An examination of the effect on the Icelandic Banking System of Verðtryggð Lán (Indexed-Linked Loans).

Abstract

In 1979 following a decade of hyperinflation, Iceland introduced a form of long term lending known as Verðtryggð lán, negatively amortised, index-linked loans whose outstanding principal is increased by the rate of the consumer price inflation index(CPI). These loans subsequently became the primary form of long term lending within Iceland by commercial banks and other institutions.

The loans were part of a general government policy which used indexation to the CPI to address the economic consequences of the hyperinflation. This progressively linked increases in prices, wages and eventually loans directly to the CPI. Although most other forms of indexation were subsequently removed, loan indexation has remained, and these loans now comprise the majority of mortgages in Iceland. Although it is still often argued that index-linked loans helped to stop the hyperinflation, these arguments are typically based on high level macro-economic interpretations of the Icelandic economy, they fail the scientific test of providing specific mechanisms to support their claims. In this paper we take the opposite approach, and present a detailed analysis of the monetary mechanics used for the loans, and their effect on the Icelandic economy, based on a complete model of their interaction within the banking system at the fundamental level of all its transactions - the double entry bookkeeping level.

Based on this analysis there appears to be no evidence or mechanism that would support the claim that index-linked loans reduce or stop inflation. Instead our research shows that the bookkeeping treatment of these loans within the banking system directly contributes to the banking system’s monetary expansion rate, and hence index-linked loans act to increase the inflation rate to which they are linked, rather than reducing it. They consequently create a positive feedback loop within the banking system’s monetary regulation operating directly on the money supply. Our results indicate that the additional monetary expansion caused by these loans has ranged between 4% to 12% per anum over the past 20 years, and continuing excessive inflation can be expected until these loans are removed from the economy. As a consequence borrowers with these loans will find eventual repayment difficult if not impossible. Since the feedback into monetary expansion only occurs at annual CPI rates above approximately 2%, we suggest one solution would be to stabilise the money supply to 0% growth, and we explore some ways this could be achieved by modifying the Basel Regulatory Framework within the Icelandic Banking System.

Introduction

When macro-economic comparisons are made between countries, it is rarely the case that differences in the types of lending, particularly long term lending, are discussed. There are significant differences though. In the United States mortgage lending is predominantly made at a fixed rate for the duration of the loan, while in the United Kingdom long term lending rates are linked to the Bank of England’s rate, and can vary during the loan111Keynesian policy measures that operate directly on the centrally set interest rate consequently have far more immediate effect in their country of origin, than in countries with fixed rate regimes.. In Iceland, as a result of of measures to combat a decade long hyperinflation that followed the collapse of the Bretton Wood’s accord in the 1970’s, the majority of long term lending between 1979-2013 has used an unusual form of financial instrument, the index-linked loan or Verðtryggð lán. These are loans structured with a base fixed interest rate, and an additional component which directly links their outstanding principal to the Consumer Price Inflation index (CPI)222See Appendix A for the calculation formula for these loans..

Indexed linked loans were the predominant form of long term consumer and commercial lending in Iceland between 1980-2008 and are still available today, although they are now competing with variable and fixed rate loans. They are typically structured as 25 or 40 year loans, with a fixed interest rate, and an additional component that increases the outstanding principal of the loan based on the CPI. This latter is structured to negatively amortise over the first half of the loan. As is typical with negatively amortised loans, while the initial repayments are lower than comparable fixed or variable rate loans, the total cost of the loan is considerably higher due to the growth of the outstanding principal during the negatively amortised years of the loan.

Considerable confusion has surrounded the technical aspects of the loans, with particular respect to the calculation of the indexation component, and the associated indexation index which has been modified several times. Historical information on the interest and indexation rates applied to these loans has proved difficult to find, and we draw the reader’s attention to the qualification we must put on the sources used in this paper. In all cases where alternatives exist, we have chosen the most conservative series - and consequently the examples given in this paper may be under-estimates of the actual situation of the debt load imposed by these loans.

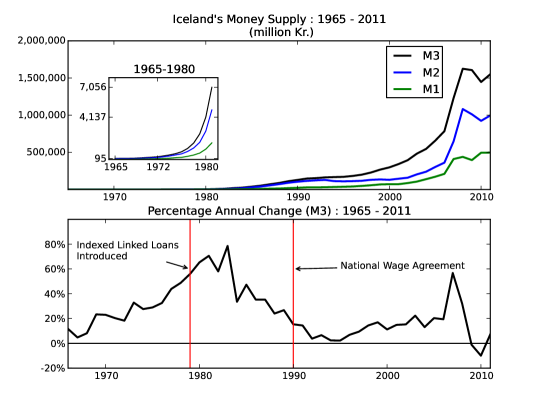

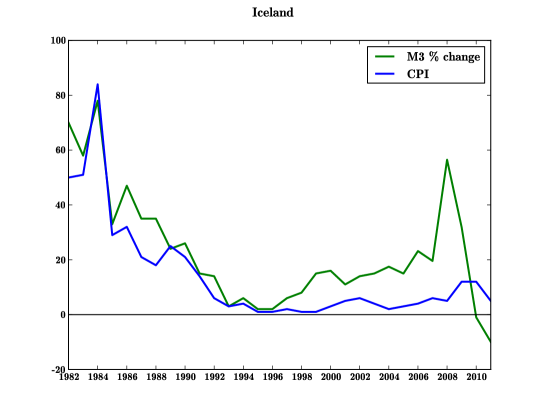

There has also been a long standing question on how these loans interact with the banking system, and in particular its regulatory controls over the money and loan supply. Although it is frequently claimed that they were a key component of efforts to control the hyperinflationary environment in Iceland[1], no specific mechanism has ever been offered to explain this interaction, and the empirical data does not support this claim. As shown in Figure 4, the peak of hyperinflationary monetary expansion in Iceland occurred in 1983, 3 years after the loans were introduced, and the sharp subsequent falls in the monetary expansion rate can be correlated directly with negotiated agreements to suspend wage indexation. This claim is also contradicted by the renewed rates of high monetary expansion that were experienced in Iceland at the end of the 1990’s, which ultimately culminated in another hyperinflationary episode in the years immediately preceding the 2007 collapse, despite the then dominance of these loans within the monetary system. The second hyperinflationary period in 2005-7 also occurred despite the Central Bank’s adherence to economic theories on banking system regulation and progressively raising interest rates to 18% to control the ’overheating’ of the economy.

The negative amortisation applied to the principal by the indexation on these loans results in its substantial growth over the period of the loan, it also raises the question of whether these loans can influence the monetary expansion rate of the banking system, and through that the inflation rate? The mechanical operation of the Banking System is performed using double entry bookkeeping, and its rules require that a matching entry in the bank’s accounts must be made to balance this principal increase. When a bank loan is issued the matching entry is the deposit created on the bank’s ledger and added to the borrower’s account. While this creates money in the form of a bank deposit, the banking system is in theory regulated so that the creation of bank deposit money by lending is matched by its removal when loan principal is repaid. As indexation increases the principal of these loans, two critical questions must be posed: what is the operation that accompanies the increase in the loan’s principal to maintain the balance of the bank’s bookkeeping ledgers, and can this operation influence the money and credit supply originating from the bank?

Most macro-economic analysis of credit crises concentrates on high level statistics of the economy such as overall borrowing levels, currency relationships and GDP based comparisons, and has a marked tendency to treat the banking system and its effects on inflation through the money and loan supply that it controls as a black box. Even recent analysis of the behaviour of these loans is notable for a distinct tendency to treat inflation as a force of nature, and concentrates on indexation as an approach to deal with its consequences, rather than discussing the causes of inflation and in particular the underlying growth of the money supply. Both Mixa[2] and Finnbogadóttir[3] for example, stress indexation’s importance as a means of compensating for Iceland’s historically high inflation rates, without any exploration of its causes.

In this paper we will take the opposite approach, and concentrate on the causes of the historically high rate of growth in the Icelandic money supply, and the behaviour of the banking system that led to this growth. We will focus on the mechanical causes of the regulatory issues encountered in the Icelandic banking system over the last 30 years, and the general failure of modern banking regulatory frameworks in Iceland and elsewhere to control the monetary expansion of the banking system. We will show that rather than preventing inflation, the index-linked loans contribute to the underlying rate of monetary expansion at an amount that is a function of the rate of inflation, thereby creating a positive feedback loop operating directly on the money supply.555Positive feedback is a mathematical process within dynamic systems where the result of a repeated sequence of operations feeds back into the inputs to the process, resulting in an increasingly larger output from the process over time, which is then re-introduced into the calculation as one of the inputs.

1 Verðtryggð lán - Index-linked Loans

1.1 History

The Icelandic Krona was first established as an independent currency by the Money act of 1875, part of a series of constitutional reforms in 1874 which began the process of establishing independence from Denmark. As a de facto member of the Scandinavian Monetary Union[4], the exchange rate for an Icelandic Krona was set at the common exchange rate of 0.4032258g of fine gold to one Krona666The fineness of a previous metal refers to the ratio of the primary metal to any additives or impurities traditionally expressed as parts per 1,000. A fine ounce of gold is a troy ounce of pure gold content in a gold bar.

The Gold Standard, which in one form or other was the dominant banking regulation from the 19th century until the collapse of the Bretton Woods agreement in 1973, attempted to regulate the bank deposit expansion process by creating a fixed relationship between the price of gold and initially the amount of paper currency issued by individual banks. As over time the central bank role became established, the regulatory relationship shifted to deposits owned by the commercial banks which were required to be held at the central bank, and direct control over the physical currency was removed from the commercial banks.

Iceland declared independence from Denmark in 1944, following which it was a signatory member of the Bretton Woods fixed exchange system[5] until its breakup in 1973.777 Data on the Icelandic Money supply since 1965 is available from Seðlabanki Ísland’s annual report, which is available online from the Central Bank’s site www.cb.is from 1997 and from the Icelandic National Archives from 1965. The Central Bank provides three measures, M1, M2 and M3, where M1 is defined as demand deposits and Notes and Coins in circulation, M2 as M1 plus sight deposits, and M3 as M2 plus time deposits. In this paper we use M3 as the measure for the total Icelandic money supply. Care has to be taken in international comparisons of M measures, since there is as yet no commonly agreed definition, and many countries include forms of debt in their gross monetary measurements. There is some evidence that a tradition of centrally controlled interest rates, rather than those determined by a free market process, may have been inherited from its period as a colony. Under Danish rule a maximum interest rate of 4% on mortgages was set by law in 1855, this limit being increased to 6% in 1890, and 8% on all interest rates from 1933. Formal separation of a central bank did not occur until 1965, prior to that Landsbanki provided centralised facilities and in 1952 its interest rate was made the national norm[1].

Iceland was a signatory member of the Bretton Woods agreement in 1944, and participated in that regime until its break up in 1973. While the earlier monetary history appears to be unavailable, high rates of monetary expansion can be seen from the beginning of the central bank’s money supply series in 1965 as shown in Figure 4. By 1969, and while still in the Bretton Wood’s fixed exchange rate framework the M3 money supply was growing at an annual rate above 20%. By 1973, the year of the Bretton Woods collapse, the annual rate of monetary expansion had reached 33%. Iceland then experienced hyperinflationary rates of monetary expansion throughout the 1970’s, peaking in 1983 when the money supply expanded by 83% in a single year. Understandably this long period of monetary instability has had significant repercussions for both the Icelandic economy, and the behaviour of its consumers and businesses.

During the 1960’s and 1970’s Iceland had a central bank reserve requirement on deposit liabilities of 20%. At the beginning of the hyperinflationary period there does appear to have been an attempt to control the expansion by increasing the reserve requirement, which was raised to 28% with an additional 2% special liquidity requirement. As described in the Icelandic Central Bank’s 1981 Annual report888Page 10., this attempt failed:

"The monetary development in 1980 supported a theory saying that fluctuations in the monetary creation are entirely reflected in the bank’s liquidity since no absorbing instruments exist. The intended contractionary impact of reserve requirements has been wiped out by the rules of rediscounting"

The assumptions behind the theoretical description of the operation of reserve requirements presented in economic textbooks ignore the practicalities involved in the day to day management of temporary imbalances that are created as money flows between banks. Inter-bank lending and other methods such as rediscounting999Borrowing based on an underlying asset which is itself a debt. allow banks to manage their day to day reserve requirement, by lending excess reserves and borrowing to make up shortfalls, and this also allows them to circumvent the full force of the reserve controls. This problem was also mentioned by Keynes in 1929[6]101010Pages 234-243. in a discussion on the effects of the different practices between the US Federal Reserve Banks, and the Bank of England in managing the bank rate and rediscounting.

The immediate cause of the 1969-1988 hyperinflation111111Defining hyperinflation somewhat arbitrarily as an annual monetary expansion greater than 20%. appears to have been physical printing of money by the Icelandic Government as a source of revenue. Although direct proof of this is hard to obtain, an International Monetary Fund(IMF) review of the decade following the introduction of indexation by Cornelius[7] gives it as the cause, and it is consistent with the subsequent behaviour of the monetary system. A 1998 working paper from the Icelandic central bank by Andersen and Guðmundsson[8] alludes to seignorage121212Strictly, the difference between the value of a monetary token, and the cost of its production. Used in Economics as a general term for the government’s ability to use its privileged position to profit from printing money. as a cause but then suggests that this was a relatively small contribution as a percentage of GDP (3%). This is a slightly disingenuous argument as it overlooks the role of physical money in the regulatory control over the behaviour of the banking system. The amount of lending and consequent bank deposit creation by commercial banks in gold standard regulatory regimes131313Under the current Basel regulatory framework, there is still a multiplier relationship, but it is significantly throttled by the separate regulatory controls on each individual bank’s capital reserve requirements. is partially regulated as a multiplier of their reserves at the central bank which can be increased by cash deposits. Increases in reserve holdings caused by physical printing can trigger a considerably greater expansion in the part of the money supply represented by deposits within the banking system, in the absence of any other regulatory controls on the banking system.141414The relationship between physical cash, a bank asset, and the customer’s deposit at the bank, is statistically multiplexed within the banking system. As a consequence, attempts by Governments within fractional reserve banking regimes to profit from money printing necessarily fail, as the purchasing power of physical money introduced into the monetary system by the government is rapidly reduced by the considerably larger expansion it creates in bank deposits. The resulting hyperinflation has however proved to be one of the most economically damaging forces in human history.

The Icelandic monetary authority’s response to the 1980’s hyperinflation as described by Jónsson[1] in Central Bank Working Paper No. 5, was widespread indexation, linking prices and wages directly to the inflation rate. A side-effect of the hyperinflation was a short window of opportunity for those with long term loans taken out before the hyperinflation began, whose loans were effectively written off by the extreme monetary expansion at the end of the 1970’s. Jónsson’s paper minimises attention to the precise causes of the hyperinflation, and concentrates on the indexation of lending as a solution to the particular problem of preserving the value of loan capital. This solution was the introduction of indexation on loans loans in 1979, with the value of loan capital being directly linked to the CPI inflation rate.

In an environment where the money supply is doubling every two years and the consumer inflation rate is over 50% a year; where wages and prices are largely indexed to the inflation rate; it is entirely understandable that protection of loan capital should be seen as a priority. Moreover, as Jónsson points out, indexation of debt provided a critical pressure on political efforts to stop the hyperinflationary expansion as increases in wages due to indexation were then matched by increases in borrowing costs, so a behavioural component can certainly be argued for. Unfortunately the introduction of indexation on bank lending disregards several critical differences between bank loans, and other forms of lending such as corporate and government bonds. In particular, it neglects to consider the role the banking system itself plays in creating inflation, through the expansion of the money supply in the form of bank deposits. It also overlooks the source of bank profit, which is derived from the interest on the loans they make. Because bank lending relies on the creation and destruction of money (as principal is repaid), while profits are derived from the interest payments on outstanding loans, banks are relatively immune to the effects of any money supply expansion that they cause and do not experience capital destruction in the way that other lenders do.

The hyperinflationary period continued throughout the 1980’s as various attempts were made to unwind the set of mutual feedback relationships that had now been created between the money supply, lending, and indexation on wages. The monetary expansion rate dropped noticeably in 1984 following the introduction in 1983 of a temporary suspension of wage indexation[8], and was finally brought under control in 1990 when the national wage agreement ended wage indexation with monetary growth falling sharply from 14.36% in 1991 to 3.77% in 1992.

Loan indexation remained however, on mortgages, some forms of commercial borrowing and student loans; and some of its longer term consequences were becoming apparent. In its 1992 Annual Report the Central Bank reports that:

"Third, the indexation of financial assets as well as higher and positive interest rates have had the impact that household debt has accumulated instead of being eroded through inflation."

Other consequences went unrecognised. The 1990’s were a period of low inflation, in Iceland and elsewhere, as the impact of rapid technological developments in manufacturing substantially increased the supply of goods and services worldwide. Iceland experienced historically low rates of monetary expansion between 1994 to 1998 which coincided with changes to the banking regulatory framework. The new Bank of International Settlement (BIS) rules on the treatment of equity capital, generally known as the Basel Accords[9], came into effect in Iceland at the beginning of 1993. They introduced a number of significant changes to the regulatory framework as described in the Central Bank’s 1992 report:

The BIS rules on equity capital came into effect at the beginning of 1993. They are somewhat different from the rules that have applied in this country up to now, the main difference being twofold. One, the amount of equity needed to cover loans differs, depending on the type of collateral behind a loan. Thus, no equity need stand behind a loan to the central government for example, compared with 8% equity against loans to companies without a quality mortgage. Two the definition of equity ratio is widened to some extent so that certain subordinated debt of banks may be counted as part of equity. Furthermore the equity ratio is increased from 5% to 8% of capital which need not mean a substantial increase since the percentage is calculated on a lower base than before.

The Basel Accords formalised a secondary control on the regulatory limits on bank lending, the capital reserve requirement, and were primarily intended to control the exposure of banks to excessive loan defaults by regulating the amount of risk they could be exposed to. They were not intended to directly regulate the bank deposit expansion process, and that they do in fact exert an influence on it, is probably serendipitous. While the central bank reserves regulate the amount of lending that a bank can perform as a function of those deposits for which it is required to maintain a reserve151515This varies considerably, for example in the USA only ”Net transaction accounts” incur a reserve requirement. In Iceland currently reserve requirements apply to all accounts with a maturity period of less than 2 years, as well as debt securities and money market instruments. Rules on Minimum Reserve Requirements, 15/4/2008, http://www.cb.is/lisalib/getfile.aspx?itemid=5850, the capital reserve requirement regulates the amount of lending that a bank can perform as a risk weighted function of its capital base.

Over time the capital reserve requirement generally dominates in determining a bank’s lending limits. In the event of a shortfall in their central bank reserves, Banks can borrow either from other banks or as a last resort from the central bank. When problems arise due to pressure on clearing and reserve liquidity the central bank can generally be relied on to intervene. As a consequence, the central bank reserve requirement is ineffective in limiting long term lending expansion, and this can be seen quite clearly in the Icelandic statistics where the monetary expansion during the 2000’s was accompanied by a sharp increase in the amount of inter-bank lending.

Banks can individually increase the size of their capital reserves from profits, and so the capital requirements place no absolute limits on money and loan expansion. By any standards the index-linked loans are also extremely profitable for their issuers. They carry a guaranteed base rate which is calculated on a negatively amortised principal controlled by indexation to the CPI. In addition personal debt in Iceland has historically been treated as full recourse, and in practice cannot be discharged through bankruptcy. However the high profitability of the loans depends entirely on a positive inflation rate. As shown in Figure 8, for rates of inflation that are approximately 3% or less (it depends to some extent on loan duration), the loans behave similarly to fixed rate compound interest mortgages, and the negative amortisation isn’t triggered. Had the banking system’s regulatory framework in Iceland succeeded in imposing an absolute limit on deposit growth, these loans could not have caused an increase in the money supply and the consequent inflation. In that regime, any increase in the bank deposit portion of the money supply caused by the negative amortisation would have had to be offset by a decrease in lending. In practice, the net effect would have been stable house prices, a stable or decreasing CPI, and the loans would have been no more expensive than their fixed rate equivalents.

With no absolute limit on the amount banks can increase their capital holdings, except for their profitability, this did not occur. Instead, as banks recognised the additional income accrued from the negative amortisation of the index-linked loans, they were able to use part of this income to increase their required capital holdings. This in turn allowed them to increase the size of their loan book, resulting in an increase in the total amount of money represented by bank deposits, and as a consequence, in additional inflation. Financial liberalisation in the late 1990’s only exacerbated the problem by fuelling a credit boom in housing, which since the Icelandic CPI calculation includes a house price component, further accelerated the monetary growth from these loans.

1.2 Detailed Description

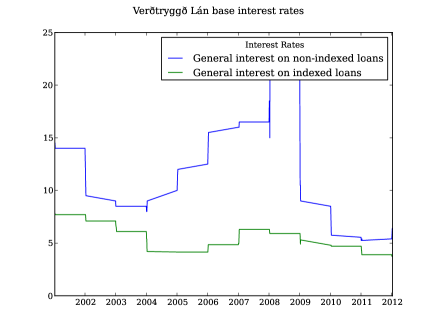

Indexed linked loans are structured with two components: a base interest rate, and the indexation which is applied on the principal. Originally the base rate was fixed for the duration of the loan, but since 2004 loans have been available with base rates that are fixed for 5 years and then reviewed. There do not appear to be any contractual limits on how this review will be performed.

Finding a reliable series of the base rate interest rate that has been used for these loans has been difficult. Since 2001 a rate has been determined by the central bank161616Act No. 38/2001 on interest and price indexation, Article 4: ”In cases involving indexed claims, the interest rate shall be equal to the rate decided by the Central Bank, having regard to the lowest rate of interest on new, general, indexed loans from credit institutions, and posted in accordance with Article 10”, however figures from some institutions are at variance with this rate. Information on the base interest rate used for these loans in this paper is derived from the Statistics Iceland weighted average interest rates series for the commercial banks, "Indexed securities Real interest, % per year available at www.statice.is". These have been cross checked with the Central Bank series from 2001.171717Source spreadsheet Almvex.xls, available at: http://www.cb.is/statistics/interest-rates which provides the base central bank rate set for these loans. They appear to be slightly lower than the rates used by the commercial banks used, prior to privatisation in 2001, so these graphs may slightly underestimate actual payment levels. Figure 2 shows the base rate values for indexed-linked loans and non-indexed loans from the Central Bank’s statistics.

The indexation component is calculated from the CPI index using the Janus rule(see below), which is applied to the outstanding principal of the loan. Calculation of the repayments on these loans over their lifetime depends on the combination of these two data series. The most reliable source appears to be Statistics Iceland which provides several indexation series181818www.statice.is, Statistics section 8. Prices and consumption, Consumer price index, Indices for indexation from 1979. most of which date from the 1990’s or later. Table 1 shows the three tables listed under ’Indices for indexation from 1979’.

| Series | |

|---|---|

| Credit Terms Index | 1979-1995 |

| Consumer price index for indexation | 1995-2013 |

| The old credit term index of financial obligations | 1995-2013 |

Since the ’old credit term index’ series appears to be a continuation of the ’consumer price index for indexation series’ and together they cover the entire period, these are the series used in this paper for calculations.

Given that the principal of these loans is indexed to inflation, it is interesting that the Central Bank also chose to vary the base rate by significant amounts over the 2001-2012 period, seemingly in response to increases in inflation during that period and presumably guided by Keynesian theories. Perhaps more significant, at least for the theories, is the absence of any corresponding contraction in the expansion rate of the money supply during this period.

The indexation component, which is applied to the outstanding principal, is weighted across a 12 month period using the Janus rule191919Jónsson[1] p14-15, which applies past inflation and a future estimate of inflation to arrive at a weighted average. The calculation is performed using this approach in order to mitigate the effect of large short term fluctuations in the CPI, but the calculation of successive percentage changes in this way is not mathematically neutral: as a side effect it effectively prevents the borrower from benefiting from short periods of deflation which would have triggered a corresponding decrease in loan principal.202020Mathematically, the application of successive percentage modifications is not commutative, so this treatment results in the indexed amount of the loan growing slightly faster than it would have otherwise. Longer periods of deflation can cause principal reductions, as can be seen in Figures 4 and 5 following the 2008 crash.

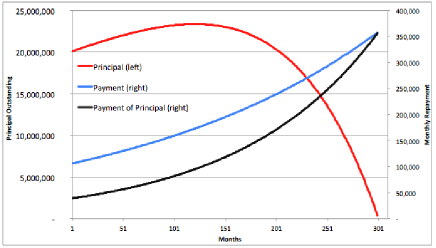

Figure 3 shows the theoretical repayment profile of the principal for sample loans with a 4% base rate, and the median inflation rate for the 1980-2011 period of 5.4%212121Since the hyperinflationary period in the 1980’s distorts the average rate considerably, the median rather than the average is used for these charts..

The repayment structure for the loans results in a varying period of negative amortisation, the length of which depends on the duration of the loan and the rate of inflation during the loan. The loans are structured so that the indexation component results in principal growth (negative amortisation) from the beginning of the loan. However borrower repayments can theoretically overcome the negative amortisation during the first part of the loan during periods of very low inflation. Depending to some extent on the repayment point in the loan, the CPI must be below approximately 3% for a 25 year loan and 1.5% for a 40 year loan. This behaviour can be seen very briefly during the 1990’s when between 1994-1998 the average inflation rate was between 1.5-2.25%.

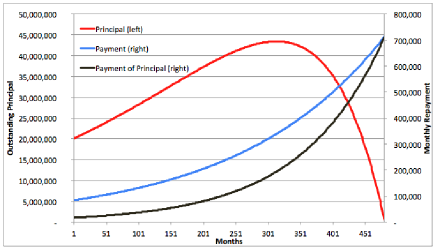

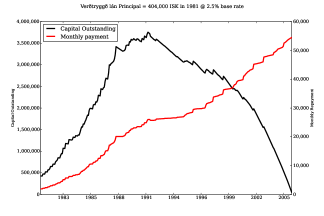

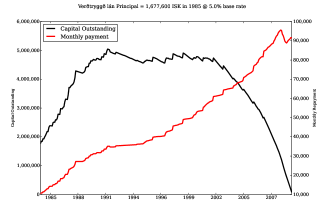

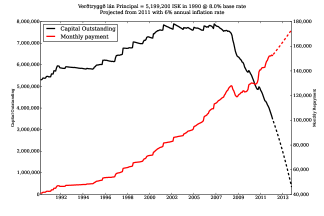

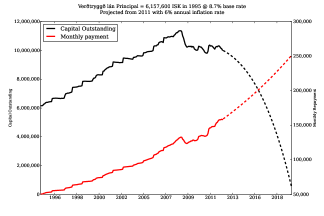

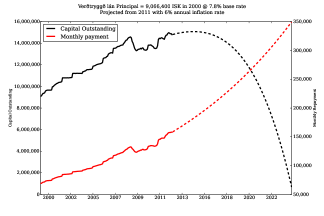

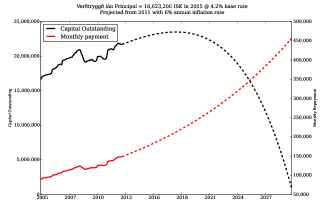

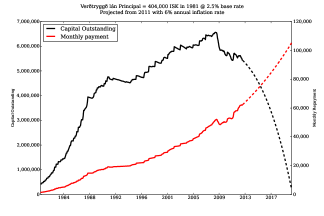

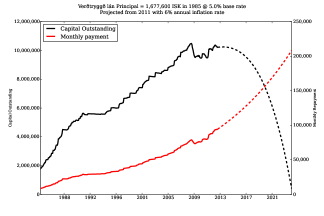

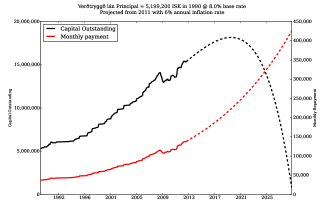

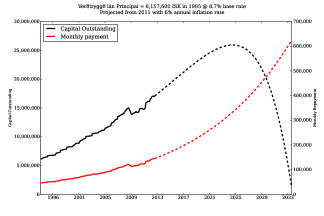

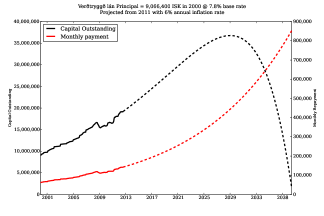

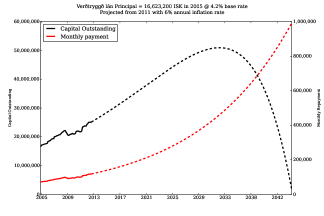

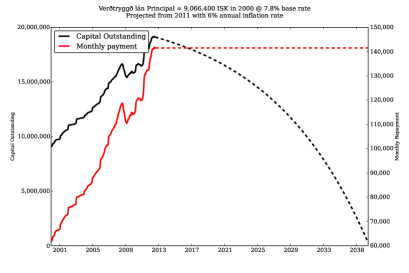

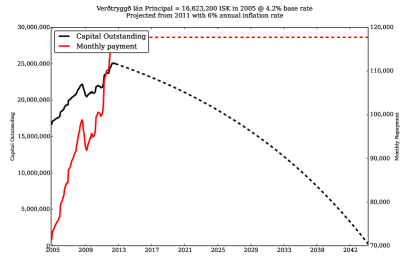

Figures 4 and 5 show a series of repayment profiles calculated from the indexation figures from Statistics Iceland222222Source: www.statice.is statistical series ”Indices for indexation from 1979”, extrapolated where necessary from the end of 2011 using the average indexation for 2011 (shown dashed). In order to provide a basis of comparison for the loans that is relatively neutral to the underlying monetary expansion and its effect on the monetary unit of measurement, the base amount of the loan in the figures is 80% of the average price for a house in Reykjavik during the year the loan was taken out.232323The source for house prices is þjóðskrá Íslands (Registers Iceland http://www.skra.is/lisalib/getfile.aspx?itemid=7850) . The monthly repayment for the mortgage is shown in red, and the outstanding principal in black.

1.3 Interaction with Monetary Regulation

Increases in the consumer price inflation rate have two fundamental causes: either scarcity of the goods and services in the index causing a rise in prices due to supply and demand factors, or expansion in the money supply. Conversely excess supply will cause a drop in prices, as will a reduction in the quantity of money. This relationship follows directly from the quantity theory of money[10] which is one of the fundamental equations of Economics 242424 where P is the aggregate price level, M is the money supply and Q is the quantity of monetary transactions performed with M. See Mallett[11] for comments on the reason for the removal of V from this version of the equation. Analysis of price data must consequently be performed with some caution since for any given price movement there are two possible causes, which without reference to the underlying money supply data it is impossible to untangle. This result applies generally and includes relationships between currencies, which are a balance of export and import demands and the relative expansion of the money supplies of the countries concerned. Iceland’s money supply has usually expanded at considerably higher rates than those of its trading parties, consequently the foreign exchange fluctuations which are often cited as the direct cause of inflation in its banks’ annual reports are better regarded as a consequence of money supply growth rather than its cause.

Money supply expansion can similarly arise from two different sources. Banks as part of their normal operations create money in the form of a bank deposit, when a loan is made. This money is then destroyed as loan principal is repaid. Whether or not there is a net increase in the money supply depends on the regulation of this process such that the rate of new lending is matched by the rate of repayment of the principal on existing loans across the entire banking system. Physical printing of money by the government, especially in the gold standard banking regimes that were regulated by central bank reserves will also lead to rapid hyperinflation, since the additional physical money(which is treated as an asset) can simultaneously trigger a multiplier expansion in bank deposits(a liability) by effectively lifting the reserve limits. In Basel regulatory frameworks this effect is still present, but since lending is also constrained by the capital limits its effects are not so dramatic.

There appear to exist several problems in the current regulatory framework which relies on a combination of central bank reserve regulation, and controls on the ratio of bank capital to their lending portfolio (see Mallett for specific details[12]). Modern banking systems demonstrate a wide range of expansion rates ranging from 1.27 times in the last decade in Germany, 2x in the USA, up to Russia whose money supply has increased by 20 times since its last revaluation in 2000. Iceland’s expansion rate of 6.76x in the post bank privatisation period 1999-2008 is at the high end of the range.

There are then certainly grounds for suspicion that index-linked loans may be causing systemic side effects, and in particular interacting with the money supply. Whether or not this is actually the case appears to depend critically on the precise bookkeeping operations that are used by the banks to perform the indexation on the loans they retain on their asset books.

1.4 Bookkeeping of Icelandic Indexed Linked Loans

| Central Bank | Bank A | |||||

|---|---|---|---|---|---|---|

| Assets | Liabilities | Assets | Liabilities | |||

| Loans | 10000 | 5000 | Deposit A.C1 | |||

| 5000 | Deposit A.C2 | |||||

| 210 | Reserves | 210 | ||||

| 210 | Cash | 790 | 1000 | Capital | ||

| 210 | 210 | Total | 11000 | 11000 | ||

Table 2 shows a simplified view of the asset and liability ledgers for a single bank, and their relationship with those of the central bank. Under double entry bookkeeping, all operations on the ledgers must be performed as (credit, debit) tuples. Each single action, depositing money for example, results in two matching transactions, as a result of which the total amount of assets must always be equal to the total amount of liabilities. In this example we show an initial state with two deposit accounts, a matching quantity of loans, capital holdings of 1000, and central bank reserves (an asset) of 210 with a corresponding deposit (a liability from the central bank’s perspective) at the central bank. The cash ’asset’ represents either physical cash, or asset accounts at other banks. We will assume that the risk weighted multiplier of 50% for mortgages (Basel 2) applies, and so that bank is well within its capital limits for its lending book.

It should be mentioned that the reality of bank operations differs significantly from the description commonly found in Economic textbooks. Central bank reserves are not held back from customer’s deposit accounts as is often implied, but are separate holdings, and are classified as a bank asset, and not as a liability as the customer’s deposit accounts are.252525Strictly, the central bank reserve requirement was a fraction of the physical cash deposited at the bank. The customer’s deposit account was the liability entry reflecting this deposit. Bank loan’s were written as assets, with a matching deposit. The introduction of cheques and other forms of direct transfer between customer accounts, effectively introduced two forms of equivalent, but not identical money into the monetary system. Historically writers in the early 20th Century such as Keynes[6] would distinguish customer deposits as ’deposit money’ or similar, and there has been considerable debate about its precise status. Today with electronic transfers being used for almost all monetary transactions in Iceland and elsewhere, it is the amount of money held in bank deposits that is most critical for determining the price level, while the money classified as assets, either in the form of physical cash or deposit accounts at other banks including the central bank, plays both a regulatory role, and is also critical in providing liquidity for inter-bank clearing relationships.

| Central Bank | Bank A | |||||

|---|---|---|---|---|---|---|

| Assets | Liabilities | Assets | Liabilities | |||

| Loans | 10500 | 5500 | Deposit A.C1 | |||

| 5000 | Deposit A.C2 | |||||

| 210 | Reserves | 210 | ||||

| 210 | Cash | 790 | 1000 | Capital | ||

| 210 | 210 | Total | 11500 | 11500 | ||

To illustrate with an example, Table 3 shows a bank loan being created to a customer at Bank A, with the accompanying double entry bookkeeping operations. In this example, Bank A makes a loan of 500 to its customer C1, the resulting ledger changes are shown in blue. Besides the increase in its deposits and loans books, it also increases its central bank reserve holdings to maintain its required regulatory position. As it was overcapitalised before the loan was made, it remains within its Basel Capital limits. When the loan principal is repaid is is reduced, as is the deposit account of the depositor making the repayment. When interest is paid on the loan there are no direct money supply implications as is also sometimes believed: a debit is made to the customer’s account, and a credit to the bank’s interest income account. Since both of these are classified as liabilities there is no net change to that side of the balance sheet, and the transaction is money supply neutral.

Under double entry bookkeeping rules any change to a single ledger, such as loan assets, must be matched by a corresponding debit or credit to another ledger, maintaining the fundamental accounting equation . Consequently when loan indexation causes the book value of a bank loan asset to increase, there must be some form of matching operation to maintain the balance across the bank’s books, and it is in the handling of this event where the possibility of potential interactions with the money supply arises. The impact of the index-linked loans on the banking system depends fundamentally on this rather obscure bookkeeping question - what is the compensating operation for the increase in the loan’s principal(an asset), caused by the combination of indexation and the negative amortisation structure of these loans? There appear to be two alternatives.

One approach would be to use a contra-asset account. Contra-asset accounts are asset accounts with a credit balance, which effectively act as offsetting (negative) balances on assets.262626In double entry bookkeeping the arithmetic operation of ’credit’ and ’debit’ within a balanced ledger system depend on the side of the ledger they are being applied to, rather than their english meanings. Credits to an asset account will reduce the balance for example, while debits increase it, and the opposite applies to liability accounts. The general rule is that all operations must consist of (credit, debit) tuples, and the individual Asset/Liability classification of ledgers is fundamentally determined by the need to ensure equality between the total of assets and liability ledgers as these operations are performed. In bank accounting the classification of asset and liability accounts is sometimes the opposite to that used by non-banks: for example bank deposits are classified as liabilities, and loans to customers as assets. This would maintain the balance sheet identities and would not have any direct monetary impacts.

There is some evidence from Búnaðarbanki Íslands’ Annual Report in the early 1980’s that suggests this approach may have been used earlier. Between 1981-1994 they show an Asset balance for accrued interest and indexation, (Áfallnir vextir og verðbætur). There is however no obvious correspondence between the growth in this item and the entry for index-linked loans. Between 1984-5 for example, outstanding principal for index-linked loans grew from 752 million ISK to 1,300 million ISK, whilst the growth in the accrued interest and indexation account was only 102 million ISK, and the annual inflation rate was 34%.272727Búnaðaribanki was one of the three main banks in Iceland up until its merger with Kaupthing in 2003. Kaupthing was nationalised following the 2007 crash, and is now known as Arion Bank.

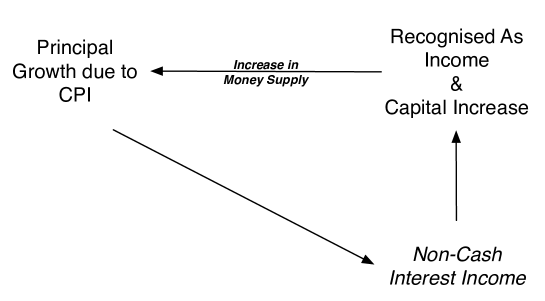

The bookkeeping which appears to have been used for these loans is shown in Tables 4 and 5.282828This description follows what was reported to us in discussions with Icelandic Auditors specialised in banking. The matching balance for any increase in the loan principal due to indexation is first credited to the liability non-cash, interest income received account. At the end of the year, banks are allowed to recognise this account as income, subject to regulatory controls on loss provisions and allowances for loan defaults, and regulatory capital. When this occurs the money credited to this account as a result of loan indexation is recognised as an expense or dividend payment and transferred to a deposit account. At this point it becomes money and can affect the price level. The result is a feedback loop operating on the money supply, as shown in Figure 6.

The following exert from Chapter VI of the Rules on the financial statements of credit institutions No. 34 of 3 November 2003292929http://en.fme.is/media/utgefid-efni/rules_834_2003.pdf (page 14), also supports this treatment, where it details the reporting requirements for indexation. In particular:

Profit and loss account item 1.2, "Interest on loans and advances etc.", shall comprise interest receivable, indexation and commissions receivable, calculated on a time basis or by reference to the amount of the claim, on Assets item 4, "Loans and advances", including credited discount on loans and advances

To illustrate these operations in more detail, Table 4 shows the result of an increase of 500 in the loan principal at Bank A and the corresponding entry in the non-cash income liability ledger. Bank B is set at the initial condition for comparison. Table 5 then shows the subsequent recognition of part of the amount as income and payment to the deposit holder A.C1 as a bank expense as salary, dividend payment to shareholder, payment for services, etc. A small amount would also need to be withheld to cover the increased Basel capital reserve required for the new loan value, which is not shown in this example.

| Central Bank | Bank A | |||||

| Assets | Liabilities | Assets | Liabilities | |||

| Loans | 10500 | 5000 | Deposit A.C1 | |||

| 5000 | Deposit A.C2 | |||||

| 500 | Non-cash Income(Bank) | |||||

| 20 | Reserves | 20 | ||||

| 40 | Cash & Eq | 980 | 1000 | Capital | ||

| Total | 11500 | 11500 | ||||

| Bank B | ||||||

| Loans | 10000 | 5000 | Deposit B.C3 | |||

| 5000 | Deposit B.C4 | |||||

| 20 | Reserves | 20 | ||||

| Cash & Eq | 980 | 1000 | Capital | |||

| 40 | 40 | Total | 11000 | 11000 | ||

| Central Bank | Bank A | |||||

| Assets | Liabilities | Assets | Liabilities | |||

| Loans | 10500 | 5000 | Deposit A.C1 | |||

| 5450 | Deposit A.C2 | |||||

| 20 | Reserves | 20 | Non-cash Income(Bank) | |||

| 40 | Cash & Eq | 980 | 1050 | Capital | ||

| Total | 11500 | 11500 | ||||

| Bank B | ||||||

| Loans | 10000 | 5000 | Deposit B.C3 | |||

| 5000 | Deposit B.C4 | |||||

| 20 | Reserves | 20 | ||||

| Cash & Eq | 980 | 1000 | Capital | |||

| 40 | 40 | Total | 11000 | 11000 | ||

It is not known why the loans were structured to negatively amortise the indexation component, since it is not strictly necessary. The negative amortisation is created by the application of an annuity factor to the repayment schedule which decays over time, creating progressively higher capital repayments. The point at which the growth in the repayment amount overcomes the negative amortisation also depends on the underlying growth in the principal - as can be seen when comparing the hyperinflationary period with later loans. The negative amortisation of the loans does make them initially significantly less expensive than the alternative, and this may have been required to make them appear affordable. It is also not known if this bookkeeping treatment is unique to Iceland. Other countries, notably Chile have attempted to use indexation to control high inflation (see Lefort[13] for a survey of the literature on Chile’s experience); negatively amortized loans are also available in other countries, and played a part in the US subprime collapse.

1.5 Quantitative Analysis

Analysis of how much additional inflation these loans cause is difficult. As long as there is sufficient loan demand, the current banking system will expand the money supply to whatever limit is otherwise imposed by the regulatory framework it is operating under. Since the Basel framework imposes no absolute limits on total capital levels across the banking system, and central bank reserve requirements are not applied to all accounts, the expansion rate seems to primarily depend on the rate of increase of the capital reserve, which in turn depends directly on the profitability of the banks, and their individual lending decisions. A bank could choose not to expand their capital reserve if they felt that the new lending being requested was too risky for example, although this doesn’t appear to have been a factor in Icelandic banking decisions during the bubble period. The question is how much of the capital expansion can be attributed to these loans, and how much would have occurred anyway? While we cannot put an absolute figure on this, we can estimate upper and lower bounds.

For a very brief period between July 1993 and April 1995, the annual inflation rate in Iceland fell below 2%. This is under the threshold for negative amortisation to occur on these loans, and so during this time there would have been little or no monetary growth due to this factor. The effect of this can be seen in Figure 4c, where principal growth flatlines for 2 years, and then subsequently increases.

The annual M3 series from Seðlabanki Ísland’s shows a growth in M3 of 2.3% for 1994-95, so we can regard this as an approximate lower bound on the expansion rate of the Icelandic banking system without the influence of the growth in principal caused by indexation.

Figure 7 shows the relative growth of the Icelandic CPI versus the M3 growth over the 1980-2012 period. If we exclude the hyperinflationary periods between 1967-1990, and 2005-8303030This latter period featured the main Icelandic Banks developing several innovative approaches to financing capital expansion, which are currently the subject of legal action. we can see that that the M3 expansion rate increased from 6.86% in 1996 to 14.97% in 2004. So we can place the upper bound on monetary expansion due to these loans between 4.56% and 12.67%, bearing in mind that the precise amount of negative amortisation with the loans is a function of the inflation rate itself. Consequently there is a positive feedback loop involved, illustrated in Figure 6. which implies that the rate of expansion is likely to increase over time.

To compare the additional cost of these loans Table 6 shows 25 and 40 year repayment totals for Icelandic versus fixed rate US loans at a range of interest rates.

| Amount | Base Rate | Indexed (1990) | Fixed Rate | Indexed (1990) | Fixed Rate |

|---|---|---|---|---|---|

| 25 Years | 40 Years | ||||

| 20,000,000 | 4.0% | 55,981,097 | 31,670,200 | 134,458,782 | 40,122,000 |

| 20,000,000 | 5.0% | 62,000,204 | 35,075,400 | 155,131,850 | 46,290,800 |

| 20,000,000 | 7.0% | 74,959,290 | 42,406,700 | 199,926,304 | 59,657,400 |

Besides the extra cost of the loans, Table 6 also illustrates a less obvious aspect of the loans, their profile depends critically on when they were taken out. While it might be expected that the loans would behave similarly whenever they were created, this is not the case. Borrowers in the 1980’s experienced hyperinflationary increases in their loan principal, but their salaries were also indexed. In the 1990’s, a period of relatively low monetary expansion occurred, at the same time as productivity greatly increased, with the result that inflation was low, and the negative amortisation of the loans was minimised. In the 2000’s however, borrower’s experienced both high inflation and higher interest rates for the fixed interest rates on the loans. While salaries generally rose above the inflation rate during the early part of the decade, post-2008 salaries generally dropped significantly. This also helps to explain the disproportionate difference in the cost of the 25 versus the 40 year index-linked loans, once the negative amortisation component is taken into account.

2 Conclusion

One of the striking problems of current banking system research is that there is relatively little focus on an integrated view of the entire system’s behaviour. Consequently when reforms are proposed they typically address single issues affecting one part of the system, and not infrequently - as the index-linked loans illustrate only too well - create new problems elsewhere. This paper should of course also be read in that context. A far deeper understanding of the larger implications for monetary systems of indexation instruments is required than is currently available, and this is an area requiring considerably more research.

This failure to identify an integrated understanding of banking system behaviour has long proved problematic for policy makers. The indexed-linked loans were originally introduced with the objective of stabilising the Icelandic banking system during a period of hyperinflation triggered by government money printing. That government printing of money can cause hyperinflation is of course well known, but that one of the causes of this form of runaway monetary expansion arises from interaction with the banking system’s regulatory controls is not. That indexing loans would cause monetary expansion due to obscure details of the bookkeeping treatment used, is also not the most obvious of side effects.

There are other objections that can be raised against the index-linked loans besides their inflationary influence though. The formula used for their calculation are not readily available; their historical calculation also rests on time series data on the applied indexation rate that is difficult to locate; and it is has consequently proved extremely difficult for borrowers to validate their payment schedule. Since changes are periodically made to how the indexation is calculated their future behaviour is also impossible to predict, considerably complicating individual financial planning. With the newer form of the loan that has been issued since 2005, the base interest rate can also be arbitrarily adjusted by the lender after an initial period, and there appear to be no contractual limits on this.

The negative amortisation of the principal, which is responsible for the loan’s interaction with the CPI, also violates normal principles of prudential borrowing. Borrowers do not typically begin repaying capital until 15-20 years into the loan, and they incur extraordinary debt loads as a direct consequence, especially with the 40 year loans. Unfortunately these loans have been the predominant form of lending in Iceland for over 30 years, and the long term outlook is not known: in particular excepting loans which are repaid through property sale, what percentage of these loans are ever successfully repaid?

The long term prognosis for recent borrowers in particular is grim. As shown in Figure 5, the combination of high inflation before the crash, and the high base interest rates at the beginning of the 21st century will make it extremely hard if not impossible for many borrowers to fully repay these loans, and while statistics on the proportion of 40 year loans are not available, they are believed to be the majority of these loans. Icelandic policy since the crash has been to attempt to protect vulnerable and lower income groups, and Stefán Ólafsson[14] has presented a detailed analysis of household situation and policy responses showing the partial success of this. However, the various forms of relief offered have often penalised those who acted responsibly during the bubble - in 2008 for example borrowers were allowed to apply for a revaluation of their loans to no more than 110% of the value of the house, effectively penalising those who had substantial personal equity in their houses. Additional relief has also been provided through tax deductible interest rate subsidies to a maximum of 900,000 ISK for married couples in 2012. As a consequence house price levels have been largely maintained, but there has been considerable pressure on rental levels, leading to high rents, and then to compensating increases in tax funded rental subsidies.

A further complication lies in the ownership of the loans. Indexed linked loans were available from the Icelandic Banks, and from the Housing Finance Fund(HFF)[15] which is a government owned provider of mortgage credit. They were also securitized. A 2006 Report by Kaupthing Bank[16] showed ownership split between the Icelandic Banks(20%), Mutual Funds(9%), private holdings(8%) foreign investors(46%) and the Icelandic Pension Funds(17%). While within Iceland there are widespread calls for indexation to be removed from these loans, ownership by the pension funds who are required to index link their pension payments, and in particular the high foreign ownership considerably complicates any formal adjustments.

It should be emphasised that only index-linked loans directly owned by commercial banks or similar institutions performing fractional reserve lending can contribute to money supply growth through the mechanisms described in this paper. However all borrowers with these loans are affected by the consequent growth in the money supply. Since substantial quantities of these loans were securitized and sold abroad (the Glacier Bonds), all Icelanders are potentially affected by the resulting foreign exchange imbalances which are being temporarily managed through capital controls. It seems entirely too probable that this will cause further feedback issues when the capital controls are lifted. If loan indexation causes higher inflation, then currency outflows on these loans will increase, weakening the Krona exchange rate, and further increasing inflation as the cost of imported goods rise - which then increases monetary expansion through the indexed loans, leading inexorably to higher inflation.

In addition borrowers are now faced with loan and money supply growth in the banking system originating from the newly introduced fixed rate loans which are not negatively amortized.313131Since the crash loans with a fixed interest rate for the first 5 years, and varying subsequently have been introduced by the banks. While the Icelandic money supply contracted by 10% in the immediate aftermath of the crash, it grew by 7% in 2011. New borrowers with these loans will benefit from the monetary expansion caused by the indexed-linked loans, as the resulting inflation reduces their debt burden; just as it increases the debt burden for those with indexed-linked loans. Consequently it seems highly probable that over time those with indexed-linked loans who are unable to refinance into fixed rate loans, will be effectively trapped into eventual bankruptcy, as a rapid divergence in individual situations divides house owners with growing debt from indexed-linked loans, from those with declining debt with the newer fixed rate loans.

Somewhat ironically, given the original reasons for introducing the loans was monetary stability, there is a possible solution that would effectively remove indexation from these loans, without the need for any formal loan modifications. This is quite simply to stabilise the money supply to 0% growth, which could then be expected to similarly stabilise the CPI. As shown in Figure 8, when the CPI is 3% or less, these loans behave identically to compound interest fixed rate loans, and the negative amortisation and consequent money supply interaction ceases.

This would also help to mitigate the pension fund exposure to these loans, as in a constant money economy with low or negligible inflation their indexation requirement towards their pensioners is also resolved. They would also benefit from a considerably lower default rate on their loans than would otherwise be the case, resulting in lower capital losses. An economy with a constant money supply would also provide considerably clearer signals to its policy makers through the price mechanisms, since the distortions caused by varying rates of monetary expansion would be removed, and this would considerably aid the establishment of sound and prudent policy direction.

Achieving this goal would require adjustments to the regulatory banking framework, and a legal mandate established to support it. Mechanically speaking there are several ways the problem could be approached. The simplest would be to adjust the current Basel Regulatory framework to maintain a constant capital amount across the banking system, while also creating a unified risk weighting for all types of lending, and in particular removing the 0% weighting on lending to governments.

The larger economic effects of monetary stability are not known, since this does not appear to have ever been achieved during the fractional reserve banking era. We suspect that one side effect would be that many of the economic indicators that we are used to, steadily increasing prices, steadily increasing government debt, would look quite different with a constant money supply, since the distortion introduced by the change in the unit of measurement for these statistics - money - would be removed. However not enough is known about any long term side-effects this might create for liquidity provisions within the banking system as money is transferred between banks. Central bank inflation targets (typically 2%) arise from the observation that low but positive rates of inflation appear to be beneficial - but the mechanisms causing this effect are unknown, as is their general applicability. There would also be potential competitive issues between banks, if mechanisms were not developed for banks to trade capital within the system, but potential stability issues if they were. However it can be argued that these problems are also present in the current system. A medium term policy of stabilisation using this approach, careful monitoring, and an accelerated research program into longer term regulatory frameworks capable of providing monetary stability, in conjunction with a deeper investigation into the macro-economic consequences of these loans would seem to be the safest approach, given the current state of economic knowledge, to deal with these issues.

More problematic are the potential exchange repercussions if Iceland did achieve monetary stability, which is the danger that improbable as it might sound, the Krona becomes a store of value. The general failure of modern banking regulation to provide monetary stability has created a world of widely varying monetary expansion rates, and Iceland is not in a position to support significant investment demand for its currency. Until these issues are addressed on a worldwide basis, small countries with relatively stable currencies are placed in difficult situations - as the recent experience of Switzerland shows. This would present an interesting challenge to Iceland’s monetary authorities, and restrictions on Krona ownership, or other mechanisms might need to be introduced to protect the Icelandic economy if this eventuality arose.

There are other approaches that have been applied by countries with excessive mortgage debt, for example the USA’s deliberate expansion of its money supply over the last 4 years. This approach is reliant both on the preponderance of fixed interest rate lending in its monetary system, and the unique position the US dollar currently occupies as a global trading currency. As a solution it is not available to Iceland simply because of the pre-dominance of index-linked loans in the monetary system.

It is unlikely that any single solution, even quantitative stability, is likely to be the only required measure in Iceland’s situation. The issues created by the indexed-linked loans are complex, and potentially very far reaching, given their 40 year duration. Monetary policies must be developed that are based on a grounded understanding of the direct causes of inflation, rather than simplistic attempts to address some of its symptoms within a complex and poorly understand financial environment. A co-ordinated systems based approach is required, and one that is tailored to the unique circumstances that Iceland, and its citizens finds itself in, rather than reliant on economic policy originating from very different monetary systems.

Acknowledgements

I would like to thank Guðmundur Ásgeirsson and Andri Már Ólafsson for their invaluable help with background research and Icelandic sources; Valborg Stefánsdóttir and Anton Holt at the Library of the Central Bank of Iceland for their assistance with access to historical information on the Icelandic Banking System; Dr. Jón Þór Sturluson for discussions on fractional reserve banking mechanisms, and with Einar Jón Erlingsson for assistance with the formula and calculations for the loans; Charles Keen, David Gudjonsson for their considerable help with review comments; and Dr. Kristinn Thorisson for his extraordinary support and guidance with the fundamental research on banking systems this paper builds on. The author takes sole responsibility for any remaining errors.

References

- [1] Bjarni Bragi Jónsson. Financial Indexation and Interest Rate Policy in Iceland. Working Paper 5: Central Bank of Iceland, Economics Dept, October 1999.

- [2] Mar Wolfgang Mixa. Verðtryggðlá fjárskuldbindinga. September 2012. Institute for Financial Literacy.

- [3] Esther Finnbogadóttir and Guðrún Inga Ingólfsdóttir and Yngvi Hardðarson. Verðtrygging á Íslandi. Kostir og gallar. (The Pros and Cons of Icelandic Indexed linked loans). Askar Capital hf., March 2010.

- [4] Michael Bergman and Stefan Gerlach and Lars Jonung. The rise and fall of the Scandinavian Currency Union 1873-1920. European Economic Review, 37(2-3):507–517, 1993.

- [5] US Dept. of State Publication 2866. Proceedings and Documents of the United Nations Monetary and Financial Conference 1944. Technical report, July 1948.

- [6] John Maynard Keynes. A Treatise on Money. Macmillan, 1929.

- [7] Peter K. Cornelius. Monetary Indexation and Revenues from Money Creation: The case of Iceland. IMF Working Paper Ref: WP/90/20, March 1990.

- [8] Palle S. Andersen and Már Guðmundsson. Inflation and Disinflation in Iceland. Central Bank of Iceland, Working paper No. 1, January 1998.

- [9] Basel Committee on Banking Supervision. International convergence of capital measurement and capital standards. Technical report, 2006.

- [10] Irving Fisher. The Purchasing Power of Money, its Determination and Relation to Credit, Interest and Crises. Macmillan, New York, 1911.

- [11] Jacky Mallett. Description of the Operational Mechanics of a Basel Regulated Banking System. Working Paper: Available for review at www.arxiv.org, 2012.

- [12] Jacky Mallett. What are the limits on Commercial Bank Lending? Journal of Advances in Complex Systems, August 2012.

- [13] Fernando Lefort and Klaus Schmidt-Hebbel. Indexation, Inflation and Monetary Policy: An Overview. Central Bank of Chile, 2002.

- [14] Stefán Ólafsson. Iceland’s Financial Crisis and Level of Living Consequences. Working Paper No. 3:2001 Social Research Centre, University of Iceland, December 2011.

- [15] Jon Runar Sveinsson. The Formation of Urban Homeownership in Iceland. ENHR Conference, University of Cambridge, July 2004.

- [16] Kaupthing Bank. The Icelandic Bond Market. 2006.

Appendix

Calculation of Indexed Linked Loans

There are two forms of Verðtryggð lan with slightly different repayment profiles, Fixed Amortization and Fixed payment. In both cases repayment is structured as an annuity, with the annuity factor partially determining the capital repayment. As a consequence, for rates of inflation above 2-3% (depending on the duration of the loan), repayments during the first years of the loan may not cover principal repayment and the remained is negatively amortized. This leads to considerable variation in the point at which principal repayment does begin, depending in part on the duration of the loan, and on the prevailing rates of inflation during the loan.

Fixed Amortization(real terms)

For an period loan with an initial principal of and a fixed rate interest rate component of . Inflation is measured as the percentage change in the CPI, .

| Amortization in real terms: | ||||

| Amortization in nominal terms: | ||||

| The per (end of) period Principal in real terms: | ||||

| The per period Principal in nominal terms: | ||||

| Interest payments in real terms (paid at end of period): | ||||

| Interest payments in nominal terms (paid at end of period): | ||||

| Total payments per period: | ||||

Fixed payment (annuity in real terms)

With terms as above, the fixed payment in real tems is derived from the standard equation of annuities:

| Payment in nominal terms: | ||||

The breakdown of interest and capital payments is then calculated recursively:

| Nominal Interest Payment: | ||||

| Nominal amortization: | ||||

| Nominal principal: |

As the CPI changes over time, the re-payment schedule is adjusted through re-calculation of the ’fixed’ payment.