Assessing Relative Volatility/Intermittency/Energy Dissipation111Has appeared in Electronic Journal of Statistics 8(2), 1996–2021 (2014). This version contains an application to electricity prices (Appendix D) that was omitted from the published version.

Abstract

We introduce the notion of relative volatility/intermittency and demonstrate how relative volatility statistics can be used to estimate consistently the temporal variation of volatility/intermittency when the data of interest are generated by a non-semimartingale, or a Brownian semistationary process in particular. This estimation method is motivated by the assessment of relative energy dissipation in empirical data of turbulence, but it is also applicable in other areas. We develop a probabilistic asymptotic theory for realised relative power variations of Brownian semistationary processes, and introduce inference methods based on the theory. We also discuss how to extend the asymptotic theory to other classes of processes exhibiting stochastic volatility/intermittency. As an empirical application, we study relative energy dissipation in data of atmospheric turbulence.

Keywords: Brownian semistationary process, energy dissipation, intermittency, power variation, turbulence, volatility.

2010 Mathematics Subject Classification: 62M09 (Primary), 76F55 (Secondary)

1 Introduction

The concept of volatility expresses the ubiquitous phenomenon that observational fields exhibit more variation than expected; that is, more than the most basic type of random influence222Often thought of as Gaussian. envisaged.

Accordingly, volatility is a relative concept, and its meaning depends on the particular setting under investigation. Once that meaning is clarified the question is how to assess the volatility empirically and then to describe it in stochastic terms and incorporate it in a suitable probabilistic model.

The ‘additional’ random fluctuations denoted as volatility/intermittency, generally vary, in time and/or in space, in regard to Intensity (activity rate and duration) and Amplitude. Typically the volatility/intermittency may be further classified into continuous and discrete (i.e., jumps) elements, and long and short term effects.

In turbulence and certain other areas of study the phenomenon is refered to as intermittency (Frisch, 1995, Chapter 8) rather than volatility. Energy dissipation is a key concept in the statistical theory of turbulence, and is in the character of a specific type of intermittency.

In finance the investigation of volatility is well developed and many of the procedures of probabilistic and statistical analysis applied (Barndorff-Nielsen and Shephard, 2010) are similar to those of relevance in turbulence.

In this paper, we introduce the notion of relative volatility/intermittency and the closely related statistics, realised relative power variations. They pave the way for practical applications of some recent advances in the asymptotic theory of power variations of non-semimartingales (see, e.g., Corcuera et al. (2006) and Barndorff-Nielsen et al. (2011, 2013)) to volatility/intermittency measurements and inference with empirical data.

In the non-semimartingale setting, realised power variations need to be scaled properly, in a way that depends on the smoothness of the process through unknown parameters, to ensure convergence. Realised relative power variations, however, are self-scaling and, moreover, admit a statistically feasible central limit theorem, which can be used, e.g., to construct confidence intervals for the realised relative volatility/intermittency. (Self-scaling statistics have also been recently used by Podolskij and Wasmuth (2013) to construct a goodness-of-fit test for the volatility coefficient of a fractional diffusion.)

This paper is organised as follows. Section 2 presents some results from the theory of Brownian semistationary processes that are pertinent to assessment of volatility/intermittency, and the definitions of relative volatility/intermittency and realised relative power variations are given in Section 3. A stable functional central limit theorem for realised relative power variations of Brownian semistationary processes is presented in Section 4. An application to empirical data on atmospheric turbulence is carried out in Section 5, and Section 6 concludes. Appendices contain a discussion of extending the theory beyond Brownian semistationary processes (Appendix A), an alternative method of assessing the volatility/intermittency of a Brownian semistationary process (Appendix B), some supporting results (Appendix C), and a preliminary analysis of electricity spot prices using the methodology of the paper (Appendix D).

2 Brownian semistationary processes and realised volatility/intermittency

2.1 Probabilistic setup

Brownian semistationary () processes, introduced by Barndorff-Nielsen and Schmiegel (2009), may be used as models of timewise development of homogeneous and isotropic turbulent velocity fields. More concretely, a process can be used to describe the velocity at a fixed point in space and in the main direction of the flow in a turbulent field. While the original motivation for processes arose out of a study in turbulence, these processes have since found widespread interest in regard to their theoretical properties and to applications beyond physics, including, e.g., modelling of electricity price dynamics (Barndorff-Nielsen et al., 2013).

A generic process is defined on a complete filtered probability space via the decomposition

| (2.1) |

where the process

| (2.2) |

is constructed from a standard Brownian motion and a non-zero333More precisely, a.e. sample path is not equal to zero on a set with positive Lebesgue measure. càglàd volatility/intermittency process , both of which are adapted to , and using a square integrable kernel such that

for all . This condition ensures the existence of the stochastic integral in (2.2). In the decomposition (2.1), is a process that allows for skewness in the distribution of . The process is assumed to fulfill one of two negligibility conditions, viz. (2.7) and (4.3) given below (Appendix C presents more concrete criteria that can be used to check these conditions).

Example 2.1.

In the context of turbulence, the gamma kernel

| (2.3) |

where , , and , has a special role. In particular, if and is stationary with , then the autocorrelation function of is identical to von Kármán’s autocorrelation function (von Kármán, 1948) for ideal turbulence and also belongs to the Whittle–Matérn family of correlation functions (Guttorp and Gneiting, 2005). The parameter value agrees with Kolmogorov’s (K41) scaling law of turbulence (Kolmogorov, 1941a, b).

Example 2.2.

The process can be specified as

| (2.4) |

where the kernel belongs to , which makes the integral in (2.4) convergent under the assumption . In particular, can be chosen to be of the gamma form (2.3). Lemma C.1 in Appendix C provides sufficient conditions for the process to be negligible in the sense of conditions (2.7) and (4.3) when is a gamma kernel.

2.2 Assessing volatility/intermittency

In relation to the process , a central question is that of determining the dynamics of volatility/intermittency from . If were a semimartingale and of finite variation, then the answer would be given by the quadratic variation of . In fact, if

| (2.5) |

then is a semimartingale with for any , where

is the accumulated volatility/intermittency (Barndorff-Nielsen and Schmiegel, 2009). Assuming normalisation , given a set of equidistant discrete observations of at time points , where , the accumulated volatility can then be estimated consistently as the limit in probability for of the realised quadratic variation

More generally, the volatility/intermittency functional for any can be estimated consistently as using the realised -th order power variation

| (2.6) |

rescaled by , where with , see Barndorff-Nielsen et al. (2006).

Whenever the process is not identically equal to zero, the condition (2.5) is both sufficient and necessary for to be a semimartingale. However, in many interesting situations (2.5) does not hold and thus is not a semimartingale. They include the case where is a gamma kernel with , which is of interest for turbulence. Then, in order to determine by a limiting procedure from the realised quadratic variation the latter has to be rescaled by a factor depending on and the scaling properties of . Specifically, as shown by Barndorff-Nielsen and Schmiegel (2009), the appropriate scaling can be described using the second-order structure function (or variogram)

of the Gaussian core of defined by , .

Let us now recall the general version of the law of large numbers for power variations of processes, due to Barndorff-Nielsen et al. (2011). To this end, we need to introduce some conditions concerning the kernel and the volatility/intermittency process . Below stands for a function that is slowly varying at zero, indexed by a given function . Recall that slow variation at zero requires that for any .

Assumption 2.3.

For some , the kernel and the process satisfy:

-

(i)

.

-

(ii)

and for any . Moreover, is non-decreasing on for some .

-

(iii)

a.s. for any .

Moreover, the second-order structure function satisfies:

-

(iv)

.

-

(v)

.

-

(vi)

For some ,

Example 2.4.

Remark 2.5.

Under Assumption 2.3, the process is not a semimartingale, unless is identically equal to zero. The parameter describes the smoothness of the process and is analogous to the Hurst parameter of fractional Brownian motion. In fact, the increments of the Gaussian core over short time intervals are ‘close’ to increments of fractional Brownian motion with Hurst parameter , see Corcuera et al. (2013, p. 2557).

The following statement is a special case of Theorem 3 of Barndorff-Nielsen et al. (2011) that provides a law of large numbers for multipower variations of processes.

Theorem 2.6.

Remark 2.7.

Assumption 2.3 (iv) implies, by Potter’s bounds for slowly varying functions (Bingham et al., 1987, Theorem 1.5.6), that for any and there exist , such that

| (2.8) |

for any . Then, the negligibility condition (2.7) holds if

for any . Another consequence of (2.8) is that under the assumptions of Theorem 2.6 the ‘raw’ realised quadratic variation satisfies

(In the critical case the limit of is indeterminate, unless we have more information on the slowly varying part of the structure function near zero.)

3 Realised relative volatility/intermittency

3.1 Consistent estimation of relative volatility/intermittency

Using Theorem 2.6 for estimation of the accumulated volatility requires knowledge of the scaling factor . More precisely, the behaviour of the second-order structure function near zero should be known or determinable from data with sufficient accuracy. We discuss the viability of estimation of the scaling factor in Appendix B.

However, instead of the precise of value of for fixed , we are often more interested in measuring the dynamics of , as a function of , in relative terms. That is, for we are interested in the relative volatility/intermittency process

which captures the variation of in but loses the original scale of measurement. Clearly, under the assumptions of Theorem 2.6, we may estimate consistently using the realised relative quadratic variation of ,

that is, as . The realised relative quadratic variation is entirely empirically determined, self-scaling, and its consistency does not require information on the second-order structure function .

More generally, for any , the relative volatility/intermittency functionals

| (3.1) |

can be estimated consistently using the realised -th order relative power variations

as outlined in the following result.

Theorem 3.1.

3.2 Connection to relative energy dissipation in turbulence

Let us briefly consider the interpretation of relative volatility/intermittency from the point of view of physics. In the classical theory of turbulence (see, e.g., Frisch, 1995), velocity fields are assumed to be differentiable — that is, in place of a process we would consider a differentiable function describing the velocity component in the main direction of the flow. Then, for , the surrogate energy dissipation of at time is defined as

and the coarse-grained energy dissipation of over the interval as

Using the mean value theorem, it is easy to show that the realised quadratic variation of , viz. , is connected to via the convergence

Thus, we find that the realised relative quadratic variation satisfies

where the limit is the relative energy dissipation of over the subinterval of . Within the turbulence literature, this definition of the relative energy dissipation is strongly related to the definition of a multiplier in the cascade picture of the transport of energy from large to small scales (see Cleve et al. (2008) and references therein).

Motivated by this discussion, in the turbulence context we interpret as the relative energy dissipation of over .

4 Central limit theorem for realised relative power variations

4.1 Stable convergence

We are about to derive a stable central limit theorem for realised relative power variations of processes. To this end, recall first that random elements in some metric space converge stably (in law) to a random element in , defined on an extension of the underlying probability space , if

for any bounded, continuous function and bounded random variable on . We write then . Stable convergence, introduced by Rényi (1963), is stronger than ordinary convergence in law and weaker than convergence in probability. It is essential to note that the limiting random element is defined on an extension of the original probability space. In fact, when is -measurable, the convergence is equivalent to (Podolskij and Vetter, 2010, Lemma 1).

Remark 4.1.

The usefulness of stable convergence can be illustrated by the following example that is pertinent to the asymptotic results below. Suppose that in , where and is a positive random variable independent of . In other words, follows asymptotically a mixed Gaussian law with mean zero and conditional variance . If is a positive, consistent estimator of , i.e., , then the stable convergence of allows us to deduce that . We refer to Rényi (1963), Aldous and Eagleson (1978), Jacod and Shiryaev (2003, pp. 512–518), and Podolskij and Vetter (2010, pp. 332–334) for more information on the properties of stable convergence.

4.2 Stable functional central limit theorem

As a preparation for the stable central limit theorem for realised relative power variations, we recall the stable central limit theorem for realised power variations of processes, due to Barndorff-Nielsen et al. (2011). As usual, the central limit theorem requires somewhat stronger assumptions than the corresponding law of large numbers (Theorem 2.6). In particular, we need to control the Hölder regularity of the volatility/intermittency process as follows.

Assumption 4.2.

There exists a constant such that for any and ,

where is a constant that may depend on and .

In what follows, we write for the space of càdlàg functions from to , endowed with the usual Skorohod metric (Jacod and Shiryaev, 2003, Chapter V). (Recall, however, that convergence to a continuous function in this metric is equivalent to uniform convergence.) We also introduce a function given by

| (4.1) |

where are the coefficients in the expansion of the function , , in second and higher-order Hermite polynomials , satisfying (in the case we have, clearly, and for all ). The sequence is the correlation function of fractional Gaussian noise with Hurst parameter , namely

| (4.2) |

Theorem 4.3.

Remark 4.4.

Remark 4.5.

Building on Theorem 4.3, we can prove the following stable central limit theorem for realised relative power variations of .

Theorem 4.6.

Theorem 4.6 follows from Theorem 4.3 by invoking the following simple result concerning the stable convergence of a process that has been normalised by its terminal value.

Lemma 4.7.

Let be fixed and suppose that:

-

•

, for any , is a process defined on with non-decreasing sample paths in such that a.s.,

-

•

is a process defined on with non-decreasing sample paths in such that a.s.,

-

•

is a process defined on an extension of with sample paths in .

If

| (4.6) |

then

Proof.

Since and have non-decreasing sample paths and the sample paths of are continuous, we have

by (4.6). Due to the properties of stable convergence, we obtain then

| (4.7) |

Let us now consider the decomposition

Using again the fact that convergence to a continuous function in is equivalent to uniform convergence, it follows that the map from to is continuous on . Since and have continuous sample paths, the assertion follows from (4.7) and the properties of stable convergence. ∎

For practical applications, we need a statistically feasible version of Theorem 4.6. Conditional on , the limiting process on the right-hand side of (4.5) is a Gaussian bridge. In particular, its (unconditional) marginal law at time is mixed Gaussian with mean zero and conditional variance

| (4.8) |

To be able to estimate the conditional variance (4.8), we need a consistent estimator of the factor that depends on the smoothness parameter . To this end, the following fact is crucial.

Lemma 4.8.

The function is continuous.

Proof.

It suffices to show that is continuous on for any . Applying the mean value theorem twice to (4.2), we can show that there is a constant such that for any and . Thus for any the function is continuous on , by Lebesgue’s dominated convergence theorem. Moreover, since and , we have for any and ,

The continuity of follows then by applying Lebesgue’s dominated convergence theorem to the outer sum in (4.1) (recall that ). ∎

Barndorff-Nielsen et al. (2011, 2013) and Corcuera et al. (2013) have developed estimators of , based on the observations , that are consistent as . Using such an estimator, Lemma 4.8, and the properties of stable convergence, we obtain a feasible central limit theorem for realised relative power variations.

Proposition 4.9.

4.3 Inference on relative volatility/intermittency

Proposition 4.9 can be used to construct approximative, pointwise confidence intervals for the relative volatility/intermittency . Since, by construction, assumes values in , it is natural to constrain the confidence interval to be a subset of . Thus, we define for any the corresponding confidence interval as

where is the -quantile of the standard Gaussian distribution.

Another application of the central limit theory is a non-parametric homoskedasticity test that is similar in nature to the classical Kolmogorov–Smirnov and Cramér–von Mises goodness-of-fit tests for empirical distribution functions. This extends the homoskedasticity tests proposed by Dette et al. (2006) and Dette and Podolskij (2008) to a non-semimartingale setting. Another extension of these tests to non-semimartingales, namely fractional diffusions, is given by Podolskij and Wasmuth (2013). The approach is also similar to the cumulative sum of squares test (Brown et al., 1975) of structural breaks studied in time series analysis literature. To formulate our test, we introduce the hypotheses

As mentioned above, Theorem 4.6 implies that under ,

| (4.9) |

The distance between the realised relative power variation and the linear function can be measured using various norms and metrics. Here, we consider the typical sup and norms that correspond to the Kolmogorov–Smirnov and Cramér–von Mises test statistics, respectively. More precisely, we define the statistics

| (4.10) | ||||

where is any consistent estimator of . Under , these statistics have the classical Kolmogorov–Smirnov and Cramér–von Mises limiting distributions, respectively, as outlined in the following result.

Proposition 4.10.

Suppose that the assumptions of Theorem 4.6 hold. Then, under ,

| (4.11) | ||||

| (4.12) |

where is a standard Brownian bridge, independent of the filtration . Moreover, under , both and diverge to infinity as .

Proof.

Remark 4.11.

Remark 4.12.

The finite-sample performance of the test statistics and is explored in a separate paper (Bennedsen et al., 2014a).

5 Application to turbulence data

We apply the methodology developed above to empirical data of turbulence. The data consist of a time series of the main component of a turbulent velocity vector, measured at a fixed position in the atmospheric boundary layer using a hotwire anemometer, during an approximately 66 minutes long observation period at sampling frequency of 5 kHz (i.e. 5000 observations per second). The measurements were made at Brookhaven National Laboratory (Long Island, NY), and a comprehensive account of the data has been given by Drhuva (2000).

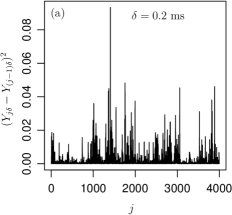

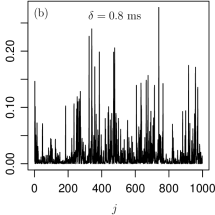

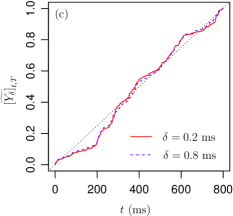

As a first illustration, we study the observations up to time horizon milliseconds. Using the smallest possible lag, ms, this amounts to 4000 observations. Figure 1(a) displays the squared increments corresponding to these observations. As a comparison, the same time horizon is captured in Figure 1(b) but with lag ms. Figure 1(c) compares the associated accumulated realised relative energy dissipations/quadratic variations. The graphs for these two lags show very similar behaviour, exhibiting how the total time interval is divided into a sequence of intervals over which the slope of the energy dissipation is roughly constant. On the other hand, the amplitudes of the volatility/intermittency are of the same order in the whole observation interval.

To be able to draw inference on relative volatility/intermittency using the data, we need to address two issues. Firstly, for this time series, the lags ms and ms are below the so-called inertial range of turbulence, where a process with a gamma kernel, a model of ideal turbulence, provides an accurate description of the data—see Corcuera et al. (2013), where the same data are analysed. Secondly, the data were digitised using a 12-bit analog-to-digital converter. Thus, the measurements can assume at most different values, and due to the resulting discretisation error, a non-negligible number of increments are in fact equal to zero (roughly 20 % of all increments). These discretisation errors are bound to bias the estimation of the parameter , which is needed for the inference methods. We mitigate these issues by subsampling, namely, we apply the inference methods using a considerably longer lag, ms, which is near the lower bound of the inertial range for this time series (Corcuera et al., 2013, Figure 1).

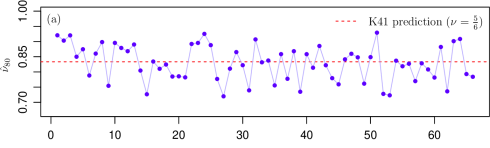

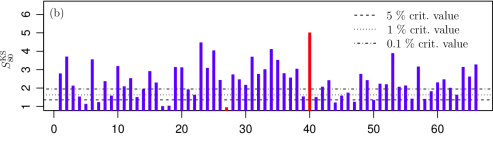

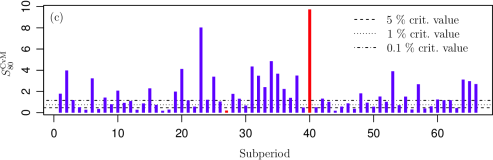

We divide the time series into 66 non-overlapping one-minute-long subperiods, testing the constancy of , i.e., the null hypothesis , within each subperiod. Figure 2(a) displays the estimates of for each subperiod using the change-of-frequency method (Barndorff-Nielsen et al., 2013; Corcuera et al., 2013). All of the estimates belong to the interval and they are scattered around the value predicted by Kolmogorov’s (K41) scaling law of turbulence (Kolmogorov, 1941a, b). The homoskedasticity test statistics, for , and their critical values, derived using Proposition 4.10, in Figure 2(b) indicate that the null hypothesis of the constancy of is typically rejected. Moreover, the two variants, and lead to rather similar results.

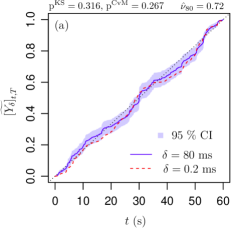

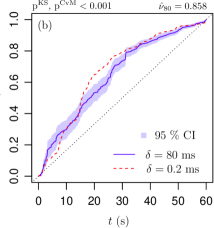

To understand what kind of intermittency the tests are detecting in the data, we look into two extremal cases, the 27th and 40th subperiods (the red bars in Figure 2(b) and (c)). To this end, we plot the realised relative energy dissipations, with ms, during the 27th and 40th subperiods in Figure 3(a) and (b), respectively. We also include the pointwise confidence intervals, the p-values of the homoskedasticity tests, and as a reference, the realised relative quadratic variations using the smallest possible lag ms. While the realised relative quadratic variations exhibit a slight discrepancy between the lags ms and ms, it is clear that 40th subperiod indeed contains significant intermittency, whereas during the 27th subperiod, the (accumulated) realised relative energy dissipation grows nearly linearly.

|

|

|

|

|

6 Conclusion

We have introduced the concept of relative volatility/intermittency and we have shown how relative volatility/intermittency can be assessed using realised relative quadratic variations in the context of non-semimartingale Brownian semistationary () processes. (Straightforward extensions of the methodology beyond processes are discussed in Appendix A.)

Realised relative quadratic variations are parameter-free statistics that provide estimates of the relative volatility/intermittency in subintervals of the full observation range, by relating the realised quadratic variation over each subinterval to the total realised quadratic variation for the entire range. They provide robust estimates of the relative accumulated volatility/intermittency as this develops over time and are intimately connected to the concept of relative energy dissipation in the statistical theory of turbulence. An extension to vector valued processes is an issue of interest, in particular in relation to the definition of the energy dissipation in three-dimensional turbulent fields.

Moreover, we have applied our estimation and inference methods to assess relative intermittency/energy dissipation in empirical data of atmospheric turbulence. In ongoing work (Bennedsen et al., 2014b), these methods are also being applied to volatility estimation with electricity price data, which exhibit non-negligible correlations in returns that can be successfully captured by models based on processes (Barndorff-Nielsen et al., 2013). See, however, Appendix D for a preliminary analysis of electricity spot prices using the methodology developed in this paper.

Acknowledgements

The authors would like to thank Mikkel Bennedsen and Mark Podolskij for valuable comments. M.S. Pakkanen acknowledges support from CREATES (DNRF78), funded by the Danish National Research Foundation, from the Aarhus University Research Foundation regarding the project “Stochastic and Econometric Analysis of Commodity Markets”, and from the Academy of Finland (project 258042).

Appendix A Relative volatility/intermittency in the context of fractional processes and beyond

We have introduced relative volatility/intermittency in the context of processes, but the concept has much wider applicability. The key asymptotic results for realised relative power variations, Theorems 3.1 and 4.6, can easily be generalised to other classes of processes. Indeed, Lemma 4.7 can take any stable444Stable convergence is crucial for the validity of Lemma 4.7. functional central limit theorem for power variations of some process (provided that the limiting process is continuous) as an ‘input’ to produce a ‘relative’ version of the result. As an example, we consider now briefly a generalisation to another class of non-semimartingales, namely fractional processes that are defined as integrals with respect to fractional Brownian motion. We also list below a number of other possible generalisations.

More concretely, let us consider a process given by

| (A.1) |

where is a fractional Brownian motion with Hurst parameter and is a volatility/intermittency process with finite -variation for some (we refer to Corcuera et al. (2006) for the definition of -variation). The integral in (A.1) is defined pathwise, in particular, it is not necessary to assume that is adapted to the natural filtration of . We could also add to a skewness term analogous to of (2.1), but for simplicity it is eschewed here.

Corcuera et al. (2006, Theorem 1) show that for any and , the -th power variation of satisfies

where . Thus, analogously to Theorem 3.1, we find that for any ,

uniformly in , where

Further, when , , and the sample paths of are -Hölder continuous with , it holds that (Corcuera et al., 2006, Theorem 4) for any ,

where is a standard Brownian motion independent of the natural filtration of . Using Lemma 4.7, we can then conclude that

in .

In addition to and fractional processes, relative volatility/intermittency statistics could be used in a similar vein at least in the following settings:

-

•

Power and multipower variations of continuous Itô semimartingales, based on the asymptotic theory developed by Barndorff-Nielsen et al. (2006). Also, the consistency of realised relative power variations of certain multifractal processes (Duvernet, 2010; Duvernet et al., 2010; Ludeña and Soulier, 2014), which are non-Itô semimartingales, could be shown.

-

•

Power variations of stochastic integrals with respect to symmetric -stable Lévy processes (Corcuera and Farkas, 2010).

- •

-

•

Power variations of two-parameter ambit fields driven by white noise, observed on a line segment (Barndorff-Nielsen and Graversen, 2011) or on a square lattice (Pakkanen, 2014). However, in these settings only consistency of realised relative power variations can be established using the currently available asymptotic theory.

Appendix B Estimating the scaling factor of realised quadratic variation

As seen in Sections 2 and 4, the asymptotic theory for power variations of the process requires a suitable scaling of the realised power variation by a factor that depends on the second-order structure function . We will now discuss whether the scaling factor can be estimated from the observed data, which would be an alternative to using relative volatility/intermittency statistics. For simplicity, we focus on quadratic variations, which are the most relevant in practical applications.

Assumption 2.3 postulates that behaves like as , apart from a slowly varying factor . If is ‘well-behaved’ and normalised in the sense that , then in Theorem 2.6 for the case the scaling factor can be replaced with , to wit,

| (B.1) |

for any . The condition holds, e.g., when is the gamma kernel (2.3) with and is chosen in a suitable way (Barndorff-Nielsen et al., 2011, p. 1173). If, additionally, as , which is again true in the aforementioned situation with of the gamma form, the convergence in the central limit theorem (Theorem 4.3) in the case can be simplified to

| (B.2) |

As shown by Barndorff-Nielsen et al. (2013) and Corcuera et al. (2013), the smoothness parameter can be estimated consistently in the infill asymptotic setting with an estimator with the usual rate of convergence . Then it is natural to ask, whether we can simply substitute with in (B.1) and (B.2) without affecting the asymptotic behaviour of the scaled realised quadratic variation. From the following result we learn that with the estimated scaling indeed attains consistency. However, the second-order behaviour is affected by the estimated scaling: the rate of convergence becomes slower and the asymptotic distribution is non-standard, due to the estimation error of . Similar results have been shown (under constant volatility) by Coeurjolly (2001, Proposition 4) in the context of fractional Brownian motion and by Brouste and Iacus (2013, Theorem 1) in the context of fractional Ornstein–Uhlenbeck processes.

Proposition B.1.

Proof.

(a) Let us write

where . By the condition (B.3), we find that

| (B.4) |

Thus, as , and the assertion follows then from (B.1).

(b) Let us consider the decomposition

where

By (B.2), we have clearly

Due to (B.1) and the properties of stable convergence, it suffices now to show that as . To this end, define , . Observe that

| (B.5) |

and in view of the condition (B.3) it remains to show that the second term on right-hand side of (B.5) converges to zero in probability as . To this end, let and consider

where by (B.4). Using the elementary inequality , valid when , we finally deduce that

since

which in turn is a simple consequence of the condition (B.3). ∎

Appendix C Sufficient conditions for the negligibility of the skewness term

This appendix provides some methods of checking the negligibility conditions (2.7) and (4.3) with some concrete specifications of the process .

Suppose first that the process is given by

where is a constant and the process is measurable and locally bounded. Then we can establish rather simple conditions for its negligibility in the asymptotic results for power variations. By Jensen’s inequality, we have for any , , and ,

where is a random variable that depends locally on the path of . Thus, we find that for any ,

as . Then, in view of Remarks 2.7 and 4.5 and the restriction , the condition (2.7) holds always and (4.3) holds provided that (which is always true if ).

Suppose now, instead, that follows

| (C.1) |

where is the gamma kernel

for some , , and . We assume that the process is measurable, locally bounded, and satisfies

| (C.2) |

for any , which is true, e.g., when the auxiliary process , , has a càdlàg or continuous modification.

Lemma C.1.

Proof.

Let us first look into the properties of . For the sake of simpler notation, we make the innocuous assumption that . Since

| (C.4) |

we find that is decreasing when . When , is increasing on and decreasing on .

Let be fixed, , and let be such that . Below, all big estimates hold uniformly in such . We consider the decomposition

where

When , is bounded and we have , where

and when , we find that

Next, we want to show that

| (C.5) |

In the case the derivative is bounded and (C.5) is immediate. Suppose that . Then, on any finite interval, where depends on the interval. Using the mean value theorem, we obtain

which implies (C.5). To bound , note that, by (C.4), for all , where is a constant. For any , we have . Thus, by the mean value theorem,

and, consequently,

Appendix D Application to electricity spot price data

We also briefly exemplify the concept of relative volatility using electricity spot price data from the European Energy Exchange (EEX). Specifically, we consider deseasonalised daily Phelix peak load data (that is, the daily averages of the hourly spot prices of electricity delivered between 8 am and 8 pm) with delivery days ranging from January 1, 2002 to October 21, 2008. Weekends are not included in the peak load data, and in total we have 1775 observations. This time series was studied in the paper by Barndorff-Nielsen et al. (2013) and the deseasonalisation method is explained therein. As usual, we consider here logarithmic prices.

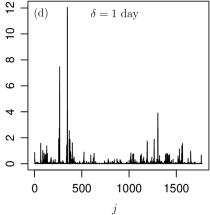

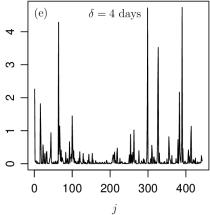

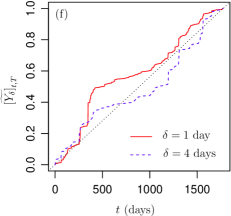

Figure 4(d) shows the squared increments up to the total time horizon days with lag day. The same time horizon is captured in Figure 4(e) but with a resolution days. Figure 4(f) compares the corresponding accumulated realised relative quadratic variations. The results for these two lags do not show the same similarity as with the turbulence data (Figure 1(a–b)). Judging by eye, we observe that the intensity of the volatility is changing with lag . This lag dependence is also observed in the amplitudes, again in contrast to the figures on the left hand side. (However, more quantitative investigation of such amplitude/density arguments is outside the scope of the present paper.) The dependence of the estimation results on the lag is, at least partly, explained by the relatively low sampling frequency of the data. With day, the increments are dominated by a few exceptional observations (which may correspond to jumps or intraday volatility bursts). Choosing days reduces the contribution of these observations since the time series exhibits significant first-order autocorrelation (Barndorff-Nielsen et al., 2013, Figure 1).

Remark D.1.

It was shown by Barndorff-Nielsen et al. (2013) that by suitably choosing both and to be of gamma type it is possible to construct a process with normal inverse Gaussian one-dimensional marginal law, which corresponds closely to the empirics for the time series of log spot prices considered. Moreover, the estimated value of the smoothness parameter for this time series falls in the interval .

References

- Aldous and Eagleson (1978) Aldous, D. J. and G. K. Eagleson (1978). On mixing and stability of limit theorems. Ann. Probability 6(2), 325–331.

- Anderson and Darling (1952) Anderson, T. W. and D. A. Darling (1952). Asymptotic theory of certain “goodness of fit” criteria based on stochastic processes. Ann. Math. Statistics 23, 193–212.

- Barndorff-Nielsen et al. (2013) Barndorff-Nielsen, O. E., F. E. Benth, and A. E. D. Veraart (2013). Modelling energy spot prices by volatility modulated Lévy-driven Volterra processes. Bernoulli 19(3), 803–845.

- Barndorff-Nielsen et al. (2011) Barndorff-Nielsen, O. E., J. M. Corcuera, and M. Podolskij (2011). Multipower variation for Brownian semistationary processes. Bernoulli 17(4), 1159–1194.

- Barndorff-Nielsen et al. (2013) Barndorff-Nielsen, O. E., J. M. Corcuera, and M. Podolskij (2013). Limit theorems for functionals of higher order differences of Brownian semistationary processes. In A. N. Shiryaev, S. R. S. Varadhan, and E. Presman (Eds.), Prokhorov and Contemporary Probability Theory, pp. 69–96. Berlin: Springer.

- Barndorff-Nielsen and Graversen (2011) Barndorff-Nielsen, O. E. and S. E. Graversen (2011). Volatility determination in an ambit process setting. J. Appl. Probab. 48A, 263–275.

- Barndorff-Nielsen et al. (2006) Barndorff-Nielsen, O. E., S. E. Graversen, J. Jacod, M. Podolskij, and N. Shephard (2006). A central limit theorem for realised power and bipower variations of continuous semimartingales. In Y. Kabanov, R. Liptser, and J. Stoyanov (Eds.), From stochastic calculus to mathematical finance, pp. 33–68. Berlin: Springer.

- Barndorff-Nielsen and Schmiegel (2009) Barndorff-Nielsen, O. E. and J. Schmiegel (2009). Brownian semistationary processes and volatility/intermittency. In H. Albrecher, W. Rungaldier, and W. Schachermayer (Eds.), Advanced financial modelling, Volume 8 of Radon Ser. Comput. Appl. Math., pp. 1–25. Berlin: Walter de Gruyter.

- Barndorff-Nielsen and Shephard (2010) Barndorff-Nielsen, O. E. and N. Shephard (2010). Volatility. In R. Cont (Ed.), Encyclopedia of Quantitative Finance, pp. 1898–1901. Chicester: Wiley.

- Bennedsen et al. (2014a) Bennedsen, M., A. Lunde, and M. S. Pakkanen (2014a). Discretization of Lévy semistationary processes with application to estimation. In preparation.

- Bennedsen et al. (2014b) Bennedsen, M., A. Lunde, and M. S. Pakkanen (2014b). Modelling energy prices by Brownian semistationary processes. In preparation.

- Bingham et al. (1987) Bingham, N. H., C. M. Goldie, and J. L. Teugels (1987). Regular variation. Cambridge: Cambridge University Press.

- Brouste and Iacus (2013) Brouste, A. and S. M. Iacus (2013). Parameter estimation for the discretely observed fractional Ornstein-Uhlenbeck process and the Yuima R package. Comput. Statist. 28(4), 1529–1547.

- Brown et al. (1975) Brown, R. L., J. Durbin, and J. M. Evans (1975). Techniques for testing the constancy of regression relationships over time. J. Roy. Statist. Soc. Ser. B 37, 149–192.

- Cleve et al. (2008) Cleve, J., J. Schmiegel, and M. Greiner (2008). Apparent scale correlations in a random multiplicative process. Eur. Phys. J. B 63, 109–116.

- Coeurjolly (2001) Coeurjolly, J.-F. (2001). Estimating the parameters of a fractional Brownian motion by discrete variations of its sample paths. Stat. Inference Stoch. Process. 4(2), 199–227.

- Corcuera and Farkas (2010) Corcuera, J. M. and G. Farkas (2010). Power variation for Itô integrals with respect to -stable processes. Stat. Neerl. 64(3), 276–289.

- Corcuera et al. (2013) Corcuera, J. M., E. Hedevang, M. S. Pakkanen, and M. Podolskij (2013). Asymptotic theory for Brownian semi-stationary processes with application to turbulence. Stochastic Process. Appl. 123(7), 2552–2574.

- Corcuera et al. (2006) Corcuera, J. M., D. Nualart, and J. H. C. Woerner (2006). Power variation of some integral fractional processes. Bernoulli 12(4), 713–735.

- Dette and Podolskij (2008) Dette, H. and M. Podolskij (2008). Testing the parametric form of the volatility in continuous time diffusion models—a stochastic process approach. J. Econometrics 143(1), 56–73.

- Dette et al. (2006) Dette, H., M. Podolskij, and M. Vetter (2006). Estimation of integrated volatility in continuous-time financial models with applications to goodness-of-fit testing. Scand. J. Statist. 33(2), 259–278.

- Drhuva (2000) Drhuva, B. R. (2000). An experimental study of high Reynolds number turbulence in the atmosphere. Ph. D. thesis, Yale University.

- Duvernet (2010) Duvernet, L. (2010). Convergence of the structure function of a multifractal random walk in a mixed asymptotic setting. Stoch. Anal. Appl. 28(5), 763–792.

- Duvernet et al. (2010) Duvernet, L., C. Y. Robert, and M. Rosenbaum (2010). Testing the type of a semi-martingale: Itō against multifractal. Electron. J. Stat. 4, 1300–1323.

- Frisch (1995) Frisch, U. (1995). Turbulence: The Legacy of A. N. Kolmogorov. Cambridge: Cambridge University Press.

- Guttorp and Gneiting (2005) Guttorp, P. and T. Gneiting (2005). On the Whittle–Matérn correlation family. Technical Report 080, The National Research Center for Statistics and the Environment, University of Washington.

- Jacod and Shiryaev (2003) Jacod, J. and A. N. Shiryaev (2003). Limit theorems for stochastic processes (Second ed.). Berlin: Springer.

- Kolmogorov (1941a) Kolmogorov, A. N. (1941a). Dissipation of energy in locally isotropic turbulence. Dokl. Akad. Nauk SSSR 32, 19–21.

- Kolmogorov (1941b) Kolmogorov, A. N. (1941b). The local structure of turbulence in incompressible viscous fluids. Dokl. Akad. Nauk SSSR 30, 301–305.

- Lehmann and Romano (2005) Lehmann, E. L. and J. P. Romano (2005). Testing statistical hypotheses (Third ed.). New York: Springer.

- Ludeña and Soulier (2014) Ludeña, C. and P. Soulier (2014). Estimating the scaling function of multifractal measures and multifractal random walks using ratios. Bernoulli 20(1), 334–376.

- Pakkanen (2014) Pakkanen, M. S. (2014). Limit theorems for power variations of ambit fields driven by white noise. Stochastic Process. Appl. 124(5), 1942–1973.

- Podolskij and Vetter (2010) Podolskij, M. and M. Vetter (2010). Understanding limit theorems for semimartingales: a short survey. Stat. Neerl. 64(3), 329–351.

- Podolskij and Wasmuth (2013) Podolskij, M. and K. Wasmuth (2013). Goodness-of-fit testing for fractional diffusions. Stat. Inference Stoch. Process. 16(2), 147–159.

- Rényi (1963) Rényi, A. (1963). On stable sequences of events. Sankhyā Ser. A 25, 293 302.

- von Kármán (1948) von Kármán, T. (1948). Progress in the statistical theory of turbulence. J. Marine Res. 7, 252–264.