Theory of Performance Participation Strategies

Abstract

The purpose of this article is to introduce, analyze and compare two performance participation methods based on a portfolio consisting of two risky assets: Option-Based Performance Participation (OBPP) and Constant Proportion Performance Participation (CPPP). By generalizing the provided guarantee to a participation in the performance of a second risky underlying, the new strategies allow to cope with well-known problems associated with standard portfolio insurance methods, like e.g. the CPPI cash lock-in. This is especially an issue in times of market crisis. However, the minimum guaranteed portfolio value at the end of the investment horizon is not deterministic anymore, but subject to systematic risk instead. With respect to the comparison of the two strategies, various criteria are applied such as comparison of terminal payoffs and payoff distributions. General analytical expressions for all moments of both performance participation strategies as well as standard OBPI and CPPI are derived. Furthermore, dynamic hedging properties are examined, in particular classical delta hedging.

keywords:

investment strategies, performance participation, CPPP, OBPP, CPPI, OBPI1 Introduction

In this paper we introduce and analyze the class of performance participation strategies. With this respect we define performance participation strategies as financial strategies which are designed to provide a minimum performance in terms of a fraction of the outcome of one risky asset while keeping the potential for profits resulting from the outperformance of another risky asset. Due to this minimum performance feature they can be considered as a generalization of the well-known class of portfolio insurance strategies.

While the provided guarantee is not deterministic anymore but subject to systematic risk instead, these strategies avoid the cash lock-in feature that face standard CPPI methods and thus are able to take advantage of a possible market recovery. After a sharp market drop, like e.g. at the beginning of 2009, the entire risk budget is maybe exhausted and the portfolio fully invested in the cash market afterwards. The defensive portfolio allocation then remains unchanged until the end of the investment horizon (or the next reallocation date) and prohibits to participate in a potential market regeneration. Consequently, the CPPI portfolio will only return the riskless interest rate and the associated costs of insurance significantly diminish the resulting return.

To cope with the above issues we substitute the primary risk-free asset with a second risky investment alternative, also called the reserve asset. This allows to provide even in critical market situations, where standard portfolio insurance approaches tend to fail, a participation in the performance of a risky investment opportunity. In order to minimize the additionally introduced risk one could e.g. think about the minimum variance portfolio as a risky reserve asset, but also riskier alternatives are possible.

In this paper we introduce two different performance participation strategies, one static, option-based approach as well as a dynamic portfolio reallocation rule. With respect to the former we pick up the among practitioners very popular Best of Two111Note that the name ’Best of Two’ is registered by the Conrad Hinrich Donner Private Bank (see Vitt and Leifeld (2005)). (Bo2) strategy. It was first introduced by Dichtl and Schlenger (2002) and mainly relies on the concept of so-called exchange options. An exchange option written on a pair of risky assets and gives the option holder the right to exchange at maturity the performance of one asset against the other.222See, e.g., Margrabe (1978) for details. Thus, by setting up a static portfolio consisting of an adequate number of shares of one of the risky assets and the same number of exchange options written on the second risky asset the investor will receive at the end of the investment period the return (except for strategy costs) of the better performing asset during the observation horizon. In this way, by guaranteeing a performance participation in one of the risky assets serious portfolio losses can be narrowed, while keeping the potential of full participation in rising markets. The based-upon OBPP (Option-Based Performance Participation) constitutes a generalization of the Best of Two concept to provide general investor-defined levels of performance participation. A similar approach was already mentioned in Lindset (2004) within the context of relative guarantees for life insurance contracts or pension plans.

With respect to the latter dynamic approach we rely on the for portfolio insurance purposes well-established CPPI concept. In their seminal papers Black and Jones (1987) as well as Black and Perold (1992) originally introduced the CPPI approach on a portfolio consisting of two risky assets, i.e. with stochastic floor. Nevertheless, in a wide range of the literature in the field of portfolio insurance strategies the CPPI investment rule is restricted to a constant, deterministic interest rate and one risky asset. In this paper we pick up Black and Perold (1992)’s original idea to define the CPPP (Constant Proportion Performance Participation) strategy as a dynamic approach to performance participation. In analogy to the CPPI concept, the resulting strategy not only guarantees a minimum performance participation in one of the risky assets but also allows for a leveraged participation in the outperformance of a second asset.

Within the scope of this paper we provide a detailed analysis and comparison of the OBPP and the CPPP with respect to various criteria. Although the two strategies were already mentioned in different areas of the financial literature, to the authors’ knowledge no profound theoretical analysis was conducted so far. In the case of the OBPP strategy the literature is scarce: Except for Margrabe (1978)’s basic paper about the evaluation of exchange options, there only exist some empirical performance reviews with a focus on the practical application of the Bo2 strategy, like e.g. the works of Dichtl and Schlenger (2002, 2003) and Vitt and Leifeld (2005) and more popular articles in practicioners’ journals. With respect to the CPPP strategy, as mentioned earlier, the basic literature like e.g. Black and Jones (1987), (Black and Rouhani, 1989) or (Bertrand and Prigent, 2005), mainly restricts to the one-dimensional case with one risky asset and a risk-free interest rate.

We therefore first of all provide a formalized and unified definition of the two performance participation strategies. This enables us to establish a very important relationship between standard portfolio insurance and more general performance participation strategies. Based on that finding, generalized analytical expressions for all moments of the payoff distributions of the standard portfolio insurance strategies as well as the built-upon performance participation strategies are derived. The subsequent analysis is conducted in the spirit of (Black and Rouhani, 1989) and Bertrand and Prigent (2005) for portfolio insurance strategies.

The remainder of this paper is organized as follows: In Section 2, we briefly introduce and discuss the two performance participation strategies under consideration. We examine their final payoffs and show that the newly introduced strategies can be directly linked to the standard CPPI and the standard OBPI method. A detailed analytical analysis of the moments of the resulting payoff distributions is conducted in Section 3. With regard to the practical implementation Section 4 especially covers the dynamic behavior of the two strategies. To conclude the analysis, Section 5 summarizes the main findings and gives some concluding remarks.

2 Definition of the OBPP and the CPPP Strategy

2.1 Financial market setup

With respect to the theoretical analysis of the two performance participation strategies we define a two-dimensional Black-Scholes model on the filtered probability space . The financial market thus offers three investment possibilities: two risky assets , and a riskless cash account that are traded continuously in time during the investment period . Within the context of performance participation strategies the time horizon is regarded as the time horizon for the provided participation. The risk-free asset grows with constant continuous interest rate , i.e. . The evolution of the remaining two assets, such as a stock, stock portfolio or market index, is subject to systematic risk and the corresponding price process of stock is modeled by the geometric Brownian motion

| (1) |

Here, denotes a standard two-dimensional Brownian motion with respect to the real-world measure and the Brownian filtration . The constant matrices and with

describe the drifts, the volatilities and the correlations of the asset prices, where we assume and . Due to these risk-return characteristics now and in the following we will call asset the reserve asset and the riskier asset the active asset.333Note that this notation was already used in the early papers of Black and Jones (1987) and Black and Perold (1992). Furthermore, in order to eliminate any arbitrage opportunities the matrix has to be regular inducing . The two risky underlyings are thus not perfectly correlated with each other and the resulting log-returns are bivariately normally distributed subject to

and variance-covariance matrix

Within the scope of this paper we restrict ourselves to self-financing strategies, that is strategies where money is neither injected nor withdrawn from the portfolio during the trading period . Moreover, we are focussing on performance participation strategies that are built on the two risky assets , only. Following Black and Scholes (1973) the underlying market is assumed to provide the usual perfect market conditions including no arbitrage and completeness.444See, e.g., Black and Scholes (1973) or Shreve (2008).

As introduced in Section 1, performance participation strategies are investment strategies built on the two risky assets , that provide a minimum performance in terms of a fraction of the outcome of the reserve asset while keeping the potential for profits resulting from the outperformance of the active asset . To facilitate a return perspective now and in the following we assume w.l.o.g. that the initial values of both risky underlyings equal the initial portfolio value , i.e.

The next sections provide a formalized and unified definition of the two performance participation strategies. We start with the definition of the OBPP strategy as a static example of a performance participation trading rule.

2.2 The Option-Based Performance Participation (OBPP) strategy

The Option-Based Performance Participation (OBPP) strategy generates the desired participation with the aid of exchange options. An exchange option gives the option holder the right to exchange at its expiry one risky asset for another. Margrabe (1978) was the first to introduce and develop an equation for the value of an exchange option. Let denote the terminal trading date. The minimum terminal wealth which must be achieved is given by the fraction of the performance of the reserve asset at maturity , i.e.

| (2) |

In analogy to standard portfolio insurance strategies we denote the current value of the (stochastic) performance participation the floor.

Thus, purchasing at inception an adequate number of shares of the active asset and one exchange option written on shares of the reserve asset and shares of , respectively, enables the desired performance participation. Note that the dampening factor is related to the value of the exchange option and thus reflects the costs of the desired performance guarantee. It will be analyzed in more detail later on.

More precisely, given the payoff of the exchange option at maturity

| (3) |

the obtained terminal portfolio value of the OBPP strategy then yields

| (4) | ||||

| (5) |

Hence, additionally to the guaranteed wealth a participation - at a percentage - in the outperformance of the active asset is possible. The obtained payoff is the maximum of the stochastic floor and the down-scaled performance of the active asset . Thus, within the context of the OBPP strategy the purchased exchange option can be interpreted as a protecting put option with stochastic strike .555Note that Margrabe (1978) was the first to use this interpretation. Following from put-call-parity for exchange options666See Margrabe (1978). the portfolio setup (4) is furthermore equivalent to holding the stochastic floor plus the exchange option that gives the option holder at its maturity the right to exchange shares of the reserve asset against shares of the active asset . With this respect, the exchange option plays the role of a call option written on the scaled underlying with stochastic strike .

The percentage of the active asset is derived in such a way to match the investor’s initial endowment and insurance needs . More precisely, at inception the initial capital is adequately split to purchase both shares of representing the stochastic floor and the protecting exchange option . This implies the condition777Note that Equation (6) can be solved for the adequate percentage using standard zero search methods like, e.g., the Newton gradient method. Furthermore, it only possesses a solution in if we assume . This solution will be unique as the value of the exchange option and thus the initial OBPP portfolio value are strictly monotone in . In case that and substituting Equation (6) yields and there will be no solution.

| (6) |

Note that since the value of the exchange option is always positive, the put-call-parity for exchange options directly induces the upper bound .

The OBPP is designed as a static investment strategy.888Note that in practice the underlying exchange option will usually be dynamically replicated. This synthesized OBPP represents a dynamic strategy as well. For further details we refer the interested reader to Section 4. Hence, once allocated the portfolio constitution remains unchanged during the investment period . By applying Margrabe (1978)’s formula for the price of the exchange option the current value of the OBPP portfolio at any time is given by

| (7) |

where

| (8) |

and

| (9) | ||||

| (10) |

Here, denotes the cumulative distribution function of the standard normal distribution. The constant given by

| (11) |

is the volatility of the ratio process999See (Margrabe, 1978) or later on Remark 2. . Since it is a decreasing function in the correlation , the protecting exchange option is the cheaper the higher the correlation between the two underlyings. A high correlation signifies a likewise simultaneous evolution of the risky assets. Thus, the probability that the option will be executed at maturity is reduced.

Note that since the value of the exchange option is always positive, for all dates the portfolio value is actually always above the floor . The desired minimum performance participation is thus not only provided at the terminal date but also on an intertemporal basis. Furthermore, the portfolio weights of the corresponding replicating strategy are always smaller or equal to one. The OBPP strategy is thus leveraging neither of the two underlyings. As we will see in the sequel, this is one of the main differences between the two performance participation strategies under consideration.

As we have mentioned above, the constant represents the diffusion of the process , which we denote now and in the following by . With respect to that asset ratio, also called the index ratio101010The notation goes back to (Black and Perold, 1992)., we can establish a very important relationship between the newly introduced OBPP and the standard OBPI strategy.

Lemma 1 (OBPP and OBPI value).

Given the financial market defined in (1) and the risky asset . Furthermore, let denote the horizon of the desired insurance level in terms of the initial endowment of a standard OBPI strategy, whose current portfolio value at time is given by111111See, e.g., Bertrand and Prigent (2005).

| (12) |

Here, denotes the Black-Scholes value of a vanilla call option at time , with maturity , written on shares of the risky asset with strike , risk-free interest rate and volatility . The number of shares of the risky underlying is adapted to the desired terminal guarantee and the initial endowment via the condition

| (13) |

Then, at any time the OBPP strategy can be represented as a portfolio consisting of shares of a standard OBPI strategy in the discounted market with as numéraire

| (14) |

Note that in the discounted market with as numéraire we thus consider the discounted assets and . Whereas the former is constant, yielding the risk-free interest rate , the later represents the index ratio . The same applies to the initial portfolio value that reduces to . All other parameters remain the same.

Proof.

The relationship can be easily derived by observing that the discounted exchange option with respect to as numéraire is equivalent to a standard vanilla call option written on shares of the risky underlying , with strike and risk-free interest rate . More precisely, let , denote the equivalent martingale measure corresponding to the numéraire . Then, following from the risk-neutral pricing formula and the change of numéraire theorem121212See, e.g., Shreve (2008). we obtain for the value of the exchange option at time

Since the value of a call option only depends on the risk-free interest rate as well as the volatility of the risky asset, yielding and in the discounted market, we conclude that

Overall this leads to131313Note that this equality was already shown in Margrabe (1978) using a different motivation.

| (15) |

Note that due to this discounting property the adequate number of shares is the same for the OBPP and the OBPI.

Hence, the additionally introduced source of risk in terms of a risky reserve asset manifests itself as stochastic numéraire that allows to reduce the newly introduced performance participation strategy to its portfolio insurance equivalent in the discounted asset universe. The stochastic dynamics of the index ratio are provided in the following remark. ∎

Remark 2.

Define the value process of the ratio of the two risky assets . The process is lognormal and given by the geometric Brownian motion

| (16) |

with drift

| (17) |

volatility as defined in Equation (11) and Wiener process

| (18) |

Proof.

The stochastic dynamics follow directly from Itô’s lemma and the one-dimensional Lévy theorem.141414See, e.g., Shreve (2008). ∎

To conclude the section we analyze the additional scaling factor in more detail. As mentioned earlier, it is necessary to provide arbitrary investor-specific levels of performance participation . The OBPP is thus a generalization of the earlier mentioned Best of Two strategy

that (except for the factor ) returns the better performing underlying at the end of the investment horizon . It corresponds to the special case of the OBPP where . Note that the factor cannot be omitted and is necessary to adjust the portfolio allocation to the prespecified initial endowment .

With respect to arbitrary participation levels the percentage is a decreasing function of . For this purpose we recall the initial endowment Condition (6)

or following from put-call-parity for exchange options equivalently

where the left-hand side is decreasing in whereas the value of the exchange option is increasing in and decreasing in , respectively.

Note that in the special case where the reserve asset is given by a zero-coupon bond with face value , i.e. , the exchange option with risk-free asset reduces to a standard vanilla call option written on with strike , i.e.151515See Margrabe (1978).

The OBPP strategy with level of performance participation then represents a standard OBPI strategy with respect to the deterministic insurance level .

In the next section we will elaborate on Black and Perold (1992)’s idea of a CPPI strategy defined on a portfolio consisting of two risky assets. Since their original approach to portfolio insurance with a risky reserve asset is not widely spread in the literature we will redefine it as a dynamic approach to the more general class of performance participation strategies. Furthermore, the name will be adapted to cope with the more general performance participation feature.

2.3 The Constant Proportion Performance Participation (CPPP) strategy

Similar to the OBPP strategy the Constant Proportion Performance Participation (CPPP) strategy aims at providing a minimum return participation in the reserve asset while benefiting from an outperformance of the active asset . This is achieved by applying the CPPI investment rules to a portfolio consisting of two risky assets. In contrast to the OBPP strategy the CPPP represents a dynamic strategy since the portfolio is continuously reallocated over time. Furthermore, the applied allocation rules even allow for a leveraged participation in .

Let again denote the minimum investor-defined level of performance participation in the risky reserve asset that defines the portfolio floor , i.e.

This minimum portfolio value has to be achieved not only at the end of the investment horizon but at any time Furthermore, we define at time the cushion as the excess portfolio value with respect to the current floor

Note that the requirement of a positive initial cushion , where , establishes the natural bound on the level of performance participation. In order to ensure the required floor at any time the basic idea of the CPPP method now consists in analogy to the standard CPPI strategy in investing a constant proportion of the cushion in the active asset . This is the reason why we call the strategy constant proportion performance participation. The remaining part of the portfolio is invested in the reserve asset . More precisely, the exposures and to the active and the reserve asset , , respectively, at time are determined by

The constant multiplier affects the participation in the (out)performance of asset and the potential leverage effect with respect to . In general, the strategy is well-defined for any . However, we will restrict to the more interesting case when the payoff function is convex in the value of the active asset .

In their seminal paper Black and Perold (1992) already derive the value of the CPPP portfolio by establishing a similar relationship with the standard CPPI strategy as it is the case for OBPP and OBPI according to Equation (14).

Lemma 3 (CPPP and CPPI value).

Given the financial market defined in (1) and the risky asset . Furthermore, let denote the horizon of the desired insurance level in terms of the initial endowment of a standard CPPI strategy with multiplier , whose current portfolio value at time is given by161616See, e.g., Perold et al. (1988).

| (19) | ||||

with the non-negative function defined as

Then, at any time the CPPP strategy can be represented as a portfolio consisting of shares of a standard CPPI strategy in the discounted market with as numéraire

| (20) |

where and . All other parameters remain the same. More precisely, the current CPPP portfolio value is calculated as

| (21) | ||||

where .

Proof.

Recall that a change of numéraire does not affect the underlying self-financing CPPP investment rule.171717See, e.g., Shreve (2008). Thus, the number of shares allocated of asset , at time in the original (denoted by ) and the discounted CPPP portfolio181818Note that for clearness we sometimes omit the detailed declaration of all parameters of the performance participation strategy PP and simply denote the current portfolio value by . (denoted by ) are the same and yield

This can be further transformed to

which actually represents a standard CPPI strategy with respect to the risk-free interest rate and the index ratio .191919Note that this relationship was already stated in Black and Perold (1992). Equation (21) then follows directly from (20) by substituting , , , and in (19). ∎

Remark 4 (Cushion dynamics).

The cushion process of the CPPP is lognormal and given by

| (22) |

with mean rate of return and volatility

| (23) | ||||

| (24) |

Proof.

The stochastic dynamics of follow by application of Itô’s lemma and the one-dimensional Lévy theorem. ∎

Hence, similar to the OBPP, the additional source of risk in terms of a risky reserve asset manifests itself as stochastic numéraire that allows to reduce the newly introduced performance participation strategy to its portfolio insurance equivalent in the discounted asset universe. In the sequel the derived relationships (14) and (20) will be very useful for the analysis of the characteristics of the two performance participation strategies. Especially with respect to the moments of the resulting payoff distributions as well as the dynamic behavior it allows to perform most of the examinations in terms of the standard portfolio insurance strategies in the reduced discounted market framework. The main benefit being that the latter strategies have already been extensively studied from an analytical point of view.202020See, e.g., Black and Rouhani (1989), Black and Perold (1992), Bertrand and Prigent (2005) or Zagst and Kraus (2009).

Equation (21) represents the basic properties of the CPPP. At any time the value of the strategy consists of the current value of the guarantee and the strictly positive cushion which is proportional to and . Thus, the CPPP value always lies strictly above the dynamically insured floor . Furthermore, the CPPP value process is path independent.

In contrast to the OBPP approach the CPPP includes an additional degree of freedom which is introduced by the multiplier . The payoff above the stochastic guarantee, i.e. the cushion, is linear in for and it is convex in (and ) for . In the latter case the resulting exposure to the active asset is likely to exceed the actual portfolio value. This is due to the leveraging effect associated with . The exposure to asset is then financed by short-selling the reserve asset .

Note that in the special case when the reserve asset is given by a zero-coupon bond with face value , i.e. , the CPPP strategy with level of performance participation reduces to a standard CPPI strategy with respect to the deterministic insurance level .

In what follows we compare the two performance participation strategies with respect to various criteria including moments as well as the dynamic behavior.

3 Comparison of the Payoff Distributions

In order to compare the two methods we retain the assumption that the initial portfolio values are the same and equal the initial asset prices, i.e.

Furthermore, the two strategies are supposed to provide the same participation in the performance of the reserve asset . Hence,

in the case of the CPPP strategy and the adequate number of shares of the OBPP strategy is derived from Condition (6)

Note that these two conditions do not impose any constraint on the multiplier as the second parameter of the CPPP strategy. In what follows, this leads us to consider CPPP strategies for various values of the multiplier; Among them the unique value which complies with equality of payoff expectations as an additional condition (see Section 3.2.2 for details). We start with the analysis of the payoff functions of both strategies.

3.1 Comparison of the payoff functions

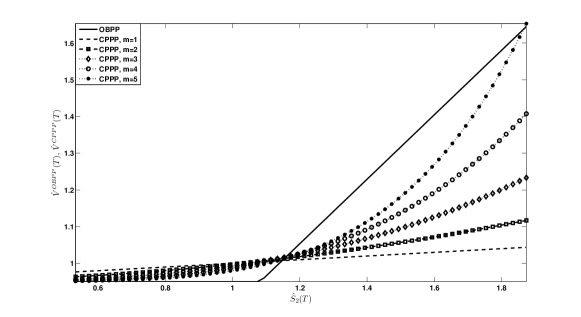

In the simplest case one of the payoff functions of the two methods would statewisely dominate the other one. More precisely, this implies that one of the portfolio values always lies above the other one for all terminal values , . However, since and due to the absence of arbitrage this is not possible.212121See Black and Rouhani (1989).

Lemma 5.

Neither of the two payoffs is greater than the other one for all terminal values , of the underlying risky assets. The two payoff functions thus intersect one another.

Proof.

Figure 1 illustrates this finding using a simple numerical example with typical values for the financial market presented in Table 1.222222The asset characteristics were obtained from monthly return data of the JP Morgan EMU Government Bond Index and the Dow Jones Eurostoxx 50 Index over the time period 01/1995-10/2009. Furthermore, the adequate number of shares and exchange options corresponding to the initial endowment and an investor-defined level of performance participation are provided. If not mentioned otherwise, now and in the following we will consider this setting as our reference model scenario for numerical calculations.

| Market parameters | Reserve asset | Active asset | Strategy parameters | |

|---|---|---|---|---|

| 6.6% | 9.7% | 100 | ||

| 3.7% | 21.4% | 1 (year) | ||

| -0.15 | 0.95 | |||

| 22.3% | 0.8780 | |||

The graph visualizes the strategy payoffs according to (14) and (20) as functions of the terminal index ratio , i.e. the standard OBPI and CPPI in the discounted market. With respect to the CPPP strategy different values of the multiplier are analyzed. For each value of the multiplier the payoffs intersect at least once. The CPPP payoff exceeds the OBPP one not only for very large values of the index ratio but also for the more important range of moderate outperformance and even underperformance of the active asset with respect to the reserve asset. For it is a linear and for an exponential function of . As the value of the multiplier increases, the CPPP portfolio value becomes more convex in . In contrast, the OBPP payoff is a (piecewise) linear function of the terminal index ratio.

The examination of the terminal performances is only a first step within the scope of a comparison of the two strategies. However, a detailed analysis must also take into account the entire payoff distributions - including the probabilities of bullish and bearish markets. In the sequel we will thus derive explicit formulas for the moments of the resulting distributions. This enables us to extend the analysis especially to the first four moments.

3.2 Comparison of the moments of the payoff distributions

3.2.1 Moments of the CPPP and the OBPP strategy

To derive explicit formulas for the moments of the payoff distributions of the OBPP and the CPPP we will make use of the similarity of performance participation and portfolio insurance strategies according to (14) and (20). As a byproduct we obtain general formulas for the moments of the standard OBPI and CPPI, too.

Lemma 6.

Let denote the portfolio value of the OBPP or the CPPP strategy at time and the respective value of the corresponding portfolio insurance strategy in the discounted market according to (14) and (20). Then, the th moment , of the performance participation strategy PP with respect to the real-world measure can be calculated as

| (25) |

where denotes the th moment of the associated portfolio insurance strategy with respect to the equivalent probability measure defined by the Radon-Nikodym derivative232323See, e.g., Shreve (2008).

| (26) |

and

| (27) |

Proof.

The proof is given in A. ∎

Thus, similar to the portfolio values themselves the moments of the payoff distributions of the performance participation strategies are directly linked to the moments of the corresponding portfolio insurance strategies in the discounted market. However, an additional change of probability measure has to be conducted.

In the following, we generally derive the th moments of the payoffs of a standard OBPI and CPPI strategy. Note that the calculation of the expected value as well as the variance was e.g. already proceeded in Bertrand and Prigent (2005) (expectation only) or Zagst and Kraus (2009). We start with the CPPI.

Proposition 7 (CPPI moments).

The th moment, , of a standard CPPI portfolio with level of insurance and multiplier at any time is given by

| (28) |

Proof.

The proof is given in B. ∎

A more sophisticated calculation leads to the following general analytic expression for the moments of the OBPI payoff distribution.

Theorem 8 (OBPI moments).

The th moment, , of the payoff of a standard OBPI strategy with level of portfolio insurance at maturity is given by

| (29) | |||

where

| (30) |

Proof.

The proof is provided in C. ∎

According to Lemma 6 the th moments of the performance participation strategies follow from the th moments of the corresponding portfolio insurance strategies with respect to the equivalent probability measure in the discounted market. The corresponding asset characteristics are provided in the following remark.

Remark 9.

The stochastic dynamics of the index ratio with respect to the equivalent probability measure , defined in Equation (26) are given by

| (31) |

with drift

| (32) |

diffusion as defined in Equation (11) and Wiener process

| (33) |

The risk-free interest rate remains the same under the change of probability measure.

Proof.

The stochastic dynamics of under the real-world measure are given in Remark 2. Then, following from the Girsanov theorem242424See, e.g., (Shreve, 2008). the stochastic process , defined by

| (34) | ||||

| (35) |

is a two-dimensional Brownian motion under the equivalent probability measure , . Substituting (34) and (35) in (16) proves the proposition.252525Note that following from the Lévy theorem is again a Brownian motion. ∎

The moments of the CPPP and the OBPP strategy are then finally derived.

Lemma 10 (CPPP moments).

The th moment, , of a CPPP portfolio with level of performance participation and multiplier at any time is given by

| (36) |

where , and as defined above.

Lemma 11 (OBPP moments).

The th moment, , of the payoff of an OBPP strategy with level of performance participation at maturity is given by

| (37) | |||

where

| (38) |

With the above general expressions for the th moments we have all the essential information to describe the entire payoff distributions of the two performance participation (portfolio insurance) strategies. The usually reported central moments are obtained by a final transformation.

Remark 12 (Central moments).

By applying the binomial theorem the th central moment of a random variable follows directly from its th moment , by

| (39) |

In the sequel we will especially compare the first four (central) moments of the payoff distributions of the two performance participation strategies in more detail. We start with the expected strategy payoffs. As mentioned earlier, with respect to the CPPP strategy we will analyze various values of the multiplier , among them the unique value for which the expectations of the two strategies are equal. Its derivation and analysis is the focus of the following section.

3.2.2 Equality of payoff expectations

The expected payoffs of the CPPP and the OBPP follow directly from Lemma 10 and Lemma 11 as the first moments of the resulting terminal portfolio value distributions

| (40) | ||||

| (41) | ||||

where and , as defined in (38).

The expected payoff of the CPPP strategy is independent of the variance-covariance structure of the underlying risky assets. Thus, the expected return is not affected by the additional source of risk. Moreover, it is an exponentially growing function in the value of the multiplier if and only if the further condition is satisfied. Since the multiplier controls the exposure to the active asset this is a natural expectation from the CPPP payoff sensitivity and justifies our initial assumption made in Section 2.1. In contrast, an increase in the desired level of performance participation (exponentially) reduces the expected payoff (in case that ). The enhanced participation guarantee in the reserve asset comes at the price of a diminished cushion and thus less upside potential stemming from a potential outperformance of the active asset .

With respect to the expected payoff of the OBPP strategy we observe an analog sensitivity on the fraction . As motivated in Section 2.2 an increase in is accompanied by a decrease in the number of shares/exchange options .

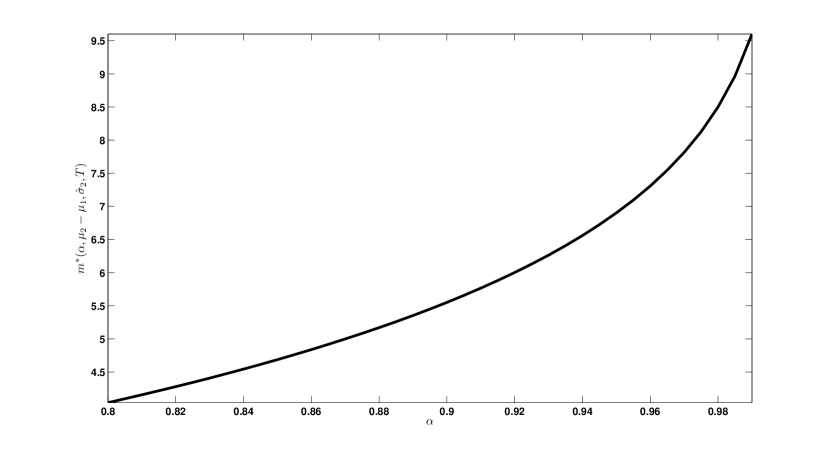

Lemma 13 (Multiplier ).

For any parameterization of the financial market (1) and any level of performance participation there exists a unique value of the multiplier such that

which is given by

| (42) |

Here, denotes the Black-Scholes value of a vanilla call option written on shares of asset with strike , risk-free interest rate , volatility , evaluated at time for maturity .

Proof.

Following from (14) and (20) the problem can be reduced to the equivalent problem for the standard portfolio insurance strategies in the discounted world and with respect to the equivalent probability measure , i.e.

where and . The stochastic dynamics of with respect to are provided in (31). This issue was already solved in Bertrand and Prigent (2005) yielding the proposed multiplier . ∎

Note that since and thus the value of the multiplier is always bigger than one. For any value of the multiplier the expected payoff of the CPPP strategy exceeds that of the OBPP strategy and vice versa.

The special multiplier is an increasing function of the investor-defined level of performance participation . This sensitivity was already motivated in Bertrand and Prigent (2005) for the standard OBPI and CPPI. Although both expected payoffs are decreasing in the fraction the CPPP is usually more sensitive to its variation. This is mainly caused by the leveraging effect of the multiplier that exponentially amplifies the reduction of the cushion.

As an example, Figure 2 visualizes the evolution of as a function of the level of performance participation for the standard case presented in Table 1. With respect to the standard level of performance participation the multiplier according to Equation (42) yields . Note that since the risky reserve asset features a higher drift than the risk-free asset the associated lower excess return will usually induce higher values of the multiplier than it is the case for the standard CPPI strategy.

Furthermore, is a decreasing function in the excess drift . Although both expected values are increasing in the drift difference262626Recall that the rho of Black-Scholes standard vanilla call option is always positive. See, e.g., Hull (2009)., again the CPPP payoff reacts usually more sensitively to a change as it is amplified by the multiplier . Thus, for higher excess drifts a smaller value of is sufficient to maintain an equivalent level of return expectation.

In the next step we include higher (central) moments in our analysis. Since the payoffs under consideration are non-linear a mean-variance approach is not sufficient. This leads us to examine, besides expectation, also standard deviation, skewness and kurtosis.

3.2.3 Comparison of the first four moments

Table 2 provides the obtained values for the expectation (), standard deviation (), skewness () and kurtosis () of the returns of the OBPP and the CPPP strategy in the case of the standard parameterization provided in Table 1. With respect to the CPPP strategy different values of the multiplier are analyzed including the special value . Note that for the sake of simplicity the results are given in a return dimension instead of the usual portfolio value dimension.

| OBPP | CPPP | ||||||

|---|---|---|---|---|---|---|---|

| 8.10% | 7.34% | 7.72% | 7.91% | 8.12% | 8.33% | ||

| 12.37% | 19.92% | 5.02% | 9.58% | 13.92% | 20.74% | 31.84% | |

| 2.3606 | 37.7639 | 1.1672 | 7.6060 | 16.9331 | 41.4930 | 118.2519 | |

| 7.4806 | 1.3912 | 5.3743 | 222.9118 | 1.6409 | 1.7946 | 3.0765 | |

We obtain comparable results as for standard portfolio insurance strategies (see Bertrand and Prigent (2005)). Both strategies generate an asymmetric payoff profile. However, due to the significantly higher positive skewness of the CPPP in comparison to the OBPP, it should be preferred with respect to that criterion. Furthermore, the strategy’s (excess) kurtosis largely exceeds that of the OBPP. This feature is explained by the outperformance of the dynamic strategy in the right tail of the distribution where .

When differing from the special multiplier to consider more general values of , we have to distinguish two situations. If the multiplier is higher than , then the CPPP strategy provides a higher expected payoff than the OBPP. The improved upside potential/intensified participation in the better returning asset is not for free and comes at the price of more risk, i.e. an increasing standard deviation. Since the CPPP thus exceeds the risk associated with the OBPP, none of the two strategies dominates the other one in a mean-variance sense.

In contrast, if the multiplier takes smaller values than , then both the expected CPPP payoff as well as the strategy’s standard deviation are decreasing. Thus, the CPPP provides a smaller return expectation than the OBPP. Furthermore, for small negative deviations of with respect to the risk of the OBPP will still remain less than that associated with the CPPP. Consequently the OBPP strictly dominates the CPPP in a mean-variance sense. Nevertheless, for sufficiently large differences both the expected payoff as well as the standard deviation of the CPPP strategy take smaller values than the OBPP ones. Hence, none of the strategies dominates the other one with respect to the mean-variance criterion.

Bertrand and Prigent (2005) further analyze the probability distributions associated with the standard OBPI and the standard CPPI strategy with a special focus on the payoff ratio . Among others they conclude that for usual values of the multiplier the probability that the CPPI outperforms the OBPI at the terminal date is increasing in the level of insurance. As the probability of exercising the call option at maturity decreases with the increasing strike, the upside potential of the OBPI strategy is significantly reduced. Due to the special relationship between performance participation and portfolio insurance strategies following from (14) and (20) this result remains valid for the more general OBPP and CPPP, as

For further details of the analysis we refer the interested reader to Bertrand and Prigent (2005).

In the following we will briefly study the dynamic properties of the two strategies and in particular their "Greeks". Due to the elaborated relationship between performance participation and standard portfolio insurance strategies the analysis can be kept short for sensitivities where the additional source of risk is not of direct interest.

4 The Dynamic Behavior of OBPP and CPPP

With respect to the practical realization of the OBPP strategy, in many situations the use of standardized traded options is not possible. For example, the underlying(s) may be a diversified fund for which no single option is available. Furthermore, the desired investment period may also not coincide with the maturity of a listed option. OTC options, on the other hand, involve several drawbacks like counterparty risk or liquidity problems and raise the question for the fair price of the contingent claim.

In practice, the underlying exchange options are thus usually synthesized by dynamic replication. In the presumed Black-Scholes model (1) the perfect hedging strategy according to the Margrabe formula (8) exists. Based on the induced dynamic hedging rule one can show that the OBPP strategy actually represents a generalized CPPP strategy with time-variable multiplier. Moreover, the study of the derived multiplier allows to quantify the risk exposure associated with the OBPP strategy.

Since in practice the number of rebalancing trades is limited due to the associated transaction costs, the dynamic replication of the exchange option induces hedging risks. This is the reason why we also analyze the hedging properties (i.e. the Greeks) of both methods. Special focus is put on the behavior of the exposures to the two risky underlyings during the investment period.

4.1 OBPP as generalized CPPP

For the CPPP method the multiplier is the key parameter that controls the amount invested in the active asset and the possible leverage associated with it. Moreover, as shown in Section 3.2.1, it directly affects the risk-return ratio of the resulting portfolio. Knowing about the importance of the multiplier, Bertrand and Prigent (2005) were able to show for the standard OBPI strategy the existence of such an "implicit"’ parameter. This finding remains valid for the two-asset OBPP strategy. The respective implicit multiplier for the OBPP is deduced in the following proposition.

Lemma 14 (OBPP multiplier).

The OBPP method is equivalent to a generalized CPPP method with time-variable multiplier given by

| (43) |

where as defined in (9).

Proof.

In analogy to the CPPP strategy the OBPP multiplier is equal to the ratio of the exposure to the active asset and the OBPP cushion. The former is given by the amount invested in asset to replicate the exchange option and the latter by the value of the exchange option itself. In terms of the discounted asset universe, respectively, this is equal to the exposure to to replicate the corresponding call option on the relative asset divided by the OBPI cushion, which is the call value.

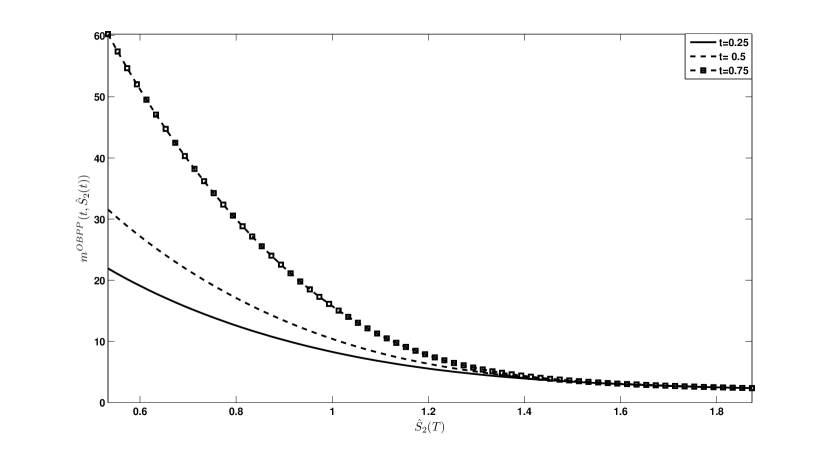

As an example Figure 3 visualizes the OBPP multiplier as a function of the index ratio at time for the case of the standard parameterization provided in Table 1.

Hence, the OBPP multplier is at any time a decreasing function of the index ratio . Furthermore, following from the Margrabe formula (8) it is always bigger than .

It can be easily seen that the OBPP multiplier usually takes higher values than that of standard CPPP strategies, except for the case when the active asset significantly outperforms the reserve asset and the associated exchange or call option, respectively, is thus (deeply) in the money. This is due to the small values of the OBPP cushion, i.e. the value of the exchange option, when the index ratio is small.

The high values of the multiplier involve potential risk when the market drops suddenly: it means that either the OBPP cushion is too small or the exposure to the riskier asset is too high. In contrast, with an increasing outperformance of the active asset over the reserve asset the low values of the multiplier prevent the OBPP portfolio from being overinvested in the riskier asset. Nevertheless, a direct implication of that feature is that in the case of a sustainable outperformance of the active asset over the entire investment period, without any drop, the CPPP strategy will perform better due to the higher active exposure.

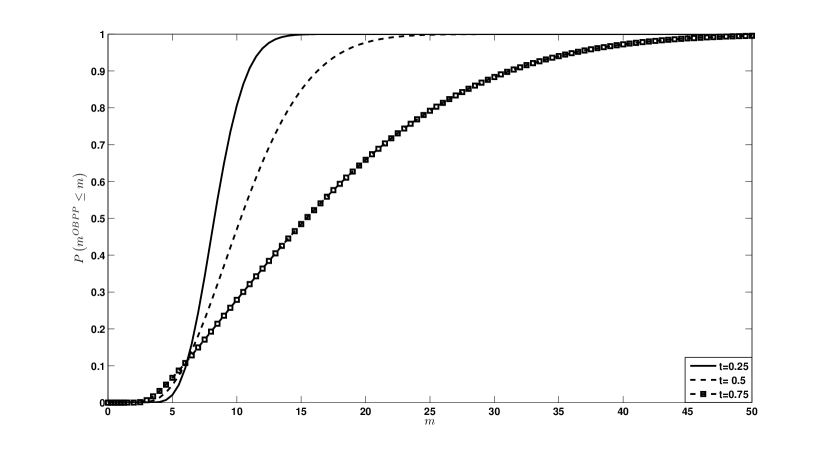

To conclude the analysis of Figure 4 visualizes the evolution of the cumulative distribution function of the OBPP multiplier over time for the standard parameter set provided in Table 1.

As time increases, the probability of obtaining higher values of the OBPP multiplier increases.272727Note that close to maturity of the exchange option (or the corresponding call option in the discounted asset framework) the multiplier is either infinity when the exchange (call) option is not executed, since both the cushion and the exposure are nil. Otherwise converges to . Bertrand and Prigent (2005) argue that this is essentially due to the rise of variance with time.

In the next step we will analyze the Greeks of the OBPP and the CPPP in more detail which represent the dynamic hedging properties of the two performance participation strategies.

4.2 The Greeks of the performance participation strategies

We start with the delta representing one of the main concerns of a portfolio manager.

4.2.1 The delta

Recall that the delta measures the rate of change of the portfolio value with respect to changes in the underlying asset prices. In the case of the OBPP the sensitivities of the strategy performance on the asset performances follow directly from the deltas of the underlying exchange option. An analog calculation as for the derivation of the delta of a vanilla call option yields

The deltas of the OBPP strategy are always positive, smaller (or equal) to one and tend to () and () as the investment horizon approaches its end and (), respectively. In contrast, if the option is at-the-money, i.e. , the deltas converge to and , respectively, as time to maturity approaches zero. This limiting behavior is easy to understand from the payoff structure of the exchange option: as the time to maturity tends to zero the OBPP portfolio is mainly invested in the better performing asset. However, no leveraging is included.

For the CPPP strategy the deltas follow by partial differentiation of the portfolio value (21) as

| (44) | ||||

| (45) |

Whereas similar to the OBPP strategy is always positive, is always smaller than the level of performance participation and especially for high values of the multiplier and a strong outperformance of with respect to likely to take (highly) negative values. Simultaneously, the is then very likely to take significantly higher values than one. The observed sensitivity is due to the convex leveraging feature of the CPPP strategy in the active asset. The strategy value as well as become the more convex in the higher the value of the multiplier . A high stochastic floor in terms of thus significantly reduces the cushion and the overall performance of the strategy. Furthermore, since is a decreasing function in time , is increasing and is decreasing with time.

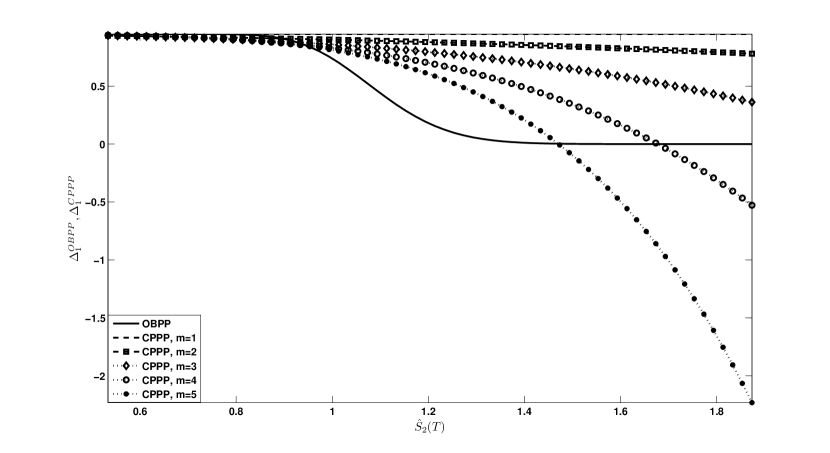

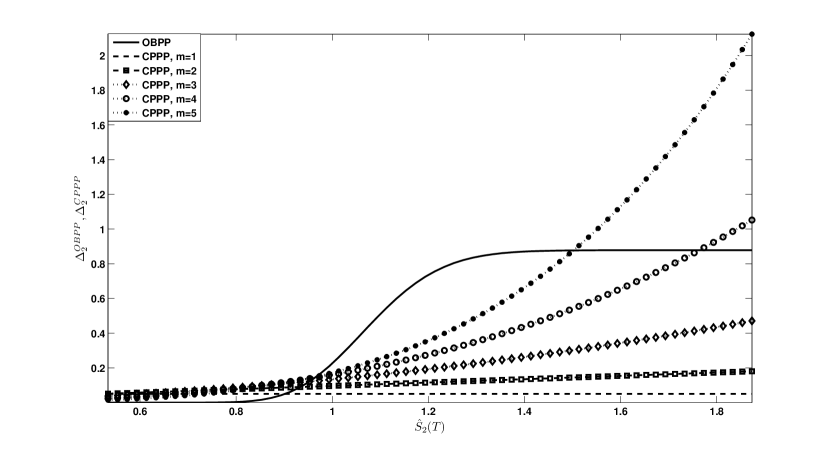

Figure 5 and 6 show the evolution of the deltas of the two performance participation strategies with respect to the reserve asset and the active asset as functions of the index ratio at time . The standard parameter set given in Table 1 is applied. With respect to the CPPP strategy different values of the multiplier are analyzed.

Notice that for moderate , i.e. when the exchange (or the discounted call) option is in-the-money, the OBPP delta with respect to the active asset (with respect to the reserve asset ) is greater (smaller) than that of the CPPP one. This induces a higher risk of the option-based strategy in the case of a sudden market downturn of relative to . In contrast, if the active asset significantly outperforms the reserve asset, i.e. when the option is deeply in-the-money, then the CPPP fall exceeds the OBPP one.

Bertrand and Prigent (2005) analyze the delta of standard portfolio insurance strategies in more detail. In fact, due to the relationship between performance participation and portfolio insurance strategies according to (14) and (20) the deltas of the the OBPP and the CPPP with respect to the active asset are actually equal to the deltas of the corresponding standard portfolio insurance strategies with respect to the discounted underlying

Thus, all results derived by Bertrand and Prigent (2005) remain valid for the generalized performance participation strategies in terms of the index ratio instead of the former risky asset . Among others they show that in probability the CPPP is significantly less sensitive to the ratio than the OBPP.

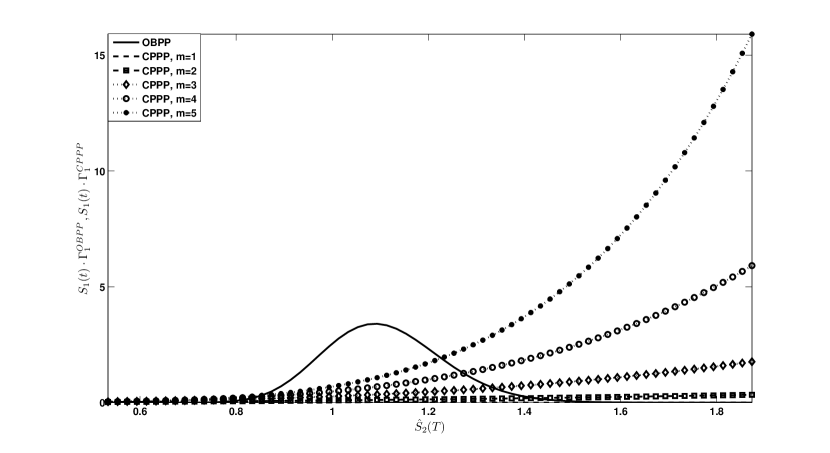

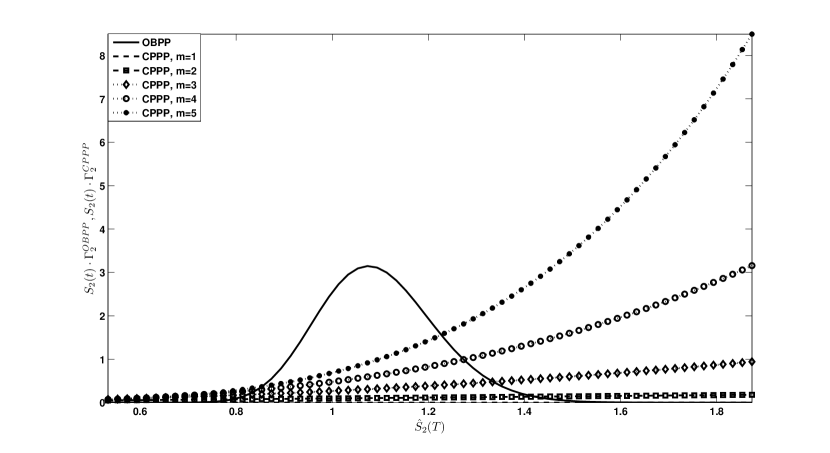

Next we will analyze the gamma of the OBPP and the CPPP that measures the convexity of the portfolio values in the underlying asset prices. It is important to ensure an effective delta hedge.

4.2.2 The gamma

Recall that the gamma measures the rate of change in the delta with respect to changes in the underlying prices. In the case of the OBPP it follows directly from the gamma of the underlying exchange option. An analog calculation to the derivation of a call option’s gamma yields

Hence, the OBPP gammas are always positive and converge - except for the at-the-money-case - to zero as the option approaches its maturity. When the option is at-the-money, i.e. , then , converges to zero and takes the value . Overall, the gammas diverge to infinity in this case.

Analogously, the gammas of the CPPP strategy follow by partial differentiation of the derived deltas (44) and (45) as

Thus, the CPPP gammas are always positive justifying the convex leveraging feature of the strategy.

Figure 7 and 8 visualize the OBPP and the CPPP gammas as a function of the index ratio at time . The standard parameterization provided in Table 1 is applied. With respect to the CPPP different values of the multiplier are analyzed. Note that the common factor or with respect to or , respectively, has been omitted.

With respect to the CPPP strategy the gammas are especially important for very high values of the index ratio . Nevertheless, for the most probable realizations of around one, and especially when the exchange option is in-the-money, the CPPP gamma is smaller than the OBPP one for a large range of values. Furthermore, since is monotonically decreasing in time , the CPPP gammas are decreasing when approaching the end of the investment horizon; yet, they never reach zero. In contrast, with the time to maturity approaching zero the OBPP gammas will converge to zero for an in- or out-of-the money call and diverge if .

To conclude the section we briefly look at the portfolio vegas of the two performance participation strategies under consideration.

4.2.3 The vega

The vega measures the strategy’s sensitivity on the volatility(ies) of the underlying assets. Since both the CPPP and the OBPP portfolio value only depend on the aggregated volatility of the index ratio we restrict our analysis of the vega to this special diffusion. We recall that is a decreasing function in the asset correlation . Furthermore, using the assumption it is increasing in ; with respect to the sensitivity is ambigous.

Due to the special relationship between performance participation and portfolio insurance strategies according to (14) and (20) the vegas of the two strategies follow directly from the vegas of the underlying portfolio insurance strategies in the discounted market. More precisely, we obtain282828See, e.g., Hull (2009) for the call vega and Bertrand and Prigent (2005) for the vega of the CPPI strategy. Note that similar to Bertrand and Prigent (2005) the effect of the volatility on the initial price of the call/exchange option is not taken into account since it only depends on the expected volatility and not on the actual one.

Whereas the vega of the OBPP strategy is always positive, the vega of the CPPP strategy takes negative values for . Thus, an increase in the volatility of the index ratio reduces the actual CPPP portfolio value. The extent of the decrease is the larger the higher the value of the multiplier and the longer the elapsed investment time since inception. If the value of the CPPP strategy is independent on a change in the tracking error . In contrast, the vega of the exchange/call option is positive, since an increase in the volatility increases the probability that the option will be executed at its expiry and thus its price. The closer the investment horizon approaches maturity the smaller is the impact of a change in since .

As an example Figure 9 visualizes the discounted OBPP and CPPP vega as a function of the index ratio at time . The standard model parameterization provided in Table 1 is applied. With respect to the CPPP different values of the multiplier are analyzed.

Table 3 summarizes the described sensitivities of the strategy Greeks with respect to the magnitude of the index ratio .

| OBPP | CPPP | OBPP | CPPP | OBPP | CPPP | ||||

| neg. | neg. | neg. | neg. | ||||||

| pos. | pos. | pos. | pos. | ||||||

| pos. | pos. | pos. | pos. | ||||||

| pos. | pos. | pos. | pos. | ||||||

| pos. | neg. | pos. | neg. | ||||||

Overall, the two portfolios react in a similar way on a change in the value of the index ratio or the associated volatility when the active asset is significantly outperformed by the reserve asset. Thus, neither of the two strategies can be preferred. In contrast, for exceptionally high values of the CPPP strategy requires significantly more hedging effort than the OBPP as it is extremely sensitive on changes in the value of the active asset or the volatility of the index ratio. This sensitivity is even amplified with higher values of the multiplier . Nevertheless, for the most probable realizations of the asset ratio around one, the OBPP appears riskier with respect to a sudden market drop.

To conclude our analysis of the OBPP and the CPPP strategy we summarize the main results and give some concluding remarks.

5 Conclusion

In this paper we have introduced the class of performance participation strategies that guarantee a minimum return in terms of a percentage of a stochastic benchmark while keeping the potential for profits from the outperformance of a second, riskier asset. The new strategy class thus represents a generalization of the well-established portfolio insurance methods where the provided guarantee is not deterministic anymore but subject to systematic risk instead.

Moreover, with the OBPP and the CPPP we have presented a static as well as a dynamic example of a performance participation method that are closely related to the well-known OBPI and CPPI strategy. In fact, we have shown that the two strategy classes can be transformed into each other by discounting with the reserve asset as numéraire. Based on that very important relationship we were able to derive general analytic expressions not only for all of the moments of the payoff distributions of the performance participation strategies but also for the standard OBPI and CPPI method.

In the subsequent analysis we have compared the OBPP and the CPPP with respect to various criteria, including the payoff distributions as well as the dynamic behavior. We conclude that neither of the two strategies generally dominates the other one. This comes from the non-linearity of the payoff functions. Nevertheless, as the investor-defined level of performance participation increases the CPPP strategy seems to be more relevant than the OBPP one. Since the probability of exercising the exchange option at maturity decreases with the desired participation level, the upside potential of the OBPP is significantly reduced.

A concluding analysis of the dynamic behavior of the two strategies showed that the (synthesized) OBPP can actually be considered as a generalized CPPP strategy with time-variable multiplier. Although the OBPP payoff exceeds the CPPP one when the associated exchange option is around or slightly in the money it is more sensitive to drops in the index ratio and to transaction costs. Furthermore, since the OBPP inherent multiplier represents a decreasing function of , especially in the case of constantly rising markets the CPPP is likely to outperform the OBPP.

So far we have restricted our analysis of the OBPP and the CPPP to the comparison of the moments of the payoff distributions as well as the dynamic behavior. However, a detailed analysis should also include investor-specific utility functions and criteria of stochastic dominance which was analyzed for the standard OBPI and CPPI in (Zagst and Kraus, 2009). This will be the subject of further research.

Appendix A Moments (Proof of Lemma 6)

Following from (14) and (20) the current value of the performance participation strategy PP is given by

where is the current value of the associated portfolio insurance strategy in the discounted market with risk-free interest rate and risky asset . Thus, the th moment, yields

where denotes the (unconditional) expectation with respect to the real-world measure . Define for the equivalent probability measure via the Radon-Nikodym derivative292929See, e.g., Shreve (2008).

with

Then, applying the Bayes rule303030See, e.g., Shreve (2008). and substituting the explicit asset price leads to

where , denotes the th moment of the associated portfolio insurance strategy with respect to the equivalent probability measure .

Appendix B Moments of the CPPI strategy (Proof of Theorem 7)

The portfolio value of the CPPI strategy (19) at time is given by

with deterministic floor

and lognormally distributed cushion process

where313131See, e.g., Bertrand and Prigent (2005) or (Zagst and Kraus, 2009).

| (46) | |||||

| (47) | |||||

| (48) | |||||

Hence, by applying the binomial theorem the th moment can be decomposed as

where and denotes the (unconditional) expectation with respect to the real-world measure . Together with

as well as (47) and (48) this finally leads to

Appendix C Moments of the OBPI strategy (Proof of Theorem 8)

The payoff of the OBPI strategy (12) at maturity is given by

Hence, by applying the binomial theorem the th moment can be decomposed as

| (49) |

where , for denotes the th upper partial moment of shares of the terminal asset price with respect to the benchmark . is the (unconditional) expectation with respect to the real-world measure .

Reapplication of the binomial theorem reduces the calculation of to

| (50) | |||

| (51) | |||

The expected value is derived within the scope of the calculation of the fair value of so-called power options.323232See, e.g., (Heynen and Kat, 1996) or (Macovschi and Quittard-Pinon, 2006). It basically consists in a repeated application of the change of probability measure defined in (26). Thus, we obtain for

| (52) | ||||

Hence, substituting (50) and (52) in (49) finally leads to

References

- Bertrand and Prigent [2005] Philippe Bertrand and Jean-Luc Prigent. Portfolio Insurance Strategies : OBPI versus CPPI. Finance, 26(1):5 – 32, 2005.

- Black and Jones [1987] Fischer Black and Robert Jones. Simplifying portfolio insurance. Journal of Portfolio Management, 14(1):48 – 51, 1987. ISSN 00954918. URL http://search.ebscohost.com/login.aspx?direct=true&db=buh&AN=15198743&site=ehost-live.

- Black and Perold [1992] Fischer Black and André F. Perold. Theory of constant proportion portfolio insurance. Journal of Economic Dynamics & Control, 16(3-4):403–426, July-October 1992. ISSN 0165-1889. 10.1016/0165-1889(92)90043-E. URL http://www.sciencedirect.com/science/article/B6V85-45R2GY4-G/2/98ef4a75b7a87bdfeafd4a772771fdfc.

- Black and Rouhani [1989] Fischer Black and R. Rouhani. The Institutional Investor Focus on Investment Management, chapter Constant proportion portfolio insurance and the synthetic put option : a comparison, page 780. Institutional Investor Series in Finance. Ballinger Pub Co, Aug 1989. ISBN 0887302750.

- Black and Scholes [1973] Fischer Black and Myron Scholes. The pricing of options and corporate liabilities. Journal of Political Economy, 81(3):5053921, May-Jun 1973. ISSN 00223808. URL http://search.ebscohost.com/login.aspx?direct=true&db=buh&AN=5053921&site=ehost-live.

- Dichtl and Schlenger [2002] Hubert Dichtl and Christian Schlenger. Aktien oder Renten? - Die Best of Two-Strategie. Die Bank, 1:30–35, 2002. URL http://www.wiso-net.de/webcgi?START=A60&DOKV_DB=ZECU&DOKV_NO=DIBA200201007&DOKV_HS=0&PP=1.

- Dichtl and Schlenger [2003] Hubert Dichtl and Christian Schlenger. Aktien oder Renten? - Das Langfristpotenzial der Best of Two Strategie. Die Bank, 12:809–813, 2003. URL http://www.wiso-net.de/webcgi?START=A60&DOKV_DB=ZECH&DOKV_NO=DIBA2003120279&DOKV_HS=0&PP=1.

- Heynen and Kat [1996] Ronald C. Heynen and Harry M. Kat. Pricing and hedging power options. Asia-Pacific Financial Markets, 3(3):253–261, Sep 1996. ISSN 1387-2834. 10.1007/BF02425804. URL http://www.springerlink.com/content/kp01048x6h223707/.

- Hull [2009] John C Hull. Options, futures, and other derivatives. The Prentice Hall series in finance. Pearson Prentice Hall, Upper Saddle River, NJ, 7. ed. edition, 2009. ISBN 9780136015864. URL http://www.gbv.de/dms/zbw/556635841.pdf.

- Lindset [2004] Snorre Lindset. Relative guarantees. The GENEVA Papers on Risk and Insurance - Theory, 29(2):187–209, Dec 2004. ISSN 0926-4957. 10.1023/B:GEPA.0000046569.76912.0e.

- Macovschi and Quittard-Pinon [2006] Stefan Macovschi and Francois Quittard-Pinon. On the pricing of power and other polynomial options. Journal of Derivatives, 13(4):61–71, 2006. ISSN 10741240. URL http://search.ebscohost.com/login.aspx?direct=true&db=buh&AN=21215788&site=ehost-live.

- Margrabe [1978] William Margrabe. The value of an option to exchange one asset for another. The Journal of Finance, XXXIII(1):177–186, Mar 1978.

- Perold et al. [1988] André F. Perold, , and William F. Sharpe. Dynamic strategies for asset allocation. Financial Analysts Journal, 44(1):16, jan-feb 1988. ISSN 0015198X. URL http://search.ebscohost.com/login.aspx?direct=true&db=buh&AN=6936181&site=ehost-live.

- Shreve [2008] Steven E. Shreve. Stochastic Calculus for Finance II: Continuous-Time Models. Springer FinanceTextbook. Springer, New York, NY, second edition, 2008. ISBN 9780387401010.

- Vitt and Leifeld [2005] Marcus Vitt and Holger Leifeld. Die Portfoliostruktur optimieren. Die Bank, 2:20–23, 2005. URL http://www.wiso-net.de/webcgi?START=A60&DOKV_DB=ZECO&DOKV_NO=DIBA2005020060&DOKV_HS=0&PP=1.

- Zagst and Kraus [2009] Rudi Zagst and Julia Kraus. Stochastic dominance of portfolio insurance strategies - OBPI versus CPPI. Annals of Operations Research, 2009. ISSN 0254-5330. 10.1007/s10479-009-0549-9.