Minimax risk of matrix denoising by singular value thresholding

David Donoholabel=e1]donoho@stanford.edu

[Matan Gavishlabel=e2]gavish@stanford.edu

[

Stanford University

Department of Statistics

Stanford University

Sequoia Hall, 390 Serra Mall

Stanford, California 94305-4065

USA

E-mail: e2

(2014; 4 2013; 7 2014)

Abstract

An unknown by matrix is to be estimated from noisy measurements

, where the noise matrix has i.i.d. Gaussian entries.

A popular matrix denoising scheme solves the nuclear norm penalization problem

, where denotes

the nuclear norm (sum of singular values). This is the analog, for matrices,

of penalization in the vector case. It has been empirically observed

that if has low rank, it may be recovered quite accurately from the

noisy measurement .

In a proportional growth framework where the rank , number of rows

and number of columns all tend to proportionally to each

other (, ), we evaluate the asymptotic minimax

MSE .Our formulas involve

incomplete moments of the quarter- and semi-circle laws (, square

case) and the Marčenko–Pastur law (, nonsquare case). For

finite and , we show that MSE increases as the nonzero singular values

of grow larger. As a result, the finite- worst-case MSE, a quantity

which can be evaluated numerically, is achieved when the signal is

“infinitely strong.”

The nuclear norm penalization problem is solved by applying soft thresholding

to the singular values of . We also derive the minimax threshold, namely

the value , which is the optimal place to threshold the

singular values.

All these results are obtained for general (nonsquare, nonsymmetric) real

matrices. Comparable results are obtained for square symmetric

nonnegative-definite matrices.

62C20,

62H25,

90C25,

90C22,

Matrix denoising,

nuclear norm minimization,

singular value thresholding,

optimal threshold,

Stein unbiased risk estimate,

monotonicity of power functions of multivariate tests,

matrix completion from Gaussian measurements,

phase transition,

doi:

10.1214/14-AOS1257

keywords:

[class=AMS]

keywords:

††volume: 42††issue: 6

\docsubty

FLA

and

NSFSupported in part by NSF Grant DMS-09-06812 (ARRA).

SGFSupported in part by a William R. and Sara Hart Kimball

Stanford Graduate Fellowship and a Technion EE Sohnis Promising

Scientist Award.

1 Introduction

Suppose we observe a single noisy matrix , generated by adding noise

to

an unknown matrix , so that , where is a noise matrix.

We wish to recover the matrix with some bound on the mean squared error

(MSE). This is hopeless when is a completely general matrix,

and the

noise is arbitrary; but when happens to be of relatively

low rank,

and the noise matrix is i.i.d. standard Gaussian, one can indeed

guarantee quantitatively accurate recovery. This paper provides explicit

formulas for the best possible guarantees obtainable by a popular,

computationally practical procedure.

Specifically, let , and be -by- real matrices (a

set we denote by

), and suppose that

has i.i.d. entries, . Consider the following

nuclear-norm penalization (NNP) problem:

(1)

where denotes the sum of singular values of ,

also known

as the nuclear norm, denotes square root of the sum

of squared

matrix entries, also known as the Frobenius norm and is a penalty

factor. A solution to (NNP) is efficiently computable by modern convex

optimization software Grant2010 ; it shrinks away from in the

direction of smaller nuclear norm.

Measure performance (risk) by mean-squared error (MSE). When the

unknown

is of known rank and belongs to a matrix class , the

minimax MSE of NNP is

(2)

namely the worst-case risk of , where is the

threshold for which this worst-case risk is the smallest possible. Here,

denotes expectation with respect to the random noise matrix ,

conditional on a given value of the signal matrix , and

denotes the denoiser

acting on the matrix . Note that the symbol

denotes a matrix class, not a particular matrix.

For square

matrices, , we write instead of . In a very clear sense gives the best possible

guarantee for the MSE of NNP, based solely on the rank and problem

size, and not

on other properties of the matrix .

1.1 Minimax MSE evaluation

In this paper, we calculate the minimax MSE

for two matrix classes :

{longlist}[(1)]

General matrices: :

The signal is a real matrix ().

Symmetric matrices: : The signal

is a real, symmetric

positive semidefinite matrix, a set we denote by .

In both cases, the asymptotic MSE (AMSE) in the “large ” asymptotic

setting admits considerably simpler and more accessible formulas than the

minimax MSE for finite . So in addition to the finite-

minimax MSE, we

study the asymptotic setting where a sequence of problem size triplets

is indexed by , and where, along this

sequence and . We think of

as

the matrix shape parameter; corresponds to a square matrix, and

to a matrix wider than it is tall. We think of as the

fractional rank parameter, with implying low rank

relative to

matrix size. Using these notions we can define the asymptotic minimax

MSE (AMSE)

We obtain explicit formulas for the asymptotic minimax MSE in terms of

incomplete moments of classical probability distributions: the quarter-circle

and semi-circle laws (square case ) and the Marčenko–Pastur

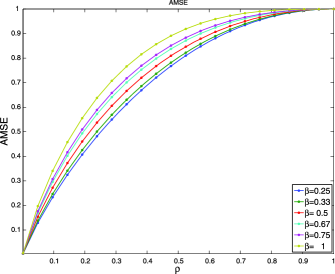

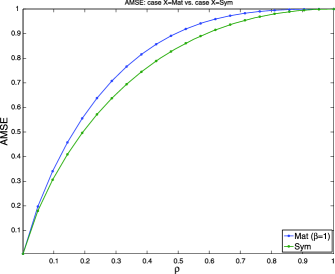

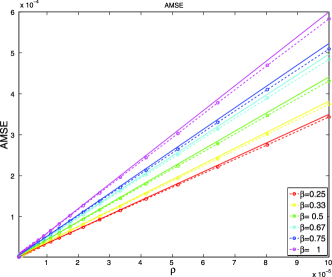

distribution (nonsquare case ). Figures 1 and 2 show how

the AMSE

depends on the matrix class , the rank fraction and the

shape factor

. We also give explicit formulas for the optimal regularization

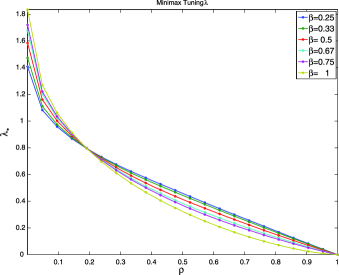

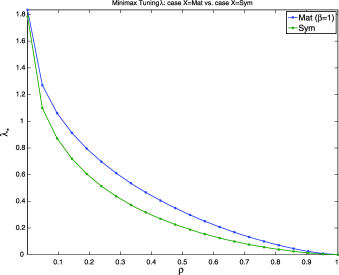

parameter , also as a function of ; see Figures 3

and 4.

These minimax MSE results constitute best possible guarantees, in the

sense that for

the procedure in question, the MSE is actually attained at some rank

matrix, so that no better guarantee is possible for the given tuning parameter

; but also, no other tuning parameter offers a better such

guarantee.

1.2 Motivations

We see four reasons to develop these bounds.

1.2.1 Applications

Several important problems in modern

signal and

image processing, in network data analysis and in computational biology

can be cast as recovery of low-rank matrices from noisy data, and

nuclear norm minimization has become a

popular strategy in many cases; see, for example, Shabalin2010 , Cand2012 and

references therein. Our results provide sharp limits on what such

procedures can

hope to achieve, and validate rigorously the idea that low rank

alone is

enough to provide some level of performance guarantee; in fact, they precisely

quantify the best possible guarantee.

1.2.2 Limits on possible improvements

One might wonder

whether some other procedure offers even better

guarantees than NNP. Consider then

the minimax risk over all procedures, defined by

(3)

where is some measurable function of

the observations, and its corresponding minimax AMSE

where the sequences and are as above.

Here one wants to find the best possible

procedure, without regard to efficient computation.

We also prove a lower bound on the minimax MSE

over all procedures, and provide an asymptotic evaluation

In the square case (), this simplifies to

.

The NNP-minimax MSE

is by definition larger than the minimax MSE, .

While there may be

procedures outperforming NNP, the performance improvement

turns out to be limited. Indeed, our formulas show that

while

(4)

For square matrices (), this simplifies to

(5)

In words, the potential improvement in minimax AMSE of any other

matrix denoising procedure

over NNP is at most a factor of ; and if any such improvement were

available, it would only be available in extreme low-rank situations.

Actually obtaining such an improvement in performance guarantees

is an interesting research challenge.

1.2.3 Parallels in minimax decision theory

The low-rank matrix

denoising problem stands in a line of now-classical problems in minimax

decision theory. Consider the sparse vector denoising problem, where an

unknown vector of interest yields noisy observations with

noise ; the vector is sparsely

nonzero——with and

independent.

In words, a vector with a fraction of nonzeros is observed with

noise. In this setting, consider the following -norm penalization

problem:

(6)

The sparse vector denoising problem

exhibits several striking structural resemblances to low-rank matrix denoising:

•

Thresholding representation.

For a scalar , define the soft thresholding nonlinearity by

In words, values larger than are shifted toward zero by

,

while those smaller than are set to zero. The solution

vector of ()

obeys ; namely, it

applies

coordinate wise.

Similarly, the solution of (NNP) applies

coordinate wise to the singular values of the noisy matrix .

{remark*}

By this observation, () can also be called

“soft thresholding”

or “soft threshold denoising,” and in fact, these other terms are the

labels in

common use. Similarly, NNP amounts to “soft thresholding of singular

values.” This paper will henceforth use the term singular value

soft thresholding

(SVST).

•

Sparsity/low rank analogy. The objects to be recovered in the

sparse vector denoising problem have sparse entries; those to be

recovered in

the low-rank matrix denoising problem have sparse singular values. Thus the

fractional sparsity parameter is analogous to the fractional rank

parameter . It is natural to ask the same questions about

behavior of minimax MSE in

one setting (say, asymptotics as ) as in the other

setting ().

In fact, such comparisons turn out to be illuminating.

•

Structure of the least-favorable estimand.

Among sparse vectors of a given fixed sparsity fraction ,

which of these is the hardest to estimate? This should maximize the

mean-squared error

of soft thresholding, even under the most clever choice of .

This least-favorable configuration is singled out in the minimax AMSE

(7)

In this min/max, the least favorable situation has all its nonzeros, in some

sense, “at infinity”; that is, all sparse vectors which place large

enough values

on the nonzeros are nearly least favorable, that is, essentially make

the problem

maximally difficult for the estimator, even when it is optimally tuned. In

complete analogy, in low-rank matrix denoising we will see that all low-rank

matrices, which are in an appropriate sense “sufficiently large,” are thereby

almost least favorable.

•

Structure of the minimax smoothing parameter.

In the sparse vector denoising AMSE (7) the

achieving the infimum is a type of optimal

regularization parameter, or optimal threshold. It decreases as

increases, with as .

Paralleling this, we show that the low-rank matrix denoising AMSE (2) has minimax singular value soft threshold decreasing as increases,

and as .

Despite these similarities, there is one major difference between

sparse vector denoising and low-rank matrix denoising.

In the sparse vector denoising problem, the soft-thresholding minimax MSE

was compared to the minimax MSE over all procedures by Donoho and

Johnstone Donoho1994 .

Let

denote the soft thresholding AMSE and define the minimax AMSE over all

procedures via

where here denotes any procedure which

is measurable in the observations.

In the limit of extreme sparsity, soft thresholding is

asymptotically minimaxDonoho1994 ,

Breaking the chain of similarities, we are not able to

show a similar asymptotic minimaxity for

SVST in the low rank matrix denoising problem.

Although equation (4) says that

soft thresholding of singular values is asymptotically

not more than a factor of 3 suboptimal, we doubt that

anything better than a factor of can be true; specifically,

we conjecture that SVST suffers a minimaxity gap. For example, for

, we conjecture that

We believe that interesting new estimators will be found improving upon

singular value soft thresholding by essentially this factor of .

Namely, there may

be substantially better guarantees to be had under extreme sparsity,

than those which can be offered

by SVST.

Settling the minimaxity gap for SVST seems a challenging new research question.

1.2.4 Indirect observations

Evaluating the Minimax MSE of SVST has

an intriguing new motivation Donoho2011 , Donoho2013 , OymakHassibi12 ,

arising from the newly evolving fields of compressed sensing and matrix

completion.

Consider the problem of recovering an unknown matrix from noiseless, indirect measurements.

Let be a linear operator, and consider

observations

In words, contains linear measurements

of the matrix object . See the closely related trace regression model Rohde2011 which also includes

measurement noise. Can we recover ?

It may seem that measurements are required, and in general

this would be true;

but if happens to be of low rank, and has suitable properties,

we may need substantially fewer measurements.

Consider reconstruction by nuclear norm minimization,

(8)

Recht and co-authors found that when the matrix representing the

operator

has i.i.d. entries, and the matrix is of rank ,

the matrix is recoverable from measurements

for certain combinations of and Recht2010 .

The operator offers so-called Gaussian measurements when the

representation of the operator as a matrix has i.i.d. Gaussian entries.

Empirical work by Recht, Xu and Hassibi Recht2010a , Recht2008 , Fazel,

Parillo and Recht Recht2010 ,

Tanner and Wei Tanner2012 and

Oymak and Hassibi OymakHassibi11

documented for Gaussian measurements a phase transition

phenomenon, that is,

a fairly sharp transition from success to failure as increases, for

a given .

Putting and it appears that there is

a critical sampling rate ,

such that, for ,

NNM is successful for large , while for ,

NNM fails.

provides a sharp “sampling limit” for low rank matrices, that is,

a clear statement of how many measurements are needed to recover a low

rank matrix,

by a popular and computationally tractable algorithm.

In very recent work, Donoho2011 , Donoho2013 , OymakHassibi12 , it

has been shown empirically

that the precise location of the phase transition coincides with

the minimax MSE

(9)

a key requirement for discovering and verifying (9)

empirically was to obtain an explicit formula for

the right-hand side; that explicit formula is derived and proven in

this paper. Relationship (9)

connects two seemingly unrelated problems: matrix denoising from direct

observations and matrix recovery from

incomplete measurements. Both problems are attracting a large and

growing research literature.

Equation (9) demonstrates the importance of minimax

MSE calculations

even in a seemingly unrelated setting where there is no noise and no

statistical decision to be made!

2 Results

2.1 Least-favorable matrix

We start by identifying the least-favorable situation for matrix

denoising by

SVST.

Theorem 1((The worst-case matrix for SVST has its principal subspace “at

”)).

Define the risk function of a denoiser

at by

(10)

Let , and .

For the worst-case risk of on

matrices of rank

at most ,

we have

(11)

where is any fixed matrix of rank exactly .

2.2 Minimax MSE

Let denote the marginal distribution of the th

largest eigenvalue of a standard central Wishart matrix ,

namely, the th

largest eigenvalue of the random matrix where has

i.i.d. entries.

Define for and

where

(13)

is a combination of the complementary incomplete moments of standard

central Wishart

eigenvalues

for .

Theorem 2((An implicit formula for the finite- minimax MSE)).

The minimax MSE of SVST over -by- matrices of rank at most

is given by

where the minimum on the right-hand sides is unique.

In fact, we will see that

is convex in .

As the densities of the standard central Wishart eigenvalues are known

Zanella2009a , this makes it possible, in principle, to tabulate

the finite- minimax

risk.

2.3 Asymptotic minimax MSE

A more accessible formula is obtained by calculating the large- asymptotic

minimax MSE, where and both grow

proportionally to

. Let us write minimax AMSE for asymptotic minimax MSE.

For the case we assume a limiting rank fraction

and limiting aspect ratio

and consider

Similarly, for the case , we assume a limiting rank fraction

and consider

The Marc̆enko–Pastur distribution Marcenko1967

gives the asymptotic empirical distribution of Wishart eigenvalues. It has

density

(16)

where .

Define the

complementary incomplete moments of the Marc̆enko–Pastur distribution

(17)

Finally, let

(18)

with

.

Theorem 3((An explicit formula for the minimax AMSE)).

For the minimax AMSE of SVST we have

(19)

(20)

with ,

where the minimum on the right-hand sides is unique.

Moreover, for any , the function

is continuous and increasing on , with

and

. The same is true for .

The curves , for different

values of

, are shown in Figure 1. The curves

and

are shown in Figure 2.

Figure 1: The minimax AMSE curves for case ,

defined in (19),

for a few values of .Figure 2: The minimax AMSE curves for case

with and case .

Theorem 4((A characterization of the minimax AMSE for general )).

For any and ,

the function

is decreasing on

with

(22)

(23)

For ,

the minimizer is the unique root of the

equation in

(24)

where the left-hand side of (24) is a

decreasing function of .

The minimizer can therefore be determined

numerically by binary search.

[In fact, we will see that is the unique minimizer of the convex

function .]

Evaluating and

to precision

thus requires evaluations of the complementary

incomplete Marc̆enko–Pastur moments (17).

For square matrices (), this computation turns out to be even simpler,

and only requires

evaluation of elementary trigonometric functions.

Theorem 5((A characterization of the minimax AMSE for )).

We have

where

(27)

are the complementary incomplete moments of the quarter circle law.

Moreover, for

(29)

where is the unique solution to

the transcendental equation

(30)

The left-hand side of (30) is

a decreasing function of .

In pt-mmx-runmycode we make available a Matlab script, and a web-based

calculator for evaluating

and . The implementation

provided employs

binary search to solve

(24) [or (30) for ]

and then feeds the minimizer into (2.3) [or

into (5) for

].

2.5 Asymptotically optimal tuning for the SVST threshold

The crucial functional , defined in (21),

can now be explained as the optimal (minimax)

threshold of SVST in a special system of units.

Let denote the minimax tuning threshold, namely

Theorem 6((Asymptotic minimax tuning of SVST)).

Consider again a sequence with a

limiting rank fraction and a limiting aspect ratio

.

For the asymptotic minimax tuning threshold we have

The curves ,

namely the scaled asymptotic minimax tuning threshold for SVST,

are shown in Figure 3

for different values of .

The curves

and

are shown in Figure 4.

Figure 3: (Nonsquare cases.) The scaled asymptotic minimax tuning

threshold for SVST,

,

when and ,

for a few values of .Figure 4: (Square case.) The scaled asymptotic minimax tuning

threshold for SVST,

and

,

when .

2.6 Parametric representation of the minimax AMSE for square matrices

For square matrices (, ) the minimax

curves

and admit a parametric representation in the

plane using elementary trigonometric functions.

Theorem 7((Parametric representation of the minimax AMSE curve for )).

As ranges over

,

is a parametric representation of , and similarly

is a parametric representation of .

2.7 Minimax AMSE in the low-rank limit

Theorem 8((Minimax AMSE to first order in near )).

For the behavior of the minimax curves near , we have

and in particular

Moreover,

The minimax AMSE curves for

small values of

, and the corresponding approximation slopes are

shown in Figure 5 for several values of . We find

it surprising that asymptotically, symmetric positive definite

matrices are

no easier to recover than general square matrices. This phenomenon is also

seen in the case of sparse vector denoising, where in the limit of extreme

sparsity, the nonnegativity of the nonzeros does not allow one to

reduce the

minimax MSE.333Compare results in Donoho1994 with

Donoho1992 . To be clear, in both matrix denoising and vector denoising,

there is an MSE advantage for each fixed positive rank fraction/sparsity

fraction. It is just that the benefit goes away as either fraction tends to

.

We note that this first-order AMSE near agrees with a different

asymptotic model for minimax MSE of SVST over large low-rank matrices

Donoho2013b . There, the asymptotic prediction for AMSE

near is found to be in agreement with the empirical

finite- MSE.

Figure 5: The minimax AMSE curves for

small values of

(dashed lines)

and the corresponding approximation slopes (solid

lines).

2.8 AMSE vs. the asymptotic global minimax MSE

In (3) we have introduced global minimax MSE

,

namely the minimax risk over all measurable denoisers

.

To define the large- asymptotic global minimax MSE analogous to

(2.3),

consider sequences where and

both grow proportionally to

, such that both limits and

exist.

Define the asymptotic global minimax MSE

(31)

Theorem 9.

(1) For the global minimax MSE we have

(32)

for case , and if , for case .

{longlist}[(3)]

For the asymptotic global minimax MSE we have

(33)

for case , and if , for case . Here

.

Let

(34)

denote our lower bound on asymptotic global minimax MSE.

Then

(35)

and

(36)

2.9 Outline of this paper

The body of the paper proves the above results. Section 3

introduces notation, and proves auxiliary lemmas. In Section 4 we

characterize the worst-case MSE of SVST for matrices of a fixed size (Theorem 1). In Section 5 we derive formula (2.2)

for the

worst-case MSE, and prove Theorem 2. In Section 6 we pass to the large- limit and derive formula

(2.3), which provides the worst-case asymptotic MSE in the

large-

limit (Theorem 3).

In Section 7 we investigate the minimizer of the asymptotic

worst-case MSE function, and its minimum, namely the minimax AMSE, and prove

Theorem 4.

In Section 8 we extend our

scope from SVST denoisers to all denoisers, investigate the global

minimax MSE

and prove Theorem 9.

In the interest of space, Theorems 5,

67 and

8

are proved in the supplemental article Donoho2013c . The supplemental

article also contains

a derivation of the Stein unbiased risk

estimate for SVST, which is instrumental in the proof of Theorem 1,

and other technical auxiliary lemmas.

3 Preliminaries

3.1 Scaling

Our main object of interest, the worst-case MSE of SVST,

(37)

is more conveniently expressed using a specially calibrated risk function.

Since the SVST denoisers are scale-invariant, namely

we are free to introduce the scaling

and define the risk function of a denoiser

at

by

(38)

Then, the worst-case MSE of at is given by

(39)

To vary the SNR in the problem, it will be convenient to vary the norm

of the

signal matrix instead, namely, to consider

with .

3.2 Notation

Vectors are denoted by boldface lowercase letters, such as ,

and their

entries by . Matrices are denoted by uppercase letters, such as

, and

their entries by .

Throughout this text, will denote the data matrix . We use and to denote the

set of real-valued

-by- matrices, and group of -by- orthogonal matrices,

respectively. denotes the Frobenius matrix norm on

,

namely the Euclidean norm of a matrix considered as a vector in .

We denote matrix multiplication by either or .

We use the following convenient notation for matrix diagonals: for a matrix

, we denote by its main diagonal,

(40)

Similarly, for a vector

, and that we suppress in our

notation, we denote by

the “diagonal” matrix

(41)

We use a “fat” singular value decomposition (SVD) of

, with and

. Note

that the SVD is not uniquely determined, and in particular can contain

the singular values of in any order. Unless otherwise noted, we will

assume that the entries of are nonnegative and sorted in

nonincreasing order, . When , the

last columns of are not uniquely determined; we will

see that

our various results do not depend on this choice. Note that

with the “fat” SVD, the matrices and have the

same dimensionality, which simplifies the notation we will need.

When appropriate, we let univariate functions act on vectors entry-wise,

namely, for and , we write

for

the vector with entries .

3.3 acts by soft thresholding of the data singular

values

By orthogonal invariance of the Frobenius norm,

(1) is equivalent to

(42)

through the relation .

It is well known that the solution to (42) is

given by

,

where

denotes

coordinate-wise soft

thresholding of with threshold .

The SVST estimator (1) is therefore given by Koltchinskii2011a

(43)

Note that (43) is well defined, that is, does

not depend on the particular SVD chosen.

In case , observe that the solution to (1) is

constrained to lie

in the linear subspace of symmetric matrices. The solution is the same whether

the noise matrix has i.i.d. standard normal entries, or

whether is

a symmetric Wigner matrix where has

i.i.d. standard normal entries. Below, we assume that the data in case

is

of the form where and has this Wigner form, namely,

the singular values are the absolute values of

eigenvalues of the

symmetric matrix .

4 The least-favorable matrix for SVST is at

We now prove Theorem 1, which characterizes the worst-case

MSE of the

SVST denoiser for a given . The theorem

follows from

a combination of two classical gems of the statistical literature. The

first is

Stein’s unbiased risk estimate (SURE) from 1981, which we

specialize to the SVST estimator; see also Cand2012 . The second is

Anderson’s celebrated monotonicity property for the integral of a symmetric

unimodal probability distribution over a symmetric convex set

Anderson1955 , from 1955, and more specifically its implications for

monotonicity of the power function of certain tests in multivariate hypothesis

testing Das1964 .

To simplify the proof, we introduce the following definitions, which

will be

used in this section only.

Definition 1((A weak notion of matrix majorization based on singular values)).

Let have singular value vectors ,

respectively, which as usual we assume are sorted in nonincreasing order:

and

.

If for , we write .

We note that by rescaling an arbitrary rank-

matrix, it is always possible to majorize any fixed matrix of rank at

most (in the sense of

Definition 1).

Lemma 1.

Let be a matrix of rank ,

and let be a matrix of

rank at most . Then there exists

for which .

{pf}

Let be the vectors of singular values of

, respectively,

each sorted in

nonincreasing order.

Then . Take .

For we have ,

and for

we have .

The above weak notion of majorization gives rise to a weak notion of

monotonicity:

Definition 2((Orthogonally invariant function of a matrix argument)).

We say that is an orthogonally invariant function if

for all and all orthogonal

and .

Definition 3((SV-monotone increasing function of a matrix argument)).

Let be orthogonally invariant.

If, whenever and , satisfies

(44)

for and , we say that is

singular-value-monotone increasing, or SV-monotone increasing.

We now provide a sufficient condition for SV-monotonicity, which

follows from

Anderson’s seminal monotonicity result

Anderson1955 . The following lemma is proved in the supplemental article

Donoho2013c .

Lemma 2.

Assume that can be decomposed as , where

for each , is

a bounded, orthogonally invariant function. Further assume that for each

, is

quasi-convex, in the sense that for all , the set

is convex in .

Then is SV-monotone increasing.

The second key ingredient in the proof of Theorem 1 is the Stein

unbiased risk estimate for SVST.

Let be a weakly differentiable estimator of from data

, where has i.i.d. standard normal entries. The Stein

unbiased risk

estimate Stein1981 is a function of the data, , for

which . In our case, and

are matrices in , and Stein’s theorem (Stein1981 , Theorem 1) implies

that for

we have

In the supplemental article Donoho2013c , we derive SURE for a

large class

of invariant matrix denoisers. As a result, we prove:

Lemma 3((The Stein unbiased risk estimate for SVST)).

For each , there exists an event

and a function, which maps a matrix with

singular values

to

enjoying the following properties:

{longlist}[(1)]

, where is the

distribution of the

matrix with .

is a finite sum of bounded, orthogonally

invariant, quasi-convex functions.

Denoting as usual , where

and , we have

Putting together Lemmas 2 and 3,

we come to a crucial property of SVST.

Lemma 4((The risk of SVST is monotone nondecreasing in the signal singular

values)).

For each , the map is a bounded,

SV-monotone increasing function. In particular, let

with . Then

(45)

{pf}

By Lemma 3, the function

satisfies the conditions of Lemma 2 and is

therefore SV-monotone increasing. It follows that

To see that the risk is bounded, note that for any , we

have by Lemma 3

\upqed

{pf*}

Proof of Theorem 1

By Lemma 4, the map

is bounded and monotone

nondecreasing in

. Hence

exists and is

finite, and

(46)

for all

. Since , obviously

and we only need to show the

reverse inequality. Let be an arbitrary matrix of rank

at most

.

By Lemma 1 there exists such that . It

now follows from Lemma 4 and (46) that

\upqed

5 Worst-case MSE

Let and , and consider them fixed for

the remainder

of this section. Our second main result,

Theorem 2, follows immediately

from Theorem 1, combined with the

following lemma, which is proved in the supplemental article Donoho2013c .

In the supplemental article Donoho2013c we prove the following lemma:

Lemma 6.

The function ,

defined in

(2.2)

on

, is convex and obtains a unique minimum.

Our second main result is an immediate consequence:

{pf*}

Proof of Theorem 2

Let be an arbitrary fixed matrix of rank .

For case , by Theorem 1 and Lemma 5,

where we have used Lemma 6, which also asserts

that the minimum is unique.

Now let be an arbitrary, fixed symmetric positive semidefinite

matrix of rank .

For case , by the same lemmas,

\upqed

6 Worst-case AMSE

Toward the proof of our third main result, Theorem 3, let

be fixed. We first show that in the proportional growth framework,

where the rank , number of rows and

number of columns all tend to proportionally to each other,

the key quantity in our formulas can be evaluated by complementary incomplete

moments of a Marc̆enko–Pastur distribution, instead of a sum of

complementary incomplete moments of Wishart eigenvalues.

Definition 4.

For a pair of matrices , we denote by the singular values, in nonincreasing

order, of

(47)

where is the projection of on

and is

the projection on

. Similarly, for a pair of matrices , denote by

the

eigenvalues, in

nonincreasing order, of

(48)

Lemma 7.

Consider sequences and and numbers

and such that

and .

Let , as in Definition 4, where has i.i.d.

entries.

Define and

, and let

.

Then

{pf}

Write , and recall that

by the Marc̆enko–Pastur law Marcenko1967 ,

in the sense of weak convergence of probability measures,

where is the Marc̆enko–Pastur probability

distribution

with density given by (16).

Now,

as required.

Lemma 8.

Let and such that

and,

and set .

Then

where the right-hand side is defined in (2.3), with for

case and for case .

{pf}

For case , let be an arbitrary fixed matrix of

rank .

For case ,

an arbitrary, fixed symmetric positive semidefinite

matrix of rank .

By Theorem 1 and Lemma 5,

In the supplemental article we prove a variation of Lemma 6 for the asymptotic setting:

Lemma 9.

The function , defined in

(2.3)

on

, where

,

is convex and obtains a unique minimum.

This allows us to the prove our third main result.

{pf*}Proof of Theorem 3

By Lemma 8,

with for case and for case ,

where we have used Lemma 9, which also

asserts that the

minimum is unique.

7 Minimax AMSE

Having established that the asymptotic worst-case MSE (2.3)

satisfies

(19) and (20), we turn to its

minimizer . The notation follows (21).

{pf*}

Proof of Theorem 4

By equation (4.2) in the supplemental article

Donoho2013c , the condition

is thus equivalent, for any , to

(49)

establishing (24) in particular for

.

By Lemma 9, the minimum exists and is unique; namely

this equation has a unique

root in .

One directly verifies that

. The limits (22) and

(23) follow from the fact that

is decreasing. To establish this,

it is enough to observe that

for all , which can be verified

directly.

Theorem 5, which provides more a explicit formula

for the

minimax AMSE in square matrix case (), is proved in the supplemental

article Donoho2013c .

8 Global minimax MSE and AMSE

In this section we prove Theorem 9, which provides

a lower

bound on the minimax risk of the family of all measurable matrix

denoisers (as opposed

to the family of SVST denoisers considered so far) over -by-

matrices of rank at most .

Consider the class of singular-value matrix denoisers, namely

all mappings

that act on the data only through their singular values. More specifically,

consider all denoisers

of the form

(50)

where and

.

(Note that this class contains SVST denoisers but does not exhaust all

measurable denoisers.)

The mapping in (50) is not well defined in general, since

the SVD of , and in particular the order of the singular values in the

vector , is not uniquely determined.

However, (50)

is well defined when each function

is invariant under permutations of its coordinates. Since the equality

may hold for vectors with negative

entries, we are led to the following definition.

Definition 5.

By singular-value denoiser we mean any

measurable mapping

which takes the form (50),

where each entry

of is a function

that is invariant under permutation and

sign changes of its

coordinates. We let denote the class of such mappings.

For a detailed introduction to real-valued or matrix-valued functions which

depend on a matrix argument only through its singular values, see Lewis1995 , Lewis2005 .

The following lemma is proved in the supplemental article Donoho2013c .

Lemma 10((Singular-value denoisers can only improve in worst-case)).

Let be an arbitrary measurable matrix

denoiser. There

exists a singular-value denoiser such that

{pf*}

Proof of Theorem 9

We consider the case .

By Lemma 10, it is enough to show that

where is an arbitrary singular-value denoiser.

Indeed, let be a fixed arbitrary matrix of rank .

The calculation leading to equation (3.9) in the

supplemental article

Donoho2013c is valid for any

rule in , and implies that

,

where and

(51)

Write ,

and let . We therefore have

Combining equations (3.17) and (3.15) in the

supplemental article Donoho2013c , we have

A similar argument yields

,

and the first part of the theorem follows. The second part of the theorem

follows since, taking the limit as prescribed, we have

, and .

For the third part of the theorem, we have by Theorem 8,

\upqed

9 Discussion

In the Introduction, we pointed out several ways that

these matrix denoising results for SVST estimation

of low-rank matrices parallel results for soft thresholding

of sparse vectors. Our derivation of the minimax MSE formulas

exposed two more parallels:

•

Common structure of minimax MSE formulas.

The minimax MSE formula vector denoising problem involves certain

incomplete moments of the standard Gaussian distribution Donoho2011 .

The matrix denoising problem involves completely analogous

incomplete moments, only replacing the Gaussian by the

Marčenko–Pastur distribution or (in the square case )

the quarter-circle law.

•

Monotonicity of SURE. In both settings, the

least-favorable estimand places the signal

“at ,” which yields a convenient formula for

Minimax MSE Donoho2011 .

In each setting, validation of the least-favorable estimation

flows from monotonicity, in an appropriate sense, of Stein’s unbiased

risk estimate within that specific setting.

Acknowledgments

We thank Iain Johnstone, Andrea Montanari and Art Owen for advice at

several crucial

points, and the anonymous referees for many helpful suggestions.

{supplement}

[id=suppA]

\stitleProofs and additional discussion

\slink[doi]10.1214/14-AOS1257SUPP \sdatatype.pdf

\sfilenameaos1257_supp.pdf

\sdescriptionIn this supplementary material we prove Theorems 5,

6,

7,

8 and other lemmas. We also derive the Stein

unbiased risk

Estimate (SURE) for SVST, which is instrumental in the proof of

Theorem 1. Finally, we discuss similarities

between singular value

thresholding and sparse vector thresholding.

References

(1){barticle}[mr]

\bauthor\bsnmAnderson, \bfnmT. W.\binitsT. W.

(\byear1955).

\btitleThe integral of a symmetric unimodal function over a symmetric

convex set and some probability inequalities.

\bjournalProc. Amer. Math. Soc.

\bvolume6

\bpages170–176.

\bidissn=0002-9939, mr=0069229

\bptokimsref\endbibitem

(2){barticle}[mr]

\bauthor\bsnmCandès, \bfnmEmmanuel J.\binitsE. J.,

\bauthor\bsnmSing-Long, \bfnmCarlos A.\binitsC. A. and \bauthor\bsnmTrzasko, \bfnmJoshua D.\binitsJ. D.

(\byear2013).

\btitleUnbiased risk estimates for singular value thresholding and

spectral estimators.

\bjournalIEEE Trans. Signal Process.

\bvolume61

\bpages4643–4657.

\biddoi=10.1109/TSP.2013.2270464, issn=1053-587X, mr=3105401

\bptnotecheck year

\bptokimsref\endbibitem

(3){barticle}[mr]

\bauthor\bsnmDas Gupta, \bfnmS.\binitsS.,

\bauthor\bsnmAnderson, \bfnmT. W.\binitsT. W. and \bauthor\bsnmMudholkar, \bfnmG. S.\binitsG. S.

(\byear1964).

\btitleMonotonicity of the power functions of some tests of the

multivariate linear hypothesis.

\bjournalAnn. Math. Statist.

\bvolume35

\bpages200–205.

\bidissn=0003-4851, mr=0158474

\bptokimsref\endbibitem

(4){bmisc}[author]

\bauthor\bsnmDonoho, \bfnmDavid L.\binitsD. L. and \bauthor\bsnmGavish, \bfnmMatan\binitsM.

(\byear2013).

\bhowpublishedCompanion website for the article the phase

transition of matrix recovery from Gaussian measurements matches

the minimax MSE of matrix denoising.

Available at http://www.runmycode.org/CompanionSite/Site265.

\bptokimsref\endbibitem

(5){bmisc}[author]

\bauthor\bsnmDonoho, \binitsD. and \bauthor\bsnmGavish, \binitsM.

(\byear2014).

\bhowpublishedSupplement to “Minimax risk of matrix denoising by

singular value thresholding.”

DOI:\doiurl10.1214/14-AOS1257SUPP.

\bptokimsref

\endbibitem

(6){barticle}[mr]

\bauthor\bsnmDonoho, \bfnmDavid L.\binitsD. L.,

\bauthor\bsnmGavish, \bfnmMatan\binitsM. and \bauthor\bsnmMontanari, \bfnmAndrea\binitsA.

(\byear2013).

\btitleThe phase transition of matrix recovery from Gaussian

measurements matches the minimax MSE of matrix denoising.

\bjournalProc. Natl. Acad. Sci. USA

\bvolume110

\bpages8405–8410.

\biddoi=10.1073/pnas.1306110110, issn=1091-6490, mr=3082268

\bptokimsref\endbibitem

(7){barticle}[mr]

\bauthor\bsnmDonoho, \bfnmDavid L.\binitsD. L.,

\bauthor\bsnmJohnstone, \bfnmIain\binitsI. and \bauthor\bsnmMontanari, \bfnmAndrea\binitsA.

(\byear2013).

\btitleAccurate prediction of phase transitions in compressed sensing

via a connection to minimax denoising.

\bjournalIEEE Trans. Inform. Theory

\bvolume59

\bpages3396–3433.

\biddoi=10.1109/TIT.2013.2239356, issn=0018-9448, mr=3061255

\bptnotecheck year

\bptokimsref\endbibitem

(8){barticle}[author]

\bauthor\bsnmDonoho, \bfnmDavid L.\binitsD. L. and \bauthor\bsnmJohnstone, \bfnmIain M.\binitsI. M.

(\byear1994).

\btitleMinimax risk overl -balls forl -error.

\bjournalProbab. Theory Related Fields

\bvolume303

\bpages277–303.

\bptokimsref\endbibitem

(9){barticle}[mr]

\bauthor\bsnmDonoho, \bfnmDavid L.\binitsD. L.,

\bauthor\bsnmJohnstone, \bfnmIain M.\binitsI. M.,

\bauthor\bsnmHoch, \bfnmJeffrey C.\binitsJ. C. and \bauthor\bsnmStern, \bfnmAlan S.\binitsA. S.

(\byear1992).

\btitleMaximum entropy and the nearly black object.

\bjournalJ. R. Stat. Soc. Ser. B Stat. Methodol.

\bvolume54

\bpages41–81.

\bidissn=0035-9246, mr=1157714

\bptnotecheck related

\bptokimsref\endbibitem

(10){barticle}[author]

\bauthor\bsnmGavish, \bfnmMatan\binitsM.

and \bauthor\bsnmDonoho, \bfnmDavid L.\binitsD. L.

(\byear2014).

\btitleThe optimal hard threshold for singular

values is .

\bjournalIEEE Trans. Inform. Theory

\bvolume60

\bpages5040–5053.

\bptokimsref\endbibitem

(11){bmisc}[author]

\bauthor\bsnmGrant, \bfnmMichael\binitsM. and \bauthor\bsnmBoyd, \bfnmStephen P.\binitsS. P.

(\byear2010).

\bhowpublishedCVX: Matlab software for disciplined convex programming,

version 2.0 beta. Available at http://cvxr.com/cvx, September 2013.

\bptokimsref\endbibitem

(12){barticle}[mr]

\bauthor\bsnmKoltchinskii, \bfnmVladimir\binitsV.,

\bauthor\bsnmLounici, \bfnmKarim\binitsK. and \bauthor\bsnmTsybakov, \bfnmAlexandre B.\binitsA. B.

(\byear2011).

\btitleNuclear-norm penalization and optimal rates for noisy low-rank

matrix completion.

\bjournalAnn. Statist.

\bvolume39

\bpages2302–2329.

\biddoi=10.1214/11-AOS894, issn=0090-5364, mr=2906869

\bptokimsref\endbibitem

(14){barticle}[mr]

\bauthor\bsnmLewis, \bfnmAdrian S.\binitsA. S. and \bauthor\bsnmSendov, \bfnmHristo S.\binitsH. S.

(\byear2005).

\btitleNonsmooth analysis of singular values. I. Theory.

\bjournalSet-Valued Var. Anal.

\bvolume13

\bpages213–241.

\biddoi=10.1007/s11228-004-7197-7, issn=0927-6947, mr=2162512

\bptokimsref\endbibitem

(15){barticle}[author]

\bauthor\bsnmMarcenko, \bfnmVladimir\binitsV. and \bauthor\bsnmPastur, \bfnmLeonid\binitsL.

(\byear1967).

\btitleDistribution of eigenvalues for some sets of random matrices.

\bjournalMathematics USSR Sbornik

\bvolume1

\bpages457–483.

\bptokimsref\endbibitem

(16){bmisc}[author]

\bauthor\bsnmOymak, \bfnmSamet\binitsS. and \bauthor\bsnmHassibi, \bfnmBabak\binitsB.

(\byear2010).

\bhowpublishedNew null space results and recovery

thresholds for matrix rank minimization.

Preprint. Available at http://arxiv.org/pdf/1011.6326v1.pdf.

\bptokimsref\endbibitem

(17){bmisc}[author]

\bauthor\bsnmOymak, \bfnmSamet\binitsS. and \bauthor\bsnmHassibi, \bfnmBabak\binitsB.

(\byear2012).

\bhowpublishedOn a relation between the minimax risk and the phase

transitions of compressed recovery.

In 2012 50th Annual Allerton Conference on Communication, Control,

and Computing 1018–1025. IEEE, Piscataway, NJ.

Available at

http://ieeexplore.ieee.org/stamp/stamp.jsp?arnumber=6483330.

\bptokimsref\endbibitem

(18){barticle}[mr]

\bauthor\bsnmRecht, \bfnmBenjamin\binitsB.,

\bauthor\bsnmFazel, \bfnmMaryam\binitsM. and \bauthor\bsnmParrilo, \bfnmPablo A.\binitsP. A.

(\byear2010).

\btitleGuaranteed minimum-rank solutions of linear matrix equations

via nuclear norm minimization.

\bjournalSIAM Rev.

\bvolume52

\bpages471–501.

\biddoi=10.1137/070697835, issn=0036-1445, mr=2680543

\bptokimsref\endbibitem

(19){binproceedings}[author]

\bauthor\bsnmRecht, \bfnmBenjamin\binitsB.,

\bauthor\bsnmXu, \bfnmWeiyu\binitsW. and \bauthor\bsnmHassibi, \bfnmBabak\binitsB.

(\byear2008).

\btitleNecessary and sufficient conditions for success of the

nuclear norm heuristic for rank minimization.

In \bbooktitleProceedings of the 47th IEEE Conference on Decision and

Control Cancun, Mexico.

\bptokimsref\endbibitem

(20){barticle}[mr]

\bauthor\bsnmRecht, \bfnmBenjamin\binitsB.,

\bauthor\bsnmXu, \bfnmWeiyu\binitsW. and \bauthor\bsnmHassibi, \bfnmBabak\binitsB.

(\byear2011).

\btitleNull space conditions and thresholds for rank minimization.

\bjournalMath. Program.

\bvolume127

\bpages175–202.

\biddoi=10.1007/s10107-010-0422-2, issn=0025-5610, mr=2776714

\bptnotecheck year

\bptokimsref\endbibitem

(21){barticle}[mr]

\bauthor\bsnmRohde, \bfnmAngelika\binitsA. and \bauthor\bsnmTsybakov, \bfnmAlexandre B.\binitsA. B.

(\byear2011).

\btitleEstimation of high-dimensional low-rank matrices.

\bjournalAnn. Statist.

\bvolume39

\bpages887–930.

\biddoi=10.1214/10-AOS860, issn=0090-5364, mr=2816342

\bptokimsref\endbibitem

(22){bmisc}[author]

\bauthor\bsnmShabalin, \bfnmAndrey\binitsA. and \bauthor\bsnmNobel, \bfnmAndrew\binitsA.

(\byear2010).

\bhowpublishedReconstruction of a low-rank matrix in

the presence of Gaussian noise.

Preprint. Available at \arxivurlarXiv:1007.4148.

\bptokimsref\endbibitem

(23){barticle}[mr]

\bauthor\bsnmStein, \bfnmCharles M.\binitsC. M.

(\byear1981).

\btitleEstimation of the mean of a multivariate normal distribution.

\bjournalAnn. Statist.

\bvolume9

\bpages1135–1151.

\bidissn=0090-5364, mr=0630098

\bptokimsref\endbibitem

(24){barticle}[author]

\bauthor\bsnmTanner, \bfnmJared\binitsJ. and \bauthor\bsnmWei, \bfnmKe\binitsK.

(\byear2013).

\btitleNormalized iterative hard thresholding for matrix completion.

\bjournalSIAM J. Sci. Comput.

\bvolume35

\bpagesS104–S125.

\bidmr=3120763

\bptokimsref\endbibitem

(25){barticle}[author]

\bauthor\bsnmZanella, \bfnmAlberto\binitsA.,

\bauthor\bsnmChiani, \bfnmMarco\binitsM. and \bauthor\bsnmWin, \bfnmMoe Z.\binitsM. Z.

(\byear2009).

\btitleOn the marginal distribution of the eigenvalues of Wishart matrices.

\bjournalIEEE Transactions on Communications

\bvolume57

\bpages1050–1060.

\bptokimsref\endbibitem