Optimal Placement of Distributed Energy Storage in Power Networks

Abstract

We formulate the optimal placement, sizing and control of storage devices in a power network to minimize generation costs with the intent of load shifting. We assume deterministic demand, a linearized DC approximated power flow model and a fixed available storage budget. Our main result proves that when the generation costs are convex and nondecreasing, there always exists an optimal storage capacity allocation that places zero storage at generation-only buses that connect to the rest of the network via single links. This holds regardless of the demand profiles, generation capacities, line-flow limits and characteristics of the storage technologies. Through a counterexample, we illustrate that this result is not generally true for generation buses with multiple connections. For specific network topologies, we also characterize the dependence of the optimal generation cost on the available storage budget, generation capacities and flow constraints.

I Introduction

I-A Motivation

Energy storage technologies have been argued as “critical to achieving national energy policy objectives and creating a modern and secure electric grid system.” [1]. They have many potential applications in power networks, e.g., see [2, 3] for a detailed survey. At faster time scales (seconds to minutes), storage can be used to reduce variability of renewable sources of energy like wind or solar [4, 5, 6, 7]. At slower time scales (over hours), it can be used for load shifting [8, 9], i.e., generate when it is cheaper and use storage dynamics to follow the demand. Though still very expensive, storage devices based on pumped hydro, compressed air, Lithium-ion based and other technologies have shown significant technical improvements and cost drops [9, 10] over the last decade and are expected to play a central role in an efficient power system [11, 12, 13, 14, 8, 15, 16, 1, 2].

Two natural questions to ask for storage are: (a) What is the optimal investment policy for storage? Where to place them, and how to size them? (b) Once installed, what is the optimal control policy for the storage as well as the generation schedule to minimize generation costs? In this paper, we formulate both problems for slower time-scales in a common framework and present results on sizing such storage units in a network and a charging/ discharging policy for the installed units.

I-B Prior work

Now, we provide a brief overview of the relevant literature. Optimal control policy for storage units has been extensively studied. While the authors in [17, 18, 19] examine the control of a single storage device without a network, the authors in [20, 21] explicitly model the role of the networks in the operation of distributed storage resources. Storage resources at each node in the network are assumed to be known a priori in these settings.

Sizing of storage devices has been studied by several authors, e.g., [22, 23] using purely economic arguments, without explicitly considering the network constraints of the physical system. Authors in [18, 24] have looked at optimal sizing of storage devices in single-bus power systems for fast-time scales, while Kanoria et al. [20] compute the effect of sizing of distributed storage resources on generation cost for specific networks.

The optimal storage placement problem on a general power network has been formulated and studied recently through simulations. The network imposes non-convex power-flow constraints that render such optimization problems NP-hard. These are handled through (a) linearization using DC approximation [25, 26], or (b) a relaxation of the feasible sets using semidefinite programming [27, 28, 29]. For the storage placement problem, Sjödin et al. in [30] uses the former, while Bose et al. in [31] uses the latter.

I-C Our Contribution

In this paper, we study the joint investment decision and control problem for storage devices in a power network. Our main contribution is the result in Theorem 1: when minimizing a convex and nondecreasing generation cost with any fixed available storage budget over a slow time-scale of operation, there always exists an optimal storage allocation that assigns zero storage at nodes with only generation that connect via single transmission lines to the rest of the network. This holds for arbitrary demand profiles and other network parameters.

First, we describe the salient features of our model. As in [20, 18], the investment decision problem is an infinite horizon problem. Hourly aggregate demands over large geographical locations often show periodicity [32] and hence the optimization can be equivalently solved over one time period. The storage units are assumed to have finite capacities and ramp rates. Power exchanges with these devices suffer losses due to inefficiencies. Also, since we optimize the amount of storage placed on each bus, storage is assumed to be infinitely divisible. This is, however, not a limitation for our main result, as is explained in Section IV. The generators have finite capacities with convex nondecreasing costs [33, 20, 19]. The network has been modeled using linearized DC power-flow approximation [34] with finite line-flow capacities. This neglects reactive power over the network, defines voltage magnitudes to be at their nominal values at all buses and assumes the voltage phase angle differences between nodes to be small. Though this is a simplification of the full AC model of the power system with known limitations [26], this approximation is widely used for analysis in optimal power flow [26, 34, 35], transmission expansion planning [36] and electricity market operations [37, 38, 39]. The focus of this work is to derive structural properties of the storage placement problem using the linearized DC model as in [30, 20]; this complements the studies without network models in [19, 18] and simulation studies with a full AC model of the power flow equations [21, 31]. The result generalizes our work in [40] and provides (partial) analytic justification of the observation made empirically in [31, 21, 30]: optimal storage allocation seldom places storage capacities at generator-only buses.

Next, we briefly discuss some of the qualifications of this work. First, to solve a complete storage investment strategy, we need a cost-benefit analysis of installing this new technology. In other words, the savings due to storage needs to be matched with the cost of installation and operation of such units on the grid. In this work, however, we only focus on minimizing cost of generation that estimates the potential benefits of storage. Second, our main result applies to bulk storage on a slow time-scale and does not naturally generalize to scenarios with intermittent renewable generation. Dealing with fast time-scale variability of generation needs a stochastic control framework as in [18, 20]; this, however, is not the focus of the current paper. Third, our main result characterizes storage allocation at generation-only buses that link to the rest of the network via a single transmission line. As shown in Section IV-D, the result does not necessarily hold for generator-only buses with multiple links to the network. Also, it does not address the sizing or placement for any other kind of nodes in the network. We emphasize that this is a preliminary work on storage placement. To the best of our knowledge, this is the first theoretical result on this problem so far over a general power network. Our analysis suggests that there is a potential to exploit the rich underlying structure of this problem; ongoing research aims at finding these properties and overcoming the limitations mentioned.

II Problem formulation

Consider a power network that is defined by an undirected connected graph on nodes (or buses) . For two nodes and in , let denote that is connected to in by a transmission line. We model time to be discrete and indexed by . Now consider the following notation.

-

•

is the known real power demand at bus at time . Hourly demand profiles often show diurnal variations [41], i.e., they exhibit cyclic behavior. Let time-steps denote the cycle length of the variation. In particular, for all , , assume

-

•

is the real power generation at bus at time and it satisfies

(1) where, is the generation capacity at bus .111We do not include ramp constraints on the generators.

-

•

denotes the cost of generating power at bus . The cost of generation is assumed to be independent of time and depends only on the generation technology at bus . Also, suppose that the function is non-decreasing and convex. These assumptions apply to commonly used cost functions in the literature [33, 28, 21, 29], e.g., convex and nondecreasing piecewise linear or quadratic ones.

-

•

The power sent from bus towards bus for two nodes in is limited by thermal and stability constraints as

(2) where is the capacity of the corresponding line.

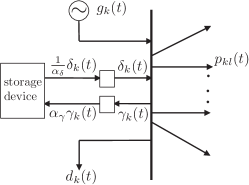

Figure 1: Power balance at node . -

•

and are the average charging and discharging powers of the storage unit at bus at time , respectively. The energy transacted over a time-step is converted to power units by dividing it by the length of the time-step. This transformation conveniently allows us to formulate the problem in units of power [31]. Let denote the charging and discharging efficiencies, respectively of the storage technology used, i.e., the power flowing in and out of the storage device at node at time is and , respectively [18, 42]. The roundtrip efficiency of this storage technology is .

-

•

denotes the storage level at node at time and is the storage level at node at time . From the definitions above, we have

(3) For each , assume , so that the storage units are empty at installation time.

-

•

is the storage capacity at bus . Thus, for all satisfies

(4) -

•

is the available storage budget and denotes the total amount of storage capacity that can be installed in the network. Our optimization algorithm decides the allocation of storage capacity at each node and thus, we have222Note that we do not restrict the capacity sizes a priori. The problem formulation can be extended to include any linear constraints on ’s.

(5) -

•

The charging and discharging rates of storage device at node are bounded above by ramp limits; these limits are assumed to be proportional to the installed storage capacity at node , i.e.,333Note that and are specific to a storage technology. We consider the installment of one kind of storage over the network. Though we present our results with one storage technology, it can be generalized to the joint placement of installing multiple storage types with individual storage budgets for each technology.

(6a) (6b) where and are fixed constants.

Balancing power that flows in and out of bus at time , as shown in Figure 1, we have:

| (7) |

The power flow from bus to bus relates to the voltages at the buses through Kirchoff’s law. Since power is quadratic in voltage, the power flow equations introduce quadratic equalities that render most optimization problems over power networks nonconvex and hence hard to solve and analyze. The role of nonconvexity in power flow optimization has been widely studied in the power system literature ; see [43, 44] surveys. Nonconvex optimizations, in general, are hard to solve and difficult to analyze. To make the model amenable to analysis, one option is to linearize the power flow equations around an operating point. Such a linearization technique popularly used in the literature is the DC approximation [45, Ch. 9] [46, Ch. 6] [25]; for completeness, we discuss it in Appendix A. In this model, the transmission losses (resistances in transmission lines) and reactive power flows in the network are ignored. Specifically, suppose is the susceptance of the transmission line joining buses and and is the voltage phase angle at bus at time . Then, using DC approximation, it can be shown that

| (8) |

Though we ignore all transmission losses for presenting our result, we generalize it in Section IV-B to include losses. The loss model used is discussed further in Appendix A.

Optimally placing storage over an infinite horizon is equivalent to solving this problem over a singe cycle, provided the state of the storage levels at the end of a cycle is the same as its initial condition [31]. Thus, for each , we have

| (9) |

For convenience, denote . Using the above notation, we define the following optimization problem.

Storage placement problem :

| over | |||

| subject to |

where, (1) represents generation constraints, (2), (7) represent power flow constraints, (4),(5),(6),(9) represent the constraints imposed on the charging/discharging control policy of the energy storage devices, and (8) represents the DC approximated Kirchoff’s laws. For the power network, and are state variables, while are controllable inputs to the system.

Given the demand profiles and network parameters, can be efficiently solved to define the optimal investment decision strategy for sizing storage units at different buses, the economic dispatch of the various generators and the optimal control policy of the installed storage units.

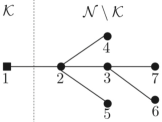

Now, restrict attention to network topologies where each bus either has generation or load but not both444An intermediate bus (one that has no generation or load) is modeled as a load bus. Any losses associated with the node is included as a load.. Partition the set of buses into two groups and where they represent the generation-only and load-only buses respectively and assume and are non-empty. For any subset of , define the following optimization problem.

Restricted storage placement problem :

| over | |||

| subject to | |||

Problem corresponds to placing no storage at the (generation) buses of the network in subset . We study the relation between the problems and in the rest of the paper.

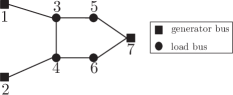

We say bus has a single connection if it has exactly one neighboring node . Similarly, a bus has multiple connections if it has more than one neighboring node in . We illustrate the notation using the network in Figure 2. and . Buses 1 and 2 have single connections and all other buses in the network have multiple connections.

III Main Result

For a subset , let and be the optimal values for problems and , respectively. Now, we are ready to present the main result of this paper.

Theorem 1.

Let be a subset of generation nodes that have single connections. Consider the storage placement problem , the restricted storage placement problem and their respective optimal costs and . If is feasible, then is feasible and .

Problem , in general, may have multiple optimal solutions, but Theorem 1 proves that there always exists an optimal allocation of storage capacities that places no storage at any subset of generation buses with single connections, regardless of the demand profiles, generation capacities, line-flow limits and characteristics of the storage technologies.

Next, we make the following remarks about the result. (a) Notice that we have restricted our attention to generator buses in that have single connections only. This does not generalize to the case if includes generator buses with multiple connections; see Section IV-D for an example. (b) Storage capacity allocation at each bus has been assumed to be infinitely divisible, i.e., each that satisfies the budget constraint in (5) is feasible. But it might be impractical to implement an optimal allocation with arbitrarily small storage capacities. This, however, is not a limitation for the result in Theorem 1 as it only specifies zero storage capacities at some buses and does not characterize storage sizes at others. (c) In our formulation, we assume perfect knowledge of the entire demand profile. The result in Theorem 1, however, holds true for any demand profile as long as the storage placement problem is feasible.

Before presenting the proof, we provide some intuition behind the result. Consider a generator bus that has a single connection to node in the network. First, we solve the storage placement problem for this network. Suppose this results in some storage capacity installed at bus with some charging/ discharging profile . To construct a solution of the restricted storage problem , a natural idea to explore is to shift this storage from bus to bus and operate it with the optimal control policy () obtained from the solution of . This shift can be done, provided that the optimal generation profile , itself, defines a feasible flow over the transmission line, i.e., for all . The key insight to prove this fact is that at the time instant where is at its maximum, the storage at bus cannot be charging. If it was indeed charging, one could generate less and charge less at the same time. In what follows, we formalize this argument.

III-A Proof of Theorem 1

We only prove the case where the round-trip efficiency is , but the result holds for as well. Assume is feasible throughout. For any variable in problem , let be the value of the corresponding variable at the optimum. In our proof, we use the following technical result.

Lemma 1.

Suppose is convex. Then, for any and :

Proof:

Applying Jensen’s inequality to the convex function , we have

The result follows from adding the inequalities above. ∎

Consider node and . Node is uniquely defined as has a single connection. Problem , in general, has multiple optima. In the following result, we characterize only a subset of these optima.

Lemma 2.

There exists an optimal solution of such that for all and all ,

-

(a)

,

-

(b)

.

Proof:

The feasible set of problem is a bounded555 Without loss of generality, let bus be the slack bus and hence for all . Boundedness of the set of feasible solutions of then follows from the relations in (1), (2), (5), (6) and (8). polytope and the objective function is a continuous convex function. Hence the set of optima of is a convex compact set [47]. Now, with every point in the set of optimal solutions of , consider the function . This is a linear continuous function on the compact set of optima of and hence attains a minimum. Consider the optimum of where this minimum is attained. We prove parts (a) and (b) in Lemma 2 for this optimum.

(a) Suppose, on the contrary, we have , and for some . Define

Note that . Now, for bus , construct modified generation, charging and discharging profiles that differ from only at as follows:

Note that, for all , the storage level and the power flowing from bus to bus remain unchanged throughout. It can be checked that the modified profiles define a feasible point of . Since is non-decreasing, we have and hence the additivity of the objective in over and implies that this feasible point has an objective function value of at most . It follows that this feasible point defines an optimal point of . Also, we have and thus, this optimum of has a strictly lower , contradicting our hypothesis. This completes the proof of Lemma 2(a).

(b) If for all , then trivially holds. Henceforth, assume , and consider , such that .

Now, suppose that and hence from Lemma 2(a). Since storage charges by an amount , we have . Also, by hypothesis and hence the storage at node discharges from to zero in . Let be the first time instant after when the storage device at bus discharges, i.e.

| (10) |

Thus, . Now, we argue that . Since , clearly . Suppose this inequality is strict. Then we show how to construct an optimum of with a lower to contradict our hypothesis. Define

Observe that . Construct the modified generation, charging and discharging profiles at node , that differ from only at and as follows:

Also, define the modified storage level using and . To provide intuition to the above modification, we essentially generate and store less at time by an amount . This means at a future time , we can discharge less from the storage device and hence have to generate more to compensate. From the definition of , it follows that for , we have , , and . Also, the line flows remain unchanged. For the storage levels, it can be checked that

This proves that the modified profiles define a feasible point for . Also, we have

| (11a) | ||||

| (11b) | ||||

where (11a) follows from the non-decreasing nature of and (11b) follows from our assumption and Lemma 1. The modified profiles are feasible in with an objective value at most . Thus, they define an optimum of . Also,

This implies that this optimum of has a lower , contradicting our hypothesis. Hence, we have .

Finally,

This completes the proof of the lemma. ∎

To prove Theorem 1, consider the optimal solution of that satisfies Lemma 2(b). For , itself defines a feasible flow over the line joining buses and , where is the unique neighboring node of in graph . Now, transfer the storage device at bus to bus . In particular, define a new storage capacity and operate it with a charging (and discharging) profile (and similarly for ). For node , define the new voltage phase angle . The power flow from bus to bus is then given as . These profiles define a feasible point of with an objective value of . Combining with the fact that , we conclude . Finally, we do this successively for each to obtain .

IV Discussion and extensions

Here, we discuss our main result in more detail. We begin by considering cases where Theorem 1 is helpful to the network planner in Section IV-A. Then in Section IV-B, we present an extension of our result to the case with losses in the network. We comment on the importance of convexity in the problem formulation in Section IV-C and finally explore storage placement at buses with multiple connections in Section IV-D.

IV-A Applicability of Theorem 1

Figure 3 depicts a few power networks, where Theorem 1 applies, i.e., network topologies with generator buses that have single connections. While this may seem quite restrictive, in practice, many networks have generators of this type. The single generator single load case in Figure 3a models topologies where generators and loads are geographically separated and are connected by a transmission line, e.g., see [48]. This is common where the resources for the generation technology (like coal or natural gas) are available far away from where the loads are located in a network. Figure 3b is an example of a radial network, i.e., an acyclic graph. Most distribution networks conform to this topology666Two assumptions in our model hold for transmission networks but not strictly for distribution networks: (a) Resistances in distribution lines are not negligible and hence DC approximation does not generally apply [26], (b) Three different types of loads, namely, constant power, constant current and constant impedance loads show different behavior in distribution networks [33]; but in aggregate, demands can be modeled as constant power loads in transmission networks, as in IEEE distribution feeders [49]., e.g., see [49, 29]. Also, isolated transmission networks, e.g., the power network in Catalina island [5] are radial in nature.

Next, we discuss how Theorem 1 defines an investment strategy that is robust to many system parameters. Our result suggests that it remains optimal not to place any storage at buses in set even if the demand profiles, generation capacities, line flow capacities or admittances in the network change. Consider the example in Figure 3a. Suppose the line flow capacity is larger than the peak value of the demand profile, i.e., . It can be checked that placing all the available storage at the generator bus is also an optimal solution. If at a later time during the operation of the network, the demand increases such that the peak demand surpasses the line capacity, this placement of storage no longer remains optimal and requires new infrastructure for storage to be built on the demand side to avoid load shedding. If, however, we use the optimum as suggested by the problem and place all storage on the demand side from the beginning, then this placement not only can accommodate the change in the demand, but it also remains optimal under the available storage budget. To explore another such direction, suppose another generator is built to supply the load in Figure 3a. From Theorem 1, it follows that we still do not need storage allocation at bus 1 even with the extended network.

IV-B Modeling losses in the network

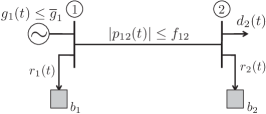

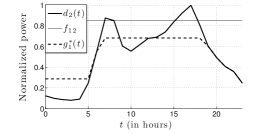

Our problem formulation uses linearized DC approximation for the power flow equations. This approximation ignores all transmission losses in the network. Here, we explore one popular way to incorporate losses and generalize the result in Theorem 1. To simplify the presentation, consider the single generator single load network shown in Figure 4. Generator at bus 1 is connected to a load at bus 2 using a single line, i.e., and . We make further simplifications: assume , i.e., the storage devices are perfectly efficient. Hence, define for and ,

Recall that is the power injected at bus 1 towards bus 2. However, it suffers a loss before reaching bus 2. As detailed in Appendix A, losses in such a network can be approximated to be quadratic in the power sent, i.e., loss , where is some positive constant that depends on the impedance of the transmission line. Thus, power received at bus 2 is . Then balancing power on both buses, we get for ,

| (12) |

Let the storage placement problem with losses incorporated be . Following the definition of , define the restricted storage placement problem with losses as ; this is essentially the problem with the extra constraint . Let the optimal costs of these problems be and , respectively. With this notation, we have the following result.

Proposition 1.

The storage placement problems with losses and satisfy .

In what follows, we provide a proof sketch; details are deferred to Appendix B. Perhaps the first thing one notices about the problems and is that they are nonconvex due to the quadratic equality in (12). Modify the problems and to their convex relaxations, where the second equality in (12) is changed to . Call these relaxations as problems and , respectively. Let their optimal costs be and , respectively. Using the set inclusion relations among the feasible sets of the programs , and , it is easy to argue that

| (13) |

Then the proof proceeds in two steps. First, we show and then prove that the relaxation is tight, i.e. . Using (13), it is straightforward to see that these two statements imply Proposition 1.

We briefly discuss our result in Proposition 1 here. First, notice that the optimization problem is non-convex due to the constraint in (12). Consequently, it is computationally hard to solve. However, considers a convex relaxation of this nonconvex constraint and is a convex program that often admits an efficient solution. In addition, we have and thus provides a computationally tractable way of exactly solving . Second, notice that Proposition 1 considers losses that are quadratic in the power sent. The proof technique generalizes to the case with any convex function of the power sent. Third, we have presented Proposition 1 for a two-node network only. This idea can be generalized to a network with losses to derive a result similar to Theorem 1, i.e., in a network with quadratic (or convex) losses, there exists an optimal storage placement with zero storage at generators with single connections.

IV-C Effect of concave cost functions

Theorem 1 assumes a nondecreasing convex cost of generation; this is commonly found in practice, e.g., the costs of coal-based generators are often increasing quadratic functions [33]. Convexity is sufficient for our result to hold, but may not be necessary. However, the following example shows that the theorem need not generalize for arbitrary non-decreasing functions. Consider the network in Figure 4 and let the cost of generation at bus 1 be a concave cost function , if and otherwise. With , let the load bus have a demand profile and connecting them. Further let , , and . All quantities are in per units. It can be checked that the optimal generation profile of is , thus, . On the other hand, the generation profile is feasible for . Hence, . We also remark that when is not convex, and are not convex programs and, hence, cannot be solved efficiently.

IV-D On generators with multiple connections

Our result in Theorem 1 considers generator buses that have single connections only. A natural direction to generalize the result is to include generator buses with multiple connections. However, we show through an example that generator buses with multiple connections may not always have zero storage capacity in the optimal allocation. Consider a 3-node network as shown in Figure 5. All quantities are in per units. Let the cost of generation at node 1 be . Let and the demand profiles at nodes 2 and 3 be and . Also, suppose that the line and generation capacities are and the available storage budget is . Finally, assume no losses and ignore the ramp constraints in the charging and discharging processes, i.e. and . The optimal storage allocation for the two problems and is and , respectively. Also, the optimal generation profile for the two problems can be computed to be and , respectively. Thus, .

We provide some intuition behind the design of the counterexample. First, notice that if demands at buses 2 and 3 are multiples of each other, i.e., for some constant (and so are the line capacities), the 3-node network can be roughly thought of as two single-generator-single-load systems with nodes and , respectively and one can again prove that the generator node does not need any storage capacity in an optimal allocation. We formalize this statement in Proposition 5 in Appendix C. Thus to expect in , we consider demand profiles that show opposite trends. Second, if or is the minimum value required for a feasible flow, we show in Proposition 4 in Appendix C that there exists an optimal point with . Hence, we consider a storage budget that is in the middle. Third, note that if line capacities are large, then an optimal allocation with trivially exists. Thus, we construct for which and are feasible but the network is congested. This illustrates some key directions to look at for characterizing cases where for generator buses with multiple connections.

V Concluding remarks

In this paper, we formulate the optimal storage placement problem for load shifting at slow time scales. We show in Theorem 1 that generator nodes with single connections get zero storage capacity at optimal allocation; this holds regardless of the demand profiles, generation capacities, line-flow limits and characteristics of the storage technologies. The counterexample in Section IV-D shows that such a general result does not hold beyond the settings in Theorem 1. However, notice that the demand profiles of the two demand nodes considered in this counterexample show opposite variations. When demands vary similarly, e.g., in Appendix C (specifically Proposition 5), it can be shown that one does not need storage installed at the generator node for the same network. This suggests that one would expect to discover structural results when demand profiles and/ or network topologies are restricted to a certain class. Characterizing these classes is a natural direction to explore.

In our formulation, we have neglected any fixed installment cost of storage; we have only minimized the total generation cost over every cycle of operation. It is easy to argue that the result extends to the case where such installment costs are linear in the storage capacity installed. The role of general (possibly nonlinear) installment costs on investment decisions would be an interesting are of study.

As a final remark, we have only focussed on minimizing the cost of conventional generation. The primary use of storage in this work is load shifting, i.e., arbitrage between power consumed at different times through storage rather than following the load variations with generation. However, an important application of storage is to mitigate intermittency of stochastic renewable generation at faster time-scales. We would like to pursue the implications and extensions of this paper to such scenarios.

VI Acknowledgements

The authors gratefully acknowledge Prof. K. Mani Chandy (Caltech), Mr. Paul DeMartini (Resnick Institute, Caltech), Christophe Hennekinne (Cambridge) and all the reviewers for their comments.

References

- [1] “Distributed energy storage serving national interests: Advancing wide-scale DES in the United States,” KEMA Inc, 2012.

- [2] S. Chu and A. Majumdar, “Opportunities and challenges for a sustainable energy future,” Nature, vol. 488, no. 7411, pp. 294–303, 2012.

- [3] “Electrical energy storage,” IEC White paper, 2011.

- [4] Y. M. Atwa and E. F. El-Saadany, “Optimal allocation of ESS in distribution systems with a high penetration of wind energy,” IEEE Trans. on Pow. Sys., vol. 25, no. 4, pp. 1815–1822, Nov. 2010.

- [5] H. Xu, U. Topcu, S. Low, C. Clarke, and K. Chandy, “Load-shedding probabilities with hybrid renewable power generation and energy storage,” in 48th Annual Allerton Conf. on Comm., Control, and Comp. IEEE, 2010, pp. 233–239.

- [6] C. Budischak, D. Sewell, H. Thomson, L. Mach, D. Veron, and W. Kempton, “Cost-minimized combination of wind power, solar power and electrochemical storage, powering the grid up to 99.9% of the time,” Jour. of Pow. Sources, 2012.

- [7] D. Biello. (2008) Storing the breeze: New battery might make wind power more reliable. [Online]. Available: http://www.scientificamerican.com/article.cfm?id=storing-the-breeze-new-battery-might-make-wind-power-reliable

- [8] J. Eyer and G. Corey, “Energy storage for the electric grid: Benefits and market potential assessment guide,” Sandia Nat. Lab., 2010.

- [9] D. Rastler, Electricity Energy Storage Technology Options: A White Paper Primer on Applications, Costs and Benefits. Electric Power Research Institute, 2010.

- [10] “2020 Strategic analysis of energy storage in California,” Cali. Energy Comm., Nov., 2011.

- [11] R. Schainker, “Executive overview: Energy storage options for a sustainable energy future,” in Proc. of IEEE PES Gen. Meeting, 2004, pp. 2309–2314.

- [12] A. Nourai, “Installation of the first distributed energy storage system at american electric power,” Sandia Nat. Labs, 2007.

- [13] P. Denholm, E. Ela, B. Kirby, and M. Milligan, “The role of energy storage with renewable electricity generation,” Nat. Renewable Ener. Lab., 2010.

- [14] P. Varaiya, F. Wu, and J. Bialek, “Smart operation of smart grid: Risk-limiting dispatch,” Proc. of the IEEE, vol. 99, no. 1, pp. 40–57, 2011.

- [15] J. Greenberger. (2011) The smart grid’s problem may be storage’s opportunity. [Online]. Available: http://theenergycollective.com/jim-greenberger/70813/smart-grids-problem-may-be-storages-opportunity

- [16] D. Lindley, “Smart grids: The energy storage problem.” Nature, vol. 463, no. 7277, p. 18, 2010.

- [17] I. Koutsopoulos, V. Hatzi, and L. Tassiulas, “Optimal energy storage control policies for the smart power grid,” in IEEE Int. Conf. on Smart Grid Comm. IEEE, 2011, pp. 475–480.

- [18] H. Su and A. Gamal, “Modeling and analysis of the role of fast-response energy storage in the smart grid,” arXiv preprint arXiv:1109.3841, 2011.

- [19] M. Chandy, S. Low, U. Topcu, and H. Xu, “A simple optimal power flow model with energy storage,” in Proc. of 49th Int. Conf. on Decision and Control., 2010.

- [20] Y. Kanoria, A. Montanari, D. Tse, and B. Zhang, “Distributed storage for intermittent energy sources: Control design and performance limits,” in Proc. of 49th Annual Allerton Conf. on Comm., Control, and Comp. IEEE, 2011, pp. 1310–1317.

- [21] D. Gayme and U. Topcu, “Optimal power flow with large-scale energy storage integration,” To appear in IEEE Trans. on Pow. Sys., 2012.

- [22] M. Kraning, Y. Wang, E. Akuiyibo, and S. Boyd, “Operation and configuration of a storage portfolio via convex optimization,” in Proc. of the IFAC World Congress, 2010, pp. 10 487–10 492.

- [23] P. Denholm and R. Sioshansi, “The value of compressed air energy storage with wind in transmission-constrained electric power systems,” Energy Policy, vol. 37, pp. 3149–3158, 2009.

- [24] P. Harsha and M. Dahleh, “Optimal management and sizing of energy storage under dynamic pricing for the efficient integration of renewable energy,” in preparation.

- [25] K. Purchala, L. Meeus, D. Van Dommelen, and R. Belmans, “Usefulness of DC power flow for active power flow analysis,” in IEEE PES Gen. Meeting. IEEE, 2005, pp. 454–459.

- [26] B. Stott, J. Jardim, and O. Alsaç, “DC power flow revisited,” IEEE Trans. on Power Sys., vol. 24, no. 3, pp. 1290–1300, Aug. 2009.

- [27] X. Bai, H. Wei, K. Fujisawa, and Y. Wang, “Semidefinite programming for optimal power flow problems,” Int. Jour. of Elec. Pow. & Energy Sys., vol. 30, no. 6-7, pp. 383–392, 2008.

- [28] J. Lavaei and S. Low, “Zero duality gap in optimal power flow problem,” IEEE Trans. on Power Sys., vol. 27, no. 1, pp. 92–107, Feb. 2012.

- [29] S. Bose, D. Gayme, S. Low, and K. Chandy, “Quadratically constrained quadratic programs on acyclic graphs with application to power flow,” To appear in IEEE Trans. on Aut. Control, 2012.

- [30] A. E. Sjödin, D. Gayme, and U. Topcu, “Risk-mitigated optimal power flow for wind powered grids,” in Proc. of the American Ctrl. Conf., 2012.

- [31] S. Bose, F. Gayme, U. Topcu, and K. Chandy, “Optimal placement of energy storage in the grid,” in Proc. of 51st Int. Conf. on Decision and Control. IEEE, 2012.

- [32] Today’s outlook. [Online]. Available: http://www.caiso.com/outlook/SystemStatus.html

- [33] A. R. Bergen and V. Vittal, Power Systems Analysis, 2nd ed. Prentice Hall, 2000.

- [34] K. Purchala, L. Meeus, D. Van Dommelen, and R. Belmans, “Usefulness of DC power flow for active power flow analysis,” in Proc. of IEEE PES General Meeting. IEEE, 2005, pp. 2457–2462.

- [35] K. S. Pandya and S. K. Joshi, “A survey of optimal power flow methods,” Jour. of Theoretical and App. Info. Tech., vol. 4, no. 5, pp. 450–458, 2008.

- [36] I. J. Silva, M. J. Rider, R. Romero, and C. A. Murari, “Transmission network expansion planning considering uncertainty in demand,” Power Systems, IEEE Transactions on, vol. 21, no. 4, pp. 1565–1573, 2006.

- [37] N. S. Rau, “Issues in the path toward an rto and standard markets,” IEEE Trans. on Power Systems, vol. 18, no. 2, pp. 435–443, 2003.

- [38] ——, Optimization principles: practical applications to the operation and markets of the electric power industry. John Wiley & Sons, Inc., 2003.

- [39] C. Wu, S. Bose, A. Wierman, and H. Mohesenian-Rad, “A unifying approach to assessing market power in deregulated electricity markets.”

- [40] C. Thampoulidis, S. Bose, and B. Hassibi, “Optimal large-scale storage placement in single generator single load networks,” 2013, accepted at IEEE PES Gen. Meeting.

- [41] Hourly load data. [Online]. Available: http://www.pjm.com/markets-and-operations/energy/real-time/loadhryr.aspx

- [42] M. Korpaas, A. T. Holen, and R. Hildrum, “Operation and sizing of energy storage for wind power plants in a market system,” Int. Jour. of Elec. Pow. & Energy Sys., vol. 25, no. 8, pp. 599–606, 2003.

- [43] R. P. O Neill, A. Castillo, and M. B. Cain, “The iv formulation and linear approximations of the ac optimal power flow problem (opf paper 2),” Technical report, US FERC, Tech. Rep., 2012.

- [44] S. Frank, I. Steponavice, and S. Rebennack, “Optimal power flow: a bibliographic survey: Parts i & ii,” Energy Systems, vol. 3, no. 3, pp. 259–289, 2012.

- [45] J. J. Grainger and W. D. Stevenson, Power system analysis. McGraw-Hill New York, 1994, vol. 621.

- [46] G. Andersson, “Modelling and analysis of electric power systems,” EEH-Power Systems Laboratory, Swiss Federal Institute of Technology (ETH), Zürich, Switzerland, 2004.

- [47] S. Boyd and L. Vandenberghe, Convex Optimization. Cambridge Univ. Press, 2004.

- [48] L. Gaillac, J. Castaneda, A. Edris, D. Elizondo, C. Wilkins, C. Vartanian, and D. Mendelsohn, “Tehachapi wind energy storage project: Description of operational uses, system components, and testing plans,” in IEEE PES Transmission and Distribution Conf. and Expo., 2012, pp. 1 –6.

- [49] IEEE Distribution Test Feeders. [Online]. Available: http://www.ewh.ieee.org/soc/pes/dsacom/testfeeders/index.html

- [50] B. Stott, J. Jardim, and O. Alsac, “Dc power flow revisited,” IEEE Trans. on Power Systems, vol. 24, no. 3, pp. 1290–1300, 2009.

- [51] C. Coffrin, P. Van Hentenryck, and R. Bent, “Approximating line losses and apparent power in ac power flow linearizations,” in Power and Energy Society General Meeting, 2012 IEEE. IEEE, 2012, pp. 1–8.

Appendix A DC Approximation and losses

In this section, we derive the linearized DC approximation and the loss model for the power flow equations from Kirchoff’s laws. We start with introducing some notation. Define and for any complex number , let define its conjugate.

Recall that the power network is defined by an undirected connected graph on nodes (or buses) . Let be the voltage at bus . Since, the power network works in sinusoidal alternating current mode, the voltages and currents are represented as complex numbers777This is often referred to as the phasor representation [33] that essentially represents the time-varying signal in the Fourier domain.. For convenience, let , where is the magnitude and is the argument of . The transmission line joining buses and has an admittance . Usually, is positive since most transmission lines are inductive in nature. Also, let there be shunt elements associated with each bus. For the shunt element, however, is usually non-negative since shunt elements are generally capacitive888We refer the reader to [33] for the one phase equivalent lumped circuit model of power systems..

From Kirchoff’s laws, it then follows that the apparent power injection (generation - demand) at bus satisfies

| (14) |

A-A DC Approximation

Now, we introduce the DC approximation [45, Ch. 9], [46, Ch. 6], [33, 25, 50]:

-

1.

Resistances in transmission lines are small compared to the inductances and hence ignored, i.e., . Shunt reactances are similarly ignored, i.e., .

-

2.

Voltage magnitudes are maintained close to their nominal values. Measured in per units, for all .

-

3.

Voltage phase angle differences across a transmission line are small, i.e., for , we have and .

Using the above approximation in (14), we get

| (15) |

Notice that the right hand side of (15) is real and hence ; in DC approximation, there is no reactive power flow. The loss associated with bus (or more accurately in its shunt element) is and is usually included in the net real power demand at bus .

A-B Modeling Losses

Now, we turn to modeling losses. We refer the reader to [51, 50] for detailed discussions on incorporating losses in linearized DC approximated power flow equations. For any complex number , let denote its magnitude and denote the real part of . For nodes in graph , notice that the current flowing from bus to bus is given by . The resistance on this line is . Then the loss on this line is given by

Using the approximations and , we have

Given the DC approximation, the power that flows from bus to is . Thus the loss incurred on the transmission line is given by

Appendix B Proof of Proposition 1

Recall the definitions of problems and defined for the single generator single load network in Figure 4. As outlined in Section IV-B, the proof consists of two steps: (a) and (b)

B-A Proof of

From the size of the feasible sets, it is easy to check that We will show that equality holds in the above relation as follows: we start with an optimal solution of and appropriately modify it to yield a solution with the same generation profile (thus, the same cost) but such that it satisfies (thus, feasible for ). Denote the generation profile, storage profiles and storage capacities of such an optimal solution of as , , , and , respectively. Also, let denote the optimal storage level at the generation node at time . From the feasibility constraints of :

| (16) |

The main idea of the proof is similar to that of Theorem 1: we “shift” the storage with capacity from node to node , i.e., the modified storage capacity at node 2 becomes and its associated storage profile becomes . Notice that the added term must be a feasible storage profile, i.e., it satisfies (4) and (9); they are repeated here for convenience. For ,

| (17) |

Also, it must satisfy the power balance equation

| (18) |

In the absence of losses () in Theorem 1, it was sufficient to choose ; this choice, however, need not satisfy (18) for . In what follows, we show how to construct a suitable .

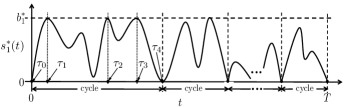

Consider a representative storage profile in Figure 6. We divide the time horizon into “cycles” which are time intervals with the property that is only at the start and end of the interval and strictly positive in between. We construct that has the same set of cycles as , i.e.

| (19) |

It is easy to check that it suffices to construct over one such cycle. To reflect this change, the relations in (17) are modified as follows: the summations run over from the start of a cycle and is replaced by the end of the cycle.

For convenience, define . Without loss of generality, we construct over the first cycle as in Figure 6. Also, let be the sequence of time instants at which the storage at node is at its capacity999If within the cycle, then .. Formally, we have

Consider the optimal solution of which attains the minimum of the function over the set of optimal solutions of . We begin by showing a useful property of this optimal solution in the following result.

Lemma 3.

Consider such that and .

-

(a)

If , then .

-

(b)

If there exists such that , then .

Proof:

The proof mimics the proof of Lemma 2; we omit some details for brevity.

(a) Suppose to the contrary . Define

Then it can be checked that . Construct a modified generation, charging and discharging profile at node , , that differ from only at and as follows:

As in the proof of Lemma 2, it can be shown that the modified profiles define a feasible and optimal solution. However, we also have and which contradicts our hypothesis.

(b) This proof is similar to the first part. Suppose to the contrary . Define

Again, we have and thus we construct modified profiles that differ from only at and as follows:

It can be checked that the modified profiles define a feasible and optimal solution with and , contradicting our hypothesis. ∎

Next, we choose scalars for each that helps us in defining . First, define

and for ,

Notice that always exists. However, may not be defined if . Now, define the scalars ’s as follows.

| (20) | ||||

| (21) | ||||

| (22) |

We characterize the properties of ’s in the following result.

Lemma 4.

For ,

-

(a)

,

-

(b)

for all .

Proof:

(a) From (20)-(22), it is straightforward to conclude that ’s are nonnegative. Next, we show the following property: for any such that , we have

| (23) |

Suppose to the contrary that . Define

Notice that . We define a modified generation profile that differs from only at . Specifically, . Clearly, . Furthermore, from the definition of , it follows that

| (24) | ||||

Now, the function is decreasing for . Thus, we have

i.e., satisfies (16) at . Hence, is feasible. Furthermore, for all . Since the cost of generation is nondecreasing, it implies that is in fact optimal. However, which contradicts our initial assumption. This completes the proof of (23).

Now we turn to prove . Let in (23) equal . Using (23) in the definition of , it is easy to conclude that , for each .

Finally, for , if exists, then choose and . Applying Lemma 3, we get . If does not exist, let be any instant after , where . Again, applying Lemma 3 with and using (23), we get . That completes the proof of Lemma 4(a).

(b) It suffices to prove that

| (25) |

First, consider the case . If , then from the definition of , it follows that . If, on the other hand, , then from Lemma 3, we have .

Now, we use the ’s to construct as follows. For , and :

It is left to prove that a storage placement solution defined by , , , , is indeed feasible for . Denote We show this in the following four steps.

To verify : For any , it follows from (16) that

When combined with Lemma 4(b), we get

| (26) |

For identify in (26) to establish the desired result. For use from Lemma 4(a) to find that . Combine this with (26) to conclude.

To verify : This is similar to the proof of Lemma 2(b). Consider to be the time instant in the cycle where is maximum. Using Lemma 3, it can be argued that . Hence, .

To verify : This follows from the feasibility of the problem .

To verify , and : First, consider the case . We have . Also, from Lemma 4(a). Combining the above,

Next, consider the case , for . Note that for each . Thus, we have

| (27) | ||||

| (28) |

From (27), we find that . This follows from two observations: (i) from Lemma 4(a) and (ii) from the feasibility of . On the other hand, (28) establishes that . For this observe that: (i) from Lemma 4(a) and (ii) from the feasibility of . The argument for the case is similar. Finally, we analyze . Using (28), we have

B-B Proof of

Among the optimal points of , consider the one that minimizes ; let be the corresponding optimal generation profile and storage charging/ discharging profile at node 2. If for all , then are feasible for and hence . Now, suppose to the contrary there exists such that

| (29) |

We consider the following two cases.

Case 1:

Then and hence . Let . Notice that always exists. Define

It can be checked that . Construct modified storage profile that differs from only at and as follows:

Then, it can be shown that and . Also, and . Thus, the solution defined by the modified profile is feasible. It is also optimal since it has the same generation profile . However, which leads to a contradiction.

Case 2:

Here, we construct a modified generation profile as follows. If , let . Otherwise, set such that and . It is easy to check that such a exists since the quadratic function increases in and decreases in . In both cases, and hence defines an optimal generation profile with , which is a contradiction.

Appendix C Partial results on specific network topologies

Here, we present some partial results on the storage placement problems for two specific classes of networks: (1) a 2-node network with a single generator bus and a single load bus in Figure 4, and (2) a star network with a central generator bus serving multiple loads via transmission-constrained lines. We explore some salient features of the optimal placement. For ease of presentation, we assume that the costs are strictly convex at each node, neglect storage efficiency losses and ignore ramping constraints with . The proofs of the results are included in Appendix D.

C-A Single Generator Single Load Network

For this network, placing all the available storage resources at the load bus is always optimal. This is an immediate consequence of Theorem 1. Now, for any fixed demand profile at the load bus, we analyze the behavior of the optimal cost of production as a function of the generation capacity , the line flow capacity and the available storage budget . Through this analysis, we hope to gain insights on marginal savings in terms of generation cost with additional investments in storage capacity, line capacity and storage budget. Let the parameterized storage placement problem be and its optimal cost be . Similarly define, and . Then the optimal costs satisfy the following:

Proposition 2.

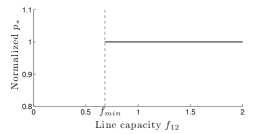

For any , problem is feasible iff , where

| (30) |

Moreover, if , then .

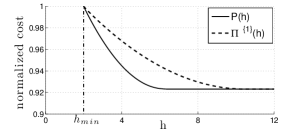

We interpret this result as follows. If either the line flow limit or the generation capacity , the load cannot be satisfied. Notice that is non-increasing in ; this suggests that storage can play a role in avoiding transmission upgrades when dealing with lowering generation costs [23]. However, when and , the optimal cost of operation does not depend on the specific values of and . Thus, investing in line limits and generation capacities over do not reduce the cost of operation. The behavior of as a function of is illustrated in Figure 7b.

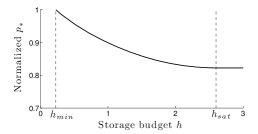

Next, we characterize the behavior of and its optimal cost as a function of . For a given and , the minimum required storage budget to serve the load depends on the demand profile ; it may even be the case that the problem remains infeasible no matter how large the storage budget is. Also, when we allow larger storage budgets, the generation cost does not reduce beyond a point, i.e., there exists such that for all . Between and , the optimal cost is decreasing and convex in . Thus, we have diminishing marginal returns on the investment on storage, i.e., the benefit of the first unit installed is more than that from the second unit. The behavior of is illustrated in Figure 7c. In what follows, we formalize this discussion.

Construct the sequence as follows. Let . Define iteratively:

| (31) |

for , where is the smallest integer for which . Note that the sequence depends only on the demand profile . For any , let .

Proposition 3.

Problem satisfies:

-

(a)

If , then is infeasible for all .

-

(b)

Suppose, . Then, is feasible iff and is convex and non-increasing in , where

(32) Furthermore, is constant for all , where

(33) where

(34)

C-B Star Network

Consider the star network on nodes as shown in Figure 8. For this network and . We showed in Section IV-D that for such a generator bus with multiple connections, placing zero storage at bus 1 is not necessarily always optimal for an arbitrary storage budget . However, Proposition 4 below shows that provided that the available storage budget is either (a) exactly equal to the minimum value required for which and are feasible or (b) is large enough.

To formalize notation, consider the problems , and their optimal costs and as a function of . For simplicity, we consider the case . Then we have the following result.

Proposition 4.

Suppose for all . There exists , such that and are feasible if and only if , where

| (35) |

Also, and satisfy

-

(a)

,

-

(b)

there exists such that for all .

The behavior of and is depicted in Figure 9 for the case where . We end this section with a remark on . The proof in Appendix D essentially shows that , and where is the finite optimal storage level at bus 2 for the problem .

Now, we restrict attention to a special case of the problem over the star network.

Proposition 5.

Suppose there exists positive constants , such that for all and

| (36) |

If is feasible, then is feasible and .

We showed through an example in Section IV-D that generator nodes with multiple connections may need nonzero storage capacities under optimal allocation. However, the demand profiles considered in the specific example showed opposite trends. In practice, aggregate demand profiles at various nodes show similar diurnal variations [41]. To study this, we consider the case where loads at various demand nodes are proportional to each other and the line capacities are proportional to the average demands at each node. In Proposition 5, we recover a result similar to Theorem 1. This suggests a potential direction for future investigation: to characterize the properties of storage placement when demands show similar variations and the transmission lines have suitable capacities to meet the demand.

Appendix D Proofs of partial results

Here, we present the proofs of Propositions 2–5. For the single generator single node and the star networks, we drop the voltage angles . For any value of the power flow from bus to bus , voltage angles can always be chosen to satisfy the power flow constraint in (8). Furthermore, since , define be the power that flows into the storage device at node at time . Notice that can be positive or negative depending on whether power flows in or out of the storage device. Also, the storage level of the storage device at node , at time can be written as .

D-A Proof of Proposition 2

We drop subscripts from the variables , and the superscript from for ease of notation throughout Sections D-A and D-B.

From Theorem 1, it suffices to show the claim for and . First, we show that if is feasible, then . Fix any and let be a feasible generation profile. Since , we have for any

| (37) |

Furthermore, for any , the power extracted from the storage device between time instants and cannot exceed the total storage budget and hence we have

| (38) |

Since is feasible, for all . Hence, combining (37) and (38), we get

Next, we show that is sufficient for to be feasible. Consider the optimal generation profile for the relaxed problem . Suppose it satisfies

| (39) |

Then is also feasible and optimal for problem for . Also, for . It remains to show that (39) indeed holds. Consider the following notation.

In the above definition for convenience. If , then (39) clearly holds. Henceforth, assume . Then, satisfies:

| (40) |

Now, suppose the following holds:

| (41) |

If (41) holds, it follows from (40):

and hence (39) is satisfied. Next, we show that (41) indeed holds to complete the proof. First we prove that , i.e., the storage device at node fully discharges at time . Suppose . As in Lemma 2, we construct a modified generation profile and storage control policy that is feasible and has an objective function value no greater than . But, the optimal generation profile is unique since the cost function is assumed to be strictly convex. Hence we derive a contradiction. By hypothesis, and hence storage device at bus discharges for some . Let be the first such time instant. Define

Notice that . Consider the modified generation profile and control policy , that differ from and only at and as follows:

Using Lemma 1, we have

It can be checked that the modified profiles are feasible for . The details are omitted for brevity. This is a contradiction and hence .

Next, we characterize . If , then . If , we prove that , i.e., the storage device at node is fully charged at time . Suppose . As above, we construct a modified generation profile and storage control policy that achieves an objective value no greater than to derive a contradiction. In particular, define

Observe, Consider and , that differ from and only at and as follows:

As above, this defines a feasible point for and achieves an objective value strictly less than . This is a contradiction and hence for .

D-B Proof of proposition 3

From Theorem 1, it suffices to prove the claim for and .

To the contrary of the statement of the Proposition suppose that and is feasible for some . Then, it follows directly from Proposition 2 that , contradicting our hypothesis.

First we show that if is feasible then . Suppose is feasible. Then, for all Proposition 2 implies that Rearranging this we get Also, and hence:

Now we show that is sufficient for to be feasible. The relation can be equivalently written as follows:

| (42) |

Also, by hypothesis, we have

| (43) |

Combining (42) and (43), we get . Then, Proposition 2 implies that is feasible. Convexity and non-decreasing nature of as a function of follows from linear parametric optimization theory [47].

Finally, we prove that is constant for all , where is as defined in (33). The proof idea here is as follows. We construct the optimal generation profile for the problem and show that it is feasible and hence optimal for the problem provided holds. Problem can be re-written as follows.

| subject to | (44a) | |||

| (44b) | ||||

Let the Lagrange multipliers in equations (44a)–(44b) be , , and , respectively. It can be checked that the following primal-dual pair satisfies the Karush-Kuhn-Tucker conditions and hence is optimal for the convex program and its Lagrangian dual [47]. We omit the details for brevity.

The above profile of satisfies:

and hence is feasible and optimal for . Note that for all . Thus, for , we have

Maximizing the above relation over all we get . Therefore, is feasible and optimal for provided that .

D-C Proof of Proposition 4

First we show that is necessary for to be feasible. Consider any feasible solution of . For any and , we have since the power extracted from the storage device at node cannot exceed the corresponding storage capacity . Also, for any the power flow on the line joining buses 1 and satisfies for all . Combining the above relations and rearranging, we get Also for , and hence

| (46) |

Thus we get . If is feasible, then is also feasible and hence is necessary for both problems to be feasible. Now we prove that it is also sufficient. In particular, we show that for , is feasible. For convenience, define

| (47) |

Then . Rearranging (47), we get

| (48) |

Also, by hypothesis, we have

| (49) |

Combining equations (48) and (49), we have

| (50) |

For each , consider a single generator single load system as follows. Let the demand profile be , the capacity of the transmission line be and the total available storage budget be . For this system, the right hand side in (50) coincides with the definition of in (2). From Proposition 2, it follows that there is a feasible generation profile (say ) and a storage control policy that define a feasible flow over this single generator single load system and meet the demand. Now, for the star network, construct the generation profile

and operate the storage units at each node with the control policy defined above. Also, for all . It can be checked that this defines a feasible point for .

Next, we prove that . Let be optimal storage capacities for problem . Then the optimal storage capacities satisfy the following relations:

where the first one follows from (46) and the second one follows from the constraint on the total available storage capacities. Rearranging the above equations, we get and hence . This completes the proof of part (a).

To prove part (b) of Proposition 4, we start by showing that

| (51) |

Assume is feasible. For , we drop the variables , and consider the problems and over the variables , . The variables and are defined accordingly for all . We argue that the optimal points of lie in a bounded set. Note that and thus the control policies are bounded for all . Also, the cost function is convex and hence its sub-level sets [47] are bounded. From the above arguments and the power-balance at bus 1, the optimal policy is also bounded. Thus, the set of optimal solutions of is a bounded set. Furthermore, this set is also closed since the objective function and the constraints are continuous functions. As in the proof of Lemma 2, associate the function with every point in the set of optimal solutions of . This is a continuous function on a compact set and hence attains a minimum. Consider the optimum of where this minimum is attained. We prove (51) by showing that for all at this optimum.

Assume to the contrary, that is non-zero for some . Define

Also, define and notice that .

Case 1: : Construct the modified generation and charging/ discharging profiles that differ from only at and as follows:

where . As in the proof of Lemma 2, this is feasible for . Also, by Lemma 1:

The details are omitted for brevity. This feasible point satisfies

| (52) |

and hence defines an optimal point of with a strictly lower value of the function . This is a contradiction.

Case 2: : As above we construct modified storage control policies for all , keeping the generation profile constant to define an optimal point of with a lower value of to derive a contradiction.

Let the modified control policy at bus be as follows:

Instead, we distribute this to storage devices at , as follows:

for some and . To ensure feasibility of the modified profiles it suffices to check that the line flow constraints are satisfied at and . In other words, we show that there exists such that for all ,

Equivalently, we prove that

Recall that and are feasible for . Thus and . Also, at and . Thus, we have

where the last inequality follows from the hypothesis . The modified profiles satisfy as in (52). As argued above this is a contradiction and hence (51) holds.

For , is finite. Define Then, note that are also feasible for and for all . This completes the proof.

D-D Proof of Proposition 5

As in the statement of the proposition, assume demand profiles are fixed and satisfy with and positive constants. Also, fix storage budget .

First, we introduce some notation. Denote the parametrization of with respect to the line flow capacities as . For any instance of define the problem as the storage placement problem in a single generator single load network with line flow constraint , demand profile and storage budget . Denote the optimal cost of . Given an optimal solution of , it is straightforward to construct a feasible solution for with the same cost. Hence,

| (53) |

Now assume a specific realization of the line flow capacities, say , such that (36) is satisfied. Then, it can be checked from (35) that is feasible for all values of the storage budget. In what follows we construct an optimal solution of , which assigns zero storage at the generator. Define

and . Clearly, satisfies (36) and .

Let and . Consider the problems and . It can be checked from (2) in Proposition 2 that both problems are feasible. Moreover, Proposition 2 establishes that . But, from (53). Combining,

| (54) |

We start with an optimal solution of and construct a feasible solution with the same generation cost for . Then, we use (54) to deduce optimality of this solution. Our construction is such that zero storage is assigned at the generator, which establishes the desired result.

From Theorem 1, there exists an optimal solution to which assigns zero storage at the generator; let and be the optimal generation profile and optimal storage control policy of the load bus, respectively. From the feasibility constraints,

| (55) |

Using this, it can be checked that , and , defines a feasible solution for . Since the solution is also feasible for . In view of (54) this completes the proof.