Estimation of the lead-lag parameter from non-synchronous data

Abstract

We propose a simple continuous time model for modeling the lead-lag effect between two financial assets. A two-dimensional process reproduces a lead-lag effect if, for some time shift , the process is a semi-martingale with respect to a certain filtration. The value of the time shift is the lead-lag parameter. Depending on the underlying filtration, the standard no-arbitrage case is obtained for . We study the problem of estimating the unknown parameter , given randomly sampled non-synchronous data from and . By applying a certain contrast optimization based on a modified version of the Hayashi–Yoshida covariation estimator, we obtain a consistent estimator of the lead-lag parameter, together with an explicit rate of convergence governed by the sparsity of the sampling design.

doi:

10.3150/11-BEJ407keywords:

, and

1 Introduction

Market participants usually agree that certain pairs of assets share a “lead-lag effect,” in the sense that the lagger (or follower) price process tends to partially reproduce the oscillations of the leader (or driver) price process , with some temporal delay, or vice-versa. This property is usually referred to as the “lead-lag effect.” The lead-lag effect may have some importance in practice, when assessing the quality of risk management indicators, for instance, or, more generally, when considering statistical arbitrage strategies. Also, note that it can be measured at various temporal scales (daily, hourly or even at the level of seconds, for flow products traded on electronic markets).

The lead-lag effect is a concept of common practice that has some history in financial econometrics. In time series for instance, this notion can be linked to the concept of Granger causality, and we refer to Comte and Renault [4] for a general approach. From a phenomenological perspective, the lead-lag effect is supported by empirical evidence reported in [6, 3] and [18], together with [20] and the references therein. To our knowledge, however, only few mathematical results are available from the point of view of statistical estimation from discretely observed, continuous-time processes. The purpose of this paper is to – partly – fill in this gap. (Also, recently, Robert and Rosenbaum study in [23] the lead-lag effect by means of random matrices, in a mixed asymptotic framework, a setting which is relatively different than in the present paper.)

1.1 Motivation

(

-

1)]

-

(1)

Our primary goal is to provide a simple – yet relatively general – model for capturing the lead-lag effect in continuous time, readily compatible with stochastic calculus in financial modeling. Informally, if , with , is the time-shift operator, we say that the pair will produce a lead-lag effect as soon as is a (regular) semi-martingale with respect to an appropriate filtration, for some , called the lead-lag parameter. The usual no-arbitrage case is embedded into this framework for . More in Section 2 below.

-

(2)

At a similar level of importance, we aim at constructing a simple and efficient procedure for estimating the lead-lag parameter based on historical data. The underlying statistical model is generated by a – possibly random – sampling of both and . The sampling typically happens at irregularly and non-synchronous times for and . We construct, in the paper, an estimator of based on a modification of the Hayashi–Yoshida covariation estimator; see [11] and [13]. Our result is that the lead-lag parameter can be consistently estimated against a fairly general class of sampling schemes. Moreover, we explicit the rate of convergence of our procedure.

-

(3)

From a financial point of view, unless appropriate time shifts are operated, our model incapacitates our primary assets and to be a semi-martingale with respect to the same filtration. This is consistent, as far as modeling is concerned, but allows, in principle, for market imperfections such as statistical arbitrage if the lead-lag parameter is different from zero. More in Section 3.4 below. Addressing such a possibility is indeed the issue of the lead-lag effect, but we will content ourselves with detecting whether the lead-lag effect is present or not. The quantization of statistical arbitrage in terms of (and other parameters such as trading frequency, market friction, volatility and so on) lies beyond the scope of this paper.

-

(4)

From a statistical inference point of view, the statistician and the data provider are not necessarily the same agents, and this leads to technical difficulties linked to the sampling strategy. The data provider may choose the opening/closing for and , possibly traded on different markets, possibly on different time clocks. He or she may also sample points at certain trading times or events which are randomly chosen in a particular time window. This typically happens if daily data are considered. At a completely different level, if high-frequency data are concerned, trading times are genuinely random and non-synchronous. Our approach will simultaneously incorporate these different points of view.

1.2 Organization of the paper

In Section 2, we present our stochastic model for describing the lead-lag effect. We start with the simplest Bachelier model with no drift in Section 2.1. The issue boils down to defining properly the lead-lag effect between two correlated Brownian motions. In Section 2.2, a general lead-lag model is presented for two-dimensional process, for which the marginal processes are semi-martingales with locally bounded drift and continuous local martingale part, with properly defined diffusion coefficients.

We present our main result in Section 3. Section 3.1 gives a precise construction of the underlying statistical experiment with the corresponding assumptions on the observation sampling schemes. The estimation procedure is constructed in Section 3.2, via an appropriate contrast function based on the covariation between and when one asset is artificially shifted in time, the amount of this shift being the argument of the contrast function. Our estimator is robust to non-synchronous data and does not require any pre-processing contrary to the previous tick algorithm; see, for example, [27]. In Section 3.3, we state our main result in Theorem 1: we show that the lead-lag parameter between and can be consistently estimated from non-synchronous historical data over a fixed time horizon . The rate is governed by , the maximal distance between two data points. We show that the rate of convergence of our estimator is essentially and not , as one would expect from a regular estimation problem in diffusion processes; see, for example, [7]. This comes from the underlying structure of the statistical model, which is not regular, and which shares some analogy with change-point problems. As for our procedure, we investigate further its asymptotic properties in Proposition 1 when we confine ourselves to the simpler case where and are marginally Brownian motions that are observed at synchronous data points. In that case, we can exhibit a central limit theorem for our contrast function. A closer inspection of the limiting variance reveals the effect of the correlation between the two assets, which also plays a role in the accuracy of the estimation procedure. Finally, we show in Proposition 2 that a simple central limit theorem cannot hold for our estimator. We discuss this effect which is somewhat linked to the discretisation of our method.

Theorem 1 is good news, as far as practical implementation is concerned, and is further addressed in the discussion in Section 3.4, appended with numerical illustrations on simulated data in Section 5 and on real data in Section 6. The proofs are delayed until Section 4 and the Appendix contains auxiliary technical results.

2 The lead-lag model

2.1 The Bachelier model

A simple lead-lag Bachelier model with no drift between two Brownian motion components can be described as follows. On a filtered space , we consider a two-dimensional -Brownian motion such that for every and for some . Let be some terminal time, fixed throughout the paper. For , set

where and , are given constants. The corresponding Black–Scholes version of this model is readily obtained by exponentiating and . We introduce a lead-lag effect between and by operating a time shift: let represent the lead or lag time between and (and assume for simplicity that ). Put

| (1) |

Our lead-lag model is the two-dimensional process

Since we have with , a Brownian motion independent of , we obtain the simple and explicit representation

| (2) |

for . In this representation, the interpretation of the lead-lag parameter is transparent. Alternatively, if we start with a process having representation

| (3) |

as in (2), the lead-lag interpretation between and readily follows. Since , the sample path of anticipates on the path of by a time shift and to an amount – measured in normalized standard deviation – proportional to . In that case, we say that is the leader, and is the lagger. For the case , we intertwine the roles of and in the terminology.

Remark 0.

Note that, except in the case , the process is not an -martingale. However, each component is a martingale with respect to a different filtration: is an -martingale and is an -martingale, with , and .

2.2 Lead-lag between two semi-martingales

We generalize the lead-lag model (3) to semi-martingales with local martingale components that can be represented as Itô local martingales.

We need some notation. Let be some terminal time, and let represent the maximum temporal lead-lag allowed for the model, fixed throughout the paper. On a probability space , let be a filtration satisfying the usual conditions. We denote by the restriction of to the time interval .

Definition 1.

The two-dimensional process is a regular semi-martingale with lead-lag parameter if the following decomposition holds:

with the following properties:

-

•

The process is a continuous -local martingale, and the process is a continuous -local martingale.

-

•

The quadratic variations and are absolutely continuous w.r.t. the Lebesgue measure, and their Radon–Nikodym derivatives admit a locally bounded version.

-

•

The drifts and have finite variation over .

Definition 2.

The two-dimensional process is a regular semi-martingale with lead-lag parameter if the same properties as in Definition 1 hold, with and intertwined and replaced by .

Remark 0.

If is a regular semi-martingale with lead-lag parameter , then the process is a continuous -local martingale, with the (inverse of the) shift operator defined in (1).

Remark 0.

If is a regular semi-martingale with lead-lag parameter , then the process is a regular semi-martingale with lead-lag parameter .

3 Main result

3.1 The statistical model

We observe a two-dimensional price process at discrete times. The components and are observed over the time horizon . The following assumption is in force throughout:

Assumption A.

The process is a regular semi-martingale with lead-lag parameter .

The – possibly random – observation times are given by the following subdivisions of :

| (4) |

for and

| (5) |

for , with or not. For simplicity, we assume and . The sample points are either chosen by the statistician or dictated for practical convenience by the data provider. They are usually neither equispaced in time nor synchronous, and may depend on the values of and .

For some unknown , the process is a regular semi-martingale with lead-lag parameter , and we want to estimate based on the set of historical data

| (6) |

In order to describe precisely the property of the sampling scheme , we need some notation that we borrow from Hayashi and Yoshida [11]. The subdivision introduced in (4) is mapped into a family of intervals

| (7) |

Likewise, the subdivision defined in (5) is mapped into

We will systematically employ the notation (resp., ) for an element of (resp., ). We set

where (resp., ) denotes the length of the interval (resp., ), and is a parameter tending to infinity.

Remark 0.

One may think of being the number of data points extracted from the sampling, that is, . However, as we will see, only the (random) quantity will prove relevant for measuring the accuracy of estimation of the lead-lag parameter.

The assumptions on the sampling scheme is the following.

Assumption B.

-

[B1.]

-

B1.

There exists a deterministic sequence of positive numbers such that and as . Moreover

in probability as .

-

B2.

For all , the random times and are -stopping times if (resp., -stopping times if ). For all , the random times and are -stopping times if (resp., -stopping times if ).

-

B3.

There exists a finite grid such that and

-

[–]

-

–

For some , we have .

-

–

For some deterministic sequence , we have

and

-

Remark 0.

Since both and diverge at rate no less than , Assumption B3 implies that . With no loss of generality, we thus may (and will) assume that for all .

3.2 The estimation procedure

Preliminaries

Assume first that the data arrive at regular and synchronous time stamps over the time interval , with for simplicity. This means that we have observations

For every integer , we form the shifted time series

for every such that is an admissible time stamp111Possibly, we end up with an empty data set.. We can then construct the empirical covariation estimator

where the sum in expands over all relevant data points. Over the time interval , the number of elements used for the computation of should be of order as . Assume further for simplicity that the process is a lead-lag Bachelier model in the sense of Section 2.1, with lead-lag parameter , with an integer. On the one hand, for , we have the decomposition

with

Computing successively the fourth-order moment of the random variables and and applying Markov’s inequality and the Borel–Cantelli lemma, elementary computations show that and as almost surely, and we derive

On the other hand, for , we have

with

Thus, for fixed and , the process

is -martingale. Consequently, using the Burkholder–Davis–Gundy inequality, we easily obtain that

up to some constant . The same result holds for . We infer

up to a modification of . Using again Markov’s inequality and the Borel–Cantelli lemma, we finally obtain that

Therefore, provided , we can detect asymptotically the value that defines in the very special case , using defined as one maximizer in of the contrast sequence

Indeed, from the preceding computations, we have

| (8) |

This is the essence of our method. For an arbitrary , we can anticipate that an approximation of taking the form would add an extra error term of the order of the approximation, that is, , which is a first guess for an achievable rate of convergence.

In a general context of regular semi-martingales with lead-lag effect, sampled at random non-synchronous data points, we consider the Hayashi–Yoshida (later abbreviated by HY) covariation estimator and modify it with an appropriate time shift on one component. We maximize the resulting empirical covariation estimator with respect to the time shift over an appropriate grid.

Construction of the estimator

We need some notation. If is an interval, for , we define the shift interval . We write

for a (possibly random) interval, such that is an elementary predictable process. Also, for notational simplicity, we will often use the abbreviation

The shifted HY covariation contrast is defined as the function

Our estimator is obtained by maximizing the contrast over the finite grid constructed in Assumption B3 in Section 3.1 above. Eventually, is defined as a solution of

| (9) |

3.3 Convergence results

Since is a -local martingale, the quadratic variation process is well defined. We are now ready to assess our main result:

Theorem 1

Theorem 1 provides a rate of convergence for our estimator: the accuracy is nearly achievable, to within arbitrary accuracy. The next logical step is the availability of a central limit theorem. In the general case, this is not straightforward. We may, however, be more accurate if we further restrict ourselves to synchronous data in the Bachelier case; that is, we have data

| (10) |

over the time interval , and the process admits representation (3). We can then exhibit the asymptotic behavior of the contrast function , in a vicinity of size , of the lead-lag parameter. More precisely, we have the following proposition.

Proposition 1.

This representation is useful to understand the behavior of the contrast function : up to a scaling factor, is asymptotically proportional to the realization of the absolute value of Gaussian random variable , with

which has asymptotic value as soon as the mean dominates the standard deviation. We then have

and this is the case if ; otherwise, the pike degenerates toward , and the contrast behaves like a non-informative up to a multiplicative constant. It is noteworthy that Proposition 1 reveals the influence of the correlation in the estimation procedure. We see that if is too small, namely of order , the same kind of degeneracy phenomenon occurs: we do not have the divergence anymore, and both mean and standard deviation are of the same order; in that latter case, maximizing does not locate the true value .

The situation is a bit more involved when looking further for the next logical step, that is, a limit theorem for . The function is not smooth, even asymptotically: up to normalizing by , weakly converges to a Dirac mass at point , see Proposition 1. In that case, it becomes impossible, in general, to derive a simple central limit theorem for . Consider again the synchronous case over , and pick a regular grid with mesh such that goes to zero. In this situation, the contrast function is constant over all the points belonging to one given interval of the form , for . For definiteness and without loss of generality, we set

From Theorem 1, we know that goes to zero for any sequence such that ; therefore, we look for the behavior of the normalized error, with rate . However, the following negative result shows that this cannot happen.

Proposition 2.

Under the preceding assumptions, there is no random variable such that converges in distribution to .

The proof is given in the Appendix. Proposition 2 stems from the fact that part of the error of is given by the difference between and its approximation on the grid . This error is deterministic and cannot be controlled at the accuracy level ; see the proof in the Appendix. This phenomenon is somehow illustrated in the simulation in Section 5. Note that this negative result is not in contradiction to result (8) which states that almost surely, for large enough , . Indeed, result (8) is obtained considering a grid with mesh and a very special sequence of models where is of the form , with an integer. In the case where does not depend on , one can, of course, extend the almost sure result (8). However, what can be obtained is essentially that almost surely, for large enough , . Therefore, we almost surely identify the interval of size in which lies, but our method does not enable us to say something more accurate.

3.4 Discussion

Covariation estimation of non-synchronous data

The estimation of the covariation between two semi-martingales from discrete data from non-synchronous observation times has some history. It was first introduced by Hayashi and Yoshida [11] and subsequently studied in various related contexts by several authors. A comprehensive list of references include: Malliavin and Mancino [19], Hayashi and Yoshida [11, 13, 10, 12, 14], Hayashi and Kusuoka [9], Ubukata and Oya [26], Hoshikawa et al. [15] and Dalalyan and Yoshida [5].

About the rate of convergence

The condition of Assumption B1 is needed for technical reasons, in order to manage the fact that is random in general. In the case of regular sampling with , the nearly obtained rate is substantially better than the usual -rate of a regular parametric statistical model. This is due to the fact that the estimation of the lead-lag parameter is rather a change-point detection problem; see [16] for a general reference for the structure of parametric models. A more detailed analysis of the contrast function shows that its limit is not regular (not differentiable in the -variable), and this explains the presence of the rate . However, the optimality of our procedure is not granted, and the rate could presumably be improved in certain special situations.

Lead-lag effect and arbitrage

As stated, the lead-lag model for the two-dimensional process is not a semi-martingale, unless one component is appropriately shifted in time. This is not compatible in principle with the dominant theory of no-arbitrage models. This kind of modeling, however, seems to have some relevance in practice, and there is a natural way to reconcile both points of view.

We focus, for example, on the simplest Bachelier model of Section 2.1. We show in this paper that the lead-lag parameter can almost be identified in principle. Consequently, the knowledge of can then be incorporated into a trading strategy. If , we can obtain, in principle, some statistical arbitrage, in the sense that we can find, in the Bachelier model without drift, a self financing portfolio of assets and with initial value zero and whose expectation at time is positive.

This statistical arbitrage can be erased by introducing further trading constraints such as a maximal trading frequency and transaction cost (slippage, execution risk and so on). In this setting, we can no longer guarantee a statistical arbitrage. Moreover, we may certainly incorporate risk constraints in order to define an admissible strategy.

This outlines that although we perturb the semi-martingale classical approach, our lead-lag model is compatible in principle with non-statistical arbitrage constraints, under refined studies of risk profiles. We intend to set out, in detail, these possibilities in a forthcoming work.

Microstructure noise

Our model does not incorporate microstructure noise. This is reasonable if is thought of on a daily basis, say (if is of the order of a year or more say), but is inconsistent in a high-frequency setting where is of the order of one day. In that context, efficient semi-martingale prices of the assets are subject to the so-called microstructure noise; see, among others, Zhang et al. [28], Bandi and Russell [1], Barndorff-Nielsen et al. [2], Hansen and Lunde [8], Jacod et al. [17], Rosenbaum [25, 24]. In [21] and [22], Robert and Rosenbaum introduce a model (model with uncertainty zones) where the efficient semi-martingale prices of the assets can be estimated at some random times from the observed prices. In particular, it is proved that the usual Hayashi–Yoshida estimator is consistent in this microstructure noise context as soon as it is computed using the estimated values of the efficient prices. Using the same approach, that is, applying the lead-lag estimator to the estimated values of the efficient prices, one can presumably build an estimator which is robust to microstructure noise.

How to use high-frequency data in practice

Nevertheless, when high-frequency data are considered, we propose a simple pragmatic methodology that allows us to implement our lead-lag estimation procedure without requiring the relatively involved data pre-processing suggested in the previous paragraph. A preliminary inspection of the signature plot in trading time – the realized volatility computed with different subsampling values for the trading times – enables us to select a coarse subgrid among the trading times where microstructure noise effects can be neglected. Thanks to the non-synchronous character of high-frequency data, we can take advantage of this subsampling in trading time and obtain accurate estimation of the lead-lag parameter, at a scale that is significantly smaller than the average mesh size of the coarse grid itself. This would not be possible with a regular subsampling in calendar, time where the price at time would be defined as the last traded price before . This empirical approach is developed in the numerical illustration Section 6 on real data, in the particular case of measuring lead-lag between the future contract on Dax (FDAX) and the Euro-Bund future contract (FGBL) with same maturities.

Extension of the model

We consider this work as a first – and relatively simple – attempt for modeling the lead-lag effect in continuous time models. As a natural extension, it would presumably be more reasonable to consider more intricate correlations between assets in the model. For example, one could add a common factor in the two assets, without lead-lag effect, as suggested by the empirical study of Section 6. Through this, and in addition to the “lead-lagged correlation,” one would also obtain an instantaneous correlation between the assets. In order to estimate the lead-lag parameter in this context, one would presumably be required to consider local maxima of the contrast function we develop here. Such a development is again left out for future work.

4 Proof of Theorem 1

The proof of Theorem 1 is split in four parts. In the first three parts, we work under supplementary assumptions on the processes and the parameter space (Assumption ). We first show that if we compute the contrast function over points of the grid such that the order of magnitude of is bigger than , then the contrast function goes to zero (Proposition 3). Then we prove that, on the contrary, if the order of magnitude of is essentially smaller than , then the contrast function goes to the covariation between and (Proposition 4). We put these two results together in the third part which ends the proof of Theorem 1 under the supplementary assumptions. The proof under the initial assumptions is given in the last part.

4.1 Preliminaries

Supplementary assumptions

For technical convenience, we will first prove Theorem 1 when the sign of is known and when the components and are local martingales. Moreover, we introduce a localization tool. The quadratic variation processes of and admitting locally bounded derivatives, there exists a sequence of stopping times tending almost surely to such that the associated stopped processes are bounded by deterministic constants. Since Theorem 1 is a convergence in probability result, we can, without loss of generality, work under the supplementary assumption that the quadratic variation processes are bounded over . Therefore, we add-up the following restrictions:

Assumption .

We have Assumption A and:

-

[.]

-

.

There exists such that and .

-

.

The parameter set is restricted to . Consequently, by we mean here .

-

.

and .

We now introduce further notation. For and , let

and

We define and in the same way for and , respectively. Let and .

Remark 0.

We have the following interpretation of and : let denote the first time for which we know that an interval will have a width that is larger than . Then we keep only the and that are smaller than . If , we also consider among the observation times. Note that is not a true observation time in general. However, this will not be a problem since the set where is bigger than will be asymptotically negligible. Obviously and are -stopping times, and and are -stopping times.

Finally, for two intervals and , we define

4.2 The contrast function

We consider here the case where the order of magnitude of is bigger than . We first need to give a preliminary lemma that will ensure that the quantities we will use in the following are well defined.

Lemma 1.

Work under Assumption B2, under the slightly more general assumption that for all , the random variables and are -stopping times. Suppose that and . Then for any random variable measurable w.r.t. , the random variable is -measurable. In particular, is -measurable for any measurable function .

The proof of Lemma 1 is given in the Appendix. It is important to note that Lemma 1 implies that for and , the random variable

is -measurable. Indeed, is and implies . We now introduce a functional version of by considering the random process

We are now able to give the main proposition for the vanishing of the contrast function.

Proposition 3.

Let , and . We have

in probability.

Proof.

Assume first . Thanks to Lemma 1, we obtain a martingale representation of the process that takes the form

where the stochastic integral with respect to is taken for the filtration . As a result, the -quadratic variation of is given by

Using that the intervals are disjoint, we obtain

For a given interval , the union of the intervals that have a non-empty intersection with is an interval of width smaller than . Indeed, the maximum width of is and add to this (if it exists) the width of the interval such that , and the width of the interval such that , . Thus,

Consequently, we obtain for every and ,

For every , it follows from the Bürkholder–Davis–Gundy inequality that

where the symbol means inequality in order, up to constant that does not depend on . Pick . We derive

as , provided where is defined in Assumption B3, a choice that is obviously possible. The same argument holds for the case , but with an -integral representation in that latter case. The result follows. ∎

4.3 Stability of the HY estimator

We consider now the case where the order of magnitude of is essentially smaller than . We have the following proposition:

Proposition 4.

Work under Assumptions and B. For any sequence in such that and (remember that is defined in Assumption B3), we have

| (11) |

in probability as .

Proof.

The proof goes into several steps.

Step 1. In this step, we show that our contrast function can be regarded as the Hayashi–Yoshida estimator applied to and to the properly shifted values of plus a remainder term. If , then , and Proposition 4 asserts nothing but the consistency of the standard HY-estimator; see Hayashi and Yoshida [11] and Hayashi and Kusuoka [9]. Thus we may assume .

By symmetry, we only need to consider the case where

Set , and and

We then have

This can be written with

Remark that and are well defined since is defined on and . For every , is a -stopping time; therefore is a -stopping time, and a -stopping time as well. Thus is a variant of the HY-estimator: more precisely,

is the original HY-estimator, and we have in probability as . It follows that in probability as ; see [11] and [9].

Step 2. Before turning to the term , we give a technical lemma and explain a simplifying procedure. For an interval , set

Note that if we consider the interval at the extreme left end of the family , we have, for large enough ,

say, so we may assume that the set over which we take the supremum is non-empty.

Lemma 2.

Work under Assumption B2. The random variables are -stopping times.

The proof of this lemma is given in the Appendix. We now use a simplifying operation. For each , we merge all the such that . We call this procedure -reduction. The -reduction produces a new sequence of increasing random intervals extracted from the original sequence , which are -predictable by Lemma 2. More precisely, the end-points are -stopping times. It is important to remark that the -reduction implies that there are at most two points of type between any and . Moreover, since is a bilinear form of the increments of and , it is invariant under -reduction. Likewise for the maximum length . Thus, without loss of generality, we may assume that the are -reduced.

Step 3. We now turn to . We write

We have

We now index the intervals by and set if . Thus, the preceding line can be written

Then the Cauchy–Schwarz inequality gives that is smaller than

We easily get that

and we claim that (see next step)

| (12) |

Since , Proposition 4 readily follows.

Step 4. It remains to prove (12). Here we extend as for , and denote the extended one by the same “.” This extension is just for notational convenience, and causes no problem because, in what follows, we use the martingale property of only over the time interval . For ease of notation, we also stop writing the index for the intervals. We begin with the following remark. Take an interval , say and associated, say . Call the last observation point of type occurring before and the last observation point of type occurring before . Two situations are possible:

-

[-]

-

-

If there is no observation point of type between and , then, if it exists, is necessarily before . If it does not exist, we have .

-

-

If there are some observation points of type between and , then might also be between and . However, thanks to the -reduction, we know that is necessarily smaller than . Consequently, we have that is smaller than

where we used the following notation:

-

[-]

-

-

is the first interval such that exits to the right of .

-

-

denotes the interval of the form which is the nearest neighbor to on the left.

-

-

denotes the interval of the form which is the nearest neighbor to on the left.

-

-

is the first exit time to the right of among the .

-

-

is the first exit time to the right of among the .

-

-

For , if is not defined,

-

Hence we obtain

and so can be bound in order by

Thanks to the -reduction, we know that a given interval of the form can be associated to, at most, two values of type . Thus the second term of the preceding quantity is smaller than

where is an indexing of the intervals . Note that each is an -stopping time as it is the maximum among all

together with a strong predictability property; see Lemma 2 for a similar statement. So, using Bürkholder–Davis–Gundy inequality, (12) is proved and Proposition 4 follows. ∎

4.4 Completion of proof of Theorem 1 under Assumption

Write . By Assumption B3, we have

Therefore, there exists a sequence in such that and . For sufficiently large , we have . Moreover, on the event

implies . It follows that

Let . For large enough , the probability to have smaller than is larger than and, consequently,

This can be bounded in order by

and this last quantity converges to as by applying Proposition 3 and Proposition 4.

4.5 The case with drifts

We now give the proof of Theorem 1 under Assumptions , and B. The contrast admits the decomposition with

and

For a function defined on the interval , introduce the modulus of continuity

We have

and this term goes to in probability as .

Finally, the result is obtained in a similar way as in the no-drift case, using in place of .

4.6 The case where

5 A numerical illustration on simulated data

5.1 Synchronous data: Methodology

We first superficially analyze the performances of on a simulated lead-lag Bachelier model without drift. More specifically, we take a random process following the representation given in (2) in Section 2.1, having

In this simple model, we consider again synchronous, equispaced data with period and correlation parameters . In that very simple model, we construct with a grid with equidistant points with mesh222Note that, strictly speaking, such grid is not fine enough in order to fulfill our assumptions. However, the contrast function is constant over all the points of a given interval , , and its value is just the sum of the values obtained for the shifts and . . We consider the following variations:

-

1.

Mesh size: .

-

2.

Correlation value: .

| 0.096 | 0.099 | 0.1 | 0.102 | Other | |

|---|---|---|---|---|---|

| FG, | 0 | 0 | 300 | 0 | 0 |

| MG, | 0 | 300 | 0 | 0 | 0 |

| CG, | 1 | 0 | 0 | 299 | 0 |

| FG, | 0 | 0 | 300 | 0 | 0 |

| MG, | 0 | 299 | 0 | 1 | 0 |

| CG, | 13 | 0 | 0 | 280 | 7 |

| FG, | 0 | 0 | 300 | 0 | 0 |

| MG, | 0 | 152 | 0 | 11 | 137 |

| CG, | 10 | 0 | 0 | 66 | 124 |

5.2 Synchronous data: Estimation results and their analysis

We repeat 300 simulations of the experiment and compute the value of each time, the true value being , letting vary in . We adopt the following terminology:

-

1.

The fine grid estimation (abbreviated FG) with .

-

2.

The moderate grid estimation (abbreviated MG) with .

-

3.

The coarse grid estimation (abbreviated CG) with .

The estimation results are displayed in Table 1 below. With no surprise, for a given mesh , the difficulty of the estimation problem increases as decreases.

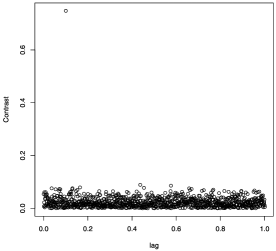

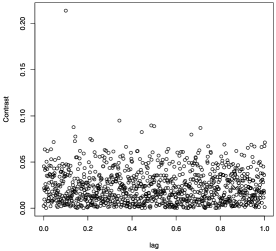

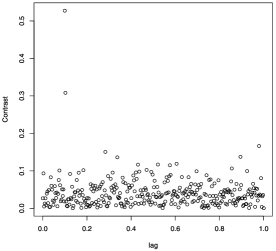

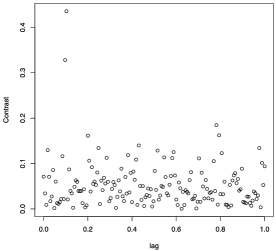

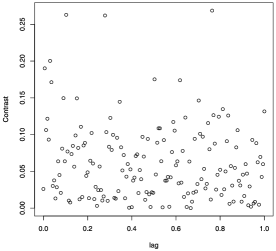

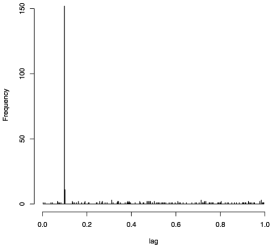

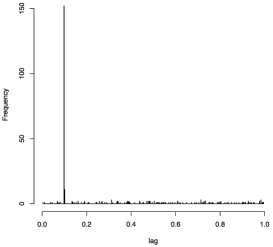

In the fine grid approximation case (FG) with mesh , the lead-lag parameter belongs to exactly. Therefore, the contrast is close to for all values , except perhaps for the exact value . This is illustrated in Figure 1 and Figure 2 below, where we display the values or . Note how more scattered are the values of for compared to . This is, of course, no surprise.

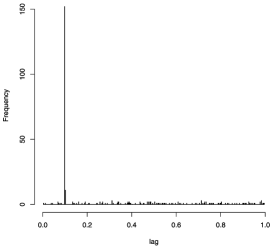

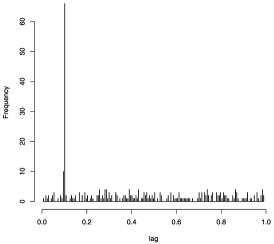

For the moderate grid (MG) and the coarse grid (CH) cases, the lead-lag parameter Hence, is close to for almost all values of except but two. When is small, the statistical error in the estimation of is such that is not well located anymore. The error in the estimation can then be substantial, but is nevertheless consistent with our convergence result. This is illustrated in Figures 3 to 8 below.

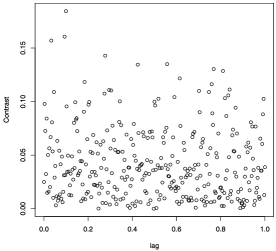

When decreases or when the mesh of the grid increases, the performance of deteriorates, as shown in Figures 7 and 8 below.

5.3 Non-synchronous data

We randomly pick 300 sampling times for over uniformly over a grid of mesh size . We randomly pick sampling times for likewise, and independently of the sampling for . The data generating process is the same as in Section 5.1. In Table 2, we display the estimation results for 300 simulations, in the fine gird case (FG) with and .

| 0.099 | 0.1 | 0.101 | 0.102 | 0.103 | 0.104 | 0.105 | |

|---|---|---|---|---|---|---|---|

| FG, | 16 | 106 | 107 | 46 | 19 | 4 | 2 |

6 A numerical illustration on real data

6.1 The data set

We study here the lead-lag relationship between the following two financial assets:

-

[-]

-

-

The future contract on the DAX index (FDAX for short), with maturity December 2010.

-

-

The Euro-Bund future contract (Bund for short), with maturity December 2010, which is an interest rate product based on a notional long-term debt instruments issued by the Federal Republic of Germany.

These two assets are electronically traded on the EUREX market, and are known to be highly liquid. Our data set has been provided by the company QuantHouse EUROPE/ASIA333http://www.quanthouse.com.. It consists in all the trades for 20 days of October 2010. Each trading day starts at 8.00 am CET and finishes at 22.00 CET, and the accuracy in the timestamp values is one millisecond.

6.2 Methodology: A one day analysis

In order to explain our methodology, we take the example of a representative day: 2010, October 13.

Microstructure noise

Since high-frequency data are concerned, we need to incorporate microstructure noise effects, at least at an empirical level. A classical way to study the intensity of the microstructure noise is to draw the signature plot (here in trading time). The signature plot is a function from to . To a given integer , it associates the sum of the squared increments of the traded price (the realized volatility) when only 1 trade out of is considered for computing the traded price. If the price were coming from a continuous-time semi-martingale, the signature plot should be approximately flat. In practice, it is decreasing, as shown by Figure 11.

According to Figure 11, for all our considered day, we subsample our data so that we keep one trade out of 20. On 2010, October 13, after subsampling, it remains 2018 trades for the Bund and 3037 trades for the FDAX.

Construction of the contrast function

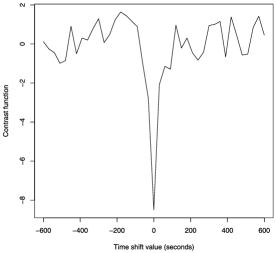

The second step is to compute our contrast function. Here the Bund plays the role of and the FDAX the role of . Therefore, if the estimated value is positive, it means that the Bund is the leader asset and the FDAX the lagger asset, and conversely. To have a first idea of the lead-lag value, we consider our contrast function for a time shift between minutes and minutes, on a grid with mesh 30 seconds. The result of this computation for October 2010, 13 is given in Figure 12.

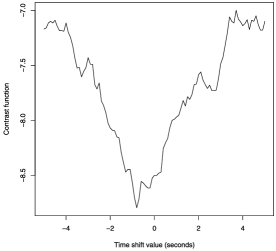

From Figure 12, we see that the lead-lag value is close to zero. Thus, we then compute the contrast function for a time shift between seconds and seconds, on a grid with mesh 0.1 second. The result of this computation for 2010, October 13 is given in Figure 13.

From Figure 13, we can conclude that on 2010, October 13, the FDAX seems to lead the Bund, with a small lead lag value of second.

6.3 Systematic results over a one-month period

We now give, in Figure 14, the results for all the days of October 2010.

| Number of trades for the | Number of trades for the | Lead-lag | |

|---|---|---|---|

| Day | bund (after subsampling) | FDAX (after subsampling) | (seconds) |

| 1 October 2010 | 2847 | 4215 | |

| 5 October 2010 | 2213 | 3302 | |

| 6 October 2010 | 2244 | 2678 | |

| 7 October 2010 | 1897 | 3121 | |

| 8 October 2010 | 2545 | 2852 | |

| 11 October 2010 | 1050 | 1497 | |

| 12 October 2010 | 2265 | 3018 | |

| 13 October 2010 | 2018 | 3037 | |

| 14 October 2010 | 2057 | 2625 | |

| 15 October 2010 | 2571 | 3269 | |

| 18 October 2010 | 1727 | 2326 | |

| 19 October 2010 | 2527 | 3162 | |

| 20 October 2010 | 2328 | 2554 | |

| 21 October 2010 | 2263 | 3128 | |

| 22 October 2010 | 1894 | 1784 | |

| 25 October 2010 | 1501 | 2065 | |

| 26 October 2010 | 2049 | 2462 | |

| 27 October 2010 | 2606 | 2864 | |

| 28 October 2010 | 1980 | 2632 | |

| 29 October 2010 | 2262 | 2346 |

The results of Figure 14 seem to indicate that, on average, the FDAX tends to lead the Bund. Indeed, the estimated lead-lag values are systematically negative. Of course these results have to be taken with care since the estimated values are relatively small (the order of one second); however, dealing with highly traded assets on electronic markets, the order of magnitude of the lead-lag values that we find are no surprise and are consistent with common knowledge. A possible interpretation – yet speculative at the exploratory level intended here – for the presence of such lead-lag effects is the difference between the tick sizes of the different assets. Indeed, the negative values could mean that the tick size of the FDAX can be considered smaller than those of the Bund.

Appendix

.1 Proof of Proposition 1

For notational clarity, for a given interval , we may sometimes write instead of when no confusion is possible. In the Bachelier case with lead-lag parameter , we work with the following explicit representation of the observation process:

| (13) |

where and are two independent Brownian motions. We have

with

We have

where is the usual hat function. Assuming further, with no loss of generality, that is an integer, we obtain the representation

We now assume without loss of generality that (the symmetric case being treated the same way). The sequence of random variables is stationary. Moreover, since the random variable involves increments of and over a domain included in because , it follows that and are independent as soon as . Moreover, we claim that

| (14) |

Therefore, by the central limit theorem, we have that

is approximately centred Gaussian, with variance

Computation of

To that end, we need to evaluate

and

since and are uncorrelated. Writing

taking square and expectation, we readily obtain that

Concerning II, since and are independent, we readily have

therefore, from , we finally infer

from which Proposition 1 follows. It remains to prove (14). By stationarity, this amounts to evaluate

To that end, we split each of the terms as follows:

Using the stochastic independence of each of these terms, multiplying and integrating, we easily obtain

.2 Proof of Proposition 2

Suppose that , in law, for some random random variable . For , we write the best approximation of by a point of the form , and , the best approximation of by a point smaller or equal to and of the form , . We have

The first term in the right-hand side of the equality is smaller than and so converges to zero. The second term can be written as

say. The sequence is a random sequence of integers, and is a deterministic sequence with values in which does not converge. Let be a subsequence such that with . Then converges in law to which implies that the support of is included in . Consider now such that with , . In the same way, we get that the support of is also included in , a contradiction.

.3 Proof of Lemma 1

Preliminary results

We first prove the following results.

Lemma 3.

Work under Assumption B2, under the slightly more general assumption that for all , the random variables and are -stopping times.

-

[(a)]

-

(a)

If , then for any -stopping time and , is an -stopping time. In particular, the random variables and are -stopping times.

-

(b)

For each , we have

and for each ,

-

(c)

Suppose that and . Then for any random variable measurable w.r.t. , the random variables and are -measurable.

Proof.

Proof of (a). For any -stopping time and ,

Proof of (b). Note first that under Assumption B2, the -stopping time is in particular an -stopping time; thus is a -field. Moreover, since and are -stopping times by definition, both and are -fields, and also the inclusion is trivial from . To obtain the equality, it suffices to observe that each of the conditions “” and “” is equivalent to the condition

for all . The second equality is proved in the same way.

Proof of (c). Since and are -stopping times by assumption, we have

the last inclusion following from (b). If , then

which implies Thus

We have that is measurable with respect to . Also is a stopping time with respect to by (a). Consequently, is -measurable, hence -measurable. Eventually, is -measurable. The other statement is proved the same way. ∎

Proof of Lemma 1 We have

Since , both and are -stopping times. Therefore, the second term on the right-hand side of the above equality is -measurable by (c) of Lemma 3.

Now we notice that if , then , therefore

The first factor on the right-hand side of the above equality is -measurable by (c) of Lemma 3, and the second factor is obviously -measurable. This completes the proof.

.4 Proof of Lemma 2

Let us fix . Let

We know that is an -stopping time by Assumption B2, and also that is an -stopping time due to . Let us show first that the s are -stopping times. Let . Let

and

It is obvious that since is an -stopping time and also

For the term , if , then . Otherwise, if , then

Eventually, we have ; hence is an -stopping time.

In conclusion, there exists at least one in . Therefore, we have , and this implies that is also an -stopping time.

Acknowledgements

This work was originated by discussions between M. Hoffmann and M. Rosenbaum with S. Pastukhov from the Electronic Trading Group research team of P. Guével at BNP-Paribas. We are grateful to M. Musiela, head of the Fixed Income research at BNP-Paribas, for his constant support and encouragements. We also thank E. Bacry, K. Al Dayri and Tuan Nguyen for inspiring discussions. Japan Science and Technology supported the theoretical studies in this work. N. Yoshida’s research was also supported by Grants-in-Aid for Scientific Research No. 19340021, the global COE program, “The research and training center for new development in mathematics” of Graduate School of Mathematical Sciences, University of Tokyo, JST Basic Research Programs PRESTO and by Cooperative Reserch Program of the Institue of Statistical Mathematics.

We are grateful to the comments and inputs of two referees and an associate editor, that help to improve a former version of this work.

References

- [1] {barticle}[mr] \bauthor\bsnmBandi, \bfnmF. M.\binitsF.M. &\bauthor\bsnmRussell, \bfnmJ. R.\binitsJ.R. (\byear2008). \btitleMicrostructure noise, realized variance, and optimal sampling. \bjournalRev. Econom. Stud. \bvolume75 \bpages339–369. \biddoi=10.1111/j.1467-937X.2008.00474.x, issn=0034-6527, mr=2398721 \bptokimsref \endbibitem

- [2] {barticle}[mr] \bauthor\bsnmBarndorff-Nielsen, \bfnmOle E.\binitsO.E., \bauthor\bsnmHansen, \bfnmPeter Reinhard\binitsP.R., \bauthor\bsnmLunde, \bfnmAsger\binitsA. &\bauthor\bsnmShephard, \bfnmNeil\binitsN. (\byear2008). \btitleDesigning realized kernels to measure the ex post variation of equity prices in the presence of noise. \bjournalEconometrica \bvolume76 \bpages1481–1536. \biddoi=10.3982/ECTA6495, issn=0012-9682, mr=2468558 \bptokimsref \endbibitem

- [3] {barticle}[auto:STB—2011/12/30—12:36:46] \bauthor\bsnmChiao, \bfnmC.\binitsC., \bauthor\bsnmHung, \bfnmK.\binitsK. &\bauthor\bsnmLee, \bfnmC. F.\binitsC.F. (\byear2004). \btitleThe price adjustment and lead-lag relations between stock returns: Microstructure evidence from the Taiwan stock market. \bjournalEmpirical Finance \bvolume11 \bpages709–731. \bptokimsref \endbibitem

- [4] {barticle}[auto:STB—2011/12/30—12:36:46] \bauthor\bsnmComte, \bfnmF.\binitsF. &\bauthor\bsnmRenaut, \bfnmE.\binitsE. (\byear1996). \btitleNon-causality in continuous time models. \bjournalEconometric Theory \bvolume12 \bpages215–256. \bptokimsref \endbibitem

- [5] {bmisc}[auto:STB—2011/12/30—12:36:46] \bauthor\bsnmDalalyan, \bfnmA.\binitsA. &\bauthor\bsnmYoshida, \bfnmN.\binitsN. (\byear2008). \bhowpublishedSecond-order asymptotic expansion for the covariance estimator of two asynchronously observed diffusion processes. Preprint. Available at arXiv:0804.0676. \bptokimsref \endbibitem

- [6] {barticle}[auto:STB—2011/12/30—12:36:46] \bauthor\bparticlede \bsnmJong, \bfnmF.\binitsF. &\bauthor\bsnmNijman, \bfnmT.\binitsT. (\byear1997). \btitleHigh frequency analysis of Lead-Lag relationships between financial markets. \bjournalJournal of Empirical Finance \bvolume4 \bpages259–277. \bptokimsref \endbibitem

- [7] {barticle}[mr] \bauthor\bsnmGenon-Catalot, \bfnmValentine\binitsV. &\bauthor\bsnmJacod, \bfnmJean\binitsJ. (\byear1993). \btitleOn the estimation of the diffusion coefficient for multi-dimensional diffusion processes. \bjournalAnn. Inst. Henri Poincaré Probab. Stat. \bvolume29 \bpages119–151. \bidissn=0246-0203, mr=1204521 \bptokimsref \endbibitem

- [8] {barticle}[mr] \bauthor\bsnmHansen, \bfnmPeter R.\binitsP.R. &\bauthor\bsnmLunde, \bfnmAsger\binitsA. (\byear2006). \btitleRealized variance and market microstructure noise. \bjournalJ. Bus. Econom. Statist. \bvolume24 \bpages127–161. \biddoi=10.1198/073500106000000071, issn=0735-0015, mr=2234447 \bptnotecheck related \bptokimsref \endbibitem

- [9] {barticle}[mr] \bauthor\bsnmHayashi, \bfnmTakaki\binitsT. &\bauthor\bsnmKusuoka, \bfnmShigeo\binitsS. (\byear2008). \btitleConsistent estimation of covariation under nonsynchronicity. \bjournalStat. Inference Stoch. Process. \bvolume11 \bpages93–106. \biddoi=10.1007/s11203-007-9009-9, issn=1387-0874, mr=2357555 \bptokimsref \endbibitem

- [10] {bmisc}[auto:STB—2011/12/30—12:36:46] \bauthor\bsnmHayashi, \bfnmT.\binitsT. &\bauthor\bsnmYoshida, \bfnmN.\binitsN. (\byear2005). \bhowpublishedEstimating correlations with missing observations in continuous diffusion models. Preprint. \bptokimsref \endbibitem

- [11] {barticle}[mr] \bauthor\bsnmHayashi, \bfnmTakaki\binitsT. &\bauthor\bsnmYoshida, \bfnmNakahiro\binitsN. (\byear2005). \btitleOn covariance estimation of non-synchronously observed diffusion processes. \bjournalBernoulli \bvolume11 \bpages359–379. \biddoi=10.3150/bj/1116340299, issn=1350-7265, mr=2132731 \bptokimsref \endbibitem

- [12] {bmisc}[auto:STB—2011/12/30—12:36:46] \bauthor\bsnmHayashi, \bfnmT.\binitsT. &\bauthor\bsnmYoshida, \bfnmN.\binitsN. (\byear2006). \bhowpublishedNonsynchronous covariance estimator and limit theorem. Research Memorandum 1020, Institute of Statistical Mathematics. \bptokimsref \endbibitem

- [13] {barticle}[mr] \bauthor\bsnmHayashi, \bfnmTakaki\binitsT. &\bauthor\bsnmYoshida, \bfnmNakahiro\binitsN. (\byear2008). \btitleAsymptotic normality of a covariance estimator for nonsynchronously observed diffusion processes. \bjournalAnn. Inst. Statist. Math. \bvolume60 \bpages367–406. \biddoi=10.1007/s10463-007-0138-0, issn=0020-3157, mr=2403524 \bptokimsref \endbibitem

- [14] {bmisc}[auto:STB—2011/12/30—12:36:46] \bauthor\bsnmHayashi, \bfnmT.\binitsT. &\bauthor\bsnmYoshida, \bfnmN.\binitsN. (\byear2008). \bhowpublishedNonsynchronous covariance estimator and limit theorem II. Research Memorandum 1067, Institute of Statistical Mathematics. \bptokimsref \endbibitem

- [15] {barticle}[mr] \bauthor\bsnmHoshikawa, \bfnmToshiya\binitsT., \bauthor\bsnmNagai, \bfnmKeiji\binitsK., \bauthor\bsnmKanatani, \bfnmTaro\binitsT. &\bauthor\bsnmNishiyama, \bfnmYoshihiko\binitsY. (\byear2008). \btitleNonparametric estimation methods of integrated multivariate volatilities. \bjournalEconometric Rev. \bvolume27 \bpages112–138. \biddoi=10.1080/07474930701853855, issn=0747-4938, mr=2424809 \bptokimsref \endbibitem

- [16] {bbook}[mr] \bauthor\bsnmIbragimov, \bfnmI. A.\binitsI.A. &\bauthor\bsnmHasminskiĭ, \bfnmR. Z.\binitsR.Z. (\byear1981). \btitleStatistical Estimation, Asymptotic Theory. \bseriesApplications of Mathematics \bvolume16. \baddressNew York: \bpublisherSpringer. \bnoteTranslated from the Russian by Samuel Kotz. \bidmr=0620321 \bptokimsref \endbibitem

- [17] {barticle}[mr] \bauthor\bsnmJacod, \bfnmJean\binitsJ., \bauthor\bsnmLi, \bfnmYingying\binitsY., \bauthor\bsnmMykland, \bfnmPer A.\binitsP.A., \bauthor\bsnmPodolskij, \bfnmMark\binitsM. &\bauthor\bsnmVetter, \bfnmMathias\binitsM. (\byear2009). \btitleMicrostructure noise in the continuous case: The pre-averaging approach. \bjournalStochastic Process. Appl. \bvolume119 \bpages2249–2276. \biddoi=10.1016/j.spa.2008.11.004, issn=0304-4149, mr=2531091 \bptokimsref \endbibitem

- [18] {barticle}[auto:STB—2011/12/30—12:36:46] \bauthor\bsnmKang, \bfnmJ.\binitsJ., \bauthor\bsnmLee, \bfnmC.\binitsC. &\bauthor\bsnmLee, \bfnmS.\binitsS. (\byear2006). \btitleEmpirical investigation of the lead-lag relations of returns and volatilities among the KOSPI200 spot, futures and options markets and their explanations. \bjournalJournal of Emerging Market Finance \bvolume5 \bpages235–261. \bptokimsref \endbibitem

- [19] {barticle}[mr] \bauthor\bsnmMalliavin, \bfnmPaul\binitsP. &\bauthor\bsnmMancino, \bfnmMaria Elvira\binitsM.E. (\byear2002). \btitleFourier series method for measurement of multivariate volatilities. \bjournalFinance Stoch. \bvolume6 \bpages49–61. \biddoi=10.1007/s780-002-8400-6, issn=0949-2984, mr=1885583 \bptokimsref \endbibitem

- [20] {bmisc}[auto:STB—2011/12/30—12:36:46] \bauthor\bsnmO’Connor, \bfnmM.\binitsM. (\byear1999). \bhowpublishedThe cross-sectional relationship between trading costs and lead/lag effects in stock & option markets. The Financial Review 34 95–117. \bptokimsref \endbibitem

- [21] {bmisc}[auto:STB—2011/12/30—12:36:46] \bauthor\bsnmRobert, \bfnmC. Y.\binitsC.Y. &\bauthor\bsnmRosenbaum, \bfnmM.\binitsM. (\byear2011). \bhowpublishedA new approach for the dynamics of ultra high frequency data: The model with uncertainty zones. Journal of Financial Econometrics 9 344–366. \bptokimsref \endbibitem

- [22] {bmisc}[auto:STB—2011/12/30—12:36:46] \bauthor\bsnmRobert, \bfnmC. Y.\binitsC.Y. &\bauthor\bsnmRosenbaum, \bfnmM.\binitsM. (\byear2012). \bhowpublishedVolatility and covariation estimation when microstructure noise and trading times are endogenous. Math. Finance 22 133–164. \bptokimsref \endbibitem

- [23] {barticle}[mr] \bauthor\bsnmRobert, \bfnmChristian Y.\binitsC.Y. &\bauthor\bsnmRosenbaum, \bfnmMathieu\binitsM. (\byear2010). \btitleOn the limiting spectral distribution of the covariance matrices of time-lagged processes. \bjournalJ. Multivariate Anal. \bvolume101 \bpages2434–2451. \biddoi=10.1016/j.jmva.2010.06.014, issn=0047-259X, mr=2719873 \bptokimsref \endbibitem

- [24] {barticle}[mr] \bauthor\bsnmRosenbaum, \bfnmMathieu\binitsM. (\byear2009). \btitleIntegrated volatility and round-off error. \bjournalBernoulli \bvolume15 \bpages687–720. \biddoi=10.3150/08-BEJ170, issn=1350-7265, mr=2555195 \bptokimsref \endbibitem

- [25] {barticle}[mr] \bauthor\bsnmRosenbaum, \bfnmMathieu\binitsM. (\byear2011). \btitleA new microstructure noise index. \bjournalQuant. Finance \bvolume11 \bpages883–899. \biddoi=10.1080/14697680903514352, issn=1469-7688, mr=2806970\bptnotecheck year \bptokimsref \endbibitem

- [26] {bmisc}[auto:STB—2011/12/30—12:36:46] \bauthor\bsnmUbukata, \bfnmM.\binitsM. &\bauthor\bsnmOya, \bfnmK.\binitsK. (\byear2008). \bhowpublishedA test for dependence and covariance estimator of market microstructure noise. Discussion Papers in Economics And Business, 07-03-Rev.2, 112–138. \bptokimsref \endbibitem

- [27] {barticle}[mr] \bauthor\bsnmZhang, \bfnmLan\binitsL. (\byear2011). \btitleEstimating covariation: Epps effect, microstructure noise. \bjournalJ. Econometrics \bvolume160 \bpages33–47. \biddoi=10.1016/j.jeconom.2010.03.012, issn=0304-4076, mr=2745865 \bptnotecheck year \bptokimsref \endbibitem

- [28] {barticle}[mr] \bauthor\bsnmZhang, \bfnmLan\binitsL., \bauthor\bsnmMykland, \bfnmPer A.\binitsP.A. &\bauthor\bsnmAït-Sahalia, \bfnmYacine\binitsY. (\byear2005). \btitleA tale of two time scales: Determining integrated volatility with noisy high-frequency data. \bjournalJ. Amer. Statist. Assoc. \bvolume100 \bpages1394–1411. \biddoi=10.1198/016214505000000169, issn=0162-1459, mr=2236450 \bptokimsref \endbibitem