Sharp regularity near an absorbing boundary for solutions to second order SPDEs in a half-line with constant coefficients

Abstract.

We prove that the weak version of the SPDE problem

with a specified bounded initial density, , and a standard Brownian motion, has a unique solution in the class of finite-measure valued processes. The solution has a smooth density process which has a probabilistic representation and shows degeneracy near the absorbing boundary. In the language of weighted Sobolev spaces, we describe the precise order of integrability of the density and its derivatives near the origin, and we relate this behaviour to a two-dimensional Brownian motion in a wedge whose angle is a function of the ratio . Our results are sharp: we demonstrate that better regularity is unattainable.

1. Introduction

Let be a standard Brownian motion on a complete filtered probability space and be a deterministic bounded probability density function on the half-line . In this paper, we consider the problem of finding a finite-measure valued process, , satisfying the weak stochastic partial differential equation

| (1.1) |

for all and . Here, we use the abbreviation and write for the space of bounded, twice-differentiable functions that vanish at the origin and have bounded first and second derivatives. The coefficients , , and and the time horizon are deterministic constants. We prove this problem has a unique solution, show how to construct this solution, and establish its regularity near the absorbing boundary.

This stochastic partial differential equation (SPDE) arises naturally as the mean-field limit of a collection of interacting particles. Specifically, suppose we have a homogeneous pool of particles each experiencing an independent noise driven by a Brownian motion with speed and drift , as well as a common noise . If we kill each of the particles upon hitting the origin, then describes the limiting spatial distribution of the particles at time as the number of particles becomes large. In [BHH+11], this model is proposed for the pricing of portfolio credit derivatives, and in that context the common noise, , corresponds to a market risk factor and the event that a particle hits the origin represents a default of one of the names in the portfolio. As the particles in this model are independent and identically distributed conditional on knowing the history of , we can study the system by considering the conditional mean behaviour of a single particle. In Section 2 we use this idea to present a simple construction of the solution to (1.1).

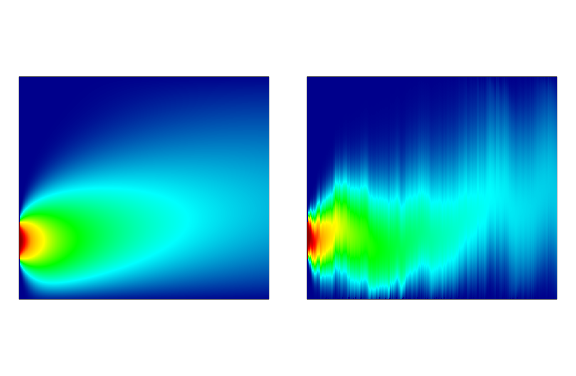

Visualising the dynamics of the solution to (1.1) is straightforward, and if then the SPDE becomes the deterministic heat equation with zero boundary condition. For non-zero the solution still has this decay, but also experiences random fluctuations in location which are driven by the Brownian motion — see Figure 1. If we denote the density of the solution by , then we can write (1.1) in differential form:

and, thinking of this equation as a PDE with irregular coefficients, we see that diffuses with speed and the transport term, , describes the (stochastic) net movement of the density in space. Lemma 3.1 of [Kry03] shows that the density of the solution is infinitely differentiable in , and this is due to the smoothing effect that heat flow produces. However, the presence of the irregular fluctuations in the density’s location causes mass close to the boundary to be destroyed in an abrupt fashion, and as a result the derivatives of the density blow-up at the origin. The purpose of this paper is to describe this degeneracy at the absorbing boundary.

Dirichlet boundary problems for SPDEs of this type have been studied extensively — for example [KK04, Kry94, KL98]. As we are working in one-dimension with constant coefficients, the simplicity of our setting allows greater insight into the behaviour of the solution near the absorbing boundary. We take advantage of a straightforward smoothing technique to present a more elementary study of the problem than is currently offered in the standard literature, and we are able to prove uniqueness of the solution to (1.1) in the broad class of finite-measure valued processes. Throughout this paper, when referring to uniqueness we shall always mean that if and are two finite-measure valued processes solving (1.1), then

The results closest to those in this paper are found in [Kry94]; there, Krylov demonstrates the existence of a unique solution to (1.1) in the class of twice-differentiable function-valued processes, , that satisfy

Furthermore, Krylov shows that if the initial density is -times differentiable with the function in for , then the solution is -times differentiable with

| (1.2) |

for . (For a function on , we will always denote the order derivative of by .)

A key ingredient in [Kry94], and the majority of the literature on this problem, is the introduction of weighted Sobolev spaces. These spaces enable us to quantify the rate at which the solution and its derivatives blow-up near the origin. In our one-dimensional setting, it suffices to use the functions

| (1.3) |

for . For a given order of derivative of the solution to (1.1), we can ask: how small can be taken in the above weighting function whilst preserving square-integrability of the product of that derivative and ? From (1.2), we can certainly take any for the derivative of the solution. A complete answer to this question is provided by the two proceeding theorems, and a critical quantity is

| (1.4) |

In the context of credit derivatives, is referred to as the correlation in the portfolio and describes the tendency of defaults to occur simultaneously. The closer is to one, the larger the value of , and therefore, observing that , the following result states that higher correlation produces less regularity near the absorbing boundary.

Theorem 1.1 (Uniqueness and regularity).

If is bounded, then there exists a unique solution, , to (1.1) in the class of finite-measure valued processes, and, for almost every , has a density on .

This result shows that, at a time later than zero, the solution has differentiability one order higher than the initial density, and is one multiple of more regular at the origin (recall that ). We should notice that, because the initial density is integrable and bounded, the condition is always satisfied. The hypotheses placed on the initial density allow its derivatives to blow-up at the origin and grow sub-exponentially towards infinity. We recover the results of [Kry94] by taking in Theorem 1.1, and therefore we have expanded upon the known regularity of the solution near the absorbing boundary.

Our results are sharp as the following result shows that we cannot take in Theorem 1.1:

Theorem 1.2 (Converse result).

If satisfies the hypotheses of Theorem 1.1, then for we have

Since the tails of the weighting functions all decay at the same rate, the only way we can obtain the blow-up observed in Theorem 1.2 is if the solution is degenerate near the absorbing boundary. With this in mind, it is clear that the first derivative of the solution cannot be bounded in a neighbourhood of the origin, otherwise we obtain the contradiction

for . In the deterministic setting () the first derivative does not have this feature, and this has been remarked upon by Krylov in [Kry03]. If we shift the density by setting

then, by the Itō–Wentzell formula, we have that solves the deterministic heat equation (with speed ) in the random region

with Dirichlet boundary condition. Theorem 5.1 of [Kry03] shows that there exists such that, with probability one, there is a dense subset of on which

On this set it is clear that the density can have no spatial derivative at the absorbing boundary.

In the next section we present the construction of the solution to (1.1) and describe its properties. A proof of Proposition 2.7 is presented in Section 3, and this is the main probabilistic result used to prove the above two theorems in Sections 4 and 5.

Acknowledgements

I would like to thank Ben Hambly for introducing me to this problem and related models, and Philippe Charmoy and James Leahy for helpful conversations.

2. The probabilistic solution

We shall construct the solution to (1.1) in this section. We have not yet proved that (1.1) can admit only one solution, therefore we refer to the measure-valued process presented here as the probabilistic solution.

Construction

Let us introduce two independent standard Brownian motions, and , that are also independent of . We define two test processes, and , by

where and are independent random variables with common law , and are also independent of every other random variable introduced so far. To kill the particles upon hitting zero, we set

Conditional on knowing the trajectory of , and are independent and identically distributed, therefore we make the following definition:

Definition 2.1 (Probabilistic solution).

Let be the natural filtration of . The probabilistic solution, , is defined to be the measure-valued process

for all and Lebesgue measurable.

Throughout this paper “ measurable” shall always mean that is Lebesgue measurable. The following is a useful representation:

Proposition 2.2.

For all and measurable we have

Proof.

Since and are equal in distribution, we have for and . Hence

as required, where the final line is due to the conditional independence of and . ∎

It is a simple calculation with Itō’s formula to show that is a solution of (1.1):

Proposition 2.3.

There exists a full subset of on which

for all and .

Proof.

Take , then Itō’s formula gives

| (2.1) | ||||

Since , we can write , and therefore, by taking the conditional expectation over (2.1) and noting that the integral then vanishes, we arrive at the required result. ∎

Remark 2.4 (The choice of test functions).

is chosen as it is the largest space for which the previous proof remains valid. The test functions’ derivatives need not be controlled at the origin, and we cannot take — the space of compactly supported smooth functions on the half-line — because in section 4 it will be necessary to set (see Definition 4.1) into (1.1) despite the fact that in general and are non-zero.

2.1. Properties

Conditional on knowing , the process is a Brownian motion started at with drift , and therefore we can write the conditional density of as

From Definition 2.1, it is a trivial fact that for any time and measurable subset , and this simple observation allows us to show that has a density process:

Proposition 2.6 (Existence of the density).

There exists a full subset of on which, for every , has a density process , and, for every , and .

Proof.

From the above, there exists a full subset of on which

for all and measurable. Therefore, if has zero Lebesgue measure, then . It follows by the Radon–Nikodym Theorem that has a density for every , and that this density satisfies

| (2.2) |

for almost all .

The most important feature of the probabilistic solution is the following estimate:

Proposition 2.7 (The -condition).

Let be bounded and be defined as in (1.4). Then for every there exists constants and such that

A proof is presented in Section 3.

In Lemma 3.5 of [BHH+11], this result is presented for an initial density supported on a finite interval away from the boundary, and that assumption allows the authors to drop the singular factor of . However, this is not the most natural initial condition; for any , takes positive values on all of , so if we stop the process at a time and then restart from the density , we still have the estimate on for despite not being supported on a finite interval away from zero. In this more general setting, we can expect a singular time factor to appear, since, for every time , as (Theorem 3.2 of [Kry03]) and so positive values of close to zero must decay instantaneously as the system evolves in time. Since , is integrable over and therefore does not present technical difficulties in later proofs of -integrability.

Using Proposition 2.2, we prove Proposition 2.7 by considering the process , which is a two-dimensional Brownian motion with components of correlation — recall (1.4). With also as in (1.4), the map defined by

| (2.3) |

transforms to a Brownian motion with uncorrelated components, and maps the quadrant to the wedge

We make use of explicit formulae in [Iye85] and [Met10] to estimate the probability that is in a small neighbourhood of the apex of the wedge and has not exited the wedge, which corresponds to the event and . The kernel smoothing technique of Section 4, which was introduced in [BHH+11] and adapted from [KX99], relates this hitting probability to the behaviour of the solution near the absorbing boundary.

3. Proof of Proposition 2.7

Let us write to indicate that and , that is, we start the two-dimensional Brownian motion, , from . From Proposition 2.2, we know

| (3.1) |

for every measurable . A change of measure allows us to eliminate the drift term in the dynamics of :

Lemma 3.1 (Eliminating drift).

Let be defined on by the Girsanov transformation

then under is a two-dimensional Brownian motion with zero drift. Let denote the expectation under . If there exists a constant such that

then Proposition 2.7 holds.

Proof.

Following the method in Lemma 3.5 of [BHH+11], for any Hölder conjugates we have

where one should note that . Hence

and, since , we can therefore choose sufficiently close to 1 so that the result holds. ∎

Remark 3.2.

We cannot take above, and so, except in the case when , this change of measure removes the possibility of considering the borderline case . Although this may seem to weaken the potential regularity available near the absorbing boundary, in proving Theorem 1.1 we make use of Lemma 4.8 which requires to be strictly smaller than the maximal value, , and hence it is unclear whether we could analyse the case regardless of this difficulty caused by eliminating the drift.

The remainder of Section 3 is devoted to showing that the hypothesis of Lemma 3.1 holds. Without loss of generality, from this point on we take and .

Conditioning on the start point of , we have

Under the transformation , the region is mapped into a region of the form

for some numerical constant . The estimate in Proposition 2.7 is unchanged under the map (modulo multiplicative constants), and so it is no loss of generality to assume . Using that is bounded, that the Jacobian of the transform is a numerical constant depending only on , and formula (8) of [Iye85] (corroborated in [Met10]), we arrive at

for some numerical constant. As , we have

| (3.2) |

and therefore we are done provided the double sum on the right-hand is finite. Using Stirling’s approximation, the inequality

for , and the asymptotic behaviour for large , we have that, for large and , the summand in (3.2) is dominated by a constant multiple of

Since , this expression is summable over and , and so we have the result. ∎

4. Proof of Theorem 1.1

We begin by proving the regularity result for the probabilistic solution. Let us write

| (4.1) |

Definition 4.1 (Heat kernels).

The absorbing and reflected heat kernels are defined to be

for and . The smoothed density and reflected smoothed density are then defined to be

for , , and .

Take any smooth compactly supported function, , then, for every , (that is the function obtained by convolving the heat kernel, , with ) is in , so putting and into (1.1) gives the following strong equation for the evolution of the smoothed density:

Proposition 4.2 (Strong smoothed evolution equation).

For , , and

| (4.2) | ||||

where is the remainder function:

Proof.

This is simply a matter of observing that

One also needs to apply the stochastic Fubini theorem [BL95] to switch integration in the space dimension with integration with respect to (and likewise with respect to time). To this end, it is enough to note that the tails of and and their derivatives decay exponentially, and so the conditions of the (stochastic) Fubini theorem are met. ∎

Differentiating equation (4.2) times (or integrating once for the case — the result is no different) and applying Itō’s formula to gives

| (4.3) | ||||

From this equation, we shall proceed to a proof by induction in Section 4.2. Before continuing, we introduce several technical lemmas in the next section.

Some technical lemmas

Lemma 4.3.

There exists a full subset of on which as for every , , and .

Proof.

This is straightforward since, for , we have

for a numerical constant . Note that we used the estimate . ∎

Lemma 4.4.

Let be an integer and suppose that for

Then, for almost every , the density is -times weakly differentiable with

| (4.4) |

Proof.

Let denote the usual inner product: . Let be a basis of for which each is smooth and bounded.

Firstly, for any and , , since is a linear combination of ’s and for . So for , integrating by parts gives

Applying Leibniz’s rule to , we see that

for some numerical constant , and that the right-hand side vanishes by Lemma 4.3, because for small . Hence we conclude

The remaining case, , is trivial.

By the above results and Fatou’s Lemma, we have

for , and therefore we can define the processes

which satisfy

Take , and set . Using we can compute

hence is the weak derivative of , and this completes the proof. ∎

Lemma 4.5.

There exists a full subset of on which

and

for every , , and .

Proof.

The result is an integration-by-parts exercise provided the following limits vanish:

for . If , then as , and the result is immediate. In the case , Lemma 4.3 gives , which is sufficient for the limit to be zero. This also implies , so the result holds for too. ∎

Lemma 4.6.

With defined as in (4.1), for every integer there exist constants for such that

Proof.

This is a simple inductive argument. ∎

Lemma 4.7.

For and

Proof.

The cases and are simple. Firstly, observe from Definition 4.1 that , so for all

and therefore we have the result for . The case follows by noting that and applying the same argument.

Now fix . Begin by noting that , where if is even and if is odd. Splitting the range of integration and integrating by parts in the definition of gives

| (4.5) |

We proceed by considering the weighted -norm of these three components.

Firstly by Lemma 4.6, there exists a numerical constant such that

therefore integrating over and applying the Cauchy–Schwarz inequality gives

| (4.6) |

as , where is a further numerical constant.

For the second term, we apply Cauchy–Schwarz to obtain

For we have , for some numerical constant , therefore

| (4.7) |

Finally, using the fact that is bounded and Lemma 4.6, there exists a numerical constant such that

and therefore

| (4.8) |

as , since . Here is a further numerical constant.

Lemma 4.8.

For and

Proof.

Interchanging differentiation and integration and applying Lemma 4.6 gives

with a numerical constant. Let and split the region of integration at , then for we have and on , and so we have

| (4.9) | ||||

The first term on the right-hand side of (4.9) vanishes as , hence we have

| (4.10) |

where we have used Proposition 2.7 with replaced by for small , and is a numerical constant. (Note as we integrate over , the singular factor of from Proposition 2.7 integrates to a finite value because .) The term in (4.10) is bounded by

for small , and, since we choose small enough so that

the limit on the right-hand side of (4.10) vanishes. ∎

The inductive proof for the regularity result

Initial case:

The initial case is when , and the result we shall demonstrate is:

| (4.11) |

By truncating the range of integration, we have

where . From Proposition 2.7, it is clear that

and therefore we are done provided . Using the inequality

we have a numerical constant such that

and so

Now let . Splitting the region of integration on and its complement, we see that on the complement the triple integral on the right-hand side above is bounded by a multiple of , and so vanishes as . Therefore we need only consider the region of integration , and so we have a numerical constant such that

where the second line follows by Proposition 2.7 and is sufficiently small. Clearly we may choose small enough so that the exponent of is positive, whereby the right-hand side vanishes and we have (4.11).

Inductive step:

Assume that for some we have

| (4.12) |

for . (We demonstrated the case above.) The proof will be complete if we can show condition (4.12) holds for , since then, by induction, the condition holds for all and we can apply Lemma 4.4 to give the regularity result of Theorem 1.1 for the probabilistic solution .

Let us begin by multiplying throughout equation (4.3) by the square of the weighting function and integrating over . To do so we apply Lemma 4.5 and arrive at

| (4.13) | |||

Eliminating the negative terms from the right-hand side and applying the Cauchy–Schwarz inequality gives

| (4.14) | |||

We are done provided the seven terms on the right-hand side of inequality (4.14) have a finite limit-infimum as . This is true of the second to fifth terms by the inductive hypothesis (4.12), and, with this, the final two terms vanish by Lemma 4.8. From Lemma 4.7, the first term remains finite in the limit-infimum, hence we have shown the probabilistic solution satisfies the regularity properties in Theorem 1.1.

Uniqueness

It remains to show that the probabilistic solution is indeed the unique finite-measure valued solution of (1.1). To do so, suppose we have another finite-measure valued solution , and define the signed-measure valued process, , as the difference between the solutions:

Let us write for the expected value of a random measure, , that is

for measurable, then, by taking expectation in (1.1), we have that and solve

| (4.15) |

Also, if we define the expected product measure to be the unique extension of

on , applying Itō’s formula to the product using (1.1) gives that and solve

| (4.16) |

for . Equations (4.15) and (4.16) are just the deterministic heat equations with zero boundary conditions, hence their solutions are unique so we conclude and — that is, the first and second moments of and are equal in distribution.

5. Proof of Theorem 1.2

This theorem relies on the fact that the estimate in Proposition 2.7 is sharp. Specifically, Lemma 5.1 of [Jin10] states that if is supported on a finite interval away from zero, then for every there exist and such that

| (5.1) |

It is clear that if , then the empirical measure, , obtained from starting the system from , satisfies . Since we can certainly find a constant such that is non-zero, we see that (5.1) remains valid if we drop the assumption on the support of .

To complete the proof, suppose, for a contradiction, that we have and a such that

Then

for any , and let us fix a and take small enough so that we have . Then for

and, since

| (5.2) | ||||

applying the triangle inequality, multiplying by , and integrating over gives

Repeating this argument eventually yields

for all allowable . If we return to (5.2) with and take the upper limit of the integral to be and the lower limit , then, since , we arrive at

Repeating this manipulation once more gives the following for :

with a constant. This is a contradiction of (5.1) for the case , and hence we have Theorem 1.2. ∎

References

- [BC09] A. Bain and D. Crisan. Fundamentals of Stochastic Filtering. Springer, New York, 2009.

- [BHH+11] N. Bush, B.M. Hambly, H. Haworth, L. Jin, and C. Reisinger. Stochastic Evolution Equations in Portfolio Credit Modelling. SIAM Journal of Financial Mathematics, 2(1):627–664, 2011.

- [BL95] K. Bichteler and S.J. Lin. On the stochastic Fubini theorem. Stochastics and Stochastic Reports, 54(3-4):271–279, 1995.

- [Iye85] Satish Iyengar. Hitting lines with two-dimensional brownian motion. SIAM Journal of Applied Mathematics, 45(6):983–989, 1985.

- [Jin10] L. Jin. Particle systems and SPDEs with applications to credit modelling. D.Phil Thesis, University of Oxford, 2010.

- [KK04] K-H. Kim and N. V. Krylov. On SPDEs with Variable Coefficients in One Space Dimension. Potential Analysis, 21(3):209–239, 2004.

- [KL98] N.V. Krylov and S.V. Lototsky. A Sobolev space theory of SPDEs with constant coefficients in a half line, volume 30. 1998.

- [Kry94] N.V. Krylov. A -theory of the Dirichlet problem for SPDEs in general smooth domains. Probability Theory and Related Fields, 98(3):389–421, 1994.

- [Kry03] N.V. Krylov. Brownian trajectory is a regular lateral boundary for the heat equation. SIAM J. Math. Anal., 34(5):1167–1182, 2003.

- [KX99] T.G. Kurtz and J. Xiong. Particle representations for a class of nonlinear SPDEs. Stochastic Processes and their Applications, 83(1):103–126, 1999.

- [Met10] A. Metzler. On the first passage problem for correlated Brownian motion. Statistics & Probability Letters, 80(5-6):277–284, 2010.