Measuring stationarity in long-memory processes

Abstract

In this paper we consider the problem of measuring stationarity in locally stationary long-memory processes. We introduce an -distance between the spectral density of the locally stationary process and its best approximation under the assumption of stationarity. The distance is estimated by a numerical approximation of the integrated spectral periodogram and asymptotic normality of the resulting estimate is established. The results can be used to construct a simple test for the hypothesis of stationarity in locally stationary long-range dependent processes. We also propose a bootstrap procedure to improve the approximation of the nominal level and prove its consistency. Throughout the paper, we will work with Riemann sums of a squared periodogram instead of integrals (as it is usually done in the literature) and as a by-product of independent interest it is demonstrated that the two approaches behave differently in the limit.

AMS subject classification: 62M10, 62M15, 62G10

Keywords and phrases: spectral density, long-memory, non-stationary processes, goodness-of-fit tests, empirical spectral measure, integrated periodogram, locally stationary process, bootstrap

1 Introduction

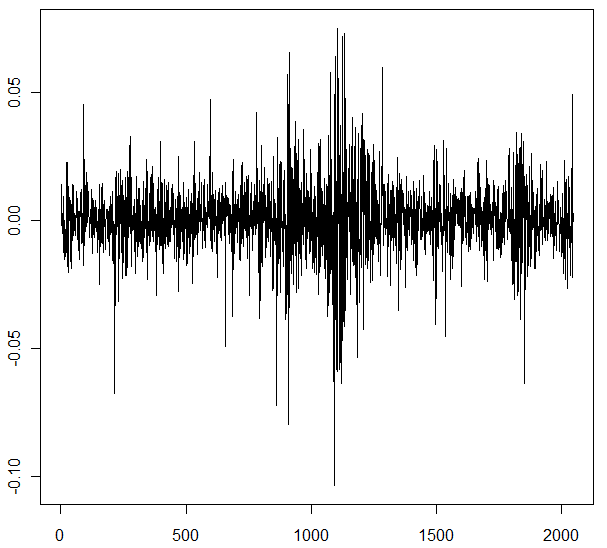

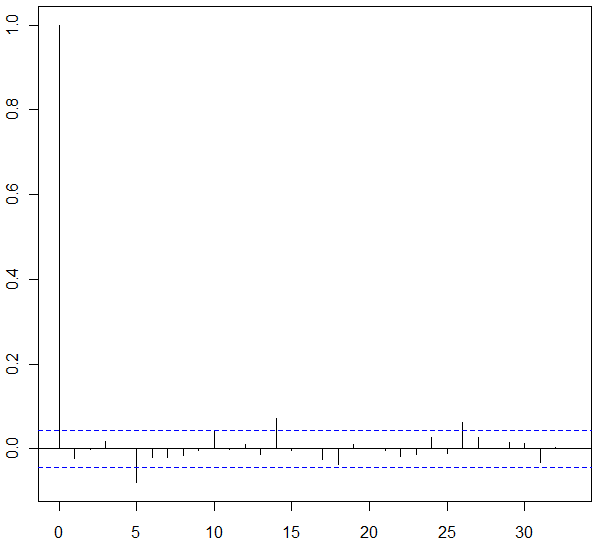

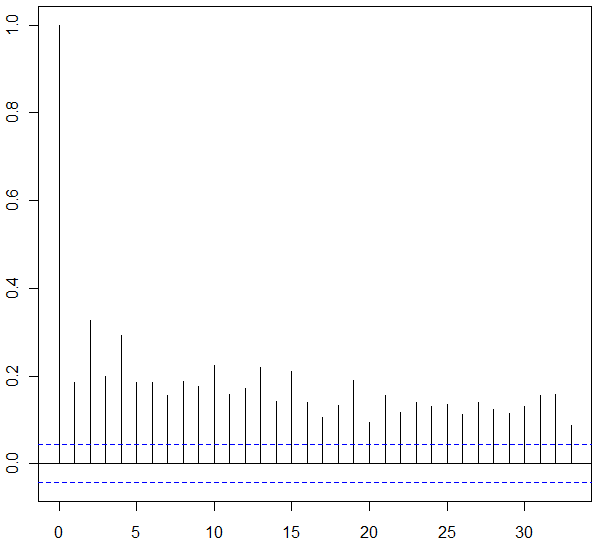

The assumption of (second-order) stationarity is quite common in the analysis of time series data like wind speeds, computer network traffic or stock returns. This condition allows for a well developed statistical analysis, and there exist numerous books and articles dealing with parameter estimation or forecasting techniques. However, under the assumption of stationarity many real world phenomena can only be described by complicated and less intuitive models. A typical example can be found in the left panel of Figure 1 which shows log-returns of the IBM stock between June 9th 2004 and July 24th 2012. We observe that the autocovariance function (ACF) of the log-returns is converging to zero very “fast” as , while this is not the case for the ACF of the squared returns [see the middle and right panel in Figure 1]. The latter effect serves as the usual motivation to employ stationary long-memory models in the analysis of stock volatilities [see Breidt et al., (1998)]. This means that stationary processes satisfy

| (1.1) |

for some , which is called the long-memory parameter. Examples which fit into this framework are the well-known FARIMA()-models introduced by Granger and Joyeux, (1980) and Hosking, (1981). However, these kinds of processes are not very intuitive and it was suggested by several authors that one should use simple but non-stationary “short-memory” models instead [see for example Mikosch and Starica, (2004), Starica and Granger, (2005), Fryzlewicz et al., (2006) or Chen et al., (2010) among others]. Therefore an important question of interest in this context is, if the data should be analyzed by a stationary long-range dependent model or by a non-stationary “short-memory” model.

In the present paper we propose a measure of stationarity in long-range dependent locally stationary processes, which is used for the construction of a consistent test for the hypothesis of stationarity.

Since the assumption of stationarity is crucial in the application of various statistical tools, there exist several procedures to validate this condition in the context of short-memory processes. A first test for stationarity in locally stationary processes [as introduced by Dahlhaus, (1997)] was proposed by von Sachs and Neumann, (2000) and is based on the estimation of wavelet coefficients by a localized version of the periodogram. Paparoditis, (2009, 2010) suggested an -distance between the estimated spectral densities under the assumptions of stationarity and of local stationarity, and Dwivedi and Subba Rao, (2010) developed a Portmanteau-type test statistic to detect deviations from stationarity. Besides the choice of a window width for the localized periodogram, which is inherent in essentially any statistical inference for locally stationary processes, all these methods require the choice of at least one additional smoothing parameter, such as the order of the wavelet expansion, a bandwidth for the estimation of the spectral density or the order in a Portmanteau-type test. Dette et al., 2011a developed tests for stationarity in the framework of locally stationary processes which only require the choice of one regularization parameter, namely the window length for the localized periodogram in the estimation procedure. These authors considered the -distance

| (1.2) |

between the time varying spectral density and its approximation through a spectral density corresponding to a stationary process. It is easy to see that the process is stationary (i.e. the time varying spectral density does not depend on ) if and only if , and can be considered as a measure of deviation from stationarity in the frequency domain. This quantity corresponds to the measure used in Paparoditis, (2009), but unlike to this author, Dette et al., 2011a estimated directly via Riemann sums of the (squared) local periodogram instead of a smoothed local periodogram and thus avoided the choice of a smoothing parameter. Preuß et al., (2012) proposed an alternative measure for deviations from stationarity which is based on the Kolmogorov-Smirnov distance

| (1.3) |

[see also Dahlhaus, (2009)]. Both approaches have their pros and cons. In particular tests based on the distance (1.3) are -consistent (here denotes the sample size). On the other hand it is well known that - although such tests are consistent against alternatives converging to the null hypothesis at a parametric rate - Kolmogorov-type and related tests greatly weigh down contributions from high frequency components [see Ghosh and Huang, (1991), Eubank and LaRiccia, (1992) or Fan, (1996)]. Moreover, the limiting distribution of Kolmogorov-Smirnov-type test statistics is usually not known. In principle this problem can be solved by bootstrap methods. However in many cases this yields to a loss of power. On the other hand, tests based on the -approach can often use critical values from the standard normal distribution.

As all procedures which have been suggested so far for discriminating between stationarity and non-stationarity, the tests proposed by Dette et al., 2011a and Preuß et al., (2012) are only applicable to short-memory processes, and the development of a corresponding methodology in the context of long-range dependence is missing. In fact, although stationary long-memory models are employed numerously in practice, there do not exist many tests for the hypothesis of stationarity which include these processes. Berkes et al., (2006), Sibbertsen and Kruse, (2009) and Dehling et al., (2011) consider CUSUM and Wilcoxon type tests to discriminate between long-range dependence and one change in mean. However a change with respect to the mean is of course only the simplest possible deviation from stationarity and there is particular interest in measuring deviations in the dependency structure over time as well.

Recently, Preuß and Vetter, (2012) developed a test for stationarity which includes the long-range dependent case and is based on the distance (1.3). As mentioned in the previous paragraph there exist several situations where this approach is not the best and for this reason we consider in this paper an alternative test which is based on the measure defined in (1.2). For this purpose, we estimate the integrals in the distance in (1.2) by Riemann sums where the unknown spectral densities are replaced by periodograms. For the resulting statistic we will show that an appropriately standardized statistic converges to a standard normal distribution if the (possibly time varying) long-memory parameter is smaller than . These results are used to develop a bootstrap procedure for the approximation of the limit distribution and to prove its consistency in the general case.

Although that the proof of asymptotic normality seems to be more of theoretical nature, because the bootstrap procedure derived in the second part of the paper can in principle also be applied in the case , these results are of interest from several perspectives. Firstly, several arguments used in the proof of asymptotic normality are also required in the proof of consistency of the bootstrap procedure and easier illustrated in the unconditional case. Secondly, and most important, the estimate of is based on estimates of the integrated and integrated squared spectral density and , respectively. For this purpose we use Riemann sums of the squared periodogram instead of not computable integrals as it is usually done in the literature [see Taniguchi, (1980), Fox and Taqqu, (1987) and Palma and Olea, (2010) among others]. Although one might expect that both estimators exhibit a similar behavior with respect to weak convergence, it is demonstrated in Section 3 that this is not the case in the present context. A similar observation was also made by Deo and Chen, (2000) in the case of short-memory stationary processes. To the best of our knowledge, even in the (much simpler) stationary case, Riemann sums of a squared periodogram have not been considered in the literature for the long-range dependent case.

The remaining part of this paper is organized as follows: In Section , we introduce the necessary notation and define an empirical measure of stationarity. In Section 3, we prove that an appropriately standardized version of this measure converges weakly to a standard normal distribution if the time varying long-memory parameter is smaller than . In Section , we present a bootstrap procedure to approximate the distribution of and prove its consistency. The finite sample properties are investigated in Section . Finally, we defer all technical details to appendices in Section and .

2 Measuring stationarity in locally stationary long-memory processes

In order to obtain a measure of stationarity including the long-range dependent case, we require a set-up which is flexible enough to cover stationary long-memory processes and a reasonable time-varying extension of it as well. For this reason, we consider the following theoretical framework of a locally stationary long-memory process [similar approaches can be found in Beran, (2009), Palma and Olea, (2010) and Roueff and von Sachs, (2011)].

Assumption 2.1.

Let denote a sequence of stochastic processes which have a MA() representation of the form

| (2.1) |

such that

| (2.2) |

where are independent and standard normal distributed random variables. We further assume the following conditions.

-

1)

There exist twice continuously differentiable functions () such that

(2.3) and

(2.4) holds uniformly in as , where are twice differentiable functions, and are constants and .

-

2)

The time varying spectral density

(2.5) is twice continuously differentiable on . Moreover, and all its partial derivatives up to order two are continuous on .

-

3)

There exists a constant , which is independent of and , such that for

(2.6) (2.7) In addition, we assume

(2.8) (2.9)

For the sake of a transparent notation, we will use as a universal constant throughout this paper. Note that the process is stationary if for all . Condition (2.2) ensures that the infinite sum in (2.1) exists in the sense, and (2.3) means that the process can be approximated by a stationary model on a small time interval. It is also worthwhile to mention that the assumption of Gaussianity is only imposed here to simplify technical arguments [since they are quite involved even in this case]; see Remark 3.5 for more details. Next, we consider the process

| (2.10) |

in order to visualize some properties of a locally stationary long-memory process. Firstly, is stationary for every fixed and analogously to the stationary case, the condition (2.4) implies the existence of bounded functions such that

and

| (2.11) |

[see Palma and Olea, (2010)]. Consequently, the autocovariance function is not absolutely summable and the time varying spectral density has a pole at for any .

As an example which fits in this theoretical set-up we consider the time varying FARIMA() model defined by the equation

| (2.12) |

where denotes the backshift operator,

for given functions , and is twice continuously differentiable with . It is shown in Preuß and Vetter, (2012) that under certain regularity conditions on the functions , , these equations have a locally stationary solution in the sense of Assumption 2.1. If the functions , and do not depend on , (2.12) corresponds to the common FARIMA() equation [see for example Palma, (2007) for conditions for the existence of a solution], which is included in our theoretical framework.

For the construction of an estimate of the quantity (1.2) we note that

| (2.13) |

where

| (2.14) | |||||

| (2.15) |

Consequently, it follows from that the distance is only well defined if . We assume without loss of generality that the sample size can be decomposed into blocks with length (i.e. ) where and are positive integers and is even. A rough estimator for the time varying spectral density is then given by the local periodogram at the rescaled time point which is defined by

where for [see Dahlhaus, (1997)]. This is the usual periodogram computed from the observations , and it can be shown that it is asymptotically unbiased for the time-varying spectral density if and . However, is not consistent just as the usual periodogram. In addition, is an unbiased (but not consistent) estimate of the quantity instead of .

We now construct empirical versions of (2.14) and (2.15) by replacing the integrals through appropriate Riemann-sums and substitute and by and , respectively. For this purpose, we define the rescaled mid-points of the blocks

and consider the statistics

| (2.16) | |||||

| (2.17) |

where denote the usual Fourier frequencies. The empirical measure of stationarity (1.2) is finally given by

| (2.18) |

We would like to point out here that it is far from obvious that is a consistent estimator of . In general it is not true that an integrated function of the periodogram converges to the corresponding integrated function of the spectral density. This - at a first glance - is a counterintuitive property of the integrated periodogram and was already observed by Taniguchi, (1980) in the context of stationary short-memory processes. These problems are also visible here as well as we require a multiple of to obtain an asymptotically unbiased estimator for . In the following section we will prove consistency of and study its weak convergence.

3 Consistency and weak convergence

Throughout this paper, the symbols and denote convergence in probability and weak convergence, respectively. In order to specify the bias of and we define

and obtain the following results.

Theorem 3.1.

Suppose Assumption 2.1 holds with and that the conditions

| (3.1) |

are satisfied. Then and in particular

as .

Theorem 3.2.

Suppose Assumption 2.1 holds with and that the conditions

| (3.2) |

are satisfied. Then as we have

where the covariance matrix and the constant are given by

| (3.3) | |||||

| (3.4) |

respectively, and the vector is of order . In particular, this term vanishes if the functions are independent of for all [i.e. the spectral density of the underlying process is independent of ].

A similar result for the short-memory situation has been derived by Dette et al., 2011a . In contrast to their result, there appears an additional bias term in Theorem 3.2. This term is negligible under the additional condition which holds under the stronger restriction due to (3.2). On the other hand, under the null hypothesis of a time independent spectral density

| (3.5) |

we have that (this follows from the proof of Theorem 3.2 in the Appendix). Since the covariance matrix (3.3) contains the integrated fourth power of the spectral density, we obtain from (2.11) that Theorem 3.2 is not valid whenever . Writing , a straightforward application of the Delta-method yields the following result.

Corollary 3.3.

Under the null hypothesis (3.5) we have and the asymptotic variance in (3.3) reduces to . The asymptotic bias can easily be estimated by the statistic and we infer from Theorem 3.2

Thus Slutzky’s Lemma together with (3.6) yields

| (3.8) |

under the null hypothesis. To construct an asymptotic level -test for stationarity, it therefore remains to estimate the variance in (3.8), and an estimator for this quantity is given by with

The consistency of this estimator follows from the next theorem.

Theorem 3.4.

If the assumptions of Theorem 3.2 are satisfied, we have

and therefore an asymptotic level -test is obtained by rejecting the null hypothesis (3.5) whenever

| (3.10) |

where denotes the -quantile of the standard normal distribution. It follows from Theorem 3.2 that this test is consistent, because the left hand side of (3.10) converges to infinity, whenever there exists a such that the function is not constant.

Remark 3.5.

If the innovation process in (2.1) is not Gaussian, it can be shown that Corollary 3.3 is still valid where the asymptotic variance in (3.3) has to be replaced by

and and denote the second and fourth cumulants of the innovation process, respectively. In particular, under the null hypothesis of stationarity, it follows that and hence no adjustments in the asymptotic level -test in (3.10) are necessary to address non normal distributed innovations.

Remark 3.6.

We note that for locally stationary long-range dependent models the asymptotic variances of the statistics

and of , defined in (2.16), are different. In fact it follows by similar arguments as given in the appendix that

while

by Theorem 3.2. Moreover, similar arguments as given in the proof of this statement show that even in the stationary case the asymptotic variance of the statistic and its discretized version are not the same (here denotes the usual periodogram and are the Fourier frequencies). Deo and Chen, (2000) observed the same effect in the context of stationary short-memory processes.

4 Critical values by resampling

We now consider the more general set-up with as specified in Assumption 2.1. We will show that in this case a bootstrap procedure can be used to approximate the distribution of under the null hypothesis (3.5). We employ the FARI() bootstrap which was recently introduced by Preuß and Vetter, (2012) and fits an FARIMA()-model to the data, where converges to infinity with increasing sample size . To prove consistency of this procedure, we require the following technical assumptions.

Assumption 4.1.

For the stationary process with strictly positive spectral density , there exists a constant such that the process

| (4.1) |

has an AR()-representation of the form

| (4.2) |

where denotes a Gaussian White Noise process with variance and the coefficients in the representation satisfy

| (4.3) | |||||

| for | (4.4) |

Note that under the null hypothesis of a time independent spectral density, it follows that for all , but under the alternative we usually have . The FARI() bootstrap incorporates the following steps: First we choose a to construct an estimator, say , of the long-range dependence parameter in model (4.1). Secondly we calculate an estimator of

| (4.5) |

by fitting an AR()-model to the data. In order to describe the main idea of our procedure in more detail, we introduce the “true” approximating process by

| (4.6) |

where the parameters are defined in (4.5) and is a Gaussian White Noise process with mean zero and variance . If the process approximates and therefore is “close” to the stationary process whose spectral density is given by . Under the null hypothesis of stationarity, this function coincides with the spectral density of . Hence, observing the data , the FARI() bootstrap precisely works as follows:

-

1)

Choose and calculate as the minimizer of

where

is the usual periodogram, and

is the spectral density of a stationary FARIMA()-model. Note that the estimator is the classical Whittle estimator of a stationary process [see Whittle, (1951)].

-

2)

Calculate for and simulate a pseudo-series according to the model

where denotes an independent sequence of standard normal distributed random variables.

-

3)

Create the pseudo-series from the equation

(4.7) and compute in the same way as where the original observations are replaced by the bootstrap replicates .

Our main theorem in this section describes the theoretical properties of this procedure.

Theorem 4.2.

Assume that the null hypothesis (3.5) holds and let Assumption 2.1 and 4.1 be fulfilled. Furthermore, suppose that the conditions

| (4.8) |

are satisfied for some , and assume for the growth rate (rate of convergence) of the following:

-

i)

There exist sequences such that

(4.9) (4.10) -

ii)

The condition

(4.11) is fulfilled uniformly with respect to , where denotes the estimator used in step 1) of the bootstrap procedure and are the corresponding “true” parameters.

Then there exist random variables and such that

The estimate in (d) also holds if the null hypothesis (3.5) is not satisfied.

Note that conditions like (4.9)-(4.11) are standard in the context of parametric bootstraps [see for example Berg et al., (2010) or Kreiß et al., (2011)] and a detailed discussion of them is given in Preuß and Vetter, (2012). We now obtain an asymptotic level -test based on as follows: Calculate B bootstrap replicates , denote by the resulting order statistic and reject the null hypothesis whenever

| (4.12) |

Theorem 4.2 and the argumentation in Paparoditis, (2010) indicate that this procedure is valid for obtaining an asymptotic level -test. In order to prove this more formally, we follow Bickel and Freedman, (1981) by considering the Mallow metric between two distributions and , where the infimum is taken over all pairs of random variables with marginal distributions and . Theorem 4.2 then yields the following result which states that the test (4.12) has, in fact, asymptotic level .

Theorem 4.3.

5 Finite sample properties

In this section we examine the finite sample properties of the proposed decision rule (4.12). An important problem is the choice of the window length for the calculation of the local periodogram and the choice of the AR parameter in the bootstrap procedure. Throughout this section we choose as the minimizer of the AIC criterion [see Akaike, (1973)], which is defined by

in the context of stationary processes due to Whittle, (1951) [here is the spectral density of the fitted stationary FARIMA() process and is the usual stationary periodogram]. We therefore restrict ourselves to an analysis of the sensitivity with respect to in the following, and it will turn out that the test (4.12) using the FARI() bootstrap exhibits a remarkable robustness with respect to the choice of . All reported results of this section are based on simulation runs and bootstrap replications.

5.1 Size of the test

In order to investigate the approximation of the nominal level we simulate data from the

FARIMA() model

| (5.1) |

and the FARIMA() process

| (5.2) |

for different values of and where the random variables are independent standard normal distributed. The rejection probabilities for the bootstrap test (4.12) are displayed in Table 2–4 where . We observe a very precise approximation of the nominal level in nearly all cases which is rather robust with respect to different choices of the parameter and .

In order to study the power of the test we consider the following alternatives

| (5.3) | ||||

| (5.4) | ||||

| (5.5) |

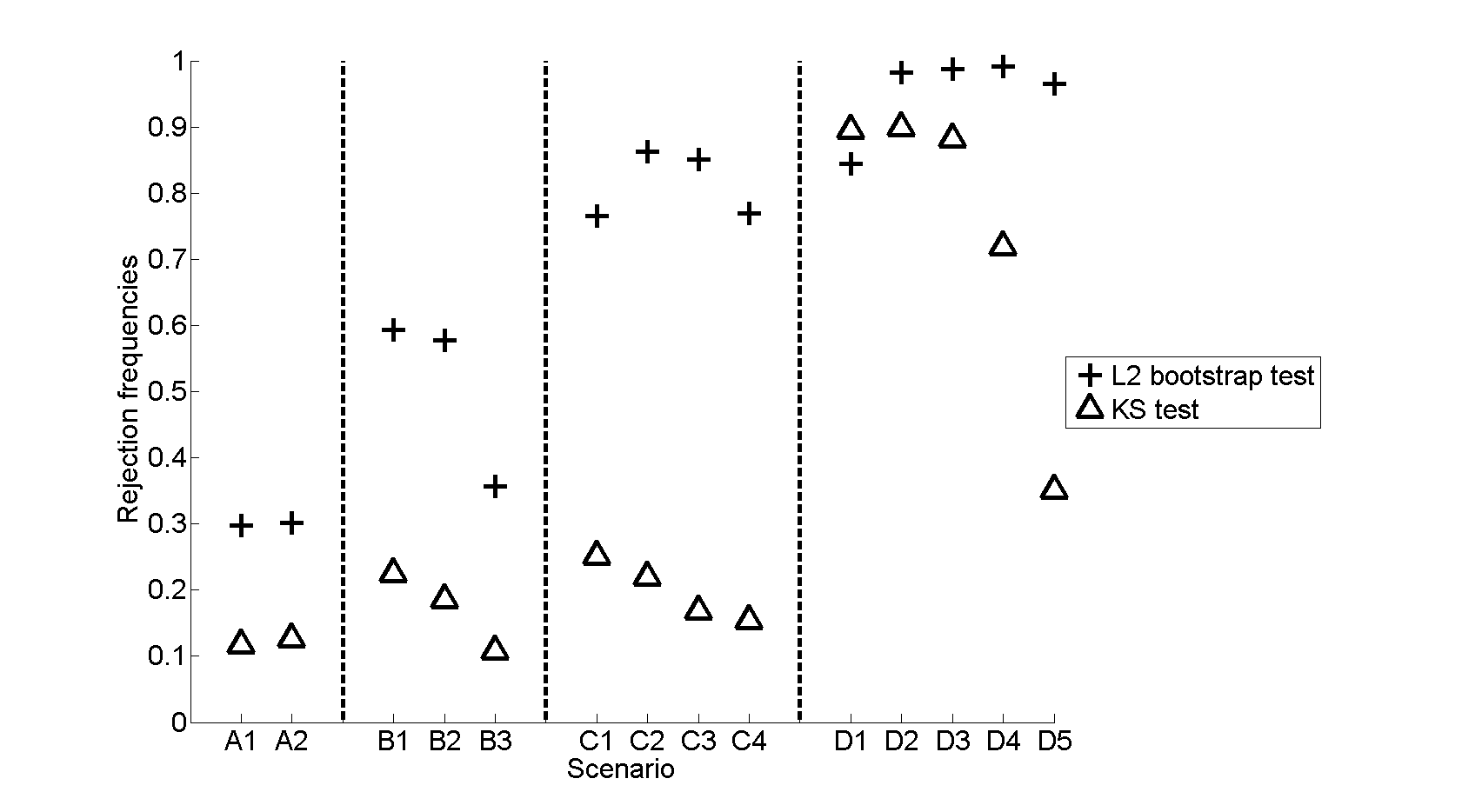

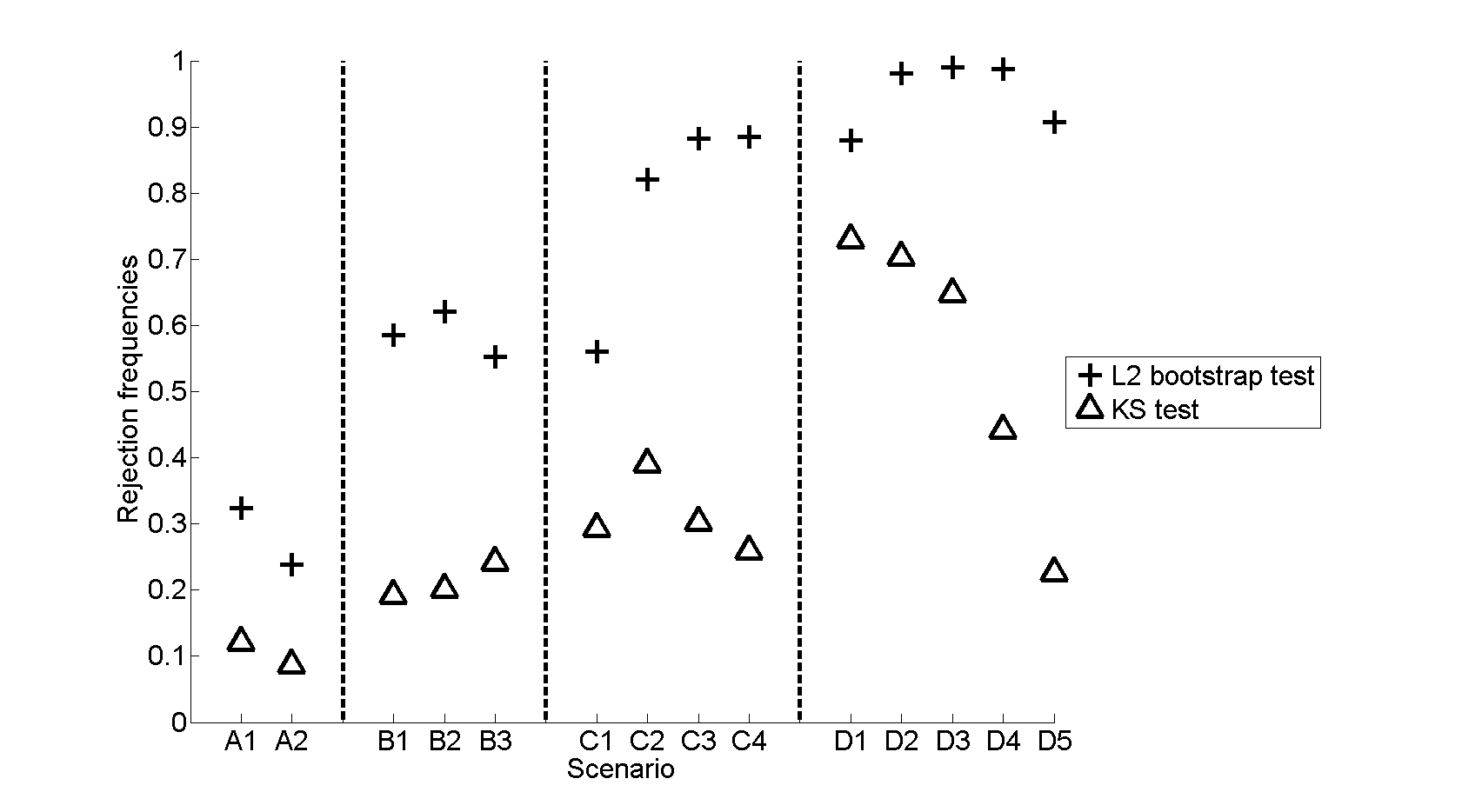

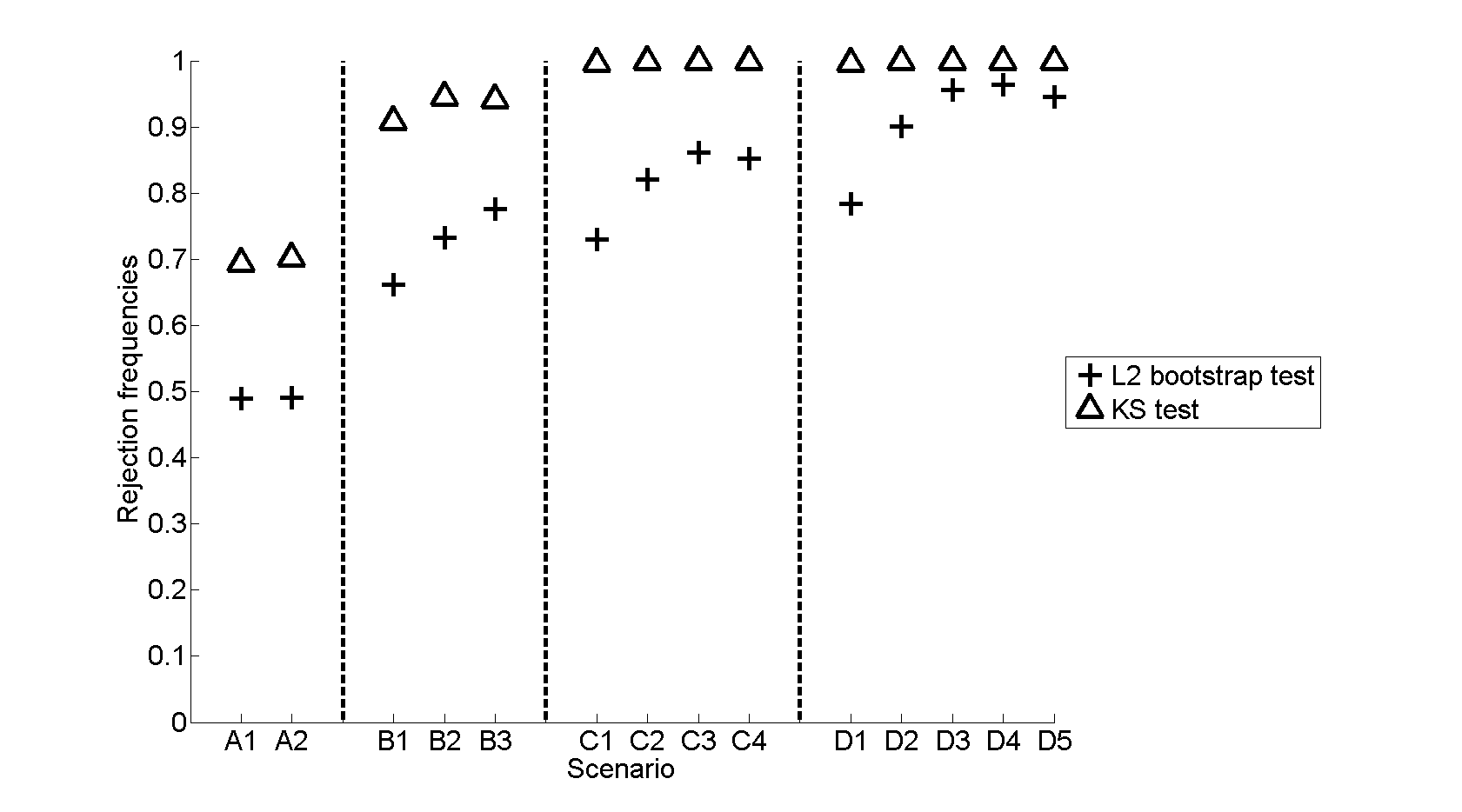

where . These kinds of alternatives were investigated by several authors in the context of locally stationary short-memory processes [see Paparoditis, (2010) and Dahlhaus, (1997)]. The rejection frequencies for the bootstrap test (4.12) are depicted in Figure 3–4 for different combinations of and . Additionally, the results for the Kolmogorov-Smirnov approach of Preuß and Vetter, (2012) are presented. We observe that the new procedure clearly outperforms the test of Preuß and Vetter, (2012) for the models (5.3) and (5.4) while the Kolmogorov-Smirnov test works better for the process (5.5). In addition, we observe that the new decision rule is less sensitive with respect to different choices of than the test based on the Kolmogorov-Smirnov distance.

| A1 | 128 | 16 | 8 | .126 | .182 | .072 | .123 | .036 | .074 | .073 | .126 | .084 | .147 |

| A2 | 128 | 8 | 16 | .140 | .200 | .085 | .132 | .041 | .090 | .073 | .128 | .084 | .118 |

| B1 | 256 | 32 | 8 | .065 | .135 | .064 | .119 | .042 | .088 | .062 | .113 | .075 | .147 |

| B2 | 256 | 16 | 16 | .080 | .132 | .056 | .108 | .040 | .082 | .051 | .109 | .062 | .109 |

| B3 | 256 | 8 | 32 | .068 | .111 | .045 | .095 | .046 | .097 | .072 | .147 | .049 | .114 |

| C1 | 512 | 64 | 8 | .054 | .109 | .049 | .106 | .039 | .089 | .049 | .114 | .082 | .134 |

| C2 | 512 | 32 | 16 | .038 | .093 | .043 | .086 | .039 | .085 | .059 | .108 | .065 | .132 |

| C3 | 512 | 16 | 32 | .061 | .095 | .051 | .102 | .045 | .081 | .059 | .109 | .043 | .104 |

| C4 | 512 | 8 | 64 | .060 | .107 | .053 | .098 | .045 | .083 | .060 | .116 | .042 | .093 |

| D1 | 1024 | 128 | 8 | .039 | .104 | .042 | .093 | .042 | .085 | .035 | .093 | .079 | .132 |

| D2 | 1024 | 64 | 16 | .053 | .104 | .058 | .097 | .050 | .110 | .057 | .101 | .068 | .126 |

| D3 | 1024 | 32 | 32 | .033 | .076 | .058 | .114 | .046 | .086 | .070 | .107 | .062 | .115 |

| D4 | 1024 | 16 | 64 | .046 | .089 | .036 | .091 | .044 | .084 | .054 | .109 | .044 | .099 |

| D5 | 1024 | 8 | 128 | .037 | .073 | .041 | .091 | .041 | .091 | .061 | .131 | .045 | .097 |

| A1 | 128 | 16 | 8 | .107 | .164 | .063 | .114 | .050 | .108 | .072 | .121 | .108 | .166 |

| A2 | 128 | 8 | 16 | .106 | .160 | .064 | .118 | .041 | .085 | .073 | .124 | .078 | .138 |

| B1 | 256 | 32 | 8 | .064 | .123 | .048 | .104 | .042 | .094 | .075 | .131 | .079 | .137 |

| B2 | 256 | 16 | 16 | .058 | .125 | .051 | .101 | .040 | .101 | .065 | .112 | .055 | .116 |

| B3 | 256 | 8 | 32 | .079 | .124 | .047 | .089 | .051 | .091 | .053 | .106 | .050 | .105 |

| C1 | 512 | 64 | 8 | .050 | .093 | .048 | .090 | .051 | .103 | .047 | .104 | .075 | .133 |

| C2 | 512 | 32 | 16 | .047 | .104 | .044 | .087 | .039 | .085 | .053 | .109 | .068 | .124 |

| C3 | 512 | 16 | 32 | .042 | .097 | .044 | .087 | .057 | .106 | .046 | .105 | .060 | .104 |

| C4 | 512 | 8 | 64 | .050 | .102 | .053 | .101 | .052 | .088 | .058 | .121 | .062 | .114 |

| D1 | 1024 | 128 | 8 | .044 | .090 | .046 | .102 | .051 | .107 | .039 | .092 | .076 | .140 |

| D2 | 1024 | 64 | 16 | .043 | .082 | .040 | .088 | .050 | .098 | .046 | .098 | .060 | .106 |

| D3 | 1024 | 32 | 32 | .045 | .089 | .054 | .097 | .057 | .103 | .060 | .104 | .066 | .115 |

| D4 | 1024 | 16 | 64 | .044 | .087 | .038 | .087 | .049 | .094 | .059 | .106 | .051 | .101 |

| D5 | 1024 | 8 | 128 | .041 | .082 | .041 | .089 | .038 | .086 | .061 | .103 | .054 | .103 |

| A1 | 128 | 16 | 8 | .072 | .116 | .054 | .107 | .041 | .085 | .044 | .088 | .077 | .123 |

| A2 | 128 | 8 | 16 | .068 | .122 | .054 | .112 | .059 | .125 | .073 | .117 | .070 | .133 |

| B1 | 256 | 32 | 8 | .045 | .100 | .060 | .101 | .041 | .081 | .042 | .082 | .036 | .084 |

| B2 | 256 | 16 | 16 | .053 | .096 | .058 | .104 | .045 | .094 | .045 | .102 | .060 | .104 |

| B3 | 256 | 8 | 32 | .064 | .123 | .057 | .113 | .049 | .101 | .042 | .092 | .061 | .130 |

| C1 | 512 | 64 | 8 | .043 | .089 | .043 | .095 | .044 | .086 | .045 | .088 | .041 | .095 |

| C2 | 512 | 32 | 16 | .046 | .109 | .067 | .112 | .052 | .093 | .051 | .096 | .043 | .086 |

| C3 | 512 | 16 | 32 | .048 | .099 | .055 | .095 | .062 | .114 | .050 | .102 | .051 | .098 |

| C4 | 512 | 8 | 64 | .038 | .097 | .055 | .100 | .047 | .100 | .046 | .093 | .042 | .092 |

| D1 | 1024 | 128 | 8 | .053 | .103 | .060 | .099 | .051 | .099 | .071 | .118 | .044 | .094 |

| D2 | 1024 | 64 | 16 | .044 | .100 | .062 | .124 | .048 | .090 | .068 | .119 | .042 | .093 |

| D3 | 1024 | 32 | 32 | .053 | .107 | .064 | .116 | .044 | .082 | .045 | .094 | .043 | .098 |

| D4 | 1024 | 16 | 64 | .044 | .096 | .038 | .084 | .042 | .093 | .045 | .087 | .042 | .087 |

| D5 | 1024 | 8 | 128 | .049 | .109 | .042 | .085 | .054 | .109 | .048 | .083 | .042 | .096 |

| A1 | 128 | 16 | 8 | .068 | .112 | .060 | .103 | .030 | .081 | .060 | .108 | .053 | .111 |

| A2 | 128 | 8 | 16 | .060 | .117 | .051 | .103 | .061 | .110 | .062 | .114 | .068 | .117 |

| B1 | 256 | 32 | 8 | .059 | .122 | .048 | .102 | .045 | .094 | .038 | .078 | .040 | .083 |

| B2 | 256 | 16 | 16 | .053 | .109 | .041 | .095 | .047 | .093 | .040 | .080 | .048 | .091 |

| B3 | 256 | 8 | 32 | .060 | .100 | .048 | .098 | .057 | .119 | .050 | .092 | .061 | .106 |

| C1 | 512 | 64 | 8 | .059 | .110 | .064 | .122 | .052 | .099 | .056 | .099 | .055 | .101 |

| C2 | 512 | 32 | 16 | .060 | .122 | .044 | .107 | .041 | .103 | .043 | .113 | .046 | .086 |

| C3 | 512 | 16 | 32 | .061 | .116 | .056 | .122 | .049 | .089 | .046 | .088 | .052 | .099 |

| C4 | 512 | 8 | 64 | .056 | .095 | .057 | .118 | .057 | .110 | .047 | .100 | .055 | .102 |

| D1 | 1024 | 128 | 8 | .063 | .125 | .054 | .102 | .039 | .086 | .044 | .101 | .051 | .098 |

| D2 | 1024 | 64 | 16 | .051 | .109 | .061 | .112 | .047 | .107 | .056 | .106 | .047 | .100 |

| D3 | 1024 | 32 | 32 | .055 | .092 | .057 | .111 | .048 | .095 | .057 | .106 | .047 | .119 |

| D4 | 1024 | 16 | 64 | .065 | .124 | .061 | .116 | .043 | .092 | .048 | .087 | .049 | .098 |

| D5 | 1024 | 8 | 128 | .059 | .116 | .052 | .095 | .049 | .093 | .035 | .075 | .050 | .115 |

Acknowledgements. This work has been supported in part by the Collaborative Research Center “Statistical modeling of nonlinear dynamic processes” (SFB 823, Teilprojekt A1, C1) of the German Research Foundation (DFG).

References

- Akaike, (1973) Akaike, H. (1973). Information theory and an extension of the maximum likelihood principle. Budapest, Akademia Kiado, 267-281.

- Beran, (2009) Beran, J. (2009). On parameter estimation for locally stationary long-memory processes. Journal of Statistical Planning and Inference, 139:900–915.

- Berg et al., (2010) Berg, A., Paparoditis, E., and Politis, D. N. (2010). A bootstrap test for time series linearity. Journal of Statistical Planning and Inference, 140:3841–3857.

- Berkes et al., (2006) Berkes, I., Horvarth, L., Kokoszka, P., and Shao, Q. M. (2006). On discriminating between long-range dependence and changes in mean. Annals of Statistics, 34:1140–1165.

- Bickel and Freedman, (1981) Bickel, P. J. and Freedman, D. A. (1981). Some asymptotic theory for the bootstrap. Annals of Statistics, 9:1196–1217.

- Breidt et al., (1998) Breidt, J., Crato, N., and De Lima, P. (1998). The detection and estimation of long memory in stochastic volatility. Journal of Econometrics, 83:325–348.

- Brillinger, (1981) Brillinger, D. R. (1981). Time Series: Data Analysis and Theory. McGraw Hill, New York.

- Chen et al., (2010) Chen, Y., Härdle, W., and Pigorsch, U. (2010). Localized realized volatility modeling. Journal of the American Statistical Association, 105(492):1376–1393.

- Dahlhaus, (1997) Dahlhaus, R. (1997). Fitting time series models to nonstationary processes. Annals of Statistics, 25(1):1–37.

- Dahlhaus, (2009) Dahlhaus, R. (2009). Local inference for locally stationary time series based on the empirical spectral measure. Journal of Econometrics, 151:101–112.

- Dehling et al., (2011) Dehling, H., Rooch, A., and Taqqu, M. S. (2011). Nonparametric change-point tests for long-range dependent data. to appear in Scandinavian Journal of Statistics.

- Deo and Chen, (2000) Deo, R. and Chen, W. (2000). On the integral of the squared periodogram. Stochastic Process and their Applications, 85:159–176.

- (13) Dette, H., Preuß, P., and Vetter, M. (2011a). A measure of stationarity in locally stationary processes with applications to testing. Journal of the American Statistical Association, 106(495):1113–1124.

- (14) Dette, H., Preuß, P., and Vetter, M. (2011b). Supplemental material to “A measure of stationarity in locally stationary processes with applications to testing”. http://dx.doi.org/10.1198/jasa.2011.tm10811.

- Dwivedi and Subba Rao, (2010) Dwivedi, Y. and Subba Rao, S. (2010). A test for second order stationarity of a time series based on the discrete fourier transform. Journal of Time Series Analysis, 32(1):68–91.

- (16) Erdelyi, A. (1954a). Tables of Integral Transforms, Vol.1. McGraw-Hill, New York.

- (17) Erdelyi, A. (1954b). Tables of Integral Transforms, Vol.2. McGraw-Hill, New York.

- Eubank and LaRiccia, (1992) Eubank, R. and LaRiccia, V. (1992). Asymptotic comparison of Cramer-von Mises and nonparametric function estimation techniques for testing goodness-of-fit. Annals of Statistics, 20(4):2071–2086.

- Fan, (1996) Fan, J. (1996). Test of significance based on wavelet thresholding and Neyman’s truncation. Journal of the American Statistical Association, 91(434):674–688.

- Fox and Taqqu, (1987) Fox, R. and Taqqu, M. S. (1987). Central limit theorems for quadratic forms in random variables having long-range dependence. Probability Theory and Related Fields, 74:213–240.

- Fryzlewicz et al., (2006) Fryzlewicz, P., Sapatinas, T., and Subba Rao, S. (2006). A Haar-Fisz technique for locally stationary volatility estimation. Biometrika, 93:687–704.

- Ghosh and Huang, (1991) Ghosh, B. and Huang, W.-M. (1991). The power and optimal kernel of the Bickel-Rosenblatt test for goodness of fit. Annals of Statistics, 19(2):999–1009.

- Gradshteyn and Ryzhik, (1980) Gradshteyn, I. and Ryzhik, I. (1980). Table of Integrals, Series, and Products. Academic Press, New York.

- Granger and Joyeux, (1980) Granger, C. W. J. and Joyeux, R. (1980). An introduction to long-memory time series models and fractional differencing. Journal of Time Series Analysis, 1:15–29.

- Hosking, (1981) Hosking, J. R. M. (1981). Fractional differencing. Biometrika, 68:165–176.

- Kreiß et al., (2011) Kreiß, J.-P., Paparoditis, E., and Politis, D. N. (2011). On the range of the validity of the autoregressive sieve bootstrap. to appear in Annals of statistics.

- Mikosch and Starica, (2004) Mikosch, T. and Starica, C. (2004). Non-stationarities in financial time series, the long range dependence and the IGARCH effects. The Review of Economics and Statistics, 86:378–390.

- Palma, (2007) Palma, W. (2007). Long-Memory Time Series: Theory and Methods. Wiley Series in Probability and Statistics.

- Palma and Olea, (2010) Palma, W. and Olea, R. (2010). An efficient estimator for locally stationary Gaussian long-memory processes. Annals of Statistics, 38(5):2958–2997.

- Paparoditis, (2009) Paparoditis, E. (2009). Testing temporal constancy of the spectral structure of a time series. Bernoulli, 15:1190–1221.

- Paparoditis, (2010) Paparoditis, E. (2010). Validating stationarity assumptions in time series analysis by rolling local periodograms. Journal of the American Statistical Association, 105(490):839–851.

- Preuß and Vetter, (2012) Preuß, P. and Vetter, M. (2012). On discriminating between long-range dependence and non stationarity. Technical report, Ruhr-Universität Bochum. http://www.ruhr-uni-bochum.de/imperia/md/content/mathematik3/publications/longmemory24092012.pdf.

- Preuß et al., (2012) Preuß, P., Vetter, M., and Dette, H. (2012). A test for stationarity based on empirical processes. to appear in Bernoulli.

- Roueff and von Sachs, (2011) Roueff, F. and von Sachs, R. (2011). Locally stationary long memory estimation. Stochastic Processes and their Applications, 121:813–844.

- Sibbertsen and Kruse, (2009) Sibbertsen, P. and Kruse, R. (2009). Testing for a change in persistence under long-range dependencies. Journal of Time Series Analysis, 30:263–285.

- Starica and Granger, (2005) Starica, C. and Granger, C. (2005). Nonstationarities in stock returns. The Review of Economics and Statistics, 87:503–522.

- Taniguchi, (1980) Taniguchi, M. (1980). On estimation of the integrals of certain functions of spectral density. Journal of Applied Probability, 17:73–83.

- von Sachs and Neumann, (2000) von Sachs, R. and Neumann, M. H. (2000). A wavelet-based test for stationarity. Journal of Time Series Analysis, 21:597–613.

- Whittle, (1951) Whittle, P. (1951). Hypothesis Testing in Time Series Analysis. Almqvist and Wiksell, Uppsala.

6 Appendix: technical details

In the following, we will state two results which will be central for the proof of the statements in Sections and .

Theorem 6.1.

If Assumption 2.1 is satisfied with , the following statements are correct.

-

a)

where the vector is of order . In particular, this term vanishes if the functions are independent of for all .

- b)

-

c)

If and with , then we have

where denotes a vector containing merely ones ().

It follows by the same arguments as given in Section of Preuß and Vetter, (2012), that there exist parameters such that the bootstrap process defined in (4.7) can be represented as

| (6.1) |

where are the innovations from part of the bootstrap description. We now assume that the null hypothesis (3.5) holds, and consider the process

| (6.2) |

where the coefficients are the coefficients in (2.10). We then define as in (2.18) whereby the random variables are replaced by . The next theorem shows that the random variable can be approximated by .

Theorem 6.2.

Let be fixed and denote with the event where . If Assumption 2.1 and the inequality

| (6.3) |

are satisfied, then

6.1 Proof of Theorem 6.1:

Note that corresponds to the error which occurs if the coefficients are replaced by and that contains the approximation error of through with denoting the midpoint of the -th block. The following four statements conclude the proof for

| (6.4) | |||||

| (6.5) | |||||

| (6.6) | |||||

| (6.7) |

Proof of (6.4): Without loss of generality, we only consider the first summand in . Due to the independence of the random variables , we obtain that only those terms contribute to the sum where the conditions and are satisfied, which implies the inequality . Thus, the first term in can be expressed as

where we used the well known identity

| (6.8) |

[note that we only have to consider three possible values of since ]. It is easy to see that

where

| (6.10) | |||||

| (6.11) |

In order to complete the proof of (6.4), it therefore suffices to demonstrate that the last three expressions are of order . We commence with (6.1). Setting and using (2.4), it follows that there exists a constant such that

| (6.12) |

(note that all terms where one of the variables or vanishes are of smaller or the same order). This argument will be employed continuously throughout this proof without mentioning it explicitly. Note that the summand does not occur in the numerator of the above expression due to the symmetry of and in (6.1), and that denotes a universal constant throughout the whole proof. Setting , we obtain and the expression on the right hand side of (6.12) can be written as

where means that is bounded by some finite constant for all . By using (2.4), (6.8), (7.2) and similar arguments, we obtain that (6.10) is bounded by

and since (6.11) is shown analogously, we therefore conclude the proof of (6.4).

Proof of (6.5): The result follows by similar arguments as used in the treatment of (6.1)–(6.11).

Proof of (6.6): Without loss of generality, we only consider the first summand and replace by

[the error due to this replacement is negligible, which follows by analogous arguments as given for the term at a later stage of this proof]. Due to the independence of the random variables , we obtain the sum of three terms [compare the definition of for the first two summands and the definition of for the third one] and we restrict ourselves to the first one, i.e. we only consider

Using a Taylor expansion, we can write

with , and therefore splits into two terms which will be denoted by and in the following discussion. We start with the treatment of the first summand. Employing the independence of the innovations we obtain that the indices corresponding to non vanishing terms must satisfy and . Applying (6.8) afterwards yields and this combined with (2.4) and (2.6) implies

We restrict ourselves to the cases and since the remaining terms are of smaller order. A straightforward calculation yields

| (6.13) | |||||

| (6.14) |

and by using the second summand it follows that is bounded by

where we used Lemma 7.1c) and 7.1b) for the first and second inequality, respectively. Next, we show that is of order , and for this reason we choose such that . Using (2.4), (2.6), (2.7) and , the claim then follows by a further application of Lemma 7.1b)

Proof of (6.7): The statement follows from (2.3) and similar arguments as given in the proofs of (6.4) and (6.6).

In order to proof the assertion for , one proceeds in the same way and the details are omitted for the sake of brevity. However it turns out that the expression corresponding to does not vanish in this case and there appears an additional bias, which will be denoted by .

Proof of part b) We restrict ourselves to the proof of

and recall the definition of the remainder

All other statements can be verified completely analogously and the details are omitted. By combining the arguments from the proof of part a) and from Dette et al., 2011b , we obtain that

where

and

We start with . Because of the independence of the random variables , the restrictions , , and are necessary for a non vanishing term. Consider and sum over by using . Then, can be written as

An application of (2.4) yields similar to the proof of part a) that the above expression is of order , if

-

(i)

[compare (6.10)],

-

(ii)

[we prove this claim in Lemma 7.2 in the appendix since this kind of restriction did not occur in the proof of part a)],

-

(iii)

we drop [compare (6.1)],

-

(iv)

we drop and [compare (6.11)],

-

(v)

we drop and [compare (6.1)].

By rearranging the equation to , it follows

By using the same techniques as in , we obtain

Note that, in contrast to the term , the cases where do not vanish. In fact, using the three equalities

we deduce

| (6.15) | |||||

Proof of part c) Exemplarily we consider the case and . The other cases can be treated similarly with an additional amount of notation. Following the same lines as in the proof of Theorem 3.1 in Dette et al., 2011a , it is sufficient to choose an arbitrary indecomposable partition

of the table

| (6.16) |

[see Brillinger, (1981)] and to treat the term

with , for , , and . We now discuss the conditions which yield a contribution different from in this sum. Note that some of the are equal to each other and we will therefore write for the different values and consider as a function depending on . Using the independence of the random variables and summing with respect to , the conditions

| (6.17) | |||

| (6.18) | |||

| (6.19) |

follow. Rearranging the equations in (6.19) for a variable and plugging them into the equations (6.17) (where in every equation only one variable is replaced) yields, due to the indecomposability of the partition and , that the conditions

| (6.28) |

must hold, where and . By employing (2.4), we can bound the above expression up to a constant by

Using Lemma 7.1b) in the appendix, this term can be (up to a constant) bounded by

We now assume without loss of generality that

| (6.29) |

holds for (the more general case follows analogously with an additional amount of notation). In this case the absolute values in the above expression can be skipped. It follows, as in Dette et al., 2011a , that the conditions on the imply that, if is chosen, there are only finitely many possible choices for , . Thus it suffices to consider the following sum

with and (because of (6.29) and there are no other possible values for ). We remind that (due to the indecomposability of the partition) the -fractions inside the addend are hooked. This means that for two different fractions there exists a chain of fractions (starting with the first considered fraction and ending with the second one), such that in every element of the chain there exists at least one element which also occurs in the consecutive fraction. We will perform a summation in a particular way and in order to illustrate this, we consider the first two fractions and assume that and are (up to a the algebraic sign) the same. We distinguish two cases.

-

(i)

If , we obtain from Lemma 7.1a) that

(6.30) (6.31) Furthermore we have which follows from the conditions and .

-

(ii)

If and , it follows from Lemma 7.1b) that

(6.32) (6.33)

In both cases, it is possible that variables cancel out, for example if and in the first and second case, respectively. We apply (6.30)–(6.33) in total -times. In the first -applications, we use and (depending on the algebraic sign of the variable which appears in both fractions) and in the th and th application we employ and . We furthermore assume that variables cancel out while utilizing these inequalities. Afterwards variables remain with , namely , and other variables with values in . Denoting these variables with we obtain

with some . We first consider the case . If and , it follows that the above term equals

If or , we apply Lemma 7.1a) and b) in order to obtain the same upper bound (it can be shown that, in this case, there appears an additional factor in the denominator, so the corresponding term is, in fact, of smaller order). The same upper bound holds for .

6.2 Proof of Remark 3.6:

If we replace by the corresponding integrated version , the derivation of the asymptotic variance can be carried out almost analogously as in the proof of Theorem 6.1b) except that the term, where the variable in equals or , does not occur, because for the integrated version one can use

| (6.34) |

6.3 Proof of Theorem 6.2:

Proof of part a): We define and as where the observed data are replaced by and , respectively. By using (6.1) and writing for the bootstrap analogue of , we then get

[compare the first set of equalities in the proof of Theorem 6.1 a)], where . By using the decomposition

the above expression splits into four terms and for the sake of brevity we only consider the first one. The other cases are treated similarly. As in the proof of Theorem 6.1 a) we then obtain terms and which are defined as , where the coefficients are replaced by [note that since the coefficients of the bootstrap process do not possess any time dependence]. If we employ (6.3) and combine it with the fact that on the set , we get

| (6.35) |

which together with (2.4) and the assumptions of the theorem implies

| (6.36) |

Note that the coefficients in the MA() representation of the bootstrap processes do not depend on time and that for such processes we only required

| (6.37) |

in the proof of Theorem 6.1 a) to obtain appropriate bounds for the error. By using (6.35) and (6.36) instead of (6.37) and similar arguments as given in the proof of Theorem 6.1 a) it follows that

where is defined as but with replaced by

Since and are treated analogously, the claim follows [note that cancels out since the coefficients do not possess any time dependence].

6.4 Proofs of the results in Section 3 and 4:

Proof of Theorem 3.2: The claim follows by employing the Cramér-Wold device in combination with Theorem 6.1.

Proof of Theorem 3.4: Similarly to the proof of Theorem 6.1, the two equations

can be established. By Markov’s inequality the assertion of the theorem follows.

Proof of Theorem 4.2: We define as and as but with replaced by from (2.10). Then part a) is obvious, because we have for all under the null hypothesis and and are both independent and standard normal distributed. Part b) follows from the proof of Theorem 6.1, so we focus on part c) and d). Note that (2.11) and Theorem 6.1 a), b) imply

which directly yields part d). If we have

| (6.38) |

for every , Part c) follows from Theorem 6.2, (4.8), the conditions on the rate of if is chosen sufficiently small. Finally, (6.38) is a consequence of Lemma 4.3 in Preuß and Vetter, (2012).

Proof of Theorem 4.3: By employing the triangle inequality we can bound the Mallow metric between and by

[where and are the random variables from Theorem 4.2 specified in the proof of which]. It follows from the proof of Theorem 6.1 that the first summand converges to zero and the second summand equals zero because of Theorem 4.2 a). So it suffices to treat the third summand which is bounded by

We obtain from Theorem 6.1 a) and b) that a constant exists such that

| (6.39) |

[note the we are under the null hypothesis and that we therefore have ]. This combined with Theorem 6.2, (6.38) and the conditions on the growth rate on yields that we can restrict ourselves to the second term, which is [up to the constant ] bounded by

7 Appendix: Auxiliary Lemmas

Finally we show some lemmas which were employed in the above proofs.

Lemma 7.1.

Suppose . Then there exists a constant such that the following holds:

-

a)

If and , then

(7.1) -

b)

If and , then it follows for

(7.2) -

c)

If and , then

(7.3) (7.4)

Proof: a) Using equation 3.196(3) in Gradshteyn and Ryzhik, (1980), it follows that

b) If we can bound the middle sum in (7.2) by

The last inequality follows from the equations 3.196(2) and 3.191(2) [for choosing ] in Gradshteyn and Ryzhik, (1980). On the other hand, if we have

The last inequality follows with Gradshteyn and Ryzhik, (1980) as above.

c) We start with (7.3). Using equation 13.2(18) in Erdelyi, 1954b yields

Concerning (7.4) we use equation 6.4(23) in Erdelyi, 1954a which implies

Lemma 7.2.

If , then

Proof: Firstly, we set and . Then we define and rearrange to . Since , it follows that if are fixed, there are at most two possible values for . Hence it is enough to consider the following expression with