | STD | Sao Tome and Principe Dobra | Frontier | Middle-East and Africa |

| 64 | SYP | Syrian Pound | Frontier | Middle-East and Africa |

| 65 | ZMK | Zambian Kwacha | Frontier | Middle-East and Africa |

| 66 | JOD | Jordanian Dinar | Frontier | Middle-East and Africa |

| 67 | BND | Brunei Dollar | Frontier | Asia |

| 68 | BDT | Bangladeshi Taka | Frontier | Asia |

| 69 | KHR | Cambodian Riel | Frontier | Asia |

| 70 | FJD | Fiji Dollar | Frontier | Asia |

| 71 | PKR | Pakistan Rupee | Frontier | Asia |

| 72 | WST | Samoan Tala | Frontier | Asia |

| 73 | LKP | Lao Kip | Frontier | Asia |

| 74 | LKR | Sri Lankan Rupee | Frontier | Asia |

3 The Return Cross-Correlation Matrix

To quantify the degree of correlation between the exchange rate movements for different currencies, we first measure the fluctuations using the logarithmic return so that the result is independent of the scale of measurement. If is the exchange rate of the -th currency at time (in terms of USD), then the logarithmic return is defined as

| (1) |

For daily return, = 1 day. By dividing the time-series of returns thus obtained with their standard deviation (which is a measure of the volatility of the currency exchange rate), , we obtain the normalized return, . We observed that the cumulative distribution of the returns displayed power-law scaling in the tails, i.e., where is the corresponding exponent value. Using maximum likelihood estimation, the exponents for the different currencies were obtained and they were found to be distributed over a narrow range of values with a peak around . This indicates that the so-called inverse-cubic law distribution of returns, reported in many studies of stock price fluctuations Lux96 ; Gopikrishnan98 ; Pan07b ; Pan08 , also holds for currency exchange rate movements Koedijk90 ; Muller90 . This further strengthens the universality of this empirical fact about the nature of market fluctuations and supports the validity of explaining this feature using very general models which do not consider details of particular markets or economies (see, e.g., Ref. Vikram11b ).

After obtaining the return time series for all currencies over the period of days, we calculate the cross-correlation matrix whose individual elements , represent the correlation between returns for a pair of currencies and . If the fluctuations of the different currencies are uncorrelated, the resulting random correlation matrix (referred to as a Wishart matrix) has eigenvalues distributed according to Sengupta99 :

| (2) |

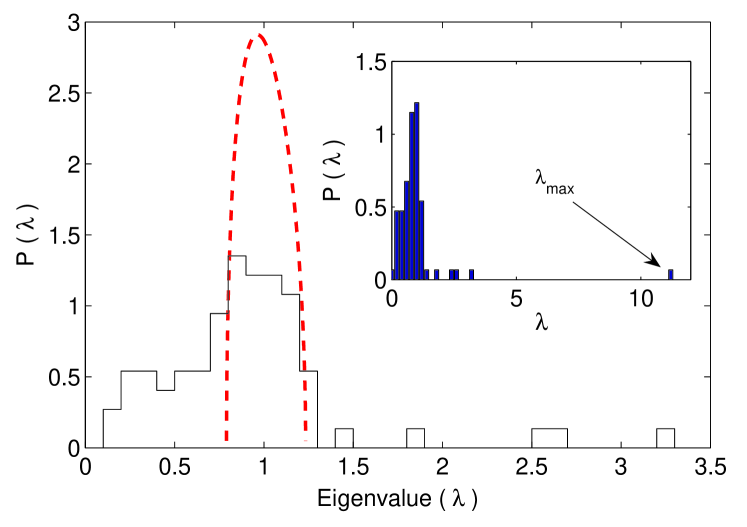

with , such that . The bounds of the distribution are given by and . For the data we have analyzed, , which implies that in the absence of any correlation the spectral distribution should be bounded between and . We observe from Fig. 1 that the bulk of the empirical eigenvalue distribution indeed falls below the upper bound given by , although a significant fraction of the eigenvalues are smaller than what we expect from the lower bound . Also, a small number () of the largest eigenvalues are seen to deviate from the bulk of the distribution predicted by random matrix theory, and we focus our analysis on these modes to obtain an understanding of the interaction structure of the world currency market.

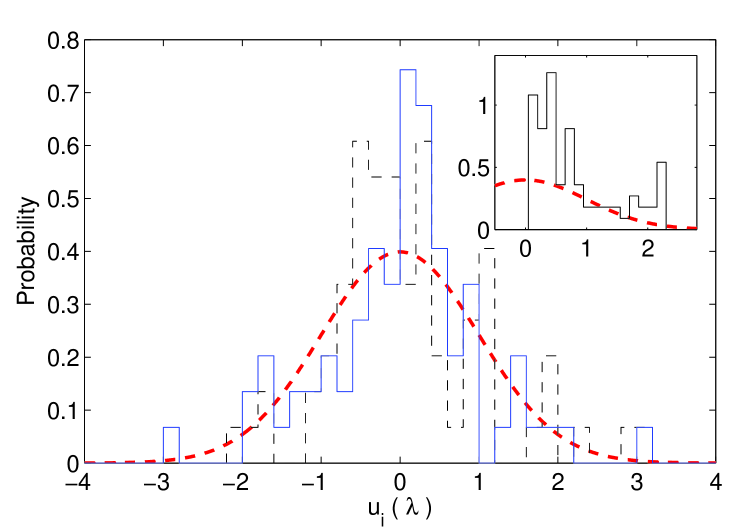

The random nature of the eigenvalues occurring in the bulk of the distribution is also indicated by the distribution of the corresponding eigenvector components. Note that, these components are normalized for each eigenvalue such that, , where is the -th component of the th eigenvector. For random matrices generated from uncorrelated time series, the distribution of the eigenvector components follows the Porter-Thomas distribution,

| (3) |

We have explicitly verified this form for the corresponding distribution of the random surrogate matrices obtained by shuffling the empirical return time series so that all correlations between the different currencies are destroyed. As seen from Fig. 2, it also approximately fits the distributions of the eigenvector components for the eigenvalues belonging to the bulk of the empirical spectral distribution. However, the eigenvectors of the largest eigenvalues (e.g., the largest eigenvalue , as shown in the inset) deviate quite significantly, indicating its non-random nature.

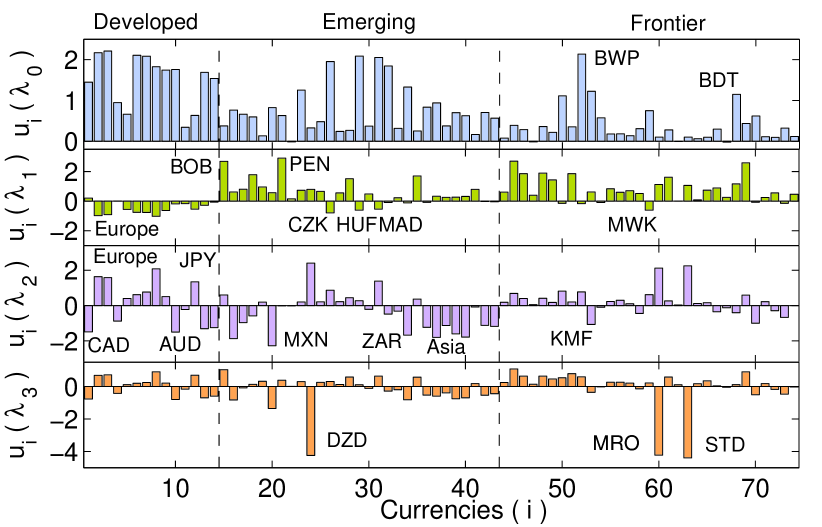

The largest eigenvalue for the cross-correlation matrix is about 9 times larger than the upper bound of the random spectral distribution. While this is similar to the situation for cross-correlations of stock movements in financial markets (e.g., see Ref. Sinha07 ; Pan07a ), the corresponding eigenvector does not show a relatively uniform composition unlike the case in equities markets where almost all stocks contribute to this mode with all elements having the same sign. Instead, there is large variation in the relative contributions of the different components to the largest eigenmode, with those of four currencies (VEB, PYG, NGN, BND) having a different sign than the rest - although with an extremely low magnitude (Fig. 3, top). This eigenmode represents the global component of the time-series of currency fluctuations which is common to all currencies. Thus, the strength of the relative contribution of a currency to the leading eigenvector can be construed as the extent to which the currency is in sync with the the overall movement of the world currency market reflecting the collective response of the world economy to information shocks (which may include major perturbations such as the worldwide financial crisis of 2007-08). Note that, this suggests that the relative strengths of the components in the leading eigenvector may be used as a measure of the role the corresponding currency plays in the world market (and to an extent, that the country plays in the international economy). Seen from this point of view, it is perhaps not surprising that most of the currencies belonging to countries in the developed markets category contribute significantly to this mode which reflects their dominance in the world economy. We also see that the countries in the emerging markets category can be very different from each other in terms of their role in the global mode, with components corresponding to the East European economies such as Czech Republic, Hungary and Poland having some of the largest contributions. Turning to the frontier markets category, while the contributions of most of these currencies have very low magnitude, a few countries (most notably Botswana but also Bangladesh, Kazakhstan and Comoros) stand out for the relatively high strength of the corresponding eigenvector component. The strong contribution from these countries could be either because of their impressive economic performance (e.g., Botswana has maintained one of the world’s highest economic growth rates from the time of its independence in 1966 cia ) or possibly due to remittances in foreign currencies from expatriates working abroad having a large contribution to the national economy (as in the case of Bangladesh). As newly developing economies are potentially highly profitable but risky targets for foreign investment, it may be of interest to explore the possibility of using this measure to identify frontier markets having strong interaction with the world market which may make them relatively safer to invest in. On the other hand, from the point of view of portfolio diversification for reducing risk, one may use such a measure to identify economies whose fluctuations have the least in common with the global mode.

Of even more interest for understanding the topological structure of interactions in the world currency market are the intermediate eigenvalues in between the largest eigenvalue and the bulk predicted by random matrix theory. For equities markets, it has been shown that in many cases the eigenvectors corresponding to these eigenvalues are localized, i.e., a relatively small number of stocks, usually having similar market capitalization or belonging to the same business sector, contribute significantly to these modes Pan07a ; Gopikrishnan01 ; Plerou02 . Fig. 3 shows that the different currencies contribute to the different eigenvectors corresponding to the three largest intermediate eigenvalues very unequally. For example, from the eigenvector corresponding to , the second largest eigenvalue, we observe that many Latin American currencies such as those of Bolivia and Peru, have a dominant contribution in this mode with the contribution of European currencies (and a few non-European ones, such as those of Morocco and Malawi, where the corresponding economy is closely connected to that of Europe) being not only different but actually having the opposite sign. The third eigenvector exhibits contributions of different signs from European and Japanese currencies on the one hand, and established as well as rapidly developing economies of America, Asia-Pacific and Africa (such as Canada, Mexico, South Africa, Australia, New Zealand, Israel, Singapore and India) on the other. The fourth eigenvector has significant contributions from only three currencies, those of Algeria, Mauritania and Sao Tome & Principe. This may reflect existing economic linkages between these countries that has resulted in such strong coupling in the movements of their currency exchange rates with respect to the US Dollar.

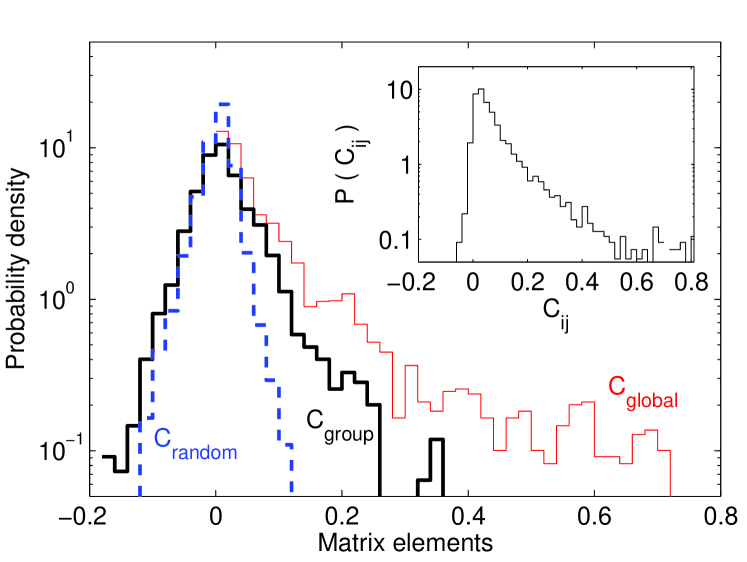

Despite the above insights, a direct inspection of eigenvector composition for the intermediate eigenvalues does not very often yield a straightforward interpretation of the group of currencies dominantly contributing to a particular mode. This is because apart from information about interactions between currencies, the cross-correlations are also affected strongly by the global mode corresponding to the overall market movement. In addition, there are a large number of modes belonging to the random bulk which correspond to idiosyncratic fluctuations. Both the global and random modes can mask significant intra-group correlations. Thus, in order to identify the topological structure of interactions between the currencies we need to remove the global mode corresponding to the largest eigenvalue and also filter out the effect of random noise (contributed by the eigenvalues belonging to the bulk of the spectral distribution). For this we use the filtering method proposed in Ref. Kim05 based on the expansion of a matrix in terms of its eigenvalues and the corresponding eigenvectors : . This allows the correlation matrix to be decomposed into three parts, corresponding to the global, group and random components:

| (4) |

where, the eigenvalues have been arranged in descending order (the largest labelled 0) and is the number of intermediate eigenvalues. From the empirical data it may not be obvious what is the value of , as the bulk may differ from the predictions of random matrix theory because of underlying structure induced correlations. For this reason, we use visual inspection to choose , and verify that small changes in this value do not alter the results. Our results are robust with respect to small variations in the estimation of because the error involved is only due to the eigenvalues closest to the bulk that have the smallest contribution to . Fig. 4 shows the result of the decomposition of the entire cross-correlation matrix (shown in the inset) into the three components. In contrast to the case of stock-stock correlations in financial markets (e.g., Ref. Pan07a ), in the currency market the group correlation matrix elements show a significantly reduced tail and is completely enveloped by the distribution of the global correlation matrix elements . This implies that there are a relatively small fraction of strongly interacting currencies, implying that the segregation into groups may be weak in this market.

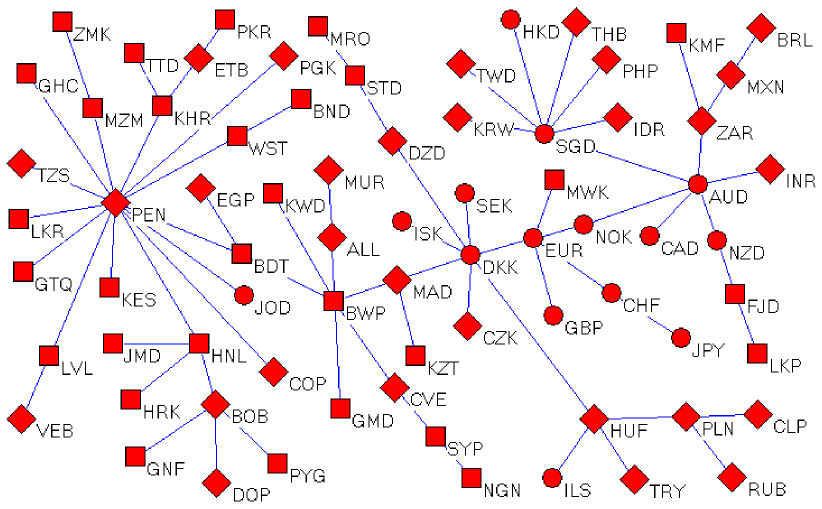

In order to graphically present the interaction structure of the stocks using the information in the group correlation matrix Cgroup, we first use a method suggested by Mantegna Mantegna99 to transform the correlation between currencies into distances to produce a connected network in which co-moving currencies are clustered together. The distance between two currencies and are calculated from the cross-correlation matrix , according to . These are used to construct a minimum spanning tree, which connects all the nodes of a network with edges such that the total sum of the distance between every pair of nodes, , is minimum. As seen in Fig. 5, for the currency market this method reveals clusters of currencies belonging to countries having similar economic profile and/or belonging to the same geographical region. In particular, note the cluster centered around the hub node (i.e., a node having significantly more connections than the average) corresponding to SGD which consists exclusively of currencies belonging to developed or emerging economies of the Asia-Pacific region such as those of Hong Kong, Taiwan, Thailand, Indonesia etc. On the other hand, the currencies clustered around the hub AUD are related by the geo-economic status of the corresponding countries of being major non-European players in the world economy (e.g., Canada, Mexico, Brazil, South Africa and India). It should be noted that the hubs of these two clusters (SGD and AUD) are directly linked to each other and are in turn connected to the cluster of European currencies (comprising two hubs corresponding to the Euro and the Danish currency) suggesting a close interplay in the currency movements of all the important countries driving international economic dynamics. Possibly more intriguing is the occurrence of a much bigger cluster (containing a third of all the currencies considered) arranged around the largest hub in the network which corresponds to the Peruvian currency. This cluster comprises a wide assortment of currencies belonging to countries spread geographically around the world but which share an economic resemblance in that most of them are in a relative state of underdevelopment compared to the economies considered earlier. It thus appears that the tree network representing the underlying interactions in the world currency market can be approximately divided into a part comprising developed or rapidly growing economies (dominated by Europe and Asia-Pacific) and another part composed of relatively underdeveloped ones (consisting mostly of Latin American and African countries), with the currency movements of these two groups being relatively independent of each other. Note that the two parts, in particular, the hubs corresponding to PEN and DKK, are bridged by the currencies of Morocco, Botswana and Bangladesh, which therefore have an importance in governing the collective dynamics of the world economy disproportionate to their intrinsic economic status. This can potentially explain the strong contribution of these currencies to the leading eigenvector of the cross-correlation matrix that represents the global eigenmode which has been discussed earlier in this article.

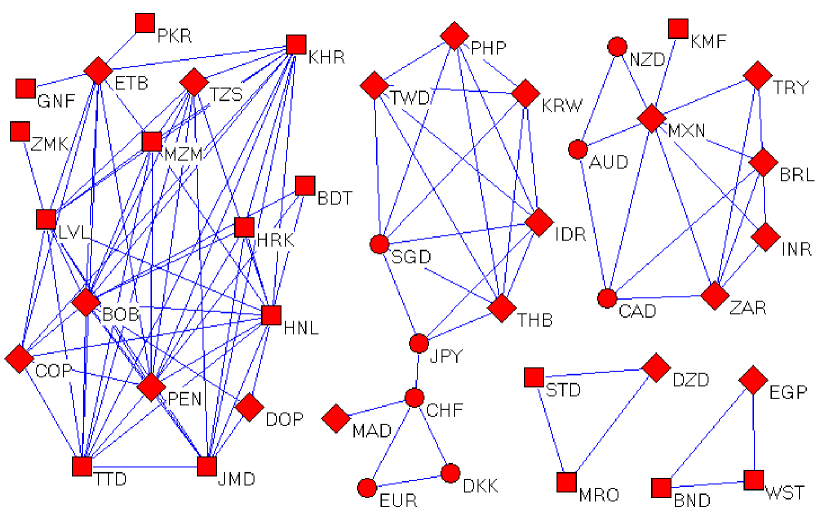

We have also used an alternative method of graph visualization in order to highlight any existing groups of currencies having significant mutual interactions. For the case of stocks in financial markets, the modules obtained by this technique often represent strongly performing business sectors in the economy Sinha07 ; Pan07a . It is thus plausible that the currency communities identified using this method will represent important groupings driving the world economy. The binary-valued adjacency matrix of the network is generated from by using a threshold such that if , otherwise. An appropriate choice of the threshold makes apparent any clustering in the network that is implied by the existence of a tail in the distribution. Fig. 6 shows the resultant network for the best choice of (= 0.133) in terms of creating the largest clusters of interacting currencies (isolated nodes have not been shown). The five clusters differ considerably in size, with two of them corresponding to strongly interacting currency triads (with the DZD-MRO-STD triad being the currencies having the dominant contribution to the fourth largest eigenmode identified earlier in Fig. 3). The next largest cluster, having nine currencies, consists of rapidly emerging economies outside Europe - including Brazil, India and South Africa of the BRICS group as well as Turkey and Mexico from the “Next Eleven” (N-11) group identified in Ref. Oneill05 as countries having potential of becoming some of the largest economies in the world in the coming years - and a few non-European developed economies such as Australia and Canada. The even larger cluster comprising eleven currencies is dominated by the countries of Asia-Pacific such as Taiwan and Singapore as well as the N-11 countries Indonesia, Korea and Philippines, which have either developed or fast growing economies; however, through the Japanese Yen, these currencies are also connected to a smaller sub-cluster of European currencies which contains the Euro apart from the Swiss and Danish currencies (note also the presence of the currency of Morocco, a north African country but one that has strong economic ties with Europe). The largest cluster has seventeen densely inter-connected currencies which are geographically spread around the world, although half of them are from Latin America or the Caribbean. Possibly this cluster reflects a new wave of fast growing economies (e.g., it includes two N-11 countries, Bangladesh and Pakistan) whose development trajectory may affect the global economy in the future as profoundly as the rise of India and China has affected it in the past decades.

4 Conclusions

In this article we have analyzed the topological structure of interactions in the world currency market by using the spectral properties of the cross-correlation matrix of exchange rate fluctuations. We see that the eigenvalue distribution is similar to that seen in equities markets and consists of a bulk approximately matching the predictions of random matrix theory. In addition, there are several deviating eigenvalues which contain important information about groups of strongly interacting components. However, the composition of the leading eigenvector shows a remarkable distinction in that, unlike the relatively homogeneous nature of the eigenvector for cross-correlations in the equities market where all stocks contribute almost equally to the market or global mode, the different currencies can have widely differing contributions to the global mode for exchange rate cross-correlations. This possibly reflects the extent to which the fluctuations of a currency is in sync with the overall market movement and may also be used to measure the influence of a currency in the world economy. While, as is probably expected, the large components of this mode mostly belong to currencies of the developed economies of western Europe as well as the rapidly growing economies of the Asia-Pacific region, there are unexpectedly strong contributions from currencies outside this group - such as those of Botswana, Bangladesh and Kazakhstan. This indicates that these economies may be playing an important role in directing the collective dynamics of the international currency market that is not exclusively dependent on their intrinsic economic strength, but rather the position they occupy in the network of interactions among the currencies. This is confirmed by the reconstructed network of interactions among the currencies as a minimum spanning tree. This network shows a segregation between clusters dominated by developed or rapidly growing economies on the one hand, and relatively underdeveloped economies on the other. While these two parts can show dynamics relatively independent of each other, a few currencies - those of Morocco, Botswana and Bangladesh - act as a bridge between them. Thus the role of these currencies as vital connecting nodes of the world currency market possibly give them a much more important position than would be expected otherwise. We have also used an alternative graph representation technique to identify several groups of strongly interacting currencies. Some of the smaller clusters may be reflecting possible economic or other relations between the corresponding countries. However, the largest cluster comprises a densely interconnected set of currencies belonging to countries that are geographically spread apart. We speculate that these could well belong to the next wave of fast emerging economies that will drive the economic growth of the world in the future. This is significant from the point of view of applications, as such economies are potentially lucrative targets for foreign investment and are eagerly sought after by portfolio fund managers. Methods of identifying early the next fast growth economies assume critical importance in such a situation. Our analysis of cross-correlations of exchange rate fluctuations suggests that prominent clusters in the reconstructed networks of interactions in the world currency market may potentially provide us with such methods.

Acknowledgements.

We would like to thank R K Pan who helped in developing the software used for the analysis reported here and S Sridhar for stimulating discussions. Part of the work was supported by the Department of Atomic Energy, Government of India through the IMSc Complex Systems Project (XII Plan).References

- (1) Sinha S, Chatterjee A, Chakraborti A, Chakrabarti BK (2011) Econophysics: An Introduction. Wiley-VCH, Weinheim

- (2) Gabaix X, Gopikrishnan P, Plerou V, Stanley HE (2003) A theory of power-law distributions in financial market fluctuations. Nature (Lond.) 423: 267-270.

- (3) Farmer, JD, Smith DE, Shubik M (2005) Is economics the next physical science ? Physics Today 58(9): 37–42

- (4) Vijayaraghavan VS, Sinha S (2011) Are the trading volume and the number of trades distributions universal ? In: Abergel F, Chakrabarti BK, A Chakraborti, Mitra M (eds) Econophysics of Order-driven Markets. Springer, Milan, pp. 17-30.

- (5) Sinha S, Pan RK (2007) Uncovering the internal structure of the Indian financial market: Large cross-correlation behavior in the NSE. In: Chatterjee A, Chakrabarti BK (eds) Econophysics of Markets and Business Networks. Springer, Milan, pp. 3-19.

- (6) Pan RK, Sinha S (2007) Collective behavior of stock price movements in an emerging market. Phys. Rev. E 76: 046116.

- (7) Ausloos M, Ivanova K (2001) Correlations between reconstructed EUR exchange rates versus CHF, DKK, GBP, JPY and USD. Int. J. Mod. Phys. C 12: 169-195.

- (8) Mizuno T, Takayasu H, Takayasu M (2006) Correlation network among currencies. Physica A 364: 336-342.

- (9) Drozdz S, Gorski AZ, Kwapien J (2007) World currency exchange rate cross-correlations. Eur. Phys. J. B 58: 499-502.

- (10) Jennings J (2011) Globalizations and the ancient world. Cambridge Univ. Press, Cambridge.

- (11) Bank for International Settlements (2010) Foreign exchange and derivatives market activity in April 2010. Triennial Central Bank Survey

- (12) Sarkar A, Barat P (2006) Fluctuation dynamics of exchange rates on Indian financial market. In: Chatterjee A, Chakrabarti BK (eds) Econophysics of Stock and Other Markets. Springer, Milan, pp. 67-76.

- (13) http://www.oanda.com/currency/historical-rates/

- (14) http://www.msci.com/products/indices/market_classification.html

- (15) Lux T (1996) The stable Paretian hypothesis and the frequency of large returns: an examination of major German stocks. Appl. Fin. Econ. 6: 463-475.

- (16) Gopikrishnan P, Meyer M, Amaral LAN, Stanley HE (1998) Inverse cubic law for the distribution of stock price variations. Eur. Phys. J. B 3: 139–140.

- (17) Pan RK, Sinha S (2007) Self-organization of price fluctuation distribution in evolving markets. Europhys. Lett. 77: 58004.

- (18) Pan RK, Sinha S (2008) Inverse-cubic law of index fluctuation distribution in Indian markets. Physica A 387: 2055-2065.

- (19) Koedijk KG, Schafgans MMA, deVries CG (1990) The tail index of exchange rate returns. J. Internat. Econ. 29: 93-108.

- (20) Muller, UA, Dacorogna MM, Olsen RB, Pictet OV, Schwarz M, Morgenegg C (1990) Statistical study of foreign exchange rates, empirical evidence of a price change scaling law, and intraday analysis. J. Banking Finance 14: 1189-1208.

- (21) Vikram SV, Sinha S (2011) Emergence of universal scaling in financial markets from mean-field dynamics. Phys. Rev. E 83: 016101.

- (22) Sengupta A M, Mitra P P (1999) Distribution of singular values for some random matrices. Phys. Rev. E 60: 3389-3392.

- (23) http://www.cia.gov/library/publications/the-world-factbook/geos/bc.html

- (24) Gopikrishnan P, Rosenow B, Plerou V, Stanley H E (2001) Quantifying and interpreting collective behavior in financial markets. Phys. Rev. E 64: 035106.

- (25) Plerou V, Gopikrishnan P, Rosenow B, Amaral L A N, Guhr T, Stanley H E (2002) Random matrix approach to cross correlations in financial data. Phys. Rev. E 65: 066126.

- (26) Kim D-H, Jeong H (2005) Systematic analysis of group identification in stock markets. Phys. Rev. E 72: 046133.

- (27) Mantegna R N (1999) Hierarchical structure in financial markets. Eur. Phys. J. B 11: 193–197

- (28) O’Neill J, Wilson D, Purushothaman R, Stupnytska (2005) How solid are the BRICs. GS Global Economics Paper 134.