Nonparametric Independence Screening in Sparse Ultra-High Dimensional Varying Coefficient Models

Abstract

The varying-coefficient model is an important nonparametric statistical model that allows us to examine how the effects of covariates vary with exposure variables. When the number of covariates is big, the issue of variable selection arrives. In this paper, we propose and investigate marginal nonparametric screening methods to screen variables in ultra-high dimensional sparse varying-coefficient models. The proposed nonparametric independence screening (NIS) selects variables by ranking a measure of the nonparametric marginal contributions of each covariate given the exposure variable. The sure independent screening property is established under some mild technical conditions when the dimensionality is of nonpolynomial order, and the dimensionality reduction of NIS is quantified. To enhance practical utility and the finite sample performance, two data-driven iterative NIS methods are proposed for selecting thresholding parameters and variables: conditional permutation and greedy methods, resulting in Conditional-INIS and Greedy-INIS. The effectiveness and flexibility of the proposed methods are further illustrated by simulation studies and real data applications.

keywords:

Sure independence screening; Variable selection; Sparsity; Conditional permutation; False positive ratesE-mail:myb@swufe.edu.cn

1 Introduction

The development of information and technology drives big data collections in many areas of advanced scientific research ranging from genomic and health science to machine learning and economics. The collected data frequently has an ultra-high dimensionality that is allowed to diverge at nonpolynomial (NP) rate with the sample size , namely for some . For example, in biomedical research such as genomewide association studies for some mental diseases, millions of SNPs are potential covariates. Traditional statistical methods face significant challenges in dealing with such a high-dimensional problem with large sample sizes.

With the sparsity assumption, variable selection helps improve the accuracy of estimation and gain scientific insights. Many significant variable selection techniques have been developed, such as Bridge regression in Frank and Friedman (1993), Lasso in Tibshirani (1996), SCAD and folded concave penalty in Fan and Li (2001), the Elastic net in Zou and Hastie (2005), Adaptive Lasso (Zou, 2006), and the Dantzig selector in Candes and Tao (2007). Methods on the implementation of folded concave penalized least-squares include the local linear approximation algorithm in Zou and Li (2008) and the plus algorithm in Zhang (2010). However, due to the simultaneous challenges of computational expediency, statistical accuracy and algorithmic stability, these methods do not perform well in ultra-high dimensional problems.

To tackle these problems, Fan and Lv (2008) introduced a sure independence screening (SIS) method to select important variables in ultra-high dimensional linear regression models via marginal correlation learning. Hall and Miller (2009) extended the method to the generalized correlation ranking, which was further extended by Fan, Feng and Song (2011) for ultra-high dimensional nonparametric additive models, resulting in nonparametric independence screening (NIS). On a different front, Fan and Song (2010) extended the SIS idea to ultra-high dimensional generalized linear models and devised a useful technical tool for establishing the sure screening results and bounding false selection rates. Other related methods include data-tilling method (Hall, Titterington and Xue, 2009), marginal partial likelihood method MPLE (Zhao and Li, 2010), and robust screening methods by rank correlation (Li, et al., 2012) and distance correlation (Li, Zhong and Zhu, 2012). Inspired by these previous work, our study will focus on variable screening in nonparametric varying-coefficient models with NP dimensionality.

It is well known that nonparametric models are flexible enough to reduce modeing biases. However, they suffer from the so-called “curse of dimensionality”. A remarkable simple and powerful nonparametric model for dimensionality reductions is the varying-coefficient model,

| (1) |

where is the vector of covariates, is some observable exposure variables, is the response, and is the random noise with conditional mean 0 and finite conditional variance. An intercept term (i.e., ) can be introduced if necessary. This model assumes that the variables in the covariate vector X enter the model linearly, meanwhile it allows regression coefficient functions to very smoothly with the exposure variable. The model retains general nonparametric characteristics and allows the nonlinear interactions between the exposure variable and the covariates. It arises frequently from economics, finance, politics, epidemiology, medical science, ecology, among others. For an overview, see Fan and Zhang (2008).

When the dimensionality is finite, Fan, Zhang and Zhang (2001) proposed the generalized likelihood ratio (GLR) test to select variables in the varying-coefficient model (1). For the time-varying coefficient model, a special case of (1) with the exposure variable being the time , Wang, Li and Huang (2008) applied the basis function approximations and the SCAD penalty to address the problem of variable selection. In the NP dimensional setting, Lian (2011) utilized the adaptive group Lasso penalty in time-varying coefficient models. These methods still face the aforementioned three challenges.

In this paper, we consider a nonparametric screening by ranking a measure of the marginal nonparametric contributions of each covariate given the exposure variable. For each given covariate, we fit marginal regressions of the response against the covariate conditioning on :

| (2) |

Let and be the solution to (2) and and be their nonparametric estimates. Then, we rank the importance of each covariate in the joint model according to a measure of marginal utility (which is equivalent to the goodness of fit) in its marginal model. Under some reasonable conditions, the magnitude of these marginal contributions provides useful probes of the importance of variables in the joint varying-coefficient model. This is an important extension of SIS (Fan and Lv, 2008) to a more flexible class of varying coefficient models.

The sure screening property of NIS can be established under certain technical conditions. In some very specific cases, NIS can even be model selection consistent. In establishing this kind of results, three factors are related to the minimum distinguishable marginal signals: the stochastic error in estimating the nonparametric components, the approximation error in modeling nonparametric components, and the tail distributions of the covariates. Following Fan and Lv (2008) and Fan, Feng and Song (2011), we propose two nonparametric independence screening approaches in an iterative framework. One is called Greedy-INIS, in which we adopt a greedy method in the variable screening step. The other is called Conditional-INIS which is built on conditional random permutation to determine a data driven screening threshold. They both serve to effectively control the false positive rate and false negative rate with enhanced performance.

This article is organized as follows. In Section 2, we fit each marginal nonparametric regression model via B-spline basis approximation and screen variables by ranking a measure of these estimators. In Section 3, we establish the sure screening property and model selection consistency under certain technical conditions. Iterative NIS procedures (namely Greedy-INIS and Conditional-INIS) are developed in Section 4. In Section 5, a set of numerical studies are conducted to evaluate the performance of our proposed methods.

2 Models and Nonparametric Marginal Screening Method

In this section we study the varying-coefficient model with the conditional linear structure as in (1). Assume that the functional coefficient vector is sparse. Let be the true sparse model with nonsparsity size . We allow to grow with and denote it by whenever necessary.

2.1 Marginal Regression

For , let and be the minimizer of the following marginal regression problem:

| (3) |

where denotes the joint distribution of and is the class of square integrable functions under the measure . By some algebra, we have that the minimizer of (3) is

| (4) |

Let , we rank the marginal utility of covariates by

| (5) |

where It can be seen that

| (6) |

For each , if , then has the same quantity as the measure of marginal functional coefficient . On the other hand, this marginal utility is closely related to the conditional correlation between and , as if and only if almost surely.

2.2 Marginal Regression Estimation with B-spline

To obtain an estimate of the marginal utility , , we approximate and by functions in , the space of polynomial splines of degree on , a compact set. Let denote its normalized B-spline basis with where is the sup norm. Then

where and are scalar coefficients.

We now consider the following sample version of the marginal regression problem:

| (7) |

where , and .

It is easy to show that the minimizers of (7) is given by

| (8) |

where

| (12) |

is an matrix. As a result, the estimates of and , are given by

| (13) |

where is an -dimension vector with all entries 0. Similarly, we have the estimate of the intercept function by

| (14) |

where

| (15) |

We now define an estimate of the marginal utility as

| (16) | |||||

where . Note that throughout this paper, whenever two vectors a and b are of the same length, ab denotes the componentwise product. Given a predefined threshold value , we select a set of variables as follows:

| (17) |

Alternatively, we can rank the covariates by the residual sum of squares of marginal nonparametric regressions, which is defined as

| (18) |

and we select variables as follows,

| (19) |

where is a predefined threshold value.

It is worth noting that ranking by marginal utility is equivalent to ranking by the measure of goodness of fit . To see the equivalence, first note that

| (20) |

and

| (21) |

It follows from (20) and (21) that

| (22) |

Since the first two terms on the right hand side of (22) do not vary in , ranking by is the same as that by . Therefore, selecting variables with large marginal utility is the same as picking those that yield small marginal residual sum of squares.

To bridge and , we define the population version of the marginal regression using B-spline basis. From now on, we will omit the argument in and write B whenever the context is clear. Let and , where and are the minimizer of

| (23) |

and , where is the minimizer of

| (24) |

It can be seen that

| (25) | |||||

| (26) |

where

| (27) | |||||

3 Sure Screening

In this section, we establish the sure screening properties of the proposed method for model (1). Recall that by (6) the population version of marginal utility quantifies the relationship between and as follows:

| (28) |

Then the following two conditions guarantee that the marginal signal of the active components does not vanish.

- (i)

-

Suppose for , is uniformly bounded away from 0 and infinity on , where is the compact support of . That is, there exist some positive constants and , such that .

- (ii)

-

, for some and .

Then under conditions (i) and (ii),

| (29) |

Note that in condition (ii), the number of basis functions is not intrinsic. By the Remark 1 below, should be chosen in correspondence to the smoothness condition of the nonparametric component. Therefore, condition (ii) depends only on and smoothness parameter in condition (iii). We keep here to make the relationship more explicit.

3.1 Sure Screening Properties

The following conditions (iii)-(vii) are required for the B-spline approximation in marginal regressions and establishing the sure screening properties.

- (iii)

-

The density function of is bounded away from zero and infinity on . That is, for some constants and .

- (iv)

-

Functions and belong to a class of functions , whose th derivative exists and is Lipschitz of order . That is,

for some positive constant , where is a nonnegative integer and such that .

- (v)

-

Suppose for all , there exists a positive constant and , such that

(30) uniformly on , for any . Furthermore, let , where . Suppose there exists some positive constants and satisfying , such that

(31) uniformly on , for any .

- (vi)

-

The random errors are i.i.d with conditional mean 0, and there exists some positive constants and satisfying , such that

(32) uniformly on , for any .

- (vii)

-

There exists some constant such that .

Proposition 1

Under conditions (i)-(v), there exists a positive constant such that

| (33) |

In addition, when for some , we have

| (34) |

Remark 1

It follows from Proposition 1 that the minimum signal level of is approximately the same as , provided that the approximation error is negligible. It also shows that the number of basis functions should be chosen as

for some positive constant . In other words, the smoother the underlying function is (i.e., the larger is), the smaller we can take.

The following Theorem 1 provides the sure screening properties of the nonparametric independence screening method proposed in Section 2.2.

Theorem 1

Suppose conditions (i)-(vi) hold.

-

(i)

If as , then for any , there exist some positive constants and such that

(35) -

(ii)

If condition (vii) also holds, then by taking with , there exist positive constants and such that

(36)

Remark 2

According to Theorem 1 , we can handle NP dimensionality

It shows that the number of spline bases also affects the order of dimensionality: the smaller is, the higher dimensionality we can handle. On the other hand, Remark 1 points out that it is required to have a good bias property. This means that the smoother the underlying function is (i.e. the larger is), the smaller we can take, and consequently higher dimensionality can be handled. The compatibility of these two requirements requires that , which implies that . We can take , which is the optimal convergence rate for nonparametric regression (Stone, 1982). In this case, the allowable dimensionality can be as high as

3.2 False Selection Rates

According to (34), the ideal case for vanishing false-positive rate is when

so that there is a natural separation between important and unimportant variables. By Theorem 1(i), when (35) tends to zero, we have with probability tending to 1 that

Consequently, by choosing as in Theorem 1(ii), NIS can achieve the model selection consistency under this ideal situation, i.e.,

In particular, this ideal situation occurs under the partial orthogonality condition, i.e., is independent of given , which implies for

In general, the model selection consistency can not be achieved by a single step of marginal screening. The marginal probes can not separate important variables from unimportant variables. The following Theorem 2 quantifies how the size of selected models is related to the matrix of basis functions and the thresholding parameter .

Theorem 2

Under the same conditions in Theorem 1, for any , there exist positive constants and such that

| (37) | |||||

where , and is a functional vector of dimension.

4 Iterative Nonparametric Independence Screening

As Fan and Lv (2008) points out, in practice the nonparametric independence screening (NIS) would still suffer from false negative (i.e., miss some important predictors that are marginally weakly correlated but jointly correlated with the response), and false positive (i.e., select some unimportant predictors which are highly correlated with the important ones). Therefore, we adopt an iterative framework to enhance the performance of this method. We repeatedly apply the large-scale variable screening (NIS) followed by a moderate-scale variable selection, where we use group-SCAD penalty as our selection strategy. In the NIS step, we propose two methods to determine a data-driven threshold for screening, which result in Conditional-INIS and Greedy-INIS, respectively.

4.1 Conditional-INIS Method

The conditional-INIS method builds upon conditional random permutation in determining the thresholding . Recall the random permutation used in Fan, Feng and Song (2011), which generalizes that Zhao and Li (2010). Randomly permute Y to get and compute , where is a permutation of , based on the randomly coupled data that has no relationship between covariates and response. Thus, these estimates serve as the baseline of the marginal utilities under the null model (no relationship). To control the false selection rate at under the null model, one would choose the screening threshold be , the th-ranked magnitude of . Thus, the NIS step selects variables . In practice, one frequently uses , namely, the largest marginal utility under the null model.

When the correlations among covariates are large, there will be hardly any differentiability between the marginal utilities of the true variables and the false ones. This makes the selected variable set very large to begin with and hard to proceed the rest of iterations with limited false positives. For numerical illustrations, see section 5.2. Therefore, we propose a conditional permutation method to tackle this problem. Combining the other steps, our Conditional-INIS algorithm proceeds as follows.

- 0.

- 1.

-

Regress Y on , and get intercept and their functional coefficients’ estimators . Conditioning on , the -dimensional partial residual is

For all , compute using , which measures the additional utility of each covariate conditioning on the selected set .

To determine the threshold for NIS, we apply random permutation on the partial residual , which yields . Compute based on the decoupled data . Let be the th-ranked magnitude of . Then, the active variable set of variables is chosen as

In our numerical studies, .

- 2.

-

Apply the group-SCAD penalty on to select a subset of variables . Details about the implementation of SCAD will be described later.

- 3.

-

Repeat step 1-2, where we replace in step 1 by , , and get and in step 2. Iterate until for some or , for some prescribed positive integer .

4.2 Greedy-INIS Method

Following Fan, Feng and Song (2011), we also implemented a greedy version of INIS method. We skip step 0 and start from step 1 in the algorithm above (i.e., take ), and select the top variables that have the largest marginal norms . This NIS step is followed by the same group-SCAD penalized regression as in step 2. We then iterate these steps until there are two identical subsets or the number of variables selected exceeds a prespecified . In our simulation studies, is set as .

4.3 Implementation of SCAD

In the group-SCAD step, variables are selected as through minimizing the following objective function:

| (38) |

where and is the SCAD penalty such that

with . We set as suggested and solve the optimization above via local quadratic approximations (Fan and Li, 2001). is chosen by BIC criteria , where is the number of covariates chosen. By Antoniadis and Fan (2001) and Yuan and Lin (2006), the norm-penalty in (38) encourages the group selection.

5 Numerical Studies

In this section, we carry out several simulation studies to assess the performance of our proposed methods. If not otherwise stated, the common setup for the following simulations are: cubic B-spline, sample size , the number of variables , and the number of simulations for each example.

5.1 Comparison of Minimum Model Size

In this study, as in Fan and Song (2010), we illustrate the performance of NIS method in terms of the minimum model size (MMS) needed to include all the true variables, i.e., to possess sure screening property.

Example 1

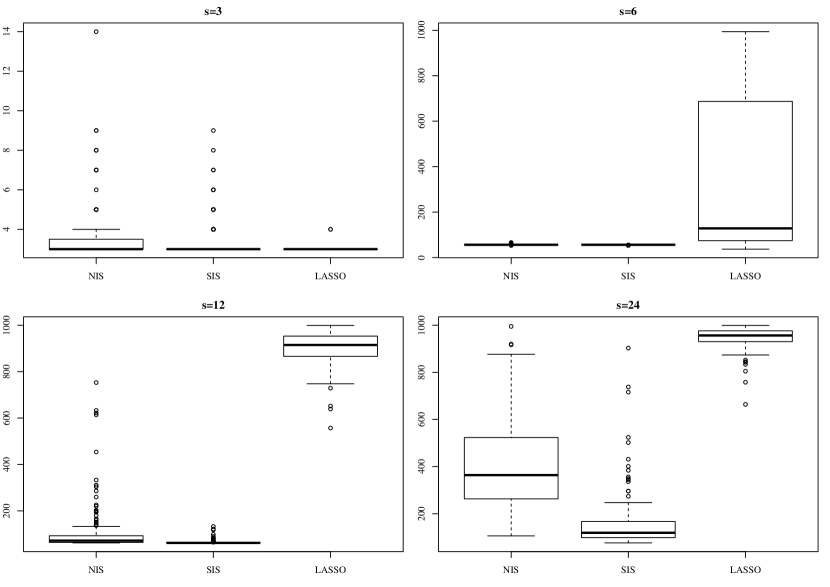

Following Fan and Song (2010), we first consider a linear model as a special case of the varying coefficient model. Let be i.i.d. standard normal random variables and

where are standard normal random variables. We construct the following model: , where and has nonzero components. To carry out NIS, we define an exposure independently from the standard uniform distribution.

We compare NIS, Lasso and SIS (independence screening for linear models). The boxplots of minimum model size are presented in Figure 1. Note that when , the irrepresentable condition fails, and Lasso performs badly even in terms of pure screening. On the other hand, SIS performs better than NIS because the coefficients are indeed constant, and there are fewer parameters () involved in SIS than those of NIS ().

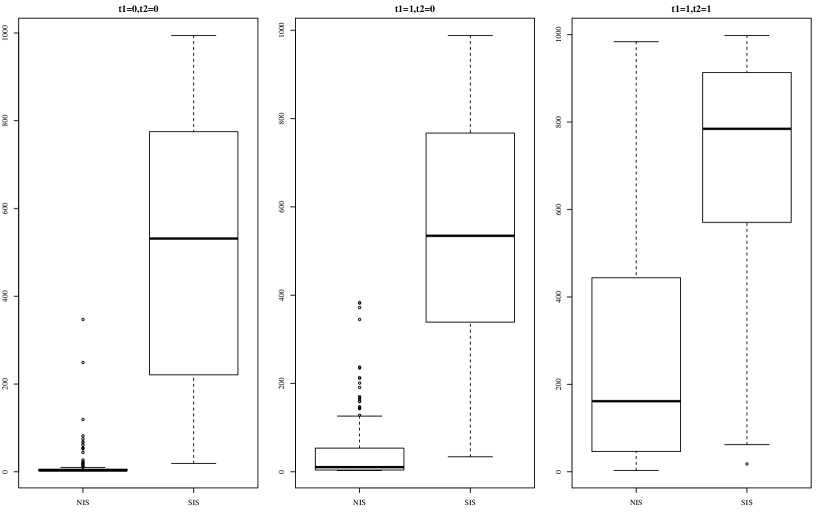

Example 2

For the second example, we illustrate that when the underlying model’s coefficients are indeed varying, we do need nonparametric independence screening. Let be i.i.d. uniform random variables on , based on which we construct X and as follows:

where and controls the correlation among the covariates X and the correlation between X and , respectively. When , ’s are uncorrelated, and when the correlation is . If , ’s and are also correlated with correlation coefficient 0.5.

For the varying coefficients part, we take coefficient functions

The true data generation model is

where ’s are i.i.d. standard Gaussian random variable.

Under different correlation settings, the comparison MMS between NIS and SIS methods are presented in Figure 2. When the correlation gets stronger, independence screening becomes harder.

5.2 Comparison of Permutation and Conditional Permutation

In this section, we illustrate the performance the conditional random permutation method.

Example 3

Let be i.i.d. standard normal, be i.i.d. standard uniformly distributed random variables, and the noise follows the standard normal distribution. We construct and as follows:

We will take , resulting in uncorrelated case and and , corresponding to for all and . By taking (i.e., take the maximum value of the marginal utility of the permuted estimates), we report the average of the true positive number (TP), model size, the lower bound of the marginal signal of true variables and the upper bound of the marginal signal of false variables for different correlation settings based on simulations. Their robust standard deviations are also reported therein.

Based on Table 1, we see that when the correlation gets stronger, although sure screening properties can be achieved most of the time via unconditional () random permutation thresholding, the model size becomes very large and therefore the false selection rate is high. The reason is that there is no differentiability between the marginal signals of the true variables and the false ones. This drawback makes the original random permutation not a feasible method to determine the screening threshold in practice.

Model TP Size K=0 1.12(0.15) 0.22(0.03) K=1 0.72(0.11) 0.11(0.02) K=4 NA 0.06(0.01) 0.06(0.01) K=8 NA 0.05(0.01) 0.05(0.01)

We now applied the conditional permutation method, whose performance is illustrated in Table 1 for a few choices of tuning parameter . The screening threshold is taken as with . Generally speaking, although the lower bound of the true positives’ signals may be smaller than the upper bound of false variables’ signals, the largest norms still have a high possibility to contain at least some true variables. When conditioning on this small set of more relevant variables, the marginal contributions of false positives get weaker. Note that in the absence of correlation, when (here ), the first variables have already included all the true variables (i.e., ), hence the minimum of true signal is not available. In other cases, we see that the gap between the marginal signals of true variables and false variables become large enough to differentiate them. Table 1 shows that by using the thresholding via the conditional permutation method, not only the sure screening properties are still maintained, but also the model sizes are dramatically reduced.

5.3 Comparison of Model Selection and Estimation

In this section we explore the performance of Conditional-INIS and Greedy-INIS method. In our iterative framework, conditional permutation serves as the initialization step (step 0) and we take in the rest of the paper. For each method, we report the average number of true positive (TP), false positive (FP), prediction error (PE), and their robust standard deviations. Here the prediction error is the mean squared error calculated on the test dataset of size generated from the same model. As a measure of the complexity of the model, signal-to-noise-ratio (SNR), defined by , is computed. Table 2 reports the results using the simulated model specified in Example 3. We now illustrate the performance by using another example.

| Model | Correlation | Conditional-INIS | Greedy-INIS | |||||

|---|---|---|---|---|---|---|---|---|

| X’s | X’s-W | TP | FP | PE | TP | FP | PE | |

Example 4

Let , and be the same as in Example 3. We now introduce more complexities in the following model:

The results are present in Table 3.

| Model | Correlation | Conditional-INIS | Greedy-INIS | |||||

|---|---|---|---|---|---|---|---|---|

| X’s | X’s-W | TP | FP | PE | TP | FP | PE | |

Through the examples above, Conditional-INIS and Greedy-INIS show comparable performance in terms of TP, FP and PE. When the covariates are independent or weakly correlated, sure screening is easier to achieve and false positive is rare; as the correlation gets stronger, we see a decrease in TP and an increase in FP. It seems that Greedy-INIS selects slightly more false positives than Conditional-INIS, the reason being that in each step Greedy-INIS selects the top variable(s) by fitting the residuals conditional on previously chosen variable set and tends to overfit. However, the coefficient estimates for these false positives are fairly small, hence they do not affect prediction error very much. Regarding computation efficiency, Conditional-INIS performs better in our simulated examples, as it usually only requires two to three iterations, while Greedy-INIS would need at least iterations (here and and respectively for Examples 3 and 4).

5.4 Real Data Analysis on Boston Housing Data

In this section we illustrate the performance of our method through a real data analysis on Boston Housing Data (Harrison and Rubinfeld, 1978). This dataset contains housing data for 506 census tracts of Boston from the 1970 census. Most empirical results for the housing value equation are based on a common specification (Harrison and Rubinfeld, 1978),

where the dependent variable MV is the median value of owner-occupied homes, the independent variables are quantified measurement of its neighborhood whose description can be found in the manual of R package mlbench. The common specification uses and to get a better fit, and for comparison we take these transformed variables as our input variables.

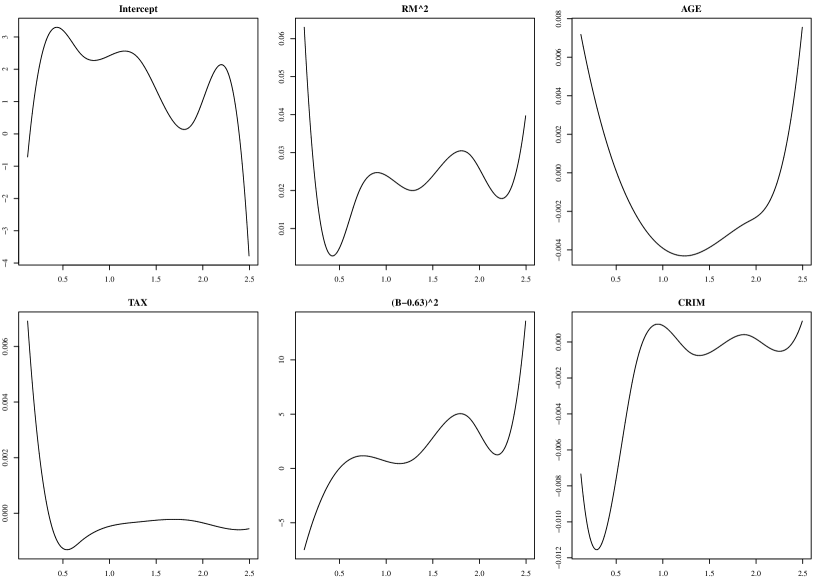

To exploit the power of varying coefficient model, we take the variable , the weighted distances to five employment centers in the Boston region, as the exposure variable. This allows us to examine how the distance to the business hubs interact with other variables. It is reasonable to assume that the impact of other variables on housing price varies with the distance, which is an important characteristic of the neighborhood, i.e. the geographical accessibility to employment. Interestingly, Conditional-INIS selects the following submodel:

| (39) | |||||

where . The estimated functions ’s are presented in Figure 3. This varying coefficient model shows very interesting aspects of housing valuation. The evidence of nonlinear interactions with the accessibility is clearly evidenced. For example, RM is the average number of rooms in owner units, which represents the size of a house. Therefore, the marginal cost of a big house is higher in employment centers where population is concentrated and supply of mansions is limited. The cost per room decreases as one moved away from the business centers and then gradually increases. CRIM is the crime rate in each township, which usually has a negative impact, and from its varying coefficient we see that it is a bigger concern near (demographically more complex) business centers. AGE is the proportion of owner units built prior to 1940, and its varying coefficient has a parabola shape: positive impact on housing values near employment centers and suburb areas, while negative effects in between. NOX (air pollution level) is generally a negative impact, and the impact is larger when the house is near employment centers where air is presumably more polluted than suburb area.

We now evaluate the performance of our INIS method in a high dimensional setting. To accomplish this, let be i.i.d. the standard normal random variables and follow the standard uniform distribution. We then expand the data set by adding the artificial predictors:

Note that are the independent variables in original data set ( here) and the variables are known to be irrelevant to the housing price, though the maximum spurious correlation of these 987 artificial predictors to the housing price is now small. We take , , and randomly select samples as training set, and compute prediction mean squared error (PE) on the rest samples. As a benchmark for comparison, we also do regression fit on directly using SCAD penalty without screening procedure. We repeat times and report the average prediction error and model size, and their robust standard deviation. Since are artificial variables, we also include the number of artificial variables selected by each method as a proxy for false positives. The results are presented in Table 4.

| method | PE | Size | SNV |

|---|---|---|---|

| Conditional-INIS (p = 1000) | |||

| Greedy-INIS (p = 1000) | |||

| SCAD fit (p=12) |

As seen from Table 4, our methods are very effective in filtering noise variables in a high dimensional setting, and can achieve comparable prediction error as if the noise were absent. In conclusion, the proposed INIS methodology is very useful in high-dimensional scientific discoveries, which can select a parsimonious close-to-truth model and reveal interesting relationship between variables, as illustrated in this section.

Acknowledgements

This project was supported by the National Institute of General Medical Sciences of the National Institutes of Health through Grant Numbers R01-GM072611 and R01-GMR01GM100474 and National Science Foundation grant DMS-1206464. The bulk of the research was carried while Yunbei Ma was a postdoctoral fellow at Princeton University.

Appendix

A.1. Properties of B-splines

Our estimation use the B-spline basis, which have the following properties (de Boor 1978): For each and , and for . In addition, there exist positive constants and such that for any ,

| (40) |

Then under condition (iii), there exist positive constants and such that for ,

| (41) |

where and .

Furthermore, under condition (iii), it follows from (40) that for any such that ,

Or equivalently,

| (42) |

A.2. Technical Lemmas

Some technical lemmas needed for our main results are shown as follows. Lemma 1 and Lemma 2 give some characterization of exponential tails , which becomes handy in our proof. Lemma 3 and Lemma 4 is a Bernstein type inequality.

Lemma 1

Let , be random variables. Suppose has a conditional exponential tail: for all and uniformly on the compact support of , where and . Then for all ,

| (43) |

Proof. Recall that for any non-negative random variable , . Then we have

The lemma follows from the fact .

Lemma 2

Let , and be random variables. Suppose that there exist , and , such that , and

for all and uniformly on . Then for some and ,

| (44) |

for all and uniformly on .

Proof. For any , let and . Then uniformly on , we have

Let and . It can be shown that is increasing when . Hence when , which implies when ,

On the other hand, when ,

Lemma 2 holds.

Lemma 3

(Bernstein inequality, lemma 2.2.11, van der Vaart and Wellner (1996)). For independent random variables with mean zero such that for every (and all ) and some constants and . Then

for .

Lemma 4

(Bernstein’s inequality, lemma 2.2.9, van der Vaart and Wellner (1996)). For independent random variables with bounded range and mean zero,

for .

The following lemmas are needed for the proof of Theorem 1.

Lemma 5

Suppose conditions (i) and (iii)-(vi) hold. For any , there exist some positive constants and such that for , ,

and

Proof. Recall . Let and . Then

We first bound . Note that for each and , are a sequence of independent random variables with mean zero. By condition (v), (41), and Lemmas 1 and 2, we have for every , there exists a constant , such that

| (45) | |||||

where the first inequality comes from the Minkowski inequality. Hence, it follows from Lemma 3 that for any ,

| (46) |

Next we bound . Again ’s are centered independent random variables. By conditions (v)-(vi), (41), and Lemmas 1 and 2, we have for every , there exists a constant , such that

Thus, according to Lemma 3,

| (47) |

Similarly, we can show that

| (48) | |||||

and

| (49) |

Let and . Then, the combination of (46) - (49) by union bound of probability yields the desired result.

Lemma 6

Under conditions (i), (iii) and (v), there exist positive constants and , such that for ,

| (50) |

Proof. Recall that . For any such that ,

Consider eigenvalues and () of the middle matrix on the right hand side of the equation above, we have (trace) and (determinant). Therefore, by Lemma 1

and by assumption (i)

Using the above two bounds on the minimum and maximum eigenvalues, we have

By (42), we have

Take and , result follows.

Throughout the rest of the proof, for any matrix A, let be the operator norm and be the infinity norm.

Lemma 7

Suppose conditions (i), (iii) and (v) hold. For any and , there exist some positive constants and such that

and

In addition, for any given positive constant , there exists some positive constant such that

and for any positive constant , there exists some positive constant such that

Proof. Observe that for

where , and Then

| (53) | |||||

We first bound . Recall that on , so

for all and By (41),

By Lemma 4, we have

It then follows from the union bound of probability that

| (54) |

We next bound . Note that for ,

where Lemma 1 was used in the last inequality. By Lemma 3, we have

It then follows from the union bound of probability that

| (55) |

Similarly we can bound . For every , for , there exists a constant such that

By Lemma 3, we have

It then follows from the union bound of probability that

| (56) |

We next prove the second part of the lemma. Note that for any symmetric matrices A and B (Fan, Feng and Song, 2011),

| (59) |

It then follows from (59) that

which implies that

| (60) | |||||

Let in (60) for . According to (50), we have

| (61) | |||||

for some positive constant . Next observe the fact that for and ,

This is because is equivalent to , or ; on the other hand, implies as , and therefore . Then let , it follows from (61) that

| (62) | |||||

Following the same proof, by (42) we also have for any positive constant , there exists some positive constant , such that

| (63) | |||||

The second part of the lemma then follows from the fact that for any symmetric matrix A, .

A.3. Proof of Main Results

Proof of Proposition 1.

Note that .

By Stone (1982), there exist and such that and , where is the space of polynomial splines of degree with normalized B-spline basis , and is some positive constant. Here denotes the sup norm. Let and be -dimensional vectors such that for and .

Recall that and .

By definition of and , we have

and therefore . In other words,

On the other hand, by the least-squares property,

and by conditioning in and , we have

The last two equalities imply that

Thus, by the Pythagorean theorem, we have

and

| (64) |

Similary, we have

| (65) |

By taking (c.f. Lemma 1), the first part of Proposition 1 follows from (64) and (65):

| (66) | |||||

Then the desired result follows from for some .

We first focus on . Let , , and . Then

Denote the last three terms respectively by , , and .

We first deal with . Note that

| (67) |

By Lemma 5 and the union bound of probability,

| (68) |

According to the second part of Lemma 7, for any given positive constant , there exists a positive constant such that

Then it follows from (50) that

| (69) |

Combining (67)-(69) and based on the union bound of probability, we have

| (70) | |||||

We next bound . Note that

| (71) |

By Lemma 1,

| (72) | |||||

where the calculation as in (45) was used.

To bound , note that

| (74) |

Then it follows from Lemmas 6, Lemma 7, (69), (72), (74) and the union bound of probability that there exist , and such that

| (75) | |||||

Hence, combining (70), (73) and (75), there exist some positive constants , and such that

| (76) | |||||

Similarly, we can prove that there exist positive constants , and such that

| (77) | |||||

Let for any given (e.g., take ). There exist some positive constants and such that

| (78) | |||||

Then Theorem 1(i) follows from the union bound of probability.

We now prove part (ii). Note that on the event

by Proposition 1, we have

| (79) |

Hence, by choosing , we have . On the other hand, by the union bound of probability, there exist positive constants and , such that

and Theorem 1(2) follows.

Proof of Theorem 2. Let

where is a -dimensional vector of functions. Then we have

where is a -dimension vector with all entries 0. This implies

recalling . It follows from orthogonal decomposition that and (recall the inclusion of the intercept term). Therefore,

and

| (80) |

Note that by the definition of ,

By Lemma 6 and (80), the last term is of order . This implies that the number of cannot exceed for any .

On the set

the number of cannot exceed the number of , which is bounded by . By taking , we have

Then the desired result follows from Theorem 1(i).

References

- Antoniadis and Fan (2001) Antoniadis, A. and Fan, J. (2001). Regularized wavelet approximations (with discussion). Jour. Ameri. Statist. Assoc., 96, 939-967.

- Candes and Tao (2007) Candes, E. and Tao, T. (2007). The Dantzig selector: statistical estimation when is much larger than (with discussion), Ann. Statist., 35, 2313-2404.

- Fan, Feng and Song (2011) Fan, J., Feng, Y. and Song, R. (2011). Nonparametric independence screening in sparse ultra-high-dimensional additive models, J. Am. Statist. Assoc., 106, 544-557.

- Fan and Li (2001) Fan, J. and Li, R. (2001). Variable selection via nonconcave penalized likelihood and its oracle properties, J. Am. Statist. Assoc., 96, 1348-1360.

- Fan and Lv (2008) Fan, J. and Lv, J. (2008). Sure independence screening for ultrahigh dimensional feature space (with discussion), J.Roy. Statisti. Soc. B., 70, 849-911.

- Fan and Song (2010) Fan, J. and Song, R. (2010). Sure independence screening in generalized linear models with NP-dimensionality, Ann. Statist., 38, 3567-3604.

- Fan, Zhang and Zhang (2001) Fan, J., Zhang, C. and Zhang, J. (2001). Generalized likelihood ratio statistics and wilks phenomenon, Ann. Statist., 29, 153-193.

- Fan and Zhang (2008) Fan, J. and Zhang, W. (2008). Statistical methods with varying coefficient models. Stat. Interface., 1, 179-195.

- Frank and Friedman (1993) Frank, I.E. and Friedman, J.H. (1993). A statistical view of some chemometrics regression tools (with discussion), Technometrics, 35, 109-148.

- Hall and Miller (2009) Hall, P. and Miller, H. (2009). Using Generalised Correlation to Effect Variable Selection in Very High Dimensional Problems, J. Comput. Graph. Stat., 18, 533-550.

- Hall, Titterington and Xue (2009) Hall, P., Titterington, D. M. and Xue, J. H. (2009). Tilting methods for assessing the influence of components in a classifier, J.Roy. Statisti. Soc. B., 71, 783-803.

- Harrison and Rubinfeld (1978) Harrison, D. and Rubinfeld, D. (1978). Hedonic housing prices and the demand for clean air, J. Environ. Econ. Manag. 5, 81-102.

- Hastie and Tibshirani (1990) Hastie, T. and Tibshirani, R. (1990). Generalized Additive Models, London: Chapman & Hall.

- Hastie and Tibshirani (1993) Hastie, T. and Tibshirani, R. (1993). Varying-coefficient models. J.Roy. Statisti. Soc. B., 55, 757-796.

- Li, et al. (2012) Li, G, Peng, H., Zhang, J. and Zhu, L. (2012). Robust rank correlation based screening. Ann. Statist., 40, 1846-1877.

- Li, Zhong and Zhu (2012) Li, R., Zhong, W. and Zhu, L. (2012). Feature screening via distance correlation learning. J. Am. Statist. Assoc., to appear.

- Lian (2011) Lian, H. (2011). Flexible shrinkage estimation in high-dimensional varying coefficient models, manuscript.

- Stone (1982) Stone, C.J. (1982). Optimal glaobal rates of convergence for nonparametric regression, Ann. Statist., 10, 1040-1053.

- Tibshirani (1996) Tibshirani, R. (1996). Regression shrinkage and selection via the lasso, J.Roy. Statisti. Soc. B., 58, 267-288.

- van der Vaart and Wellner (1996) van der Vaart, A.W. and Wellner, J.A. (1996). Weak Convergence and Empirical Processes. Springer, New York.

- Vershynin (2011) Vershynin R. (2011). Introduction to the non-asymptotic analysis of random matrices, manuscript.

- Wang, Li and Huang (2008) Wang, L., Li, H., and Huang, J. Z. (2008). Variable selection in nonparametric varying-coefficient models for analysis of repeated measurements. J. Am. Statist. Assoc., 103, 1556-1569.

- Yuan and Lin (2006) Yuan, M. and Lin, Y. (2006). Model selection and estimation in regression with grouped variables. Jour. Roy. Statist. Soc. B, 68, 49-67.

- Zhang (2010) Zhang, C.-H. (2010), Nearly unbiased variable selection under minimax concave penalty, Ann. Statist., 38, 894-942.

- Zhao and Li (2010) Zhao, D. S., and Li, Y. (2010). Principled Sure Independence Screening for Cox Models With Ultra-High-Dimensional Covariates. manuscript, Harvard University.

- Zou (2006) Zou, H. (2006) The adaptive Lasso and its oracle properties, J. Am. Statist. Assoc., 101, 1418-1429.

- Zou and Hastie (2005) Zou, H. and Hastie, T. (2005). Addendum: Regularization and variable selection via the Elastic net, J.Roy. Statisti. Soc. B., 67, 301-320.

- Zou and Li (2008) Zou, H. and Li, R. (2008). One-step sparse estimates in nonconcave penalized likelihood models, Ann. Statist., 36, 1509-1533.