Optimal dividends in the dual model under transaction costs

Abstract.

We analyze the optimal dividend payment problem in the dual model under constant transaction costs.

We show, for a general spectrally positive Lévy process, an optimal strategy is given by a -policy that brings the surplus process down to whenever it reaches or exceeds for some . The value function is succinctly expressed in terms of the scale function. A series of numerical examples are provided to confirm the analytical results and to demonstrate the convergence to the no-transaction cost case, which was recently solved by Bayraktar et al. [8].

Key words: dual model; dividends; impulse control;

spectrally positive Lévy processes; scale functions.

JEL Classification: C44, C61, G24, G32, G35

AMS 2010 Subject Classifications: 60G51, 93E20

1. Introduction

We solve the optimal dividend problem under fixed transaction costs in the so-called dual model, in which the surplus of a company is driven by a Lévy process with positive jumps (spectrally positive Lévy process). This is an appropriate model for a company driven by inventions or discoveries. The case without transaction costs has recently been well-studied; see [3], [7], [2], and [4]. In particular, in [8], we show the optimality of a barrier strategy (reflected Lévy process) for a general spectrally positive Lévy process of bounded or unbounded variation.

A strategy is assumed to be in the form of impulse control; whenever dividends are accrued, a constant transaction cost is incurred. As opposed to the barrier strategy that is typically optimal for the no-transaction cost case, we shall pursue the optimality of the so-called -policy that brings the surplus process down to whenever it reaches or exceeds for some . While, as in [18, 22], an optimal strategy may not lie in the set of -policies for the spectrally negative Lévy case, we shall show that it is indeed so in the dual model for any choice of underlying spectrally positive Lévy process. As a related work, we refer the reader to a compound Poisson dual model by [25] where transaction costs are incurred for capital injections. In inventory control, the optimality of similar policies, called -policies, is shown to be optimal in [9, 10] for a mixture of a Brownian motion and a compound Poisson process and in [24] for a general spectrally negative Lévy process.

Following [8], we take advantage of the fluctuation theory for the spectrally positive Lévy process (see e.g. [11], [13] and [17]). The expected net present value (NPV) of dividends (minus transaction costs) under a -policy until ruin is first written in terms of the scale function. We then show the existence of the maximizers that satisfy the continuous fit (resp. smooth fit) at when the surplus process is of bounded (resp. unbounded) variation and that the derivative at is one when and is less than or equal to one when . These properties are used to verify the optimality of the -policy.

In order to evaluate the analytical results and to examine the connection with the no-transaction cost case developed by [8], we conduct a series of numerical experiments using Lévy processes with positive i.i.d. phase-type jumps with or without Brownian motion [1]. We shall confirm the existence of the maximizers and examine the shape of the value function at and . We further compute for a sequence of unit transaction costs and confirm that, as , the value function as well as and converge to the ones obtained for the no-transaction cost case in [8].

The rest of the paper is organized as follows. Section 2 gives a mathematical model of the problem. In Section 3, we compute the expected NPV of dividends under the -policy via the scale function. Section 4 shows the existence of that maximize the expected NPV over and . Section 5 verifies the optimality of the -policy. We conclude the paper with numerical results in Section 6.

2. Mathematical Formulation

We will denote the surplus of a company by a spectrally positive Lévy process whose Laplace exponent is given by

| (2.1) |

where is a Lévy measure with the support that satisfies the integrability condition . It has paths of bounded variation if and only if and . In this case, we write (2.1) as

with ; the resulting drift of the process is . We exclude the trivial case in which is a subordinator (i.e., has monotone paths a.s.). This assumption implies that when is of bounded variation.

Let be the conditional probability under which (also let ), and let be the filtration generated by . Using this, the drift of is given by

| (2.2) |

In order to make sure the problem is non-trivial and well-defined, we assume throughout the paper that this is finite.

Assumption 2.1.

We assume that .

A (dividend) strategy is given by a nondecreasing, right-continuous and -adapted pure jump process starting at zero in the form with , . Corresponding to every strategy , we associate a controlled surplus process , which is defined by

where is the initial surplus and . The time of ruin is defined to be

A lump-sum payment cannot be more than the available funds and hence it is required that

| (2.3) |

Let be the set of all admissible strategies satisfying (2.3). The problem is to compute, for , the expected NPV of dividends until ruin

where is the unit transaction cost, and to obtain an admissible strategy that maximizes it, if such a strategy exists. Hence the (optimal) value function is written as

| (2.4) |

3. The -policy

We aim to prove that a -policy is optimal for some . For , a -policy, , brings the level of the controlled surplus process down to whenever it reaches or exceeds . Let us define the corresponding expected NPV of dividends as

| (3.1) |

where is the corresponding ruin time. In this section, we shall express these in terms of the scale function.

3.1. Scale functions

Fix . For any spectrally positive Lévy process, there exists a function called the q-scale function

which is zero on , continuous and strictly increasing on , and is characterized by the Laplace transform:

where

Here, the Laplace exponent in (2.1) is known to be zero at the origin and convex on ; therefore is well-defined and is strictly positive as . We also define, for ,

Notice that because is uniformly zero on the negative half line, we have

| (3.2) |

Let us define the first down- and up-crossing times, respectively, by

| (3.3) |

Then we have for any

| (3.4) | ||||

Notice for the case of spectrally negative Lévy process starting at , analogous results hold by replacing with .

Fix and define as the Laplace exponent of under with the change of measure

| (3.5) |

see page 213 of [17]. It is given for all by

If and are the scale functions associated with under (or equivalently with ). Then, by Lemma 8.4 of [17],

| (3.6) |

which is well-defined even for by Lemmas 8.3 and 8.5 of [17].

Remark 3.1.

-

(1)

If is of unbounded variation, it is known that is ; see, e.g., Chan et al. [12]. Hence,

-

(a)

is and for the bounded variation case, while it is and for the unbounded variation case, and

-

(b)

is and for the bounded variation case, while it is and for the unbounded variation case.

-

(a)

-

(2)

Regarding the asymptotic behavior near zero, we have that

(3.7) and

(3.8) -

(3)

As in (8.18) and Lemma 8.2 of [17],

where is understood as the right-derivative if it is not differentiable. In all cases, for all .

3.2. The expected NPV of dividends for the -policy

Now we obtain (3.1) using the scale function. By the strong Markov property, it must satisfy, for every and ,

| (3.9) |

where . Solving for , we have

| (3.10) |

The Laplace transform , , was computed in Corollary 3 of [15]. The following result is the derivative of this transform at .

Lemma 3.1.

For ,

where

4. Candidate strategies

Using the results in the previous section, we now have an analytical expression for (3.1) or equivalently (3.9). For and , this expression reduces to

| (4.1) | ||||

where

| (4.2) | ||||

For , we have

| (4.3) |

In view of (4.3), a necessary condition for a -policy to be optimal is that and maximize . In this section, we first obtain the first-order conditions by computing its partial derivatives with respect to and and then show the existence of finite-valued maximizers. In the rest of the paper, the derivative is understood as the right-derivative when the scale function fails to be differentiable on .

4.1. First-order conditions

Lemma 4.1.

For every ,

Proof.

Lemma 4.2.

For ,

where

Remark 4.1.

The first-order conditions obtained above are for (4.3). However, these are in fact the same for (4.1) for any . Differentiating the first equality of (4.1),

| (4.4) |

whose sign is the same as that of thanks to (3.4) which guarantees that the expression inside the square brackets is positive. Moreover, by differentiating (4.1) and by Lemma 4.1, for ,

whose sign is the same as that of due to item (3) of Remark 3.1.

4.2. Existence and some properties of maximizers

Now we are ready to show that the maximizers of exist. We will also describe equations that can be used to identify these points.

Lemma 4.3.

We have for sufficiently large .

Proof.

By Lemma 3.1 and (3.4), for any ,

and hence

| (4.5) | ||||

where , . It follows from Exercise 8.5 of [17] and Proposition 2 of [5] that and as , respectively. As a result, and hence there exists such that

| (4.6) |

Now because by Remark 3.1(3), we have for any . Hence for any fixed ,

Now by the definition of as in (3.10), for any fixed ,

which is negative by (4.6). On the other hand, because and attain , we have

| (4.7) |

Lemma 4.4.

Fix any , .

This lemma, together with Lemma 4.1 and Remark 3.1(3), implies that, for any fixed , is negative near ; consequently there exist (which can be shown to be when is of unbounded variation). Because is continuous and we have a compact domain for large by Lemma 4.3, we have a maximum. Furthermore, Lemmas 4.1 and 4.4 show that if and maximize , it must hold that is away from .

Lemma 4.5.

Suppose and maximize . Then and . In particular, if , we must have .

Proof.

Combining the above arguments, we arrive at the following proposition.

Proposition 4.1.

There exist that maximize and satisfy the following two properties.

-

(1)

and ;

-

(2)

either with , or with .

Remark 4.2.

Suppose and are such that and . Then, . To see why this is so, by Lemma 4.4, implies that and, together with , we have .

5. Verification of optimality

By Proposition 4.1, there exist such that and either

- Case 1:

-

with , or

- Case 2:

-

with .

We will show that such a -policy describes an optimal policy (and as a result the conditions written in terms of and are both necessary and sufficient for to be optimal.) Propositions 5.1 and 5.2 will play a key role.

By substituting in (4.1),

In fact, by (3.2) and by the definition of as in (4.2), we can write for any ,

| (5.1) |

It is clear that it is continuous at . Regarding its differentiability, we have

| (5.2) | ||||

whose limit equals

| (5.3) |

Because , the differentiability at is satisfied if and only if is of unbounded variation by (3.7) and Remark 4.2. We summarize these observations in the lemma below.

Lemma 5.1 (smoothness at ).

The function is continuous (resp. differentiable) at when is of bounded (resp. unbounded) variation.

Remark 5.1.

By Remark 3.1(1) and Lemma 5.1, the function is and (resp. and ) when is of bounded (resp. unbounded) variation.

Let be the infinitesimal generator associated with the process applied to a sufficiently smooth function

Here makes sense anywhere on .

Proposition 5.1.

-

(1)

for ,

-

(2)

for .

Proof.

(1) By Proposition 2 of [5] and as in the proof of Theorem 8.10 of [17], the processes

are martingales. Thanks to the smoothness of and on (see Remark 3.1(1)), we obtain for any . This step is similar to the proof of Theorem 2.1 in [8]. This implies claim (1) in view of (5.1).

Proposition 5.2.

For any , it holds that .

In order to show this proposition, we take advantage of the slope of at . By (5.2),

When , the derivative is understood as the right-derivative. Hence we arrive at the following.

Lemma 5.2 (slope at ).

For both Cases 1 and 2, . In particular, for Case 1, .

Lemma 5.3.

For any , if and only if .

Proof.

Because on , we shall focus on . Rewriting (5.4),

| (5.6) |

where . By Remarks 3.1(3) and 4.2, is decreasing on , and hence there exists a unique level such that (5.6) is negative if and only if . In other words, there are three possibilities

-

(i)

is strictly concave on or

-

(ii)

is strictly concave on and strictly convex on ,

-

(iii)

is strictly convex on .

Case 1: Suppose with . By Lemma 5.2, (5.3) and Remark 4.2,

| (5.7) |

Therefore we can safely rule out (iii) and we must have either (i) or (ii) with . For (i) (thus is decreasing on ), given , if and only if . Now suppose (ii) with . Then by the concavity on and , we have on and on . For , by the convexity on and (5.7), .

Case 2: Suppose with . In view of (5.2) and the definition of , we must have that . This together with shows that on for any of (i), (ii) and (iii). ∎

Next, we will verify the optimality of the -policy.

Theorem 5.1.

We have for every and the -policy is optimal.

Proof.

Here we only provide a sketch of a proof since it is similar to that of Lemma 6 of [18]. To verify the optimality of we only need to show that , , for all . But this result follows from applying the Itô formula to for an arbitrary , using Propositions 5.1 and 5.2 and then passing to the limit using Fatou’s lemma. Here one should be careful in applying the Itô formula since the value function may not be smooth enough at to apply the usual version. When of unbounded variation, we use Theorem 3.2 of [20], which shows that the smooth fit principle (which we proved in Lemma 5.1) is enough to kill the local time terms that might accumulate around ; see also Theorem IV.71 of [21], or Exercise 3.6.24 of [16]. On the other hand, when is of bounded variation recall from Lemma 5.1 that the value function is only continuous. However, in this case we do not need the smoothness of the value function at , simply because the first derivative term is integrated against the Lebesgue measure which is a diffuse measure. We could also directly use the first part of Theorem 6.2 of [19]. ∎

We conclude this section by showing the uniqueness of ; recall that the existence was proved in Proposition 4.1.

Proposition 5.3.

The maximizer is unique.

6. Numerical Examples

In this section, we confirm the results numerically using the spectrally positive Lévy process with i.i.d. phase-type distributed jumps [1] of the form

for some and . Here is a standard Brownian motion, is a Poisson process with arrival rate , and is an i.i.d. sequence of phase-type-distributed random variables with representation ; see [1]. The processes , and are assumed to be mutually independent. Its Laplace exponent (2.1) is then

which is analytic for every except at the eigenvalues of . Suppose is the set of the roots of the equality with negative real parts, and if these are assumed distinct, then the scale function can be written

| (6.1) |

where

see [14]. Here and are possibly complex-valued.

In our example, we shall choose a phase-type distribution which does not have a completely monotone density. Recall that, in the spectrally negative counterpart [18], the -policy may fail to be optimal if the Lévy density is not completely monotone. On the other hand, in the dual model, there is no restriction on the Lévy measure. We assume and

which give an approximation of the Weibull distribution with density function for and , obtained using the EM-algorithm; see [14] regarding the approximation performance of the corresponding scale function. Throughout this section, we let and let other parameters vary so as to see their impacts on the optimal strategy and the value function.

In our first experiment, we let , or with

- Case 1:

-

and

- Case 2:

-

and

and obtain the optimal strategies/value functions and confirm the analytical results obtained in the previous sections. We choose these parameters so that for Case 1 and for Case 2.

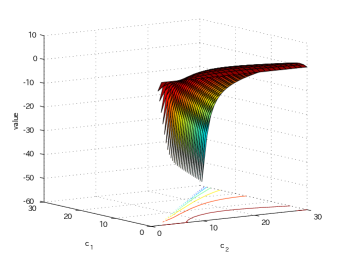

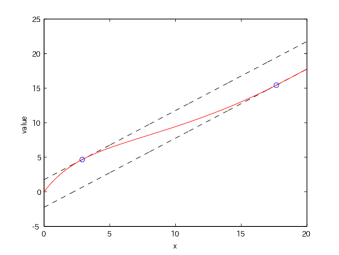

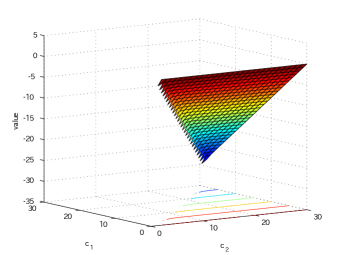

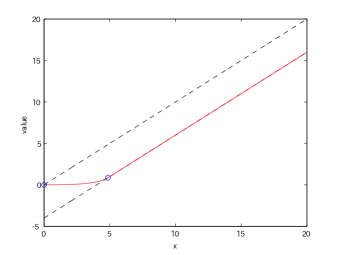

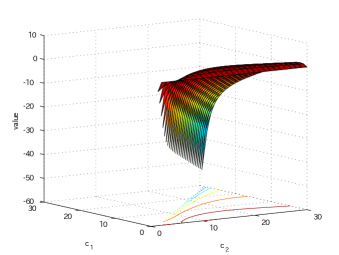

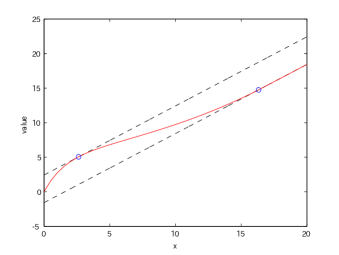

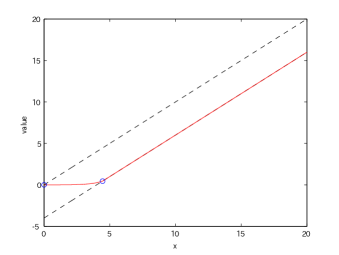

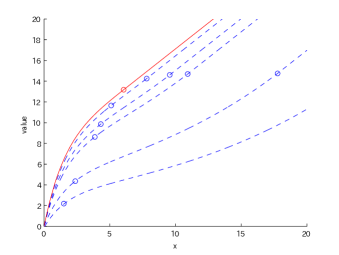

Figures 1 and 2 show the results for and , respectively. In both figures, we plot in the left column with respect to and and in the right column the value function as a function of the initial value . Recall that the values are those that maximize . As can be suggested from the contour map of , there exists a unique global maximum and hence Newton’s method is a reasonable choice of computing the maximizer . For the plots of the value functions, the circles indicate the points and and the dotted lines the 45-degree lines passing through these points.

In view of these figures, the continuity/smoothness at is readily confirmed; it appears to be differentiable for the case (in other words, the value function is tangent to the 45-degree line) while it is continuous for the case . The non-differentiability for is apparent in view of Case 2 in Figure 2. At , the value function is indeed tangent to the 45-degree line if , while for the case , we see that the slope is less than one. These results are consistent with Proposition 4.1. It is also confirmed that the slope of is smaller than only at those points inside , which verifies Lemma 5.3 and Proposition 5.2.

|

|

| Case 1: and | |

|

|

| Case 2: and | |

|

|

| Case 1: and | |

|

|

| Case 2: and | |

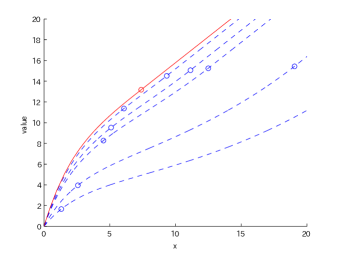

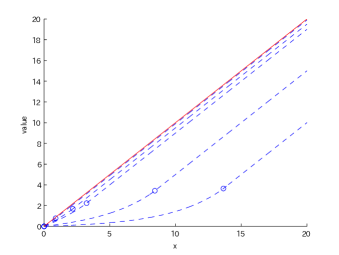

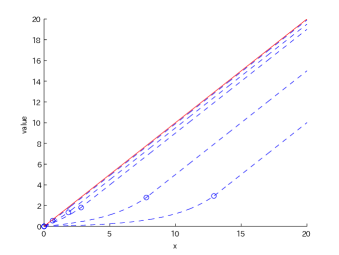

In our second experiment, we take and see if the value function converges to the one under no-transaction costs as in [8]:

| (6.2) |

for any , with the optimal barrier level

We let and consider the case (by choosing ) and also the case (by choosing ).

Figure 3 plots for each case the value function for (dotted) together with the no-transaction case (solid) as in (6.2). The circles on the plots indicate the points and also . It is easy to see that the value function is monotone in (uniformly in ), and converge to the no-transaction cost case as . The convergences of both and to are also observed. In fact, one can prove the convergence of value functions using the stability of viscosity solutions.

Proposition 6.1.

Let denote the value function corresponding to the dividend payment problem when the fixed transaction cost is (defined as above), and the value function when there are no-transaction costs. Then converges to uniformly as .

Proof.

From the definition of the problem, and is decreasing in and hence it has a point-wise limit, which we will call . The proof is completed if we can show that is a viscosity super-solution of the variational inequality that corresponds to the problem without transaction costs. But this is an immediate consequence of the stability result of the viscosity solutions (see e.g. Theorem 6.8 of [23] and Theorem 1 of [6]), since we can obtain the variational inequality in the no-transaction case by taking a limit in the case with transaction costs.

To get to uniform convergence from point-wise convergence we just proved, we appeal to Dini’s theorem to first show it on compacts. This indeed holds because we already know that and are continuous functions and as . Now, because the slopes of and are all one above and , respectively, and because can be shown to be bounded for any small (thanks to the convergence to as or modifying the proof of Lemma 4.3), the uniform convergence holds. ∎

We also observe in the figures that for , . This can be shown analytically for any .

Corollary 6.1.

If , we must have .

Proof.

|

|

| When : (left) and (right) | |

|

|

| When : (left) and (right) | |

Acknowledgements

E. Bayraktar is supported in part by the National Science Foundation under a Career grant DMS-0955463 and in part by the Susan M. Smith Professorship. A. Kyprianou would like to thank FIM (Forschungsinstitut für Mathematik) for supporting him during his sabbatical at ETH, Zurich. K. Yamazaki is in part supported by Grant-in-Aid for Young Scientists (B) No. 22710143, the Ministry of Education, Culture, Sports, Science and Technology, and by Grant-in-Aid for Scientific Research (B) No. 2271014, Japan Society for the Promotion of Science.

References

- [1] S. Asmussen, F. Avram, and M. R. Pistorius. Russian and American put options under exponential phase-type Lévy models. Stochastic Process. Appl., 109(1):79–111, 2004.

- [2] B. Avanzi and H. U. Gerber. Optimal dividends in the dual model with diffusion. Astin Bull., 38(2):653–667, 2008.

- [3] B. Avanzi, H. U. Gerber, and E. S. W. Shiu. Optimal dividends in the dual model. Insurance Math. Econom., 41(1):111–123, 2007.

- [4] B. Avanzi, J. Shen, and B. Wong. Optimal dividends and capital injections in the dual model with diffusion. Astin Bull., 41(2):611–644, 2011.

- [5] F. Avram, Z. Palmowski, and M. R. Pistorius. On the optimal dividend problem for a spectrally negative Lévy process. Ann. Appl. Probab., 17(1):156–180, 2007.

- [6] G. Barles and C. Imbert. Second-order elliptic integro-differential equations: viscosity solutions’ theory revisited. Ann. Inst. H. Poincaré Anal. Non Linéaire, 25(3):567–585, 2008.

- [7] E. Bayraktar and M. Egami. Optimizing venture capital investments in a jump diffusion model. Math. Methods Oper. Res., 67(1):21–42, 2008.

- [8] E. Bayraktar, A. Kyprianou, and K. Yamazaki. On optimal dividends in the dual model. Astin Bull., 43(3), 2012.

- [9] L. Benkherouf and A. Bensoussan. Optimality of an policy with compound Poisson and diffusion demands: a quasi-variational inequalities approach. SIAM J. Control Optim., 48(2):756–762, 2009.

- [10] A. Bensoussan, R. H. Liu, and S. P. Sethi. Optimality of an policy with compound Poisson and diffusion demands: a quasi-variational inequalities approach. SIAM J. Control Optim., 44(5):1650–1676 (electronic), 2005.

- [11] J. Bertoin. Lévy processes, volume 121 of Cambridge Tracts in Mathematics. Cambridge University Press, Cambridge, 1996.

- [12] T. Chan, A. Kyprianou, and M. Savov. Smoothness of scale functions for spectrally negative Lévy processes. Probab. Theory Relat. Fields, 150:691–708, 2011.

- [13] R. A. Doney. Fluctuation theory for Lévy processes, volume 1897 of Lecture Notes in Mathematics. Springer, Berlin, 2007. Lectures from the 35th Summer School on Probability Theory held in Saint-Flour, July 6–23, 2005, Edited and with a foreword by Jean Picard.

- [14] M. Egami and K. Yamazaki. Phase-type fitting of scale functions for spectrally negative Lévy processes. arXiv:1005.0064, 2012.

- [15] J. Ivanovs and Z. Palmowski. Occupation densities in solving exit problems for Markov additive processes and their reflections. Stochastic Process. Appl., 122(9):3342–3360, 2012.

- [16] I. Karatzas and S. E. Shreve. Brownian motion and stochastic calculus, volume 113 of Graduate Texts in Mathematics. Springer-Verlag, New York, second edition, 1991.

- [17] A. E. Kyprianou. Introductory lectures on fluctuations of Lévy processes with applications. Universitext. Springer-Verlag, Berlin, 2006.

- [18] R. L. Loeffen. An optimal dividends problem with transaction costs for spectrally negative Lévy processes. Insurance Math. Econom., 45(1):41–48, 2009.

- [19] B. Øksendal and A. Sulem. Applied stochastic control of jump diffusions. Universitext. Springer, Berlin, second edition, 2007.

- [20] G. Peskir. A change-of-variable formula with local time on surfaces. In Séminaire de Probabilités XL, volume 1899 of Lecture Notes in Math., pages 69–96. Springer, Berlin, 2007.

- [21] P. E. Protter. Stochastic integration and differential equations, volume 21 of Stochastic Modelling and Applied Probability. Springer-Verlag, Berlin, 2005. Second edition. Version 2.1, Corrected third printing.

- [22] S. Thonhauser and H. Albrecher. Optimal dividend strategies for a compound poisson process under transaction costs and power utility. Stoch. Models, 27(1):120–140, 2011.

- [23] N. Touzi. Optimal stochastic control, stochastic target problems, and backward SDE, volume 29 of Fields Institute Monographs. Springer, New York, 2013. With Chapter 13 by Angès Tourin.

- [24] K. Yamazaki. Inventory control for spectrally positive Lévy demand processes. arXiv:1303.5163, 2013.

- [25] D. Yao, H. Yang, and R. Wang. Optimal dividend and capital injection problem in the dual model with proportional and fixed transaction costs. European Journal of Operations Research, 211:568–576, 2011.