Effective Martingales with Restricted Wagers

Abstract

The classic model of computable randomness considers martingales that take real or rational values. Recent work by Bienvenu et al., (2012) and Teutsch, (2014) shows that fundamental features of the classic model change when the martingales take integer values.

We compare the prediction power of martingales whose wagers belong to three different subsets of rational numbers: (a) all rational numbers, (b) rational numbers excluding a punctured neighborhood of 0, and (c) integers. We also consider three different success criteria: (i) accumulating an infinite amount of money, (ii) consuming an infinite amount of money, and (iii) making the accumulated capital oscillate.

The nine combinations of (a)–(c) and (i)–(iii) define nine notions of computable randomness. We provide a complete characterization of the relations between these notions, and show that they form five linearly ordered classes.

Our results solve outstanding questions raised in Bienvenu et al., (2012), Chalcraft et al., (2012), and Teutsch, (2014), and strengthen existing results.

1 Introduction

1.1 Restricted wagers and effective prediction

A binary sequence that follows a certain pattern can serve as a test for the sophistication of gamblers. Only martingales that are sufficiently “smart” should be able to recognize the pattern and exploit it. Conversely, a martingale (or a class of martingales) can serve as a test for predictability. A predictable sequence is one that can be exploited by that martingale (or class of martingales). When we consider the class of all recursive martingales, unpredictable sequences are called computably random.

Following our intuitive notion of randomness, when a martingale (or a countable class of martingales) bets against the bits of a random binary sequence, its accumulated capital should (almost surely) converge to a finite value. So, a “predictable” sequence should be defined as one on which that martingale (or at least one martingale in that class) does not converge. Not converging divides into two cases: going to infinity, and oscillating. The former is used as the success criterion in the classic definition of “computable randomness”; we call it -gains. The latter we call oscillation. A third, economically appealing, success criterion requires that the martingale specify a certain amount to be consumed at each turn and the accumulated consumption go to infinity. A martingale together with a consumption function describe a supermartingale. We call the success of a supermartingale -consumption.

Things are not very interesting unless restricted wagers are introduced. It turns out that the above three success criteria are equivalent when all rational-valued martingales111Some papers consider computable real-valued martingales. These have the same prediction power as computable rational-valued martingales by simple approximation. are allowed. Matters become more involved when the wagers of martingales are restricted to subsets of the rationals. We consider three sets of wagers: , , and . The wager sets together with the success criteria form nine predictability classes. A complete characterization of the relations between these classes is given (see Figure 2).

1.2 Relations to existing literature

Computable randomness was introduced by Schnorr, (1971). For background, see also Downey and Riemann, (2007), Downey and Hirschfeldt, (2009), or Nies, (2009). The present paper is motivated by refinements of the notion of computable randomness recently introduced by Bienvenu et al., (2012), Chalcraft et al., (2012), and Teutsch, (2014). The main notion of computable randomness is -gains. Other well-studied success criteria include those of Schnorr, (1971) and Kurtz, (1981). The less familiar success criteria, -consumption and oscillation, turned out to be equivalent to the main notion of computable randomness (as mentioned above) and became folklore. When Bienvenu et al., (2012) introduced integer-valued martingales some of the folklore criteria gained renewed interest.

Bienvenu et al., (2012) showed that rational- and integer-valued martingales (rational and integer martingales, for short) are different with respect to -gains. Section 2 provides an alternative elementary proof. Theorem 5.3 shows that the separation can be done with a very simple history-independent martingale.

Bienvenu et al., (2012) asked whether martingales whose wagers take values in (defined above) were different from integer martingales with respect to -gains. Theorem 5.7 answers their question in the affirmative.

Teutsch, (2014) introduced the success criterion we call -consumption as a qualitative distinction between rational and integer martingales. He showed222Modulo a minor mistake that is corrected here. that -gains and -consumption are equivalent for rational but not for integer martingales. He asked what the relation is between -gains and -consumption for -martingales. Proposition 4.5 shows that the two are equivalent for -martingales. However, oscillation can serve as a qualitative distinction between rational and -martingales. Propositions 4.3 and 4.4 and Theorem 5.2 show that -consumption and oscillation are equivalent for rational but not for -martingales.

Bienvenu et al., (2012) used Baire category to distinguish between integer and -martingales to rational martingales. Their proof is based on the observation that the former attain local minima, since they stop once they get close to a local infimum, whereas the latter may decrease in very small steps indefinitely. Baire’s category seems to be too coarse to distinguish between two sets that exclude a punctured neighborhood of zero, such as and . Chalcraft et al., (2012) introduced a different argument when they characterized the relations between finite wager sets with respect to -gains. They asked whether their characterization extends to infinite sets. Proposition 4.3 answers this question in the negative.

2 The casino setting

Before providing the formal definitions, we first consider an illustrative example that demonstrates how to distinguish between classes of predictability (specifically, integer and rational martingales with respect to -gains).

A sequence of gamblers enter a casino. Gambler 1 declares her betting strategy, a function from finite histories of Heads and Tails to rational-valued bets. Then the rest of the gamblers, 2, 3,…(countably many of them), declare their strategies, which are restricted to integer-valued bets. The casino wants Gambler 1 to win and all the others to lose. That is, the casino should choose a sequence of Heads and Tails so that the limit of Gambler 1’s capital is infinite and everyone else’s is finite.

Is it possible? Consider the following strategy for Gambler 1. She enters the casino with two cents in her pocket (any non-dyadic fraction of a dollar will do). After periods she has dollars in her pocket and she bets on Heads (where ).

Now, Gamblers 2, 3,…declare their betting strategies. The casino places a finite sequence of Heads and Tails on which the capital of Gambler 2 is minimal among all such finite sequences. Recall that Gamblers 2, 3,…may bet only integer numbers; hence that minimum exists. At this point Gambler 2 is bankrupt. If he places a (non-zero) bet afterwards, it will contradict the fact that is a minimizer of his capital.333This argument extends to -martingales. Bienvenu et al., (2012, Lemma 4) essentially asserts that for any -martingale, any string has an extension such that the martingale is constant on extensions of . Note that Gambler 1 bets only on the fractional part of her capital, and so never decreases.

In the next stage, the casino extends by appending to it sufficiently many Heads, so that Gambler 1’s capital increases by at least 1. The casino repeats the same trick against every gambler in turn in order to bankrupt him while ensuring that Gambler 1 does not lose more than the fractional part of her capital, and then it continues to place Heads until she accumulates a dollar. QED.

3 Definitions

The set of all finite bit strings is denoted . The length of a string is denoted . The empty string is denoted . The concatenation of two strings and is denoted . For an infinite bit sequence and a non-negative integer , the prefix of of length is denoted .

A supermartingale is a function , satisfying

for every .

Remark 3.1.

Restricting supermartingales to rational values (rather than allowing all real values) is meant to avoid unnecessary technicalities that would arise from considering real-valued computable functions. This restriction does not result in a loss of generality, as the questions addressed in the present paper are such that any real-valued supermartingale could be approximated by a rational-valued one.

We call the difference ’s marginal consumption at . If ’s marginal consumption is 0 at every , we say that is a (proper) martingale.

The next couple of paragraphs contain definitions that are exemplified in Figure 1. The wager of at is defined as

Note that is positive if bets on “” and negative if bets on “” at . When is a proper martingale, our definition of wager coincides with the classic definition

The initial capital of (a supermartingale) is defined as . A proper martingale is determined by its initial capital and its wagers at every .

For a supermartingale , the proper cover of is the martingale whose initial capital and wagers are the same as ’s. The accumulated consumption of is defined as . Note that the accumulated consumption of at is the sum of ’s marginal consumption over all proper prefixes of .

| \Tree[.4 [.5 7 1 ] [.1 0 2 ] ] | \Tree[.4 [.6 9 3 ] [.2 1 3 ] ] | \Tree[.2 [.3 1 1 ] [.-1 1 1 ] ] | \Tree[.0 [.1 2 2 ] [.1 1 1 ] ] |

For a supermartingale and a string , we say that goes bankrupt at , if the sum of ’s wager and marginal consumption exceeds ’s capital. That is,

We say that goes bankrupt at if incurring a loss in the next round following will make ’s capital negative. Consequently, never goes bankrupt if and only if it is always non-negative.

For an infinite sequence , we say that goes bankrupt on , if goes bankrupt at , for some non-negative integer .

Let be a supermartingale and . If does not go bankrupt on , we say that achieves

-

•

-gains on , if ;

-

•

-consumption on , if ;

-

•

oscillation on , if .

We refer to -gains, -consumption, and oscillation as success criteria.

Remark 3.2.

Note that -consumption is the only success criterion that relies on supermartingales rather than proper martingales. The reason for defining the other criteria on supermartingales is entirely semantic. We want to distinguish between strategies (martingales/supermartingales) and payoffs (success criteria). In what follows, when -gains or oscillation are considered, it is often assumed (when no loss of generality occurs) that the supermartingales in question are in fact proper martingales.

Also, the standard definition of (super)martingales asserts non-negative values. We include the requirement that there be non-negative values in the success criteria by imposing that the martingales do not go bankrupt. It is sometimes convenient to assume (when no loss of generality occurs) that the martingales in question are non-negative. The reason for not asserting that all martingales take non-negative values is to allow for the next definition.

A (super)martingale is called history-independent if , whenever . The consumption of , however, may depend on history.

For , an -(super)martingale is a (super)martingale whose wagers take values in . We will be mainly interested in restricting the wagers to the set of integers , and the set .

We define a predictability class (class, for short) as a pair , where and .

Definition 3.3.

We say that a class implies another class if for every and every -supermartingale that achieves on , there exists an -supermartingale such that

-

(a)

achieves on ; and

-

(b)

is computable relative to (where is represented by listing its values in lowest common terms along an effective enumeration of ).

Note that implication is a transitive relation. It turns out that the classes we study exhibit the property that when they do not imply each other, they satisfy a stronger relation than just the negation of implication.

Definition 3.4.

We say that a class anti-implies another class if there exists a computable history-independent -supermartingale , such that for any countable set of -supermartingales (not necessarily computable) , there exists a sequence on which

-

(a)

achieves ; and

-

(b)

none of the elements of achieves .

Anti-implication behaves similarly to the negation of implication in the following sense.

Lemma 3.5.

Let , , and be classes. If implies and anti-implies , then anti-implies .

Proof.

Let , , be the three classes of Lemma 3.5. Take a supermartingale that separates from . Let be a countable set of -supermartingales. Let be the set of all -supermartingales computable from some element of . Since is countable, there exists a sequence on which achieves , but no element of achieves . Since implies , no element of achieves on . ∎

4 Implication results

| Wagers | Success Criterion | ||||

|---|---|---|---|---|---|

| -gains | -consumption | oscillation | |||

This section contains propositions that explain the arrows in Figure 2 and also their transitive closure, by transitivity. For any success criterion , if , then implies . This explains the upwards arrows of Figure 2, since . The leftwards arrows of Figure 2 follow from the fact that implies and the following proposition.

Proposition 4.1.

For every that includes , implies .

Proof.

Let , , and let be an -supermartingale that achieves oscillation on . We assume w.l.o.g. that is a proper martingale, because by definition achieves oscillation iff oscillates. Take , such that

We construct a supermartingale that achieves on . In the beginning waits until ’s capital drops below . Then mimics until ’s capital is above . At this point consumes and starts over waiting until ’s capital drops below , mimicking until ’s capital goes above , consuming , and starting over again.

Formally, for , define stopping times recursively by

with the convention that the infimum of the empty set is .

Define an -supermartingale by specifying , , and as follows: ; before time , and . For , set ; otherwise . At times , increases by ; otherwise doesn’t change.

Since, on , crosses the interval infinitely many times, all are finite; therefore increases infinitely many times, and so ’s consumption on is infinite.

Note that it is not assumed that and are computable relative to . Formally, a parameterized family of supermartingales is considered. Each member of this family is computable relative to , and at least one of them achieves whenever oscillates. ∎

The next proposition explains why and oscillation are the same.

Proposition 4.2.

implies .

Proof.

Let , and let be a -martingale that oscillates on . Let . There exists such that , for every .

We construct a parameterized family of -martingales, , such that each is computable from ; and oscillates between 1 and 2 on , whenever and . Note that we do not assume that is computable from or (not even relative to ).

where

Fix and . Any neighborhood of is visited by infinitely often. For , if then is either or . Hence, visits infinitely often and each time it visits, is either 0 or . Since does not converge, infinitely often. By the definition of , we get that changes from 1 to 2 and back to 1 infinitely often. ∎

The rightwards arrows in the top row of Figure 2 are explained by showing that implies . This is proved in two steps: Propositions 4.3 and 4.4. Proposition 4.3 answers a question from Chalcraft et al., (2012, p. 164) in the negative.

Proposition 4.3.

implies .

Proof.

Let be a -supermartingale. As usual, we assume w.l.o.g. that is a non-negative proper martingale. We further assume that , for all ; otherwise, consider the martingale .

We define a -martingale that makes whenever does. We define by specifying its initial capital and its wagers at any as follows:

For any and , we have

Since , for every , we have

It follows that ; therefore never goes bankrupt. Also, if , as , so does . ∎

Proposition 4.4.

implies .

Proof.

Let be a -martingale. As usual, is assumed to be a non-negative proper martingale. We define a -martingale that oscillates whenever makes .

The initial capital of is an arbitrary number . Suppose ’s initial capital is . In the first phase tries to gain money until its capital becomes at least 2. Let . During the first phase is defined as , so that either remains constant (if ) or remains constant (if ). In either case we have: ’s wager is bounded by 1; doesn’t go bankrupt; and if ’s capital grows indefinitely, the first phase is bound to terminate.

In the second phase tries to lose money. To this end, is defined as . The second phase terminates when ’s capital first drops down to some . Since ’s wagers are bounded by 1, . The second phase is guaranteed to terminate as soon as ’s capital grows sufficiently.

The two phases are repeated starting with the capital in , going above 2, and returning to again. As long as ’s capital grows indefinitely, the two phases are bound to terminate and, therefore to be repeated infinitely many times; thus oscillates. ∎

The remaining rightwards arrow in the middle row of Figure 2 is explained.

Proposition 4.5.

implies .

Proof.

Let be a -supermartingale. Assume without loss of generality that is a proper martingale and .

We define a supermartingale that achieves whenever achieves . The initial capital of is twice the initial capital of . bets proportionally to , and consumes 1 every time doubles its capital.

That is, , , for every . This ensures that the ratio between the capital of and stays constant as long as does not consume. Every time doubles its capital consumes an amount of 1 and as a result the ratio between ’s and ’s capital decreases by . As long as the ratio is at least 1, , as required.

It remains to show that , for every . For , suppose doubles its capital times along at the prefixes . That is, is the shortest prefix of such that , for all , where . By induction on , . ∎

5 Anti-implication results

Even more interesting than the implication results are the anti-implication results. By virtue of Lemma 3.5, we need only to separate adjacent strongly connected components of the diagram in Figure 2, and consider one representative from each strongly connected component.

The next theorem separates between integer -gains and -consumption.

Theorem 5.1 (Teutsch, 2014).

anti-implies .

The proof follows the main lines of Teutsch’s original proof while correcting a minor flaw.444With the notation of the original proof (Teutsch,, 2014, p. 150), a failure may occur when ’s wager is , , and . In this case (and ), violating the supposed invariants, Things I and II. We offer here a concise correction. The reader is referred to the original proof for a detailed exposition.

Proof.

Let be an arbitrary sequence of -supermartingales. Let be the -martingale with initial capital . We construct a sequence on which makes -gains and none of the makes -consumption.

We may assume w.l.o.g. that are integer-valued, because if they were not so, then would be. Also, we may include among constant martingales of arbitrarily large capital, and further assume w.l.o.g. that are non-negative. We define a sequence recursively. Assume is already defined. Define the following integer-valued functions:

| where | ||||

The above is well defined as long as , and in that case we have

| (5.1) |

The definition of is the main departure from Teutsch’s construction, where the same is used against all of the s.

Let . Note that the set in the definition of is not empty, since is bounded (by ) and is not bounded, because include arbitrarily large constant martingales.

We are now ready to define

The following properties follow by induction on :

-

(i)

(hence , by (5.1));

-

(ii)

for every , the pair is lexicographically not greater than , with strict inequality if consumes money at time ;

-

(iii)

is lexicographically strictly less than .

The only delicate point to notice when verifying (i)–(iii) is (ii), in the case where does not consume and (this is where Teutsch’s proof fails). Before proving the delicate case, we first explain how the proof of Theorem 5.1 is concluded by assuming (i)–(iii).

From (ii) and (iii) the sequence of finite sequences

is strictly decreasing. Since natural numbers cannot decrease indefinitely, it must be the case that and each is fixed for large enough. It follows from (ii) that none of achieves -consumption. Since and include arbitrarily large constants, ’s capital must go to .

It remains to verify (ii) in the case where does not consume and . In this case, if , we would have (and ). Fortunately, this situation is avoided by the definition of . If , then ; hence, by (5.1), ; hence, by the definition of and the assumption that is non-negative integer-valued, we get . ∎

The next theorem explains the separation between integer -consumption and oscillation.

Theorem 5.2.

anti-implies .

Proof.

Let be the -martingale with initial capital . That is,

for any non-negative integer and .

Define a consumption function

| and a supermartingale | ||||

that will provide the separation.

Note that , and are defined such that they all diverge to on the same set of sequences and increases only after two consecutive s and never increases in two consecutive periods.

Let be a countable set of -martingales. Assume w.l.o.g. that the members of are non-negative proper martingales with initial integer values. When a -martingale oscillates there is an integer between its limits superior and inferior; thus we can break the task of oscillation into countably many smaller tasks of oscillating around a given integer, and distribute these tasks among countably many copies of that martingale. Formally, we associate each pair with the goal of achieving

For convenience, the elements of are arranged in a sequence , such that whenever and , then .

We define a sequence recursively. Assume is defined for some . We say that receives attention at time , if is minimal with respect to the following properties:

-

(i)

,

-

(ii)

,

-

(iii)

.

Define

By (ii), no receives attention at time when ; therefore, , for every .

Let be an arbitrary integer satisfying . Since is integer-valued there exists some such that , for every . Note that only if and . Since never increases over two consecutive periods, we never have , and, therefore, the set of indexes is infinite.

Consider the sequence of -tuples of integers defined by

The proof will be concluded by showing that

-

is non-increasing with respect to the lexicographic order on , and

-

it decreases whenever .

It follows from that is fixed for large enough, and from that only finitely many times. By showing it for every , we prove that ; therefore achieves -consumption. Furthermore, for every and , does not oscillate around (by taking so large that ); therefore none of the martingales in oscillates.

It remains to prove and . Let . That is, . If then the successor of in is and according to our definition of , is not lexicographically greater than . If then , since increases only after two consecutive s; that is, is ’s successor in . By the definition of , is strictly less than , and so it remains to show that is not greater than .

If some receives attention at time , then is less than . If not, then the only thing that can make increase is that and , but this is not possible because: (a) if , then , and so ; (b) if , then there is some such that and , and so (or a smaller index) receives attention at time . ∎

A very simple history-independent strategy, betting at time , separates between and -gains.

Theorem 5.3.

anti-implies .

The proof of Theorem 5.3 is probabilistic.555A working paper by Bavly and Peretz, 2015+ provides a constructive proof. In probability theory, martingales have a slightly different meaning than the algorithmic randomness meaning that is used in the present paper. To distinguish between the two, we call a martingale process a sequence of integrable random variables adapted to a filtration , such that

We will utilize the following standard results from probability theory.

Theorem 5.4 (Doob’s martingale convergence).

Let be a martingale process. If , then exists (almost surely) and .

Corollary 5.5 (bounded second moment).

Let be a martingale process. If , then exists and is finite almost surely.

Corollary 5.6 (non-negative).

Let be a martingale process. If all are non-negative (almost surely), then exists and is finite almost surely.

The interested reader is referred to Shiryaev, (1996, Chapter 4) for proofs and further discussion.

Proof of Theorem 5.3..

The separating -martingale is very simple: it bets on at time . The more sophisticated part is constructing the separating binary sequence (given a countable set of -martingales) and setting the initial value large enough (independently of the -martingales).

Let be independent random variables assuming the values with probability . The series converges a.s., by Doob’s martingale convergence theorem, since the finite sums have bounded second moments. Let be large enough that

| (5.2) |

Note that is a universal constant; it does not depend on the realization of .

Define a history-independent -martingale to be

Let be a countable set of -supermartingales. Assume w.l.o.g. that , for every and .

We shall construct a random process , adapted to (namely, each is a function of ) that satisfies the following properties:

-

(i)

, for all (almost surely);

-

(ii)

(almost surely);

-

(iii)

.

The definition of relies on an increasing sequence of stopping times defined recursively, for any realization of . In odd intervals, between times and , is chosen randomly by setting it to . In even intervals, between times and , is determined as a function of . In both cases we make sure that given that is finite, will be finite as well (almost surely).

The purpose of the random intervals is to gain time. The martingale convergence theorem ensures that none of the martingales change much during each random interval. As time progresses gains an advantage over the -martingales, since its wagers become smaller; and so it can endure more losses. By the end of the th random interval, can incur more losses than together without going bankrupt. This is achieved by requiring that , and so never accumulates losses of more than 1 during a deterministic interval.

During the th deterministic interval, the bits of prevent from increasing (in the lexicographic order). At the same time, may incur losses, but it does not go bankrupt thanks to the advantage it gained during the preceding random interval. Since non-negative -martingales cannot decrease indefinitely, they must stop betting at some point. When none of bets, is set to be , and so it is guaranteed that will eventually regain its losses plus a positive amount of , which is the stopping condition of the deterministic interval.

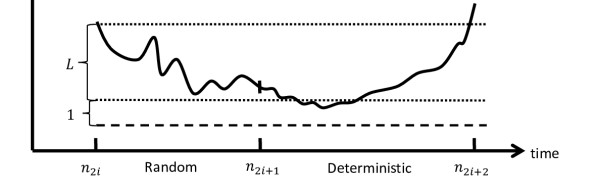

The choice of was made so that there would be an event of positive probability in which never accumulates losses of more than in any random interval. In the proceeding deterministic interval can accumulate additional losses of at most 1, and by the end of the deterministic interval it re-gains all its losses from the two time intervals (Figure 3). By setting , it is guaranteed that never goes below 1 and, therefore, does not go bankrupt (verifying (iii)).

Finally, consider the accumulated gains. The martingale convergence theorem guarantees that the accumulated gains (or loses) during the random intervals converge, for all of the martingales. The deterministic intervals are designed so that the accumulated gains of each of the -martingales are eventually non-increasing, whereas the gains of increase by at least in every deterministic interval (verifying (ii)).

We now formalize the above arguments. Let . For , let

with the convention that the infimum of the empty set is .

For and , set (note that are stopping times; hence is a function of ).

For , the value of will be determined by , as follows.

Let

With and as given above, define

Let us call the union of all random/deterministic intervals the random/ deterministic phase. Express () as a sum of two martingales, , where is active only during the random phase and only during the deterministic phase.

Formally, define and , and define , for , recursively by

| and | ||||

By Doob’s martingale convergence theorem (using that the s are non-negative martingale processes, for , and has bounded second moments), for almost every ,

| (and the limits exist). | (5.3) |

Also, if is finite, then so is (almost surely).

We turn now to analyze the deterministic phase. Denote the th deterministic time interval by . The definition of in the deterministic phase is such that is non-increasing (lexicographically, as grows), and it decreases each time ; therefore it can decrease at most times, and so, if is finite, so is . Since, for every , is lexicographically eventually non-increasing (specifically, for every ) and since natural numbers cannot decrease indefinitely, each one of the s is eventually non-increasing (for every ) and hence convergent, and

verifying (i).

By the definition of ,

| (5.4) |

Since the number of periods in which is at most , , for every ; therefore

| whenever . | (5.5) |

The separation between and -gains is made by betting at time .

Theorem 5.7.

anti-implies .

Proof.

Define a history-independent -martingale by

Denote the harmonic sum . For , we define the number of consecutive losses that can incur before going bankrupt after betting against as

The function turns out to be a useful currency for measuring ’s capital. It is an integer-valued submartingale ( is a supermartingale). It decreases by 1 upon seeing , increases by at least 1 upon seeing , and increases by upon seeing consecutive +1s.

The above can be interpreted as a production function (negative consumption function). Similar to the way in which the -martingale anti-implies , anti-implies , except that here ’s production plays the role of consumption in Teutsch, (2014).

Let us begin with an informal sketch of the proof. Let be a countable set of -supermartingales. The unboundedness of ’s production ensures that even if bets proportionally to (i.e., ) the ratio can be forced downwards until eventually. At this stage has sufficient capital to prevent from making gains and this becomes the primary goal. The secondary goal, which is pursued whenever bets 0, is to minimize the ratio until . Inductively, stage begins when . The primary goal is to prevent from making gains. Once the primary goal is achieved, the secondary goal is pursued, minimizing the ratio until .

We now formalize the above idea. As usual, assume w.l.o.g. that for every , and . Assume, also (for technical reasons that will become clear), without loss of generality that include constant martingales of arbitrarily large capital.

We define a sequence recursively. Assume by induction that is already defined. Let

By the assumption that include arbitrarily large constants, is well defined. If there is an index such that , let be the minimum of these indexes, and let

Note that in this case

| (5.7) |

Assume now that (or ). Define

Note that in this case

| (5.8) |

Since include constant martingales of arbitrarily large capital, it is sufficient to prove that and for every (and that, in particular, the limits exist).

Assume for the sake of contradiction that

By the definition of , for every , the sequence of -tuples is eventually non-increasing in the lexicographic order; therefore it stabilizes, for large enough; therefore it remains to show that (since ).

Denote the long division with a remainder of by

For all , we have (lexicographically) with a strict inequality if either or ; therefore, for some and every , and . We show that this is impossible by showing that , as (where means that ).

Since are constant after time , it is sufficient to show that (as ). Let and . We have

and so

Plugging in , it suffices to show

By eliminating constant terms and rearranging, we must show

The above follows from the estimate . ∎

Acknowledgments

The author wishes to thank two anonymous referees for many useful comments that improved the presentation of the paper substantially, Aviv Keren and Gilad Bavly for comments and suggestions, and Andy Lewis-Pye for patiently explaining concepts of computability. The early stages of this work were done in 2010–12 while the author was a postdoctoral researcher at Tel Aviv University. The author wishes to thank his hosts Ehud Lehrer and Eilon Solan.

References

- (1) Bavly, G. and Peretz, R. (2015+). How to gamble against all odds. Games and Economic Behavior (forthcoming).

- Bienvenu et al., (2012) Bienvenu, L., Stephan, F., and Teutsch, J. (2012). How powerful are integer-valued martingales? Theory of Computing Systems 51:330–351.

- Chalcraft et al., (2012) Chalcraft, A., Dougherty, R., Freiling, C., and Teutsch, J. (2012). How to build a probability-free casino. Information and Computation 211(0):160–164.

- Downey and Hirschfeldt, (2009) Downey, R. G. and Hirschfeldt, D. R. (2009). Algorithmic Randomness and Complexity. Springer.

- Downey and Riemann, (2007) Downey, R. G. and Riemann, J. (2007). Algorithmic Randomness. Scholarpedia 2(10):2574, http://www.scholarpedia.org/article/algorithmic_randomness.

- Kurtz, (1981) Kurtz, S. (1981). Randomness and genericity in the degrees of unsolvability. PhD thesis, University of Illinois at Urbana-Champaign.

- Nies, (2009) Nies, A. (2009). Computability and Randomness. Oxford University Press.

- Schnorr, (1971) Schnorr, C.-P. (1971). A unified approach to the definition of random sequences. Mathematical Systems Theory 5(3):246–258.

- Shiryaev, (1996) Shiryaev, A. N. (1996). Probability, volume 95 of Graduate Texts in mathematics. Springer.

- Teutsch, (2014) Teutsch, J. (2014). A savings paradox for integer-valued martingales. International Journal of Game Theory 43(1):145–151.