Pricing approximations and error estimates for local Lévy-type models with default

Abstract

We find approximate solutions of partial integro-differential equations, which arise in financial models when defaultable assets are described by general scalar Lévy-type stochastic processes. We derive rigorous error bounds for the approximate solutions. We also provide numerical examples illustrating the usefulness and versatility of our methods in a variety of financial settings.

Keywords: Partial integro-differential equation, Asymptotic expansion, Pseudo-differential calculus, Option pricing, Lévy-type process, Defaultable asset

1 Introduction

It is now clear from empirical examinations of option prices and high-frequency data that asset prices exhibit jumps (see, e.g., Ait-Sahalia and Jacod (2012); Eraker (2004) and references therein). From a modeling perspective, the above evidence supports the use of exponential Lévy models, which are able to incorporate jumps in the price process through a Poisson random measure. Moreover, exponential Lévy models are convenient for option pricing since, for a wide variety of Lévy measures, the characteristic function of Lévy processes are known in closed-form, allowing for fast computation of option prices via generalized Fourier transforms (see Lewis (2001); Lipton (2002); Boyarchenko and Levendorskii (2002); Cont and Tankov (2004); Almendral and Oosterlee (2005)). However, a major disadvantage of exponential Lévy models is that they are spatially homogeneous; neither the drift, volatility nor the jump-intensity have any local dependence. Thus, exponential Lévy models are not able to exhibit volatility clustering or capture the leverage effect, both of which are well-known features of equity markets.

In addressing the above shortcomings, it is natural to allow the drift, diffusion and Lévy measure of a Lévy process to depend locally on the value of the underlying process. Compared to their Lévy counterparts, local Lévy models (also known as scalar Lévy-type models) are able to more accurately mimic the real-world dynamics of assets. However, the increased realism of local Lévy models is matched by an increased computational complexity; very few local Lévy models allow for efficiently computable exact option prices (the notable exception being the Lévy-subordinated diffusions considered in Mendoza-Arriaga et al. (2010)). Since an option price can directly related to the solution of a partial integro-differential equation (Kolmogorov backward equation) by means of the Feynman-Kac formula, other classical numerical approaches, such as finite difference or Monte Carlo methods, can be employed. However, such approaches are by no means free of drawbacks (see, for instance, Andersen and Andreasen (2000); d’Halluin et al. (2005)).

Recently, there have been a number of methods proposed for finding approximate option prices in local Lévy settings. We mention in particular the work of Benhamou et al. (2009), who use Malliavin calculus methods to derive analytic approximations for options prices in a setting that includes local volatility and Poisson jumps. We also mention the work of Jacquier and Lorig (2013), who use regular perturbation methods to derive option price and implied volatility approximations in a local-Lévy setting. Another polynomial operator expansion technique was proposed in Pagliarani and Pascucci (2013) and Pagliarani et al. (2013) to compute option prices in stochastic-local-Lévy volatility models.

More recently, Lorig, Pagliarani, and Pascucci (2014c) illustrate how to obtain a family of asymptotic approximations for the transition density of the full class of scalar Lévy-type process (including infinite activity Lévy-type processes). The methods developed in Lorig et al. (2014c) can be briefly described as follows. First, one considers the infinitesimal generator of a general scalar Lévy-type process. One expands the drift, volatility and killing coefficients as well as the Lévy kernel as an infinite series of analytic basis functions. The infinitesimal generator can then be formally written as an infinite series, with each term in the series corresponding to a different basis function. Inserting the expansion for the generator into the Kolmogorov backward equation, one obtains a sequence of nested Cauchy problems for the density of the Lévy-type process.

The polynomial expansion technique described in Lorig et al. (2014c) has also been applied in multi-dimensional settings. In particular, Lorig et al. (2014b) derive explicit approximations and error bounds for implied volatilities for a general class of -dimensional diffusions. Lorig et al. (2013) derive error bounds for transition densities and option prices in a general -dimensional diffusion setting. However, in neither of these papers do the authors consider processes with jumps. For -dimensional models with jumps, Lorig et al. (2014a) derive explicit approximations for transition densities and option prices. However, the results are only formal, as no rigorous error bounds are established for the approximation. The main contribution of this paper is a rigorous proof of short-time error estimates on transition densities and option prices, under Local Lévy models with Gaussian jumps. Furthermore, the proof, which is based on a non-trivial generalization of the standard parametrix method, paves the road for further extensions in order to include more general choices of Lévy measures.

The main contributions of this paper are as follows. First, we analytically solve the sequence of nested Cauchy problems mentioned above and thereby derive an explicit expression of the approximate option price (i.e., solution of the integro-differential equation) to arbitrarily high order. Second, we provide a rigorous and detailed proof of some pointwise error estimates for the approximation. These estimates were announced, without proof, in Lorig et al. (2014c). Lastly, we illustrate how to implement our approximation formulas in Mathematica, Wolfram’s symbolic computation software. In particular, we provide numerical examples for transition densities, Call and Put prices, implied volatilities, bond prices and credit spreads. For the readers’ convenience, example Mathematica code is also made freely available on the authors’ websites. The numerical tests in this manuscript and the authors’ websites clearly demonstrate the versatility and accuracy of the method.

The rest of this paper proceeds as follows: in Section 2 we describe a financial market in which a defaultable asset evolves as an exponential Lévy-type process. We then relate the problem of the pricing of a European-style option to the solution of a partial integro-differential equation (PIDE). Next, in Section 3, we introduce a family of asymptotic solutions of the pricing PIDE. The main results are given in Sections 4, where global error bounds are proved for both the density and price approximations (Theorem 4.4 and Corollary 4.7. respectively). In addition to their practical use, these estimates are interesting from the theoretical point, as they imply some non-classical upper bounds for the fundamental solution of a certain class of integro-differential operators with variable coefficients. The proof of Theorem 4.4 is postponed to Section 6. Before proving the theorem, we provide in Section 5 a number of numerical examples, which are relevant for financial applications.

2 Market model and option pricing

For simplicity, we assume a frictionless market, no arbitrage, zero interest rates and no dividends. Our results can easily be extended to include locally dependent interest rates and dividends. We take, as given, an equivalent martingale measure , chosen by the market on a complete filtered probability space satisfying the usual hypotheses. All stochastic processes defined below live on this probability space and all expectations are taken with respect to . We consider a defaultable asset whose risk-neutral dynamics are given by

| (2.1) |

Here, is a Lévy-type process with local drift function , local volatility function and state-dependent Poisson random and Lévy measures and respectively. The random variable has an exponential distribution and is independent of . Note that , which represents the default time of , is defined here through the so-called canonical construction (see Bielecki and Rutkowski (2001)). This way of modeling default is also considered in a local volatility setting in Carr and Linetsky (2006); Linetsky (2006), and for exponential Lévy models in Capponi et al. (2013). Notice that the drift coefficient is fixed by , and in order to satisfy the martingale condition:

| (2.2) |

We assume that the coefficients are measurable in and suitably smooth in so as to ensure the existence of a strong solution to (2.1) (see, for instance, Oksendal and Sulem (2005), Theorem 1.19). We also assume that

| (2.3) |

satisfies the following three boundedness conditions

| (2.4) |

which is rather standard assumption for financial applications. We will relax some of these assumptions for the numerical examples provided in Section 5. Even without the above assumptions in force, our numerical tests indicate that our approximation techniques gives very accurate results.

We consider a European derivative expiring at time with payoff and we denote by its price process. we introduce

| (2.5) |

Then, by no-arbitrage arguments (see, for instance, Linetsky (2006, Section 2.2)) the price of the option at time is given by

| (2.6) |

From (2.6) we see that, in order to compute the price of an option, we must evaluate functions of the form111Note: we can accommodate stochastic interest rates and dividends of the form and by simply making the change: and in PIDE (2.8).

| (2.7) |

By a direct application of the Feynman-Kac representation theorem (see, for instance, Theorem 14.50 in Pascucci (2011)) the classical solution of the following Cauchy problem,

| (2.8) |

when it exists, is equal to the function defined in (2.7). Here is the integro-differential operator associated with the SDE (2.1) and defined explicitly as

| (2.9) | ||||

| (2.10) |

with and as in (2.2). We say that is the characteristic operator222More precisely, would be the characteristic operator of . of .

Sufficient conditions for the existence and uniqueness of a classical solution of a second order elliptic integro-differential equations of the form (2.8) are given in Theorem II.3.1 of Garroni and Menaldi (1992). In particular, given the existence of the fundamental solution of , we have that for any integrable datum , the Cauchy problem (2.8) has a classical solution that can be represented as

| (2.11) |

Notice that is a “defective” probability density since (due to the possibility that ) we have

| (2.12) |

3 Approximate densities and option prices via polynomial expansions

In this section we describe the approximation methodology and define the notation that will be needed in subsequent sections.

Definition 3.1.

For any , let , and be such that the following hold:

-

(i)

For any , the functions , are polynomials with , , and for any the functions , belong to .

-

ii)

For any , , we have

(3.1) where each satisfies condition (2.4). Moreover, , and

(3.2) for some positive .

Then we say that , defined by

| (3.3) | ||||

| (3.4) | ||||

| (3.5) | ||||

| (3.6) |

is an -th order polynomial expansion of .

Definition 3.1 allows for very general polynomial specifications. The idea is to choose an expansion that closely approximates , i.e. formally one has

| (3.7) |

The precise sense of this approximation will depend on the application. Below, we present three polynomial expansions. The first two expansion schemes provide an accurate approximation in a pointwise local sense, under the assumption of smooth coefficients. The last expansion scheme approximates in a global sense and can be applied even in the case of discontinuous coefficients.

Example 3.2.

(Taylor polynomial expansion)

Assume the coefficients and that the compensator

takes the form

where with , and is a Lévy measure. Then, for any fixed and , we define , and as the th order term of the Taylor expansions of , and respectively in the spatial variables around the point . That is, we set

| (3.8) |

The expansion proposed in Lorig et al. (2014b) and Lorig et al. (2014d) is the particular case when .

Example 3.3.

(Time-dependent Taylor polynomial expansion)

Under the assumptions of Example 3.2,

fix a trajectory .

We then define , and as the

th order term of the Taylor expansions of , and respectively around . This expansion for the coefficients allows the expansion point of the Taylor

series to evolve in time according to the evolution of the underlying process . For instance, one could choose . In Lorig

et al. (2014b) this choice results in a highly accurate approximation for option prices and implied volatility in the Heston (1993) model, recently included in the open-source financial library QuantLib.

Example 3.4.

(Hermite polynomial expansion)

Hermite expansions can be useful when the diffusion coefficients are discontinuous. A remarkable

example in financial mathematics is given by the Dupire’s local volatility formula for models with

jumps (see Friz

et al. (2013)). In some cases, e.g., the well-known Variance-Gamma model, the

fundamental solution (i.e., the transition density of the underlying stochastic model) has

singularities. In such cases, it is natural to approximate it in some norm rather than in

the pointwise sense. For the Hermite expansion centered at , one sets

| (3.9) | ||||

| (3.10) |

where the inner product is an integral over with a Gaussian weighting centered at and is the -th one-dimensional Hermite polynomial (properly normalized so that with being the Kronecker’s delta function).

Remark 3.5.

Although in each of the above examples, , and are polynomials in of degree , this is not a requirement of our expansion method. The degree of , and may be greater than, equal to, or less than .

We now return to Cauchy problem (2.8). Following the classical perturbation approach, we expand the solution as an infinite sum

| (3.11) |

Inserting (3.7) and (3.11) into (2.8) we find that the functions satisfy the following sequence of nested Cauchy problems

| (3.12) | ||||

| and | ||||

| (3.13) | ||||

Remark 3.6.

In fact, the nested sequence of Cauchy problems (3.12)-(3.13) satisfied by the sequence of functions is a particular choice. This choice can be motivated by considering a family of Cauchy problems, indexed by a small parameter

| (3.14) |

Note that, by (3.7), we formally have . If one seeks a solution to (3.14) of the form , then, collecting terms of like powers of one finds that and satisfy (3.13) and (3.13), respectively.

3.1 Expression for

Notice that is the characteristic operator of the following additive process

| (3.15) |

whose characteristic function is given explicitly by

| (3.16) |

where

| (3.17) |

and with , and being defined as

| (3.18) | ||||

| (3.19) | ||||

| (3.20) |

Note, the additive process in (3.15) is assumed to be defined on an appropriate probability space. It is well-known that additive processes can be constructed as time-changed Lévy processes (see (Cont and Tankov, 2004, Chapter 14)). The fundamental solution of , which exists if (Sato, 1999, Proposition 28.3), can be recovered by Fourier inversion since, by the first equality in (3.16), we have

| (3.21) |

and therefore

| (3.22) |

Given the fundamental solution , we have the representation for the solution of problem (3.12)

| (3.23) |

Assume that the payoff function and its Fourier transform . Then, by inserting the expression (3.22) for into (3.23) and integrating with respect to , we also have the following alternative representation

| (3.24) |

3.2 Expression for

The following theorem provides an explicit formula for in (3.13) expressed in terms of integro-differential operators applied to in (3.23).

Theorem 3.7.

Remark 3.8.

The operator in (3.28) can be written more explicitly as

| (3.30) | ||||

| (3.31) | ||||

| (3.32) |

Remark 3.9.

Remark 3.10.

The expression for given in (3.25) can be used in two ways. First, if the fundamental solution is explicitly available (this is always the case in the purely diffusive setting), then to obtain one can apply the operator directly to in (3.23). Second, if is not available explicitly, then one can obtain a Fourier representation for by applying the operator directly to in (3.24). The details of the latter approach will be shown in Subsection 3.2.1.

Proof of Theorem 3.7.

Let be formally defined by (3.21). The proof of Theorem 3.7 relies on the following symmetry properties: for any and , we have

| (3.34) | ||||

| (3.35) | ||||

| and | ||||

| (3.36) | ||||

| (3.37) | ||||

with acting as

| (3.38) |

Identities (3.34)-(3.35) follow directly from the spatial-homogeneity of the coefficients of . In order to prove (3.36)-(3.37), we shall use some standard properties of the Fourier transform. For any function in the Schwartz space we have

| (3.39) |

and for any Lévy measure such that , we have

| (3.40) |

Thus, by (3.39) we obtain

| (3.41) | ||||

| (3.42) | ||||

| (by (3.16)-(3.17)) | (3.43) | |||

| (by (3.20)) | (3.44) | |||

| (3.45) | ||||

| (by (3.39) and (3.40)) | (3.46) | |||

| (by (3.35), (3.34) and (3.29)) | (3.47) | |||

The identity (3.37) arises from the same arguments and because, by the symmetry property (3.34), we have

| (3.48) |

As indicated in Remark 3.9, Theorem 3.7 reduces to (Lorig et al., 2013, Thorem 3.8) in case of a null Lévy measure . The proof of the (Lorig et al., 2013, Thorem 3.8) is based on a systematic use of symmetry properties of Gaussian densities combined with some classical relations such as the Chapman-Kolmogorov equation and the Duhamel’s principle. Using the same classical relations, the proof of Theorem 3.7 follows by replacing the Gaussian symmetry properties in (Lorig et al., 2013, Lemma 5.4) with the symmetries properties (3.34)-(3.35)-(3.36)-(3.37) outlined above for additive processes. We refer to (Lorig et al., 2013, Section 5) for the details. ∎

3.2.1 Fourier representation for

Using (3.16), (3.24) and (3.25), we obtain

| (3.49) |

The term in parenthesis can be computed explicitly. However, is, in general, an integro-differential operator (when is a diffusion is simply a differential operator). Thus, for models with jumps, computing is a challenge. Remarkably, we will show that there exists a differential operator such that

| (3.50) |

where, for clarity, we have explicitly indicated using the superscript that acts on . With a slight abuse of terminology, we call the symbol 444 The operator is not a function as in the classical theory of pseudo-differential calculus. However is the symbol of . For the interested reader, any book on pseudo-differential operators is an appropriate resource to learn about symbols. See, for example Jacob (2001) or Hoh (1998). of the operator in (3.26).

Let us consider the operator in (3.29); its symbol is defined analogously to (3.50), i.e.

| (3.51) |

Explicitly, we have

| (3.52) |

where the function is defined as

| (3.53) | ||||

| (3.54) |

We note that, while is a first order integro-differential operator, its symbol is a first order differential operator. For this reason, it is more convenient to use the symbol instead of the operator . From identity (3.51) we obtain directly the expression of the symbol of in (3.28). Indeed, recalling the expression (3.1) of we have

| (3.55) | ||||

| (3.56) |

Thus we have proved the following lemma

Lemma 3.11.

The following theorem extends the Fourier pricing formula (3.24) to higher order approximations.

Theorem 3.12.

Proof.

We first note that, since the approximating operator acts in the variables, then it commutes555This was one of the main points of the adjoint expansion method proposed by Pagliarani et al. (2013). with the Fourier pricing operator (3.24). Thus, by (3.25) combined with (3.24), we get

| (3.60) | ||||

| (3.61) |

and the thesis follows from (3.50). ∎

Remark 3.13.

Computing the term in parenthesis above is a straightforward exercise since the symbol , given in (3.57), is a differential operator.

Example 3.14.

Let the -st order Taylor expansion of proposed in Example 3.2. Then we have

| (3.62) |

with

| (3.63) |

and

| (3.64) |

4 Gaussian jumps: explicit densities and pointwise error bounds

We examine here the particular case when the Lévy measure coincides with a normal distribution with state dependent parameters. Specifically, throughout this section we will assume

| (4.1) |

We will show that, under such a choice, the representation formula given in Theorem 3.7 leads to closed form (fully explicit) approximations for densities, prices and Greeks. Furthermore we will prove some sharp pointwise error bounds for such approximations at a given order .

For sake of simplicity, we will work specifically with the Taylor series expansion of Example 3.2. Throughout this section we will often make use of the convolution operator

| (4.2) |

Let us first observe that the leading term in the expansion of the fundamental solution is the transition density of a time-dependent compound Poisson process with Lévy measure

| (4.3) |

and thus it can be written as

| (4.4) | ||||

| (4.5) |

This also implies that the leading term in the price expansion is explicit, as long as the integrals of the payoff function against the Gaussian densities are computable in closed form.

Moreover we have the following representation for the operators appearing in Theorem 3.7.

Proposition 4.1.

For any , the operator in (3.28) is given by

| (4.6) |

where

| (4.7) | ||||

| (4.8) |

and

| (4.9) | ||||

| (4.10) |

with being polynomials whose coefficients only depend on

| (4.11) |

Remark 4.2.

Note that the action of the operators on the Lévy type density , as well as on , can be explicitly characterized. Indeed, a direct computation shows that, for any ,

| (4.12) | ||||

| (4.13) |

and

| (4.14) | ||||

| (4.15) |

We now fix and prove some pointwise error estimates for the -th order approximation of the fundamental solution of , defined as

| (4.16) |

where the functions solve (3.12)-(3.13) with . Hereafter, we will assume the coefficients of the operator in (2.10), with as in (4.1), to satisfy the following assumption.

Assumption 4.3.

There exists a constant such that

-

i)

(parabolicity) for any and ,

(4.17) -

ii)

(non degeneracy of the Lévy measure) the Lévy measure is as in (4.1) and, for any and ,

(4.18) -

iii)

(regularity and boundedness) for any , the functions , , , , and all of their -derivatives up to order are bounded by , uniformly with respect to .

Theorem 4.4.

Let , and or in (4.10)-(4.11). Then, under Assumption 4.3, for any and we have666Here , where denotes the sup-norm on . Note that if are constants.

| (4.19) |

where

| (4.20) |

Here, the function is the fundamental solution of the constant coefficients jump-diffusion operator

| (4.21) |

where is a suitably large constant, and is defined as

| (4.22) |

with being the convolution operator defined in (4.2).

Remark 4.5.

As we shall see in the proof of Theorem 4.4, the functions take the following form

| (4.23) |

and therefore can be explicitly written as

| (4.24) |

By Remark 4.5, it follows that, when and , the asymptotic behaviour as of the sum in (4.23) depends only on the term. Consequently, we have as tends to . On the other hand, for , , and thus also , tends to a positive constant as goes to . It is then clear by (4.19) that, with fixed, the asymptotic behavior of the error, when tends to , changes from to depending on whether the Lévy measure is locally-dependent or not.

Remark 4.6.

The proof of Theorem 4.4 is also interesting for theoretical purposes. Indeed, it actually represents a procedure to construct . Note that with being known explicitly, equation (4.19) provides pointwise upper bounds for the fundamental solution of the integro-differential operator with variable coefficients .

Theorem 4.4 extends the previous results in Pagliarani et al. (2013) where only the purely diffusive case (i.e ) is considered. In that case an estimate analogous to (4.19) holds with

Theorem 4.4 shows that for jump processes, one obtains an improvement on the asymptotic convergence from to when passing from to . On the other hand, increasing the order of the expansion for greater than one, theoretically does not give any gain in the rate of convergence of the approximation expansion as ; this is due to the fact that the expansion is based on a local (Taylor) approximation while the PIDE contains a non-local part. We refer to Section 6.2 for further details about this aspect. As for the estimate (4.19), this is in accord with the results in Benhamou et al. (2009) where only the case of constant Lévy measure is considered. Thus Theorem 4.4 extends the latter results to state dependent Gaussian jumps using a completely different technique. Extensive numerical tests showed that the first order approximation gives very accurate results and the precision appears to be further improved by considering higher order approximations.

A straightforward corollary of Theorem 4.4 is the following estimate of the error for the -th order approximation of the price, defined as

| (4.25) |

Some possible extensions of these asymptotic error bounds to general Lévy measures are possible, though they are certainly not straightforward. Indeed, the proof of Theorem 4.4 is based on some pointwise uniform estimates for the fundamental solution of the constant coefficient operator, i.e., the transition density of a compound Poisson process with Gaussian jumps. When considering other Lévy measures these estimates would be difficult to carry out, especially in the case of jumps with infinite activity, but they might be obtained in some suitable normed functional space. This might lead to error bounds for short maturities, which are expressed in terms of a suitable norm, as opposed to uniform pointwise bounds. We aim to elaborate more on this direction in our future research.

5 Examples

In this section, in order to illustrate the versatility of our asymptotic expansion, we apply our approximation technique to a variety of different Lévy-type models. We study not only option prices and transition densities, but also implied volatilities and credit spreads. In each setting, if the exact or approximate density/option price/credit spread has been computed by a method other than our own, we compare this to the density/option price/credit spread obtained by our approximation. For cases where the exact or approximate density/option price/credit spread is not analytically available, we use Monte Carlo methods to verify the accuracy of our method.

Note that, some of the examples considered below do not satisfy the conditions listed in Section 2. In particular, we will consider coefficients that are not bounded. Nevertheless, the formal results of Section 3 work well in the examples considered.

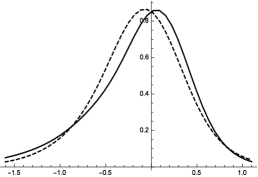

5.1 CEV-like Lévy-type processes

We consider a Lévy-type process of the form (2.1) with CEV-like volatility and jump-intensity. Specifically, the -price dynamics are given by

| (5.1) |

where is a Lévy measure. When , this model reduces to the CEV model of Cox (1975). Note that, with , the volatility and jump-intensity increase as , which is consistent with the leverage effect (i.e., a decrease in the value of the underlying is often accompanied by an increase in volatility/jump intensity). This characterization will yield a negative skew in the induced implied volatility surface. For the numerical examples for this model, we use the one-point Taylor series expansion of as in Example 3.2 with .

We will consider the case where the Lévy measure is Gaussian:

| (5.2) |

In our first numerical experiment, we consider the case of Gaussian jumps. That is, is given by (5.2). We fix the following parameters

| (5.3) |

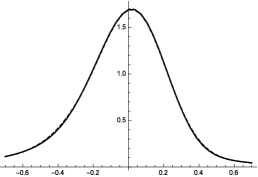

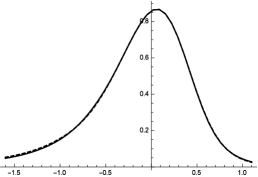

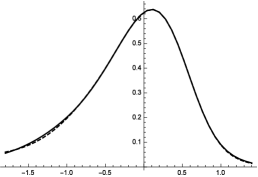

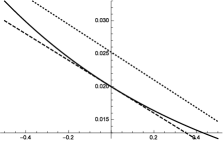

In order to examine the convergence of our density approximation, in Figure 1 we plot the approximate transition density for different values of . We note that, for , the transition densities and are nearly identical. This is typical in our numerical experiments. Numerical results associated with Figure 1 are given in Table 1.

Computation times are also an important consideration. From Theorem 3.12 and (4.25), we observe that

| (5.4) |

where, to obtain from , one simply sets . Thus, the -th order approximation (either for an option price or the transition density ) as a single Fourier integral, which must be computed numerically. The difference in computation times for a given order of approximation will depend only on the factor in parenthesis, which is simply a polynomial in and can always be computed explicitly. To gauge the numerical cost of computing the th order approximation of the transition density, we measure the average time needed to compute over a range of -values. We call the average time it takes to compute divided by the average time it takes to compute the computation time of relative to . Computation times relative to are given in Table 1.

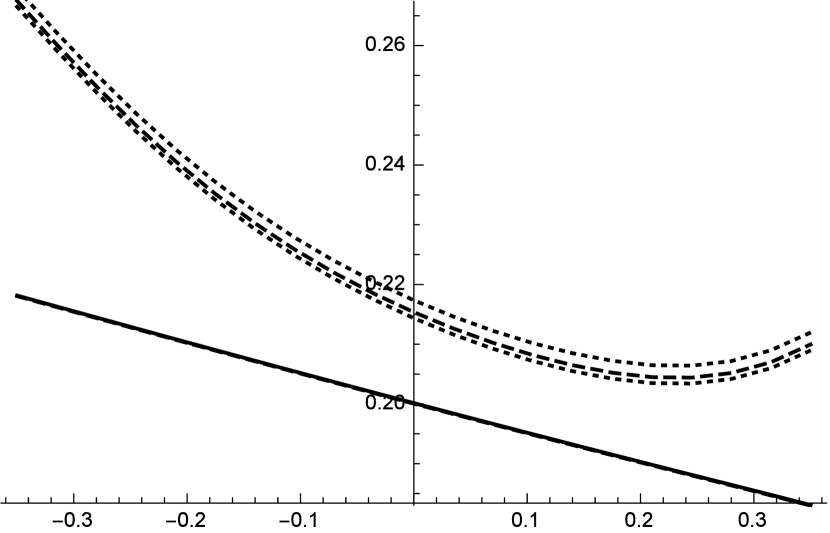

5.2 Comparison with Jacquier and Lorig (2013)

In Jacquier and Lorig (2013), the author considers a class of time-homogeneous Lévy-type processes of the form:

| (5.5) |

Here, are non-negative constants, the function is smooth and and are Lévy measures. When , the authors obtain the following expression for European-style options written on

| (5.6) | ||||

| (5.7) |

where and

| (5.8) | ||||

| (5.9) |

As in (3.24), is the (possibly generalized) inverse Fourier transform of the option payoff .

In our numerical experiment, we use the Taylor series expansion of as in Example 3.2 with . We consider Gaussian jumps (i.e., given by (5.2)) and we fix the following parameters:

| (5.10) |

where the Lévy measure is given by (5.2). Using Theorem 3.7, we compute the approximate prices and of a series of European puts with strike prices (we add the parameter to the arguments of to emphasize the dependence of on the strike price ). We also compute the price using (5.6). In (5.6), we truncate the infinite sum at .

As prices are often quoted in implied volatilities, we convert prices to implied volatilities by inverting the Black-Scholes formula numerically. That is, for a given put price , we find such that

| (5.11) |

where is the Black-Scholes price of the put as computed assuming a Black-Scholes volatility of . For convenience, we introduce the notation

| (5.12) |

to indicate the implied volatility induced by option price .

5.3 Comparison to NIG-type processes

There is a one-to-one correspondence between the generator of a Lévy-type process and its symbol , the correspondence being given by

| (5.13) |

Thus, Lévy-type processes can be uniquely characterized either through their generator or their symbol . If is an additive or Lévy process with symbol , we have the following expression for

| (5.14) |

A Normal Inverse Gaussian (NIG) (see Barndorff-Nielsen (1998)) is a Lévy process with symbol

| (5.15) |

In Chapter 14, equation (14.1) of Boyarchenko and Levendorskii (2000), that authors consider NIG-like Feller processes with symbol

| (5.16) |

where , , , and where there exist constants and such that , and . Note that if is a NIG-type process with symbol , then is a martingale if and only if . Thus, the triple fixes .

Boyarchenko and Levendorskii (2000) deduce the following asymptotic expansion for (see the equations following (14.27) and equation (16.40)).

| (5.17) | ||||

| (5.18) |

We note that, if one uses the Taylor series expansion of as in Example 3.2 with , then expansion (5.18) is contained within , the first order price approximation obtained in Theorem 3.7.

In our numerical experiment, we use the Taylor series expansion from Example 3.2 with . We fix the following parameters

| (5.19) |

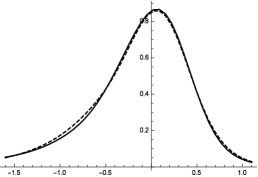

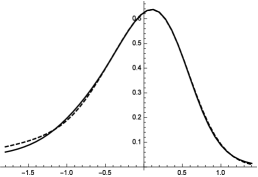

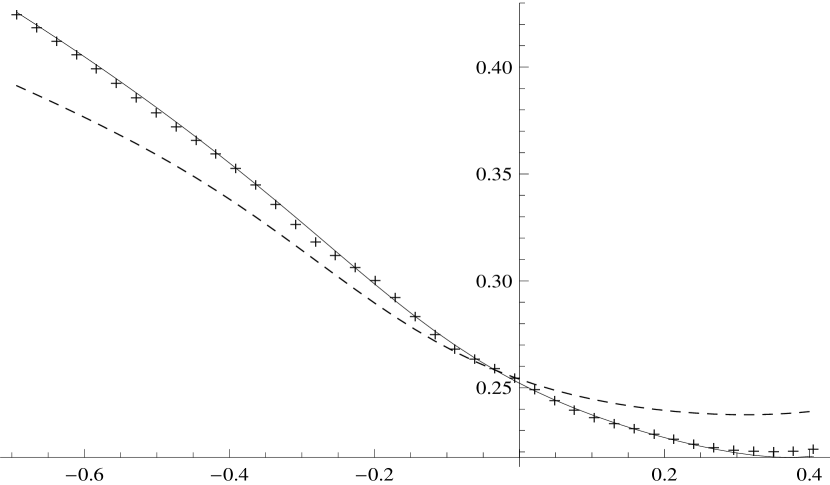

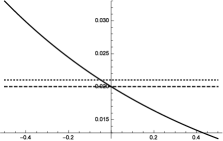

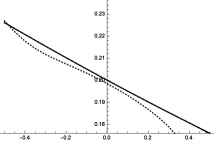

and, using Theorem 3.7, we compute the approximate prices and of a series of European puts with strike prices (we once again add the parameter to the arguments of to emphasize the dependence of on the strike price ). We also compute the exact price using Monte Carlo simulation. After converting prices to implied volatilities we plot the results in Figure 3. We observe a nearly exact match between the induced implied volatilities and .

5.4 Yields and credit spreads in the JDCEV setting

Consider a defaultable bond, written on , that pays one dollar at time if no default occurs prior to maturity (i.e., , ) and pays zero dollars otherwise. Then the time value of the bond is given by

| (5.20) |

We add the parameter to the arguments of to indicate dependence of on the maturity date . Note that is both the price of a bond and the conditional survival probability: . The yield of such a bond, on the set , is defined as

| (5.21) |

The credit spread is defined as the yield minus the risk-free rate of interest. Obviously, in the case of zero interest rates, we have: yield credit spread.

In Carr and Linetsky (2006), the authors introduce a class of unified credit-equity models known as Jump to Default Constant Elasticity of Variance or JDCEV. Specifically, in the time-homogeneous case, the underlying is described by (2.1) with

| (5.22) |

where , , . We will restrict our attention to cases in which . From a financial perspective, this restriction makes sense, as it results in volatility and default intensity increasing as , which is consistent with the leverage effect. Note that when , the asset may only go to zero via a jump from a strictly positive value. That is, according to the Feller boundary classification for one-dimensional diffusions (see Borodin and Salminen (2002), p.14), the endpoint is a natural boundary for the killed diffusion (i.e., the probability that reaches in finite time is zero). The survival probability in this setting is computed in Mendoza-Arriaga et al. (2010), equation (8.13). We have

| (5.23) | ||||

| (5.24) |

where is the Kummer confluent hypergeometric function, is a Gamma function and

| (5.25) |

We compute using both equation (5.24) (truncating the infinite series at ) as well as using Theorem 3.7. We use the Taylor series expansion of expansion of Example 3.2 with . After computing bond prices, we then calculate the corresponding credit spreads using (5.21). Approximate spreads are denoted

| (5.26) |

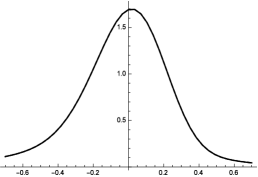

The survival probabilities are and the corresponding yields are plotted in Figure 4. Values for the yields from Figure 4 can also be found in Table 2.

Remark 5.1.

To compute survival probabilities , one assumes a payoff function and obtains

Thus, when computing survival probabilities and/or credit spreads, no numerical integration is required. Rather, one uses (3.25) and easily obtains

| (5.27) | ||||

| (5.28) | ||||

| (5.29) | ||||

| (5.30) | ||||

| (5.31) | ||||

| (5.32) |

where . It is interesting to note that

| (5.33) |

which guarantees that the (i.e., as increases from zero, the approximate survival probability decreases, as expected).

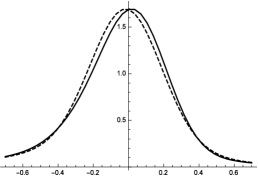

5.5 Hermite vs Taylor approximations

We are interested in comparing the relative accuracy of the Taylor series and Hermite polynomial approximations (examples 3.2 and 3.4). To this end, we consider the Constant Elasticity of Variance (CEV) model of Cox (1975). The dynamics are given by

| (5.34) |

We consider two approximations for the variance function – Taylor and Hermite. We have

| (5.35) | |||||

| (5.36) |

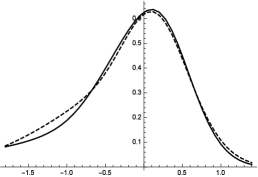

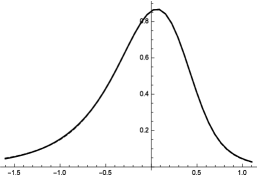

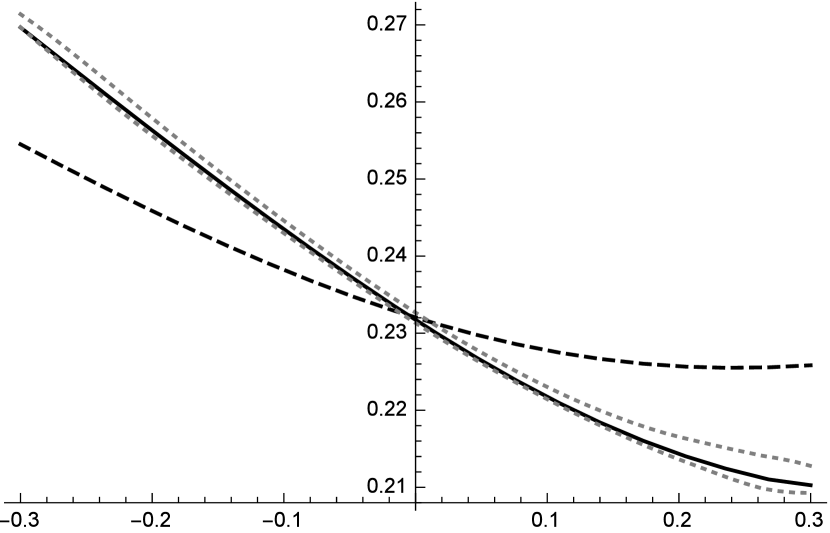

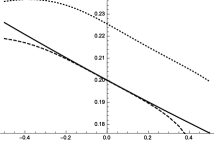

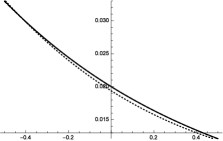

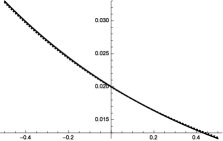

Fix a maturity date and let . Denote by the price at time of a call option with strike price . The exact call option price is given in Cox (1975). Denote by the th order approximation of a call price, as obtained using the Taylor series approximation of . Likewise, denote by the th order approximation of a call price, as obtained using the Hermite polynomial approximation of . In figure 5 we plot as a function of moneyness the exact implied volatility as well as the Taylor and Hermite approximations of implied volatility and for . We also plot, as a function of the exact diffusion coefficient as well as the Taylor and Hermite approximations of the diffusion coefficient and for . It is clear from Figure 5 that the Taylor expansion provides a more accurate approximation of than the Hermite expansion for every . Not surprisingly, Figure 5 also shows that implied volatility induced by the Taylor expansion provides a more accurate approximation of the exact implied volatility than does the Hermite approximation . Though, for , both approximations are remarkably accurate for moneyness .

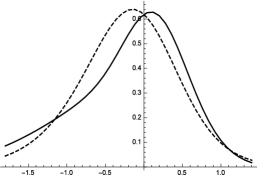

5.6 Accuracy: jumps vs no jumps

In this example, we examine (numerically) whether or not the addition of jumps affects the accuracy of our asymptotic approximation for Call prices. To this end, we consider the CEV-like Lévy-type process with Gaussian jumps, introduced in Section 5.1. We fix the following parameters:

| (5.37) |

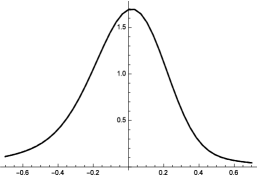

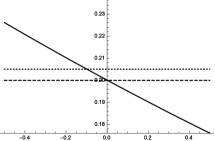

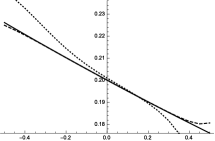

We consider two scenarios: (no jumps) and (with jumps). In each scenario we compute our third order approximation for Call prices using the Taylor series approximation (Example 3.2). We also compute, in the case of no jumps, the exact call price using the formulas given in Cox (1975). In the case where the jump intensity is non-zero, we compute a 95% confidence interval for call prices via Monte Carlo simulation. Finally, call prices are converted to implied volatilities: . The results are plotted in Figure 6.

6 Proof of Theorem 4.4

For sake of simplicity we only prove the assertion when the default intensity and mean jump size are zero , when the jump intensity and diffusion component are time-independent , and when the standard deviation of the jumps is constant . Thus we consider the integro-differential operator

with

| (6.1) |

We will give some details on how to extend the proof to the general case at the end of the section. Our idea is to use our expansion as a parametrix. That is, our expansion will serve as the starting point of the classical iterative method introduced by Levi (1907) to construct the fundamental solution of . Specifically, as in Pagliarani et al. (2013), we take as a parametrix our -th order approximation with in (4.10)-(4.11). The case can be analogously proved by using the backward parametrix approach (see Corielli et al. (2011)). For sake of brevity we skip the details for the latter case.

By analogy with the classical approach (see, for instance, Friedman (1964) and Di Francesco and Pascucci (2005), Pascucci (2011) for the pure diffusive case, or Garroni and Menaldi (1992) for the integro-differential case), we have

| (6.2) |

where is determined by imposing the condition

Equivalently, we have

and therefore by iteration

| (6.3) |

where

| (6.4) | ||||

| (6.5) |

The proof of Theorem 4.4 is based on several technical lemmas which we relegate to Section 6.3. In particular, we will use such preliminary estimates to provide pointwise bounds for each of the terms in (6.3). Finally, these bounds combined with formula (6.2) give the estimate of .

For any and , consider the integro-differential operators

| (6.6) | ||||

| (6.7) |

The function where

| (6.8) | ||||

| (6.9) |

is the fundamental solution of . Analogously, the function where

| (6.10) | ||||

| (6.11) |

is the fundamental solution of . Note that under our assumptions, at order zero, by (4.4)-(4.5) we have

| (6.12) |

We also recall the definition of convolution operator :

| (6.13) |

Note that, for any , we have

| (6.14) | ||||

| (6.15) |

Proposition 6.1.

For any and , there exists a positive constant , only dependent on , and , such that

| (6.16) |

for any , and with .

The proof of Proposition 6.1 is postponed to Section 6.1. We are now in position to prove Theorem 4.4. Indeed, by equations (6.2), (6.3) and Proposition 6.1 we have

| (and by Lemma 6.4 with ) | |||||

| . | |||||

Now, by the semigroup property

| (6.17) |

we get

for any and with , and since

can be easily checked to be convergent, this concludes the proof of Theorem 4.4.

We conclude this section with a brief discussion on how to drop the additional hypothesis on the coefficients introduced at the beginning of the section. In order to include state-dependency in the standard deviation of the jumps, i.e. , no modification is required in the first part of the proof since all the preliminary lemmas in Section 6.3 naturally apply to the general case. On the other hand, the proof of Proposition 6.1 requires some simple modifications to account for the additional terms in the expansion introduced by the state dependency of the convolution operator (see Proposition 4.1). To extend the proof to non-null mean of the jumps, i.e. , it is enough to extend Lemmas 6.4-6.10 to the more general functions such as

| (6.18) | ||||

| (6.19) |

As for the time-dependency of the coefficients and , the proof easily follows by the regularity hypothesis iii) in Assumption 4.3.

6.1 Proof of Proposition 6.1

The proof of Proposition 6.1 is based on the two following propositions.

Proposition 6.2.

For any and , there exists a positive constant , only dependent on and , such that

| (6.20) |

for any , and with .

Proof.

Recalling the expression of in (6.12), the case directly follows from Lemmas 6.5, 6.8 and 6.4 with .

For the case we first observe that, by Theorem 3.7 along with Proposition 4.1, the function takes the form

| (6.21) |

where is the operator

| (6.22) |

whereas acts as

| (6.23) |

and is the convolution operator defined in (6.13). Therefore, we have

In the computations that follow below, in order to shorten notation, we omit the dependence of in any function. By the commutative property of the operators and , and by applying Lemmas 6.5, 6.6 and 6.8 with , there exists a positive constant only dependent on and such that

| (6.24) | ||||

| (6.25) | ||||

| (6.26) | ||||

| (6.27) |

for any and with . Analogously, by the commutative property of and , and by applying Lemmas 6.8, 6.5, 6.9 and 6.7 with , there exists a positive constant only dependent on and such that

| (6.28) | ||||

| (6.29) |

for any and with . Then, (6.20) follows from (6.27) and (6.29) by applying Lemma 6.4 with and respectively. ∎

Proposition 6.3.

For any and , there exists a positive constant , only dependent on and , such that

| (6.30) |

for any , and with .

Proof.

For simplicity we only prove the thesis for . The proof for is entirely analogous to that of Proposition 6.2. Once again, hereafter we omit the dependence of in any function we consider. Recalling the expression of in (6.12), by Lemmas 6.5, 6.8 and 6.9, there exists a positive constant only dependent on such that

for any and with . Then, (6.30) follows from Lemma 6.4 with and with . ∎

We are now in position to prove Proposition 6.1.

Proof of Proposition 6.1.

We first prove the case . Let us define the operators

Let us recall that, by (3.12) and (3.13) with , we have

Thus, by (6.4) we have

where and are explicitly given by

| (6.31) | ||||

| (6.32) | ||||

| (6.33) |

Thus, by the Lipschitz assumptions on , and their first order derivatives, we obtain

| (6.34) | ||||

| (6.35) | ||||

| (6.36) |

and, as implies , by Propositions 6.2 and 6.3 there exists a positive constant , only dependent on ,,, and , such that (6.16) holds for and . To prove the general case, we proceed by induction on . First note that, by (3.12) we have

| (6.37) | ||||

| (and by (6.31) and the Lipschitz property of ) | ||||

| (6.38) | ||||

| (6.39) | ||||

| (and by applying Lemmas 6.4, 6.5, 6.8 and 6.9 with ) | ||||

| (6.40) | ||||

for any and with , and where is a positive constant only dependent on and . Assume now (6.16) holds for . Then by (6.5) we obtain

| (6.41) | ||||

| (and by inductive hypothesis and by (6.40)) | ||||

| (6.42) | ||||

| (6.43) | ||||

Now, by the semigroup property (6.17), and by the fact that777Here represents the Euler Gamma function.

| (6.44) |

with , we obtain

| (6.45) | ||||

| (6.46) |

Now, by Lemma 6.10 we have

| (6.47) | ||||

| (6.48) |

Inserting the above results into (6.46) we obtain

| (6.49) | ||||

| (6.50) |

where

| (6.51) |

Now, without loss of generality we can assume , and thus we obtain (6.16) for .

The proof for is based on the same arguments. However, in the general case the technical details become significantly more complicated. In practice, proceeding by induction, one can extend Propositions 6.2 and Proposition 6.3 to a general . Eventually, after proving the identity

| (6.52) |

one will be able to prove the estimate (6.16) on for a generic . Finally, the case is simpler because the identity (6.52) simply reduces to

| (6.53) |

and the proof becomes a simple application of Lemmas 6.4-6.10. ∎

6.2 Discussion on the difference with respect to the diffusion case

It has been proved by Pagliarani et al. (2013) that, in the purely diffusive case (i.e ), error bounds analogous to (4.19) hold with

In other words, the rate of convergence of the -th order approximation as is proportional to . The expansion is thus asymptotically convergent in . On the other hand, Theorem 4.4 shows that, when considering non-null Lévy measures, the rate of convergence do not improve for greater than .

The reasons for this discrepancy can be found in the different asymptotic behaviors of the leading term in the fundamental solution expansion of , with and without jumps. Indeed, while the short-time asymptotic behavior at the pole does not change whether or not, namely as goes to , the asymptotic behavior away from the pole radically changes when passing from the purely diffusion to the jump-diffusion case. In particular, by (6.8)-(6.9)-(6.12) it is clear that in general as goes to . On the other hand, in the particular case of being strictly differential, i.e. , the leading term reduces to

which is the Gaussian fundamental solution of a heat-type operator, and thus tends to exponentially as goes to . For this reason, the differential version of Lemma 6.9 becomes

| (6.54) |

as it is also clear by Lemma 6.8 with . Due to this fact, in the purely diffusive case, higher order polynomials of the kind arising from the -th order Taylor expansion of the operator , allow to gain an accuracy factor equal to . On the contrary, in the jump-diffusion case, such polynomials can be only used to cancel out the negative powers of the time introduced by the space derivatives, by combining Lemma 6.5 and Lemma 6.8.

6.3 Pointwise estimates

In the rest of the section, we will always assume that

| (6.55) |

Even if not explicitly stated, all the constants appearing in the estimates (6.56), (6.57), (6.59), (6.63), (6.66) and (6.70) of the following lemmas will depend also on .

Lemma 6.4.

For any and there exists a positive constant such that888Here denotes the identity operator.

| (6.56) |

for any , and .

Proof.

Lemma 6.5.

For any , and , there exists a positive constant such that

| (6.57) |

for any , and .

Proof.

For any we have

where is a polynomial of degree . To prove the Lemma we will show that there exists a positive constant , which depends only on and , such that

| (6.58) |

Proceeding as above, we set

where

Then the thesis follows from the boundedness of on , uniformly with respect to and in (6.55). Indeed the maximum of can be computed explicitly and we have

∎

Lemma 6.6.

For any and , there exists a positive constant such that

| (6.59) |

for any and .

Proof.

We first prove there exists a constant , which depends only on and , such that

| (6.61) | ||||

| (6.62) |

for any , , and in (6.55). To prove (6.61) we observe that

where

Now it is easy to check that

for any . Thus is bounded on , uniformly with respect to and in (6.55). To see the above bound, simply observe that

The proof of (6.62) is completely analogous. Finally, by (6.61)-(6.62) we have

∎

Lemma 6.7.

For any and with , there exists a positive constant such that

| (6.63) |

for any and .

Proof.

Lemma 6.8.

For any , and , there exists a positive constant such that

| (6.66) |

for any , and .

Proof.

We first show that there exist three constants , and such that

| (6.67) | ||||

| (6.68) | ||||

| (6.69) |

for any , and . In order to prove (6.67) we consider

and show that

for any . Thus is bounded on , uniformly in and in (6.55). The proof of (6.69) is completely analogous. Equation (6.68) comes directly by setting

Now, by (6.67) we have

| (by (6.68)) | ||||

| (by (6.69)) | ||||

∎

Lemma 6.9.

For any , and there exists a positive constant such that

| (6.70) |

for any and .

Proof.

Lemma 6.10.

For any and we have

| (6.71) |

Proof.

References

- Ait-Sahalia and Jacod (2012) Ait-Sahalia, Y. and J. Jacod (2012). Analyzing the spectrum of asset returns: Jump and volatility components in high frequency data. Journal of Economic Literature 50(4), 1007–50.

- Almendral and Oosterlee (2005) Almendral, A. and C. W. Oosterlee (2005). Numerical valuation of options with jumps in the underlying. Appl. Numer. Math. 53(1), 1–18.

- Andersen and Andreasen (2000) Andersen, L. and J. Andreasen (2000). Jump-diffusion processes: Volatility smile fitting and numerical methods for option pricing. Review of Derivatives Research 4(3), 231–262.

- Barndorff-Nielsen (1998) Barndorff-Nielsen, O. (1998). Processes of normal inverse Gaussian type. Finance and Stochastics 2, 41–68.

- Benhamou et al. (2009) Benhamou, E., E. Gobet, and M. Miri (2009). Smart expansion and fast calibration for jump diffusions. Finance and Stochastics 13(4), 563–589.

- Bielecki and Rutkowski (2001) Bielecki, T. and M. Rutkowski (2001). Credit Risk: Modelling, Valuation and Hedging. Springer.

- Borodin and Salminen (2002) Borodin, A. and P. Salminen (2002). Handbook of Brownian motion: facts and formulae. Birkhauser.

- Boyarchenko and Levendorskii (2002) Boyarchenko, S. and S. Levendorskii (2002). Non-Gaussian Merton-Black-Scholes Theory. World Scientific.

- Boyarchenko and Levendorskii (2000) Boyarchenko, S. I. and S. Z. Levendorskii (2000). Option pricing for truncated Lévy processes. International Journal of Theoretical and Applied Finance 03(03), 549–552.

- Capponi et al. (2013) Capponi, A., S. Pagliarani, and T. Vargiolu (2013). Pricing vulnerable claims in a Lévy driven model. preprint SSRN.

- Carr and Linetsky (2006) Carr, P. and V. Linetsky (2006). A jump to default extended CEV model: An application of Bessel processes. Finance and Stochastics 10(3), 303–330.

- Cont and Tankov (2004) Cont, R. and P. Tankov (2004). Financial modelling with jump processes, Volume 2. Chapman & Hall.

- Corielli et al. (2011) Corielli, F., P. Foschi, and A. Pascucci (2011). Parametrix approximation of diffusion transition densities. SIAM Journal of Financial Mathematics, 833–867.

- Cox (1975) Cox, J. (1975). Notes on option pricing I: Constant elasticity of diffusions. Unpublished draft, Stanford University. A revised version of the paper was published by the Journal of Portfolio Management in 1996.

- d’Halluin et al. (2005) d’Halluin, Y., P. A. Forsyth, and K. R. Vetzal (2005). Robust numerical methods for contingent claims under jump diffusion processes. IMA J. Numer. Anal. 25(1), 87–112.

- Di Francesco and Pascucci (2005) Di Francesco, M. and A. Pascucci (2005). On a class of degenerate parabolic equations of Kolmogorov type. AMRX Appl. Math. Res. Express 3, 77–116.

- Eraker (2004) Eraker, B. (2004). Do stock prices and volatility jump? Reconciling evidence from spot and option prices. The Journal of Finance 59(3), 1367–1404.

- Friedman (1964) Friedman, A. (1964). Partial differential equations of parabolic type. Englewood Cliffs, N.J.: Prentice-Hall Inc.

- Friz et al. (2013) Friz, P. K., S. Gerhold, and M. Yor (2013). How to make Dupire’s local volatility work with jumps. arXiv preprint1302.5548.

- Garroni and Menaldi (1992) Garroni, M. G. and J.-L. Menaldi (1992). Green functions for second order parabolic integro-differential problems, Volume 275 of Pitman Research Notes in Mathematics Series. Harlow: Longman Scientific & Technical.

- Heston (1993) Heston, S. (1993). A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Financ. Stud. 6(2), 327–343.

- Hoh (1998) Hoh, W. (1998). Pseudo differential operators generating Markov processes. Habilitations-schrift, Universität Bielefeld.

- Jacob (2001) Jacob, N. (2001). Pseudo differential operators and Markov processes. vol. 1: Fourier analysis and semigroups.

- Jacquier and Lorig (2013) Jacquier, A. and M. Lorig (2013). The smile of certain Lévy-type models. SIAM Journal on Financial Mathematics 4.

- Levi (1907) Levi, E. E. (1907). Sulle equazioni lineari totalmente ellittiche alle derivate parziali. Rend. Circ. Mat. Palermo 24, 275–317.

- Lewis (2000) Lewis, A. (2000). Option Valuation under Stochastic Volatility. Finance Press.

- Lewis (2001) Lewis, A. (2001). A simple option formula for general jump-diffusion and other exponential Lévy processes.

- Linetsky (2006) Linetsky, V. (2006). Pricing equity derivatives subject to bankruptcy. Mathematical Finance 16(2), 255–282.

- Lipton (2002) Lipton, A. (2002). The vol smile problem. Risk (February), 61–65.

- Lorig et al. (2013) Lorig, M., S. Pagliarani, and A. Pascucci (2013). Analytical expansions for parabolic equations. ArXiv preprint arXiv:1312.3314.

- Lorig et al. (2014a) Lorig, M., S. Pagliarani, and A. Pascucci (2014a). Asymptotics for -dimensional Lévy-type processes. In Asymptotic methods in finance. Springer.

- Lorig et al. (2014b) Lorig, M., S. Pagliarani, and A. Pascucci (2014b). Explicit implied vols for multifactor local-stochastic vol models. ArXiv preprint arXiv:1306.5447.

- Lorig et al. (2014c) Lorig, M., S. Pagliarani, and A. Pascucci (2014c). A family of density expansions for Lévy-type processes. To appear in Annals of Applied Probability.

- Lorig et al. (2014d) Lorig, M., S. Pagliarani, and A. Pascucci (2014d). A Taylor series approach to pricing and implied vol for LSV models. To appear in: Journal of Risk.

- Mendoza-Arriaga et al. (2010) Mendoza-Arriaga, R., P. Carr, and V. Linetsky (2010). Time-changed Markov processes in unified credit-equity modeling. Mathematical Finance 20, 527–569.

- Oksendal and Sulem (2005) Oksendal, B. and A. Sulem (2005). Applied stochastic control of jump diffusions. Springer Verlag.

- Pagliarani and Pascucci (2013) Pagliarani, S. and A. Pascucci (2013). Local stochastic volatility with jumps: analytical approximations. Int. J. Theor. Appl. Finance 16(8), 1350050, 35.

- Pagliarani et al. (2013) Pagliarani, S., A. Pascucci, and C. Riga (2013). Adjoint expansions in local Lévy models. SIAM J. Finan. Math. 4(1), 265–296.

- Pascucci (2011) Pascucci, A. (2011). PDE and martingale methods in option pricing. Bocconi&Springer Series. New York: Springer-Verlag.

- Sato (1999) Sato, K. (1999). Lévy processes and infinitely divisible distributions. Cambridge University Press.

|

|

|

|

|

|

|

|

|

|

|

|

| 1 | 0.1232 | 0.1138 | 0.1078 |

|---|---|---|---|

| 2 | 0.0083 | 0.0160 | 0.0217 |

| 3 | 0.0014 | 0.0056 | 0.0118 |

| 4 | 0.0004 | 0.0028 | 0.0088 |

Computation time relative to

| 1 | 1.14 | 1.07 | 1.04 |

|---|---|---|---|

| 2 | 1.59 | 1.50 | 1.45 |

| 3 | 2.32 | 2.28 | 2.21 |

| 4 | 3.46 | 3.30 | 3.25 |

|

|

| 1.0 | 0.1835 | -0.0065 | 0.0022 | 0.0001 |

|---|---|---|---|---|

| 2.0 | 0.1777 | -0.0123 | 0.0048 | 0.0003 |

| 3.0 | 0.1720 | -0.0180 | 0.0071 | 0.0003 |

| 4.0 | 0.1663 | -0.0237 | 0.0089 | -0.0001 |

| 5.0 | 0.1605 | -0.0295 | 0.0099 | -0.0006 |

| 6.0 | 0.1548 | -0.0352 | 0.0102 | -0.0011 |

| 7.0 | 0.1493 | -0.0407 | 0.0101 | -0.0013 |

| 8.0 | 0.1442 | -0.0458 | 0.0095 | -0.0011 |

| 9.0 | 0.1394 | -0.0506 | 0.0087 | -0.0005 |

| 10.0 | 0.1351 | -0.0549 | 0.0077 | 0.0007 |

|

|

|

|

|

|

|

|

|

|