Dispersive and dissipative errors in the DPG method with scaled norms for Helmholtz equation

Abstract.

We consider the discontinuous Petrov-Galerkin (DPG) method, where the test space is normed by a modified graph norm. The modification scales one of the terms in the graph norm by an arbitrary positive scaling parameter. Studying the application of the method to the Helmholtz equation, we find that better results are obtained, under some circumstances, as the scaling parameter approaches a limiting value. We perform a dispersion analysis on the multiple interacting stencils that form the DPG method. The analysis shows that the discrete wavenumbers of the method are complex, explaining the numerically observed artificial dissipation in the computed wave approximations. Since the DPG method is a nonstandard least-squares Galerkin method, we compare its performance with a standard least-squares method.

Key words and phrases:

least-squares, dispersion, dissipation, quasioptimality, resonance, stencil2010 Mathematics Subject Classification:

65N30,35J051. Introduction

Discontinuous Petrov-Galerkin (DPG) methods were introduced in [8, 10]. The DPG methods minimize a residual norm, so they belong to the class of least-squares Galerkin methods [3, 7, 14], although the functional setting in DPG methods is nonstandard. In this paper, we introduce an arbitrary parameter into the definition of the norm in which the residual is minimized. We study the properties of the resulting family of DPG methods when applied to the Helmholtz equation.

The DPG framework has already been applied to the Helmholtz equation in [12]. An error analysis with optimal error estimates was presented there. There are two major differences in the content of this paper and [12]. The first is the introduction of the above mentioned parameter, . When , the method here reduces to that in [12]. The use of such scaling parameters was already advocated in [11] based on numerical experience. In this paper, we shall provide a theoretical basis for its use. The second major difference with [12] is that in this contribution we perform a dispersion analysis of the DPG method with the scaling. We thus discover several important properties of the method as is varied.

Least-squares Galerkin methods are popular methods in scientific computation [3, 17]. They yield Hermitian positive definite systems, notwithstanding the indefiniteness of the underlying problem. Hence they are attractive from the point of view of solver design and many works have focused on this subject [18, 19]. However, as we shall shortly see in detail, for wave propagation problems, they yield solutions with heavy artificial dissipation. Since the DPG method is of the least-squares type, it also suffers from this problem. One of the goals of this paper is to show that by means of the -scaling, we can rectify this problem to some extent.

To explain this issue further, let us fix the specific boundary value problem we shall consider. Let denote the Helmholtz wave operator defined by

| (1) |

Here denotes the imaginary unit, is the wavenumber, and is a bounded open connected domain with Lipschitz boundary. All function spaces in this paper are over the complex field . The Helmholtz equation takes the form for some . Although, we consider a general f in this paper, in typical applications, with , in which case, eliminating the vector component , we recover the usual second order form of the Helmholtz equation,

This must be supplemented with boundary conditions. The DPG method for the case of the impedance boundary conditions on was discussed in [12], but other boundary conditions are equally well admissible. In the present work, we consider the Dirichlet boundary condition

| (2) |

To deal with this boundary condition, we will need the space

| (3) |

Thus, our boundary value problem reads as follows:

| (4) |

It is well known [16] that except for in , an isolated countable set of real values, this problem has a unique solution. We assume henceforth that is not in .

Before studying the DPG method for (4), it is instructive to examine the simpler least-squares Galerkin method. Set to the Cartesian product of the lowest order Raviart-Thomas and Lagrange spaces, together with the boundary condition in . The method finds such that

| (5) |

Throughout, denotes the norm, or the natural norm in the Cartesian product of several component spaces. The method (5) belongs to the so-called FOSLS [7] class of methods.

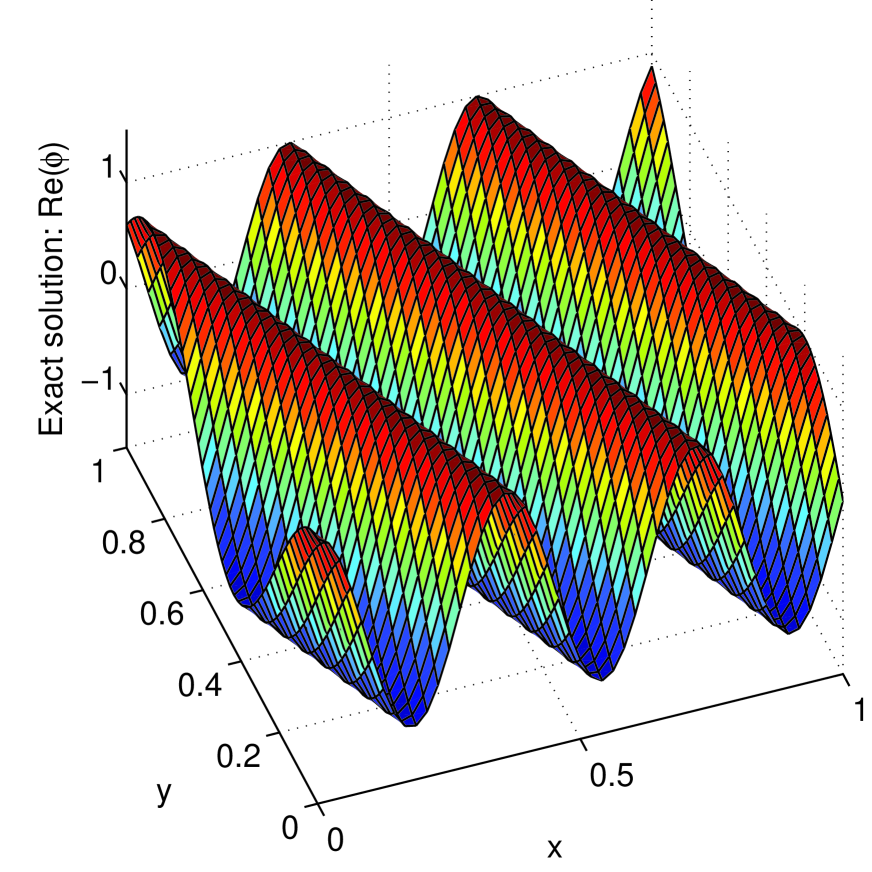

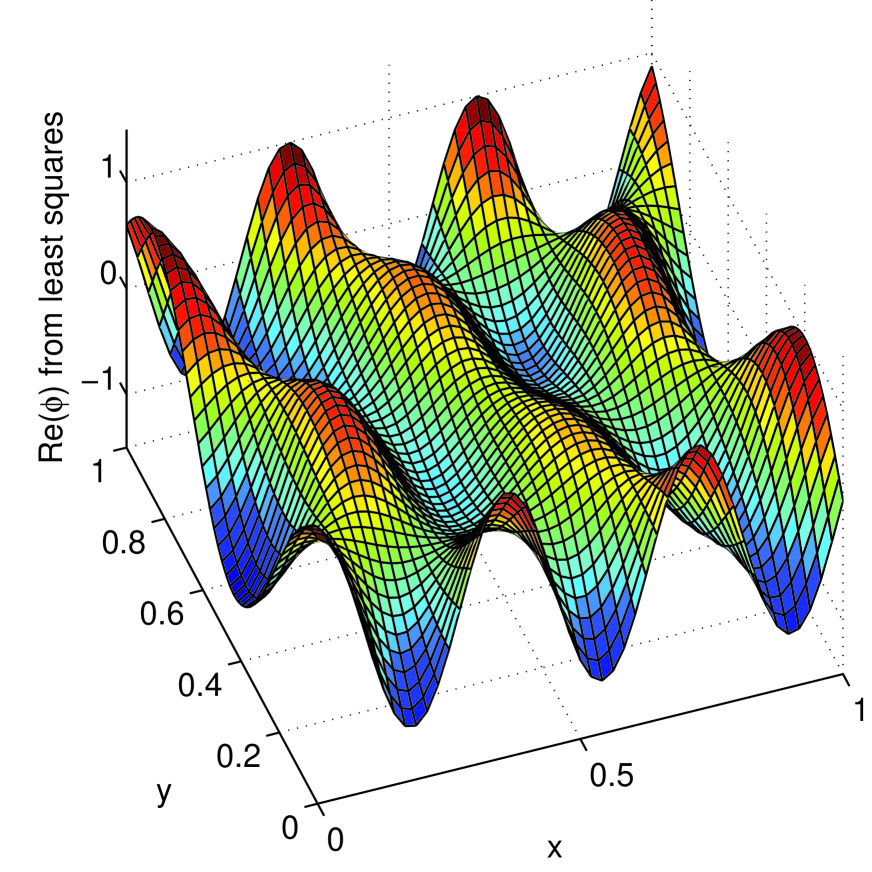

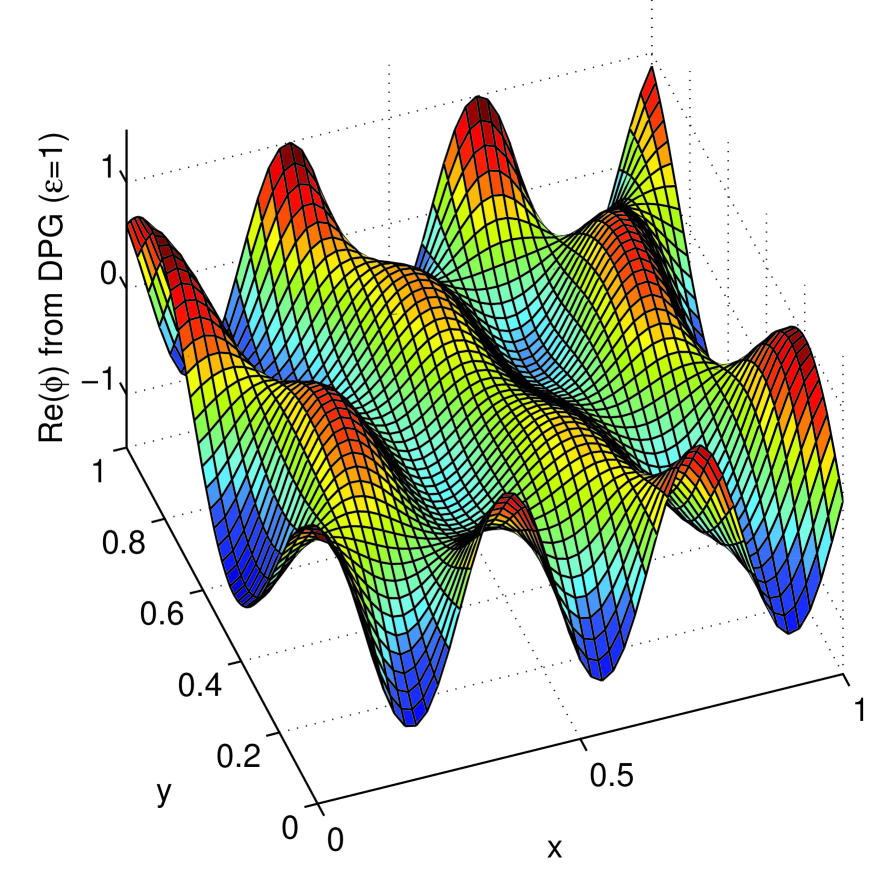

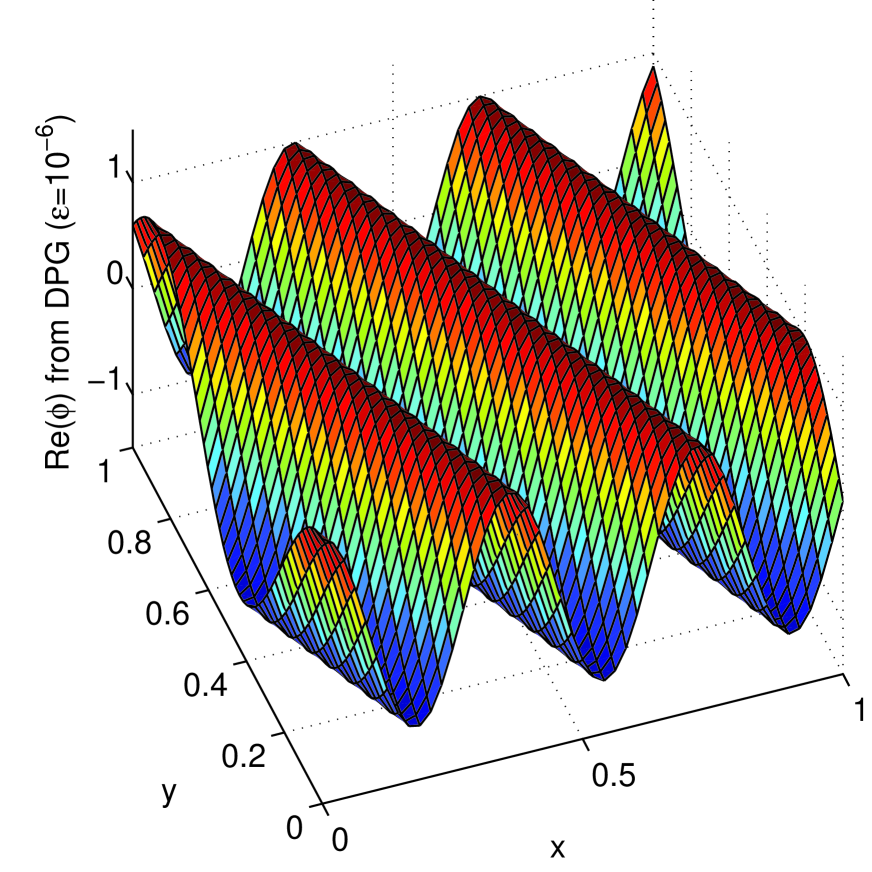

Although (5) appears at first sight to be a reasonable method, computations yield solutions with artificial dissipation. For example, suppose we use (5), appropriately modified to include nonhomogeneous boundary conditions, to approximate a plane wave propagating at angle in the unit square. A comparison between the real parts of the exact solution (in Figure 1(a)) and the computed solution (in Figure 1(b)) shows that the computed solution dissipates at interior mesh points. The same behavior is observed for the lowest order DPG method with in Figure 1(c) (see §2.4 for the definition of therein and Section 4 for a full discussion of the lowest order DPG method). The same method with however gave a solution (in Figure 1(d)) that is visually indistinguishable from the exact solution. Note that, for the DPG method with , the numerical results presented in [12] show much better performance, because slightly higher order spaces were used there. Instead, in this paper, we have chosen to study the DPG method with the lowest possible order of approximation spaces to reveal the essential difficulties with minimal computational effort.

The situation in Figures 1(b) and 1(c) improves when more elements per wavelength are used. This is not surprising in view of the asymptotic error estimates of the methods. To give an example of such an error estimate, consider the case of the impedance boundary conditions considered in [12]. It is proven there that there is a constant , independent of and mesh size , such that the lowest order DPG solution satisfies

| (6) |

for a plane wave solution. A critical ingredient in this analysis is the estimate

| (7) |

which, as shown in [12, Lemmas 4.2 and 4.3], holds for all w in the analogue of with impedance boundary conditions. Although the analysis in [12] was for the impedance boundary condition, similar techniques apply to the Dirichlet boundary condition as well, leading to (6). As more elements per wavelength are used, decreases, so (6) guarantees that the situation in Figure 1(c) will improve.

The analysis for the least-squares method is easier than the above-mentioned DPG analysis. Indeed, by (5), for any . Hence, applying (7) to the error and noting that the residual is , we obtain . By standard approximation estimates, we then conclude that there is a independent of and such that

| (8) |

This simple technique of analysis of -based least-squares methods is well-known (see e.g., [17, pp. 70–71]). As with (6), the estimate (8) implies that as the number of elements per wavelength is increased, decreases, and the situation in Figure 1(b) must improve.

Yet, Figures 1(b) and 1(c) show that these methods fail to be competitive with standard methods in accuracy for small number of elements per wavelength. The figures also illustrate one of the difficulties with asymptotic error estimates like (7) and (8). Having little knowledge of the size of , we cannot predict the performance of the method on coarse meshes. Motivated by this difficulty, one of the theorems we present (Theorem 3.1) will give a better idea of the constant involved as . Also note that the above indicated error analyses does not give us a quantitative measure of differences in wave speeds between the computed and exact waves. This motivates the dispersion analysis we present in this paper, which will address the issue of wave speed discrepancies.

We should note that there are alternative methods of the least-squares type that exhibit better performance than the standard -based least squares method. Some are based on adding further terms to the residual to be minimized (e.g., to control the curl of the vector equation [18]). Another avenue explored by others, and closer to the subject of this paper, is the idea of minimizing the residual in a dual norm [4, 5]. The main difference with our method is that our dual norms are locally computable in contrast to their nonlocal norms. This is achieved by using an ultraweak variational setting. The domain and codomain of the operator in the least-squares minimization associated to the DPG method are nonstandard, as we shall see next.

2. The DPG method for the Helmholtz equation

In this section, we briefly review the method for the Helmholtz equation introduced in [12]. We then show exactly where the parameter is introduced to get the variant of the method that we intend to study.

Let be a disjoint partitioning of into open elements such that . The shape of the mesh elements in is unimportant for now, except that we require their boundaries to be Lipschitz so that traces make sense. Let

| (9) |

where

Let be defined in the same way as in (1), except the derivatives are taken element by element, i.e., on each , we have

2.1. Integration by parts

The following basic formula that we shall use is obtained simply by integrating by parts each of the derivatives involved:

| (10) |

for smooth functions and and domains with Lipschitz boundary. Above, overlines denote complex conjugations and the integrals use the appropriate Lebesgue measure. Note that we use the notation throughout to generically denote the outward unit normal on various domains – the specific domain will be clear from context – e.g., in (10), it is . Introducing the following abbreviated notations for tuples and ,

we can rewrite (10), applied element by element, as

| (11) |

By density, (11) holds for all and all . Then, must be interpreted using the appropriate duality pairing as the last term in (11) contains interelement traces on .

It will be convenient to introduce notation for such traces: Define

as follows. For any , the restriction of on the boundary of any mesh element takes the form Although the meaning of is more or less self-evident, to include a proper definition, first let denote the space of all functions of the form where is in , normed by Let denote the dual space of . Now, consider the map , defined for smooth functions on . Since

(the left and right hand sides extend to duality pairings in and , respectively), the standard trace theory implies that can be extended to a continuous linear operator . The range of is what we denoted by “.” Throughout this paper, functions in appear together with a dot product with , so we could equally well consider the standard space , but the notation simplifies with the former. In particular, with this notation, is a single-valued function on the element interfaces since is globally in .

2.2. An ultraweak formulation

The boundary value problem we wish to approximate is (13). Recall the definition of in (3). To deal with the Dirichlet boundary condition, we will need the trace space

| (12) |

To derive the DPG method for

| (13a) | |||||

| (13b) | |||||

we use the integration parts by formula (11) to get

for all . Now we let the trace be an independent unknown in . Defining the bilinear form , we obtain the ultraweak formulation of [12]: Find in

satisfying

| (14) |

The wellposedness of this formulation was proved in [12] for the case of impedance boundary conditions. As is customary, we refer to the solution component as the numerical flux and as the numerical trace.

2.3. The -DPG method

Let be a finite dimensional trial space. The DPG method finds in satisfying

| (15) |

for all in the test space , defined by

| (16) |

where is defined by

| (17) |

and the -inner product is the inner product generated by the norm

| (18) |

Here is an arbitrary scaling parameter. Note that when , (18) defines a graph norm on . The case , analyzed in [12], is the standard DPG method. In the next section, we will adapt the analysis of [12] to the case of the variable , which we refer to as the “-DPG method.”

It is easy to reformulate the -DPG method as a residual minimization problem. (All DPG methods with test spaces as in (17) minimize a residual as already pointed out in [10].) Letting denote the dual space of , normed with , we define by . Then letting denote the operator generated by the above-defined , i.e., for all and , one can immediately see that solves (15) if and only if

This norm highlights the difference between the DPG method and the previously discussed standard -based least-squares method (5).

2.4. Inexactly computed test spaces

A basis for the test space , defined in (16), can be obtained by applying to a basis of . One application of requires solving (17), which although local (calculable element by element), is still an infinite dimensional problem. Accordingly a practical version of the -DPG method uses a finite dimensional subspace and replaces by defined by

| (19) |

In computations, we then use, in place of , the inexactly computed test space , i.e., the practical DPG method finds in satisfying

| (20) |

For the Helmholtz example, we set as follows: Let denote the space of polynomials of degree at most and in and , resp. Let denote the Raviart-Thomas subspace of . We set

Clearly, . Later, we shall solve (20) using and report the numerical results. It is easy to see using the Fortin operators developed in [15] that is injective for , which implies that (20) yields a positive definite system. However, a complete analysis using [15] tracking and dependencies, remains to be developed, and is not the subject of this paper.

3. Analysis of the -DPG method

The purpose of this section is to study how the stability constant of the -DPG method (15) depends on . The analysis in this section provides the theoretical motivation to introduce the scaling by into the DPG setting.

3.1. Assumption

The analysis is under the already placed assumption that the boundary value problem (13) is uniquely solvable. We will now need a quantitative form of this assumption. Namely, there is a constant , possibly depending on , such that the solution of (13) satisfies

One expects to become large as approaches any of the resonances in . For any , choosing and applying the above inequality, we obtain

| (21) |

This is the form in which we will use the assumption.

Note that in the case of the impedance boundary condition, the unique solvability assumption can be easily verified [20] for all . Furthermore, when that boundary condition is imposed, for instance, on the boundary of a convex domain, the estimate (21) is proved in [12, Lemmas 4.2 and 4.3] using a result of [20] . The resulting constant is bounded independently of . However, we cannot expect this independence to hold for the Dirichlet boundary condition (2) we are presently considering.

3.2. Quasioptimality

It is well-known that if there are positive constants and such that

| (22) |

then a quasioptimal error estimate

| (23) |

holds. This follows from [12, Theorem 2.1], or from the more general result of [15, Theorem 2.1], after noting that the following uniqueness condition holds: Any satisfying for all vanishes. (Since this uniqueness condition can be proved as in [12, Lemma 4.1], we shall not dwell on it here.)

Accordingly, the remainder of this section is devoted to proving (22), tracking the dependence of constants with , and using the -norm we define below. First, let

By virtue of (21), this is clearly a norm under which the space , defined in (3), is complete. The space in (12) is normed by the quotient norm, i.e., for any ,

The function in which achieves the infimum above defines an extension operator that is a continuous right inverse of and satisfies

| (24) |

With these notations, we can now define the norm on the trial space by

The following theorem is proved by extending the ideas in [12] to the -DPG method.

Theorem 3.1.

Proof.

We first prove the continuity estimate. Let and let . We use the abbreviated notations , , and . By (21) and (24),

| (25) |

The extension can be used to rewrite Then, applying the Cauchy-Schwarz inequality, and using (25), we have

| (26) |

where . With and we apply the inequality to obtain

for any . Setting so that

| (27) |

with as in the statement of the theorem. Hence, Returning to (26),

with . This verifies the upper inequality of (22).

To prove the lower inequality of (22), let r be the unique function in satisfying for any given . Then, by (21),

| (28) |

Also, since , letting , we have

| (29) |

By (11), we have , so

| (30) |

where , a function that can be bounded using (28), as follows:

for any . Choosing as in (27) and using (28)–(29),

| (31) |

Returning to (30), we now have

by virtue of (31), verifying the lower inequality of (22) with ∎

Remark 3.2.

Although we presented the above result only for the Helmholtz equation, the ideas apply more generally. It seems possible to prove a similar result abstractly, e.g., using the abstract setting in [6], for any DPG application that uses a scaled graph norm analogous to (18) (with the wave operator replaced by suitable others).

3.3. Discussion

Theorem 3.1 shows that the use of the -scaling in the test norm can ameliorate some stability problems, e.g., those that can arise from large .

Observe that the best possible value for the constant in (23) is . Indeed, if equals , then the computed solution coincides with the best approximation to u from . Theorem 3.1 shows that the quasioptimality constant of the DPG method approaches the ideal value of as .

However, since the norms depend on , we must further examine the components of the error separately, by defining

| (32a) | ||||

| (32b) | ||||

The estimate of Theorem 3.1 implies that

| (33) |

where and are the best approximation errors defined by

| (34) | ||||

Note that is independent of .

We want to compare the error bounds for the numerical fluxes and traces in the case with the case of . To distinguish these cases we will denote the error defined in (32b) by when . Clearly, (33) implies

| (35) |

For the other case, (33) implies, after multiplying through by ,

Comparing this with (35), and noting that and remain the same for different , we find that the DPG errors for fluxes and traces admit a better bound for smaller . Whether the actually observed numerical error improves, will be investigated through the dispersion analysis presented in a later section, as well as in the next subsection.

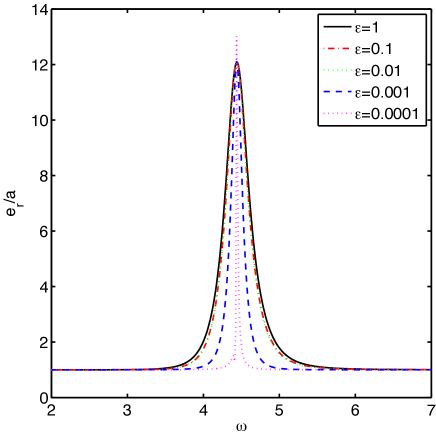

3.4. Numerical illustration

Theorem 3.1 partially explains a numerical observation we now report. We implemented the -DPG method by setting the parameter (see § 2.4) and computed . In analogy with (32), define the discretization errors and by and Although Theorem 3.1 suggests an investigation of

due to the difficulty of applying the extension operator in practice, we have investigated the ratio as a function of . Recall that is the best approximation error defined in (34), so measures how close the discretization errors are to the best possible.

For a range of wavenumbers , we chose the data so that the exact solution to (13) on the unit square would be , with . Each resulting boundary value problem was then solved using the -DPG method with , on a fixed mesh of and the corresponding discretization errors were collected.

The resulting ratios are plotted as a function of in Figure 2 for a few values. First of all, observe that the graph of the ratio begins close to the optimal value of one for all values in the figure. Next, observe that the ratio spikes up as approaches the exact resonance value , where is infinity. It is interesting to look at the points near (but not at) the resonance. Observe that as is decreased, the DPG method exhibits a “regularizing” effect at points near the resonance: E.g., at , the values of are closer to for smaller . It therefore seems advantageous to use smaller for problems near resonance.

The theoretical explanation for this numerical observation would be complete (by virtue of Theorem 3.1), if we had computed using the exact DPG test spaces (), instead of the inexactly computed spaces (). Certain discrete effects arising due to this inexact computation of test spaces will be presented in a later section.

4. Lowest order stencil

We now consider the example of square two-dimensional elements. The lowest order case of the DPG method is obtained using is constant on each edge of , is linear on each edge of , and is continuous on . Let and are constants (vector and scalar, resp.) functions on . We consider the DPG method (with ) using the lowest order global trial space

where for all mesh elements and for all mesh elements .

Let denote the indicator function of an edge . If denotes a vertex of the square element , let denote the bilinear function that equals one at and equals zero at the other three vertices of . Let . The collection of eight functions of the form and , one for each vertex, and one for each edge of , forms a basis for . We distinguish between the horizontal and vertical edges, because the unknowns there approximate different components of the velocity . Accordingly, we will denote by the indicator function of a horizontal edge and by the indicator function of a vertical edge.

The local element DPG matrix is defined using a basis for and . (While a basis for is obtained as mentioned above, a basis for is trivially obtained by three indicator functions.) If we enumerate the 11 basis functions as , , then the element DPG matrix is defined by

| (36) |

where is as defined in (19). Since this matrix depends on and , we will write . In our computations, we do not use any specialized basis for to compute the action of , so to overcome round-off problems due to ill-conditioned local matrices, we resorted to high precision arithmetic for these local computations.

To show how can be computed by mapping, let . For any square of side length , there is a translation vector such that the For any (scalar or vector) function v on , let on be the mapped function obtained by . Let us denote the matrix computed using (36), but using the mapped basis functions on , by . Then by a change of variables, it is easy to see that

| (37) |

Thus we may compute local DPG matrix by scaling the DPG matrix on the fixed reference element obtained using the normalized wavenumber and scaling parameter . It is enough to compute the element matrix using high precision arithmetic for the ensuing dispersion analysis.

Next, we eliminate the three interior variables of and consider the condensed element stiffness matrix for the variables in . At this stage it will be useful to classify these eight variables (unknowns) into three categories: (1) Unknowns at vertices (which are the coefficients multiplying the basis function ) denoted by “ ”, (2) unknowns on horizontal edges (coefficients multiplying ) denoted by “ ”, and (3) unknowns on vertical edges (coefficients multiplying the corresponding ) denoted by “ ”. The normal vectors on all horizontal and vertical edges are fixed to be and , respectively, corresponding to the direction of the above-indicated arrows.

Now suppose the mesh is a uniform mesh of congruent square elements. Assembling the above-described condensed element matrices on such a mesh, we obtain a global system where the interior variables are all condensed out. The resulting equations can be represented using the stencils in Figure 3. A row of the matrix system corresponding to an unknown of the type “ ”, connects to unknowns of the same type at other vertices, as well as unknowns of the other two types, as shown in the 21-point stencil in Figure 3(a). Similarly, the unknowns of the type “ ” and “ ” connect to other unknowns in the 13-point stencils depicted in Figures 3(b) and 3(c), respectively. These stencils will form the basis of our dispersion analysis next.

5. Dispersion analysis

This section is devoted to a numerical study of the DPG method with , by means of a dispersion analysis. The dispersion analysis is motivated by [13]. Details on dispersion analyses applied to standard methods can be found in [1] and the extensive bibliography presented therein.

5.1. The approach

To briefly adapt the approach of [13] to fit our context, we consider a general method for the homogeneous Helmholtz equation on an infinite uniform lattice . Suppose the method has different types of nodes on this lattice, some falling in between the lattice points, each corresponding to a different type of variable, with its own stencil (and hence its own equation). All nodes of the type are assumed to be of the form where lies in an infinite subset of . The solution value at a general node of the type is denoted by . Note that methods with multiple solution components are accommodated using the above mentioned node types.

The stencil, centered around , consists of a finite number of nodes, some of which belong to the stencil, and the remaining belong to other stencils. Suppose we have finite index sets , for each , such that all the nodes of the stencil centered around can be listed as with the understanding that is a node of type whenever . This allows interaction between variables of multiple types. Every node in has a corresponding stencil coefficient (or weight) denoted by . Due to translational invariance, these weights do not change if we place the stencil at another center node , hence the numbers do not depend on the center index .

We obtain the method’s equation at a general node of the type by applying the stencil centered around to the solution values , namely

| (38) |

Note that we have set all sources to zero to get a zero right hand side in (38).

Plane waves, , are exact solutions of the Helmholtz equation with zero sources (and are often used to represent other solutions). Here the wave vector is of the form for some representing the direction of propagation. The objective of dispersion analysis is to find similar solutions of the discrete homogeneous system. Accordingly, we set in (38), the ansatz

| (39) |

where and is an arbitrary complex number associated to the variable type. We want to find such discrete wavenumbers satisfying (38).

To this end, we must solve (38) after substituting (39) therein, namely

| (40) |

for all . Multiplying by , we remove any dependence on . Defining the matrix by

we observe that solving (40) is equivalent to solving

| (41) |

This is the nonlinear equation we solve to obtain the discrete wavenumber corresponding to any given and .

5.2. Application to the DPG method

Next, we apply the above-described framework to the lowest order DPG stencil discussed in Section 4. Since there are three different types of stencils (see Figure 3), we have . The first type of unknowns, denoted by “ ”, represent the DPG method’s approximation to the value of at the nodes for all . The stencil of the first type is the one shown in Figure 3(a). The unknowns of the second type represent the method’s approximation to the vertical components of on the midpoints of horizontal edges, i.e., at all points in . These unknowns were previously denoted by “ ” and has the stencil portrayed in Figure 3(b). Similarly, the third type of stencil and unknown are as in Figure 3(c). To summarize, (39) in the lowest order DPG case, becomes

The condensed DPG matrices, discussed in Section 4, can be used to compute the stencil weights in each of the three cases, which in turn lead to the nonlinear system (41) for any given propagation angle .

We numerically solved the nonlinear system for , for various choices of (propagation angle), (enrichment degree), (scaling factor in the -norm), and (mesh size). The first important observation from our computations is that the computed wavenumbers are complex numbers. They lie close to in the complex plane. The small but nonzero imaginary parts of indicate that the DPG method has dissipation errors, in addition to dispersion errors. The results are described in more detail below.

5.3. Dependence on

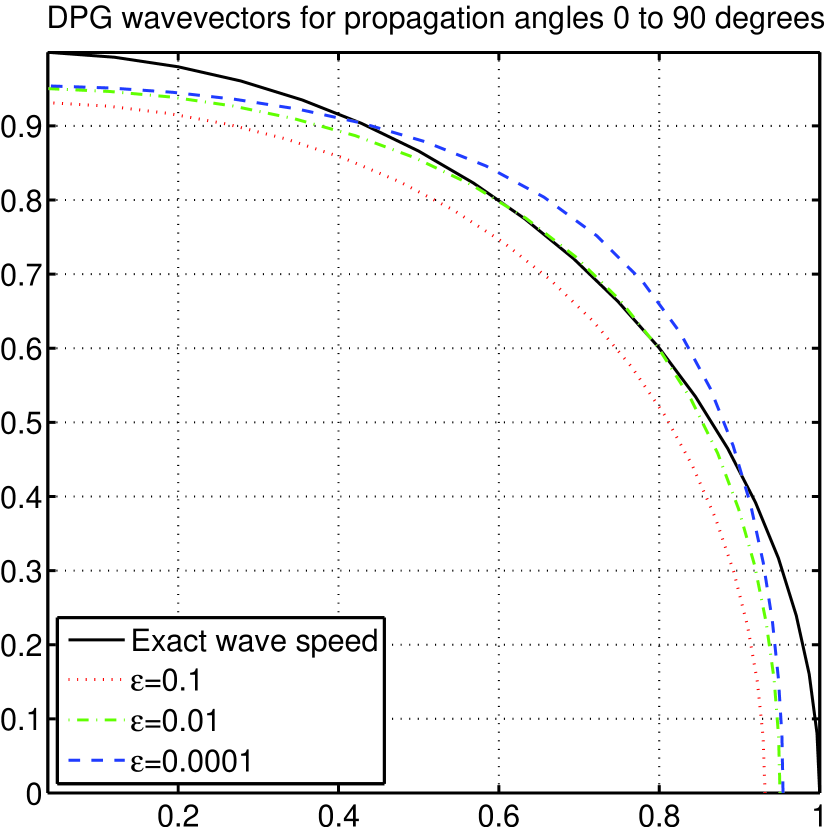

To understand how dispersion errors vary with propagation angle , we fix the exact wave number appearing in the Helmholtz equation to (so the wavelength is ) and examine the computed for each .

One way to visualize the results is through a plot of the corresponding discrete wavevectors vs. for every propagation direction . Due to symmetry, we only need to examine this plot in the region . We present these plots for the case in Figure 4. We fix . (This corresponds to four elements per wavelength if the propagation direction is aligned with a coordinate axis.) In Figure 4(a), we plot the curve traced out by the endpoints of the discrete wavevectors . We see that as decreases, the curve gets closer to the (solid) circle traced out by the exact wavevector . This indicates better control of dispersive errors with decreasing (cf. Theorem 3.1).

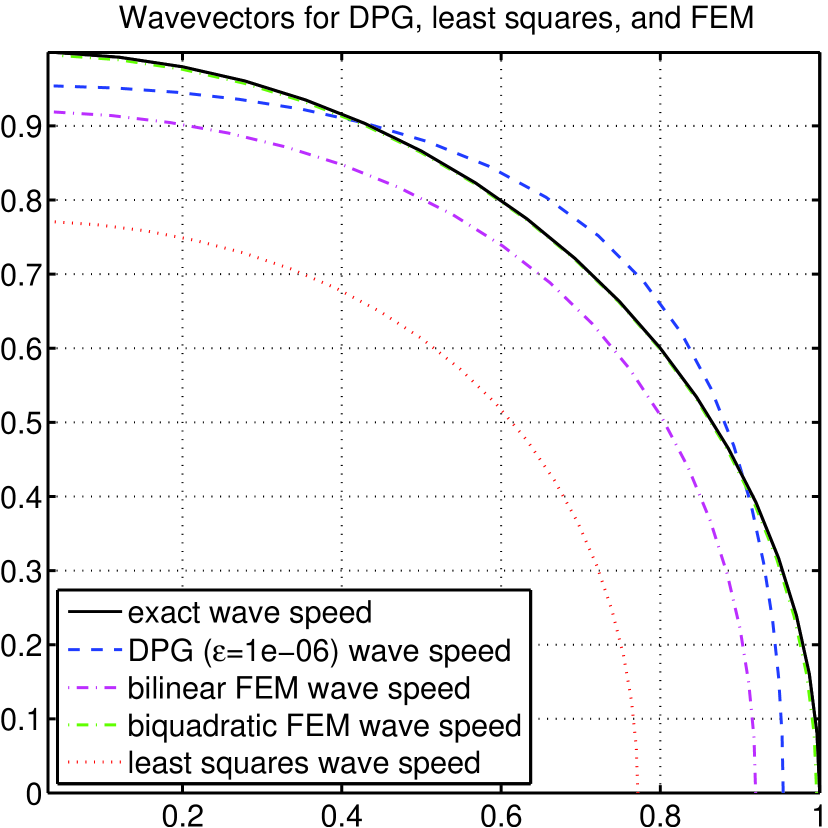

In Figure 4(b), we compare the obtained using the lowest order DPG method with the discrete wavenumbers of the standard lowest order (bilinear) finite element method (FEM). Clearly the wavespeeds obtained from the DPG method are closer to the exact than those obtained by bilinear FEM. However, since the lowest order DPG method has a larger stencil than bilinear FEM, one may argue that a better comparison is with methods having the same stencil size. We therefore compare the DPG method with two other methods which have exactly the same number of points in their stencil: (i) The biquadratic FEM, which after condensation has three stencils of the same size as the lowest order DPG method, and (ii) the conforming first order least-squares method using the lowest order Raviart-Thomas and Lagrange spaces (which has no interior nodes to condense out). While the wavespeeds from the DPG method did not compare favorably with the biquadratic FEM of (i), we found that the DPG method performs better than the least-squares method in (ii).

5.4. Dependence on and

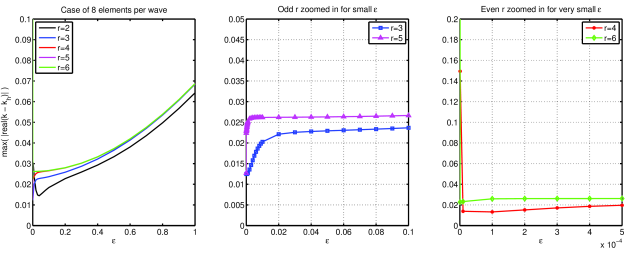

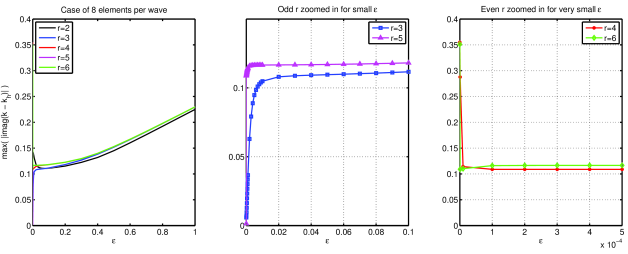

We have seen in Figure 4 that the discrete wavespeed is a function of the propagation angle . We now examine the maximum discrepancy between real and imaginary parts of and over all angles. Accordingly, define

The former indicates dispersive errors while the latter indicates dissipative errors. Fixing and (so that there are about eight elements per wavelength), we examine these quantities as a function of and in Figure 5. The first of the plots in Figures 5(a) and 5(b) show that the errors decrease as decreases from 1 to about 0.1. In view of Theorem 3.1, we expected this decrease.

However, the behavior of the method for smaller is curious. In the remaining plots of Figure 5 we see that when is odd, the errors continue to decrease for smaller , while for even , the errors start to increase as . This suggests the presence of discrete effects due to the inexact computation of test functions. We do not yet understand it enough to give a theoretical explanation.

5.5. Dependence on

Now we examine how depends on . First, let us note that the matrix in (41) only depends on . (This can be seen, for instance, from (37) and noting how the stencil weights depend on the entries of .) Hence, we will study how depends on the normalized wavenumber , restricting ourselves to the case of .

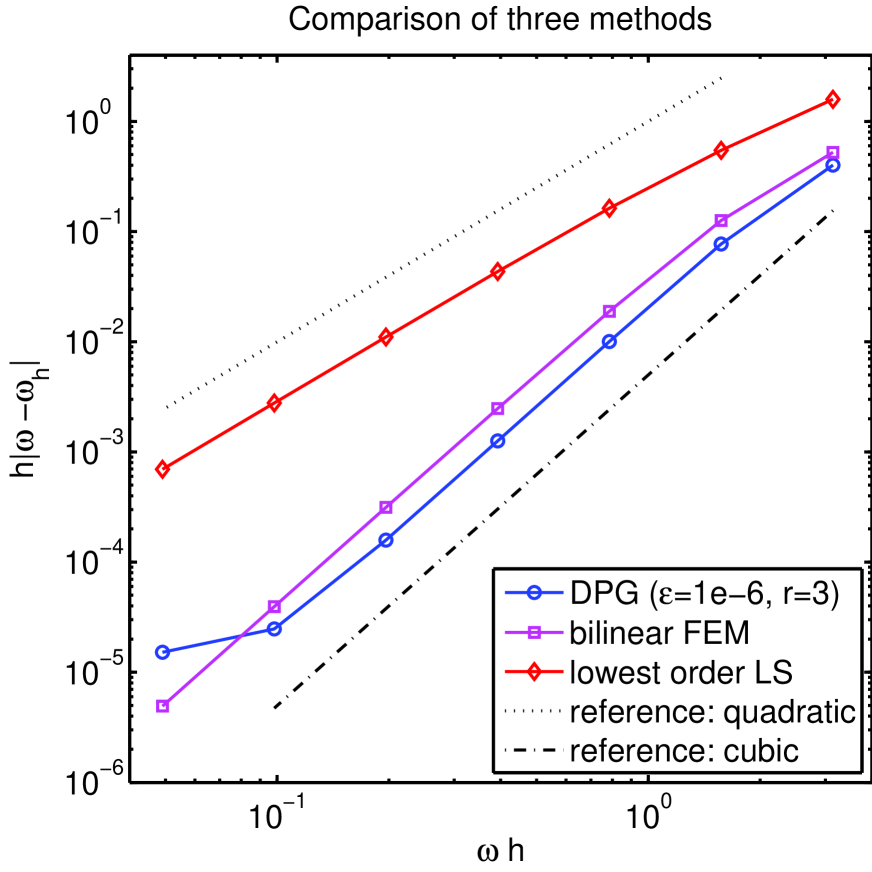

In Figure 6(a), we plot (in logarithmic scale) the absolute value of vs. for the standard bilinear FEM, the lowest order least-squares method (marked LS), and the DPG method with . We observe that while appears to decrease at for the least squares method, it appears to decrease at the higher rate of for the FEM and DPG cases considered in the same graph. For easy reference, we have also plotted lines indicating slopes corresponding to and decrease, marked “quadratic” and “cubic”, resp., in the same graph.

Note that a convergence rate of implies that the difference between discrete and exact wave speeds goes to zero at the rate

This shows the presence of the so-called [2] pollution errors: For instance, as increases, even if we use finer meshes so as to maintain fixed, the error in wave speeds will continue to grow at the rate of . Our results show that pollution errors are present in all the three methods considered in Figure 6(a). The difference in convergence rates, e.g., whether converges to zero at the rate or at the rate becomes important, for example, when trying to answer the following question: What should we use to obtain a fixed error bound for for all frequencies ? While methods with convergence rate would require , methods with convergence rate would only require .

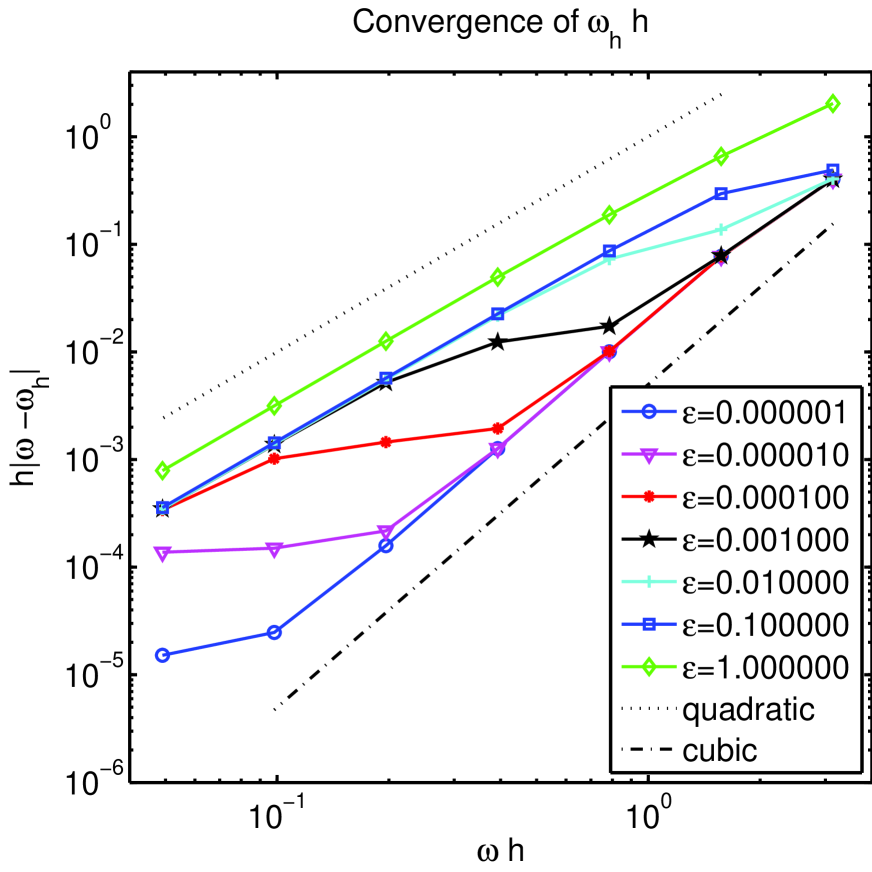

Next, consider Figure 6(b), where we observe interesting differences in convergence rates within the DPG family. While the DPG method for exhibits the same quadratic rate of convergence as the least-squares method, we observe that a transition to higher rates of convergence progressively occur as is decreased by each order of magnitude. The case shows a rate virtually indistinguishable from the cubic rate in the considered range. The convergence behavior of the DPG method thus seems to vary “in between” those of the least-squares method and the standard FEM as is decreased. The values of considered in these plots are for , which cover the numbers of elements per wavelength in usual practice.

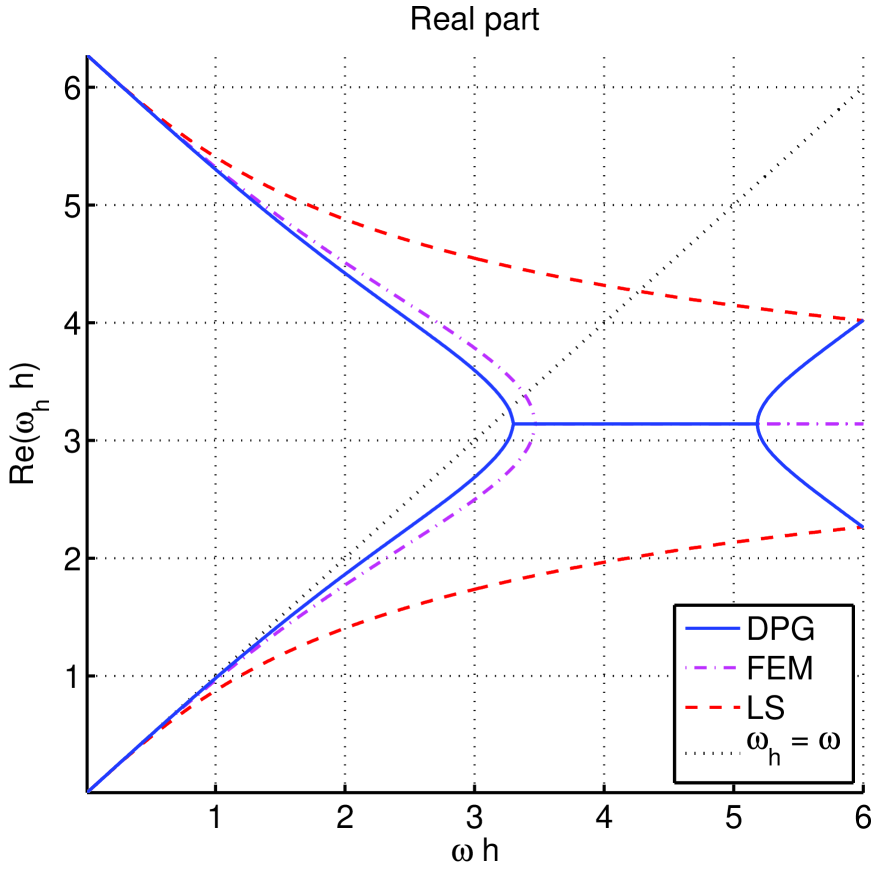

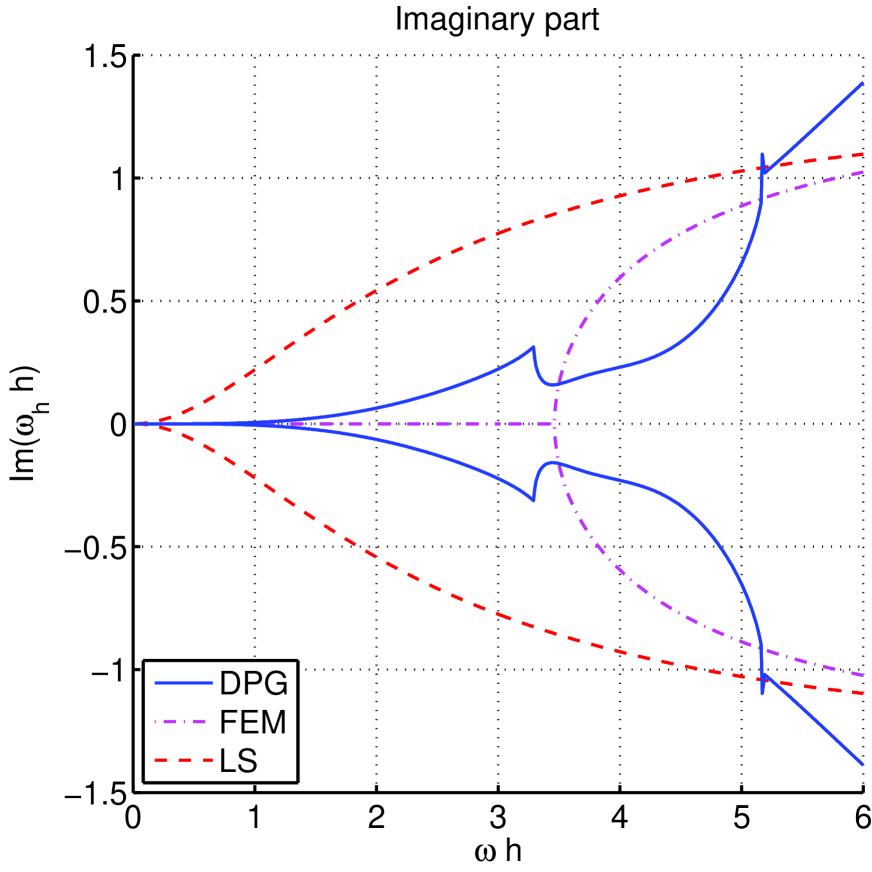

Next, we consider a wider range of following [21], where such a study was done for standard finite elements, separating the real and imaginary parts of . Our results for the case of are collected in Figure 7. To discuss these results, let us first recall the behavior of the standard bilinear finite element method (whose discrete wavenumbers are also plotted in dash-dotted curve in Figure 7). From its well-known dispersion relation (see e.g, [1]), we observe that if solves the dispersion relation, then also solves it. Accordingly, the plot in Figure 7(a) is symmetric about the horizontal line at height . Furthermore, as already shown in [21], is real-valued in the range . The threshold value was called the “cut-off” frequency. (Note that in the regime , we have less than two elements per wavelength. Note also that .) As can be seen from Figures 7(a) and 7(b), in the range , the bilinear finite elements yield with a constant real part of and nonzero imaginary parts of increasing magnitude.

We observed a somewhat similar behavior for the DPG method – see the solid curves of Figure 7, which were obtained after calculating explicitly using the computer algebra package Maple, for the lowest order DPG method, setting and . The major difference between the DPG and FEM results is that from the DPG method was not real-valued even in the regime where FEM wavenumbers were real. It seems difficult to define any useful analogue of the cut-off frequency in this situation. Nonetheless, we observe from Figures 7(a) and 7(b) that there is a segment of constant real part of value , before which the imaginary part of is relatively small. As the number of mesh elements per wavelength increases (i.e., as becomes smaller), the imaginary part of becomes small. We therefore expect the diffusive errors in the DPG method to be small when is small. Finally, we also conclude from Figure 7 that both the dispersive and dissipative errors are better behaved for the DPG method when compared to the least-squares method.

6. Conclusions

We presented and analyzed the -DPG method for the Helmholtz equation. The case was analyzed previously in [12]. The numerical results in [12] showed that in a comparison of the ratio of norms of the discretization error to the best approximation error is compared, the DPG method had superior properties. The pollution errors reported in [12] for a higher order DPG method were so small that its growth could not be determined conclusively there. In this paper, by performing a dispersion analysis on the DPG method for the lowest possible order, we found that the method has pollution errors that asymptotically grow with at the same rate as other comparable methods.

In addition, we found both dispersive and dissipative type of errors in the lowest order DPG method. The dissipative errors manifest in computed solutions as artificial damping of wave amplitudes (e.g., as illustrated in Figure 1).

Our results show that the DPG solutions have higher accuracy than an -based least-squares method with a stencil of identical size. However, the errors in the (lowest order) DPG method did not compare favorably with a standard (higher order) finite element method having a stencil of the same size. Whether this disadvantage can be offset by the other advantages of the DPG methods (such as the regularizing effect of , and the fact that it yields Hermitian positive definite linear systems and good gradient approximations) remains to be investigated.

We provided the first theoretical justification for considering the -modified DPG method. If the test space were exactly computed, then Theorem 3.1 shows that the errors in numerical fluxes and traces will improve as . However, if the test space is inexactly computed using the enrichment degree , then the numerical results from the dispersion analysis showed that errors continually decreased as was decreased only for odd . A full theoretical explanation of such discrete effects and the limiting behavior when is deserves further study.

References

- [1] M. Ainsworth. Discrete dispersion relation for -version finite element approximation at high wave number. SIAM J. Numer. Anal., 42(2):553–575 (electronic), 2004.

- [2] I. M. Babuška and S. A. Sauter. Is the pollution effect of the FEM avoidable for the Helmholtz equation considering high wave numbers? SIAM Rev., 42(3):451–484 (electronic), 2000.

- [3] P. B. Bochev and M. D. Gunzburger. Least-squares finite element methods, volume 166 of Applied Mathematical Sciences. Springer, New York, 2009.

- [4] J. H. Bramble, T. V. Kolev, and J. E. Pasciak. A least-squares approximation method for the time-harmonic Maxwell equations. J. Numer. Math., 13(4):237–263, 2005.

- [5] J. H. Bramble, R. D. Lazarov, and J. E. Pasciak. A least-squares approach based on a discrete minus one inner product for first order systems. Math. Comp., 66(219):935–955, 1997.

- [6] T. Bui-Thanh, L. Demkowicz, and O. Ghattas. A unified discontinuous Petrov-Galerkin method and its analysis for Friedrichs’ systems. ICES report, 2011.

- [7] Z. Cai, R. Lazarov, T. A. Manteuffel, and S. F. McCormick. First-order system least squares for second-order partial differential equations. I. SIAM J. Numer. Anal., 31(6):1785–1799, 1994.

- [8] L. Demkowicz and J. Gopalakrishnan. A class of discontinuous Petrov-Galerkin methods. Part I: The transport equation. Computer Methods in Applied Mechanics and Engineering, 199:1558–1572, 2010.

- [9] L. Demkowicz and J. Gopalakrishnan. Analysis of the DPG method for the Poisson equation. SIAM J Numer. Anal., 49(5):1788–1809, 2011.

- [10] L. Demkowicz and J. Gopalakrishnan, A class of discontinuous Petrov-Galerkin methods. Part II: Optimal test functions, Numerical Methods for Partial Differential Equations, 27 (2011), pp. 70–105.

- [11] L. Demkowicz, J. Gopalakrishnan, and A. Niemi. A class of discontinuous Petrov-Galerkin methods. Part III: Adaptivity. Applied Numerical Mathematics, 62:396–427, 2012.

- [12] L. Demkowicz, J. Gopalakrishnan, I. Muga, and J. Zitelli. Wavenumber explicit analysis for a DPG method for the multidimensional Helmholtz equation. Computer Methods in Applied Mechanics and Engineering, 213-216:126–138, March 2012.

- [13] A. Deraemaeker, I. Babuška, and P. Bouillard. Dispersion and pollution of the FEM solution for the Helmholtz equation in one, two and three dimensions. International Journal for Numerical Methods in Engineering, 46:471–499, 1999.

- [14] G. J. Fix and M. D. Gunzburger. On numerical methods for acoustic problems. Comput. Math. Appl., 6(2):265–278, 1980.

- [15] J. Gopalakrishnan and W. Qiu. An analysis of the practical DPG method. Math. Comp, to appear.

- [16] F. Ihlenburg. Finite element analysis of acoustic scattering, volume 132 of Applied Mathematical Sciences. Springer-Verlag, New York, 1998.

- [17] B.-n. Jiang. The least-squares finite element method. Scientific Computation. Springer-Verlag, Berlin, 1998. Theory and applications in computational fluid dynamics and electromagnetics.

- [18] B. Lee. First-order system least-squares for elliptic problems with Robin boundary conditions. SIAM J. Numer. Anal., 37(1):70–104 (electronic), 1999.

- [19] B. Lee, T. A. Manteuffel, S. F. McCormick, and J. Ruge. First-order system least-squares for the Helmholtz equation. SIAM J. Sci. Comput., 21(5):1927–1949, 2000.

- [20] J. M. Melenk. On Generalized Finite Element Methods. PhD thesis, University of Maryland, 1995.

- [21] L. L. Thompson and P. M. Pinsky. Complex wavenumber Fourier analysis of the p-version finite element method. J. Computational Mechanics, 13(4):255–275, 1994.