A CONVOLUTION METHOD FOR NUMERICAL SOLUTION OF BACKWARD STOCHASTIC DIFFERENTIAL EQUATIONS

Abstract

We propose a new method for the numerical solution of backward stochastic differential equations (BSDEs) which finds its roots in Fourier analysis. The method consists of an Euler time discretization of the BSDE with certain conditional expectations expressed in terms of Fourier transforms and computed using the fast Fourier transform (FFT). The problem of error control is addressed and a local error analysis is provided. We consider the extension of the method to forward-backward stochastic differential equations (FBSDEs) and reflected FBSDEs. Numerical examples are considered from finance demonstrating the performance of the method.

Key words: backward stochastic differential equations (BSDEs), reflected BSDEs, fast Fourier transform, parabolic PDE, numerical approximation, option valuation.

AMS 200 subject classifications: Primary 60H10, 65C30; secondary 60H30.

1 Introduction

Backward stochastic differential equations (BSDEs) have been a topic of interest since the early work of [6] and the results of [33] on their well-posedness. A BSDE is an equation of the form

| (1) |

defined on a complete filtered probability space where is a standard -dimensional Brownian motion, the terminal condition is a square integrable -measurable random variable and the driver is a functional. It is known from [33] that there exists a unique adapted square integrable backward process taking values in and a unique predictable process with values in satisfying equation (1) under Lipschitz and integrability conditions on the driver .

Many works have extended this existence and uniqueness result. [1] introduced forward-backward stochastic differential equations (FBSDEs). [30], [27] and [24] among others treat non-Lipschitz cases. Also, the theory of BSDEs has found various applications, particularly in finance and in the study of partial differential equations (PDEs). From [34] (see also [19, Section 4.1]) we have that if the Cauchy problem to the one-dimensional diffusion PDE

| (2) |

has a unique solution then the solution for the BSDE (1) with terminal condition admits the representation

| (3) | |||||

| (4) |

Conversely, the solution of the PDE (2) can be interpreted in terms of the solution of the BSDE (1). General formulations of the nonlinear Feynman-Kac formula for FBSDEs, quasilinear parabolic PDEs, and viscosity solutions have been studied extensively.

Deriving an explicit solution to a nontrivial (F)BSDE is possible only in very few situations, such as [40], [23] and [37]. Thus, numerical methods for BSDEs have been studied extensively. Numerical methods for (F)BSDEs can be classified into three main groups: PDE based methods, spatial discretization based methods, and Monte-Carlo based methods. PDE based methods, which started with the finite difference approach of [16], consider a numerical resolution of the nonlinear parabolic PDE related to the (F)BSDE. The two other methods rely on a time discretization of the (F)BSDE. Spatial discretization based methods (see [12], [2], [15], [13], [38] or [35] among others) use a deterministic space grid. On the other hand, the space discretization is random in Monte-Carlo based methods (for instance, [9], [22], and [3]).

In this paper, we propose an alternative spatial discretization method for BSDEs and illustrate its implementation in the one-dimensional case. To the best of our knowledge, the most efficient approach in this simple case is the binomial method of [35] which has connections with the theoretical work of [10] and [29]. However, our method avoids a notable drawback of the binomial method: the contraction of the space grid leading to the approximation of the Wiener process by means of scaled random walks. Indeed, we use a fixed equidistant space grid, thus allowing an exact simulation of the Wiener process at time nodes. The FFT algorithm, which plays a key role in our method, helps in producing an efficient algorithm. As in [11] and [28] in the context of option pricing under Lévy processes, we employ the FFT algorithm to compute quadratures. The presence of dynamic programming through the Euler scheme is a major similarity between our method and [28]. The method presented in [38] is somewhat similar in that transform methods are employed, but differs in the discretization scheme and the use of the Fourier-cosine expansion.

This paper is structured as follows. Section 2 reviews Euler time discretization schemes for BSDEs which are used in Section 3 to develop the convolution method. Section 4 presents a detailed error analysis of the convolution method. Some extensions of the method are presented in Section 5, numerical results for examples from finance are included in Section 6, and Section 7 concludes.

2 Time discretization of BSDEs

The convolution method developed in this paper, as any spatial discretization based method, requires the availability of a time discretization scheme for BSDEs. In this section, we Euler time discretization schemes that are widely used in numerical methods for BSDEs. Alternatives to the Euler schemes can be found in the schemes of [43] or the penalization scheme proposed by [35] inspired by a method used by [17] to prove well-posedness of reflected BSDEs. Convergence of the Euler schemes are considered by [41, 42] and [9].

For simplicity of notation we shall suppose all processes are one-dimensional (). Further, we make the following assumption to ensure existence and uniqueness of a solution to the BSDE (1).

Assumption 2.1.

We suppose a Markovian terminal condition with

| (5) |

where is real function satisfying the square integrability condition

| (6) |

In addition, both the terminal condition and the driver verify the Lipschitz condition

| (7) |

for some constant , , and .

Consider the time mesh on the time interval with time steps. Let and denote the approximate solution at time node . BSDEs with a Markovian terminal condition we set .

| (8) |

which we call the explicit Euler scheme I. Another explicit scheme consists of replacing the conditional expectation of the driver in the explicit Euler scheme I by the driver evaluated at the conditional expectations of the arguments. This procedure leads to

| (9) |

which we call the explicit Euler scheme II. The approximate processes then takes the form

| (10) |

on the entire time interval.

The global discretization error is defined as

| (11) |

for any version of the Euler scheme. Due to the Lipschitz nature of the driver , it can be proved that the explicit schemes have a first order quadratic error as noted by [8, Remark 2.1.1].

Theorem 2.1.

Under the setting of Assumption 2.1, the Euler schemes yield a first order quadratic error

| (12) |

3 Convolution method

In this section, we introduce the convolution method for the numerical solution of the BSDE (1). The method involves expressing the conditional expectations in an explicit Euler time discretization of the BSDE as convolutions, calculating the Fourier transform of the approximate solution, applying the convolution theorem of Fourier analysis, and taking the inverse Fourier transform of the results in order to recover expressions for the approximate solution which are recursive backward in time. In order to implement the convolution method we present the discretization of intermediate quadratures and their relationship to the discrete Fourier transform (DFT) which can be efficiently computed using the fast Fourier transform (FFT).

3.1 Convolution on the explicit Euler scheme II

The starting point of the convolution method for BSDEs is an explicit Euler scheme. If we consider the explicit Euler scheme II of equation (9) an approximate solution of the BSDE (1) at mesh time consists of real-valued functions , , and defined by the backward recursions

| (13) | ||||

| (14) | ||||

| (15) |

for and . Note that represents the approximate process and stands for the approximate process at mesh time while is an intermediate quantity. The notation used in equations (13)-(15) is not to be confused with the solution of the PDE (2) as we do not employ the representation (3)-(4) in this paper. The function is the density function of conditional on the value of

| (16) |

If a method for calculating the integrals of equations (14) and (15) is available, then the sequence for is an approximation to the BSDE solution of equations (3) and (4) on the interval . The stationarity and independence of Brownian increments allow us, as in [28], to express the functions and in equations (14) and (15) as convolutions. These convolutions suggest using Fourier transforms and hence the computation of the integrals via discrete Fourier transforms.

Recall the Fourier transform of an integrable real function is the function is defined as

| (17) |

where is the imaginary unit. The inverse Fourier transform recovers the function from its Fourier transform through the relation

| (18) |

For any real function define the dampened function as

| (19) |

where is a dampening parameter. Taking the Fourier transform of in equation (15) gives

| (20) |

using the convolution theorem. Moreover, making the change of variable ,

| (21) |

where is the characteristic function of the density .

The equality of equation (21) is well-defined since for any . We introduce the dampening parameter to ensure relative periodicity for the functions as shown in the sequel. In practice, integrability is not necessary since a truncation is performed in the numerical implementation. Combining equations (20) and (21) gives

| (22) |

Similarly, the Fourier transform of in equation (14) is given by

| (23) | |||||

using the differentiation properties of the Fourier transform.

From equations (22) and (23), we recover the functions and by taking the inverse Fourier transform and adjusting for the dampening factor

| (24) | |||||

| (25) |

Equations (13), (24), and (25), evaluated at , define a convolution method for the approximate solution of the BSDE (1) based on the explicit Euler scheme II.

3.2 Convolution on the explicit Euler scheme I

An alternative characterization of the approximate solution of the BSDE (1) is obtained if one considers the explicit Euler scheme I of equation (8). In this case, the approximate solution consists of functions and at mesh time which take the form

| (26) |

where

| (27) | ||||

| (28) |

for and .

Following the steps of the previous characterization equations (26) and (28) lead naturally to

| (29) | ||||

| (30) |

where both and for along with the dampened terminal condition are assumed to be integrable so that they admit Fourier transforms. Equations (27), (29), and (30) define a convolution method for the approximate solution of the BSDE (1) based on the explicit Euler scheme I.

3.3 Numerical implementation

From equations (24) and (25) or equations (29) and (30) one notices that computing the approximate solutions (, ) and (, ) at mesh time reduces to computing a function depending on two functions and in the following manner

| (31) |

if we drop the dampening factor .

This integral is numerically computed by discretizing the Fourier space with a uniform grid of points on the interval of length , where is even, such that

| (32) |

with and . Hence, for any

| (33) | |||||

where the integral is approximated using lower Riemann sums and

| (34) |

This last integral is also computed using an uniform grid of points on the restricted interval centred at such that

| (35) |

where is chosen so that the Nyquist relation is satisfied.

The discretization of the integral in equation (34) leads to an expression involving the discrete Fourier transform (DFT). The DFT is a numerical procedure that transforms a set of real or complex numbers into another set through the relation

| (36) |

for . The inverse DFT performs a reciprocal operation by computing the set of numbers using the numbers as

| (37) |

for .

As we intend to use the DFT to compute (33) and (34) we assume that the following conditions are satisfied.

Assumption 3.1.

The generic dampened function and its derivative have the same values at the boundaries of the restricted domain

| (38) | |||||

| (39) |

We approximate the integral of equation (34) by first restricting the integration interval to and then applying a composite quadrature rule with weights . Consequently,

| (41) |

for using Assumption 3.1 since is even and with

| (42) |

where stands for the Kronecker’s delta. At this point many quadrature rules are available. For example, one may use the composite trapezoidal rule with weights of the form

| (43) |

leading to . Higher order composite quadrature rules will improve accuracy in presence of a smooth driver .

A similar approach can be found in [28] which enhanced the discrete Fourier transform with a composite trapezoidal quadrature rule to compute this last integral. However, [28] omits Assumption 3.1 making the error analysis quite tedious and leading to considerable numerical errors, especially around the boundaries of the restricted domain. In addition, we use a fixed space grid whereas [28] shift the space grid through time steps. The major difference, however, is that the scheme in [28] solves the Snell envelope and does not seek a numerical solution for BSDEs.

Remark 3.1.

From equation (3.3), the restriction of the real line to the interval also solves the problem of integrability of the generic dampened function that we pointed out preceding equation (22). Indeed, the restriction is essentially equivalent to considering the truncated function . Hence, needs to be integrable only on the restricted domain.

The values of the functions are computed at the grid points by combining equations (33) and (41)

| (44) | |||||

Since we use the DFT, the underlying trigonometric (and hence periodic) interpolation allows us to set

| (45) |

In applications we shall consider functions that do not satisfy Assumption 3.1. To address this problem we slightly modify the function by adding a linear function to obtain a modified dampened function defined as

| (46) |

The following lemma gives the appropriate choice for the dampening parameter , and the coefficients and .

Lemma 3.1.

Suppose the real function is differentiable with

and let be the modified, dampened function defined in equation (46). Then

| (47) | |||||

| (48) |

solve the system of nonlinear equations

| (49) | |||||

| (50) |

for any . In addition, if

| (51) |

then and .

Proof.

The transform of equation (46) may seem over parametrized. However, using only two parameters may lead to complex parameters or to an inconsistent system.

Remark 3.2.

When implementing the method, the values of the derivative at and can be approximated by forward or backward finite differences.

Remark 3.3.

A positive constant, , which represents the minimal slope allowed in the linear transform is used to ensure equation (51) is enforced. Set

| (52) |

Under the transformation of equation (46), the computation of our approximate solution is not significantly more complex. Since the function is a (dampened) conditional expectation, properties of the conditional expectation allows the necessary adjustments as shown in the following theorem.

Theorem 3.1.

Proof.

First, let . By definition, we know that

Similarly, if , we have

∎

Theorem 3.1 shows that the computational formula of equation (44) can be applied to the dampened transform function which satisfies Assumption 3.1 after an appropriate choice of the coefficients , and using Lemma 3.1. One recovers the function by subtracting the function .

The implementation of the convolution method gives the numerical approximations and to the approximate solutions and at space nodes for any time node , . An approximate solution to the BSDE consists of a (linear) interpolation of a Brownian path through the node values and for . The following algorithm summarizes the steps necessary to implement the convolution method.

Algorithm 3.1.

Convolution Method

-

1.

Discretize the restricted real space and the restricted Fourier space with space steps so to have the real space nodes and the Fourier space nodes

-

2.

Set

-

3.

For any from

- (a)

- (b)

- (c)

- (d)

We next consider the problem of computational error.

4 Error Analysis

The convolution method induces two main types of error. In addition to the time discretization error discussed in Section 2, there is a space discretization error and we focus on this last error term. We limit our analysis to the explicit Euler scheme II since equivalent results are obtained for the explicit Euler scheme I using the same techniques.

Throughout this section , and denote the numerical solution obtained from the convolution method at time mesh , knowing the approximate solutions and at time mesh . The convolution method induces a space discretization error when approximating the values of and by and respectively. We will particularly describe the local behaviour of this error term. We define it as

| (61) |

The following lemma describes the DFT accuracy in approximating the Fourier coefficients and proves useful in the derivation of a space discretization error bound. We skip the proof since the results are well known (see [36, Theorem 3.4, p. 140] and [39, Theorem 4.4, p. 85]).

Lemma 4.1.

Suppose the integrable function

with

admits the Fourier series expansion

| (62) |

and are the nodes of the equidistant grid of

such that

where is even and .

If then

| (63) |

for and

| (64) |

for and some constant depending on . Consequently,

| (65) |

The next theorem gives an error bound for the space discretization error under smoothness conditions on the BSDE coefficients and .

Theorem 4.1.

Suppose and . Then for any and , the convolution method applied on the truncated interval yields a (local) discretization error of the form

| (66) |

where the extrapolation error satisfies

| (67) |

for some positive constants depending on the driver , the function , and the terminal time when using the trapezoidal quadrature rule.

Proof.

Suppose the solution at time is known. Since and , it is easily shown that . Also, we know from [42] and [9] that is square integrable so that is square integrable (with respect to the Gaussian density).

In light of Theorem 3.1, we can limit ourselves to the case where

so that . Let be the Fourier coefficients of on . We have that

where

for some constant by successively applying Cauchy-Schwartz and Chernoff inequalities since the solution is square integrable. Hence

| (68) | |||||

where for . So that, on one hand, we have

| (69) | |||||

| (by Lemma 4.1), | |||||

| (by boundedness of and Chernoff inequality), | |||||

Assuming , without loss of generality, define as

since is periodic and on the interval . Equation (68) becomes

| (70) |

and we note, by the continuity of , that

| (71) |

for some positive constant .

Similarly

where

| (by Cauchy-Schwartz inequality), | ||||

| (by successively applying Cauchy-Schwartz and Chernoff inequalities), | ||||

Hence

| (72) | |||||

Letting , we have

| (73) | |||||

| (by Lemma 4.1 since is bounded), | |||||

| (by boundedness of and Chernoff inequality), | |||||

| (74) |

where and, letting ,

for some . Since is the Fourier expansion of and , we have

| (75) | |||||

by the Cauchy-Schwartz inequality, for some constant .

Theorem 4.1 decomposes the spatial discretization error in three parts: the truncation error, the discretization error and the extrapolation error. Most PDE based and spatial discretization based methods for BSDEs fail in giving a bound for the error due to truncation. The error analysis shows that the truncation error has a spectral convergence of index 2 when applying the convolution method. Also, the discretization error , of first order, is similar to PDE based methods such as [16] or [31].

The extrapolation error is specific to the convolution method implemented using the DFT. Equation (67) shows that errors appear and may accumulate around the boundaries of the truncated domain. Nonetheless, the extrapolation error is mainly time related through the density and can be confined at the boundaries for fine time discretizations as shown in the following corollary.

Corollary 4.1.

Proof.

We define the global convergence error for each space node as

| (77) |

where

| (78) |

and

| (79) |

for with . The next theorem describes the stability and convergence properties of the convolution method.

Theorem 4.2.

Suppose the conditions of Theorem 4.1 are satisfied and let be the Gaussian density with zero mean and variance . If the discretization is such that

| (80) |

then the convolution method is stable and the global discretization error satisfies

| (81) |

where

| (82) |

for some constants depending on the driver , the terminal function and the terminal time . Finally .

Proof.

First note that from the definitions of equations (61) and (78)

| (83) | |||||

where is the Lipschitz constant of the driver . Also, we have that

| (84) |

Furthermore, the construction of the convolution method gives

| (85) | |||||

| (by Theorem 4.1 since the transform functions are given), | |||||

| (using the matrix-vector representation of DFTs), | |||||

Similarly,

| (86) | |||||

| (by Theorem 4.1 since the transform functions are given), | |||||

| (using the matrix representation of DFTs), | |||||

Then, combining the inequalities of equations (83), (85) and (86) leads to

where and is the Lipschitz constant of the driver . So that

| (87) | |||||

for some positive number satisfying

From the inequality of equation (87), Gronwall’s Lemma yields

| (88) |

for knowing that . Hence, the convolution method is stable for the approximate solution since its error at any time step is absolutely bounded.

5 Extensions

Various extensions of the convolution method can be made. We consider the convolution method under decoupled FBSDEs and reflected FBSDEs. These cases have interesting applications in mathematical finance, especially for option pricing.

5.1 Forward-backward stochastic differential equations

We can extend the convolution method to consider FBSDEs

| (90) |

associated to the Cauchy problem for the advection-diffusion equation

| (91) |

to which an obstacle can be added when in presence of a reflected FBSDE. When discretized with the Euler scheme, the FBSDE numerical solution is given by

| (92) |

The approximate solutions satisfy

| (93) | |||||

| (94) | |||||

where

| (95) | |||||

for and . The density of increments is Gaussian

| (96) |

with characteristic function

| (97) |

The development of the convolution method in this case also leads to transforms identical to equation (31). In our implementation, the and are actually estimates for but the scheme can easily be modified so as to estimate the derivative directly.

The equivalence

| (98) | |||||

of Theorem 3.1 still holds with

| (99) |

if and

| (100) |

if . Whenever the forward coefficients and depend on the state variable , a matrix multiplication in required to perform the DFTs.

Also, the convolution method can be used to compute conditional expectations under general Lévy processes as in [28] . Indeed, the independence of increments and the availability of the characteristic function are the only requirements to apply the method. The convolution method may also serve as a numerical method for partial differential integral equations (PIDE) under a Lévy process .

5.2 Reflected FBSDEs

Explicit Euler schemes have been constructed for reflected FBSDEs with continuous barrier which make it possible to apply the convolution method to such FBSDEs. Consider the solution of the system

| (101) |

where the lower barrier is a deterministic function of time and the Brownian motion and

| (102) |

This reflected FBSDE is associated to the following obstacle problem

| (103) |

as established by [17]. An adaptation of the explicit Euler scheme I provides the numerical solution to the reflected BSDE through the equations

| (104) |

where for any number , .

Time discretization of RBSDEs and their convergence were treated in [7] for the implicit Euler scheme. [35] proposed an equivalent scheme with a discrete filtration and proved its convergence under a binomial method. The scheme is easily solved with a convolution method by first noticing that the approximate solution at mesh time , where is the approximate reflection process, can be written as

| (105) | |||||

where

| (106) | |||||

| (107) | |||||

| (108) |

for and . The computation of and the integral part of the approximate solution is identical to the non-reflected case.

One can also naturally build an alternative scheme from the explicit Euler scheme II. The approximate solution , the approximate gradient and the approximate reflection at mesh time then take the form

| (109) |

where

| (110) | |||||

| (111) | |||||

| (112) |

for and .

6 Application to option pricing

We shall consider the case of BSDEs with non-linear and non-smooth drivers that present the lowest rate of convergence through option pricing problems. An introduction to financial applications of BSDEs, particularly to imperfect markets and American option problems, can be found in [20], [18] or [19].

The market model consists of a single risky asset (or stock) with the dynamics

| (113) |

where the process represents the stock return. We first consider a European call option with maturity and strike price under a lending rate of and a borrowing rate . The return process is an arithmetic Brownian motion

| (114) |

such that the stock has an initial value of , an expected return rate of , a dividend rate of and a volatility of .

The European call option price follows a BSDE with the return process as the forward process, the driver

| (115) |

and the terminal function

| (116) |

under the given imperfect market conditions. The American call option solves a reflected BSDE with the barrier function

| (117) |

6.1 Numerical Results

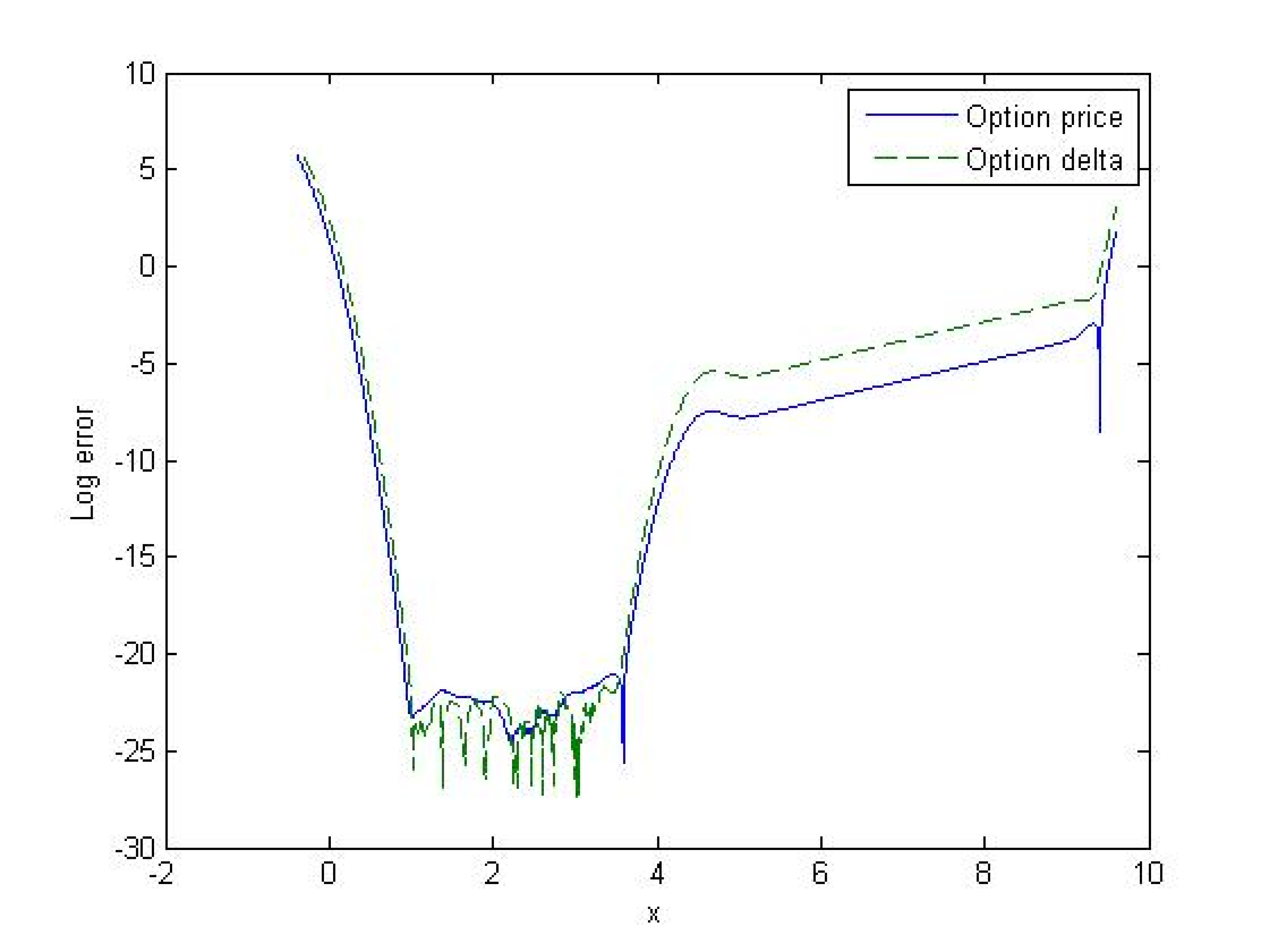

Suppose that , , , , and . When the borrowing rate equals the lending rate and , the European and the American call options have the same price. Figure 1 shows the structure of the absolute log error on European option prices and deltas where the true values are computed using the Black-Scholes formula. As expected errors are amplified at the boundaries of the truncated domain. Errors are also amplified for around-the-money options, to a lesser extent, due to the non-smoothness of the terminal function . In addition, out-of-the-money options have smaller absolute errors compared to in-the-money options.

, , , , , , .

Table 1 gives the relative percentage error for price estimates of the call option prices using both convolution schemes I and II for different time steps and the indicated strike prices. Table 2 gives the estimates for the call option deltas obtained from the approximate gradient by

| (118) |

when using the explicit Euler scheme II. The option prices and option deltas are calculated on the restricted domain with grid points and a minimal slope of (see Remark 3.3). The Black-Scholes formula gives call option prices of , and at strike prices , and respectively when the other variables are kept unchanged. The true values for the option deltas are , and when the strike price is and respectively.

The results of Table 1 and 2 show the accuracy of the convolution method on a RBSDE with a smooth linear driver. Indeed, the relative error percentages remain low (less than ) for the estimated option prices and deltas. Out-of-the-money option estimates seem to display the largest relative errors.

| K (Strike) | n=500 | n=1000 | n=2000 | n=5000 | |

|---|---|---|---|---|---|

| Convolution (Scheme I) | 110 | 0.0456 | 0.0217 | 0.0108 | 0.0043 |

| 100 | 0.0178 | 0.0095 | 0.0047 | 0.0024 | |

| 90 | 0.0049 | 0.0028 | 0.0014 | 0.0007 | |

| Convolution (Scheme II) | 110 | 0.0087 | 0.0239 | 0.0022 | 0.0001 |

| 100 | 0.0059 | 0.0024 | 0.0012 | 0.0007 | |

| 90 | 0.0028 | 0.0014 | 0.0007 | 0.0004 |

, , , , .

| K (Strike) | 90 | 100 | 110 |

|---|---|---|---|

| Convolution (Scheme I) | 0.0133 | 0.0010 | 0.2414 |

| Convolution (Scheme II) | 0.0133 | 0.0010 | 0.2414 |

, , , , .

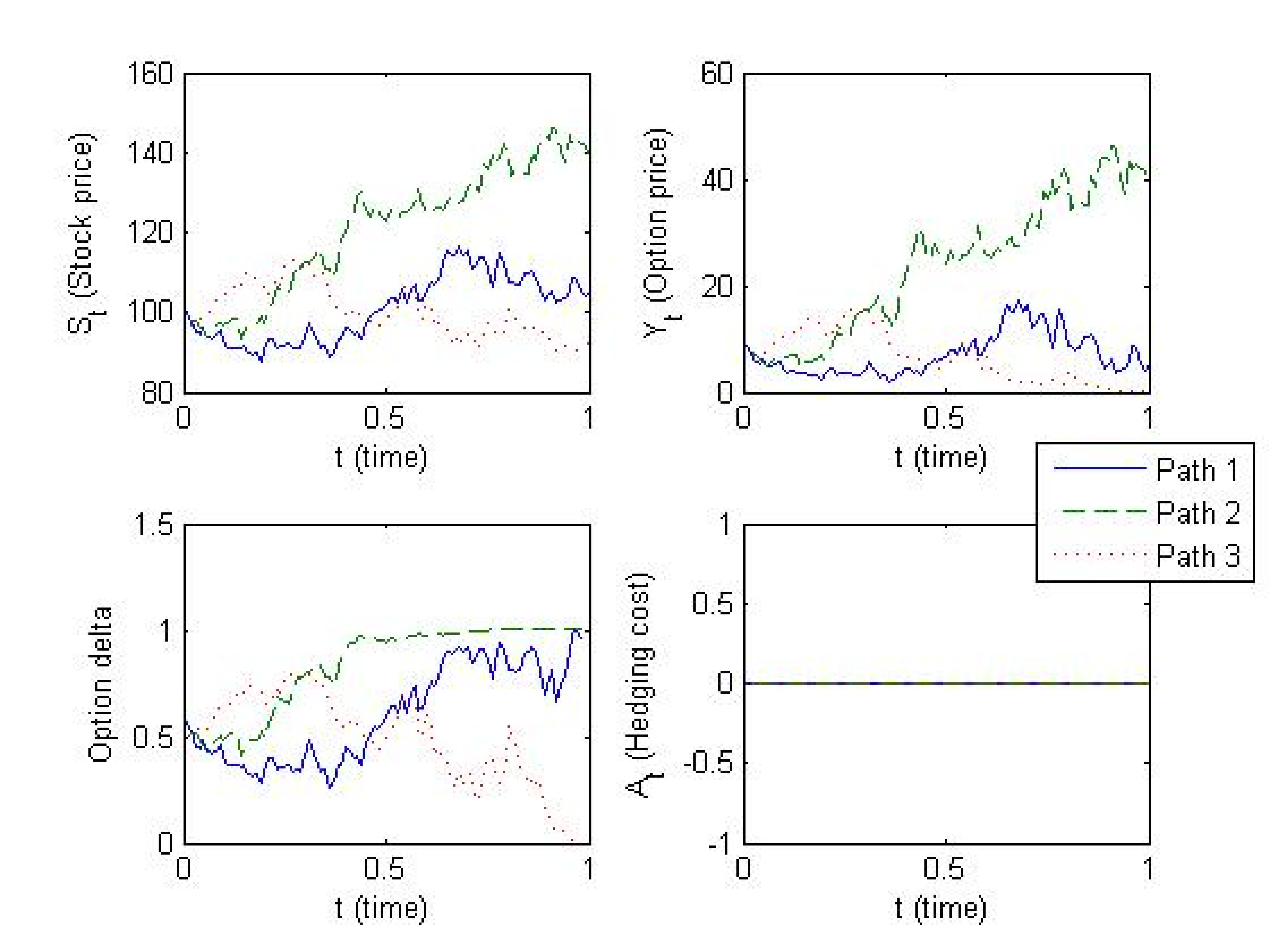

For a borrowing rate of and a dividend rate of , Table 3 shows the estimates for the European call prices when the option is at the money and . Moreover, the convolution methods return an option delta of , when applied with time steps. never hit the barrier . Paths are simulated using the solution from the convolution method applied on scheme II on the restricted domain with grid points, time steps and . We used time steps to simulate the stock price ().

| n (number of time steps) | 500 | 1000 | 2000 | 5000 |

|---|---|---|---|---|

| Convolution (Scheme I) | 9.4127 | 9.4131 | 9.4132 | 9.4133 |

| Convolution (Scheme II) | 9.4132 | 9.4133 | 9.4133 | 9.4134 |

, , , , , , .

, , , , , , , .

The option price can be calculated using a Monte-Carlo method such as the forward scheme of [3]. However, in the context of uni-dimensional BSDEs, Monte-Carlo methods will generally be less efficient than space discretization methods. As an illustration, the convolution method on both explicit Euler schemes runs in approximately seconds when pricing the options of Table 3 with time steps. On the other hand, the forward scheme runs in seconds with only time steps. We used the first power functions as basis functions and paths to generate the Monte-Carlo estimates. The Picard iterations are stopped whenever the difference in two consecutive prices is less than for a maximum number of iterations. Fifty independent valuations with the Monte-Carlo method give a confidence interval of which includes all estimates of Table 3. Hence, the convolution method gives satisfactory results even for coarse time discretization.

Table 4 provides price estimates for out-of-the-money and in-the-money options and Table 5 gives estimates for option deltas on a non-dividend-paying stock under imperfect market conditions. Both tables compare the estimates obtained with the convolution method those obtained with the binomial method of [35] . The convolution method and the binomial method give similar prices and delta values for all options which confirms the convolution method accuracy even for non-smooth drivers. Nonetheless, the binomial method is faster (less that tenth of a second for time steps) than the convolution method for the same number of time step when computing the BSDE initial values. However, simulation of BSDEs is easier under the convolution method where a simple interpolation using Brownian paths can be performed. Under the binomial method, Brownian paths must be approximated by scaled random walks.

| n (number of time steps) | K (Strike) | 500 | 1000 | 2000 | 5000 |

|---|---|---|---|---|---|

| Convolution (Scheme I) | 110 | 5.2924 | 5.2929 | 5.2931 | 5.2933 |

| 90 | 15.4289 | 15.4291 | 15.4292 | 15.4292 | |

| Convolution (Scheme II) | 110 | 5.2932 | 5.2933 | 5.2933 | 5.2934 |

| 90 | 15.4290 | 15.4291 | 15.4291 | 15.4292 | |

| Binomial Method | 110 | 5.2918 | 5.2945 | 5.2936 | 5.2937 |

| 90 | 15.4313 | 15.4263 | 15.4298 | 15.4292 | |

, , , , , .

| K (Strike) | 90 | 100 | 110 |

|---|---|---|---|

| Convolution (Scheme I) | 0.7814 | 0.5987 | 0.4104 |

| Convolution (Scheme II) | 0.7814 | 0.5987 | 0.4104 |

| Binomial Method | 0.7813 | 0.5987 | 0.4104 |

, , , , , , .

, , , , , , , .

(dividend paying stock with market frictions)

, , , , , , , .

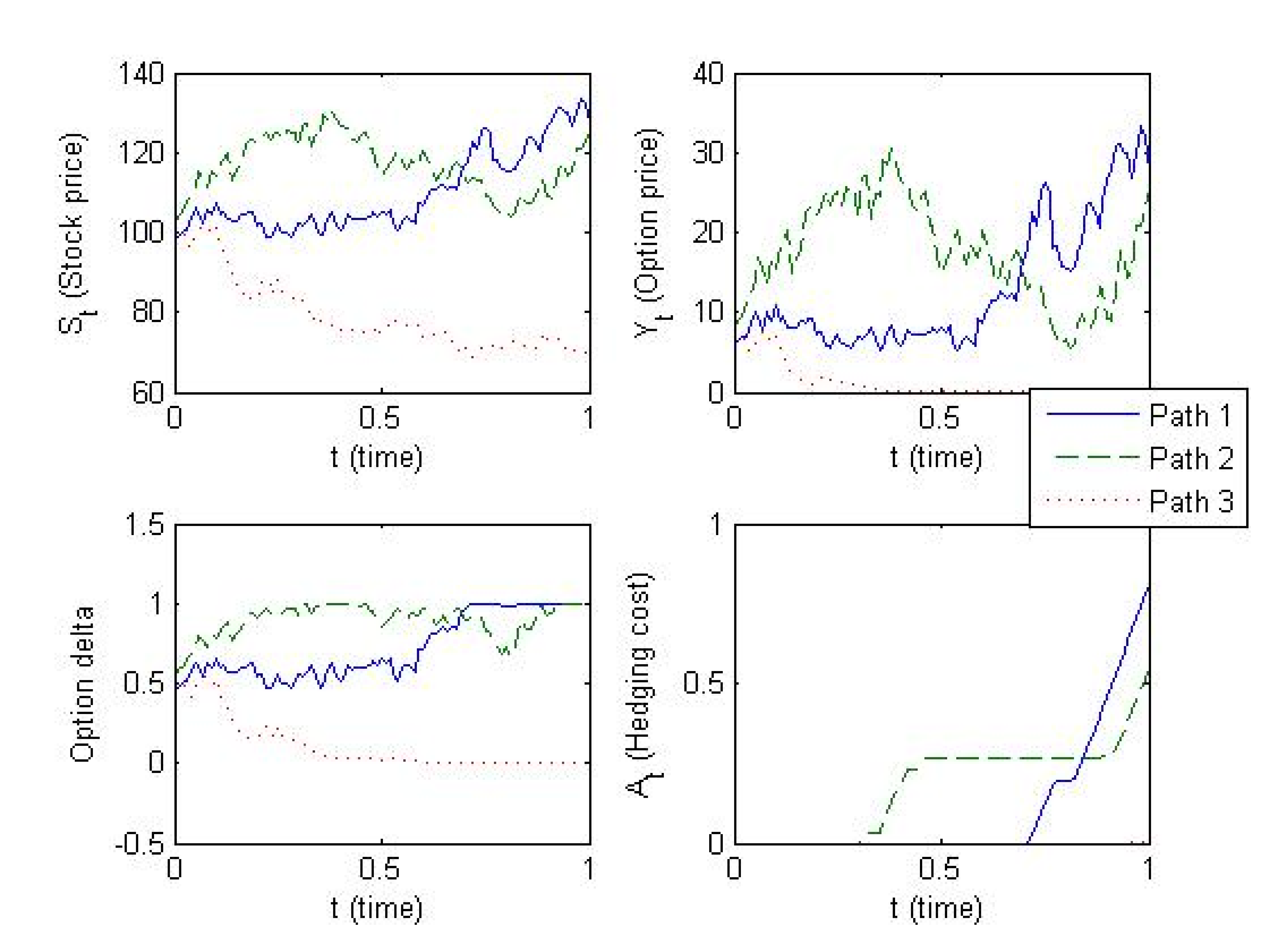

If we introduce a dividend rate of under imperfect market conditions ( and ), then the American and the European call option prices differ and the Black-Scholes formula does not apply. The convolution method estimates the (at-the-money) American call option price at and the European call option price at . We use scheme II with the restricted domain , grid points, time steps and a minimal slope of . Figure 3 shows the typical sample paths for the American option where the reflecting process (hedging cost) is now non-zero for in-the-money path indicating a difference in price with the European call option.

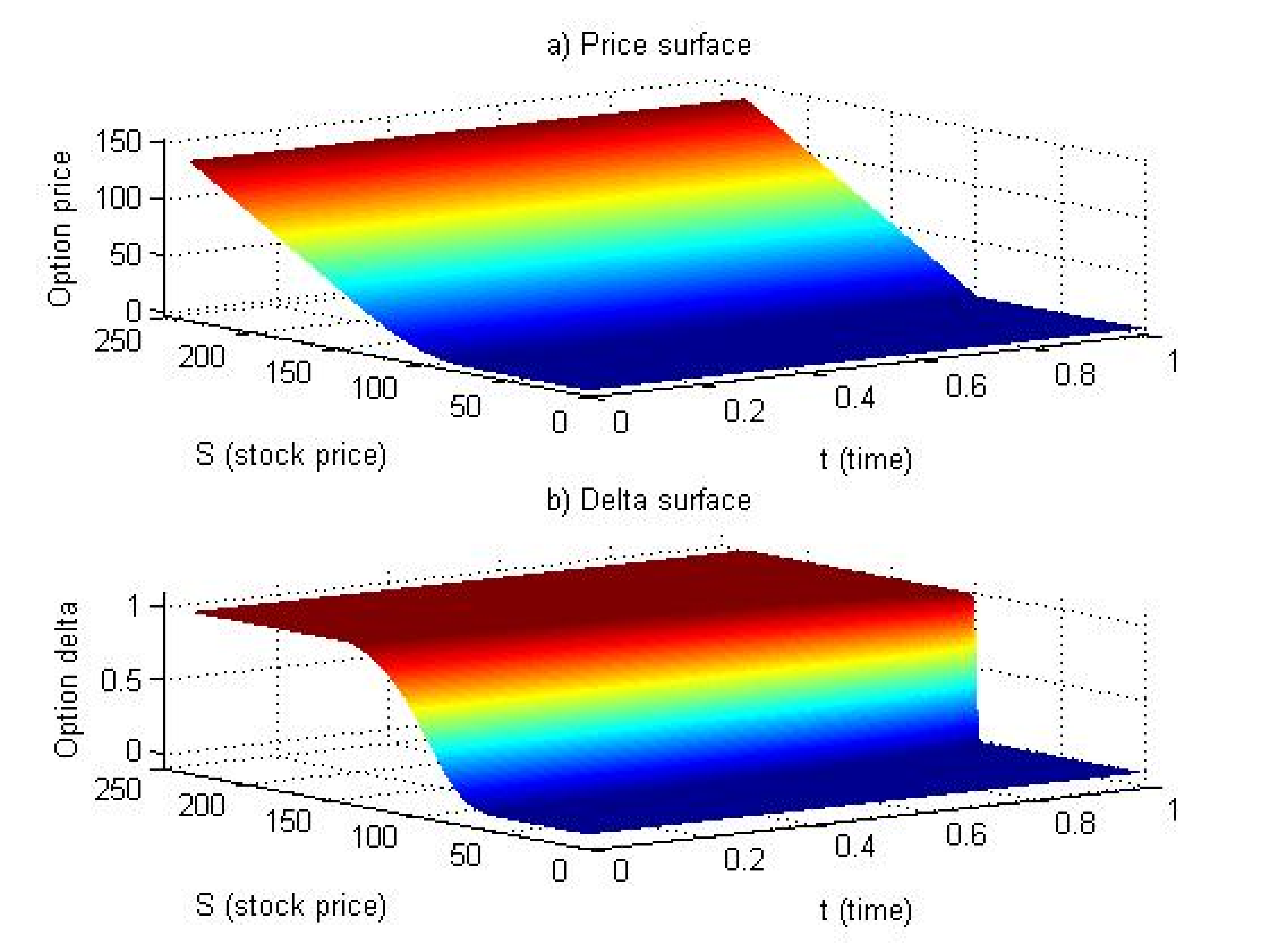

Figure 4 displays the option price and delta surfaces. The regularity of these surfaces indicates that the convolution method is efficient in handling non-smoothness in the terminal condition but also in the driver .

7 Conclusion

In this paper we presented a new spatial discretization method for the numerical solution of backward stochastic differential equations (BSDEs). This new method expresses conditional expectations appearing in explicit Euler time discretizations of the BSDE as convolutions. The convolution theorem of Fourier analysis is then applied in order to derive a recursive, backward in time, method for computing the numerical solution of the BSDE in terms of inverse Fourier transforms of previous time step solutions. After discretizing the state and Fourier space these expressions can be implemented using the fast Fourier transform (FFT) algorithm. Since the FFT algorithm is more suitable for periodic functions we introduced a transform in order to treat BSDEs with non-periodic terminal conditions. A (local) error analysis is provided which indicates that the use of the FFT performs an extrapolation that induces a non-negligible error term meaning that transform does not completely solve the problem of non-periodicity. We extend the convolution method to consider forward-backward stochastic differential equation (FBSDEs) and reflected FBSDEs which are an important extensions for financial applications.

Numerical experiments, in the context of option pricing problems, show that the convolution method is accurate and handles non-linearity and non-smoothness in the BSDE coefficients. The addition of a technique to suppress the extrapolation error is an interesting improvement to the method and shall be presented in a future paper (see [32]). Efficient implementations for multidimensional problems is an important area of future research.

References

- [1] Fabio Antonelli, Backward-forward stochastic differential equations, Ann. Appl. Probab., 3 (1993), pp. 777–793.

- [2] V. Bally and G. Pages, A quantization algorithm for solving multidimensional discrete-time optimal stopping problems, Bernoulli, 9 (2003), pp. 1003–1049.

- [3] C. Bender and R. Denk, A forward scheme for backward SDEs, Stochastic Process. Appl., 117 (2007), pp. 1793–1812.

- [4] C. Bender and J. Steiner, Least-squares Monte Carlo for backward SDEs, in Numerical methods in finance, vol. 12 of Springer Proc. Math., Springer, Heidelberg, 2012, pp. 257–289.

- [5] Y. Bergman, Option pricing with differential interest rates, Rev. Financ. Stud., 8 (1995), pp. 475–500.

- [6] J.-M. Bismut, Théorie probabiliste du contrôle des diffusions, Mem. Amer. Math. Soc., 4 (1973).

- [7] B. Bouchard and J.-F. Chassagneux, Discrete time approximation for continuously and discretely reflected BSDEs, Stochastic Process. Appl., 118 (2008), pp. 2269–2293.

- [8] B. Bouchard, R. Elie, and N. Touzi, Discrete-time approximation of BSDEs and probabilistic schemes for fully nonlinear PDEs, in Advanced financial modelling, vol. 8 of Radon Ser. Comput. Appl. Math., Walter de Gruyter, Berlin, 2009, pp. 91–124.

- [9] B. Bouchard and N. Touzi, Discrete-time approximation and Monte-Carlo simulation of backward stochastic differential equations, Stochastic Process. Appl., 111 (2004), pp. 175–206.

- [10] P. Briand, B. Delyon, and J. Memin, Donsker-type theorem for BSDEs, Electron. Comm. Probab., 6 (2001), pp. 1–14.

- [11] P. Carr and D.B. Madan, Option valuation using the Fast Fourier Transform, J. Comput. Finance, 2 (1999), pp. 61–73.

- [12] D. Chevance, Numerical methods for backward stochastic differential equations, in Numerical Methods in finance, L.C.G. Rogers and D. Talay, eds., Publ. Newton Inst., Cambridge Univ. Press, Cambridge, 1997, pp. 232–244.

- [13] D. Crisan and K. Manolarakis, Solving backward stochastic differential equations using the cubature method: Application to nonlinear pricing, SIAM Journal on Financial Mathematics, 3 (1) (2012), pp. 534–571.

- [14] J. Cvitanić and I. Karatzas, Hedging contingent claims with constrained portfolios, Ann. Appl. Probab., 3 (1993), pp. 652–681.

- [15] F. Delarue and S. Menozzi, A forward-backward stochastic algorithm for quasi-linear PDEs, Ann. Appl. Probab., 16 (2006), pp. 140–184.

- [16] J. Douglas Jr., J. Ma, and P. Protter, Numerical methods for forward-backward stochastic differential equations, Ann. Appl. Probab., 6 (1996), pp. 940–968.

- [17] N. El Karoui, C. Kapoudjian, É. Pardoux, S. Peng, and M.-C. Quenez, Reflected solutions of backward SDE and related obstacle problems for PDEs, Ann. Probab., 25 (1997), pp. 702–737.

- [18] N. El Karoui, É. Pardoux, and M.-C. Quenez, Reflected backward SDEs and American options, in Numerical Methods in finance, L. C. G. Rogers and D. Talay, eds., Cambridge University Press, 1997, pp. 215–231.

- [19] N. El Karoui, S. Peng, and M.-C. Quenez, Backward stochastic differential equations in finance, Math. Finance, 7 (1997), pp. 1–71.

- [20] N. El Karoui and M.-C. Quenez, Imperfect markets and backward stochastic differential equations, in Numerical Methods in finance, L. C. G. Rogers and D. Talay, eds., Cambridge University Press, 1997, pp. 181–214.

- [21] E. Gobet, Numerics of backward SDEs. Lecture Notes for the Summer School in Probability Theory, at Disentis (Switzerland). Numerical approximations of Backward Stochastic Differential Equations, July 2010.

- [22] E. Gobet, J.-P. Lemor, and X. Warin, A regression-based Monte Carlo method to solve backward stochastic differential equations, Ann. Appl. Probab., 15 (2005), pp. 2172–2202.

- [23] C.B. Hyndman, A forward-backward sde approach to affine models, Math. Financ. Econ., 2 (2009), pp. 107–128.

- [24] M. Kobylanski, Backward stochastic differential equations and partial differential equations with quadratic growth, Ann. Probab,, 28 (2000), pp. 558–602.

- [25] R. Korn, Contingent claim valuation in a market with different interest rates, ZOR—Math. Methods Oper. Res., 42 (1995), pp. 255–274.

- [26] J.-P. Lemor, E. Gobet, and X. Warin, Rate of convergence of an empirical regression method for solving generalized backward stochastic differential equations, Bernoulli, 12 (2006), pp. 889–916.

- [27] J. P. Lepeltier and J. San Martin, Backward stochastic differential equations with continuous coefficient, Statist. Probab. Lett., 32 (1997), pp. 425–430.

- [28] R. Lord, F. Fang, F. Bervoets, and C. Osterlee, A fast and accurate FFT-based method for pricing early-exercise options under Lévy processes, SIAM J. Sci. Comput., 30 (2008), pp. 1678–1705.

- [29] J. Ma, P. Protter, J. San Martin, and S. Torres, Numerical method for backward stochastic differential equations, Ann. Appl. Probab., 12 (2002), pp. 302–316.

- [30] X. Mao, Adapted solutions of backward stochastic differential equations with non-Lipschitz coefficients, Stochastic Process. Appl., 58 (1995), pp. 281–292.

- [31] G.N. Milstein and M.V. Tretyakov, Discretization of forward-backward stochastic differential equations and related quasi-linear parabolic equations, IMA J. Numer. Anal., 27 (2007), pp. 24–44.

- [32] P. Oyono Ngou, Fourier methods for numerical solution of FBSDEs with applications in mathematical finance, PhD thesis, Concordia University, Montréal, Canada, January 2014.

- [33] É. Pardoux and S.G. Peng, Adapted solution of a backward stochastic differential equation, Systems and Control Lett., 14 (1990), pp. 55–61.

- [34] É. Pardoux and S. Peng, Backward stochastic differential equations and quasilinear parabolic partial differential equations, in Stochastic partial differential equations and their applications (Charlotte, NC, 1991), vol. 176 of Lec. Notes Control and Inform. Sci., Springer, Berlin, 1992, pp. 200–217.

- [35] S. Peng and M. Xu, Numerical algorithms for backward stochastic differential equations with 1-D Brownian motion: convergence and simulations, ESAIM Math. Model. Numer. Anal., 45 (2011), pp. 335–360.

- [36] R. Plato, Concise numerical mathematics, vol. 57 of Graduate Studies in Mathematics, American Mathematical Society, Providence, RI, 2003.

- [37] A. Richter, Explicit solutions to quadratic BSDEs and applications to utility maximization in multivariate affine stochastic volatility models, Stochastic Process. Appl., 124 (2014), pp. 3578–3611.

- [38] M.J. Ruijter and C. W. Oosterlee, A Fourier-cosine method for an efficient computation of solutions to BSDEs, http://ssrn.com/abstract=2233823, (2013).

- [39] A. Vretblad, Fourier analysis and its applications, vol. 223 of Graduate Texts in Mathematics, Springer-Verlag, New York, 2003.

- [40] J. Yong, Linear forward-backward stochastic differential equations, Appl. Math. Optim., 39 (1999), pp. 93–119.

- [41] J. Zhang, Some fine properties of backward stochastic differential equations, PhD thesis, Purdue University, 2001.

- [42] J. Zhang, A numerical scheme for BSDEs, Ann. Appl. Probab., 14 (2004), pp. 459–488.

- [43] W. Zhao, L. Chen, and S. Peng, A new kind of accurate numerical method for backward stochastic differential equations, SIAM J. Sci. Comput., 28 (2006), pp. 1563–1581.