Premiums And Reserves, Adjusted By Distortions

Abstract

The net-premium principle is considered to be the most genuine and fair premium principle in actuarial applications. However, an insurance company, applying the net-premium principle, goes bankrupt with probability one in the long run, even if the company covers its entire costs by collecting the respective fees from its customers. It is therefore an intrinsic necessity for the insurance industry to apply premium principles, which guarantee at least further existence of the company itself; otherwise, the company naturally could not insure its clients to cover their potential, future claims. Beside this intriguing fact the underlying loss distribution typically is not known precisely. Hence alternative premium principles have been developed. A simple principle, ensuring risk-adjusted credibility premiums, is the distorted premium principle. This principle is convenient in insurance companies, as the actuary does not have to change his or her tools to compute the premiums or reserves.

This paper addresses the distorted premium principle from various angles. First, dual characterizations are developed. Next, distorted premiums are typically computed by under-weighting or ignoring low, but over-weighting high losses. It is demonstrated here that there is an alternative, opposite point of view, which consists in leaving the probability measure unchanged, but increasing the outcomes instead. It turns out that this new point of view is natural in actuarial practice, as it can be used for premium calculations, as well as to determine the reserves of subsequent years in a time consistent way.

Keywords: Premium Principles, Dual Representation, Fenchel–Young

inequality, Stochastic dominance

Classification: 90C15, 60B05, 62P05

1 Introduction

Risk adjusted insurance prices by employing distorted probability measures have been considered in this journal by Wang [WY98] and for example in [HBV12]. The idea is based on the fact that outstanding, potential losses should be over-valued, whereas small claims may be under-weighted in exchange. This procedure provides a risk-adjusted premium, which always exceeds the net premium (cf. also the recent papers [FZ08]).

In this paper we provide a different perspective in a way, which leaves the probabilities unchanged (the measure is not changed), but the claims are adjusted in an appropriate way. Considering just the premium, then both approaches provide the same result. However, the new perspective allows computing the reserves as well in a concise and time-consistent way, and this is the essential novel contribution.

Axiomatic characterizations of insurance premiums have been outlined in [WYP97], [Wan00] and in [You06]. These axiomatic treatments, initiated in an actuarial context first (early attempts appeared already in [Den90]), have been developed further in financial mathematics, for example in the celebrated seminal paper [ADEH99]. The connection between actuarial and financial mathematics is striking here, as premium principles in an actuarial context correspond to risk measures in financial mathematics, so that risk measures constitute a premium principle and vice versa. What perhaps surprises is that the name—risk measure—is a term that should be expected in actuarial science rather than in financial mathematics.

The distorted probability relates directly to a special class of risk measures, the spectral measures introduced in [AS02] and [Ace02]. An important study of spectral risk measures, although under the different name distortion functional, was provided in [Pfl06]. The concepts of (i) premium principles by distorting probability measures, (ii) distortion functionals, and (iii) spectral risk measures are essentially the same—they differ just in sign conventions, resulting in a concave or a convex description.

Distorted premium principles constitute an elementary and important class of premium principles, as every premium functional can be described by premium functionals involving distortions. They are moreover defined in an explicit way, hence there is an explicit evaluation scheme available, which is of course important for an applied actuary.

The most important distorted premium functional, which made its way to the top, is the conditional tail expectation, (in a financial context the alternative term Conditional Value-at-Risk is more accepted). The conditional tail expectation is usually associated and employed for loss distributions of entire portfolios (for example by the US and Canadian insurance supervisory authorities, [KRS09], cf. also [CT11]). Here we shall exploit that the constitutes an elementary pricing principle as well (cf. [HBV12]). It is the essential advantage of the conditional tail expectation that different representations are known, which makes this premium principle eligible in varying situations: by conjugate duality there is an expression in the form of a supremum, but in applications and for quick computations a different formulation as an infimum is extremely convenient: developed in the paper Optimization of Conditional Value-at-Risk [RU00] (cf. also [RU02]), the general formula is given in Some Remarks on the Value-at-Risk and the Conditional Value-at-Risk in [Pfl00]. The main results of this article extend both formulations to distorted premium functionals. Further, both representations can be associated with different views on distortions, providing different interpretations in an actuarial context.

A description of the distorted premium principle as a supremum is a first result of this article. The description builds on dual representations and on second order stochastic dominance. Stochastic dominance relations have been considered in the literature, but typically for the risk measure itself (the primal functions) with the negative result that coherent risk measures—in general—are not consistent with second order stochastic dominance, cf. [Gio05, Kro07]. A concise formulation, however, is available by imposing stochastic dominance constraints on the convex conjugate function (the dual function) instead of considering stochastic orders on the primal (cf. also [Sha12]), and this is elaborated here.

Besides that—and this is of particular importance for applications and a further result in this paper—a formula for the distorted premium is elaborated by involving an infimum. The infimum description builds on the Fenchel–Young inequality. This alternative representation of distorted premium functionals is the converse of the initial description, as it does not change the measure, but the outcomes instead.

The article is organized as follows. The premium principle is introduced in the following Section 2. Its description as a supremum by means of stochastic order relations is contained in Section 3. The infimum representation is elaborated in Section 4. Further implications for actuarial sciences are outlined and explained in Section 5, this section contains illustrating examples as well.

2 The Distorted Distribution

In this paper—as usual in an actuarial context—we shall associate a valued random variable with loss and therefore write to denote a random variable. is the cumulative distribution function (cdf), and

| (1) |

is the generalized inverse or quantile. The random variable can be given by employing the probability integral transform (or inverse sampling) as

| (2) |

where is a uniformly distributed random variable111 is uniformly distributed if for all . on the same probability space as and coupled in a co-monotone way with (for example , if is invertible, cf. [vdV98]).

We shall call a nonnegative, nondecreasing function

satisfying distortion, and define the antiderivative By the conditions imposed on the function is convex, nonnegative and satisfies . Moreover it has a generalized inverse, , defined in accordance with (1).

The distorted loss (distorted by the distortion ) then is

| (3) |

where is chosen as in (2). and notably have the same outcomes, but their probabilities differ. It holds that by monotonicity of (), such that

(it is said that stochastically dominates in first order). Applying the simple net premium principle to and reveals that

by monotonicity of the expectation, ensuring thus that is a plausible price for the insurance contract, the price at least exceeds the net-premium.

The premium is moreover easily accessible to the actuary, because

| (4) |

the actuary just has to replace the cdf by in his/ her computations for the premium or reserves, or consider the density

(if available; cf. [VX11]). So the premium is an expectation again—as the net premium principle—just with probabilities modified (distorted) according (4).

These considerations give rise for the following definition.

Definition 1.

Let () be a distortion and be a random variable for the conjugate exponent (), then

| (5) |

is called -distorted premium, or simple distorted premium for the loss . is called distorted premium functional.

Remark 2.

The premium is well defined and finite valued, it satisfies by Hölder’s inequality.

The distorted premium functional satisfies the following axioms, which have been proposed and formulated in a different context—for risk measures in mathematical finance—in [ADH97]. The axioms here have been adapted to account for insurance instead of financial risk (cf. also [WD98], and for reinsurance cf. [BBH09]).

Definition 3.

A function is called premium functional (or premium principle) if the following axioms are satisfied:

-

(M)

Monotonicity: whenever almost surely;

-

(C)

Convexity: for ;

-

(T)

Translation equivariance:222In an economic or monetary environment this is often called Cash invariance instead. if ;

-

(H)

Positive homogeneity: whenever .

Remark 4.

In a banking or investment environment the interpretation of a reward is more natural, in this context the mapping is often considered—and called coherent risk measure—instead (note, that essentially the monotonicity condition (M) and translation property (T) reverse for ).

The term acceptability functional was introduced in energy or decision theory to quantify and classify acceptable strategies. In this context the concave mapping , the acceptability functional, is employed instead (here, (C) modifies to concavity).

The conditional tail expectation is the most important premium principle.

Definition 5 (Conditional tail expectation).

The premium principle with distortion

| (6) |

is the conditional tail expectation at level (),

The conditional tail expectation at level is

Due to the defining equation (5) of the distorted premium the same real number is assigned to all random variables sharing the same law, irrespective of the underlying probability space. This gives rise to the notion of version independence:

Definition 6.

A premium principle is version independent333sometimes also law invariant or distribution based., if whenever and share the same law, that is if for all .

The following representation underlines the central role of the conditional tail expectation for version independent premium principles. Moreover, it is the basis and justification for investigating distorted premium principles in much more detail.

Theorem 7 (Kusuoka’s representation).

In the present context of distorted premiums it is essential to observe that any distorted premium has an immediate representation as in (7), the measure corresponding to the density is

| (8) |

with cumulative distribution function (which we may denote again by , because it is a measure on )

is a positive measure since is nondecreasing, and integration by parts reveals that it is a probability measure. Kusuoka’s representation is immediate by Riemann–Stieltjes integration by parts for the set , as

Conversely, the premium functional in Kusuoka’s representation (7) often can be expressed as a distorted premium functional with distortion , this is accomplished by the function

| (9) |

Provided that is well defined (notice that possibly has to be excluded when computing ) it is positive and a density, as .

Kusuoka representation by means of distorted premium principles.

By the preceding discussion there is a one-to-one relationship given by (8) (with inverse given by (9)) such that Kusuoka’s representation (Theorem 7) can be formulated with distorted premium functionals equally well,

| (10) |

is a set of distortions. can be restricted to consist of continuous and strictly increasing (thus invertible) density functions. A rigorous discussion is rather straight forward, although beyond the scope of this article. Here, it is just important to observe that any premium principle is built of distorted premium functionals by (10).

3 Supremum-Representation of Distorted Premium Functionals

The supremum representation of distorted premium functionals is derived from the convex conjugate relation for convex functionals. To formulate the result in a concise way we employ the notion of (second order) stochastic dominance.

Definition 8 (Convex ordering).

Let be integrable functions.

-

(i)

majorizes (denoted or ) iff

-

(ii)

The spectrum majorizes the random variable () iff

Remark 9.

Recall that for the conditional tail expectation it holds that

where is the function . It should thus be noted that

Moreover is related to a convex order or stochastic dominance conditions, which are studied for example in [MS02] or [SS07]. The dominance in convex (concave) order was used in studying risk measures for example in [FS04, Dan05].

The following Theorem 10 is a characterization of distorted premium functionals by employing the convex conjugate relationship for the dual.

Theorem 10 (Representation of distorted premium functionals as a supremum by stochastic order constraints.).

Let be a distorted premium functional. Then the representation

| (11) | ||||

holds true.

Remark 11.

The stochastic order constraint is employed here for the dual variable . Note also that the set is closed, as

Remark 12.

Remark 13.

We emphasize that the conditions and together imply that almost everywhere. Indeed, suppose that . Then . As it follows that . But this contradicts the fact that , hence is nonnegative, almost surely.

Proof of Theorem 10.

Recall the Legendre–Fenchel transformation for convex functions (cf. [SDR09]),

| (12) |

As is version independent the random variable minimizing (12) is coupled in a co-monotone way with (cf. [Hoe40] and [PR07, Proposition 1.8] for the respective rearrangement inequality, sometimes referred to as Hardy and Littlewood’s inequality or Hardy–Littlewood–Pólya inequality—cf. [Dan05]). It follows that

the infimum being among all cumulative distribution functions of . Define and , whence

| (13) |

by integration by parts of the Riemann–Stieltjes integral and as it is enough to consider .

Consider the constant random variables (), then and, by (13),

Note now that , whence

because

| (14) |

Assuming it follows from (13) that

Then choose an arbitrary measurable set and consider the random variable for some . Note that , where . With this choice

As was chosen arbitrarily it follows that has to hold for any for to be feasible.

Conversely, if (14) and for all , then

because is a nondecreasing function. Note now that

from which finally follows that

which is the assertion. ∎

The following statement derives naturally as a corollary of Theorem 10, it will be essential in the sequel.

Corollary 14.

Let be a distortion risk functional, then

| (15) |

where the infimum is attained if and are coupled in a co-monotone way.

Remark 15.

The statement of the corollary implicitly and tacitly assumes that the probability space is rich enough to carry a uniform random variable. This is certainly the case if the probability space does not contain atoms. But even if the probability space has atoms, then this is not a restriction neither, as any probability space with atoms can be augmented to allow a uniformly distributed random variable.

Proof.

Consider for a uniformly distributed random variable , then , that is . But as it follows that

almost everywhere. Observe now that any with is feasible for (11), because

and . Now let be coupled in an co-monotone way with , then such that

which is finally the second assertion. ∎

The characterization derived in the previous theorem for spectral premium functionals naturally applies to the conditional tail expectation itself. The expression can be simplified further to give the dual representation, which is often used to define the conditional tail expectation. The second statement exhibits an interesting, “recursive” structure.

Corollary 16.

The conditional tail expectation at level obeys the dual representations

Proof.

The conditional tail expectation at level is provided by the Dirac measure , and the respective distortion function is (cf. (6)). It follows from and Theorem 10 that

Observe next that for

hence

For , in addition, .

This proves the second assertion.

As for the first observe that , hence ; conversely, if and , then

which is the first assertion. ∎

4 Infimum Representation Of Distortion Premium Functionals

The latter Theorem 10 exposes the distorted risk premium as a supremum and characterizes the convex conjugate function by stochastic dominance constraints. The following theorem, the second main result of this article, provides a description in opposite terms, as an infimum. The representation extends the well known formula for the conditional tail expectation (Average Value-at-Risk) provided in [RU00], finally stated in the present form in [Pfl00].

This alternative description allows an alternative view on distortions and alternative simulations, as is the content of the following section.

Theorem 17 (Representation as an Infimum).

For any the distorted premium functional with distortion has the representation

| (16) |

where the infimum is among all arbitrary, measurable functions and is ’s convex conjugate function 444The convex conjugate function of is . The convex conjugate may evaluate to ..

Remark 18.

The statement of the Inf-Representation Theorem 17 can be formulated equivalently in the following ways.

Corollary 19.

For any the distorted risk premium with distortion allows the representations

| (17) | |||||

where the latter infimum is among arbitrary, measurable functions .

Proof of Corollary 19.

Remark 20.

Notice that has its range in the interval , and from convexity of it follows that the set is convex. Hence necessarily has to hold for all to ensure that . For convex this means in turn that

limiting thus the class of interesting functions in Corollary 19 to convex functions satisfying .

Proof of Theorem 17.

From the definition of the convex conjugate it is immediate that

for all numbers and (this is often called Fenchel–Young inequality), hence

where is any uniformly distributed random variable, i.e. satisfies . Taking expectations it follows that

As is uniformly distributed it holds that

such that

irrespective of the uniform random variable . Hence, by in Corollary 10,

establishing the inequality

As for the converse inequality consider the function

| (19) |

is well defined for all because ; is moreover increasing and convex, because is increasing and convex, and because is positive.

Recall the formula

and the fact that the infimum is attained at (cf. [Pfl00] or [GLWT12, Section 4.1] for the general formula), providing thus the explicit form

Note now that, by Fubini’s Theorem,

| (20) |

To establish the assertion (16) it needs to be shown that . For this observe first that is almost everywhere differentiable (because it is convex), with derivative

| (21) | |||||

(almost everywhere) by relation (9). Moreover , the supremum being attained at every satisfying , hence at , and it follows that

Now

But it was established already in (20) that , so that

This finally proves the second inequality. ∎

as a special case.

The conditional tail expectation is a special case of the infimum in (16). Indeed, it follows from (19) in the proof that the infimum is attained at a function of the form with conjugate

It holds that

such that

| (22) |

the classical result. Clearly, the infimum in (22) is in , a much smaller space than convex functions from to , as required in (16).

5 Implications for Actuarial Science and Claim Sampling

5.1 Comparison of and

In the introductory discussion it was outlined that claims can be sampled (based on (2)) by use of

It is obvious by this formula that the distorted claims have the same outcomes as , but their probability is disturbed by involvement of the function .

The infimum representation developed in Section 4 suggests to consider the random variable

where is the function defined in (19), and which is the optimal function for problem (17). For this function it holds that

because . We have moreover that

from which follows that

that is, stochastically dominates in first order. The cumulative distribution function of has the explicit form

and the density is by use of (21). The quantile function

| (23) |

is obtained by inversion.

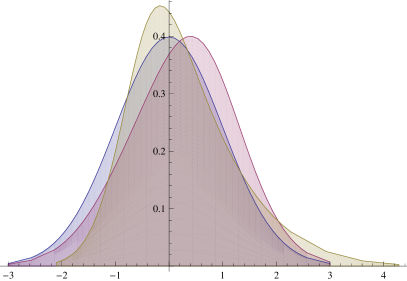

Example 21.

Figure 1 contains the densities of both distortions, and , for the standard normal distribution. The distortion function chosen in this example is . This example reveals that the mode, as well as the tails of the random variables and differ significantly; the tails of are heavier.

Opposite perspectives.

The latter formula (23) reveals that has distorted outcomes, distorted by , but the probabilities are unchanged. So can be considered as alternative to (4), doing exactly the opposite of the formula (4) stated initially: has the same probabilities as , but the outcomes are distorted by whereas has the same outcomes as , but the probabilities are distorted by . However, both, and , have the same expected value

Explicit distances.

As the cumulative distribution function is available for and as elaborated, explicit expressions are available for selected distances of random variables. An explicit representation of the Kolmogorov–Smirnov distance for example is

and the Wasserstein distance (cf. [Vil03]) has the explicit formula

5.2 Actuarial Applications

Actuarial concerns have been addressed on various locations of the paper, however, we stress again that , and in particular constitute premium principles. For a given loss distribution with monotone (increasing, or decreasing) loss function (note, that this is almost always the case in life insurance), the function can be given in a closed form.

Example 22.

Considering the simple life expectancy,555Note that the life expectancy is an annuity with an interest rate of . We have chosen an annuity as a representative example for a typical life insurance contract. Considering the life expectancy allows moreover excluding the interest rate in order to simplify the presented results. i.e. the random variable (which is strictly increasing), then and

is the distorted life expectancy.

Distorted probabilities.

Following (3) one may consider as probability of a new life table (indicated by the tilde), and use this new life table to compute premiums, as well as reserves. This is exemplary depicted in Figure 2. It is visible in this chart that the modified life table increases the life expectancy by approximately years initially, but the increasing effect disappears at the age representing the quantile (here, at the age of 60 years for , considering a person with an initial age of 50). For this reason it is appropriate to use as a premium, but it is not desirable to use the new life table to compute reserves. The reserves loose the safety loading by employing the new life table, whenever the age exceeds the quantile.

Distorted outcomes.

As already outlined it is natural to use the distorted outcomes instead of distorted probabilities in actuarial practice. As to compute the premiums the above discussion applies equally well, and an explicit form is available to compute the premium. For the exposed case of life expectancy the result is

It is the big advantage of distorted outcomes, that the reserves can be handled with the same ingredients as the premium, that is with the same probabilities and the same function : simply needs to be replaced by . It is evident in Figure 2 that the safety loading is preserved over time.

Distorted premiums, interpreted as distorted outcomes, are thus a reliable premium principle which provide not only premiums, but also reserves in a correct and time-consistent way. The distorted premium principle to compute the reserves can be applied by the actuary easily, and along with the related outcomes distorted by .

6 Concluding Remarks

This article outlines new descriptions of distorted premium principles. Distorted premium principles constitute a basic class of premium principles, as every premium satisfying sufficiently strong axioms can be built by involving just elementary distortions.

The first representation derived is described as a supremum, based on conjugate duality. The convex conjugate function is formulated in terms of second order stochastic dominance constrains.

The other representation, which is a further central result of this article, is described as an infimum and can be considered as the opposite formulation. This alternative description makes distorted premiums eligible for successful use in actuarial applications, as the reserve process is easily available for concrete insurance contracts and, above all, the process of reserves is consistent over time. The results thus make distorted premiums eligible for extended actuarial use.

7 Acknowledgment

The charts have been programmed by use of Mathematica and Excel.

References

- [Ace02] Carlo Acerbi. Spectral measures of risk: A coherent representation of subjective risk aversion. Journal of Banking & Finance, 26:1505–1518, 2002.

- [ADEH99] Philippe Artzner, Freddy Delbaen, Jean-Marc Eber, and David Heath. Coherent Measures of Risk. Mathematical Finance, 9:203–228, 1999.

- [ADH97] Philippe Artzner, Freddy Delbaen, and David Heath. Thinking coherently. Risk, 10:68–71, November 1997.

- [AS02] Carlo Acerbi and Prospero Simonetti. Portfolio optimization with spectral measures of risk. EconPapers, 2002.

- [BBH09] Alejandro Balbás, Beatriz Balbás, and Antonio Heras. Optimal reinsurance with general risk measures. Insurance: Mathematics and Economics, 44:374–384, 2009.

- [CT11] Yichun Chi and Ken Seng Tan. Optimal reinsurance under VaR and CVaR risk measures. ASTIN Bulletin, 41(2):487–509, 2011.

- [Dan05] Rose-Anne Dana. A representation result for concave Schur concave functions. Mathematical Finance, 15:613–634, 2005.

- [Den90] Dieter Denneberg. Distorted probabilities and insurance premiums. Methods of Operations Research, 63:21–42, 1990.

- [FS04] Hans Föllmer and Alexander Schied. Stochastic Finance: An Introduction in Discrete Time. de Gruyter Studies in Mathematics 27. de Gruyter, 2004.

- [FZ08] Edward Furman and Ričardas Zitikis. Weighted premium calculation principles. Insurance: Mathematics and Economics, 42:459–465, 2008.

- [Gio05] Enrico De Giorgi. Reward-risk portfolio selection and stochastic dominance. Journal of Banking & Finance, 29:895–926, 2005.

- [GLWT12] Marc Goovaerts, Daniël Linders, Koen Van Weert, and Fatih Tank. On the interplay between distortion, mean value and the Haezendonck-Goovaerts risk measures. Insurance: Mathematics and Economics, 51:10–18, 2012.

- [HBV12] Antonio Heras, Beatriz Balbás, and José Luis Vilar. Conditional tail expectation and premium calculation. ASTIN Bulletin, 42:325–342, 2012.

- [Hoe40] Wassilij Hoeffding. Maßstabinvariante Korrelationstheorie. Schriften Math. Inst. Univ. Berlin, 5:181–233, 1940. In German.

- [JST06] Elyès Jouini, Walter Schachermayer, and Nizar Touzi. Law invariant risk measures have the Fatou property. Advances in Mathematical Economics, 9:49–71, 2006.

- [Kro07] Pavlo A. Krokhmal. Higher moment coherent risk measures. Quantitative Finance, 7(4):373–387, 2007.

- [KRS09] Bangwon Ko, Ralph P. Russo, and Nariankadu D. Shyamalkumar. A note on the nonparametric estimation of the CTE. ASTIN Bulletin, 39(2):717–734, 2009.

- [Kus01] Shigeo Kusuoka. On law invariant coherent risk measures. Advances in Mathematical Economics, 3:83–95, 2001.

- [MS02] Alfred Müller and Dietrich Stoyan. Comparison methods for stochastic models and risks. Wiley series in probability and statistics. Wiley, Chichester, 2002.

- [Pfl00] Georg Ch. Pflug. Some remarks on the value-at-risk and the conditional value-at-risk. In S. Uryasev, editor, Probabilistic Constrained Optimization: Methodology and Applications, pages 272–281. Kluwer Academic Publishers, Dordrecht, 2000.

- [Pfl06] Georg Ch. Pflug. On distortion functionals. Statistics and Risk Modeling (formerly: Statistics and Decisions), 24:45–60, 2006.

- [PR07] Georg Ch. Pflug and Werner Römisch. Modeling, Measuring and Managing Risk. World Scientific, River Edge, NJ, 2007.

- [RU00] R. Tyrrell Rockafellar and Stanislav Uryasev. Optimization of Conditional Value-at-Risk. Journal of Risk, 2:21–41, 2000.

- [RU02] R. Tyrrell Rockafellar and Stanislav Uryasev. Conditional value-at-risk for general loss distributions. Journal of Banking and Finance, 26:1443–1471, 2002.

- [SDR09] Alexander Shapiro, Darinka Dentcheva, and Andrzej Ruszczyński. Lectures on Stochastic Programming. MQS-SIAM Series on Optimization 9, 2009.

- [Sha12] Alexander Shapiro. On Kusuoka representations of law invariant risk measures. Mathematics of Operations Research, November 2012.

- [SS07] Moshe Shaked and J. George Shanthikumar. Stochastic Order. Springer Series in Statistics. Springer, 2007.

- [vdV98] Aad W. van der Vaart. Asymptotic Statistics. Cambridge University Press, 1998.

- [Vil03] Cédric Villani. Topics in Optimal Transportation, volume 58 of Graduate Studies in Mathematics. American Mathematical Society, Providence, RI, 2003.

- [VX11] Emiliano A. Valdez and Yugu Xiao. On the distortion of a copula and its margins. Scandinavian Actuarial Journal, 4:292–317, 2011.

- [Wan00] Shaun S. Wang. A class of distortion operatiors for financial and insurance risk. The Journal of Risk and Insurance, 67(1):15–36, 2000.

- [WD98] Shaun Wang and Jan Dhaene. Comonotonicity, correlation order and premium principles. Insurance: Mathematics and Economics, 22:235–242, 1998.

- [WY98] Shaun S. Wang and Virginia R. Young. Risk-adjusted credibility premiums using distorted probabilities. Scandinavian Actuarial Journal, 2:143–165, 1998.

- [WYP97] Shaun S. Wang, Virginia R. Young, and Harry H. Panjer. Axiomatic characterization of insurance prices. Insurance: Mathematics and Economics, 21:173–183, 1997.

- [You06] Virginia R. Young. Premium Principles. John Wiley & Sons, Ltd, 2006.

Appendix

For reference and the sake of completeness we list the following elementary result for affine linear transformations of the convex conjugate function.

Lemma 23.

The convex conjugate of the function for and is