Rate-optimal Bayesian intensity smoothing for inhomogeneous Poisson processes

Abstract

We apply nonparametric Bayesian methods to study the problem of estimating the intensity function of an inhomogeneous Poisson process. To motivate our results we start by analysing count data coming from a call centre which we model as a Poisson process. This analysis is carried out using a certain spline prior. This prior is based on B-spline expansions with free knots, adapted from well-established methods used in regression, for instance. This particular prior is computationally feasible. Theoretically, we derive a new general theorem on contraction rates for posteriors in the setting of intensity function estimation which can be applied not just to this spline prior but also to a large number of other commonly used priors. Practical choices that have to be made in the construction of our concrete spline prior, such as choosing the priors on the number and the locations of the spline knots, are based on these theoretical findings. The results assert that when properly constructed, our approach yields a rate-optimal procedure that automatically adapts to the regularity of the unknown intensity function.

Keywords: Adaptive estimation; Bayesian nonparametric estimation; Contraction rate; Markov chain Monte Carlo; Poisson process; Splines.

1 Introduction

Poisson processes have a long-standing history and are some of the most widely used processes in statistics to study temporal and spacial count data, in diverse fields such as communication, meteorology, seismology, hydrology, astronomy, biology, medicine, actuary sciences and queueing, among others. In this paper we focus on inhomogenous Poisson processes on the real line with periodic intensity functions, which are models for count data in settings with a natural periodicity. We obtain asymptotic results as the number of observed periods goes to infinity but our approach is flexible enough to also deliver asymptotic results for estimating an intensity function on a compact in terms the either the number of observed events or in terms of the scale of the intensity function.

Nonparametric Bayesian methods, which are used more and more in many different statistical settings, have so far only been used on a limited scale to analyze such models. From the applied perspective they can be attractive for making inference about intensity functions, for the same reasons they are appealing in other situations. Estimating the intensity essentially requires some form of smoothing of the count data, and a nonparametric Bayesian approach can provide a natural way of achieving this. Using hierarchical priors we can automatically achieve a data-driven selection of the degree of smoothing. Moreover, Bayesian methods provide a way to quantify the uncertainty about the intensity using the spread of the posterior distribution. A typical implementation provides a computational algorithm that can generate a large number of (approximate) draws from the posterior. From this it is usually straightforward to construct numerical credible bands or credible sets.

The relatively small number of papers using nonparametric Bayesian methodology for intensity function smoothing have explored various possible prior distributions on intensities. An early reference is Møller et al. (1998), who consider log-Gaussian priors. Other papers employing Gaussian process priors, combined with suitable link functions, include Adams et al. (2009) and Palacios & Minin (2013). Kottas & Sansó (2007) consider kernel mixtures priors; see also the related paper DiMatteo et al. (2001), in which count data is analysed using spline-based priors.

The cited papers show that nonparametric Bayesian inference for inhomogenous Poisson processes can give satisfactory results in various applications. On the theoretical side however the existing literature provides no performance guarantees in the form of consistency theorems or related results. It is by now well known that nonparametric Bayes methods may suffer from inconsistency, even when seemingly reasonable priors are used (e.g. Diaconis & Freedman 1986). The purpose of this paper is therefore to propose a Bayesian approach to nonparametric intensity smoothing that is both computationally feasible and at the same time theoretically underpinned by results on consistency and related issues like convergence rates and adaptation to smoothness. Such theoretical results have in the last decade been obtained for various statistical settings, including density estimation, regression, classification, drift estimation for diffusions, etcetera (see e.g. Ghosal 2010 for an overview of some of these results). Until now, intensity estimation for inhomogenous Poisson processes has remained largely unexplored.

As motivation and starting point for the paper we consider the problem of analysing count data from a call center. The same type of data were analyzed by frequentist methods in the paper Brown et al. (2005). We revisit the problem using a nonparametric Bayesian method employing a spline-based prior on the unknown intensity function. In addition to a single estimator of the intensity, this method provides credible bounds indicating the degree of uncertainty. In Section 3 we study theoretical properties of our procedure, namely consistency, posterior contraction rates and adaptation to smoothness. The results show that we have set up our procedure in such a way that we obtain consistent, rate-optimal estimation of the intensity and that the method adapts automatically to the unknown smoothness of the intensity curve, up to the level of the order of the splines that are used. Section 4 concludes with some remarks and directions for further research.

2 Analysis of call center data

2.1 Data and statistical model

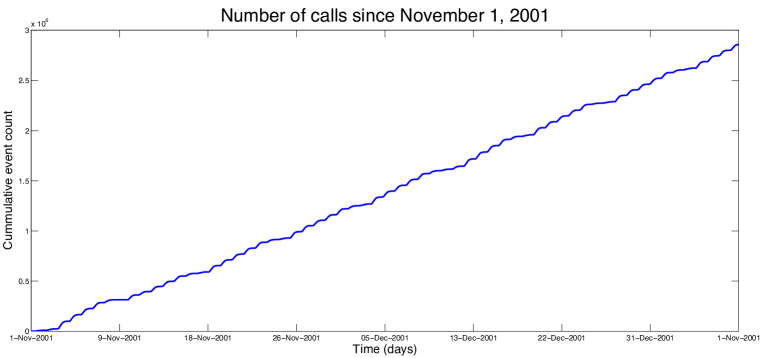

The approach we propose and study is motivated by the wish to analyse a dataset consisting of counts of telephone calls arriving at a certain call center. The dataset was obtained from the website of the S.E.E. Center (http://ie.technion.ac.il/Labs/Serveng/) of the Faculty of Industrial Engineering and Management, Technion in Haifa, Israel. It consists of counts for calls arriving at a bank’s 24 hour a day call center in the United States of America. We considered the records for the period from November 1, 2001 until December 31, 2001, covering a total of about 2.8 million incoming phone calls. These events are recorded in 30 second intervals with an average of about 32 calls per minute. The raw data are plotted in Figure 1.

We model the full count data as the realization of an inhomogenous Poisson process with an intensity function that is periodic, the period being hours (Daley & Vere-Jones 1988). This Poisson assumption is natural and is investigated in some detail in Brown et al. (2005), who could not find significant evidence to the contrary in a similar dataset (same kind of data, but over a different time interval). See also Belitser et al. (2013), who study the periodicity in the data.

This dataset is known to exhibit periodicity on different time scales; (approximate) daily, weekly, monthly and yearly periodicities seem to be present in the data. Different time scales are relevant if one would like to take analyze the intensity of the call traffic during, say, the weekends, holidays or specific times of the year. (To analyze the intensity of calls during weekends, for example, a weekly time scale would be appropriate.) By carrying out our estimation procedure under the assumption of daily periodicity we are in fact estimating the average daily call intensity between November 1, 2001 and December 31, 2001. Our study of the data over 24 hour intervals (the smallest time interval over which there is evidence of periodicity; cf. Figure 2) is motivated by the fact that the volume of calls in the dataset is already quite high even over individual days.

Let be the number of days for which we have data () and let be the period ( hours). Then the full call arrival counting process is given by , where is the number of calls arriving in the time interval . The Poisson assumption means that for every , the number of arrivals is independent of the history up till time and that is has a Poisson distribution with mean

We will assume throughout that is at least a continuous function. The periodicity assumption then means that is a -periodic function, i.e. for all . For we define the counting process by

i.e. counts the number of arrivals during day . Note that by the independence of the increments of the process , the processes are independent inhomogenous Poisson processes which have the restriction of to as intensity function.

Our goal is to make inference about this function. Note that we do not observe the full process . We only observe it at discrete times, namely every seconds. On average about calls arrive in a second time interval, so we really only see aggregated counts. Let be the time between observations ( seconds) and let be the number of counts per day that we have in our dataset ( in our case). Then for every and , the number of arrivals

| (1) |

in the th time interval on day has a Poisson distribution with parameter

| (2) |

We denote the total available count data by . It follows that the likelihood is given by

| (3) |

The case of discretized data is more relevant from the practical point of view. In the following section we describe a prior one may place on the intensity function .

2.2 Prior on the intensity function

There are different possible choices of priors for the function . A number of options considered earlier in the literature were already mentioned in the introduction (Gaussian processes, kernel mixtures, splines). The particular prior we apply in this paper to illustrate our results is motivated by the desire to have a computationally manageable procedure on the one hand and theoretical performance guarantees on the other. Still there will conceivably be more than one sensible choice meeting these requirements. In this section we restrict our efforts to the investigation of a specific spline-based prior which is described in detail in this section. We would like to clarify that we use this particular prior due to its computational simplicity and to illustrate our results from Section 3. Our theoretical results are more general and in fact cover this spline prior as a particular case.

More precisely we will employ a certain free-knot spline prior which is similar to priors considered earlier in different contexts (see for instance Smith & Kohn 1996; Denison et al. 1998; DiMatteo et al. 2001, or, more recently Sharef et al. 2010 and the references therein). Such priors have proven to be numerically attractive and capable of capturing abrupt changes in functions of interest. This last point is relevant for our particular application, since we expect fluctuations during the day due to the varying activity of businesses over the day. Recently, several theoretical results were derived for spline-based priors in various setting as well (e.g. Ghosal et al. 2000, 2008; De Jonge & van Zanten 2012; Belitser & Serra 2013). We will show in the next section that the procedure that we construct and implement has several desirable theoretical properties.

Background information on splines can be found, for example, in de Boor (2001) or Schumaker (2007). Let us fix some notations and terminology. A function is called a spline of order , with respect to a certain partition of its support, if it is times continuously differentiable and when restricted to each interval in the partition, it coincides with a polynomial of degree at most . Now consider . For any , such that let . We will refer to a vector as a sequence of inner knots.

A vector induces the partition of , with and . For , we denote by the linear space of splines of order on with simple knots (see the definition of simple knots in, e.g., Schumaker (2007)). This space has dimension and admits a basis of B-splines . The construction of involves the knots , with arbitrary extra knots and . Usually one takes and , and we adopt this choice as well. For and we denote by the spline in that has coefficient vector relative to the basis , i.e.

To define our prior on we first fix the order of the splines that we use (cubic splines are popular, they correspond to the choice ) and the minimum and maximum intensities . Then a draw from the prior is constructed as follows:

-

1.

(Number of B-splines): Draw according to a shifted Poisson distribution with mean .

-

2.

(Location of the knots): Given , construct a regular -spaced grid in . Then uniformly at random, choose grid elements (without replacement) to form a sequence of inner knots .

-

3.

(B-spline coefficients): Also given , and independent of the previous step, draw a vector of independent, uniform -distributed B-spline coefficients.

-

4.

(Random spline): Finally, construct the random spline of order corresponding to the inner knots and with B-spline coefficient vector .

The specific choices made in the construction of the prior, like the Poisson distribution on , choosing the knots uniformly at random from a grid, etcetera, are motivated by the optimality theory that we derive in Section 3. The theory shows that there is some more flexibility, but for choices too far from the ones proposed above the performance guarantees brake down. Technically, the prior on is the measure on the space of continuous functions on given by the law, or distribution of the random spline described above. The splines in are times continuously differentiable, hence in this sense the choice of determines the regularity of the prior. We will see in the next section that it also determines the maximal degree of smoothness of the true underlying intensity to which our procedure can adapt. In applications like the one we are interested in here, a sensible choice of the parameters and will typically be suggested by the average number of counts per time unit in the data. The construction of the grid in step 2. is non-standard compared to other spline-based priors proposed in the literature. It is motivated by recent work of Belitser & Serra (2013) and will allow us to derive desirable theoretical properties in the next section.

2.3 Posterior inference

For the data described in Section 2.1, with likelihood (3), and the spline prior described in Section 2.2, we implemented an MCMC procedure to sample from the corresponding posterior distribution of the intensity function of interest. The minimal and maximal intensity parameters and were set to and , respectively. These numbers were motivated by the range of the data (time is measured in hours). We took the order of the splines equal to 4.

Since our prior is very similar to the ones used previously in for instance DiMatteo et al. (2001) or Sharef et al. (2010) in regression or hazard rate estimation settings, our computational algorithm is a rather straightforward adaptation of existing methods. A generic state of the chain is a -dimensional vector where , is the model index, is a vector of inner knots and is a vector of B-spline coordinates. Together, these index a spline . We will abbreviate the corresponding posterior distribution by . Since the splines involved are easy to evaluate and integrate we can compute the likelihood, and then the posterior, up to the normalization constant, without any approximations being needed.

We consider four different types of moves for the MCMC chain, namely: a) perturbing the coefficients, b) moving the location of one knot, c) birth of a new knot and d) death of an existing knot. Each of these moves is proposed, independently and respectively, with probabilities , , and where for each , . In fact, we start by picking as parameters of the algorithm; if is the mean of the prior on , then we take , and, for , and . This choice results in if , if , if .

When perturbing the coefficients we perform simple (Gaussian) random walk MCMC steps; the standard deviation of the random walk was chosen such that we obtained an acceptance rate of roughly 23% for this type of move, as prescribed in Gelman et al. (1997). Let be the joint density of i.i.d. standard normal random variables. Our proposals correspond to a move which we accept with probability , with

Moving a knot is also straightforward; one of the current knots, say , is picked uniformly at random among those in and we propose to change its location depending on how many of its neighboring position on the -spaced grid are free – we say that two knots are neighbors if . This means that we propose a move where and differ only at the -th position: if has two free neighboring positions, then it moves to either of them with equal probability ; if only has one free neighboring position, then, with equal probability , it either moves to this free position or it does not move at all; if has no free neighboring positions then if does not move, with probability . These particular choices assure the reversibility of the moves. We accept such a proposal with probability where is given by

Birth moves and death moves, where a new knot is respectively added and removed, are reverse moves of one another and so we will outline only how to perform the birth move. We propose a move where we add a new knot to the vector and a new coefficient to the vector . In doing so, a new B-spline is introduced to the B-spline basis and a new B-spline coefficient is generated. The new knot vector contains all knots from rounded to the closest grid point on a spaced grid with the extra knot then picked uniformly at random among the remaining free positions; call it . Note that this construction does not prevent two knots in from occupying the same position; such knot vectors have posterior probability 0, though, so that the probability of moving to such a state is zero. The coefficients on this basis are then picked as where will be linear and invertible, and is a random seed, a normally distributed random number with mean , to be picked later, and variance 1. The new knot will belong to the support of B-splines, namely the -th through -th B-splines and we pick the index in depending on the knot’s position within the interval ; namely , where is the largest integer smaller or equal to . The mean of the random seed will be picked as a weighted mean of the coefficients , namely, , where the weights are normalized and

With probability we make the move , with and , where

where is the Jacobian of the linear mapping described before.

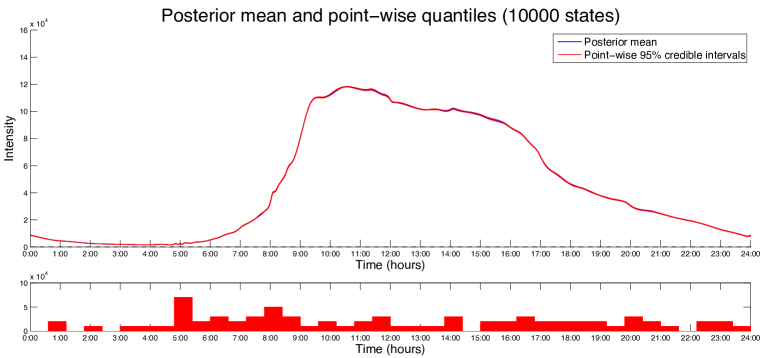

Figure 2 summarizes the outcome of the analysis. In the top panel it shows the posterior and 95% point-wise credible intervals, based on 10,000 samples from posterior. The lower panel shows a histogram for the locations of the knots corresponding to the samples from the chain used to generate the top panel. Note that as expected, relatively many knots are placed in periods in which there are relatively many fluctuations in the intensity.

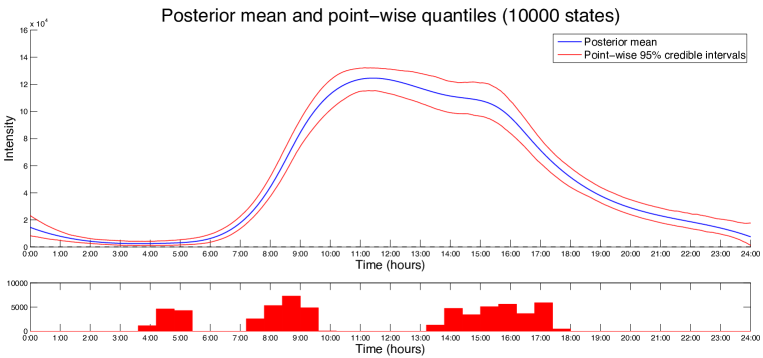

Due to the large event rate (almost million counts in total), the credible bands are very narrow. To illustrate the dependence on the amount of data we ran the analysis again with a thinned out dataset. We randomly removed counts, retaining about counts. The same analysis then leads to the posterior plot given in Figure 3. In this case, the uncertainty in the posterior distribution becomes clearly visible.

We find that the prior that we defined in Section 2.2 is a computationally feasible choice for nonparametric Bayesian intensity smoothing in the context of this kind of periodic count data. In the next section we analyze its fundamental theoretical performance. See in particular Theorem 3 in Section 3.2.

3 Theoretical results

3.1 Contraction rates for general priors

We derive our theoretical results for the particular prior we used in the Section 2 from general rate of contraction results that we present in this section. These are in the spirit of the general theorems about convergence rates of nonparametric Bayes procedures that were first developed for density estimation (Ghosal et al. 2000) and later for various other statistical settings; see for instance van der Meulen et al. (2006), Ghosal & van der Vaart (2007), Panzar & van Zanten (2009). Here we complement this literature with general rate results regarding intensity estimation for inhomogenous Poisson processes. These results are not only applicable to the spline priors we consider in this paper, but may also be used to analyze contraction rates of other priors. Moreover, we formulate the theorems not just for the case that we have discrete observations of aggregated data, as in our data example, but also for the case that the full counting process is observed.

The setting is as in Section 2.1. We fix a period . In the full observations case we assume that for , we observe an inhomogeneous Poisson process up till time , with a -periodic intensity function . Equivalently, we can say we observe independent inhomogeneous Poisson processes , indexed by , and with a common intensity function , which is a positive, integrable function on . It is well known that the law of under the intensity function is equivalent to the law of a standard Poisson process and that the corresponding likelihood is given by

| (4) |

(see for instance Jacod & Shiryaev 2003).

In the remainder of this section we will derive results will involve asymptotics in the number of observed periods . Alternatively, one could group the data and define a new Poisson process on ,

which is a Poisson process with intensity on . By identifying the function on with its periodical extension on , the likelihood of this process equals (4). If we assume that is (upper) bounded, the results from this section also imply asymptotics in terms of the number of events (or scale) of the intensity function . Asymptotics in the length of the trajectory of the process that is observed is a third equivalent formulation for our results.

We consider prior distributions that charge strictly positive, continuous functions. Given such a prior on (which we allow to depend on ) we can then compute the corresponding posterior distribution by Bayes’ formula

Formally we can view the prior as a measure on the space of all continuous, strictly positive functions on , endowed with its Borel -field. If we endow with the uniform norm, the likelihood is a continuous function on . Hence, the posterior is a well-defined measure on .

The following theorem considers the frequentist setting in which the data are assumed to be generated by an unknown, “true” intensity function . It gives conditions on the prior under which the posterior contracts around the true at a certain rate as the number of observed periods tends to infinity. The assumptions and conclusions of the theorem are formulated in terms of various distances on the intensity functions. For a continuous function on we define the norms and as usual by

For a set of positive continuous functions we write for its complement and . For and a norm on , let be the minimal number of balls of -radius needed to cover .

Theorem 1 (Contraction rate for full observations).

Assume that is bounded away from . Suppose that for positive sequences such that as , and constants it holds that for all , there exist subsets and a constant such that

| (5) | ||||

| (6) | ||||

| (7) |

Then for and all sufficiently large ,

| (8) |

as .

The proof of this theorem is given in Appendix A.1. The assumptions of the theorem parallel those of similar theorems obtained earlier for other settings including density estimation, regression, and classification. The first condition (5), the prior mass condition, requires that the prior puts sufficient mass near the truth. Conditions (6)–(7) together require that most of the prior mass, quantified in the sense of the remaining mass condition (6), is concentrated on sieves which are “small” in the sense of metric entropy, quantified by the entropy condition (7).

The condition requiring that be bounded away from zero, while needed in the proof, is essentially innocuous. Indeed, if this assumption does not hold (or if it is not know whether it holds), one might simply modify the Poisson data by adding to it an independently generated homogeneous Poisson process with intensity , say. The resulting data can be seen as a realization of a Poisson process with intensity (which is bounded away from zero by at least ) and Theorem 1 can be applied to it to make inference on and therefore on . This effectively allows us to make inference on intensities which are not bounded away from zero.

The proof of the theorem shows that conditions (6)–(7) can in fact be slightly weakened, at the cost of using more complicated distance measures on the intensities. The conditions in the theorem are more easy to work with when studying concrete priors and are expected to give sharp results in many cases. We note that if under the prior all intensities are bounded away from , then the set in (7) may be replaced by . Moreover, if all intensities are uniformly bounded by a common constant under the prior, then the square-root norm in (8) may be replaced by the -norm itself. In the next section we verify the conditions of the theorem for the spline priors used in Section 2.1.

In the case of discrete observations we only have access, for some and , to aggregated counts for and , given by (1). As before, we summarize these data using the notation . As explained in Section 2.1 the likelihood is in that case given by (3), where the ’s are defined as in (2). Consequently, the discrete-observations posterior is given by

In this case it is clear that we can not consistently identify the whole intensity function from the data, but only the integrals . In the following theorem, which deals with the convergence of the posterior distribution in the case of discrete observations, we therefore measure the convergence using a semi-metric that identifies intensity functions with the same integrals over time intervals in which we make observations. For , we define the distance by setting

The theorem has exactly the same assumptions on the prior as Theorem 1 above, but gives a contraction rate relative to the distance .

Theorem 2 (Contraction rate for discrete observations).

The proof of the theorem is given in Appendix A.2

In the next section we apply the theoretical results derived above to the spline prior considered before.

3.2 Contraction rates for the spline prior

Having the general rate of contraction results given by Theorems 1 and 2 at our disposal we can use them to study the performance of the spline-based prior defined in Section 2.2. We fix the order of the splines that are used. As before, let be the a full path up till time of an inhomogenous Poisson process with -period intensity and let be the discrete-time counts , with as in (1).

The contraction rate of the posterior will depend on the regularity of the true intensity function, measured in Hölder sense. For , let be the space of functions on with Hölder smoothness . (For the greatest integer strictly smaller than , having means that has derivatives and that the highest derivative is Hölder-continuous of order .)

Theorem 3 (Contraction rate for the spline prior).

Assume the true intensity function belongs to for some , and . Consider the prior constructed in Section 2.2. For all and all sufficiently large we have

and

as .

Note that up to a logarithmic factor, the rate of contraction in the theorem is the optimal rate for estimating an -regular function. Moreover, the prior does not depend on . Hence the procedure automatically adapts to the smoothness of the intensity function, up to the order of the splines that are used. This theorem deals with the case that we have known bounds and for the intensity. The existence lower bound is not restrictive since it can be enforced by adding a homogeneous Poisson process with known intensity to the data.

4 Concluding remarks

In this paper we work specific spline-based prior for doing nonparametric Bayesian intensity smoothing for inhomogeneous Poisson processes. We show that the method is both practically feasible and is underpinned by theoretical performance guarantees in the form of adaptive rate-optimality results.

Extensions of our results in several directions are possible. In particular, with more work it is possible to drop the assumption that we know an a-priori bound on the unknown intensity, which may be undesirable or impossible in certain situations. An obvious extension is then to put a prior on the bound. Computationally this makes the procedure more demanding, but numerical investigations indicate it is still feasible. Theoretical results can be obtained for that more general setting as well. Among other things this involves an extension of Lemma 1. Having a prior on the upper bound for may deteriorate the convergence rate however. We expect that the optimal rate will only be attained if the prior on the bound has sufficiently thin tails.

Another desirable theoretical extension would be to obtain “local” rate of convergence results. Our present results deal with global norms on the intensity functions. It is conceivable however that convergence is faster in regions where the intensity fluctuates relatively little, and faster in others. More work is necessary to derive theorems that describe this phenomenon.

Appendix A Proofs

A.1 Proof of Theorem 1

A useful observation is that we can view the statistical problem to which the theorem applies as a density estimation problem for functional data. Indeed, in the full observations case we observe a sample , which are independent, identically distributed random elements in the Skorohod space of càdlàg (right-continuous functions with left-hand limits) on (see Jacod & Shiryaev 2003, Chapter VI). Under the intensity function , the density of relative to the law of a standard Poisson process indexed by is given by

(e.g. Jacod & Shiryaev 2003, Chapter III). Hence, the density estimation results of Ghosal et al. (2000), Ghosal & van der Vaart (2001) apply in our case.

We want to apply Theorem 2.1 of Ghosal & van der Vaart (2001). This gives conditions for posterior contraction rates in terms of the Hellinger distance on densities and other, related distance measures. The Hellinger distance is in our case given by , where is the expectation corresponding to the probability measure under which the process is a Poisson process with intensity function . The other relevant distance measures are the Kullback-Leibler divergence between and and the related variance measure . For a Poisson process with intensity and a bounded, measurable function , we have

Using these relations it is straightforward to verify that we have

respectively.

The following lemma relates these statistical distances between densities to certain distances between intensity functions. We denote the minimum and maximum of two numbers and by and , respectively.

Lemma 1.

We have the inequalities

Proof.

The inequalities for follow from the fact that for .

For the Kullback-Leibler divergence we have

for . By Taylor’s formula, is bounded by a constant times in a neighborhood of . Since is bounded by for and as , we have in fact for all , say. For we have . It follows that

The first term on the right is bounded by . For the second term we note that for , we have and hence . The statement of the lemma follows.

To prove the last inequality, write as the sum of an integral over the set and an integral over the set and use the fact that for . ∎

To connect assumptions (5)–(7) to the corresponding assumptions of Theorem 2.1 of Ghosal & van der Vaart (2001) we first note that since is bounded away from and infinity by assumption, the same holds for any that is uniformly close enough to . The lemma and the definition of therefore imply that for uniformly close enough to , both and are bounded by a constant times the uniform norm . It follows that for large enough, the Kullback-Leibler-type ball

is larger than a multiple of the uniform ball . The lemma also implies that the covering number is bounded by . Hence, assumptions (5)–(7) imply that the conditions of Theorem 2.1 of Ghosal & van der Vaart (2001) are fulfilled. This theorem states that for large enough, . To complete the proof, note that by the fact that for large enough and the first inequality of the lemma, it holds, for large enough, that implies that .

A.2 Proof of Theorem 2

The proof is similar as the proof of Theorem 1, but this time we start from the observation that in the discrete-observations case, the data constitute a sample of independent, identically distributed random vectors in , where

and is given by (1). The coordinates of are independent Poisson variables with mean given by (2).

Again we apply Theorem 2.1 of Ghosal & van der Vaart (2001). In this case the Hellinger distance , Kullback Leibler divergence and variance measure are easily seen to be given by

respectively. These quantities satisfy the same bounds as in Lemma 1, but with the integrals replaced by the corresponding sums. Moreover, by expanding the square and using Cauchy-Schwarz we see that

and hence also

Using these relations the proof can be completed exactly as in Section A.1.

A.3 Proof of Theorem 3

Under the prior , the number of knots has, by construction, a shifted Poisson distribution. By Stirling’s approximation, this implies that for large ,

for some . For the sequence of inner knots constructed in the definition of the prior we have that the mesh width and the sparsity satisfy

The first of these facts follows trivially from the construction, the second one by bounding the probability of interest from below by the probability that every of the consecutive intervals of length contains at least one knot. For the B-spline coefficients we have, by independence,

for all . Theorem 1 of Belitser & Serra (2013) deals exactly with this situation. In the present setting the theorem asserts that if and , then for and positive such that , and

| (9) |

then there exist function spaces (of splines) and a constant such that

| (10) | ||||

| (11) | ||||

| (12) |

Now observe that the first two inequalities in (9) hold for

provided is large enough and . The third and fourth inequalities then hold for

if is large enough and . To complete the proof we have to link (10)–(12) to the conditions (5)–(7) of Theorems 1 and 2. Note that since (6) should hold for all , we need to have

For our choices of and this holds if . This amounts to choosing . Then if we define

the right-hand side of (10) equals . Moreover, it holds that , so if we make sure that , the desired inequality (5) holds. The considerations above imply that (6) then holds as well, for any . Recall that we found that the entropy condition holds for , provided . This means that we should choose and above such that

Since the intensities in are uniformly bounded by a common constant (see the proof of Theorem 1 of Belitser & Serra 2013), (12) implies that (7) is fulfilled.

Acknowledgement

Research supported by the Netherlands Organization for Scientific Research NWO.

References

- Adams et al. (2009) Adams, R. P., Murray, I. & MacKay, D. J. (2009). Tractable nonparametric Bayesian inference in Poisson processes with Gaussian process intensities. In Proceedings of the 26th Annual International Conference on Machine Learning. ACM.

- Belitser & Serra (2013) Belitser, E. & Serra, P. (2013). Adaptive priors based on splines with random knots ArXiv Preprint. arXiv:1303.3365 [math.ST].

- Belitser et al. (2013) Belitser, E., Serra, P. & van Zanten, H. (2013). Estimating the period of a cyclic non-homogeneous Poisson process. Scand. J. Stat. 40, 204–218.

- Brown et al. (2005) Brown, L., Gans, N., Mandelbaum, A., Sakov, A., Shen, H., Zeltyn, S. & Zhao, L. (2005). Statistical analysis of a telephone call center: a queueing-science perspective. J. Amer. Statist. Assoc. 100, 36–50.

- Daley & Vere-Jones (1988) Daley, D. J. & Vere-Jones, D. (1988). An introduction to the theory of point processes. Springer Series in Statistics. New York: Springer-Verlag.

- de Boor (2001) de Boor, C. (2001). A practical guide to splines, vol. 27 of Applied Mathematical Sciences. New York: Springer-Verlag, revised ed.

- De Jonge & van Zanten (2012) De Jonge, R. & van Zanten, J. H. (2012). Adaptive estimation of multivariate functions using conditionally Gaussian tensor-product spline priors. Electron. J. Stat. 6, 1984–2001.

- Denison et al. (1998) Denison, D. G. T., Mallick, B. K. & Smith, A. F. M. (1998). Automatic Bayesian curve fitting. J. R. Stat. Soc. Ser. B Stat. Methodol. 60, 333–350.

- Diaconis & Freedman (1986) Diaconis, P. & Freedman, D. (1986). On the consistency of Bayes estimates. Ann. Statist. 14, 1–67. With a discussion and a rejoinder by the authors.

- DiMatteo et al. (2001) DiMatteo, I., Genovese, C. R. & Kass, R. E. (2001). Bayesian curve-fitting with free-knot splines. Biometrika 88, 1055–1071.

- Gelman et al. (1997) Gelman, A., Gilks, W. R. & Roberts, G. O. (1997). Weak convergence and optimal scaling of random walk metropolis algorithms. Ann. Appl. Probab. 7, 110–120.

- Ghosal (2010) Ghosal, S. (2010). The Dirichlet process, related priors and posterior asymptotics. In Bayesian nonparametrics, Camb. Ser. Stat. Probab. Math. Cambridge: Cambridge Univ. Press, pp. 35–79.

- Ghosal et al. (2000) Ghosal, S., Ghosh, J. K. & van der Vaart, A. W. (2000). Convergence rates of posterior distributions. Ann. Statist. 28, 500–531.

- Ghosal et al. (2008) Ghosal, S., Lember, J. & van der Vaart, A. (2008). Nonparametric Bayesian model selection and averaging. Electron. J. Stat. 2, 63–89.

- Ghosal & van der Vaart (2007) Ghosal, S. & van der Vaart, A. (2007). Convergence rates of posterior distributions for non-i.i.d. observations. Ann. Statist. 35, 192–223.

- Ghosal & van der Vaart (2001) Ghosal, S. & van der Vaart, A. W. (2001). Entropies and rates of convergence for maximum likelihood and Bayes estimation for mixtures of normal densities. Ann. Statist. 29, 1233–1263.

- Jacod & Shiryaev (2003) Jacod, J. & Shiryaev, A. N. (2003). Limit theorems for stochastic processes, vol. 288 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Berlin: Springer-Verlag, 2nd ed.

- Kottas & Sansó (2007) Kottas, A. & Sansó, B. (2007). Bayesian mixture modeling for spatial Poisson process intensities, with applications to extreme value analysis. J. Statist. Plann. Inference 137, 3151–3163.

- Møller et al. (1998) Møller, J., Syversveen, A. R. & Waagepetersen, R. P. (1998). Log Gaussian Cox processes. Scand. J. Statist. 25, 451–482.

- Palacios & Minin (2013) Palacios, J. A. & Minin, V. N. (2013). Gaussian process-based Bayesian nonparametric inference of population size trajectories from gene genealogies. Biometrics To appear.

- Panzar & van Zanten (2009) Panzar, L. & van Zanten, H. (2009). Nonparametric Bayesian inference for ergodic diffusions. J. Statist. Plann. Inference 139, 4193–4199.

- Schumaker (2007) Schumaker, L. L. (2007). Spline functions: basic theory. Cambridge Mathematical Library. Cambridge: Cambridge University Press, 3rd ed.

- Sharef et al. (2010) Sharef, E., Strawderman, R. L., Ruppert, D., Cowen, M. & Halasyamani, L. (2010). Bayesian adaptive B-spline estimation in proportional hazards frailty models. Electron. J. Stat. 4, 606–642.

- Smith & Kohn (1996) Smith, M. & Kohn, R. (1996). Nonparametric regression using Bayesian variable selection. Journal of Econometrics 75, 317–343.

- van der Meulen et al. (2006) van der Meulen, F. H., van der Vaart, A. W. & van Zanten, J. H. (2006). Convergence rates of posterior distributions for Brownian semimartingale models. Bernoulli 12, 863–888.