Identification of Signal, Noise, and Indistinguishable Subsets in High-Dimensional Data Analysis

X. Jessie Jeng ††X. Jessie Jeng is an Assistant Professor in the Department of Statistics, North Carolina State University, 27695.

Abstract

Motivated by applications in high-dimensional data analysis where strong signals often stand out easily and weak ones may be indistinguishable from the noise, we develop a statistical framework to provide a novel categorization of the data into the signal, noise, and indistinguishable subsets. The three-subset categorization is especially relevant under high-dimensionality as a large proportion of signals can be obscured by the large amount of noise. Understanding the three-subset phenomenon is important for the researchers in real applications to design efficient follow-up studies. We develop an efficient data-driven procedure to identify the three subsets. Theoretical study shows that, under certain conditions, only signals are included in the identified signal subset while the remaining signals are included in the identified indistinguishable subsets with high probability. Moreover, the proposed procedure adapts to the unknown signal intensity, so that the identified indistinguishable subset shrinks with the true indistinguishable subset when signals become stronger. The procedure is examined and compared with methods based on FDR control using Monte Carlo simulation. Further, it is applied successfully in a real-data application to identify genomic variants having different signal intensity.

Keywords: Two-Level Thresholding; Signal detection; False positive control; False negative control; Multiple testing; Variable screening.

1 Introduction

The problem of identifying a small number of signals from a large amount of noise is a central topic in modern statistics due to motivations from a wide spectrum of emerging applications. Examples include the detection of astrophysical sources, surveillance for disease outbreaks, identification of causal genetic markers, etc. In real applications, it is frequently observed that strong signals can easily stand out, while weak ones are often mixed indistinguishably with the noise. This phenomenon is especially relevant under high-dimensionality as a large proportion of signals can be obscured by the large amount of noise..

In this paper, we aim to extract valuable information from the data by categorizing the data into the signal, noise, and indistinguishable subsets. More specifically, we want to identify the signal subset in the data which includes only true signals, the noise subset which includes only noise, and the indistinguishable subset, where signals and noise cannot be separated. To formulate the problem rigorously, let be the collection of noise in the data, and the collection of true signals. The p-value of the data

| (1) |

where is the uniform distribution on and is some unknown continuous distribution with for all . The -values are ordered as . Define as the separation point between the signal and indistinguishable subsets, and the separation point between the indistinguishable and noise subsets, i.e. and . Our goal is to identify the three subsets by estimating and .

Understanding the three-subset phenomenon can be important for the researchers in real applications to design appropriate follow-up studies and allocate their resources more efficiently. For instance, candidates in the signal subset may have priority for more focused study, while those in the noise subset can be removed; and, for candidates in the indistinguishable subset, additional data may be collected to further separate weak signals from the noise (Conneely and Boehnke (2010), Spencer et al. (2009), Suresh and Chandrashekara (2012), etc.).

The proposed framework of three-subset categorization helps to enrich current studies in multiple testing, which largely focus on the dichotomy of rejecting versus not rejecting null hypotheses. By controlling false positives, multiple testing procedures identify strong signals with high confidence. Popular criteria for false positive control include family-wise error (FWER) control (Dudoit et al. (2003), Dudoit et al. (2004), etc.) and false discovery rate (FDR) control (Benjamini and Hochberg (1995, 2000)). Recent developments in multiple testing focus on improving the power of FDR procedures and controlling FDR under dependence (Genovese and Wasserman (2004), Storey et al. (2004), Abramovich et al. (2006), Sun and Cai (2007), Efron (2007), Fan et al. (2012), etc.). These studies, however, would not provide informative results for the weak signals that are indistinguishable from the noise as these signals cannot be separated by controlling the selection of the noise alone. The higher the dimensionality is, the more indistinguishable signals are, and the less efficient the criterion of false positive control could be. This limitation can hinder meaningful applications of multiple testing procedures in ultra-high dimensional data analysis.

To delineate the indistinguishable and noise subsets would require an adaptive bound for the range of the weak signals. As the signals are often very sparse compared to the amount of noise, it is a challenging task to provide a statistical framework to characterize the weak signals. For instance, power analysis in multiple testing is well known to be difficult due to the limited information about the true signals. Another example is in variable selection, where screening procedures are developed to identify and then remove the noise subset (Fan and Lv (2008), Hall and Miller (2009), Fan et al. (2009), Fan et al. (2011), Zhu et al. (2011), Li et al. (2012), etc.). While significant efficiency has been demonstrated for these methods in handling ultra-high dimensional data, setting a good screening parameter remains a difficult problem as it depends on the proportion and intensity of the non-zero coefficients, which are hard to be inferred from the data. Because of the inherent difficulty of weak signal inference, even though the phenomenon of three subsets has been frequently observed (e.g. Drton and Perlman (2008)), no rigorous statistical studies have been developed to explore the properties of the three subsets, neither is an efficient categorization method available up-to-date.

In this paper, we demonstrate the existence of the signal, noise, and indistinguishable subsets in Section 2 and connect the results with some recent developments in exact signal recovery. An efficient data-driven procedure called Two-Level Thresholding (TLT) is proposed in Section 3 to identify the three subsets by estimating the separation points and . is estimated by the first level threshold , which strongly controls false positives and only selects strong signals with high probability. The more challenging part is the construction of , the second level threshold for the separation point between the indistinguishable and noise subsets. We develop a data-driven step-down procedure that traverses the ordered -values until all signals are likely to be included. We show that, under certain conditions, only signals are included in the identified signal subset while the remaining signals are included in the identified indistinguishable subset with high probability.

Besides controlling false positives and false negatives, the proposed TLT procedure adapts to the intensity of the signal, so that the two thresholding levels move closer to each other as signals become stronger and the indistinguishable subset reduces in size. In the case when all signals are strong enough to be well-separated from the noise, the two thresholding levels converge to a single point.

The construction of TLT is completely data-driven. No prior information of the data distribution is needed; neither are tuning parameters involved in the algorithm. The computation is very fast with complexity . These properties meet the needs of high-dimensional data applications.

The rest of the paper is organized as follows. We first demonstrates the existence of the three subsets in section 2. Then we introduce the construction of the TLT procedure with its theoretical properties for the identification of the three subsets in Section 3. Monte Carlo simulations are presented in Section 4 to compare the results of TLT with those of the methods based on FDR control. Real-data results are provided in Section 5 where we apply our procedure to analyze SNP array data. We conclude in Section 6 with further discussions. The proofs are relegated to the Appendix.

2 Existence of The Three Subsets

In this section we first present the sufficient and almost necessary conditions for the existence of the signal, noise, and indistinguishable subsets. The results are connected to the recent developments in exact signal recovery. A simulation example is shown to demonstrate the relationship between the sizes of the three subsets and the signal intensity. To allow a succinct theoretical study, we assume, in this section, that the observations are generated independently from a normal mixture, i.e.,

| (2) |

The following theorem shows the sufficient and almost necessary conditions for the existence of the three subsets.

Theorem 2.1

Assume model (2). Then, asymptotically, the sufficient and almost necessary condition for the existence of the signal subset is

| (3) |

for the existence of the indistinguishable subset is

| (4) |

and for the existence of the noise subset is

| (5) |

for any .

Theorem 2.1 implies that (a) all three subsets exist when signals are sparse () and the signal intensity is between the two bounds in (3) and (4); (b) when signal intensity is too small (), no signals stand outside the range of the noise, and only the indistinguishable and noise subsets exist; and (c) when signal intensity is large enough (), all signals are excluded from the range of the noise, and only the signal and noise subsets exist. Moreover, (4) shows that the higher the dimensionality is, the more likely that the indistinguishable subset exists.

2.1 Connection to Exact Signal Recovery

It is interesting to note that the sufficient and almost necessary condition for the existence of the indistinguishable subset is closely related to the condition for exact signal recovery in Ji and Jin (2012) and in Xie et al. (2011). Adopting the similar calibrations:

| (6) |

we have the following result.

Corollary 2.1

Note that condition (8) delineates the complementary set of the exact recovery region in Ji and Jin (2012). In other words, only when the indistinguishable subset does not exist is it possible to recover all signals with probability . It is also interesting to see that condition (7) coincides with the detection boundary for the maximum statistic (Donoho and Jin 2004). This shows that only when the signal subset exists is it possible for the maximum statistic to separate the hypotheses and .

2.2 A Simulation Example

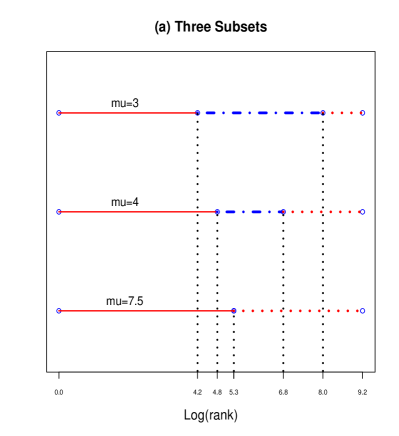

The simulation example in this section demonstrates the relationship between the signal intensity and the sizes of the three subsets. The performance of the proposed TLT procedure is also presented in this example. We generated observations and calculate their -values, among which are from and the rest from . We set at , , and . When , ; when , ; and when , . The three subsets and are delineated in Figure 1 (a) in log-scale for better view. It is clear that, as increases, the signal subset increases to include all true signals, and the indistinguishable subset decreases to an empty set.

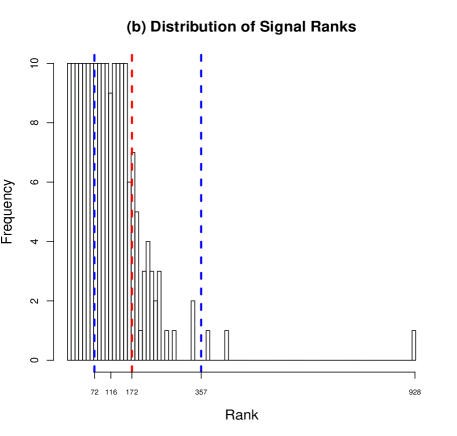

For the above example with and , the distribution of the ranks of the signals is presented in Figure 1 (b). Our estimates , and clearly , so that are all from signals. , however, is much smaller than , but include out of signals, suggesting it as a reasonable estimate for the separation between the indistinguishable and noise regions. For comparison, the cut-off point of the FDR procedure in Benjamini and Hochberg (1995) (BH-FDR) with the control level conventionally set at 0.05 is , which means BH-FDR selects from the ordered -values. The cut-off point of BH-FDR is between and , and larger than . Apparently, BH-FDR selects more signals than and a few noise, but still missing many of the signals.

3 Identification of The Three Subsets

In this section, we first construct the TLT procedure to estimate the separation points between the signal and indistinguishable subsets and between the indistinguishable and noise subsets, respectively. Similar to other adaptive procedures in multiple testing, we start with an estimate of the signal proportion . Various estimators have been developed in the literature under certain conditions on the data distribution. For example, Genovese and Wasserman (2004) and Meinshausen and Rice (2006) proposed two proportion estimators under a “purity” condition on the signal -values. Cai et al. (2007), Jin and Cai (2007), and Jin (2008) developed proportion estimators for normally distributed observations. Given an estimate for the signal proportion, our estimator for the separation between the signal and indistinguishable subsets is defined as

| (9) |

where is the tolerance level for false positives and as . The choice of the convergence speed of depends on how stringently one wants to control the family-wise type I error. Reasonable choice can be . can be regarded as an adaptive Bonferonni threshold. Its property of controlling false positives is relatively straightforward. The more challenging part is the construction of , the estimate of the separation between the indistinguishable and noise subsets. Even with the help of an estimate for signal proportion, one still does not know where the separation is since the signals are mixed with noise in the indistinguishable subset. Simply cutting at can include a lot of noise and miss many signals. We propose a data-driven procedure that traverses the ordered -values until all signals are likely to be included. This cut is defined as

| (10) |

where is the inverse cumulative distribution function of Beta, is the tolerance level for false negatives, and as . A reasonable choice can be . It is easy to see that is always greater than or equal to . In the case when , all signals are likely to rank before , then there is no need to go further along the ordered -values, and we set . On the other hand, means that some signals are missing in the first ordered -values, so that we need to go further to find all the signals. The search for starts at , which is the estimated number of signals, and ends at the smallest where is no greater than the -quantile of Beta, which is the distribution of the -th ordered -value from noise. The intuition here is that, suppose that not all signals rank before , then the number of noise in is likely to be greater than . Denote , then the -th ordered -value from noise is smaller than . This event, however, has a small probability due to the construction of where .

Next, we present theoretical results on the properties of the two thresholding levels and . For simplicity, we utilize the proportion estimator of Meinshausen and Rice (2006), which is also constructed based on -values. The estimator, defined as

| (11) |

is plugged into (9) and (10). Other proportion estimators can be used in the constructions of and in a similar way. The in (11) is a consistent estimator under the following conditions as presented in Theorem 2 and 3 in Meinshausen and Rice (2006). Let for some . Assume either

| (12) |

or

| (13) |

Condition (12) considers relatively dense signals with ; and all we need is the “purity” condition (Genovese and Wasserman (2004), Meinshausen and Rice (2006)). Condition (13) considers sparse signals with . In this case, stronger condition is needed for signal intensity, which is implied by (13).

Now we show that with high probability, only signals are ranked before and the number of signals ranked before converges to , the total number of signals. Let

for any integer .

Theorem 3.1

Theorem 3.1 shows that and are conservative estimates, which control false positives and false negatives respectively. While one can always achieve conservative estimates at and , the proposed estimators move closer to each other as signals become stronger and the indistinguishable subset gets smaller. When all signals are strong enough to be well-separated from the noise, and converge to a single point. This adaptivity property of the TLT procedure is presented in the following theorem with defined as the survival function of .

Theorem 3.2

Assume model (1). If signals are strong enough, such that for some . Then, with high probability, the indistinguishable subset does not exist, and for any satisfying , the signal and noise subsets are consistently separated by . That is,

| (16) |

as .

An intuitive understanding for the condition , , is that , which means that the total mass of is asymptotically between 0 and . Note that the expectation of the smallest -value from noise is . Therefore, with , all the -values of signals are well-separated from all the -values of noise.

Theorem 3.1 and 3.2 are developed for and with defined as in (11). If other proportion estimators are used, conditions in the theorems will be changed accordingly. For example, the proportion estimator in Cai et al. (2007) is designed for normally distributed noise and signals. Utilizing the additional properties of the distribution, this estimator is consistent under a weaker condition on the signal intensity in the sparse scenario compared to (13) (Cai et al. 2007). The theoretical properties of and in identifying the signal, noise, and indistinguishable subsets can be proved in a similar way.

In real applications, data may not satisfy the conditions for the existence of a consistent proportion estimator. However, prior knowledge can often allow practitioners to provide a possible range for the signal proportion. We demonstrate that the study of signal, noise, and indistinguishable subsets can still be carried out utilizing such prior knowledge. Suppose is bounded by

| (17) |

Define

| (18) |

and

| (19) |

where is the inverse cumulative distribution function for Beta. The next theorem states that the modified version and can still serve as conservative estimates for the separation points and .

Theorem 3.3

Although (, ) may not be as close as (, ) gets to (, ), they can provide useful information of the signal, noise, and indistinguishable subsets in many applications where conditions for the consistency of proportion estimation are hard to be satisfied and some informative prior knowledge of the signal proportion is available.

4 Simulation

In this section, we demonstrate, via simulation studies, the finite sample performance of the TLT procedure on the identification of the signal, noise, and indistinguishable subsets. In each example, observations are generated, in which the noise data points are sampled from and signals from . The selections of and with are compared with those of the BH-FDR with (Benjamini and Hochberg 1995) and the adaptive FDR (Benjamini and Hochberg (2000), Genovese and Wasserman (2004)). Setting at for results in a control level close to the conventional level (0.05) used by other methods, so that the results from different methods are comparable. is set to be equal to for simplicity.

Among the methods compared, BH-FDR is easiest to implement, while the others require estimating the signal proportion. The estimates and , the cut-off point of BH-FDR (), the cut-off point of the adaptive FDR (), as well as the number of false positives (FP) and the number of false negatives (FN) for each procedure are computed. We repeatedly generate the observations and compute performance measures for 100 times in each simulation example. The median and mean absolute deviation (MAD) of these measures are reported for more robust comparison results against the outliers in the 100 replications.

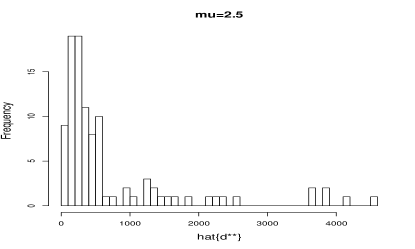

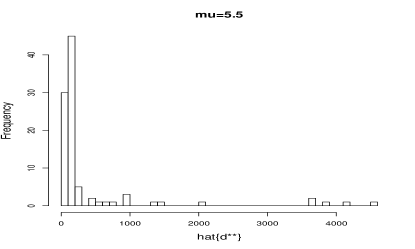

Example 1 shows the effect of signal intensity. Set and . Signal mean varies from to . Since the signal proportion is very small, the results of BH-FDR and the adaptive FDR are very close. To save space, the results of the latter are omitted in this example. Figure 2 presents the histograms of from the 100 replications for and . It shows that as signal intensity increases, the distribution of becomes more concentrated.

Table 1 shows that the cut-off point of BH-FDR () is between , the estimate of the separation between the signal and indistinguishable subsets (S-I Separation), and , the estimate of the separation between the indistinguishable and noise subsets (I-N Separation). As signal intensity increases, the indistinguishable subset shrinks and the cut-off locations of all three procedures move closer. As to the accuracy of identifying the signal, noise, and indistinguishable subsets, it is shown that the FPs of and are well controlled with having a bit higher FP when signal intensity increases. This agrees with our intuition since BH-FDR applies a less stringent rule to control false positives. FP of however is not controlled as it is not supposed to be. Interesting results are shown for the FN of . Among the signals, the proportions of mis-specified signals of are , , , and for , respectively. Compared with the FN of , which has mis-specified proportions of , , , and , has many fewer false negatives when signals are only moderately strong. This simulation shows that the proposed estimators and adapt to the signal intensity, and the identified indistinguishable subset between and shrinks with increasing .

| S-I Separation | BH-FDR | I-N Separation | |||||||

|---|---|---|---|---|---|---|---|---|---|

| FP | FN | FP | FN | FP | FN | ||||

| 3(1) | 0(0) | 97(1) | 8(4) | 0(0) | 92(4) | 325(269) | 261(253) | 28(19) | |

| 17(3) | 0(0) | 83(3) | 54(7) | 2(1) | 48(6) | 194(113) | 103(97) | 11(9) | |

| 54(4) | 0(0) | 46(5) | 92(4) | 4(3) | 12(3) | 126(44) | 29(34) | 3(3) | |

| 86(3) | 0(0) | 14(3) | 103(1) | 4(1) | 1(1) | 104(9) | 4(3) | 1(1) | |

Example 2 demonstrates the effect of signal proportion. Set and . The signal proportion changes from to . As shown in Table 2, when increases, FP of remains around . FN of is also fairly robust over the different numbers of signals. BH-FDR and adaptive FDR, on the other hand, increases in both FP and FN with increasing signal proportion.

| S-I Separation | BH-FDR | adapFDR | I-N Separation | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| FP | FN | FP | FN | FP | FN | FP | FN | |||||

| 8(3) | 0(0) | 92(3) | 27(7) | 1(1) | 74(6) | 27(7) | 1(1) | 74(6) | 227(140) | 147(135) | 21(12) | |

| 40(6) | 0(0) | 460(6) | 255(14) | 11(4) | 255(13) | 259(13) | 12(4) | 253(13) | 1119(494) | 645(462) | 31(28) | |

| 81(8.9) | 0(0) | 919(9) | 637(21) | 28(4) | 392(18) | 647(18) | 31(4) | 386(18) | 1960(589) | 996(548) | 38(31) | |

| 172(11) | 0(0) | 1828(10) | 1485(29) | 59(9) | 575(28) | 1543(32) | 72(11) | 529(24) | 3224(660) | 1268(614) | 46(32) | |

Example 3 has heterogenous noise generated for of the observations. With signal intensity and proportion fixed at and , the proportion of heterogeneous noise is 10 times the proportion of signals. This example demonstrates a common scenario in real-data applications where unjustified artifacts causes heterogeneity in the background noise. The heterogeneous noise in this example are randomly generated from with Gamma. Let the scale parameter vary from to , which results in increasing variability for the noise. Due to the small signal proportion, the results of the adaptive FDR are very close to those of the BH-FDR and omitted in this example. Table 3 shows that FPs of all procedures increase with . FNs, on the other hand, are very stable. Theorem 3.3 provides some explanation for the robustness of in controlling false negatives. Since heterogeneous noise can result in large jumps, the estimated proportion is larger than the true . Constructed using this , is essentially the in (19), which is built on an upper bound of the true . The theoretical property on false negative control is presented in (21).

| S-I Separation | BH-FDR | I-N Separation | |||||||

|---|---|---|---|---|---|---|---|---|---|

| FP | FN | FP | FN | FP | FN | ||||

| 22(4) | 5(3) | 82(3) | 69(9) | 15(4) | 45(6) | 196(67) | 107(60) | 12(7) | |

| 53(7) | 35(6) | 81(4) | 132(12) | 71(9) | 38(4) | 443(180) | 347(174) | 7(4) | |

| 94(10) | 75(9) | 80(4) | 195(15) | 130(13) | 35(4) | 556(230) | 459(223) | 7(3) | |

| 134(12) | 113(10) | 80(4) | 249(12) | 182(10) | 33(4) | 556(179) | 466(175) | 9(4) | |

Example 4 generates autocorrelated observations with for and . The number of observations are reduced to 1,000 to save computation time. Set , , , and . The results summarized in Table 4 are quite stable over different values of the autocorrelation parameter with having slightly better control on false negatives for large .

| S-I Separation | BH-FDR | I-N Separation | |||||||

|---|---|---|---|---|---|---|---|---|---|

| FP | FN | FP | FN | FP | FN | ||||

| 14(3) | 0(0) | 36(3) | 27(4) | 1(1) | 25(4) | 74(45) | 30(33) | 7(7) | |

| 13(4) | 0(0) | 37(4) | 24(7) | 1(1) | 27(7) | 69(35) | 27(28) | 7(7) | |

| 13(7) | 0(0) | 37(6) | 28(9) | 1(1) | 24(7) | 67(44) | 25(33) | 5(8) | |

| 14(13) | 0(0) | 36(13) | 29(17) | 0(0) | 20(15) | 72(51) | 27(41) | 3(4) | |

5 Real Application

We apply the three-subset identification to the genotyping data from the Autism Genetics Resource Exchange (AGRE) collection (Bucan et al. 2009) generated by high-throughput single nucleotide polymorphism (SNP) array technology. Genotypes in this data set are measured in Log R ratio (LRR), which is calculated at each SNP location as , where is the observed total intensity of both major and minor alleles and is computed from a reference genome (Peiffer et al. 2006). LRR data are widely used for detecting copy number variants (CNVs), in which the goal is to identify genomic regions with deletion or duplication of DNA segments (Feuk et al. 2006). Such DNA mutations have be reported to play important roles in population diversity and disease association (McCarroll and Altshuler 2007). Due to the fact that the intensity ratio deviates from the baseline in CNV segments, various segment detection methods have been developed to detect CNVs based on SNP array data (Olshen et al. (2004), Zhang et al. (2010), Siegmund et al. (2010), Jeng et al. (2010), Jeng et al. (2012), etc.)

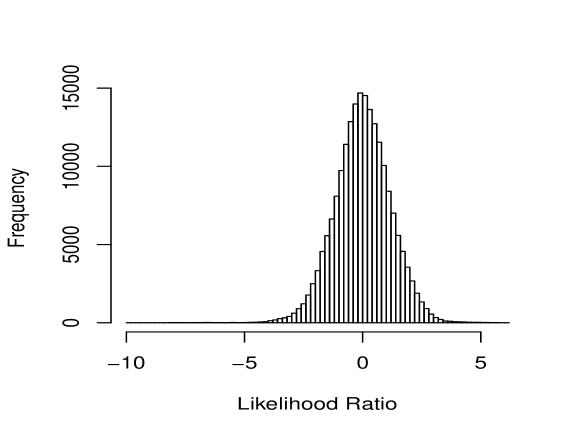

In this paper, instead of just providing a list of candidates for CNVs, we provide more insight of the data by identifying the signal, noise, and indistinguishable subsets. We specifically consider the observations on Chromosome 19 for three individuals, which are collected from 9501 SNPs for each individual. The signals are copy number deletions, which may cause LRR to be negative. For a given individual, LRR observations are first normalized, and then the likelihood ratio is calculated for each interval with length as in Jeng et al. (2010). The likelihood ratio of an interval is defined as the standardized sum of observations in that interval, and is set at 20 as most of the CNVs cover less than 20 SNPs (Zhang et al. 2009). There are such likelihood ratio statistics for each individual. When the distribution of LRR changes in an interval, the corresponding likelihood ratio is expected to deviate from the baseline. Figure 3 demonstrates the distribution of the likelihood ratios for all the intervals with length on Chromosome 19 of one individual. The outliers in the left tail are likely to come from copy number deletions. The plots are similar for other individuals and are, thus, omitted.

We calculate the -values for these likelihood ratios assuming that the background noise follow after normalization. The likelihood ratios are locally dependent due to the fact that the intervals are short and overlapping. In this example we treat them as independent observations to illustrate the method. The separations among signal, indistinguishable, and noise subsets are determined by either (9) and (10) or (18) and (19). We find that estimating the signal proportion by (11) seems to result in a much larger proportion estimate than commonly expected for SNP array data, possibly due to the artifacts involved in the data generation process (Marioni et al. 2007). Thus, we use a more reasonable bound of for this data set. Setting the upper bound at means that the copy number deletions on Chromosome 19 are approximately less than (Zhang et al. 2009). The signal, noise, and indistinguishable subsets are identified by deriving the cut-off points and . Because the intervals are overlapping, we only keep intervals having minimum -values among overlapping segments to indicate the locations of copy number deletions. All the other intervals overlapping with them are removed. and are then re-defined as the ranks among these non-overlapping intervals. For the three individuals, (, ) are (2, 18), (1, 76), and (1, 36), respectively.

We further perform validation on the identified signal, noise, and indistinguishable subsets. The candidates in each subset are compared to the reported members in a CNV database maintained in The Centre for Applied Genomics

(http://projects.tcag.ca/variation/project.html). A candidate region can overlap with zero, one, or more than one CNVs in the database. The mean value of the number of such CNVs in the database is presented for each subset in Table 5. In other words, let number of CNVs in the database that overlap with the -th candidate in the list of ranked intervals. Define

.

Table 5 shows that these mean values, in general, decrease from ovlap-s to ovlap-n. For example, in the identified indistinguishable subset of individual 3, CNVs in the database overlap with each candidate in the identified indistinguishable subset on average, while the number decreases to for the identified noise subset. This agrees with our intuition for the three subsets as larger mean values represents stronger evidence for identifying the true CNVs.

One exception is ovlap-s for individual 3. There is only one candidate in the identified signal subset, which happens to be missed in the database. A possible explanation is that this candidate is a de novo CNV only carried by individual 3.

The sample correlation between the interval length and are , , and for the three individuals, respectively, indicating that the trend observed in Table 5 is not likely caused by the length factor.

| ovlap-s | ovlap-i | ovlap-n | |||

|---|---|---|---|---|---|

| Individual 1 | 10.5 | 2 | 3.4 | 18 | 2.5 |

| Individual 2 | 4 | 1 | 4.7 | 76 | 2.1 |

| Individual 3 | 0 | 1 | 6.8 | 36 | 2.0 |

6 Further Discussion

In this paper, we developed a novel statistical framework and an efficient TLT procedure to categorize the data into the signal, noise, and indistinguishable subsets. This unique categorization can provide further insight for the data and help the practitioners to design more appropriate follow-up studies to identify the true signals in different subsets. Another motivation for the new development is its potential to provide an objective criterion for sample-size determination based on the cardinality of the indistinguishable subset. Unlike traditional sample-size calculation, which is based on a pre-specified level of signal intensity, we may determine whether the sample size is large enough by examining the size of the indistinguishable subset.

Additional insight for the quality of the data may also be achieved by examining the indistinguishable subset. For example, a large indistinguishable subset suggests that there are many small non-null observations, which are either true signals or, very often, caused by artifacts involved during the data generation. Investigating the sources of possible artifacts in follow-up studies may significantly reduce the indistinguishable subset and result in better separation between signals and noise.

We developed two related TLT schemes, one is completely data-driven, the other utilizes prior knowledge on the possible range of the signal proportion. Such flexibility allows practitioners to meet the needs of various applications. The computation for both procedures are very fast.

The study in this paper is based on -values. Other statistics carrying information about signal intensity, such as the local FDR values (Efron (2007), Sun and Cai (2007)) may be used in place of -values. It will be interesting to investigate this possibility in future research.

In this paper, we assumed independent -values to allow a succinct theoretical study of the new method. Simulation examples in section 4 demonstrate the robustness of the proposed method for autocorrelated observations. We plan to study in depth the three-subset categorization under dependence in future works. We find the recent paper by Fan et al. (2012) to be very helpful. According to their work, it is possible to estimate the arbitrary dependence structure of the -values and transform the dependent p-values into weakly dependent ones.

Last but not least, estimating the separation point between the indistinguishable and noise subsets can be related to the problem of variable screening in high-dimensional regression and can provide new insights on the well-known challenge of screening parameter selection in high-dimensional data analysis.

Acknowledgement

We thank Dr. Leonard Stefanski and Dr. John Daye for helpful discussions and comments.

Appendix: Proofs

The proofs for theorems in section 2 and 3 are provided. A preliminary lemma is first introduced to summarize part of the results in Theorem 1 and 2 in Meinshausen and Rice (2006). The proof of the lemma is omitted.

Lemma 6.1

Proof of Theorem 2.1

It is sufficient to show the following claims. For any ,

| (22) |

| (23) |

| (24) |

| (25) |

| (26) |

| (27) |

Consider (22) first.

| (28) | |||||

where the last inequality is by the extreme value theory of standard normal random variables. Also,

| (29) | |||||

where the inequality is by . Combining (28) and (29) gives (22).

Next consider (23).

| (30) | |||||

where the last inequality is by the extreme value theory of standard normal random variables. Also,

| (31) | |||||

where the inequality is by . Combining (30) and (31) gives (23).

Proof of Theorem 3.1

Consider (14) first. Since

where the third inequality is by Lemma 6.1 and the fact that -values from noise are uniformly distributed. Then (14) follows.

Next, consider (15). Define . Recall that , then

| (32) | |||||

where the first equality is by , the second equality is by , and the last step is by Lemma 6.1.

In the case of , define as the -th smallest -value from noise. Then

| (34) | |||||

where the first inequality is because when the elements from are more than in , the th smallest -value from must rank before the -value at . The second inequality is by the well-known fact that and the construction of , where

. The last step is by the definition of and Lemma 6.1. Combining (32) and (34) gives (15).

Proof of Theorem 3.2

Defines events , , and . By the construction of in (9), it is enough to show that

which is implied by

| (35) |

Consider first.

where the second inequality is by the construction of in (9) and Lemma 6.1, the fourth inequality is by when and , and the last step is by the condition .

For , it is easy to show that by similar arguments leading to (14).

Now consider . By lemma 6.1, it is enough to show that

which is implied by

| (36) |

Define

Then, by the construction of in (11), for any ,

Let . Then by condition and ,

Therefore, (36) follows. Combining the above results for , , and gives (35).

Proof of Theorem 3.2

The proof of this theorem is similar to that of Theorem 3.1 and is, thus, omitted to save space.

References

- Abramovich et al. (2006) Abramovich, F., Benjamini, Y., Donoho, D., and Johnstone, I. (2006), “Adapting to Unknown Sparsity by Controlling the False Discovery Rate,” Ann. Statist., 34, 584–653.

- Benjamini and Hochberg (1995) Benjamini, Y. and Hochberg, Y. (1995), “Controlling the False Discovery Rate: a practical and powerful approach to multiple testing,” J. Royal Stat. Soc. B, 57, 289–300.

- Benjamini and Hochberg (2000) — (2000), “On the Adaptive Control of the False Discovery Rate in Multiple Testing with Independent Statistics,” J. of Educational and Behavioral Statistics, 25, 60–83.

- Bucan et al. (2009) Bucan, M., Abrahams, B., Wang, K., Glessner, J., Herman, E., Sonnenblick, L., Retuerto, A. A., Imielinski, M., Hadley, D., Bradfield, J., Kim, C., Gidaya, N., Lindquist, I., Hutman, T., , Sigman, M., Kustanovich, V., Lajonchere, C., Singleton, A., Kim, J., , Wassink, T., McMahon, W., Owley, T., Sweeney, J., Coon, H., Nurnberger, J., Li, M., Cantor, R., Minshew, N., Sutcliffe, J., Cook, E., Dawson, G., Buxbaum, J., Grant, S., Schellenberg, G., Geschwind, D., and Hakonarson, H. (2009), “Structural variation in the human genome,” PLoS Genetics, 5.

- Cai et al. (2007) Cai, T., Jin, J., and Low, M. (2007), “Estimation and Confidence Sets For Sparse Normal Mixtures,” Ann. Statist., 35, 2421–2449.

- Conneely and Boehnke (2010) Conneely, K. N. and Boehnke, M. (2010), “META-ANALYSIS OF GENETIC ASSOCIATION STUDIES AND ADJUSTMENT FOR MULTIPLE TESTING OF CORRELATED SNPS AND TRAITS,” Genetic Epidemiology, 34(7).

- Donoho and Jin (2004) Donoho, D. and Jin, J. (2004), “Higher criticism for detecting sparse heterogeneous mixtures,” Ann. Statist., 32, 962–994.

- Drton and Perlman (2008) Drton, M. and Perlman, M. D. (2008), “A SINful approach to Gaussian graphical model selection,” Journal of Statistical Planning and Inference, 138(4).

- Dudoit et al. (2003) Dudoit, S., Shaffer, J. P., and Boldrick, J. C. (2003), “Multiple Hypothesis Testing in Microarray Experiments,” Statist. Sci., 18(1), 71–103.

- Dudoit et al. (2004) Dudoit, S., van der Laan, M., and Pollard, K. S. (2004), “Multiple Testing. Part I. Single-Step Procedures for Control of General Type I Error Rates,” Statistical Applications in Genetics and Molecular Biology., 3, article 13.

- Efron (2007) Efron, B. (2007), “Size, Power AND False Discovery Rates,” The Annals of Statistics, 35, 1351–1377.

- Fan et al. (2011) Fan, J., Feng, Y., and Song, R. (2011), “Nonparametric independence screening in sparse ultra-high dimensional additive models,” J. of American Statistical Association, 116, 544–557.

- Fan et al. (2012) Fan, J., Han, X., and Gu, W. (2012), “Control of the false discovery rate under arbitrary covariance dependence,” J. of American Statistical Association, 107, 1019–1045.

- Fan and Lv (2008) Fan, J. and Lv, J. (2008), “Sure Independence Screening for Ultra-High Dimensional Feature Space,” J. R. Statist. Soc. B, 70, 849–911.

- Fan et al. (2009) Fan, J., Samworth, R., and Wu, Y. (2009), “Ultra-Dimensional Variable Selection via Independent Learning: Beyond the Linear Model,” J. of Machine Learning Research, 10, 1829–1853.

- Feuk et al. (2006) Feuk, L., Carson, A., and Scherer, S. (2006), “Structural variation in the human genome,” Nature Review Genetics, 7.

- Genovese and Wasserman (2004) Genovese, C. and Wasserman, L. (2004), “A stochastic process approach to false discovery control,” Ann. Statist, 32, 1035–1061.

- Hall and Miller (2009) Hall, P. and Miller, H. (2009), “Using Generalized Correlation to Effect Variable Selection in Very High Dimensional Problems,” J. of Computational and Graphical Statistics, 18, 533 550.

- Jeng et al. (2010) Jeng, X. J., Cai, T. T., and Li, H. (2010), “Optimal sparse segment identification with application in copy number variation analysis,” J. Am. Statist. Ass., 105, 1156–1166.

- Jeng et al. (2012) — (2012), “Simultaneous Discovery of Rare and Common Segment Variants,” Biometrika, To appear.

- Ji and Jin (2012) Ji, P. and Jin, J. (2012), “UPS delivers optimal phase diagram in high-dimensional variable selection,” Ann. Statist., 40, 73–103.

- Jin (2008) Jin, J. (2008), “Proportion of nonzero normal means: oracle equivalence and uniformly consistent estimators,” J. of the Royal Statistical Society, Series B, 70, 461–493.

- Jin and Cai (2007) Jin, J. and Cai, T. (2007), “Estimating the null and the proportion of non-null effects in large-scale multiple comparisons,” J. American Statistical Association, 102, 495–506.

- Li et al. (2012) Li, R., Zhong, W., and Zhu, L. (2012), “Feature screening via distance correlation learning,” J. of American Statistical Association, In press.

- Marioni et al. (2007) Marioni, J. C., Thorne, N. P., Valsesia, A., Fitzgerald, T., Redon, R., Fiegler, H., Andrews, T. D., Stranger, B. E., Lynch, A. G., Dermitzakis, E. T., Carter, N. P., Tavar , S., and Hurles, M. E. (2007), “Breaking the waves: improved detection of copy number variation from microarray-based comparative genomic hybridization,” Genome Biology, 8(10).

- McCarroll and Altshuler (2007) McCarroll, S. S. and Altshuler, D. M. (2007), “Copy-number variation and association studies of human disease,” Nature Genetics, 39.

- Meinshausen and Rice (2006) Meinshausen, M. and Rice, J. (2006), “Estimating the proportion of false null hypotheses among a large number of independent tested hypotheses,” Ann. Statist., 34, 373–393.

- Olshen et al. (2004) Olshen, A. B., Venkatraman, E. S., Lucito, R., and Wigler, M. (2004), “Circular binary segmentation for the analysis of array-based DNA copy number data,” Biostatistics, 5 (4).

- Peiffer et al. (2006) Peiffer, D. A., Le, J. M., Steemers, F. J., Chang, W., Jenniges, T., Garcia, F., Haden, K., Li, J., Shaw, C. A., Belmont, J., Cheung, S. W., Shen, R. M., Barker, D. L., and Gunderson, K. L. (2006), “High-resolution genomic profiling of chromosomal aberrations using Infinium whole-genome genotyping,” Genome Res, 16.

- Siegmund et al. (2010) Siegmund, D. O., Yakir, B., and Zhang, N. R. (2010), “Detecting simultaneous variant intervals in aligned sequences,” Annals of Applied Statistics, 5, 645–668.

- Spencer et al. (2009) Spencer, C., Su, Z., Donnelly, P., and Marchini, J. (2009), “Designing genome-wide association studies: sample size, power, imputation, and the choice of genotyping chip,” PLoS Genetics, 5(5).

- Storey et al. (2004) Storey, J. D., Taylor, J. E., and Siegmund, D. (2004), “Strong control, conservative point estimation and simultaneous conservative consistency of false discovery rates: a unified approach,” J. of the Royal Statistical Society: Series B, 66, 187–205.

- Sun and Cai (2007) Sun, W. and Cai, T. (2007), “Oracle and Adaptive Compound Decision Rules for False Discovery Rate Control,” J. American Statistical Association, 102, 901–912.

- Suresh and Chandrashekara (2012) Suresh, K. and Chandrashekara, S. (2012), “Sample size estimation and power analysis for clinical research studies,” Journal of Human Reproductive Sciences, 5(1).

- Xie et al. (2011) Xie, J., Cai, T., and Li, H. (2011), “Sample size and power analysis for sparse signal recovery in genome-wide association studies,” Biometrika, 98, 273–290.

- Zhang et al. (2009) Zhang, F., Gu, W., Hurles, M., and Lupski, J. (2009), “Copy number variation in human health, disease and evolutions,” Annual Review of Genomics and Human Genetics, 10, 451–481.

- Zhang et al. (2010) Zhang, N. R., Siegmund, D. O., Ji, H., and Li, J. (2010), “Detecting Simultaneous Change-points in Multiple Sequences,” Biometrika, 97, 631–645.

- Zhu et al. (2011) Zhu, L., Li, L., Li, R., and Zhu, L.-X. (2011), “Model-free feature screening for ultrahigh dimensional data,” J. of American Statistical Association, 106, 1464–1475.