Variance optimal hedging for continuous time additive processes and applications

Abstract

For a large class of vanilla contingent claims, we establish an explicit Föllmer-Schweizer decomposition when the underlying is an exponential of an additive process. This allows to provide an efficient algorithm for solving the mean variance hedging problem. Applications to models derived from the electricity market are performed.

Key words and phrases: Variance-optimal hedging, Föllmer-Schweizer decomposition, Lévy’s processes, Electricity markets, Processes with independent increments, Additive processes.

2000 AMS-classification: 60G51, 60H05, 60J25, 60J75

1 Introduction

There are basically two main approaches to define the

mark to market of a contingent claim: one relying on the

no-arbitrage assumption and the other related to a

hedging portfolio, those two approaches converging in the

specific case of complete markets.

In this paper we focus on the hedging approach.

A simple introduction to the different hedging and pricing models in incomplete markets can be found in chapter 10 of [13].

When the market is not complete, it is not possible, in general, to

hedge perfectly an option.

One has to specify risk criteria, and

consider the hedging strategy that minimizes the distance (in terms of

the given criteria) between the payoff of the option and the terminal

value of the hedging portfolio.

In practice the price of the option is

related to two components: first, the initial-capital value

and second the quantitative evaluation of

the residual risk induced by this imperfect hedging strategy

(due to incompleteness).

Several criteria can be adopted.

The aim of super-hedging is to hedge all cases. This approach yields in general prices that are too expensive to be realistic [18].

Quantile hedging modifies this approach allowing for a limited probability of loss [20].

Indifference utility pricing introduced in [23] defines the price of an option to sell (resp. to buy) as the minimum initial value

s.t. the hedging portfolio with the option sold (resp. bought) is equivalent

(in term of utility) to the initial portfolio.

Global quadratic hedging approach was developed by M. Schweizer

([38], [40]):

the distance defined by the expectation of the square

of the difference

between the hedging portfolio and the payoff is

minimized. Then, contrarily to the case of utility maximization,

in general that approach provides

linear prices and hedge ratios with respect to the payoff.

In this paper, we follow this last approach either to derive the hedging strategy minimizing the global quadratic hedging error for a given initial capital, or to derive both the initial capital and the hedging strategy minimizing the same error. Both actions are referred to the objective measure. Moreover we also derive explicit formulae for the global quadratic hedging error which together with the initial capital allows the practitioner to define his option price.

We spend now some words related to the global quadratic hedging approach which is also called mean-variance hedging or global risk minimization. Given a square integrable r.v. , we say that the pair is optimal if minimizes the functional . The quantity and process represent the initial capital and the optimal hedging strategy of the contingent claim .

Technically speaking, the global risk minimization problem is based on the local risk minimization one which is strictly related to the so-called Föllmer-Schweizer decomposition (or FS decomposition) of a square integrable random variable (representing the contingent claim) with respect to an -semimartingale modeling the asset price: is an -local martingale and is a bounded variation process with . Mathematically, the FS decomposition, constitutes the generalization of the martingale representation theorem (Kunita-Watanabe representation), which is valid when is a Brownian motion or a martingale. Given a square integrable random variable , the problem consists in expressing as where is predictable and is the terminal value of an orthogonal martingale to , i.e. the martingale part of . In the seminal paper [21], the problem is treated for an underlying process with continuous paths. In the general case, is said to satisfy the structure condition (SC) if there is a predictable process such that and a.s. In the sequel, most of the contributions were produced in the multidimensional case. Here, for simplicity, we will formulate all the results in the one-dimensional case.

constitutes in fact the initial capital and it is given by

the expectation of under

the so called variance optimal signed measure (VOM).

Hence, in full generality, the initial capital is not guaranteed to be

an arbitrage-free price. For continuous processes, the variance optimal

measure

is proved to be non-negative under a mild no-arbitrage

condition [41].

Arai ([4] and [3]) provides sufficient conditions

for the variance-optimal martingale measure to be a probability

measure, even

for discontinuous semimartingales.

In the framework of FS decomposition, a

process which plays a significant role is the so-called

mean variance trade-off (MVT) process . This notion is

inspired by the theory in

discrete time started by [36]; under condition (SC), in the continuous time case

is defined as .

In fact, in [38] also appear a slight more general condition, called (ESC), together with a corresponding EMVT process; we will

nevertheless not discuss here further details.

If the MVT process is deterministic, [38] solves the mean-variance hedging problem

and also provides an efficient

relation between the solution of the global risk minimization problem and

the FS decomposition, see Theorem 4.1.

We remark that, in the continuous case, treated by [21],

no need of any condition on is required. It also shows that, for obtaining

the mentioned relation, previous

condition is not far from being optimal.

The next important step was done in

[30] where, under the only condition that is uniformly bounded,

the FS decomposition of any square integrable random variable

exists, it is unique and the global minimization

problem admits a solution.

More recently has appeared an incredible amount of papers in

the framework of global (resp. local) risk minimization, so that

it is impossible

to list all of them and it is beyond our scope.

Four significant papers containing a good list of references

are [42], [7], [11] and [43].

In this paper, we are not interested in generalizing the conditions under which the FS decomposition exists. The present article aims, in the spirit of a simplified Clark-Ocone formula, at providing an explicit form for the FS decomposition for a large class of European payoffs , when the process is an exponential of additive process which is not necessarily a martingale. From a practical point of view, this serves to compute efficiently the variance optimal hedging strategy which is directly related to the FS decomposition, since the mean-variance trade-off is for that type of processes deterministic. One major idea proposed by Hubalek, Kallsen and Krawczyk in [24], in the case where the log price is a Lévy process, consists in determining an explicit expression for the variance optimal hedging strategy for exponential payoffs and then deriving, by linear combination the corresponding optimal strategy for a large class of payoff functions (through Laplace type transform). Using the same idea, this paper extends results of [24] considering prices that are exponential of additive processes and contingent claims that are Laplace-Fourier transform of a finite measure. In this generalized framework, we could formulate assumptions as general as possible. In particular, our results do not require any assumption on the absolute continuity of the cumulant generating function of , thanks to the use of a natural reference variance measure instead of the usual Lebesgue measure, see Section 3.2. In the context of non stationary processes, the idea to represent payoffs functions as Laplace transforms was applied by [26] (that we discovered after finishing our paper) to derive explicit pricing formulae and by [19] to investigate time inhomogeneous affine processes. However, the [26] generalization was limited to additive processes with absolutely continuous characteristics and to the pricing application: hedging strategies were not addressed.

One practical motivation for considering processes with independent and possibly non stationary increments came from hedging problems in the electricity market. Because of non-storability of electricity, the hedging instrument is in that case, a forward contract with value where is the forward price given at time for delivery of 1MWh at time . Hence, the dynamics of the underlying is directly related to the dynamics of forward prices. Now, forward prices are known to exhibit both heavy tails (especially on the short term) and a volatility term structure according to the Samuelson hypothesis [34]. More precisely, as the delivery date approaches, the forward price is more sensitive to the information arrival concerning the electricity supply-demand balance for the given delivery date. This phenomenon causes great variations in the forward prices close to delivery and then increases the volatility. Hence, those features require the use of forward prices models with both non Gaussian and non stationary increments in the stream of the model proposed by Benth and Saltyte-Benth, see [9] and also [8].

The paper is organized as follows. After this introduction we introduce the notion of FS decomposition and describe global risk minimization. Then, we examine at Section 3 the explicit FS decomposition for exponential of additive processes. Section 4 is devoted to the solution to the global minimization problem, Section 5 to theoretical examples and Section 6 to the case of a model intervening in the electricity market. Section 7 is devoted to simulations.

2 Preliminaries on additive processes and Föllmer-Schweizer decomposition

In the whole paper, , will be a fixed terminal time and we will denote by a filtered probability space, fulfilling the usual conditions. In the whole paper, without restriction of generality will stand for the -field .

2.1 Generating functions

Let be a real valued stochastic process.

Definition 2.1.

The cumulant generating function of (the law of) is the mapping where where is the Argument of , chosen in ; is the principal value logarithm. In particular we have

where . In the sequel, when there will be no ambiguity on the underlying process , we will use the shortened notations for . We observe that includes the imaginary axis.

Remark 2.2.

-

1.

For all , where denotes the conjugate complex of .

-

2.

For all

In the whole paper will stand for

2.2 Semimartingales

An -semimartingale is a process of the form , where is an -local martingale and is a bounded variation adapted process vanishing at zero. will denote the total variation of on . If is -predictable then is called an -special semimartingale. The decomposition of an -special semimartingale is unique, see Definition 4.22 of [25]. Given two - locally square integrable martingales and , will denote the angle bracket of and , i.e. the unique bounded variation predictable process vanishing at zero such that is an -local martingale. If and are -semimartingales, denotes the square bracket of and , i.e. the quadratic covariation of and . In the sequel, if there is no confusion about the underlying filtration , we will simply speak about semimartingales, special semimartingales, local martingales, martingales.

All along this paper we will consider -valued martingales (resp. local martingales, semimartingales). Given two -valued local martingales then are still local martingales. Moreover If is a -valued martingale then is a real valued increasing process.

All the local martingales admit a cadlag version. By default, when we speak about local martingales we always refer to their cadlag version. Given a real cadlag stochastic process , the quantity will represent the jump . More details about previous notions are given in chapter I of [25].

For any special semimartingale X we define The set is the set of -special semimartingale for which is finite.

2.3 Föllmer-Schweizer Structure Condition

Let be a real-valued special semimartingale with canonical decomposition, For simplicity, we will just suppose in the sequel that is a square integrable martingale. For the clarity of the reader, we formulate in dimension one, the concepts appearing in the literature, see e.g. [38] in the multidimensional case. For a given local martingale , the space consists of all predictable -valued processes such that where . For a given predictable bounded variation process , the space consists of all predictable -valued processes such that Finally, we set

| (2.1) |

which will be the class of admissible strategies. For any , the stochastic integral process is therefore well-defined and is a semimartingale in . We can view this stochastic integral process as the gain process associated with strategy on the underlying process .

The minimization problem we aim to study is the following. Given , a pair , where and is called optimal if minimizes the expected squared hedging error

| (2.2) |

over all pairs . will represent the initial capital of the hedging portfolio for the contingent claim at time zero. The definition below introduces an important technical condition, see [38].

Definition 2.3.

Let be a real-valued special semimartingale. is said to satisfy the structure condition (SC) if there is a predictable -valued process such that the following properties are verified.

-

1.

in particular is absolutely continuous with respect to , in symbols we denote .

-

2.

a.s.

From now on, we will denote by the cadlag process This process will be called the mean-variance trade-off (MVT) process. Lemma 2 of [38] states the following.

Proposition 2.4.

If satisfies (SC) such that is a bounded r.v., then .

The structure condition (SC) appears naturally in applications to financial mathematics. In fact, it is mildly related to the no arbitrage condition at least when is a continuous process. Indeed, in the case where is a continuous martingale under an equivalent probability measure, then (SC) is fulfilled.

2.4 Föllmer-Schweizer Decomposition and variance optimal hedging

Throughout this section, as in Section 2.3, is supposed to be an -special semimartingale fulfilling the (SC) condition. Two -martingales are said to be strongly orthogonal if is a uniformly integrable martingale, see Chapter IV.3 p. 179 of [31]. If are two square integrable martingales, then and are strongly orthogonal if and only if . This can be proved using Lemma IV.3.2 of [31].

Definition 2.5.

A random variable admits a Föllmer-Schweizer (FS) decomposition, if

| (2.3) |

where is a constant, and is a square integrable martingale, with and strongly orthogonal to .

We summarize now some fundamental results stated in Theorems 3.4 and 4.6, of [30] on the existence and uniqueness of the FS decomposition and of solutions for the optimization problem (2.2).

Theorem 2.6.

We suppose that satisfies (SC) and that the MVT process is uniformly bounded in and . Let .

-

1.

admits a FS decomposition. It is unique in the sense that , and is uniquely determined by .

-

2.

For every and every , there exists a unique strategy such that

(2.4) -

3.

For every there exists a unique couple such that

Next theorem gives the explicit form of the optimal strategy under some restrictions on .

Theorem 2.7.

Proof.

In the sequel, we will find an explicit expression of the FS decomposition for a large class of square integrable random variables, when the underlying process is an exponential of additive process.

2.5 Additive processes

This subsection deals with processes with independent increments which are continuous in probability. From now on will always be the canonical filtration associated with .

Definition 2.8.

A cadlag process is a (real)

additive process iff

,

is continuous in probability, i.e.

has no fixed time of discontinuities and it has independent

increments in the following sense:

is independent of for .

is called Lévy process if it is additive and

the distribution of only depends on

for .

An important notion, in the theory of semimartingales, is the notion of characteristics, introduced in definition II.2.6 of [25]. A triplet of characteristics , depends on a fixed truncation function with compact support such that in a neighborhood of ; is some random -finite Borel measure on . If is a semimartingale additive process the triplet admits a deterministic version, see Theorem II.4.15 of [25]. Moreover , and have bounded variation for any Borel real subset . Generally in this paper denotes the Borel -field associated with a topological space .

Proposition 2.9.

Suppose is a semimartingale additive process with characteristics , where is a non-negative Borel measure on . Then given by

| (2.6) |

fulfills

| (2.7) |

where is a non-negative kernel from into verifying

| (2.8) |

Proof.

We come back to the cumulant generating function and its domain .

Remark 2.10.

In the case where the underlying process is an additive process, then

In fact, for given we have Since each factor is positive, if the left-hand side is finite, then is also finite.

3 Föllmer-Schweizer decomposition for exponential of additive processes

The aim of this section is to derive a quasi-explicit formula of the FS decomposition for exponential of additive processes with possibly non stationary increments.

We assume that the process is the

discounted price of the non-dividend paying stock which is supposed to be of the form,

for all

where is a strictly positive constant and is a

semimartingale additive process,

in the sense of Definition 2.8, but not necessarily

with stationary increments.

In the whole paper, if is a complex number,

stands for .

In particular if is a real number,

stands for .

3.1 On some properties of cumulant generating functions

We need now a result which extends the classical Lévy-Khinchine decomposition, see e.g. 2.1 in Chapter II and Theorem 4.15 of Chapter II, [25], which is only defined in the imaginary axis to the whole domain of the cumulant generating function. Similarly to Theorem 25.17 of [35], applicable for the Lévy case, for additive processes we have the following.

Proposition 3.1.

Let be a semimartingale additive process and set . Then,

-

1.

is convex and contains the origin.

-

2.

.

-

3.

If such that , i.e. , then

(3.1)

Proof.

-

1.

is a consequence of Hölder inequality similarly as i) in Theorem 25.17 of [35] .

-

2.

The characteristic function of the law of is given through the characteristics of , i.e.

where we recall that for any , and is a positive measure which integrates . Let . According to Theorem II.8.1 (iii) of [35], there is an infinitely divisible distribution with characteristics . By uniqueness of the characteristic function, that law is precisely the law of . By Corollary II.11.6, in [35], there is a Lévy process such that and are identically distributed. We define

Remark 2.10 says that , moreover clearly . Theorem V.25.17 of [35] implies , i.e. point 2. is established.

-

3.

Let be fixed; let , in particular . We apply point (iii) of Theorem V.25.17 of [35] to the Lévy process .

∎

Proposition 3.2.

Let be a semimartingale additive process. For all , has bounded variation and where was defined in Proposition 2.9.

Proof.

Using (3.1), we only have to prove that is absolutely continuous w.r.t. . We can conclude

if we show that

| (3.2) |

Without restriction of generality we can suppose . (3.2) can be bounded by the sum where

Using Proposition 2.9, we have

this quantity is finite because taking into account Proposition 3.1. Concerning we have

because of (2.8). As far as is concerned, we have

again because of (2.8). This concludes the proof of the proposition.

∎

The converse of the first part of previous Proposition 3.2 also holds. To show this, we formulate first a simple remark.

Remark 3.3.

-

1.

For every , is a martingale. In fact, for all , we have

-

2.

and it has always bounded variation.

Proposition 3.4.

Let be an additive process and . is a semimartingale if and only if has bounded variation.

Proof.

Remark 3.5.

Let . If is a semimartingale additive process, then is necessarily a special semimartingale since it is the product of a martingale and a bounded variation continuous deterministic function and by use of integration by parts.

Proposition 3.6.

The function is continuous. In particular, , , belonging to a compact real subset, is bounded.

Proof.

-

•

Proposition 3.1 implies that is continuous uniformly w.r.t. .

-

•

We first prove that , is continuous. Since , there is such that ; so

because is bounded, being of bounded variation. This implies that is uniformly integrable. Since is continuous in probability, then is continuous in . The partial result easily follows.

-

•

To conclude it remains to show that is continuous for every . Since , there is a sequence in the interior of converging to . Since a uniform limit of continuous functions on is a continuous function, the result follows.

∎

3.2 A reference variance measure

For notational convenience we introduce the set .

Remark 3.7.

We recall that is convex. Consequently we have.

-

1.

If , then . If then and .

-

2.

Since , clearly .

-

3.

Under Assumption 1 below, and so .

We introduce a new function that will be useful in the sequel.

Definition 3.8.

-

•

For any , if we denote

(3.3) -

•

To shorten notations will denote the real valued function such that,

(3.4) Notice that the latter equality results from Remark 2.2 1.

An important technical lemma follows below.

Lemma 3.9.

Let , with , then, is strictly increasing if and only if has no deterministic increments.

Proof.

It is enough to show that has no deterministic increments if and only if for any , the following quantity is positive,

| (3.5) |

By Remark 3.3, we have where Applying this property and Remark 2.2 1., to the exponential of the first term on the right-hand side of (3.5) yields

Similarly, for the exponential of the second term on the right-hand side of (3.5), one gets

Hence taking the exponential of yields

-

•

If has a deterministic increment , then is again deterministic and (3.2) vanishes and hence is not strictly increasing.

-

•

If has never deterministic increments, then the nominator is never zero, otherwise , and therefore would be deterministic.

∎

Remark 3.10.

If , setting in (3.2) implies that is equivalent to . Taking the process at discrete instants , one can define the discrete time process such that and derive the counterpart of Lemma 3.9 in the discrete time setting. Indeed, the following assertions are equivalent:

-

•

is an increasing sequence;

-

•

is never deterministic for any .

Moreover, accordingly to Proposition 3.10 in [22], we observe that, under one of the above equivalent conditions, the (discrete time) mean-variance trade-off process associated with defined by

is always bounded. According to Proposition 2.6 of [40], that condition guarantees that every square integrable random variable admits a discrete Föllmer-Schweizer decomposition. The process is the discrete analogous of the MVT process ; one can compare the mentioned result to item 1. of Theorem 2.6.

From now on, we will always suppose the following assumption.

Assumption 1.

-

1.

has no deterministic increments.

-

2.

.

We continue with a simple observation.

Lemma 3.11.

Let be a compact real interval included in . Then

Proof.

Let and , since is continuous, we have

∎

Remark 3.12.

From now on, in this section, will denote the measure

| (3.7) |

According to

Assumption 1 and Lemma 3.9, it is a positive measure which is strictly positive on each interval.

This measure will play a fundamental role.

We state below a result that will help us to show that is absolutely continuous w.r.t.

.

Lemma 3.13.

We consider two positive finite non-atomic Borel measures on , and . We suppose the following:

-

1.

-

2.

for every open ball of .

Then a.e. In particular and are equivalent.

Proof.

We consider the Borel set We want to prove that . So we suppose that there exists a constant such that and take another constant such that . Since is a Radon measure, there are compact subsets and of such that and Setting , we have and By Urysohn lemma, there is a continuous function such that, with on and on the closure of Now By continuity of there is an open set with for . Clearly ; since is relatively compact, it is a countable union of balls, and so contains a ball . The fact that on implies and this contradicts Hypothesis 2. of the statement. Hence the result follows.

∎

Remark 3.14.

-

1.

If , then point 2. of Lemma 3.13 becomes for every open interval .

-

2.

The result holds for every normal metric locally connected space , provided are Radon measures.

Proposition 3.15.

Under Assumption 1

| (3.8) |

Proof.

Remark 3.16.

Notice that this result also holds with instead of , for any such that .

3.3 On some semimartingale decompositions and covariations

Proposition 3.17.

Remark 3.18.

-

•

Clearly since and belong to and is convex by Proposition 3.1.

-

•

If , we have , so that by uniqueness of the special semimartingale decomposition, it follows that .

Proof.

Remark 3.19.

Lemma 3.11 implies that and so is a square integrable martingale for any .

3.4 On the Structure Condition

Proposition 3.17 with yields where and is a martingale such that At this point, the aim is to exhibit a predictable -valued process such that

-

1.

.

-

2.

is bounded.

In that case, according to item 1. of Theorem 2.6, there will exist a unique FS decomposition for any and so the minimization problem (2.2) will have a unique solution, characterized by Theorem 2.7 2.

Proposition 3.20.

Corollary 3.21.

Under Assumption 1, the structure condition (SC) is verified if and only if

In particular, is deterministic therefore bounded.

Remark 3.22.

Item 1. of Assumption 1 is natural. Indeed if it were not realized, i.e. if admits a deterministic increment on some interval , then would not fulfill the (SC) condition, unless is constant on . In this case, the market model would admit arbitrage opportunities.

Lemma 3.23.

The space , defined in (2.1), is constituted by all predictable processes such that

Proof.

According to Proposition 2.4, the fact that is bounded and satisfies (SC), then holds if and only if is predictable and . Since the assertion follows. ∎

3.5 Explicit Föllmer-Schweizer decomposition

We denote by the set of such that

| (3.12) |

From now on, we formulate another assumption.

Assumption 2.

.

Remark 3.24.

The proposition below will constitute an important step for determining the FS decomposition of the contingent claim for a significant class of functions , see Section 3.6.

Proposition 3.25.

Let with , (in particular ), then

Proof.

-

1.

is a consequence of Lemma 3.11.

-

2.

is square integrable because Assumption 2 and . Moreover is well-defined since

(3.18) -

3.

In order to prove that (3.15),(3.16) and (3.17) is the FS decomposition of , we need to show that

-

(a)

is -measurable,

-

(b)

-

(c)

where was defined in (2.1).

-

(d)

is a square integrable martingale.

We proceed similarly to the proof of Lemma 3.3 of [24]. Point (a) is obvious. Partial integration and point 1 of Proposition 3.17 yield

(3.19) On the other hand

(3.20) Hence, using expressions (3.19) and (3.20), by definition of in (3.14), which says we obtain

(3.21) which implies that is a local martingale.

From point 1. of Proposition 3.17, using (3.16), it follows thatThen by definition of in (3.13), yields Consequently, point (b) follows.

It remains to prove point (d) i.e. that is a square-integrable martingale for all and that and are in . (3.21) says that

By Remark 2.2 we observe first that . Moreover by definition of and , it follows

(3.22) By Proposition 3.17, 3.22 and (3.21), it follows

(3.23) Consequently

(3.24) Taking the expectation in (3.24), using point 2., (3.13), (3.14) and Lemma 3.11, we obtain

(3.25) Therefore, is a square-integrable martingale.

It remains to prove point (c) i.e. that . In view of applying Lemma 3.23, we evaluate(3.26) Similarly as for (3.24), we can show that the expectation of the right-hand side of (3.26) is finite. This concludes the proof of Proposition 3.25.

-

(a)

∎

3.6 FS decomposition of special contingent claims

We consider now payoff functions of the type

| (3.27) |

where is a (finite) complex measure in the sense of Rudin [33], Section 6.1. An integral representation of some basic European calls is provided in the sequel. We need now the new following assumption.

Assumption 3.

Let . We denote

-

1.

is compact.

-

2.

-

3.

.

-

4.

.

Remark 3.26.

- 1.

-

2.

Assumption 3 looks obscure. Examples for its validity will be provided in Section 5. For instance consider the specific case where is a Wiener integral driven by a Lévy process , i.e. and the payoffs are either a call or a put. We observe in Example 5.6 below that Assumptions 1, 2 and 3 are a consequence of the simple Assumption 4.

Remark 3.27.

We need now to obtain upper bounds on for the quantity (3.25). We will first need the following lemma which constitutes a (not straightforward) generalization of Lemma 3.4 of [24] which was stated when is a Lévy process. The fact that does not have stationary increments, constitutes a significant obstacle.

Remark 3.29.

-

1.

According to Proposition 3.25, is absolutely continuous w.r.t. .

-

2.

We recall that is included in .

-

Proof (of Lemma 3.28). According to Point 3. of Assumption 3 we denote

(3.28) For , we have Then, we get We obtain

(3.29) Since is increasing, taking into account (3.24), the measure is non-negative. It follows that

(3.30) By (3.30), in particular the density is non-negative a.e. Consequently,

(3.31) In order to prove 1. it is enough to verify that, for some ,

(3.32) In fact, (3.31), Assumption 3 point 3. and (3.28), imply that To prove (3.32) it is enough to show that

(3.33) Again Assumption 3 point 3. implies that

(3.34) where Using (3.30) and Assumption 3 it follows

(3.35) This implies that where is chosen such that . Consequently,

Coming back to (3.29), we obtain

(3.31) and Assumption 3 allow to establish

(3.36) where . This concludes the proof of point 1.

In order to prove point 2. we first observe that (3.32) implies(3.37) (3.35) implies where . Point 2. is now established with and .

We continue with the proof of point 3. We decompose where and are the increasing non negative functions given by

Moreover point 1. implies At this point, forwhich concludes the proof of point 3 of Lemma 3.28.

∎

Theorem 3.30.

Let be a finite complex-valued Borel measure on . Suppose Assumptions 1, 2, 3. Any complex-valued contingent claim , where is of the form (3.27), and , admits a unique FS decomposition with the following properties.

-

1.

and

where for , and are the same as those introduced in Proposition 3.25 and we convene that they vanish if .

-

2.

Previous decomposition is real-valued if is real-valued.

-

Proof (of Theorem 3.30). a) since by Jensen’s, where denotes the total variation of the finite measure . Previous quantity is bounded because of Lemma 3.11.

b) We go on with the FS decomposition. We would like to prove first that and are well defined square-integrable processes and .

By Jensen’s inequality, we haveSimilar calculations allow to show that

We will show now that

-

–

(A1):

-

–

(A2):

-

–

(A3):

(A1): Since , we have so

where is well defined by (3.38), below, since by Lemma 3.11,

(3.38) Lemma 3.28 implies (A1). Therefore is a well-defined square-integrable process. (A2): where the first inequality is due to the fact that is a submartingale.

By Fubini’s theorem, Lemma 3.11 and (3.24), we have

According to Lemma 3.28 point 2, previous expression is bounded by , where

(3.39) where and Using again Lemma 3.28, we obtain

(3.40) and so

(3.41) This concludes (A2).

We verify now the validity of (A3). This requires to controlUsing Jensen’s inequality, this is smaller or equal than

Lemma 3.28 gives the upper bound where was defined in (3.39). Since is finite and because of (3.40), (A3) is now established.

c) In order to conclude the proof of item 1., it remains to show that is an -martingale which is strongly orthogonal to . This can be established similarly as in [24], Proposition 3.1, by making use of Fubini’s theorem and Fubini’s theorem for stochastic integrals (cf. [31], Theorem IV.46) and (A1), (A2), (A3).Consequently, provide a (possibly complex) FS decomposition of .

-

–

-

d) It remains to prove item 2., that is to say that the decomposition is real-valued. Let and be two FS decomposition of . Consequently, since and are real-valued, we have which implies that . By Theorem 2.6 1., the uniqueness of the real-valued Föllmer-Schweizer decomposition yields that the processes , and are real-valued. ∎

3.7 Representation of call and put options

We used some integral representations of payoffs of the form (3.27). We refer to [15], [32] and more recently [17], for some characterizations of classes of functions which admit this kind of representation. In order to apply the results of this paper, we need explicit formulae for the complex measure in some example of contingent claims. Let be a strike.

-

The European Call option . For arbitrary , , we have

(3.42) -

The European Put option . For an arbitrary , , we have

(3.43)

4 The solution to the minimization problem

FS decomposition will help to provide the solution to the global minimization problem. Let be an additive process with cumulant generating function . We denote , . Next theorem deals with the case where the payoff to hedge is given as a bilateral Laplace transform of the exponential of the additive process . It is an extension of Theorem 3.3 of [24] to additive processes with no stationary increments.

Theorem 4.1.

Let where is of the form (3.27). We assume the validity of Assumptions 1, 2, 3. The variance-optimal capital and the variance-optimal hedging strategy , solution of the minimization problem , are given by and the implicit expression

| (4.1) |

where the processes , and are defined by

The optimal initial capital is unique. The optimal hedging strategy is unique up to some -null set.

Remark 4.2.

The mean variance trade-off process can be expressed as, see (3.11),

-

Proof (of Theorem 4.1).

When the underlying price is an exponential of additive process, we evaluate the so called variance of the hedging error of the contingent claim i.e. the quantity , where and were defined at Theorem 4.1.

Theorem 4.3.

This expression of the error involving the function (4.3), can be used to characterize the price models that are exponential of additive processes for which the market is complete, at least for vanilla option payoffs. For instance, by evaluating , we can verify, in Remarks 5.10 and 5.11, below, the complete market model property in the Poisson and the Gaussian case.

-

Proof (of Theorem 4.3). Since , is the trivial -field, therefore , because it is mean-zero and deterministic.

The quadratic error can be calculated using Theorem 2.7 3. It gives

(4.3) where is the remainder martingale in the FS decomposition of . We proceed now to the evaluation of . Similarly to the proof of Theorem 3.2 of [24], using (3.23), the bilinearity and the stability w.r.t. complex conjugate of the covariation together with (3.41), it is possible to show that

(4.4) It remains to evaluate for . We know by Proposition 3.17 that for all ,

Using the same terminology as in Proposition 3.25, similarly to (3.24) we have

We come back to (4.3). Recalling that where is the MVT process, we have

Since , an application of Fubini’s theorem yields

(4.5) which equals . (4.4), (4.5) and again Fubini’s theorem imply

This concludes the proof of Theorem 4.3. ∎

5 Examples

5.1 Exponential of a Wiener integral driven by a Lévy process

Let be a square integrable Lévy process and let be the cumulative generating function of with domain in the sense of Definition 2.1. is continuous because of Proposition 3.25. We observe that

| (5.6) |

where is a continuous function such that Let be a bounded Borel function. We will consider in this subsection the additive process . Let us define the set such that

Lemma 5.1.

The cumulant generating function of is such that for all , we have

In particular , where is the domain defined according to Definition 2.1.

Proof.

If is continuous, the result follows from the observation that is the limit in probability of where is a subdivision of whose mesh converges to zero. If is only Borel bounded the result can be established through approximation by convolution. ∎

We formulate the following hypothesis which will be in force for the whole subsection.

Assumption 4.

-

1.

-

2.

and .

Remark 5.2.

Lemma 3.9 applied to being the Lévy process implies that, for every , such that , we have

| (5.7) |

Remark 5.3.

Proof.

- 1.

- 2.

∎

Remark 5.5.

Suppose for a moment that

| (5.9) |

- 1.

- 2.

We consider again the same class of options as in previous subsections. To conclude the verification of Assumption 3 it remains to show the following.

-

•

is compact. This point will be trivially fulfilled in the specific cases.

-

•

(5.9).

Example 5.6.

Corollary 5.7.

We consider a process of the form

under Assumption 4.

The FS decomposition of an option of the type

and the related solution to the minimization problem

are provided by Theorem 3.30, Proposition 3.25

and Theorem 4.1 together with the expressions given below.

For we have

Again, for convenience, if then we define

5.2 Considerations about the Lévy case

If then coincides with the Lévy process and

Assumption 4 is equivalent to Hubalek et alia

Condition introduced in [24] i.e.

1. 2.

In that case we have .

Therefore

because

for any

We recall some cumulant and log-characteristic functions of some typical Lévy processes.

Remark 5.8.

-

1.

Poisson Case: If is a Poisson process with intensity , we have that . Moreover, in this case the set .

-

2.

NIG Case: This process was introduced by Barndorff-Nielsen in [5]. Then is a Lévy process with , with , and . We have and ,

-

3.

Variance Gamma case: Let . If is a Variance Gamma process with with where is again the principal value complex logarithm defined in Section 2. The expression of can be found in [24, 27] or also [13], table IV.4.5 in the particular case . In particular an easy calculation shows that we need such that so that is well-defined so that

Remark 5.9.

We come back to the examples introduced in Remark 5.8. In all the three cases, Hubalek et alia Condition is verified if . This happens in the following situations:

-

1.

always in the Poisson case;

-

2.

if is a NIG process and if

-

3.

if is a VG process and if

Remark 5.10.

If X is a Poisson process with parameter then the quadratic error is zero. In fact,

imply that for every .

Therefore . In particular all the options of type (3.27) are perfectly hedgeable.

5.3 About some singular non-stationary models

Here, we consider some singular models, in the sense that the cumulant generating function of the log-price process is not

absolutely continuous with respect to (a.c. w.r.t.) Lebesgue measure.

More precisely, let be a standard Brownian motion. A classical approach to model the volatility clustering effect consists in introducing the notion of trading time (as opposed to the real time) which accelerates or slows down the price process depending on the activity on the market. This virtual time is represented by a change of time and the log-price is then constructed by subordination

i.e. .

Now, if the change of time is singular,

then it can be proved that the log-price process is also singular.

This typically happens when the change of time

, is obtained as the cumulative distribution function of a deterministic positive multifractal measure , singular w.r.t. Lebesgue measure.

Multifractal measures

were introduced in the physical sciences to model turbulent flows [28].

More recently, in [10], the authors used this construction precisely for modeling financial volatility. But their model, the Multifractal Model of Asset Returns (MMAR), relies on a random (and not deterministic) multifractal

measure and is hence beyond the framework of this paper.

Below, we consider two examples of singular

non-stationary log-price models based on such (deterministic or random)

singular changes of time.

-

1.

Deterministic change of time (log-Gaussian continuous process): Let us consider the log-price process such that , where is a strictly increasing function, including the pathological case where a.e. For , we have so that Notice that is not necessarily a. c. w.r.t. Lebesgue measure and that this is verified as soon as . Assumption 1 1. is verified since is strictly increasing; Assumption 1 2., Assumption 2 and Assumption 3 are verified since and is continuous. Consequently all the conditions to apply Theorem 4.1 are satisfied and

Remark 5.11.

Calculating in (4.3), we find . Therefore here also the quadratic error is zero. This confirms the fact that the market is complete, at least for the considered class of options.

-

2.

Random change of time: Let denote an increasing Lévy process such that follows an Inverse Gaussian distribution with parameters and . Now, let us consider the process such that , for all , with . Then one can prove that is a NIG Lévy process with . Finally, let us consider the log-price process such that , where and is the cumulative distribution of a deterministic multifractal measure on . Hence, the cumulant generating function of is singular w.r.t. Lebesgue measure and is given by with , for all

6 Application to Electricity

6.1 Hedging electricity derivatives with forward contracts

Because of non-storability of electricity, no dynamic hedging strategy can be performed on the spot market. Hedging instruments for electricity derivatives are then futures or forward contracts. For simplicity, we will assume that interest rates are deterministic and zero so that futures prices are equivalent to forward prices. The value of a forward contract offering the fixed price at time for delivery of 1MWh at time is by definition of the forward price, . Indeed, there is no cost to enter at time the forward contract with the current market forward price . Then, the value of the same forward contract at time is deduced by an argument of Absence of (static) Arbitrage as . Hence, the dynamics of the hedging instrument is directly related (for deterministic interest rates) to the dynamics of forward prices . Consequently, in the sequel, when considering hedging on electricity markets, we will always suppose that the underlying is a forward contract and we will focus on the dynamics of forward prices.

6.2 Electricity price models for pricing and hedging application

Observing market data, one can notice two main stylized features of electricity forward prices:

-

•

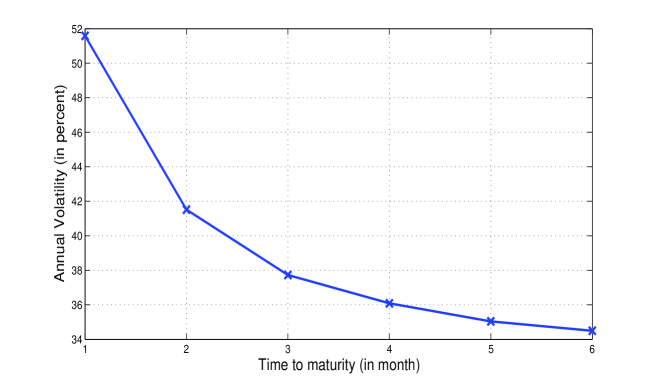

Volatility term structure of forward prices: the volatility increases when the time to maturity decreases. Indeed, when the delivery date approaches, the flow of relevant information affecting the balance between electricity supply and demand increases and causes great variations in the forward prices. This maturity effect is usually referred to as the Samuelson hypothesis, it was first studied in [34] and can be observed on Figure 1, in the case of electricity futures prices.

-

•

Non-Gaussianity of log-returns: log-returns can be considered as Gaussian for long-term contracts but begin to show heavy tails for short-term contracts.

Hence, a challenge is to be able to describe with a single model, both the non-Gaussianity on the short term and the volatility term structure of the forward curve. One reasonable attempt to do so is to consider the exponential Lévy factor model, proposed in [9] or [12]. The forward price given at time for delivery at time , denoted is then modeled by a -factors model, such that

| (6.10) |

-

•

is a real deterministic trend;

-

•

for any , is such that , where is a Lévy process on , with and ;

-

•

are called respectively the volatilities and the mean-reverting rates.

Hence, forward prices are given as exponentials of

additive processes with non-stationary increments.

In practice, we consider the case of a one or a two factors model (

or ), where the first factor is a non-Gaussian

additive process and the second factor is a Brownian motion with .

Notice that this kind of model was originally developed and studied in

details for interest rates in [32], as an extension of

the Heath-Jarrow-Morton model where the Brownian motion has

been replaced by a general Lévy process.

Of course, this modeling procedure (6.10), implies

incompleteness of the market. Hence, if we aim at pricing and hedging a

European call on a forward with maturity , it won’t be possible,

in general, to hedge perfectly the payoff with a hedging

portfolio of forward contracts.

Then, a natural approach could consist in looking for the variance

optimal initial capital and hedging portfolio. In this framework, the results of

Section 3 generalizing the results of Hubalek & al

in [24] to the case of non stationary additive process can be

useful.

6.3 The non Gaussian two factors model

To simplify let us forget the superscript denoting the delivery period (since we will consider a fixed delivery period). We suppose that the forward price follows the two factors model

| (6.11) |

-

•

is a real deterministic trend starting at . It is supposed to be absolutely continuous w.r.t. Lebesgue;

-

•

, where is a Lévy process on with following a Normal Inverse Gaussian (NIG) distribution or a Variance Gamma (VG) distribution. Moreover, we will assume that and ;

-

•

where is a standard Brownian motion on ;

-

•

and are independent;

-

•

and standing respectively for the short-term volatility and long-term volatility.

6.4 Verification of the assumptions

The result below helps to extend Theorem 4.1 to the case where is a finite sum of independent semimartingale additive processes, each one verifying Assumptions 1, 2 and 3 for a given payoff .

Lemma 6.1.

Proof.

With the two factors model, the forward price is then given as the exponential of an additive process, , such that for all ,

| (6.12) |

For this model, we formulate the following assumption.

Assumption 5.

Proposition 6.2.

Proof.

We set . We observe that We recall that and are independent so that and are independent. For clarity, we only write the proof under the hypothesis that has no deterministic increments, the general case could be easily adapted. is a process of the type studied at Section 5.1; it verifies Assumption 4 and contains .

The solution to the mean-variance problem is provided by Theorem 4.1.

Theorem 6.3.

Remark 6.4.

Previous formulae are practically exploitable numerically. The last condition to be checked is

| (6.14) |

-

1.

is a Normal Inverse Gaussian random variable; if then is verified.

-

2.

is a Variance Gamma random variable then is verified; if for instance

7 Simulations

We are interested in comparing, in simulations, the Variance Optimal (VO) strategy to

the Black-Scholes (BS) strategy when hedging a European call, with payoff ,

on an underlying stock with log-prices that have independent but non Gaussian increments. More precisely, we assume that the underlying is an electricity forward contract

with delivery date equal to the maturity of the call

.

First, we consider the case where the log-price

process is an exponential of a Lévy process,

continuing the analysis of [24], then we consider the non

stationary case.

We make use of different simulated data according to the underlying model,

stationary in one case, non stationary in the second one.

Our simulations investigate two features which were not considered in

[24] (even in the stationary case): first the robustness of the

BS hedging strategy w.r.t.

the underlying price model, second the sensitivity of the continuous

VO strategy w.r.t. to the discreteness of the trading dates.

The VO strategy knows the real incomplete price model (with the real values of parameters) whereas the BS strategy assumes (wrongly) a log-normal price model (with the real values of mean and variance). Of course, the VO strategy is by definition optimal, w.r.t. the quadratic norm. However, both strategies (VO and BS) are implemented in discrete time, hence our goal is precisely to analyze the hedging error outside of the theoretical framework of a continuously rebalanced portfolio. Moreover, we are interested in interpreting quantitatively the differences between both strategies w.r.t. to some characteristics such as the underlying log-returns distribution or the number of trading dates.

The time unit is the year and the interest rate is zero in all our simulations. The initial value of the underlying is Euros. The maturity of the option is i.e. three months from now.

7.1 Exponential Lévy

In this subsection, we simulate the log-price process as a NIG Lévy process with . Five different sets of parameters for the NIG distribution have been considered, going from the case of almost Gaussian returns corresponding to standard equities, to the case of highly non Gaussian returns. The standard set of parameters is estimated on the Month-ahead base forward prices of the French Power market in 2007:

| (7.15) |

Those parameters imply a zero mean, a standard deviation of , a skewness (measuring the asymmetry) of and an excess kurtosis (measuring the fatness of the tails) of . The other sets of parameters are obtained by multiplying the parameter by a coefficient , () being such that the first three moments are unchanged. Note that when grows to infinity the tails of the NIG distribution get closer to the tails of the Gaussian distribution. For instance, Table 1 shows how the excess kurtosis (which is zero for a Gaussian distribution) is modified with the five values of chosen in our simulations.

| Coefficient | |||||

|---|---|---|---|---|---|

| Excess kurtosis |

7.1.1 Strike impact on the initial capital and the hedging ratio

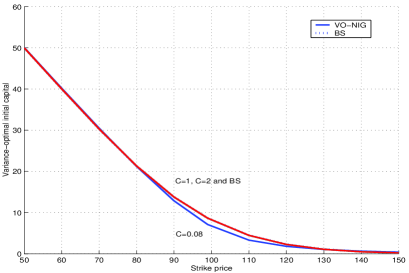

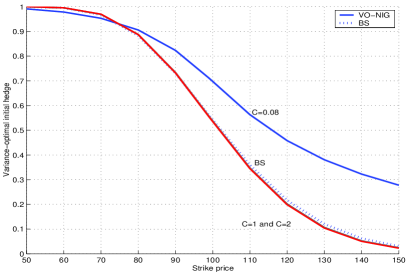

Figure 2 shows the initial capital (on the left graph) and the initial hedge ratio (on the right graph) produced by the VO and the BS strategies as functions of the strike, for three different sets of parameters . We consider trading dates, which corresponds to operational practices on electricity markets, for an option expiring in three months. One can observe that BS results are very similar to VO results for i.e. for almost Gaussian returns. However, for small values of , for , corresponding to highly non Gaussian returns, BS approach under-estimates out-of-the-money options and over-estimates at-the-money options (for Euros the BS initial capital is equal to Euros i.e. of the VO initial capital, while for , it vanishes to Cents i.e. only of the VO initial capital).

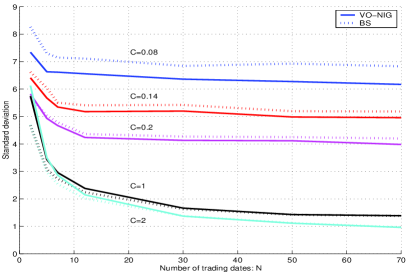

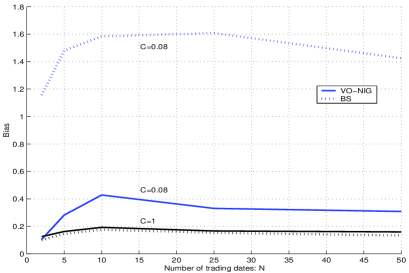

7.1.2 Hedging error and number of trading dates

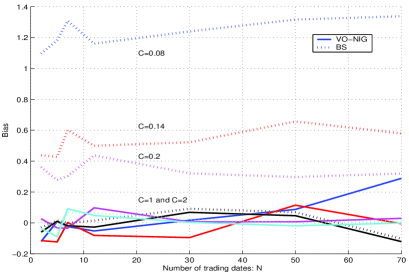

Figure 3 considers the hedging error (the difference between the terminal value of the hedging portfolio and the payoff) w.r.t. the number of trading dates, for a strike Euros (at the money) and for five different sets of parameters given on Table 1. The bias (on the left graph) and standard deviation (on the right graph) of the hedging error have been estimated by Monte Carlo method on runs. Note that we could have used the formula stated in Theorem 4.3 to compute the variance of the error, but this would have given us the limiting error which does not take into account the additional error due to the finite number of trading dates.

In terms of standard deviation, the VO strategy seems to outperform noticeably the BS strategy, for small values of ( for the VO strategy allows to reduce of the standard deviation of the error). As expected, one can observe that the VO error converges to the BS error when increases. This is due to the convergence of NIG log-returns to Gaussian log-returns when increases (recall that the simulated log-returns are almost symmetric). On Figure 3, the hedging error (both for BS and VO) decreases with the number of trading dates and seems to converge to a limiting error. Here, it is interesting to distinguish two sources of incompleteness, the rebalancing error due to the finite number of trading dates and the intrinsic error due to the price model incompleteness. For instance, one can observe that for small values of , even for small numbers of trading dates, the intrinsic error seems to be predominant so that it seems useless to increase the number of trading dates over trading dates. Moreover, surprisingly one can observe that for a small number of trading dates and for large values of , BS seems to outperform the VO strategy, in terms of standard deviation. This can be interpreted as a consequence of the central limit theorem. Indeed, when the time between two trading dates increases the corresponding increments of the Lévy process converge to a Gaussian variable. Similarly to the observation of [16], section 5., in term of hedging errors, BS strategy seems to be quite close to VO strategy. The same kind of conclusions were obtained in the discrete time setting by [1].

In term of bias, the over-estimation of at-the-money options (observed for , on Figures 2) seems to induce a positive bias for the BS error (see Figure 3), whereas the bias of the VO error is negligible (as expected from the theory).

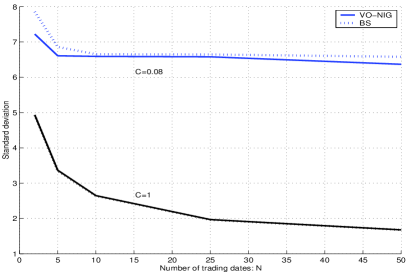

7.2 Exponential of additive processes

In this subsection, we simulate the log-price process as an additive process such that

The standard set of parameters for the distribution of is estimated on the same data as in the previous section (Month-ahead base forward prices of the French Power market in 2007):

Those parameters correspond to a standard and centered NIG distribution with a skewness of . The estimated annual short-term volatility and mean-reverting rate are and . The other sets of parameters considered in simulations are obtained by multiplying parameter by a coefficient , ( being such that the first three moments are unchanged).

The results are comparable to those obtained in the case of the Lévy process, on Figure 4.

ACKNOWLEDGEMENTS: The first named author was partially founded by Banca Intesa San Paolo. The research of the third named author was partially supported by the ANR Project MASTERIE 2010 BLANC-0121-01. All the authors are grateful to F. Hubalek for useful advices to improve the numerical computations of Laplace transforms performed in simulations. They also thank the Referee for reading carefully the manuscript and making useful comments.

References

- [1] Angelini, F. and Herzel., S. (2009). Measuring the error of dynamic hedging: a Laplace transform approach. Computational Finance, Vol. 12 (2).

- [2] Ansel, J-P. and Stricker, C. (1992). Lois de martingale, densités et décomposition de Föllmer-Schweizer. Annales de l’Institut Henri Poincaré 28, 375-392.

- [3] Arai, T. (2005). Some properties of the variance-optimal martingale measure for discontinuous semimartingales. Statistics and Probability Letters 74, 163-170.

- [4] Arai, T. (2005). An extension of mean-variance hedging to the discontinuous case. Finance and Stochastics 9, 129-139.

- [5] Barndorff-Nielsen, O.E. and Halgreen, C. (1977). Infinite divisibility of the hyperbolic and generalized inverse Gaussian distributions. Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete, Vol. 38, 309-312.

- [6] Barndorff-Nielsen, O.E. (1998). Processes of normal inverse Gaussian type. Finance and Stochastics 2, 41-68.

- [7] Benth, F. E., Di Nunno, G., Løkka, A., Øksendal, B., Proske, F. (2003). Explicit representation of the minimal variance portfolio in markets driven by Lévy processes. Conference on Applications of Malliavin Calculus in Finance (Rocquencourt, 2001). Math. Finance 13, no. 1, 55–72.

- [8] Benth, F. E. and Saltyte-Benth, J. and Koekebakker, S. (2008). Stochastic modelling of electricity and related markets. Advanced Series on statistical Science & Applied Probability, Vol. 11 / World Scientific.

- [9] Benth, F.E. and Saltyte-Benth, J. (2004). The normal inverse Gaussian distribution and spot price modeling in energy markets. International journal of theoretical and applied finance, Vol. 7(2), 177-192.

- [10] Calvet, L. and Fisher, A. and Mandelbrot, B. (1997). A multifractal model of asset returns. Discussion Papers, Cowles Foundation Yale University: 1164–1166.

- [11] ern, A. and Kallsen, J. (2007). On the structure of general man-variance hedging strategies. The Annals of probability, vol 35 No. 4, 1479-1531.

- [12] Collet, J., Duwig, D. and Oudjane N. (2006). Some non-Gaussian models for electricity spot prices. In Proceedings of the 9th International Conference on Probabilistic Methods Applied to Power Systems.

- [13] Cont, R. and Tankov, P. (2003). Financial modelling with jump processes. Chapman & Hall/CRC Press.

- [14] Cont, R., Tankov, P. and Voltchkova, E. (2007). Hedging with options in models with jumps. Stochastic analysis and applications, 197–217, Abel Symp., 2, Springer, Berlin.

- [15] Cramer, H. (1939). On the representation of a function by certain Fourier integrals. Transactions of the American Mathematical Society 46, 191-201.

- [16] Denkl, S., Goy, M., Kallsen J., Muhle-Karbe, J. and Pauwels, A. (2011). On the Performance of Delta Hedging Strategies in Exponential Lévy Models. Preprint arXiv:0911.4859v3.

- [17] Eberlein, E., Glau, C. and Papapantoleon, A. (2010). Analysis of Fourier transform valuation formula and applications. Appl. Math. Finance, 17, no. 3, 211–240.

- [18] El Karoui, N. and Quenez, M. (1995). Dynamic programming and pricing of contingent claims in an incomplete market. SIAM journal on Control and Optimization, vol 33, 29-66.

- [19] Filipović, D. (2005). Time-inhomogeneous affine processes. Stochastic Processes and Their Applications 115, 639-659.

- [20] Föllmer, H. and Leukert, P. (1999). Quantile hedging. Finance and Stochastics 3, no. 3, 251-273.

- [21] Föllmer, H. and Schweizer, M. (1991). Hedging of contingent claims under incomplete information. M. H. A. Davis and R. J. Elliott (eds.), Applied stochastic analysis, 389-414, Stochastics Monogr., 5, Gordon & Breach, New York.

- [22] Goutte, S., Oudjane, N. and Russo, F. (2010). Variance Optimal Hedging for discrete time processes with independent increments. Application to Electricity Markets. Preprint HAL-INRIA http://hal.inria.fr/inria-00473032 to appear in the Journal of computational Finance in 2013.

- [23] Hodges, S. and Neuberger, A. (1989). Optimal replication of contingent claims under transactions costs. Review of forward markets, vol 8, 222-239.

- [24] Hubalek, F., Kallsen, J. and Krawczyk, L.(2006). Variance-optimal hedging for processes with stationary independent increments. The Annals of Applied Probability, Volume 16, Number 2, 853-885.

- [25] Jacod, J. and Shiryaev, A. (2003). Limit theorems for stochastic processes. 2nd edition. Berlin Springer.

- [26] Kluge, W. (2005). Time-inhomogeneous Lévy processes in interest rate and credit risk modeling. Dissertation, Freiburg. http://www.freidok.uni-freiburg.de/volltexte/2090/pdf/diss.pdf

- [27] Madan, D.B., Carr, P.P. and Chang, E.C. (1998). The variance gamma process and option pricing. European Finance Review, 2, 79-105.

- [28] Mandelbrot, B. B. (1972). Possible Refinements of the Lognormal Hypothesis Concerning the Distribution of Energy Dissipation in Intermittent Turbulence. In: M. Rosenblatt and C. Van Atta eds., Statistical Models and Turbulence, New York: Springer Verlag.

- [29] Meyer-Brandis, T. and Tankov, P. (2008). Multi-factor jump-diffusion models of electricity prices. International Journal of Theoretical and Applied Finance, Vol. 11, No. 5, 503 - 528.

- [30] Monat, P. and Stricker, C. (1995). Föllmer-Schweizer decomposition and mean-variance hedging for general claims. The Annals of Probability, Vol. 23, No.2, 605-628.

- [31] Protter, P. (2004). Stochastic integration and differential equations. 2nd edition. Berlin Springer-Verlag.

- [32] Raible, S. (2000). Lévy processes in finance: theory, numerics and empirical facts. PhD thesis, Freiburg University.

- [33] Rudin, W. (1987). Real and complex analysis. Third edition. New York: McGraw-Hill.

- [34] Samuelson, P.A., (1965). Proof that properly anticipated prices fluctuate randomly. Industrial Management Review 6: 41-49.

- [35] Sato, K. (1999). Lévy processes and infinitely divisible distributions. Cambridge: Cambridge University Press.

- [36] Schäl, M. (1994). On quadratic cost criteria for options hedging. Mathematics of Operations Research 19, 121-131.

- [37] Schwartz, E.S. (1997). The stochastic behaviour of commodity prices: implications for valuation and hedging. Journal of Finance, LII, 923-973.

- [38] Schweizer, M. (1994). Approximating random variables by stochastic integrals. The Annals of Probability Vol. 22, 1536-1575.

- [39] Schweizer, M. (1995). On the minimal martingale measure and the Föllmer-Schweizer decomposition. Stochastic Analysis and Applications, 573-599.

- [40] Schweizer, M. (1995). Variance-optimal hedging in discrete time. Mathematics of Operations Research 20, 1-32.

- [41] Schweizer, M. (1996). Approximation pricing and the variance-optimal martingale measure. The Annals of Probability Vol. 24, 206-236.

- [42] Schweizer, M. (2001). A guided tour through quadratic hedging approaches. Option pricing, interest rates and risk management. 538-574, Handb. Math. Finance, Cambridge Univ. Press, Cambridge.

- [43] Schweizer, M. (2010). Mean variance hedging. In R. Cont (ed.), Encyclopedia of Quantitative Finance, Wiley, 1177-81.