Nonlinear Hawkes Processes

by

Lingjiong Zhu

A dissertation submitted in partial fulfillment

of the requirements for the degree of

Doctor of Philosophy

Department of Mathematics

New York University

May 2013

Professor S. R. S. Varadhan

© Lingjiong Zhu

All Rights Reserved, 2013

Dedication

To the memory of my grandpa

Zhixuan Zhu (1923-2001)

Acknowledgements

It is difficult to overstate my gratitude to my adviser Professor Varadhan. Working with Professor Varadhan has been an absolutely amazing experience for me. I thank him for always keeping his door open and patiently answering my questions. I thank him for his superb guidance, understanding, and generosity. I thank him for suggesting the topic for my thesis, which would not be possible without his deep wisdom and sharing of many new ideas. He has been everything that one can reasonably ask for in an advisor and more, and I am truly grateful to him.

I want to thank the Courant community for guiding me through this process and for putting up with me in general. Tamar Arnon does her job exceptionally well and her efforts are much appreciated. I want to thank the faculty for many well taught and interesting classes. I am indebted to Gérard Ben Arous, Sourav Chatterjee and Raghu Varadhan for writing me recommendations for my first academic job. I also want to thank Peter Carr for his interest in my thesis.

I remember a joke told by Jalal Shatah that the most important thing as an undergraduate student is to go to a top graduate program. But once you are already at a graduate school, the most important thing is to get out of it! This would not be possible without the final step, i.e. thesis defense! I am grateful to have Henry McKean, Chuck Newman and Raghu Varadhan as the three readers and Gérard Ben Arous and Lai-Sang Young as the two non-readers on my thesis committee.

Most importantly, I want to thank my fellow colleagues for all the fun memories that I take with me from Courant. New York City, without good friends, can be the most populated lonely place in the world, but thankfully the constant friendship of my fellow Courant colleagues has made these five years some of the most entertaining and pleasurable of my life. I thank Antoine Cerfon, Shirshendu Chatterjee, Oliver Conway, Sînziana Datcu, Partha Dey, Thomas Fai, Max Fathi, Mert Gürbüzbalaban, Matan Harel, Miranda Holmes-Cerfon, Arjun Krishnan, Shoshana Leffler, Sandra May, Jim Portegies, Alex Rozinov, Patrick Stewart, Adam Stinchcombe, Jordan Thomas, Chen-Hung Wu and many others for their friendship. In particular, I want to thank Dmytro Karabash, Behzad Mehrdad and Sanchayan Sen. They are not only my good friends, but coauthors as well. I also thank my office neighbor Cheryl Sylivant for her friendship.

By living in New York City, I had the great opportunities to visit as many museums and go to as many concerts as possible. I am grateful to the New York Philharmonic and Metropolitan Opera House for their student ticket offers and also many wonderful student recitals and concerts at Juilliard School, which have made my stay in New York City much more enjoyable.

I also want to thank the professors at the University of Cambridge, who provided me a solid undergraduate education. In particular, I am grateful to Rachel Camina, as well as Houshang Ardavan and Tom Körner. I also want to thank Stefano Luzzatto for supervising me on an undergraduate research project at Imperial College, London.

I am very much indebted to my family back home. I thank my parents for so many years of love and understanding. They are truly the best parents one could ask for. I also thank my grandmas, uncles and aunts for their support. Finally, I dedicate this thesis to the memory of my late grandpa. I miss him dearly.

Abstract

The Hawkes process is a simple point process that has long memory, clustering effect, self-exciting property and is in general non-Markovian. The future evolution of a self-exciting point process is influenced by the timing of the past events. There are applications in finance, neuroscience, genome analysis, seismology, sociology, criminology and many other fields. We first survey the known results about the theory and applications of both linear and nonlinear Hawkes processes. Then, we obtain the central limit theorem and process-level, i.e. level-3 large deviations for nonlinear Hawkes processes. The level-1 large deviation principle holds as a result of the contraction principle. We also provide an alternative variational formula for the rate function of the level-1 large deviations in the Markovian case. Next, we drop the usual assumptions on the nonlinear Hawkes process and categorize it into different regimes, i.e. sublinear, sub-critical, critical, super-critical and explosive regimes. We show the different time asymptotics in different regimes and obtain other properties as well. Finally, we study the limit theorems of linear Hawkes processes with random marks.

Introduction

This thesis is about the nonlinear Hawkes process, a simple point processes, that has long memory, the clustering effect, the self-exciting property and is in general non-Markovian. The future evolution of a self-exciting point process is influenced by the timing of the past events. There are applications in finance, neuroscience, genome analysis, sociology, criminology, seismology, and many other fields.

Chapter 1 includes the introduction of the model and the survey of the results already known in the literature about Hawkes processes. That includes the stability results, limit theorems, power spectra of linear Hawkes processes and stability results of nonlinear Hawkes processes.

Chapter 2 is about the functional central limit theorem of nonlinear Hawkes processes. A Strassen’s invariance holds under the same assumptions. The work in Chapter 2 is based on Zhu [114].

Chapter 3 is dedicated to the process-level large deviations, i.e. level-3 large deviations, of the nonlinear Hawkes processes. The proofs consist of the proofs of the lower bound, the upper bound and the superexponential estimates. The level-1 large deviation principle is derived as a result of the contraction principle. This chapter is based on Zhu [113].

Chapter 4 is dedicated to the study of level-1 large deviation principle for nonlinear Hawkes processes when the exciting functions are exponential or sums of exponentials. It is based on the observation that when the exciting functions are exponential or sums of exponentials, the process is Markovian and a combination of Feynman-Kac formula for the upper bound of large deviations of Markov processes and tilting of the intensity function of Hawkes processes for the lower bound will establish a level-1 large deviation principle with the rate function expressed in terms of some variational formula. This chapter is based on Zhu [112].

Chapter 5 is about the asymptotics for nonlinear Hawkes processes. In this chapter, we drop the usual assumptions on nonlinear Hawkes processes, and study the phase transitions in different regimes. We categorize nonlinear Hawkes processes into the following regimes: sublinear regime, sub-critical regime, critical regime, super-critical regime and explosive regime. Different time asymptotics and various properties are obtained in different regimes. This chapter is based on Zhu [117].

Chapter 6 is about the limit theorems for linear Hawkes processes with random marks. The Central limit theorem and the large deviation principle are derived. We end this chapter with a simple application to a risk model. This is based on the joint work with my colleague Dmytro Karabash, see [62].

During my time as a PhD student at Courant Institute, I have the joy to work on some other problems either by myself or with my colleagues. For example, I studied the large deviations of self-correcting point processes with Sanchayan Sen, see [100] and also did some work on biased random walks on Galton-Watson trees without leaves with Behzad Mehrdad and Sanchayan Sen, see [75]. But since they are not closely related to the topics of my thesis, I do not include them here.

Chapter 1 Hawkes Processes

1.1 Introduction

Hawkes process is a self-exciting simple point process first introduced by Hawkes [51]. The future evolution of a self-exciting point process is influenced by the timing of past events. The process is non-Markovian except for some very special cases. In other words, Hawkes process depends on the entire past history and has a long memory. Hawkes process has wide applications in neuroscience, see e.g. Johnson [59], Chornoboy et al. [25], Pernice et al. [93], Pernice et al. [94], Reynaud et al. [98]; seismology, see e.g. Hawkes and Adamopoulos [53], Ogata [87], Ogata [88], Ogata et al. [90]; genome analysis, see e.g. Gusto and Schbath [46], Reynaud-Bouret and Schbath [96]; psycology, see e.g. Halpin and De Boeck [48]; spread of infectious disease, see e.g. Meyer et al. [76]; finance, see e.g. Bauwens and Hautsch [7], Bowsher [13], Hewlett [56], Large [67], Cartea et al. [22], Chavez-Demoulin et al. [23], Errais et al. [36]. Embrechts et al. [35], Muni Toke and Pomponio [83], Bacry et al. [3], [4], [1]; and in many other fields.

Let be a simple point process on and be an increasing family of -algebras. Any nonnegative -progressively measurable process with

| (1.1) |

a.s. for all intervals is called the -intensity of . We use the notation to denote the number of points in the interval .

A nonlinear Hawkes process is a simple point process admitting an -intensity

| (1.2) |

where is locally integrable and left continuous, . We always assume that unless otherwise specified. Here stands for , which is important for -predictability. The local integrability assumption of is to avoid explosion and the left continuity assumption of is to ensure that the process is -predictable.

In the literature, and are usually referred to as exciting function and rate function respectively.

A Hawkes process is said to be linear if is linear and it is nonlinear otherwise. For a linear Hawkes process, we can assume that the intensity is

| (1.3) |

In this thesis, unless otherwise specified, we assume the following.

-

•

is continuous and non-decreasing.

-

•

is continuous and non-increasing.

-

•

, i.e. the Hawkes process has empty past history.

Throughout, we define as . Thus, .

The first assumption says that the occurence of the past and present events have positive impact on the occurence of the future events. The second assumption says that as time evolves, the impact of the past events is decreasing. For most of the results in this paper, these two assumptions may not be necessary. We nevertheless make them to avoid some technical difficulties.

If one looks at (1.2), it is clear that if you witness some events occuring, increases since is increasing and you would expect even more events occuring. This is called the self-exciting property. Because of this, you would expect to see some clustering effects.

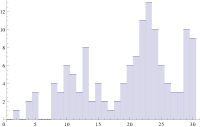

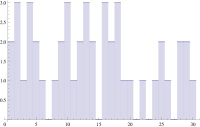

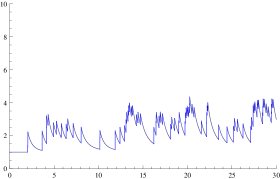

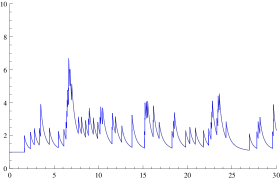

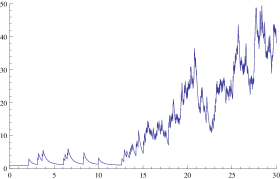

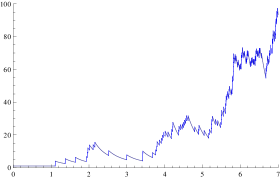

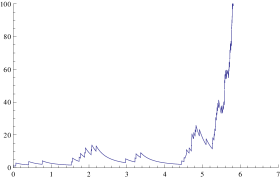

Figure 1.1 shows the histograms of a Hawkes process and a usual Poisson process. A Poisson process is stationary with independent increments. On the contrary, the Hawkes process has dependent increments and has clustering effects. As a result, in the picture, the Poisson process is more or less flat whilst the Hawkes process has peaks when it gets “excited” and has valleys when it “cools down”. Figure 1.2 shows the plot of the intensity of a Hawkes process. Unlike the usual Poisson process for which the intensity is a positive constant, the intensity of Hawkes process increases when you witness arrivals of points and it decays when there are no arrivals of points.

The self-exciting and clutstering properties of the Hawkes process make it ideal to characterize the correlations in some complex systems, including the default clustering effect in finance.

One generalization of classical linear Hawkes process is the so-called multivariate Hawkes process. We will define the multivariate Hawkes process and discuss some basic results in Section 1.6 of Chapter 1. The multivariate Hawkes process has been well studied in the literature and we would like to point out that if you have the result for the univariate Hawkes process, mathematically, it is not too difficult to generalize your result to multivariate Hawkes process.

Unlike the univariate Hawkes process, which only has the self-exciting property, the multivariate Hawkes process also has the mutually-exciting property. In the context of industry, consider that you have a large portfolio of companies, then the failure of one company can have impact on the performance of other companies. In other words, multivariate Hawkes process captures the cross-sectional clustering effect. That is why in most applications of Hawkes processes in finance, people usually consider multivariate Hawkes processes. We will review some basic results about multivariate linear Hawkes process in Chapter 1.

Another possible generalization to Hawkes process is the marked Hawkes process, i.e. Hawkes process with random marks. Just like univariate Hawkes process vesus multivariate Hawkes process, if you have the results in unmarked Hawkes process, usually it can be generalized to marked Hawkes process without much difficulty. For instance, the large deviations for linear Hawkes process is proved in Bordenave and Torrisi [11] and the large deviations for linear marked Hawkes process is then proved in Karabash and Zhu [62]. We will discuss the details of limit theorems of linear marked Hawkes process in Chapter 6.

Most of the literature on Hawkes processes studies only the linear case, which has an immigration-birth representation (see Hawkes and Oakes [54]). The stability, law of large numbers, central limit theorem, large deviations, Bartlett spectrum etc. have all been studied and understood very well. Almost all of the applications of Hawkes processes in the literature consider exclusively the linear case. Daley and Vere-Jones [27] and Liniger [71] provide nice surveys about the theory and applications of Hawkes processes.

One special case of the Hawkes process is when the exciting function is exponential. In this case, the Hawkes process is a continuous time Markov process. If is linear, the process is a special case of affine jump-diffusion process and is analytically tractable. This special case was for example studied in Oakes [85] and Errais et al. [36].

Because of the lack of computational tractability and immigration-birth representation, nonlinear Hawkes process is much less studied. However, some efforts have already been made in this direction. For instance, see Brémaud and Massoulié [14] for stability results, and Bremaud et al. [15] for the rate of convergence to stationarity. Karabash [63] recently proved the stability results for a wider class of nonlinear Hawkes processes.

As to the limit theorems, Bacry et al. [2] proved the central limit theorem for linear Hawkes process and Bordenave and Torrisi [11] proved the large deviation principle for linear Hawkes process.

For nonlinear Hawkes process, there is no explicit expression for the variance in the central limit theorem or the rate function for the large deviation principle. The method is more abstract and much more involved. Zhu [114] proved a central limit theorem for ergodic nonlinear Hawkes processes. Zhu [112] studied the large deviations in the Markovian case, i.e. when is exponential or sum of exponentials. And Zhu [113] proved the large deviation principle for more general nonlinear Hawkes processes at the process-level, i.e. level-3.

1.2 Applications of Hawkes Processes

1.2.1 Applications in Finance

The applications of Hawkes processes in finance include market orders modelling, see e.g. Bauwens and Hautsch [7], Bowsher [13], Hewlett [56], Large [67] and Cartea et al. [22]; value-at-risk, see e.g. Chavez-Demoulin et al. [23]; and credit risk, see e.g. Errais et al. [36]. Embrechts et al. [35] applied Hawkes processes to model the financial data. Muni Toke and Pomponio [83] applied Hawkes processes to model the trade-through. Bacry et al. [3] used Hawkes processes to reproduce empirically microstructure noise and discussed the Epps effect and lead-lag. The self-exciting and clustering properties of Hawkes processes are especially appealing in financial applications.

Currently, most of the applications of Hawkes process in the finance literature are about market orders modelling, see e.g. Bauwens and Hautsch [7], Bowsher [13] and Large [67].

Recently, Chavez-Demoulin and McGill [24] used Hawkes processes to study the extremal returns in high-frequency trading. The Hawkes process captures the volatility clustering behavior of the intraday extremal returns. and provides a suitable estimation of high-quantile based risk measures (e.g. VaR, ES) for financial time series.

Filimonov and Sornette [39] used Hawkes process to model market events, with the aim of quantifying precisely endogeneity and exogeneity in market activity. By using Hawkes process, Filimonov and Sornette [39] analyzed E-mini S&P futures contract over the period 1998-2010 and discovered that the degree of self-reflexivity has increased steadily in the last decade, an effect they attribute to the increased deployment of high-frequency and algorithmic trading. When they calibrated over much shorter time intervals (10 minutes), the Hawkes process analysis is found to detect precursors of the flash-crash that happened on May 6th, 2010. An early detection can benefit market regulators.

Very recently, Hardiman et al. [50] used (linear) Hawkes process to model the arrival of mid-price changes in the E-Mini S&P futures contract. Using several estimation methods, they found that the exciting function has a power-law decay and is close to . They pointed out that markets are and have always been close to criticality, challenging the studies of Filimonov and Sornette [39] which indicates that self-reflexivity (endogeneity) has increased in recent years as a result of increased automation of trading.

Egami et al. [33] studied the credit default swap (CDS) markets in both Japan and U.S. They made a dynamic analysis of the bid-ask spreads in both countries, which surged dramatically during the 2008-2009 financial crisis and they used the Hawkes process to predict the bid-ask spreads.

As pointed out in Errais et al. [36], “The collapse of Lehman Brothers brought the financial system to the brink of a breakdown. The dramatic repercussions point to the exisence of feedback phenomena that are channeled through the complex web of informational and contractual relationships in the economy… This and related episodes motivate the design of models of correlated default timing that incorporate the feedback phenomena that plague credit markets.” According to Peng and Kou [92], “We need better models to incorporate the default clustering effect, i.e., one default event tends to trigger more default events both across time and cross-sectionally.” The Hawkes process provides a model to characterize default events across time and if one uses a multivariate Hawkes process, that would describe the cross-sectional clustering effect as well.

Hawkes processes have been proposed as models for the arrival of company defaults in a bond portfolio, starting with the papers Giesecke and Tomecek [42] and Giesecke et al. [41]. It is not hard to see that when the exciting function is exponential, the linear Hawkes processes are affine jump-diffusion processes, see for instance Errais et al. [36]. With the help of the theory of affine jump-diffusions, one can then analyze price processes related to certain credit derivatives analytically.

1.2.2 Applications in Sociology

The Hawkes process has also been applied to the study of social interactions. Crane and Sornette [26] analysed the viewing of YouTube videos as an example of a nonlinear social system. They identified peaks in the time series of viewing figures for around half a million videos and studied the subsequent decay of the peak to a background viewing level. In Crane and Sornette [26], the Hawkes process was proposed as a model of the video-watching dynamics, and a plausible link made to the social interactions that create strong correlations between the viewing actions of different people. Individual viewing is not random but influenced by various channels of communication about what to watch next. Mitchell and Cates [77] used computer simulation to test the the claims in Crane and Sornette [26] that robust identification is possible for classes of dynamic response following activity bursts. They also pointed out some limitations of the analysis based on the Hawkes process.

In sociology, Hawkes process has also been used by Blundell et al. [10] to study the reciprocating relationships. Reciprocity is a common social norm, where one person’s actions towards another increases the probability of the same type of action being returned, e.g., if Bob emails Alice, it increases the probability that Alice will email Bob in the near future. The mutually-exciting processes, e.g. multivariate Hawkes processes, are able to capture the causal nature of reciprocal interactions.

1.2.3 Applications in Seismology

Ogata [87] used a particular case of the Hawkes process to predict earthquakes and the Hawkes process appears to be superior to other models by residual analysis. The specific model used by Ogata [87] is now known as ETAS (Epidemic Type Aftershock-Sequences) model. The discussions of ETAS model can be found in Daley and Vere-Jones [27].

1.2.4 Applications in Genome Analysis

Gusto and Schbath [46] used the Hawkes process to model the occurences along the genome and studied how the occurences of a given process along a genome, genes or motifs for instance, may be influenced by the occurrences of a second process. More precisely, the aim is to detect avoided and/or favored distances between two motifs, for instance, suggesting possible interactions at a molecular level. The statistical method proposed by Gusto and Schbath [46] is useful for functional motif detection or to improve knowledge of some biological mechanisms.

Reynaud-Bouret and Schbath [96] provided a new method for the detection of either favored or avoided distances between genomic events along DNA sequences. These events are modeled by the Hawkes process. The biological problem is actually complex enough to need a non-asymptotic penalized model selection approach and Reynaud-Bouret and Schbath [96] provided a theoretical penalty that satisfies an oracle inequality even for quite complex families of models.

1.2.5 Applications in Neuroscience

Chornoboy et al. [25] used the Hawkes process to detect and model the functional relationships between the neurons. The estimates are based on the maximum likelihood principle.

In most neural systems, neurons communicate via sequences of action potentials. Johnson [59] used various point processes, including Poisson process, renewal process and the Hawkes process and showed that neural discharges patterns convey time-varying information intermingled with the neuron’s response characteristics. By applying information theory and estimation theory to point processes, Johnson [59] described the fundamental limits on how well information can be extracted from neural discharges.

More recently, Pernice et al. [93] and Pernice et al. [94] have used Hawkes process to model the spike train dynamics in the studies of neuronal networks. As pointed out in Pernice et al. [93], “Hawkes’ point process theory allows the treatment of correlations on the level of spike trains as well as the understanding of the relation of complex connectivity patterns to the statistics of pairwise correlations.” Reynaud et al. [98] proposed new non-parametric adaptive estimation methods and adapted other recent similar results to the setting of spike trains analysis in neuroscience. They tested homogeneuous Poisson process, inhomogeneous Poisson process and the Hawkes process. A complete analysis was performed on single unit activity recorded on a monkey during a sensory-motor task. Reynaud et al. [98] showed that the homogeneous Poisson process hypothesis is always rejected and that the inhomogeneous Poisson process hypothesis is rarely accepted. The Hawkes model seems to fit most of the data.

The application of the Hawkes process in neuroscience has also been mentioned in Brémaud and Massoulié [14].

1.2.6 Applications in Criminology

Hawkes processes have also been used in criminology. Violence among gangs exhibits retaliatory behavior, i.e. given that an event has happened between two gangs, the likelihood that another event will happen shortly afterwards is increased. A problem like this can be modeled naturally by a self-exciting point process. Mohler et al. [78] and Egesdal et al. [34] have successfully modeled the pairwise gang violence as a Hawkes process. As pointed out in Hegemann et al. [55], in real-life situations, data is incomplete and law-enforcement agencies may not know which gang is involved. However, even when gang activity is highly stochastic, localized excitations in parts of the known dataset can help identify gangs responsible for unsolved crimes. The works before Hegemann et al. [55] incorporated the observed clustering in time of the data to identify gangs responsible for unsolved crimes by assuming that the parameters of the model are known, when in reality they have to be estimated from the data itself. Hegemann et al. [55] proposed an iterative method that simultaneously estimates the parameters in the underlying point process and assigns weights to the unknown events with a directly calculable score function.

Hawkes processses have also been used in the studies of terrorist activities. For example, Porter and White [95] used Hawkes process to examine the daily number of terrorist attacks in Indonesia from 1994 through 2007. Their model explains the self-exciting nature of the terrorist activities. It estimates the probability of future attacks as a function of the times since the past attacks.

Lewis et al. [69] used Hawkes process to model the temporal dynamics of violence and civilian deaths in Iraq.

1.3 Related Models

There are other generalizations or variations of the Hawkes processes in the literature. For example, Bormetti et al. [12] introduced a one factor model where both the factor and the idiosyncratic jump components are described by a Hawkes process. Their model is a better candidate than classical Poisson or Hawkes models to describe the dynamics of jumps in a multi-asset framework. Another example is a multivariate Hawkes process with constraints on its conditional density introduced by Zheng et al. [111]. Their study is mainly motivated by the stochastic modelling of a limit order book for high frequency financial data analysis. Dassios and Zhao [28] proposed a dynamic contagion process. It is basically a combination of a marked Hawkes process with exponential exciting function and an external shot noise process. Their model is Markovian. They also applied their model to insurance, see e.g. Dassios and Zhao [29].

In [116], Zhu incorporated Hawkes jumps into the classical Cox-Ingersoll-Ross model and obtained limit theorems and various other properties.

In seismology, Wang et al. [104] proposed a new model, i.e. the Markov-modulated Hawkes process with stepwise decay (MMHPSD), to investigate the variation in seismicity rate during a series of earthquakes sequence including multiple main shocks. The MMHPSD is a self-exciting process which switches among different states, in each of which the process has distinguishable background seismicity and decay rates. Stress release models are often used in seismology. In Brémaud and Foss [17], they created a new earthquake model combining the classical stress release model for primary shocks with the Hawkes model for aftershocks and studied the ergodicity of this new model.

1.4 Linear Hawkes Processes

In this section, let us review some known results about linear Hawkes process. Unlike the nonlinear Hawkes process, the linear Hawkes process has been very well studied in the literature. Hawkes and Oakes [54] introduced an immigration-birth representation of the linear Hawkes process, which can be viewed as a special case of the Poisson cluster process. The stability results of the linear Hawkes process, i.e. existence and uniqueness of a stationary linear Hawkes process have been summarised in Chapter 12 of Daley and Vere-Jones [27]. The rate of convergence to equilibrium has been stuided by Brémaud et al. [15]. The second-order analysis, i.e. the Bartlett spectrum etc. have been studied in Hawkes [51] and Hawkes [52]. Reynaud-Bouret and Roy [97] considered the linear Hawkes process as a special case of Poisson cluster process and studied the non-asymptotic tail estimates of the extinction time, the length of a cluster, and the number of points in an interval. Reynaud-Bouret and Roy [97] also obtained some so-called non-asymptotic ergodic theorems. The limit theorems have also been studied for linear Hawkes process. The central limit theorem was considered in Bacry et al. [2], the large deviation principle was obtained in Bordenave and Torrisi [11], and very recently the moderate deviation principle was proved in Zhu [115]. The simulations and calibrations of linear Hawkes process have been studied in Ogata [89], Møller and Rasmussen [80], [79], Vere-Jones [110], Ozaki [91] and many others.

1.4.1 Immigration-Birth Representation

Consider the linear Hawkes process with empty history, i.e. and intensity

| (1.4) |

where . It is well known that it has the following immigration-birth representation; see for example Hawkes and Oakes [54]. The immigrant arrives according to a homogeneous Poisson process with constant rate . Each immigrant reproduces children and the number of children has a Poisson distribution with parameter . Conditional on the number of the children of an immigrant, the time that a child was born has probability density function . Each child produces children according to the same laws, independent of other children. All the immigrants produce children independently. Now, is the same as the total number of immigrants and children in the time interval .

1.4.2 Stability Results

Consider the linear Hawkes process with empty history, i.e. and intensity

| (1.5) |

where . We review here the known results of existence and uniqueness of a stationary version of the process. We follow the arguments of Chapter 12 of Daley and Vere-Jones [27].

The existence of a stationary version of the process can be seen from the immigration-birth representation of the linear Hawkes process. To show uniqueness, let us do the following. Let be a stationary version with intensity

| (1.6) |

and mean intensity . For both and , we consider the shifted versions and that bring the origin back to zero. can be split into two components, the one with the same structure as , being generated from the clusters initiated by immigrants arriving after time and the component that counts the children of the immigrants that arrived before time . On , the contribution from the latter form a Poisson process with intensity

| (1.7) |

For any ,

| (1.8) | ||||

as . Let and represent the probability measures corresponding to and . For any , we have

| (1.9) |

as , where denotes the variation norm. This implies the weak convergence and thus the weak asymptotic stationarity of .

Under a stronger assumption , i.e. the mean time to the appearance of a child is finite. Since the mean number of offspring is also finite (because ), the random time from the appearance of an ancestor to the last of its descendants has finite mean, i.e. . Thus, we have

| (1.10) |

as and as , which implies that the process starting from empty history is strongly asymptotically stationary.

Brémaud et al. [15] studied the rate of convergence to the equilibrium in a more general setting, i.e. Hawkes process with random marks. Here, we only consider the unmarked case. Assume and let denote the unique stationary Hawkes process. The convergence in variation is seen via coupling, namely, and are constructed on the same space and there exists a finite random time such that

| (1.11) |

In the exponential case, there exists some such that . Let us define

| (1.12) |

If is directly Riemann integrable on , then for any

| (1.13) |

there exists such that for any .

In the subexponential case, the distribution function with density is subexponential, in the sense that,

| (1.14) |

Further assume that . Then, for any

| (1.15) |

there exists some such that for any , we have

| (1.16) |

where .

1.4.3 Bartlett Spectrum for Linear Hawkes Processes

The methods of analysis for point processes by spectrum were introduced by Bartlett [5] and [6]. We refer to Chapter 8 of Daley and Vere-Jones [27] for a detailed discussion.

Let be a second-order stationary point process on . (For the definition of second-order stationary point process, we refer to Daley and Vere-Jones [27].) Define the set as the space of functions of rapid decay, i.e. if

| (1.17) |

for some constants and all positive integers and .

For bounded measurable with bounded support and also , there exists a measure on such that

| (1.18) |

where is the Fourier transform of . is refered to as the Bartlett spectrum. We also have

| (1.19) |

Hawkes [52] proved that for the linear stationary Hawkes process with

| (1.20) |

and , the Bartlett spectrum is given by

| (1.21) |

1.4.4 Limit Theorems for Linear Hawkes Processes

When is linear, say , for some and , the Hawkes process has a very nice immigration-birth representation, see for example Hawkes and Oakes [54]. For such a linear Hawkes process, the limit theorems are very well understood. Consider a stationary Hawkes process with intensity

| (1.25) |

Taking expecatations on the both sides of the above equation and using stationarity, we get

| (1.26) |

which implies that . By ergodic theorem, we have

| (1.27) |

Moreover, Bordenave and Torrisi [11] proved a large deviation principle for .

Theorem 1 (Bordenave and Torrisi 2007).

satisfies a large deviation principle with the rate function

| (1.28) |

Recently, Bacry et al. [2] proved a functional central limit theorem for linear multivariate Hawkes process under certain assumptions. That includes the linear Hawkes process as a special case and they proved that

Theorem 2 (Bacry et al. 2011).

| (1.29) |

where is a standard Brownian motion. The convergence is weak convergence on , the space of cádlág functions on , equipped with Skorokhod topology. Here,

| (1.30) |

Unlike the central limit theorem and the law of the iterated logarithm, there are not as many good crietria one can use to prove the moderate deviation principle for nonlinear Hawkes processes, which would fill in the gap between the central limit theorem and the large deviation principle. Nevertheless, due to the analytical tractability and birth-immigration representation of linear Hawkes process, Zhu [115] proved the moderate deviations for linear Hawkes processes.

Theorem 3.

Assume , , and . For any Borel set and time sequence such that , we have the following moderate deviation principle.

| (1.31) | ||||

where .

In a nutshell, linear Hawkes processes satisfy very nice limit theorems and the limits can be computed more or less explicitly.

1.4.5 Proof of Theorem 3

Since a Hawkes process has a long memory and is in general non-Markovian, there is no good criterion in the literature for moderate deviations that we can use directly. For example, Bacry et al. [2] used a central limit theorem for martingales to obtain a central limit theorem for linear Hawkes processes. But there is no criterion for moderate deviations for martingales that can fit into the context of Hawkes processes. Our strategy relies on the fact that for linear Hawkes processes there is a nice immigration-birth representation from which we can obtain a semi-explicit formula for the moment generating function of in Lemma 1. A careful asymptotic analysis of this formula would lead to the proof of Theorem 3.

Proof of Theorem 3.

Let us first prove that for any ,

| (1.32) |

By Lemma 1, for fixed and sufficiently large, we have

| (1.33) |

where , . Here, is simply the in Lemma 1. Because depends on , we write instead of to indicate its dependence on . Clearly, is increasing in and is the minimal solution to the equation . (See the proof of Lemma 1 and the reference therein.) Since , it is easy to see that . Since , we have uniformly in . By Taylor’s expansion,

| (1.34) | ||||

Let , where

| (1.35) |

and

| (1.36) |

Substituting (1.35) and (1.36) back into (1.34) and using the fact uniformly in , we get uniformly in . Moreover, we claim that

| (1.37) | |||

| (1.38) |

To prove (1.37), notice first that

| (1.39) | ||||

Therefore,

| (1.40) |

Hence,

| (1.41) | |||

For the first term in (1.41), we have

| (1.42) |

as , since by our assumption, , which implies that as .

For the second term in (1.41), we have

| (1.43) |

This is because (1.35) is a renewal equation and . By the application of the Tauberian theorem to the renewal equation, (see Chapters XIII and XIV of Feller [38]), . Moreover, our assumptions and imply that

| (1.44) |

as .

To prove (1.38), notice that and again by the application of the Tauberian theorem to the renewal equation, (see Chapters XIII and XIV of Feller [38]), we have

| (1.45) | ||||

Finally, from (1.33) and the definitions of , and , we have

| (1.46) | |||

Hence, by (1.37), (1.38) and the fact that uniformly in , we conclude that, for any ,

| (1.47) |

Applying the Gärtner-Ellis theorem (see for example [30]), we conclude that, for any Borel set ,

| (1.48) | ||||

where

| (1.49) |

∎

Lemma 1.

For ,

| (1.50) |

where for any .

Proof.

The Hawkes process has a very nice immigration-birth representation, see for example Hawkes and Oakes [54]. The immigrant arrives according to a homogeneous Poisson process with constant rate . Each immigrant produces a number of children, this being Poisson distributed with parameter . Conditional on the number of the children of an immigrant, the time that a child is born has probability density function . Each child produces children according to the same laws independent of other children. All the immigrants produce children independently. Let , where is the number of descendants an immigrant generates up to time . Hence, we have

| (1.51) | ||||

By page 39 of Jagers [58], for all , is the minimal positive solution of

| (1.52) |

Let be the number of children of an immigrant and let be the number of descendants of immigrant’s th child that were born before time (including the th child if and only if it was born before time ). Then

| (1.53) | ||||

∎

1.4.6 Simulations and Calibrations

Assume the past of a Hawkes process is known up to present time zero, say the configuration of the history is . Let be the first jump after time zero. Then, it is easy to see that

| (1.54) |

where . This leads to a straight forward simulation method which is applicable for any simple point process. This algorithm and its theoretical foundation go back to a thinning procedure given Lewis and Shedler [70]. In the context of Hawkes processes, this simulation method was first used in Ogata [89]. It is sometimes called Ogata’s modified thinning algorithm.

If we want to simulate the stationary version of the Hawkes process on a finite time interval, then the standard method for the simulation method described above does not work as the past of the process is not known and cannot be simulated, at least not completely.

If one ignores the past of the process and simply starts to simulate the process at some given time, one speaks about an approximate simulation. In this case, one is actually simulating a transient version and not the stationary version of the process. But if one simulates for a long enough time interval, then the transient version converges to the stationary one. Such an approximate simulation method of Hawkes processes was discussed in Møller and Rasmussen [80]. A simulation method which directly simulates the stationary version without approximation is a so-called perfect simulation method. The idea is to incorporate somehow the effect of past observations without actually simulating the past of the process. For point processes, this type of simulation has first been described in Brix and Kendall [20]. In the context of Hawkes processes, the perfect simulation method was discussed in Møller and Rasmussen [79].

The calibrations, i.e. the estimation of the parameters of Hawkes processes, was first studied in Vere-Jones [110] and Ozaki [91], based on a maximum likelihood method for point processes introduced by Rubin [99]. The properties of the maximum likelihood estimator was analyzed in Ogata [86].

In Marsan and Lengline [73], an Expectation-Maximization (EM) algorithm, called “Model Independent Stochastic Declustering” (MISD), is introduced for the nonparametric estimation of self-exciting point processes with time-homogeneous background rate (For linear Hawkes process with intensity , is the background rate and is the exciting function).

The efficacy of the MISD algorithm was studied in Sornette and Utkin [101], where the authors found that the ability of MISD to recover key parameters such as depends on the values of the model parameters. In particular, they pointed out that the accuracy of MISD improves as the timescale over which the exciting function decays shortens. In Lewis and Mohler [68], they introduced a Maximum Penalized Likelihood Estimation (MPLE) approach for the nonparametric estimation of Hawkes processes. The method is capable of estimating and simultaneously, without prior knowledge of their form. Analogous to MPLE in the context of density estimation, the added regularity of the estimates allows for higher accuracy and/or lower sample sizes in comparison to MISD.

1.5 Nonlinear Hawkes Processes

Consider a simple point process with intensity

| (1.55) |

where and . Brémaud and Massoulié [14] studied the existence and uniqueness of a stationary nonlinear Hawkes process that satisfies the dynamics (1.55) as well as its stability in distribution and in variation. They allow to take negative values as well. In this thesis, we always consider to be nonnegative.

The following result is about the existence of a stationary nonlinear Hawkes process satisfying the dynamics (1.55). We do not need to be Lipschitz.

Theorem 4 (Brémaud and Massoulié [14]).

Let be a nonnegative, nondecreasing and left-continuous function, satisfying for any , for some and and let be such that . Then there exists a stationary point process with dynamics (1.55).

The following results concerns the uniqueness and stability in distribution and in variation of a nonlinear Hawkes process.

Theorem 5 (Brémaud and Massoulié [14]).

Let be -Lipschitz such that .

(i) There exists a unique stationary distribution of with finite average intensity and with dynamics (1.55).

(ii) Let . The dynamics (1.55) are stable in distribution with respect to either the initial condition (1.56) or the condition (1.57) below,

| (1.56) |

| (1.57) |

(iii) The dynamics (1.55) are stable in variation with respect to the initial condition,

| (1.58) |

if we assume further that .

Massoulié [74] extended the stability results to nonlinear Hawkes processes with random marks. He also considered the Markovian case and proved stability results without the Lipschitz condition for .

Very recently, Karabash [63] proved stability results for a much wider class of nonlinear Hawkes process, including the case when is not Lipschitz.

Moreover, Brémaud et al. [15] considered the rate of extinction for nonlinear Hawkes process, that is the rate of convergence to the equilibrium when the stationary process is an empty process. Indeed, they considered a more general setting, i.e. Hawkes process with random marks. Let be a nonlinear Hawkes process which is empty on , i.e. which satisfies the dynamics

| (1.59) |

where is locally integrable, , , is -Lipschitz and is measurable and not necessarily nonnegative and . The unique stationary process corresponding to the dynamics

| (1.60) |

is the empty process. Assume , and is locally bounded.

Then converges in variation to the empty process. The convergence in variation takes place via coupling in the sense that there exists a finite random time so that,

| (1.61) |

Depending on whether the tail of is exponential or subexponentail, the following was obtained by Brémaud et al. [15].

In the exponential case, let be such that . Assume is directly Riemann integrable. Then, for any with

| (1.62) |

there exists , for any ,

| (1.63) |

In the subexponential case, assume that distribution functinon with density is subexponential, is bounded and that , where . Then for any

| (1.64) |

there exists such that for any ,

| (1.65) |

Kwieciński and Szekli [66] considered the nonlinear Hawkes process as a special case of self-exciting process. Let be the space of point processes on , which can be regarded as an element of , the space of functions which are right-continuous with left limits, equipped with Skorohod topology. For any , if for any bounded set . For any , if and only if for the corresponding functions , i.e. for all .

Now, for a simple point process with intensity and compensator , we say that is positively self-exciting w.r.t. if for any ,

| (1.66) |

and is positively self-exciting w.r.t. if for any ,

| (1.67) |

Kwieciński and Szekli [66] pointed out that if is nonnegative and nondecreasing, then is positively self-exciting with respect to , and that if is nonnegative and nondecreasing and is nondecreasing, then is positively self-exciting with respect to .

Let be a Polish space with a closed partical ordering . A probability measure on is associated if

| (1.68) |

for all increasing sets (a set is increasing if and implies ).

Kwieciński and Szekli [66] proved that if is positively self-exciting point process w.r.t. (resp. ), then is associated (resp. ). Therefore, it implies that for a nonlinear Hawkes process, if is nonnegative and nondecreasing, then is associated and if is nonnegative and nondecreasing and is nondecreasing, then is associated .

Next, let us consider the limit theorems for nonlinear Hawkes process. When is nonlinear, the usual immigration-birth representation no longer works and you may have to use some abstract theory to obtain limit theorems. Some progress has already been made.

Brémaud and Massoulié [14]’s stability result implies that by the ergodic theorem,

| (1.69) |

as , where is the mean of under the stationary and ergodic measure.

In this thesis, we will obtain a functional central limit theorem and a Strassen’s invariance principle in Chapter 2 and a process-level, i.e. level-3 large deviation principle in Chapter 3 and thus a level-1 large deviation principle by contraction principle. We will also obtain an alternative expression for the rate function for level-1 large deviation principle of Markovian nonlinear Hawkes process as a variational formula in Chapter 4.

1.6 Multivariate Hawkes Processes

We say is a multivariate Hawkes process if for any , is a simple point process with intensity

| (1.70) |

where and . Then, is a vector and is a matrix-valued function.

Let us assume that for any , and that the spectral radius of the matrix satisfies . Then, Bacry et al. [2] proved a law of large numbers, i.e.

| (1.71) |

as almost surely and also in . If we assume further that for any ,

| (1.72) |

Then, Bacry et al. [2] proved the following central limit theorem:

| (1.73) |

converges in law as under the Skorohod topology to

| (1.74) |

where is the diagonal matrix with , .

It is well known that under the assumption that , there exists a unique stationary version of the multivariate Hawkes process satisfying the dynamics (1.70). The rate of convergence to the stationary version of the multivariate Hawkes process was obtained in Torrisi [103]. The Bartlett spectrum of the multivariate Hawkes process was derived in Hawkes [52]. Some non-asymptotics estimates for multivariate Hawkes processes were obtained in Hansen et al. [49].

A nice survey on multivariate linear Hawkes processes can be found in Liniger [71].

Chapter 2 Central Limit Theorem for Nonlinear Hawkes Processes

2.1 Main Results

In this chapter, we obtain a functional central limit theorem for the nonlinear Hawkes process under Assumption 1. Under the same assumption, a Strassen’s invariance principle also holds. Let us recall that is a nonlinear Hawkes process with intensity

| (2.1) |

Assumption 1.

We assume that

-

•

is a decreasing function and .

-

•

is positive, increasing and -Lipschitz (i.e. for any ) and .

Brémaud and Massoulié [14] proved that if is -Lipschitz with , there exists a unique stationary and ergodic Hawkes process satisfying the dynamics (1.2). Hence, under our Assumption 1 (which is slightly stronger than [14]), there exists a unique stationary and ergodic Hawkes process satisfying the dynamics (1.2).

Let and denote the probability measure and expectation for a stationary, ergodic Hawkes process, and let and denote the conditional probability measure and expectation given the past history.

The following are the main results of this chapter.

Theorem 6.

Remark 1.

By a standard central limit theorem for martingales, i.e. Theorem 9, it is easy to see that

| (2.4) |

where . In the linear case, say , Bacry et al. [2] proved that in (2.3) satisfies . That is not surprising because “should” have more fluctuations than . Therefore, we guess that for nonlinear , defined in (2.3) should also satisfy . However, it might not be very easy to compute and say something about in such a case.

In the classical case for a sequence of i.i.d. random variables with mean and variance , we have the central limit theorem as , and we also have in probability as , but the convergence does not hold a.s. The law of the iterated logarithm says that a.s. A functional version of the law of the iterated logarithm is called Strassen’s invariance principle.

It turns out that we also have a Strassen’s invariance principle for nonlinear Hawkes processes under Assumption 1.

Theorem 7.

Under Assumption 1, let be the stationary and ergodic nonlinear Hawkes process with dynamics (1.2). Let , , , , and for , let be the usual linear interpolation, i.e.

| (2.5) |

Then, , is relatively compact in , the set of continuous functions on equipped with uniform topology, and the set of limit points is the set of absolutely continuous functions on such that and .

2.2 Proofs

This section is devoted to the proof of Theorem 6. We use a standard central limit theorem, i.e. Theorem 8. In our proof, we need the fact that , which is proved in Lemma 3. Lemma 3 is proved by proving a stronger result first, i.e. Lemma 2. We will also prove Lemma 4 to guarantee that so that the central limit theorem is not degenerate.

Let us first quote the two necessary central limit theorems from Billingsley [8]. In both Theorem 8 and Theorem 9, the filtrations are the natural ones, i.e. given a stochastic process , , for .

Theorem 8 (Page 197 [8]).

Suppose , , is an ergodic stationary sequence such that and

| (2.6) |

where . Let . Then weakly, where the weak convergence is on equipped with the Skorohod topology and . The series converges absolutely.

Theorem 9 (Page 196 [8]).

Suppose , , is an erogdic stationary sequence of square integrable martingale differences, i.e. , and let . Let . Then weakly, where the weak convergence is on equipped with the Skorohod topology.

Now, we are ready to prove our main result.

Proof of Theorem 6.

Since in the stationary regime, for any and let us denote . In order to apply Theorem 8, let us first prove that

| (2.7) |

Let and be two independent copies of . It is easy to check that

| (2.8) | |||

Therefore, we have

| (2.9) | |||

where denotes the expectation of the number of points in for the Hawkes process with the same dynamics (1.2) and empty history, i.e. .

Next, let us estimate . is the expectation of the number of points in for the Hawkes process with intensity . It is well defined for a.e. under because, under Assumption 1,

| (2.10) |

which implies that -a.s.

It is clear that almost surely, so we can use a coupling method to estimate the difference. We will follow the ideas in Brémaud and Massoulié [14] using the Poisson embedding method. Consider , the canonical space of a point process on in which is Poisson with intensity under the probability measure . Then the Hawkes process with empty past history and intensity satisfies the following.

| (2.11) |

For , let us define recursively , and as follows.

| (2.12) |

Following the arguments as in Brémaud and Massoulié [14], we know that each is an -intensity of , where is the -algebra generated by up to time . By our Assumption 1, is increasing, and it is clear that and increase in for all and . Thus, is well defined and also that as , the limiting processes and exist. counts the number of points of below the curve and admits as an -intensity. By the monotonicity properties of and , we have

| (2.13) | |||

| (2.14) |

Letting (it is valid since we assume that is Lipschitz and thus continuous), we conclude that , satisfies the dynamics (1.2). Therefore, with intensity , is the Hawkes process with past history .

We can then estimate the difference by noticing that

| (2.15) |

Here means the expectation with respect to , the probability measure on the canonical space that we defined earlier.

We have

| (2.16) | ||||

where the first equality in (2.16) is due to the construction of in (2.12), the second equality in (2.16) is due to the definitions of and in (2.12) and finally the inequality in (2.16) is due to the fact that is -Lipschitz. Similarly,

| (2.17) | ||||

Iteratively, we have, for any ,

Now let . Then,

| (2.18) | |||

Here, by Lemma 3. Therefore, we have

| (2.19) | |||

Let . It is easy to check that by Assumption 1. We have

| (2.20) | |||

Since , we conclude that

| (2.21) | |||

Hence, by Theorem 8, we have

| (2.22) |

where

| (2.23) |

By Lemma 4, . Now, finally, for any , for sufficiently large,

| (2.24) | |||

as by Lemma 3. Hence, we conclude that as . ∎

Lemma 2.

There exists some such that .

Proof.

Notice first that for any bounded deterministic function ,

| (2.25) |

is a martingale. Therefore, using the Lipschitz assumption of , i.e. and applying Hölder’s inequality, for , we have

| (2.26) | |||

Let . Then, for any ,

| (2.27) | ||||

where in the first inequality in (2.27), we used the Jensen’s inequality since is convex and , and in the second inequality in (2.27), we used the fact that and again . Now choose so small that . Once and are fixed, choose so small that

| (2.28) |

This implies that for any ,

| (2.29) |

Hence, we conclude that for any ,

| (2.30) |

∎

Lemma 3.

There exists some such that . Hence .

Proof.

It is intuitively clear that . But still we need a proof.

Lemma 4.

, where is defined in (2.23).

Proof.

Let , where . is well defined because we proved (2.7). To see this, notice that

| (2.33) | ||||

by (2.7). Also, it is easy to check that

| (2.34) | |||

Let . This is an ergodic, stationary sequence such that . By (2.7), and by Theorem 9, , where . It is clear that since for any ,

| (2.35) | |||

as , where we used the stationarity of , Chebychev’s inequality and (2.7).

Now, it becomes clear that

| (2.36) | ||||

Consider . Notice that . By Jensen’s inequality and Assumption 1, we have

| (2.37) | ||||

It is clear that given the event ,

| (2.38) |

Therefore,

| (2.39) |

which implies that . ∎

Chapter 3 Process-Level Large Deviations for Nonlinear Hawkes Processes

3.1 Main Results

In this chaper, we prove a process-level, i.e. level-3 large deviation principle for nonlinear Hawkes processes. As a corollary, a level-1 large deviation principle is obtained by a contraction principle.

Let us recall that is a nonlinear Hawkes process with intensity

| (3.1) |

Throughout this chapter, we assume that

-

•

The exciting function is positive, continuous and decreasing for and for any . We also assume that .

-

•

The rate function is increasing and . We also assume that is Lipschitz with constant , i.e. for any .

Let be the set of countable, locally finite subsets of and for any and , write . For any , we write . Let denote the number of points in the set for any . We also use the notation to denote , the number of points up to time , starting from time . We define the shift operator by . We equip the sample space with the topology in which the convergence as is defined by

| (3.2) |

for any continuous with compact support.

This topology is equivalent to the vague topology for random measures, for which, see for example Grandell [45]. One can equip the space of locally finite random measures with the vague topology. The subspace of integer valued random measures is then the space of point processes. A simple point processes is a point process without multiple jumps. The space of point processes is closed. But the space of simple point processes is not closed.

Denote for any , i.e. the -algebra generated by all the possible configurations of points in the interval . Denote the space of probability measures on . We also define as the space of simple point processes that are invariant with respect to with bounded first moment, i.e. for any , . Define as the set of ergodic simple point processes in . We define the topology of as follows. For a sequence in and , we say as if and only if

| (3.3) |

as for any continuous and bounded and

| (3.4) |

as . In other words, the topology is the weak topology strengthened by the convergence of the first moment of . For any , in , one can define the metric by

| (3.5) |

where is the usual Prokhorov metric. Because this is an unusual topology, the compactness is different from that in the usual weak topology; later, when we prove the exponential tightness, we need to take some extra care. See Lemma 22 and (iii) of Lemma 21.

We denote by the set of real-valued continous functions on . We similarly define . We also denote by the set of all bounded progressively measurable and predictable functions.

Before we proceed, recall that a sequence of probability measures on a topological space satisfies the large deviation principle (LDP) with rate function if is non-negative, lower semicontinuous and for any measurable set ,

| (3.6) |

Here, is the interior of and is its closure. See Dembo and Zeitouni [30] or Varadhan [106] for general background regarding large deviations and their applications. Also Varadhan [107] has an excellent survey article on this subject.

In the pioneering work by Donsker and Varadhan [31], they obtained a level-3 large deviation result for certain stationary Markov processes.

We would like to prove the large deviation principle for nonlinear Hawkes processes by proving a process-level, also known as level-3 large deviation principle first. We can then use the contraction principle to obtain the level-1 large deviation principle for .

Let us define the empirical measure for the process as

| (3.7) |

for any , where for and for any . Donsker and Varadhan [31] proved that in the case when is a space of càdlàg functions on endowed with Skorohod topology and taking values in a Polish space , under certain conditions, satisfies a large deviation principle, where is a Markov process on with initial value . The rate function is some entropy function.

Let be the relative entropy of with respect to restricted to the -algebra . For any , let be the regular conditional probability distribution of . Similarly we define .

Let us define the entropy function as

| (3.8) |

Notice that describes the Hawkes process conditional on the past history . It has rate at time , which is well defined for almost every under if since implies for all .

When , for a.e. under , which implies that on . By the theory of absolute continuity of point processes, see for example Chapter 19 of Lipster and Shiryaev [72] or Chapter 13 of Daley and Vere-Jones [27], the compensator of is absolutely continuous, i.e. it has some density say, such that by the Girsanov formula,

| (3.9) | ||||

where . Both and are -predictable for . For the equality in (3.9), we used the fact that is a martingale under and for any which is bounded, progressively measurable and predictable, we have

| (3.10) |

We will use the above fact repeatedly in this chapter.

The following theorem is the main result of this chapter.

Theorem 10.

For any open set ,

| (3.11) |

and for any closed set ,

| (3.12) |

We will prove the lower bound in Section 3.2, the upper bound in Section 3.3, and the superexponential estimates that are needed in the proof of the upper bound in Section 3.4.

Once we establish the level-3 large deviation result, we can obtain the large deviation principle for directly by using the contraction principle.

Theorem 11.

satisfies a large deviation principle with the rate function given by

| (3.13) |

Proof.

Since is continuous, satisfies a large deviation principle with the rate function by the contraction principle. (For a discussion on contraction principle, see for example Varadhan [106].)

| (3.14) | ||||

Notice that

| (3.15) |

and

| (3.16) |

and

| (3.17) |

Hence,

| (3.18) |

For the lower bound, for any open ball centered at with radius ,

| (3.19) | ||||

For the upper bound, for any closed set and ,

| (3.20) | ||||

Finally, by Lemma 17, we have the following superexponential estimates

| (3.21) |

Hence, for the lower bound, we have

| (3.22) |

and for the upper bound, we have

| (3.23) |

which holds for any . Letting , we get the desired result. ∎

3.2 Lower Bound

Lemma 5.

For any , .

Proof.

Write . Thus, it is sufficient to show that for any . Note that and when and when and finally . Hence for any . ∎

Lemma 6.

Assume . Then,

| (3.24) |

where are some constants independent of .

Proof.

If , then for a.e. under , which implies that and thus , where and are the compensators of under and respectively. (For the theory of absolute continuity of point processes and Girsanov formula, see for example Lipster and Shiryaev [72] or Daley and Vere-Jones [27].) Since , we have for some . By the Girsanov formula,

| (3.25) |

Notice that .

| (3.26) | ||||

Therefore, we have

| (3.27) |

On the other hand, by Lemma 5,

| (3.28) | ||||

Thus,

| (3.29) |

Choosing and , we get

| (3.30) |

∎

Lemma 7.

We have the following alternative expression for .

| (3.31) |

Proof.

implies that for almost every under , also since . Thus,

| (3.32) | ||||

so by choice of .

By the theory of absolute continuity of point processes, see for example Chapter 13 of Daley and Vere-Jones [27], if , if and only if , where and are the compensators of under and respectively. If that’s the case, we can write for some and there is Girsanov formula

| (3.33) |

which implies that

| (3.34) |

For any , and the equality is achieved when . Thus, clearly, we have

| (3.35) |

On the other hand, we can always find a sequence convergent to and by Fatou’s lemma, we get the opposite inequality.

Now, assume that we do not have for a.e. under . That implies that . We want to show that

| (3.36) |

Let us assume that

| (3.37) |

We want to prove that .

Let be the point process on with compensator . Clearly and .

For any ,

| (3.38) | |||

Therefore,

| (3.39) | ||||

by lower semicontinuity of the relative entropy , Fatou’s lemma, and the fact that weakly as . Hence . ∎

Lemma 8.

is lower semicontinuous and convex in .

Proof.

By Lemma 7, we can rewrite as

| (3.40) | ||||

If , then and weakly. Since , is continuous on , and since is uniformly bounded, . Hence,

| (3.41) |

Let , where . Then, and thus . Also, , where is some constant. Therefore,

| (3.42) |

as . Next, notice that

| (3.43) | |||

as . Similarly, we have

| (3.44) |

Hence,

| (3.45) |

The supremum is taken over a linear functional of , which is continuous in , therefore the supremum over these linear functionals will be lower semicontinuous. Similarly, since in the variational formula expression of in Lemma 7, the supremum is taken over a linear functional of , is convex in . ∎

Lemma 9.

is linear in .

Proof.

It is in general true that the process-level entropy function is linear in . Following the arguments in Donsker and Varadhan [31], there exists a subset which is measurable and a measurable map such that for all and for all . Therefore, there exists a universal version, say independent of such that . Since that is true for all , it also holds for . Hence,

| (3.46) |

i.e. is linear in . ∎

In this chapter, we are proving the large deviation principle for Hawkes processes started with empty history, i.e. with probability measure . But when time elapses, the Hawkes process generates points and that create a new history. We need to understand how the history created affects the future. What we want to prove is some uniform estimates to the effect that if the past history is well controlled, then the new history will also be well controlled. This is essentially what the following Lemma 10 says. Consider the configuration of points starting from time up to time . We shift it by and denote that by such that , where is restricted to . These notations will be used in Lemma 10.

Remark 2.

At the very beginning of the chapter, we defined . It should not be confused with in this section.

Lemma 10.

For any such that and any open neighborhood of , there exists some such that and as and

| (3.47) |

Proof.

Let us abuse the notations a bit by defining

| (3.48) |

For any , since and is Lipschitz with constant , we have

| (3.49) | ||||

Define

| (3.50) |

By the maximal ergodic theorem,

| (3.51) | ||||

| (3.52) |

as . Thus as .

Fix any and . Since is decreasing, , integration by parts shows that

| (3.53) | ||||

where .

Therefore, uniformly for ,

| (3.54) |

where and

| (3.55) |

Define

| (3.56) |

Then, uniformly in ,

| (3.57) |

as . Thus as .

Hence, uniformly for and ,

| (3.58) | ||||

| (3.59) |

where and .

Observe that

| (3.60) |

Let .

Uniformly for ,

| (3.61) | |||

Since , by ergodic theorem,

| (3.62) |

and since satisfies,

| (3.63) |

for almost every under ,

| (3.64) |

is stationary, so as . Also, as . Remember that . By choosing big enough, we conclude that

| (3.65) |

Since it holds for any , we get the desired result. ∎

Theorem 12 (Lower Bound).

For any open set ,

| (3.66) |

Proof.

It is sufficent to prove that for any , , for any neighborhood of , . Since for every invariant measure , there exists a probability measure on the space of ergodic measures such that , for any such that , without loss of generality, we can assume that , where , and . By linearity of , . Divide the interval into subintervals of length , let , be the right hand endpoints of these subintervals, and let . For each , take as in Lemma 10. We have , as . Choose neighborhoods of , such that . We have

| (3.67) | ||||

Now, applying Lemma 10 and the linearity of ,

| (3.68) |

∎

3.3 Upper Bound

Remark 3.

By following the argument in Donsker and Varadhan [31], if is weakly continuous, then

| (3.69) |

for any compact . If the Hawkes process has finite range of memory, i.e. has compact support, and if it is continuous, then, for any , if , we have

| (3.70) | |||

as , which implies that .

If the Hawkes process does not have finite range of memory, then we should use the specific features of the Hawkes process to obtain the upper bound.

Before we proceed, let us prove an easy but very useful lemma that we will use repeatedly in the proofs of the estimates in this chapter.

Lemma 11.

Let be progressively measurable and predictable. Then,

| (3.71) |

Proof.

Since is a martingale, by Cauchy-Schwarz inequality,

| (3.72) | ||||

∎

Define

| (3.73) | ||||

Here is progressively measurable and predictable, and means that is progressively measurable, predictable and also bounded and continuous.

Lemma 12.

For any and , we have, for any ,

| (3.74) |

Proof.

For any , writing ,

| (3.75) | ||||

by Jensen’s inequality and the fact that by iteratively conditioning since for any . ∎

Remark 4.

Under , the progressively measurable rate function is well defined since it only creates a history between time and time . Similary, in the proof in Lemma 12, for any should be interpreted as the expectation is given any history created between time and , which is well defined.

Next, we need to compare and .

Lemma 13.

For any , and ,

| (3.76) |

Proof.

| (3.77) | |||

It is easy to see that is -measurable and

| (3.78) |

for any . Hence,

| (3.79) | |||

By Hölder’s inequality and Lemma 17, we have

| (3.80) | |||

Furthermore,

| (3.81) | |||

For the first term

| (3.82) | |||

Therefore,

| (3.83) |

where as ; in other words, it vanishes.

For the second term,

| (3.84) | |||

Assume that is decreasing and . By applying Jensen’s inequality twice, we can estimate the second term above,

| (3.85) | |||

where . Thus,

| (3.86) |

Similarly, we can estimate the first term.

For the third term, by Jensen’s inequality, we have

| (3.87) | |||

Since is decreasing, . Thus

| (3.88) |

Let and . Then,

| (3.89) | |||

Notice that

| (3.90) |

where as , which implies that

| (3.91) |

Moreover,

| (3.92) | |||

Notice that it holds for any and that as , which implies

| (3.93) |

Putting all these things together and applying Hölder’s inequality several times, we find that for any , and ,

| (3.94) |

∎

Lemma 14.

| (3.95) |

Proof.

Assume . For any , there exists some such that

| (3.96) |

We can find a sequence as . By Fatou’s lemma,

| (3.97) | |||

If , then, for any , there exists some such that

| (3.98) |

Repeat the same argument as in the case that . ∎

Lemma 15.

For any compact set ,

| (3.99) |

Proof.

Notice that

| (3.100) |

By choosing small enough, we have for some constant . Therefore

| (3.101) |

which implies (by comparing and and the superexponential estimates in Lemma 17)

| (3.102) |

Therefore, we need only to consider compact sets such that for any , .

Now for any compact consisting of with and for any and for any , , by Hölder’s inequality, Chebychev’s inequality, and Lemma 12,

| (3.103) | |||

By Lemma 13,

| (3.104) |

Since it holds for any , we get

| (3.105) |

For any compact , given and , by Lemma 14, there exists and such that . Since the linear integral is a continuous functional of (see the proof of Lemma 8), there exists a neighborhood of such that for all . Since is compact, there exists such that . Hence

| (3.106) |

Note that for any and ,

| (3.107) | |||

Thus, for ,

| (3.108) |

whence for any compact . ∎

Theorem 13 (Upper Bound).

For any closed set ,

| (3.109) |

3.4 Superexponential Estimates

In order to get the full large deviation principle, we need the upper bound inequality valid for any closed set instead of for any compact set, which requires some superexponential estimates.

Lemma 16.

For any ,

| (3.114) |

Proof.

| (3.115) | ||||

Note that since . Therefore,

| (3.116) |

where as . Since it holds for any , we get the desired result. ∎

Lemma 17.

For any and ,

| (3.117) |

Therefore, for any ,

| (3.118) |

Proof.

Lemma 18.

We have the following superexponential estimates.

(i) For any ,

| (3.121) |

(ii) For any ,

| (3.122) |

(iii) For any ,

| (3.123) |

Proof.

(i) Define

| (3.124) |

Then and has compensator and has compensator . Notice that

| (3.125) |

It is clear that is dominated by the usual Poisson process with rate . By Lemma 19,

| (3.126) |

On the other hand,

| (3.127) | ||||

By Lemma 17, we have

| (3.128) |

for any . Hence

| (3.129) |

Finally, for some positive to be chosen later,

| (3.130) | ||||

Let . Then as . Let . Then, by the definition of and abusing the notation a little bit, we see that . Since is increasing, its inverse function exists and as . We have

| (3.131) | ||||

It is clear that . Choose

| (3.132) |

Then as and

| (3.133) | ||||

Hence,

| (3.134) |

(ii) It is easy to see that (iii) implies (ii).

(iii) Observe first that

| (3.135) | ||||

For the first term, notice that is dominated by a usual Poisson process with rate . Thus, by Lemma 20,

| (3.136) |

For the second term, and

| (3.137) |

By Lemma 17,

| (3.138) |

and by the same argument as in (i),

| (3.139) |

For the third term, notice that

| (3.140) |

So we can get the same superexponential estimate as before. Finally, for the fourth term,

| (3.141) |

We can get the same superexponential estimate as before. ∎

Lemma 19.

Assume is a Poisson process with constant rate . Then for any ,

| (3.142) |

Proof.

Let , where is to be chosen later. By Jensen’s inequality and stationarity and independence of increments of the Poisson process,

| (3.143) | ||||

for some . Choose . Then,

| (3.144) |

for some . Therefore, by Chebychev’s inequality,

| (3.145) |

which holds for any . Letting , we get the desired result. ∎

Lemma 20.

Assume is a Poisson process with constant rate . Then for any ,

| (3.146) |

Proof.

Let be some function of to be chosen later. Following the same argument as in the proof of Lemma 19, we have

| (3.147) | |||

Choosing will do the work. ∎

The following Lemma 21 provides us the superexponential estimates that we need. These superexponential estimates have basically been done in Lemma 18. The difference is that in the statement in Lemma 18, we used and in Lemma 21 it is changed to which is what we needed. Lemma 21 has three statements. Part (i) says if you start with a sequence of simple point processes, the limiting point process may not be simple, but this has probability that is superexponentially small. Part (ii) is the usual superexponential we would expect if were equipped with weak topology. But since we are using a strengthened weak topology with the convergence of first moment as well, we will also need Part (iii).

Lemma 21.

We have the following superexponential estimates.

(i) For some as ,

| (3.148) |

(ii) For some as ,

| (3.149) |

(iii) For some as ,

| (3.150) |

Proof.

Lemma 22.

For any , define

| (3.155) | |||

where as , as and as . Let and

| (3.156) |

Then is compact.

Proof.

Observe that for , the sets

| (3.157) |

are relatively compact in . Let be the closure of , which is then compact.

For any , for any . We can choose big enough and an increasing sequence such that and as , uniformly for ,

| (3.158) | ||||

as . Therefore, is tight in the weak topology and by Prokhorov theorem is precompact in the weak topology. In other words, for any sequence in , there exists a subsequence, say such that weakly as for some . By the definition of , are uniformly integrable, which implies that as . It is also easy to see that is closed by checking that each is closed. That implies that . Finally, we need to check that is a simple point process. Let . We have for any ,

| (3.159) | ||||

Hence, is precompact in our topology. Since is closed, it is compact. ∎

3.5 Concluding Remarks

In this chapter, we obtained a process-level large deviation principle for a wide class of simple point processes, i.e. nonlinear Hawkes processes. Indeed, the methods and ideas should apply to other simple point processes as well and we should expect to get the same expression for the rate function . For , it should be of the form

| (3.160) |