Convex risk minimization via proximal splitting methods

Abstract. In this paper we investigate the applicability of a recently introduced primal-dual splitting method in the context of solving portfolio optimization problems which assume the minimization of risk measures associated to different convex utility functions. We show that, due to the splitting characteristic of the used primal-dual method, the main effort in implementing it constitutes in the calculation of the proximal points of the utility functions, which assume explicit expressions in a number of cases. When quantifying risk via the meanwhile classical Conditional Value-at-Risk, an alternative approach relying on the use of its dual representation is presented as well. The theoretical results are finally illustrated via some numerical experiments on real and synthetic data sets.

Keywords. portfolio optimization, convex risk measure, utility function, primal-dual proximal splitting algorithm

AMS subject classification. 90C25, 90C46, 47A52

1 Introduction and preliminaries

In financial mathematics, quantifying the risk of future random outcomes is an essential concern for decision makers who, of course, have their own attitude towards risk. In the classical portfolio theory by Markowitz, the variance was used to measure the risk of future returns. However, subsequent developments in the theory of risk measures showed that the variance does not have desirable properties, one major drawback being given by the fact that it measures deviations of the random variable in both directions, i. e. it penalizes losses and gains in the same way.

When dealing with uncertainty, modern risk measures build on the wide-spread recognition that asymmetry is a desirable property since investors have different positions on downside and upside outcomes. The first axiomatic way of defining risk measures has been given by Artzner, Delbaen, Eber and Heath in [1] and refers to coherent risk measures. Nevertheless, it has become a standard in modern risk management to assess the riskiness of a portfolio by means of convex risk measures, introduced by Föllmer and Schied in [17], as well as of convex deviation measures, introduced by Rockafellar, Uryasev and Zabarankin in [23]. The convex deviation measures are connected with the risk measures when those are applied to the difference between a random variable and its expectation, instead of to the random variable itself, both being designed to be used in risk analysis. However, deviation measures evaluate uncertainty in the form of nonconstancy, whereas risk measures can be understood as estimates of capital requirements for future net worths.

In this paper we give a unifying framework for solving portfolio optimization problems assuming the minimization of a general convex risk functional subject to constraints on the expected return of the portfolio and on the budget. The convex risk measure in the objective is expressed in terms of the Optimized Certainty Equivalent (OCE), a fundamental concept for quantifying risk by means of a utility function introduced by Ben-Tal and Teboulle in [3] (see also [4]). For the particular case of the Conditional Value-at-Risk an alternative approach involving its dual representation is also considered. The approach we propose in this paper assumes the solving of these constrained optimization problems, which in their majority have an nondifferentiable objective function with an intricate formulation, via a primal-dual proximal splitting method which has been recently introduced in [10]. In the last years one can notice an increasing interest in primal-dual algorithms when solving nondifferentiale convex optimization problems (see, for instance, [6, 9, 10, 11, 12, 13, 14, 25]), as they achieve a full splitting which assumes a separate evaluation of each function via its proximal points, while the occurring linear continuous operators and their adjoints are only evaluated via forward steps. Most primal-dual algorithms also allow inexact evaluations of the proximal points which, however, can have a negative impact on the overall performance. On the other hand, in a lot of applications, as it will be also the case for majority of the convex risk measures considered in this paper, exact implementations of the proximal operators are possible. We refer to the mentioned literature for applications of the primal-dual methods in image and signal processing, location theory and machine learning.

The structure of the paper is the following. In the remaining of this subsection we give some elements of convex analysis, present the primal-dual proximal algorithm along with its convergence behaviour and introduce the necessary apparatus for defining convex risk measures. Section 2 is dedicated to the formulation of the portfolio optimization problem to be solved, when the risk is quantified via the Optimized Certainty Equivalent, and to investigations on the applicability of the primal-dual method in this context. In Section 3 an alternative approach for solving the portfolio optimization problem having as objective the Conditional Value-at-Risk is presented. We illustrate the applicability of the proposed primal-dual method in the context of portfolio optimization problems in Section 4 by some numerical experiments on real and synthetic data.

1.1 Convex analysis

Let be a real Hilbert space with inner product and associated norm . The symbol denotes the set of strictly positive real numbers and . For a given set , the function , defined by for and , otherwise, denotes its indicator function. For a function we denote by its effective domain and call proper if and for all . Let be

The conjugate function of is , for all and, if , then , as well. The (convex) subdifferential of at is the set , if , and is taken to be the empty set, otherwise. For a linear continuous operator , the operator , defined via for all and all , denotes its adjoint.

Having two proper functions , their infimal convolution is defined by , for all , being a convex function when and are convex. The parallel sum of the subdifferentials of and , seen as set-valued operators, is defined as , , where . One has that for every . For , its subdifferential is a maximally monotone operator (cf. [19]) and by we denote the proximal point of at , representing the unique optimal solution of the optimization problem

| (1.1) |

For every we have Moreau’s decomposition formula (cf. [2, Theorem 14.3])

| (1.2) |

where Id denotes the identity operator on . When is a nonempty convex and closed set, the proximal point of at is

being nothing else than the projection of on .

For and , , given real Hilbert spaces, , , , and , nonzero linear continuous operators we consider the convex optimization problem

and its Fenchel-type conjugate dual problem (see, for instance, [5, 10, 13])

By denoting with and the optimal objective values of the problems and , respectively, in general one has weak duality, i.e., . Strong duality, which is the situation when and the dual problem has an optimal solution, holds, when some appropriate qualification condition is fulfilled. The following error-tolerant proximal splitting algorithm which is suitable for simultaneously solving the problems and was given in [10, Algorithm 3.1]. Its competitiveness is emphasized by several numerical experiments in the context of location and image processing problems, also in comparison to other recently introduced iterative schemes.

Algorithm 1.1.

Let , and and , be strictly positive real numbers such that

Furthermore, let be a sequence in , a sequence in , and sequences in for all and set

| (1.17) |

Remark 1.1.

When , the infimal convolution is nothing else than the function . In this situation, the conjugate of is the function identical to zero and for all one has .

The subsequent theorem was given in [10, Theorem 3.1] and characterizes the convergence behaviour of the sequences generated by Algorithm 1.1.

Theorem 1.1.

Suppose that there exists such that

| (1.18) |

-

(i)

If

and then

-

(a)

converges weakly to a point such that, when setting

is an optimal solution to the primal problem , is an optimal solution to the dual problem and .

-

(b)

and for .

-

(c)

whenever and are finite-dimensional Hilbert spaces, and for , then converges strongly to an optimal solution to and converges strongly to an optimal solution to .

-

(a)

-

(ii)

If

then converges strongly to an optimal solution to the primal problem , converges strongly to an optimal solution to the dual problem and .

1.2 Convex risk measures

Let be an atomless probability space, where the elements of represent future states, or individual scenarios (and are allowed to be only finitely many), is a -algebra on measurable subsets of and is a probability measure on . For a measurable random variable the expectation value with respect to is defined by . Whenever takes the value on a subset of positive measure we have . Equalities between random variables are to be interpreted in an almost surely (a.s.) way. Random variables which take a constant value i.e a.s., will be identified with the real number . Similarly, inequalities of the form , , , etc., are to be viewed in the sense of holding almost surely. By we denote the distribution function of , i. e. . By taking this into account, essential supremum and essential infimum of a random variable are, respectively,

Each random variable can be represented as , where are random variables defined via and for all .

Consider further the real Hilbert space

endowed with inner product and norm defined for arbitrary via

respectively.

Definition 1.1 (Risk functions).

A proper function is called risk function. The risk function is said to be

-

(i)

convex, if for all , ;

-

(ii)

positively homogeneous, if and for all , ;

-

(iii)

monotone, if implies for all ;

-

(iv)

cash-invariant, if for all , ;

-

(v)

a convex risk measure, if is convex, monotone and cash-invariant;

-

(vi)

a coherent risk measure, if is a positively homogeneous convex risk measure.

Axioms for coherent risk measures were first given in the literature by Artzner, Delbaen, Eber and Heath in [1], while later one, Föllmer and Schied considered in [17] the convex risk measures, by replacing the sublinearity with the weaker assumption of convexity. More precisely, when the value is understood as a capital requirement for the future net worth , a convex risk measure guarantees that the capital requirement of the convex combination of two positions does not exceed the convex combination of the capital requirements of the positions taken separately. For properties and examples of coherent and convex risk measures we refer to [1, 4, 7, 15, 16, 18, 20, 21, 22, 23].

In our investigations a central role will be played by a generalized convex risk measure associated to the so-called Optimized Certainty Equivalent, which was introduced for concave utility functions in [3] and adapted to convex utility functions in [7]. For the utility functions considered throughout this paper we make the following assumption.

Assumption 1.1 (Convex utility function).

Let be a proper, convex, lower semicontinuous and nonincreasing function such that and .

In the literature the two conditions imposed on are known as the normalization conditions and are equivalent to and for all . The generalized convex risk measure we use in order to quantify the risk was given under the name Optimized Certainty Equivalent (OCE) in [4] and is defined as (see, also, [7])

| (1.19) |

By Assumption 1.1, it follows that for every and that fulfills the requirements of being a convex risk measure.

2 Solving a general portfolio optimization problem

Consider a portfolio with a number of different positions with returns , , a nonzero vector of expected returns and a given lower bound for the expected return of the portfolio. In this section we discuss the employment of Algorithm 1.1 when solving for different convex utility functions the optimization problem

| (2.1) |

which assumes the minimization of the risk of the portfolio subject to constraints on the expected return of the portfolio and on the budget. Here, denotes the vector in having all entries equal to . By using (1.19), we obtain the following reformulation of the problem (2.1)

| (2.2) |

which will prove to be more suitable for being solved by means of the primal-dual proximal splitting algorithm presented in the previous section. In this sense, the following result, which relates the optimal solutions of the two optimization problems is of certain importance.

Proposition 2.1.

Proof.

Remark 2.1.

A sufficient condition guaranteeing that

was given in [7, Theorem 4] and reads

| (2.3) |

where , , denotes the recession function of the function . Moreover, in the light of the same result, it follows that under (2.3)

thus is lower semicontinuous. Since is compact, this further implies that (2.1) has an optimal solution and, consequently, that (2.2) has an optimal solution, too. All particular convex utility functions we deal with in this paper fulfill condition (2.3).

According to Proposition 2.1, determining an optimal solution to problem (2.2) will lead to an optimal solution to the portfolio optimization problem (2.1). However, as we will show in the following, problem (2.2) is a particular case of the problem , thus it can be solved by Algorithm 1.1, but also by some other primal-dual proximal splitting methods. In order to show this, let us first consider the linear (hence continuous) operator

In order to determine its adjoint operator we use that

for all and all and get

Further, by considering the convex and closed sets

the optimization problem (2.2) can be equivalently written as

| (2.4) |

It is obvious that the functions , and are proper, convex and lower semicontinuous. Furthermore, in the light of Assumption 1.1 and by using Fatou’ lemma, it follows that has these properties, as well. This means that problem (2.4) fits into the formulation of the problem .

Remark 2.2.

By having a closer look into the formulation of Algorithm 1.1, one can notice the exposed role played by the proximal points of the functions occurring in the objective of the problem to be solved. Having these determined, one can easily obtain via (1.2) the proximal points of their conjugates, when needed. It is an easy calculation to see that for and it holds

with

where (see, for instance, [2, Example 28.16 and Example 3.21]),

As we show below, in order to determine the proximal points of one needs more intricate arguments.

Proposition 2.2.

For arbitrary random variables and it holds

| (2.5) |

Proof.

We have

Hence, using the interchangeability of integration and minimization (see [24, Theorem 14.60]), we have

∎

In what follows we provide explicit formulae for the proximal points of some popular convex utility functions considered the literature, which will be of importance for the numerical experiments presented in the last section and which involve the convex risk measures which rely on them.

2.1 Piecewise linear utility

For we consider the piecewise linear utility function

Assumption 1.1 is fulfilled since and and, since for all (see [7])

condition (2.3) is fulfilled, as well. Hence, gives rise to the lower semicontinuous coherent risk measure

| (2.6) |

For every and it holds

When setting and for some , the convex risk measure (2.6) becomes the classical so-called Conditional Value-at-Risk at level (see, for example, [20, 21])

| (2.7) |

The infimum in the in the expression of the Conditional Value-at-Risk is attained for every at the so-called Value-at-Risk at level , i.e.,

2.2 Exponential utility function

Consider the exponential utility function , . It fulfills Assumption 1.1 and, since , condition (2.3) is fulfilled, as well. It gives rise via (1.19) to the so-called entropic risk measure

| (2.8) |

which is a lower semicontinuous convex risk measure. For arbitrary and it holds

Although no closed form expression for the proximal points of can be given, these can be efficiently calculated by applying Newton’s method under the use of previous iterates as starting points.

2.3 Indicator utility function

2.4 Quadratic utility function

2.5 Logarithmic utility function

For , we consider the logarithmic utility function

For this special utility function, one can also show that , hence that (2.3) is fulfilled. The properties in Assumption 1.1 hold as well and therefore, via (1.19), we obtain the convex risk measure

The proximal points of the logarithmic utility function take an explicit expression. For arbitrary and , it holds

3 An alternative approach for CVaR

In this section we propose an alternative approach for solving the portfolio optimization problem (2.1) when the risk measure in the objective is the Conditional Value-at-Risk at a given confidence level . To this aim we work in a discrete probability space with finite, which is the natural framework in real-life applications. We denote by the cardinal of the set . Thus, the probability measure can be represented as a vector with , and and the space of random variables can be identified with the finite-dimensional space . The investigations made in this section rely on the following dual representation of the Conditional Value-at-Risk given in [18, 22], namely, for every it holds

| (3.1) |

where

| (3.2) |

By introducing the convex and closed sets

we obtain , hence, for every it holds

| (3.3) |

where the last equality follows from [2, Theorem 15.3 & Proposition 15.5] and the fact that the intersection of the relative interiors of the sets and is nonempty.

Thus, for given the portfolio optimization problem

| (3.4) |

can be equivalently written as

| (3.5) |

where and are the sets already introduced in the previous section and is defined as .

One can easily notice that the optimization problem (3.4) fits in the formulation of the general convex optimization problem , all the extended real-valued functions present in its objective being proper, convex and lower semicontinuous, and thus it can be solved by means of Algorithm 1.1. We would also like to point out that the primal-dual splitting algorithms proposed in [13, 25] are also designed to solve convex optimization problems involving infimal convolutions, however, they cannot be applied in this situation. This is because they require that one of the two functions occurring in the infimal convolution are strongly convex, which is for the problem (3.5) not the case. For the implementation of Algorithm 1.1 one has only to determine the projections on some simple convex and closed sets, for which one actually has explicit expressions. We would also like to emphasize that, from this point of view, it is p referable to work with the sets and separately, instead of dealing with their intersection .

Remark 3.1.

The approach described above can be analogously employed when considering portfolio optimization problems having as objective a weighted sum of Conditional Value-at-Risk functionals taken at different levels of confidence.

4 Numerical experiments

4.1 Simulated data

The first numerical experiments we made followed the scope to compare different approaches for solving the portfolio optimization problem which assumes the quantification of risk by means of the Conditional Value-at-Risk. More precisely, we compared the performances of Algorithm 1.1 when applied in the context of the approaches proposed in the sections 2 and 3, but also with the linear programming approach, widely used in this context in the literature. To this end we used synthetic data obtained by creating random returns , where represents the number of assets in the portfolio.

We first solved with the Matlab routine linprog the reformulation of (3.4) as a linear program, that can be easily obtained by means of (2.7). Then we used the primal-dual method given in Algorithm 1.1 to solve (3.4) via two different approaches, namely, on the one hand, by solving the reformulation (2.4) proposed in Section 2 and, on the other hand, by solving the reformulation (3.5) given in Section 3 and relying on the dual representation of the objective. We terminated the algorithms when subsequent iterates start to stay within an accuracy level of with respect to the set of constraints and to the optimal objective value reported by the linear programming solver. Within these examples we used the confidence level . The algorithms were implemented in Matlab on an Intel Core i- processor under Windows 7 (64 Bit).

| LP (linprog) | OCE (iterations) | DR (iterations) | ||

|---|---|---|---|---|

| s | s() | s() | ||

| s | s() | s() | ||

| s | s() | s() | ||

| s | s() | s() | ||

| s | s() | s() | ||

| s | s() | s() |

The computational results presented in Table 4.1 show that both approaches proposed in this paper outperformed to linear programming approach from the point of view of the time needed to determine an optimal portfolio for different choices of and . When running Algorithm 1.1 we used the following parameters:

-

•

OCE: , , , , ;

-

•

DR (): , , , , ;

-

•

DR (): , , , , .

4.2 Real data

For the experiments described as follows we took weekly opening courses over the last 13 years from assets belonging to the indices DAX and NASDAQ in order to obtain the returns , for and . The data was provided by the Yahoo finance database. Assets which do not support the required historical information like Volkswagen AG (DAX) or Netflix, Inc. (NASDAQ) were not taken into consideration.

We solved the portfolio optimization problem (2.1) by taking as objective function the corresponding convex risk measures induced by the linear, exponential, indicator, quadratic and logarithmic utility function. More precisely, we solved with Algorithm 1.1 its equivalent reformulation (2.1) and used to this end the formulae for the proximal points of each utility function given in Section 2. The values of the expected returns associated with ranged from (Commerzbank AG, DAX) to (priceline.com Incorporated, NASDAQ).

Table 4.2 collects some computational results when computing by using Algorithm 1.1 optimal solutions for the five utility functions. The stopping criterion was the same as in Section 4.1. Table 4.2 shows that Algorithm 1.1 in combination with the worst-case risk measure, i.e., the one induced by the indicator utility function, performed poorly on the given dataset. It also shows that the algorithm is sensitive with respect to the lower bound of the expected return . When calculating the proximal points of the exponential utility function we used five iterations of Newton’s method with previous iterates as starting points to obtain an appropriate approximation.

| linear () | exponential | indicator | quadr. () | log. () | |

|---|---|---|---|---|---|

| s() | s() | - () | s() | s() | |

| s() | s() | - () | s() | s() | |

| s() | s() | - () | s() | s() | |

| s() | s() | - () | s() | s() | |

| s() | s() | - () | s() | s() | |

| s() | s() | - () | s() | s() |

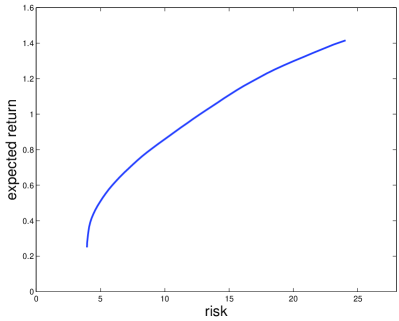

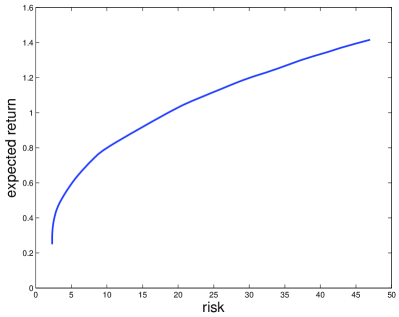

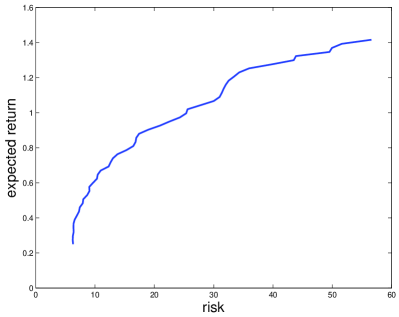

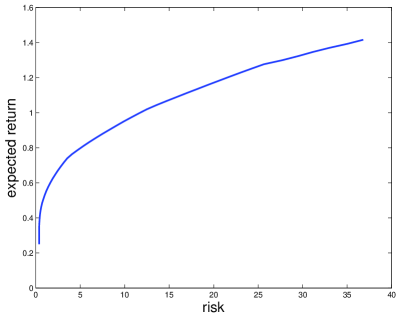

Figure 4.1 shows the efficient frontiers for problem (2.1). When using the indicator utility function we stopped the algorithm after a number of iterations. The objective value, however, still oscillated in this scenario.

References

- [1] P. Artzner, F. Delbaen, J.M. Eber and D. Heath. Coherent measures of risk. Math. Finance 9(3), 203–228, 1999.

- [2] H.H. Bauschke and P.L. Combettes. Convex Analysis and Monotone Operator Theory in Hilbert Spaces. CMS Books in Mathematics, Springer, New York, 2011.

- [3] A. Ben-Tal and M. Teboulle. Expected utility, penalty functions and duality in stochastic nonlinear programming. Manag. Sci. 32(11), 1445–1466, 1986.

- [4] A. Ben-Tal and M. Teboulle. An old-new concept of risk measures: the optimized certainty equivalent. Math. Finance 17(3), 449–476, 2007.

- [5] R.I. Boţ. Conjugate Duality in Convex Optimization. Lecture Notes in Economics and Mathematical Systems, Vol. 637, Springer, Berlin, 2010.

- [6] R.I. Boţ, E.R. Csetnek and A. Heinrich. A primal-dual splitting algorithm for finding zeros of sums of maximally monotone operators. arXiv:1206.5953v1 [math.OC], 2012.

- [7] R.I. Boţ and A.R. Frătean. Looking for appropriate qualification conditions for subdifferential formulae and dual representations for convex risk measures. Math. Meth. Oper. Res. 74(2), 191–215, 2011.

- [8] R.I. Boţ, S.M. Grad and G. Wanka. Duality in Vector Optimization. Springer, Berlin, 2009.

- [9] R.I. Boţ and C. Hendrich. Convergence analysis for a primal-dual monotone + skew splitting algorithm with applications to total variation minimization. arXiv:1211.1706v1 [math.OC], 2012.

- [10] R.I. Boţ and C. Hendrich. A Douglas-Rachford type primal-dual method for solving inclusions with mixtures of composite and parallel-sum type monotone operators. arXiv:1212.0326 [math.OC], 2012.

- [11] L.M. Briceño-Arias and P.L. Combettes. A monotone + skew splitting model for composite monotone inclusions in duality. SIAM J. Optim. 21(4), 1230–1250, 2011.

- [12] A. Chambolle and T. Pock. A first-order primal-dual algorithm for convex problems with applications to imaging. J. Math. Imaging Vis. 40(1), 120–145, 2011.

- [13] P.L. Combettes and J.-C. Pesquet. Primal-dual splitting algorithm for solving inclusions with mixtures of composite, Lipschitzian, and parallel-sum type monotone operators. Set-Valued Var. Anal. 20(2), 307–330, 2012.

- [14] L. Condat. A primal-dual splitting method for convex optimization involving Lipschitzian, proximable and linear composite terms. J. Optim. Theory Appl. 2012. http://dx.doi.org/10.1007/s10957-012-0245-9

- [15] H. Föllmer and A. Schied. Convex measures of risk and trading constraints. Finance Stochast. 6(4), 429–447, 2002.

- [16] H. Föllmer and A. Schied. Robust representation of convex measures of risk. In: K. Sandmann and P. Schönbucher (eds.), Advances in Finance and Stochastics, pp. 39–56, Springer, Berlin, 2002.

- [17] H. Föllmer and A. Schied. Stochastic Finance. A Introduction in Discrete Time. Walter de Gruyter, Berlin, 2002.

- [18] H. Lüthi and J. Doege. Convex risk measures for portfolio optimization and concepts of flexibility. Math. Program. 104(2–3), 541–559, 2005.

- [19] R.T. Rockafellar. On the maximal monotonicity of subdiferential mappings. Pacific Journal of Mathematics 33(1), 209–216, 1970.

- [20] R.T. Rockafellar and S. Uryasev. Optimization of conditional value-at-risk. J. Risk 2(3), 21–42, 2000.

- [21] R.T. Rockafellar and S. Uryasev. Conditional value-at-risk for general loss distributions. J. Bank Finance 26(7), 1443–1471, 2002.

- [22] R.T. Rockafellar, S. Uryasev and M. Zabarankin. Deviation measures in risk analysis and optimization. Report 2002-7, ISE Dept., Univ. of Florida, 2002.

- [23] R.T. Rockafellar, S. Uryasev and M. Zabarankin. Generalized deviations in risk analysis. Finance Stoch. 10(1), 51–74, 2006.

- [24] R.T. Rockafellar and R.J.B. Wets. Variational Analysis. Springer, Berlin, 1998.

- [25] B.C. Vũ. A splitting algorithm for dual monotone inclusions involving cocoercive operators. Adv. Comp. Math. 38(3), 667–681, 2013.