Option pricing with linear market impact and non-linear Black-Scholes Equations

Abstract.

We consider a model of linear market impact, and address the problem of replicating a contingent claim in this framework. We derive a non-linear Black-Scholes Equation that provides an exact replication strategy.

This equation is fully non-linear and singular, but we show that it is well posed, and we prove existence of smooth solutions for a large class of final payoffs, both for constant and local volatility. To obtain regularity of the solutions, we develop an original method based on Legendre transforms.

The close connections with the problem of hedging with gamma constraints [29], [31], [25], with the problem of hedging under liquidity costs [9] are discussed. The optimal strategy and associated diffusion are related with the second order target problems of [32], and with the solutions of optimal transport problems by diffusions of [33].

We also derive a modified Black-Scholes formula valid for asymptotically small impact parameter, and finally provide numerical simulations as an illustration.

1. Introduction

This paper is about the derivation and mathematical analysis of a pricing model that takes into account the market impact of the option’s hedger, i.e. the feedback mechanism between the option’s delta-hedging and the price dynamics. We will throughout the paper assume a linear market impact: each order to buy stocks impacts the stock price by (). This scaling, that will be discussed hereafter, means that the impact in terms of relative price move depends on the amount of stock traded expressed in currency, hence is homogeneous to the inverse of the currency i.e. percents per dollar.

| (1) |

We will examine several situations where is either constant, or can be also a function of the solution itself.

The literature devoted to the study of the market impact itself is quite vast, and it is more frequent to find an impact that varies as a power law of the size of the trade (see for example [2]). Although our linear approach is clearly not the most realistic in terms of market microstructure, it has the advantage of avoiding arbitrage opportunities, as well as not being sensitive to the hedging frequency: in a non-linear model, splitting an order in half and repeating it twice would not yield the same result, a situation that we want to avoid here, as we aim at deriving a time continuous formulation.

In addition we assume that the market impact is permanent: there is no relaxation following the immediate impact, where the price goes back partially to its pre-trade value. The case with relaxation has been studied in a companion paper [1].

1.1. Order book modeling

From an order book perspective, our market impact model consists in assuming an order book with continuous positive density around the mid-price, and where following a market-order starting at price (say a buy order for example), where liquidity has been consumed up to , the new mid-price becomes , and the liquidity removed between and is instantaneously refilled with buy orders (or sell orders if the price had moved down after a sell order). Clearly this model is a great simplification of what is actually observed in real markets (see [34] for instance), but as we will show this simple approach is enough to obtain a non-trivial modification of the usual Black-Scholes equation. More precisely: Assume a static order book, parametrized by a mid price and a supply intensity in the following way: the number of stocks available for purchase between and equals to .

We assume that the (local) liquidity (expressed in currency) available between and equals . Simple calculations show that the scaling (1) implies that is actually constant, which explains our choice, as we believe that the quantity is the good measure of a stock’s liquidity. Then independently of this choice, when spending an amount (expressed in currency) in stocks, the order book will be consumed up to given by

while the number of stocks purchased will be

One sees right away that, at the leading order, the average price of execution is . In a subsequent study [1], the authors consider an immediate relaxation of the price after the liquidity is consumed, hence the liquidity of the order book is rebuilt around for a certain relaxation factor . We will only adress here the case . The choice is the one that has been studied by Cetin, Soner and Touzi in [9]: no permanent market impact, but liquidity costs.

1.2. Motivations and links with previous works

In terms of concrete applications, the problem of derivatives pricing with market impact arises when the delta hedging of the option implies a volume of transactions on the underlying asset that is non-negligible compared to the average daily volume traded. For example, a well observed effect known as stock pinning arises when the hedger is long of the (convex) option for a large notional, and one observes then a decrease of realized volatility if the underlying ends near the strike at maturity. In financial terms, the hedger of the option makes a loss if the volatility realizes below its implied value. This stylized fact can be recovered by our pricing equation. Conversely, when selling a convex option for a large notional, a common market practice on derivatives desks is to super-replicate the option by the cheapest payoff satisfying a constraint of gamma (the second derivative of the option), the gamma max being adjusted to the liquidity available on the option’s underlying. Hence there are two issues arising here:

- -

- -

Our approach addresses those two issues: first, via the market impact mechanism, it induces a constraint on the gamma when selling a convex payoff, and it constraints the theta (the time derivative of the option) when selling a concave payoff. Thus it recovers two important stylized facts of the gamma constraint approach, moreover it incorporates liquidity costs in the price. It can be noted that the parabolic operator that we obtain through market impact lies somehow between the gamma-constraint operator of [29] and the liquidity costs operator of [9].

A formal argument shows that, playing on the dependency of the market impact parameter with the solution, one can recover exactly the gamma constraint pricing equation of Cheridito Soner Touzi [25], or the liquidity cost equation of Cetin, Soner and Touzi in [9]. This can be seen as closely related to the work of Serfaty and Kohn [20] that recover non-linear heat equations by stationary games approach. From a financial modelling perspective, this would amount to assume a supply curve for the price of gamma-hedging.

Concerning the mathematical techniques, as opposed to [25], [9], [31], [5], [6], we adress the problem of finding exact replication strategies, while the aforementioned work deal with stochastic target problems: find the cheapest trading strategy that super-replicates the final payoff. The solutions of these two problems coïncide in general, but may differ in some degenerate cases (see [30], [1]). Apart from introducing the linear market impact model (which has then led to the subsequent studies [5], [6], [1]), the main contribution of this paper is a complete study of a fully non linear parabolic equation associated to a new class of stochastic control problems (see Theorem 5.5). We will also prove a representation formula that gives some qualitative informations about the modified dynamics. Those two results are then used to derive rigorously an asymptotic expansion of the solution for small market impact, leading to a modified Black-Scholes-Legendre formula, as well as a simple and efficient way of computing the market impact effect.

We believe that the techniques used toward obtaining these results are original and of independent interest. As will be discussed hereafter, these results can be seen as related to regularity results concerning porous media equations (see the book of Vazquez [36] for a complete reference), in particular in the case of Fast Diffusion Equations, as well as the papers by Crandall and Pierre [13], [11] about interior regularity for non-linear diffusions.

The stochastic target problem associated to our model has been studied in two companion papers [5], [6], where it is shown that the exact replication strategy is actually the optimal solution for the stochastic target problem. To make a connection between the two results, it is important to notice that through stochastic control techniques, one is able to derive a viscosity formulation of the value function. It is only when this function has enough regularity that one can deduce the optimal strategy from the value function, hence the importance of the question of regularity.

1.3. The pricing equation

As we will see, assuming no interest rates and dividends, the pricing equation that we obtain can be put under the form

| (2) |

which reads also

where can be either constant or dependent of the solution as . In this case we obtain a wide class of fully non-linear Black Scholes equations of the form

As will be shown, one can derive any parabolic equation of this form through an ad-hoc choice of , as long as and .

The case of equation (2) is quite challenging for the mathematical perspective: the operator is not uniformly elliptic (when goes to ), and is singular (when goes to ). Standard theory does not apply right away, and an ad-hoc regularity theory must be developed. Still, we will be able to show interior (i.e. not relying on a smooth terminal payoff) regularity of solutions for constant and boundary regularity (i.e. assuming a good terminal condition) for non-constant .

1.4. Second order target problems and optimal transport by diffusions

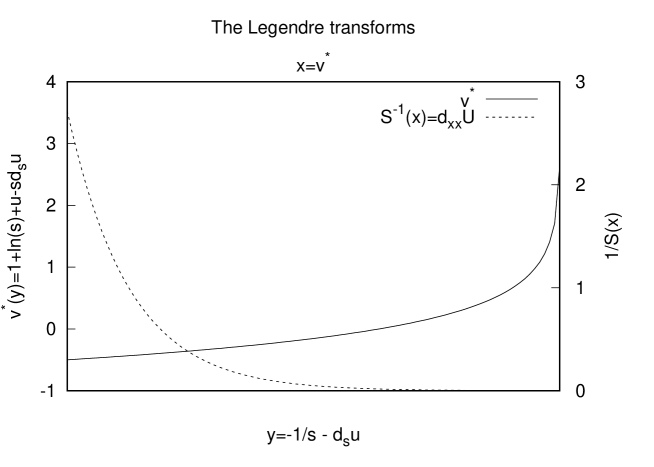

There is also a clear connection between this work and the work by Soner and Touzi and Zhang [32] about dual formulation of second order target problems, and also with the problems of optimal transport by controlled martingales studied in [33]. Indeed observe that the elliptic operator in (2) is convex, and then applying the reasoning of [32] based on the Legendre transform representation of , one can show formally that a solution to (2) will also be solution of the following variational problem:

| (3) |

where starts from at time and follows , is a Brownian motion, is the set of all bounded positive adapted processes on , and is given and positive.

This can be seen as a stochastic version of Hopf-Lax formula,

| (4) |

see [4], which is a representation formula for solutions to

where is the Legendre transform of . The fact that, in general, the solution of a variational problem like (3) is indeed the viscosity solution of an associated parabolic equation (which here would be 2) has been studied in [32]. In this particular case we will be able to actually characterize the optimal in (3), and show that the optimal diffusion is a martingale up to time under mild conditions, which allow to be unbounded.

Then, still reasoning formally, transports its initial distribution on its final distribution minimizing the transport cost

which is a particular case of the problem studied in [33]. More generally the link between the variational problem (3) and optimal transport arises through the use of Kantorovitch duality, see [17], [18], [7] and also [37] for an overview on optimal transport, and also [24] for further extensions to non-linear variational problems.

The regularity results that we obtain here will provide the regularity of the optimizers in the aforementioned problems.

1.5. Organization of the paper

The rest of the paper is organized as follows: in the next section (Section 2) we provide a heuristic derivation of the pricing equation, and discuss its practical relevance for financial modelling.

Section 3 gives the time continuous formulation of the problem as a system of stochastic differential equations, and shows that the pricing equation (2) actually leads to an exact replication strategy when it admits a smooth solution, see Theorem 3.2.

Section 4 establishes the connection between the solution of (2) and the problem (3), and discusses also the link with optimal transport and robust hedging.

Section 5 contains the regularity results for the pde (2). Theorems 5.5, 5.7 and 5.13, contain the main a priori estimates for solutions to (2), that hold under mild conditions on the final payoff. These results lead then to the existence, regularity and uniqueness of the solutions to (2): Theorem 5.16.

Section 6 establishes representation formulas for the solution: Theorems 6.7, 6.3 and 6.8. These representation formulas are a probabilistic counterpart to the pde (2), and give qualitative insight about the solution, and establish further results concerning the optimizers of the problem (3).

In section 7 we derive a first order expansion of the solution for small market impact (). This leads also to modified Black-Scholes-Legendre formula (see formulas (100, 102, 103)), which is easily computed by analytic formulas or standard Monte-Carlo simulations. It should formally be also valid in the liquidity costs case of [9].

Section 8 illustrates the paper with a numerical solution of the pde.

1.6. Acknowledgements

This paper has been in gestation for a long time, its motivation originally appeared while the author was a member of the Quantitative Research team at BNP Paribas Capital Markets, and I thank my colleagues there for stimulating discussions. Part of this work has also been done under the hospitality of the Chair of Quantitative Finance at the Ecole Centrale de Paris, and I thank in particular Frédéric Abergel. I also thank Bruno Bouchard, Nizar Touzi, Juan Vazquez, Fernando Quiros, and Fima Klebaner for enlightening discussions.

2. Heuristics

We assume that we have sold an option whose value is , and greeks are as usual

We also introduce the Gamma in currency, i.e.

| (5) |

The strategy that we use is the following: we assume a priori that there exists an exact replication strategy, that consists in holding stocks. We compute the equation that must be followed by , and the modified dynamics that this strategy implies. We then check that this strategy allows indeed to perfectly replicate the final claim.

Starting from a delta-hedged portfolio, assume that the stock price moves by . We will assume that this initial move of is given as is usual by

where is a standard Brownian motion, and its increment between and (those objects will be introduced more formally later on). A ‘naive’ hedge would be to buy stocks, but as this order will impact the market, the portfolio will not end up delta-hedged. Assume instead a hedge adjustment of stocks, and let us find such that spot ends up at a final value . Using (1), we write that

and this yields

This identity expresses the fact that the number of titles bought is , hence that the portfolio is delta-hedged at the end of the trade. Performing a first order Taylor expansion leads to

| (6) |

which yields

| (7) |

Remember that is computed with respect to the option the portfolio is short of, hence when one sells a call for example. Assuming that (to be discussed later), one sees that : as expected the hedger increases the volatility by buying when the spot rises, and selling when it goes down.

One can also reach the conclusion (7) by following an iterative hedging strategy: after the initial move , the hedge is adjusted ”naively” by stocks, which then impacts the price by . A second re-hedge of is done, which in turn impacts the price and so forth. The final spot move is thus the sum of the geometric sequence

One sees right away that in this sequence, the critical point is reached when the ”first” re-hedge (i.e. buying stocks after the initial move of ) doubles the initial move: the sum will not converge. This situation will be discussed hereafter.

Then the value of the portfolio containing -1 option + stocks at the beginning of time , and stocks at time evolves as

and is the profit realized during the re-hedging. In a perfect frictionless market, this term is zero, as one buys stocks at a price , and the ”post-re-hedge” value of the stocks is . To compute we recall that

| (8) | Immediate impact of an order to buy N stocks | ||||

| (9) | Average execution price |

The computation of then yields

with . Finally if is the the value of the hedger’s trading strategy, and setting , one obtains:

| (10) |

2.0.1. The pricing equation

We now assume that the option is sold at its fair price, hence at first order in time. Then we have as moves to ,

and we thus get

with defined by (7). We recall now that the initial move of i.e. in our notations, is driven by a geometric Brownian motion, as in the Black-Scholes model, so . Then one can following Itô’s formula replace by in the previous Taylor expansion, and this simplifies into

| (11) | |||

| (12) | |||

| (13) |

Remark. Note that if we change assumption (9) in

| (14) | Average execution price |

then we get the equation

as found in [23]. This equation is not parabolic however.

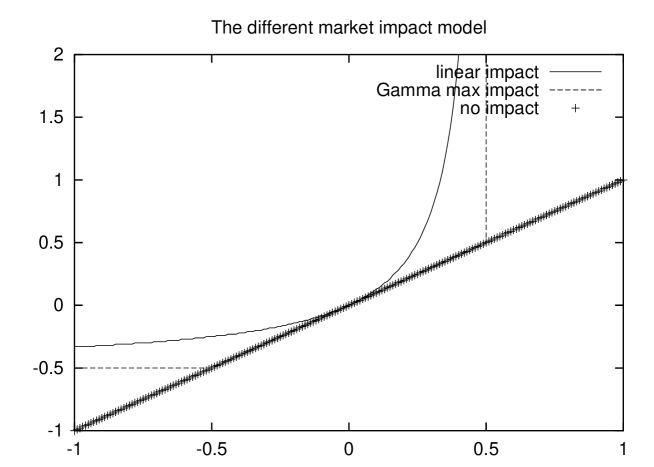

When , we we recover the standard Black-Scholes equation. This equation clearly poses problems when goes to 0, and even becomes negative. This case arises when one has sold a convex payoff () and an initial move of would be more than doubled during a naive re-hedging (see above) due to our market impact, . Intuitively, the hedger runs after the spot, without being able to reach a point where he is hedged,and the spot runs away to infinity or to 0. In that case, believing the model, when , , when the spot moves up, one should sell stocks instead of buying, because the market impact will make the spot go down. One relies on the market impact to take back the spot at a level where we the portfolio is hedged. This situation is clearly nor realistic, nor acceptable from a trading perspective … On the other hand, if we consider a smooth function that satisfies for all time the constraint

solving (11, 12) with terminal payoff then our approach will be shown to be valid, and the system (11, 12) yields an exact replication strategy (we shall prove this in the verification theorem hereafter). Note that our approach has been presented in the case of a constant volatility, but would adapt with no modification to another volatility process, local or stochastic. The function is increasing, which guarantees that the time independent problem is elliptic, and thus the evolution problem is a priori well posed, although the question of the existence of solutions to the fully non-linear pricing equation still remains.

Another (informal) way to see the constraint on , is to consider instead of

The physical interpretation of the singular part is that areas with large positive ( i.e such as ) will be quickly smoothed out and will instantaneously disappear, as if the final payoff was smoothed (again this argument will be made rigorous later on). This amounts to replace the solution by the smallest function greater than and satisfying the constraint () (a semi-concave envelope, the so-called ”face-lifting” in [31]). This is actually a common practice on derivatives trading desks: one replaces then a single call by a strip of calls, in order to cap the , and this approach has been used by in [6]. It can be expressed by turning the system (11, 12) into

| (15) | |||

| (16) |

for some , still with . Under this formulation the problem enters into the framework of viscosity solutions, see [12].

Note that on the other hand, areas with large negative (the hedger is buying a convex payoff) would have very little diffusion, which also poses a problem as the equation is not uniformly parabolic any more.

The functions are represented in Fig. 1.

3. Time Continuous Formulation of the Problem

We now formulate our problem as a system of stochastic differential equations, as done in [5], [6]. This formulation is similar to the one of Soner and Touzi [29], [31] of stochastic target problems, or to the formulation of backward stochastic differential equations problems [10]. The crucial difference is that here the spot process itself has its dynamic modified by the controls.

We consider a probability space supporting a standard Brownian motion and its associated filtration . The drift will be a bounded adapted process, and we consider bounded processes (the controls) , adapted to the filtration . For two semi-martingales , denotes their covariation (and denotes the quadratic variation of ). Both and are given, they can be constant or have some dependency, which will be made explicit when needed. We will consider the following system of stochastic differential equations,

| (17) | |||||

| (18) | |||||

| (19) |

where starts from at . It has been established rigorously in [5], Proposition 1, how to obtain this system as the limit of a discrete (in time) trading strategy. In particular, note the modified drift

| (20) |

At each time the hedger holds units of the risky asset, whose value is . From equations (17, 18), and are two continuous semi-martingales. Equation (17) states that the spot price is driven by an exogenous source of noise and by the market impact (note the non-trivial modification of the drift process , however this will not affect the pricing equation). Equation (19) takes into account the order book’s behaviour to give the value process of a trading strategy, it can be written as

It is the continuous version of (10).

Combining (18) and (17) one sees right away that

We will assume for now the condition

| (21) |

We have the first elementary result:

Proposition 3.1.

The replication problem is to find a self financed strategy, hence controls , and an initial wealth such that

On the other hand the super-replication problem of [31] is to find the lowest initial wealth such that there exists an admissible control reaching the target, i.e.

The two problems are not equivalent in all cases, in particular, if the associated HJB equation is not parabolic (see [30]). In that case the verification theorem does not apply, and the optimal strategy is not straightforward (and might not even be unique). As we will show, the pricing equation is in our case well posed, and by solving it we are able to exhibit directly an exact replication strategy. We address the super-replication problem in two companion papers [5], [6].

For a smooth function such that , we consider the strategy given by (and hence ). One obtains for the wealth

while Itô’s formula applied to reads

Obviously, a function satisfying

looks like the good candidate. We know that

for some adapted process (that depends on and on ). Then the condition on turns into

3.1. The pricing equation

We rewrite the equation above as

| (22) |

with being given by

| (23) |

with the terminal condition

| (24) |

3.2. The intensity dependent impact

Let us now turn to a slightly more general heuristic, by allowing the parameter to depend on the trading strategy. In the previous approach we have assumed that the market impact of buying stocks is, in terms of price, , regardless of the time on which the order is spread. We now assume that . The quantity relates to the trading intensity, i.e. to the rate at which stocks are traded by the option’s hedger, hence a gamma dependent market impact can make sense. The system of stochastic differential equations governing the evolution is now given by

3.3. The Verification Theorem

We conclude this section by stating a verification result and a representation formula for solutions to the replication problem. We first introduce two versions of condition (2.0.1):

| (29) |

and the strict version of (29)

| (30) |

3.3.1. The risk-neutral dynamic

We consider on a probability and a -Brownian motion, and consider the solution of:

| (31) | |||||

| (32) | |||||

| (33) |

When we might just write instead of .

Theorem 3.2.

Let be a smooth solution of (22, 23, 24) satisfying (30). Assume also that

-

i)

are bounded,

-

ii)

are bounded.

Then there exists a strong solution defined up time to the system (25, 26, 27) above, such that and and, almost surely,

| (34) |

The evolution of under is given by

with defined in (20). There exists absolutely continuous with respect to such that satisfies (31, 32, 33) under , and there holds

| (35) |

In particular, the result of the Theorem hold if is constant and satisfy the assumptions i) to v) of Theorem 5.7.

Proof. The proof of (34) is a simple application of Itô’s formula, since we restrict ourselves to the case where the solution of (22) is smooth, the modified volatility remains bounded, and thus the solution is a solution in the classical sense. For the expression of , we just compute . The conditions i) and ii) together with condition (21) imply that remains bounded. The condition ii) needs some a priori estimates to be enforced, but is trivially satisfied in the case where is constant, which will be our main focus in this paper. Conversely the condition on is straightforward to check, and is also found to be necessary for the proof of uniform boundedness of the volatility (see Theorem 5.7). Then under the assumptions on , the existence of is a standard application of Girsanov’s Theorem (see [19]). Under , follows (31, 32, 33), and (35) follows by observing that

and then by taking the expectation of (34) under .

This result shows that, under existence of a smooth solution to (22), the claim is replicable by the self financed strategy that consists in holding stocks, and that the cost of this replication strategy is given for all time by . Note again that the profit generated by the hedging strategy is no more the usual expression , but includes an additional term due to the market impact (more exactly due to the difference of the price after market impact and the executed price, i.e. the liquidity costs). It is always positive (i.e. in favor of the option’s seller). As observed above this seems surprising, but note that the change of volatility from to acts always against the option’s seller , and the sum of the two impacts is always against the option’s seller.

4. Dual formulation of the problem

We mention here the connection between our pricing equation and the dual formulation of second order target problems studied in [32]. The equation we study here is still

, and we assume that , satisfy the conditions of Theorem 5.16, so that is smooth on . is convex, and we compute the Legendre transform (a slightly modified Legendre transform) of :

Note that from the strict convexity of , there will hold

| (37) |

and that the supremum in (37) is reached for , which we recognize as the modified variance in our model. For a Brownian motion, with filtration , we define

For we can define such that

| (39) | |||||

| (40) |

and define, for a terminal condition,

Then applying Itô’s formula to (which is allowed from the regularity of ) we have that

hence from (4),

which shows that , with equality if and only if , hence is the risk-neutral diffusion (31, 32, 33). Letting, for

| (41) |

we have thus obtained the following:

Theorem 4.1.

Remark. In Theorem 6.3, our result is stronger, as formula (42) holds for any such that , and hold up to cases where might no be finite. We will also show that the optimal process remains a true martingale up to time under mild assumptions on , which allow for the optimal to be unbounded, hence .

4.1. Relation to a problem of optimal transport

As mentioned in the introduction, having found by solving (22), and specifying an initial distribution for , we let be the law of . Then realizes also

where the infimum is taken over all the process , that have laws at time 0, at time , and follow (40). This problem of optimal transport by martingales has been studied by Touzi and Tan in [33]. Therefore, our regularity results can be seen as a step towards the regularity of optimal transport by diffusion, for this particular cost. Moreover, as we will see in Theorem 6.8, when the volatility is constant, we obtain a closed formula to express the final density in terms of the terminal condition .

4.2. Interpretation in terms of robust hedging

Assuming one is trying to find a robust hedging strategy for the claim when the volatility of the underlying is unknown. The formula (42) gives the optimal upper bound on the price of the claim over all possible diffusions that satisfy

as it gives the cheapest hedging strategy that will super-replicate the claim for satisfying the above constraint.

5. Smooth solutions via Legendre-Fenchel Transform

In this section we prove existence and regularity of the solution to (22, 23, 24), in the cases of constant or local volatility , and with constant market impact parameter . In particular, our result will give the conditions on and for which solution has enough regularity to satisfy the assumptions of the Verification Theorem (Theorem 3.2), and to define the dynamics of . The case of non-constant is treated in the appendix.

5.1. Notations

-

-

As we will work with Hölder spaces, we note for , , , (resp. ) (resp. ) the usual Hölder norm of of order with respect to and order with respect to . When no subscript or is specified, the continuity will be with respect to .

-

-

We shall denote the space of functions with bounded norm for all compact sets .

-

-

Classically we will denote .

-

-

Whenever needed, we will consider a Brownian motion supported on a filtered probability space, and denote the expectation under the probability measure .

5.2. Some facts about the Legendre-Fenchel transform

A reference on this topic is [27].

Definition 5.2.

Let , its Legendre transform is defined by

| (43) |

If is convex and l.s.c. then . Moreover

-

-

If is continuously differentiable at then,

and the reverse equality hold since .

-

-

If then .

-

-

At a point where is defined and positive, is defined and satisfies

-

-

If depends smoothly on a parameter , for all ,

5.3. Transformation of the pricing equation via Legendre transforms

Starting from a classical (see Definition 5.1) solution of (22, 23, 24), we consider

| (44) |

Then is convex under (29), and satisfies

| (45) |

Consider the Legendre transform of defined by

| (46) |

From Definition 5.2, for the pair () where the maximum is attained, there will hold

Moreover, one will have

Then it follows that

| (47) | |||||

By straightforward computations, , the inverse function of , satisfies

| (48) | |||||

To construct properly , we use also the Legendre transform. Since is increasing, a primitive of is convex, hence one will have for , at any point where is continuous, i.e. everywhere in the domain of .

Construction of the terminal value for the transformed equations

Proposition 5.3.

Let satisfy . Define such that

Then

-

(1)

is non decreasing ,

-

(2)

wherever exists,

-

(3)

,

-

(4)

either such that above or .

-

(5)

If is finite then is identically below this limit, otherwise is finite everywhere and .

-

(6)

If is constant on some interval then is identically above for some , otherwise is positive everywhere and .

-

(7)

For all where and is continuous there holds

-

(8)

Under assumption (51), one has necessarily that

From (5) and (8) we thus have Lebesgue a.e.

| (49) | |||||

| (50) |

Proof.

-

(1)

The first point comes from the fact that for .

-

(2)

This is just the definition of the Legendre transform, and the fact that for the optimal (see Definition 5.2).

-

(3)

The third point comes the fact that is defined and finite on . If one had then this would imply that below .

-

(4)

The two cases correspond to being either finite (equal to ) of .

-

(5)

below 0 implies that . If is finite, then . This in turn implies that below this limit. The other assertion follows from point 3 since .

-

(6)

If above some value , then and above . Then is constant above .

-

(7)

Point 7 is just the fact that , hence

and the assertion follows.

-

(8)

For point 8, the first part follows from point 5, and implies the second part. Note that from (51), and are finite everywhere.

5.4. Main assumptions

5.5. The case of constant volatility

We now show that (22, 23, 24) admits a unique smooth solution when are constant. In this case solves also (48), hence one can recover the function by solving a simple heat equation, which then leads to the solution . Therefore, the condition for existence of a smooth solution can be stated as a condition on the function at time . We will have the following result:

Theorem 5.5.

Remark. As we will see, is positive and increasing, thus the condition (51) on is only about the behaviour of near 0. It allows the set to be non-empty, in particular any globally Lipschitz function such that

satisfies (51). Surprisingly, even if for above a certain threshold, condition (51) might be satisfied, as it just implies that is identically 0 above a certain threshold. Conversely if for close to then (51) can not be satisfied. This is a feature of the log-normal dynamics that ”send the mass to 0”.

Proof. Starting from the terminal payoff , as explained above, one constructs , and then , and then which is defined almost everywhere on the set . For , let be given by

| (53) |

Condition (51) implies that is well defined, solves 48 (which is a heat equation with constant coefficients), and so does , and the properties listed in Proposition 5.3 ensure that belongs to and for , is strictly increasing and strictly concave, being given by

and having limits at and at .

Then one follows backward our previous transformations of :

The bounds on are a direct consequence of the following lemma:

Lemma 5.6.

Let be the classical solution to (22) on with constant , constructed as above from . Then is non-increasing and is non decreasing.

Proof. Observe that for a classical solution of (22), and defined from , one has and . We will have proved the lemma if we show that for any , if (resp. ) then for time the same inequality holds. This will hold if which solves the heat equation, satisfies the maximum principle. This type of result is in general is not true on the whole line without any growth assumptions, see [35], but in our case this is granted as we have constructed through the representation formula (5.5).

Bounds on can be obtained obtained by looking at , that solves

The bounds on are classically obtained by differentiating the equation, and imply the bounds on .

Finally the uniqueness is a consequence of Widder’s Theorem (see [19], Chapter 4, Theorem 3.6) since starting from a classical solution to (22) one can build from as explained above, and then will be a positive solution to the heat equation, for which uniqueness holds.

5.6. The case of non-constant volatility

Here we show the following a priori estimate

Theorem 5.7.

Remarks. The interest of this result is to be able to define the dynamics of up to time for all without relying on stopping times. For this we need a uniform bound in space like (55).

The conditions on might not be minimal, but they allow for a large class of payoffs: all payoffs with linear or logarithmic growth at 0 and infinity. In particular any combination of vanilla options.

If the proof becomes much simpler. The interest of the result lies in the fact that one can prescribe independently the behaviour at and .

Proof of Theorem 5.7.

We recall that

and using this yields

| (57) |

while, as noted in (48) the inverse of , , follows

| (58) |

We will treat (57) as an equation of the general form

| (59) |

The strategy will be the following:

- -

-

-

In order to have those a priori estimates, we will use a barrier argument: we will show by the comparison principle that the solution is pinched between an upper and a lower bound, and this control used with the convexity of the solution will in turn lead to a control of the gradient.

- -

-

-

The growth conditions i) and ii) will then allow by a scaling argument to show the uniform bound (55).

Note that from our assumption , hence for , and the equation (57) has a singular boundary condition which will need careful treatment. On the other hand, from points 3 and 8 of Proposition 5.3, and . One should think of as a perturbation of , see Fig. 2.

We will need for our estimates the following comparison result:

Lemma 5.8.

The proof is deferred to the appendix, section B.1. It is a simple comparison principle, but is not trivial, since following some famous counterexamples by Tychonoff, (see [35]) uniqueness and comparison for solutions of the heat equation on the whole line does not hold unless some growth conditions are imposed. Here we do not need any growth but we use the concavity of the solution, hence this Theorem can be seen as a Widder’s type Theorem which states uniqueness of positive solutions to the heat equation.

We next need the following lemma:

Lemma 5.9.

Under assumptions of Theorem 5.7, one can find another constant instead of such that the properties i) and ii) are satisfied by the solution on .

Proof of Lemma 5.9. By direct computations, the assumptions on imply for that, for some constants :

-

i)

As goes to ,

-

ii)

As goes to ,

We start by constructing the barriers that are the inverse functions of in Lemma 5.8. Lemma 5.8 implies then that

for . The controls on imply for

hence solving for time ,

with that depend also on . A similar estimate hold for with other constants . These controls translate back to and , and by comparison to to yield the result of the Lemma.

By convexity of , Lemma 5.9 yields then the following control on :

Lemma 5.10.

There exists such that

Moreover if then ,

| (63) |

Proof. This is a direct consequence of the previous Lemma 5.9. The accurate control on the upper and lower barrier (same logarithmic growth for upper and lower barrier) yields a precise estimate of the gradient.

Proof of Theorem 5.7.

We can invoke an appropriate result of regularity (see Lieberman [22], Lemma 12.13) that state that locally is Hölder continuous in space. Adapted to our case here is the result:

Lemma 5.11 ([22]).

Let solve on equation (57), such that for some , . Then for , for , for

The dependence with respect to is controlled by ,the lower and upper bounds on and If moreover then .

For , consider for some

Then , and solves

| (64) |

We now use Lemma 5.10, which yields that for some positive constants , one has

Hence, Lemma 5.11 applies, and granted we have a bound on (as assumed in the Theorem), is bounded and Hölder continuous uniformly with respect to . Then using Schauder estimates ([22], see also [38] for a very synthetic proof) this gives a uniform control on and in . This in turn guarantees that is also uniformly bounded in , and and since , one obtains the result that is uniformly bounded on .

We obtain a bound on from below as a consequence of Harnack inequality. Using the choice of and (63), will satisfy uniformly with respect to

and given the bound on , this implies

| (65) |

for some . Then, differentiating twice the equation (64), we obtain that solves an equation of the form

| (66) |

where . Under the assumption that is bounded, the coefficient are uniformly bounded with respect to , and is also bounded away from 0. We already now that is positive, bounded and continuous, moreover by (65) we have that

We can now invoke Harnack inequality for the solution of (66) (see [22] Theorem 6.27) that implies that, locally, the supremum of at a given time is controlled by the infimum of at time . Hence the infimum of has to stay uniformly away from 0. This in turn implies that remains uniformly bounded away from on , hence that is bounded away from , and we have obtained the following lemma:

Lemma 5.12.

For , belongs to , and there exists depending on such that for ,

We now differentiate the equation with respect to to obtain regularity for . Since is bounded, we also have that is bounded in for compactly supported in . We also assume that bounded, hence belongs to . Then we observe that

hence

This implies that and are bounded, and the same holds then for , given that is bounded away from as we just showed.

To prove regularity up to the initial boundary when the initial data is such that is uniformly bounded in (which is the case if is bounded) we just apply standard parabolic regularity (see [22], Theorem 5.14).

5.7. Local interior bounds

Under minimal assumptions on , one can still establish local interior regularity. The proof of this result is deferred to the Appendix C.1, as it is a similar to the proof of Theorem 5.7.

Theorem 5.13.

Remark. The bound can be be made dependent only on for varying in .

5.8. Initial regularity

We also mention that regularity holds up to the initial time on cylinder ”above” areas where is smooth. This result will be useful to define the stock’s dynamic as a proper martingale up to time (see Theorem 6.3).

Theorem 5.14.

Proof. It uses a classical cutoff argument. Multiplying by a cutoff function compactly supported in , solves

for . One already has from Lemma 5.11 a global bound on , from Lemma 5.11. Since is smooth on the parabolic boundary of , classical Schauder regularity (see again Lieberman [22], Theorem 5.14) applies up to the boundary and yields the desired result.

5.9. Construction of solutions

We now prove the existence of solutions, using the a priori bounds and the continuity method:

Proposition 5.15.

Proof. We consider for defined as follows:

where is non-negative, non-increasing and satisfies:

We start from , and consider the derivative of solution to (22) with respect to : solves

with , where and If for some there holds

| (68) | |||

| (69) |

then one can define the unique strong solution on to

and can be found by the following representation formula

and . Hence the linearized operator is invertible at a point satisfying (68, 69), and from the implicit functions theorem one can find a solution for close to .

Then, under the assumption of Theorem 5.7, (68, 69) hold on , while, as on , Theorem 5.5, yields that (68,69) hold on . Therefore one can apply the continuity method (see [16]) to build the curve , and enjoys uniformly the a priori estimates of Theorem 5.7. Finally solves (22, 23, 24).

5.10. Existence and uniqueness results

We conclude with the main existence, regularity result:

Theorem 5.16 (Existence and regularity).

Remarks. Those solutions will then naturally enjoy the a priori estimates of Theorem 5.7 or 5.13, as they are satisfied for any classical solution.

Again, in view of Tychonov’s counterexamples [35], such a uniqueness result in seems surprising without any growth condition, but recall that in our definition of classical solutions (Definition 5.1) we embed an assumption of semi-concavity for .

Proof. One can approximate by a sequence satisfying the assumptions i) to v)of Theorem (5.7). By letting go to 0 the interior estimates do not depend on , and using a standard compactness argument the sequence of solutions converges locally uniformly, and the a priori estimates pass to the limit.

We prove now the uniqueness part, and for this we need the following result whose proof is deferred to the appendix A.1.

Theorem 5.17.

We already know that the a priori estimate of Theorem 5.7 holds. Then by the comparison result of Theorem 5.17 applied on (which is allowed using the interior a-priori estimates), one obtains that

is non-increasing. We can conclude if for the two solutions there holds

| (70) |

This comes by considering the rescaled solution introduced in the proof of Theorem 5.7. By a compactness argument, converges to in as , uniformly with respect to , which implies (70).

6. Representation of the solution

We consider as above a standard Brownian motion on a filtered probability space , and to be the solution to (31, 32, 33), i.e.

with as initial condition. Following the notations introduced previously, we introduce with , and, and is the inverse of with respect to :

| (71) | |||||

| (72) |

and (72) has to be understood in the sense of Proposition 5.3.

6.1. A maximum principle for the second derivative

We state this result of independent interest for as in (23), but it is valid for a large range of non-linear diffusions. The result will be used in the proof of Theorem 6.3.

Theorem 6.1.

Proof. We proceed by approximation. On one can choose smooth and close to , so that the solution to (22) with on the parabolic boundary of is smooth in the interior of and globally on . Then is smooth enough to differentiate twice the equation, and solves

| (75) |

which, by Schauder regularity implies , uniformly and since implies that and hence are (locally in , uniformly with respect to ) Lipschitz. As we are on a bounded domain, by uniqueness converges to , and to . The stochastic differential equation (31,32,33) admits then a unique local strong solution, and is uniquely defined by the representation formula:

where is the first exit time outside of . We now let go to 0, as a.s., assuming an a priori bound on , the equality above remains true by uniform integrability. If the upper bound on is not assumed, there still remains the lower bound as , and by Fatou’s lemma, the inequality (6.1) holds.

We now introduce a modified process that will be key to study the properties of the process .

Proposition 6.2.

Remark. When we recover that .

Proof. We have that

Rearranging the terms we obtain that

and the result follows.

6.2. Dual representation formula and martingale property under

Based on the variational formulation (3), we now have a representation result for the solution , as well as a martingale property result for solution of (31, 32, 33).

Theorem 6.3.

Remark. As we will see, condition (78) implies and thus implies to be in the second case of point 4 in Proposition 5.3.

Proof. Consider the stopping time

| (84) |

and define the stopped process the process stopped at time . We then have the following Proposition:

Proposition 6.4.

The process defined above is a martingale on , and under the probability given by

satisfies on

| (85) |

for a Brownian motion under . If moreover is a martingale up to time , then we define accordingly and (85) holds up to time .

Proof. The proof is a straightforward application of Girsanov’s Theorem (see [19]).

To prove (81), we use the representation formula (6.1). Given the uniform bounds we have on and from Theorem 5.13, we claim that there exists a constant independent of such that

| (86) |

Indeed, if this is not true, considering the stopping time , by formula (6.1) one can show that for any , which contradicts the regularity result of Theorem 5.13. Then almost surely, is finite, which shows that almost surely , and moreover that almost surely is continuous up to time .

To prove that is a martingale up to time , we consider the stopped process . By the result of Theorem (5.13), goes to a.s. as goes to 0. The sequence is a sequence of martingales up to time that satisfies for all . If we can show that the family is equi-integrable, and that it converges to , then satisfies , and by standard arguments, as is non-negative, this implies that is a martingale up to time . We consider the family , and its inverse , and we have using Proposition 6.4

where

First we observe that by Chebyshev’s inequality can be bounded by . Then we have

Proof. Indeed remember that is the inverse of and that . This is then an consequence of Lemma 5.8 combined with the concavity of : under assumption (78), is bounded away from on every set , bounded

Finally is bounded in uniformly with respect to and if we have a uniform bound on , we have a uniform bound on which shows the equi-integrability of the family. Having observed above that is almost surely continuous up to time , converges a.s. to , hence which allows to conclude. It thus remains to show that

Lemma 6.6.

Under the assumptions of Theorem 6.3, is bounded in , uniformly with respect to .

Proof. We will use Theorem 6.1 and the inequality (6.1). We need to bound

which, assuming a bound on is equivalent to a bound on , and which follows directly from the fact that

from Theorem 6.1. Since is bounded by Theorem 5.13, the result follows.

To prove (83) we use again the stopped process . Then for , (35) holds up to , i.e.

where is as in (32). Under our assumptions satisfies for some , . This combined with the above identity implies that

hence, since is finite, and using Cauchy-Schwartz’s inequality, is uniformly bounded as goes to 0.

We now prove that identity (35) holds even when is not smooth up to time . We consider the stopping times . Then there will hold by Itô’s formula

where . Arguing as Lemma 6.6, is bounded under the assumption that is bounded. By monotone convergence, converges thus to . Then under (29), is bounded above by , hence by Fatou’s lemma

as we know already that is a martingale. We then have the first inequality

On the other hand we know that is concave hence by Jensen’s inequality (and using again that is a martingale)

where is chosen so that is non increasing (such a exists since is bounded by below). By monotone convergence the second term goes to 0 and the third converges easily to 0, which shows that

and equality thus follows:

| (87) |

Remark. As stated in the Theorem, this equality holds true even if is always finite under the assumptions of the Theorem, and then (87) is equivalent to (79).

Following the same lines, for any element of one can reproduce the computations of section 4 and find that

It is straigthforward to show that the second part converges to

when goes to , and this shows one part of (80). To show the other side (that indeed realizes the supremum), one considers again the stopped process and . Then , belongs to , and the same arguments as above show that

6.3. Black-Scholes representation formula, and explicit formulation of the density

We go back to the equation (58). As has already been observed is given by

where has been defined in (71), and satisfies

| (88) |

We consider for a probability on , a -Brownian motion and the solution to

| (89) | |||||

Under the assumptions of Theorem 5.13, has enough regularity to check that is a local martingale on . We have then the following representation result, which we call a Modified Black-Scholes representation:

Theorem 6.7 (Local volatility).

We state right away an extension of this result in the constant volatility case, which will come as a corollary of Theorems 6.3 and 6.7.

Theorem 6.8 (Constant volatility).

Remarks. The representation formula (90) is a Widder’s type uniqueness result, as it shows that the solution of the parabolic equation (88) (seen as a linear equation) is unique and defined by the representation formula (90). Again the key ingredient here is that we restrict ourselves to concave solutions (wich replaces the positivity assumption needed in Widder’s Theorem.)

Regarding formulas (92) and why we call it a modified Black-Scholes formula, it is well known that the classical Black-Scholes formula for a call option consists of two terms

Indeed, for , ), this identity becomes a tautology since in the Black-Scholes model, both and are martingales under the risk neutral probability. In the linear market impact model, there is a risk-neutral probability (the probability in our notations), and while is not the expectation of its final value (see formula 35), hence not a martingale under , when is constant, remains a martingale, and formula (92) reads similarly

Taking , satisfies

| (97) |

with . Then

with . We now let be the solution to

and then is a martingale, and a similar result hold. In the limit , we recover simply that is a martingale.

Proof of Theorem 6.7. It has already been seen that is a local martingale under , and it remains to prove that is a martingale up to time . Arguing as in the proof of Lemma 5.8 (see section B.1 in Appendix) , we have

therefore letting

can be bounded by above by a constant independent of , as is bounded. Hence if is equi-integrable, is equi-integrable, which implies that . This is enough to conclude following standard arguments (see [19]) that is a martingale, which in turn allows to conclude that is a martingale up to time .

The proof of

Lemma 6.9.

Under assumption (51), is equi-integrable for .

is deferred to the appendix, section B.2.

To prove the existence of , from Proposition 5.2, under condition (51) there holds

-

-

,

-

-

,

and is non-decreasing, which allows to conclude the existence and uniqueness of .

Proof of Theorem 6.8. This theorem is a corollary of Theorems 6.3 and 6.7. For Point 1, once is a martingale up to , one can define the probability , and follows then

| (98) |

for a Brownian motion.

For point 2, when is constant, follows also equation 58, which shows the Step 2 of the Point 2, and one then uses formula (90).

Point 3 is the direct consequence of (98),

Point 4 is a particular case of (3) when . Note that as remarked at the end of the proof of Theorem 6.3, the finiteness of is equivalent to the finiteness of .

7. a Black-Scholes-Legendre formula

In this section we derive the first order expansion of the solution with respect to the market impact parmeter . To establish rigorously this expansion, we will need the regularity results of the pricing equation, and the representation formula previously established.

7.1. Formal computations

For this we will use the identity (34). We are in the case where are constant. We still consider a probability under which follows (31, 32, 33), and we let be a probability under which for a Brownian motion. Consider the Black and Scholes solution, i.e. the solution to (22) for , a formal Taylor expansion around of (22) yields

and We now evaluate . To do this, we define

| (99) |

note that

for the Legendre transform of . Observe that, if solves the Black Scholes equation, then is a martingale under (this is checked by a simple computation). Then .

We have then, under ,

Then

moreover, . Then we obtain a first modified Black-Scholes-Legendre formula

| (100) | |||||

We then observe that, if is any reasonable Lipschitz function and

| (101) |

Then

Hence, replacing by in the above formula will only add terms of order 2 terms in . In the case of a call (resp. put) option with strike this yields (resp. ). Now let

(resp. ) be the Black Scholes call (resp. put) price, then

| (102) | |||||

| (103) |

Remarks. Note that (100) allows to compute the first order market impact correction using a simple Monte-Carlo/analytical pricer, for any terminal payoff as long as one is able to compute . It can be computed without relying on the constant volatility assumption, so it can still be computed in presence of local or even stochastic volatility, however, in those cases is not a martingale anymore, so the first order expansion should be slightly different.

Note also that the analytical price of call spread with strikes would be easily computed since in that case .

Note that the correction term is indeed quadratic in .

The correction obtained here is also formally valid for the case of pure liquidity costs studied by Cetin, Soner and Touzi [9], since at first order the two pricing equations are the same, it also should be valid for any fully non-linear modification of the Black Scholes equation.

It now remains to turn the formal expansion into a rigorous statement.

7.2. First order expansion of the solution

Theorem 7.1.

Let be a terminal payoff and let be defined as in (101). Assume that is globally Lipschitz and satisfies the assumptions i) to iv) of Theorem 5.7, and that is bounded. Let be the solution of (22, 23, 24) with constant volatility parameter . Then is differentiable with respect to and there holds

| (104) |

where follows (31, 32, 33), and moreover

| (105) |

Proof. We first start with a smoothed terminal payoff satisfying the constraint (30). Let be the derivative of with respect to . Then

and is supported on . One can thus write

where is solution of (31). We have that as it is supported on . Then in order to show (104), we need to show that this integral indeed converges to the expected limit, as converges to , in particular near . From Theorem 5.7, and given our assumptions on , there hold uniform bounds on and on for . Hence the integral up to will converge when goes to thanks to the dominated convergence Theorem. We just need to show that

converges to as , uniformly with respect to and to the terminal condition , as long as satisfies the assumptions of the Theorem. For this we will use the results of Theorem 6.3.

Lemma 7.2.

Proof. Under the assumptions of Theorem 7.1, the assumptions of Theorem 6.3 are satisfied, hence is a martingale up to time , and one can define as in Proposition 6.4. Then of course is a martingale under , hence is a martingale under , and as shown in Theorem 6.7, is also a martingale under , hence so is .

We now observe that

and

| (106) |

We then compute

where in the third line we have used Theorem 5.16, formula (3). Then assuming that is bounded, there exists such that

| (107) |

and this estimate is propagated by the heat equation, so that for another value of the bound (107) holds on . Plugging this into the above equality yields

where we have used Girsanov’s Theorem for the second line. We now use (106) which yields for

where solves (by Proposition 7.2)

| (108) |

Then it follows that, letting

we have, for another constant ,

Moreover, we have using (108)

so that by Cauchy Schwartz’s inequality

for , hence , where . It remains to show that converges to 0 uniformly with respect to as . This is a straightforward consequence of the dominated convergence theorem, as is bounded under our assumptions.

8. Numerical simulations

In this section we present for illustration purposes a numerical implementation of the model. Another study of a numerical implementation scheme is provided in the companion paper [6]. We propose the following numerical scheme: We set to a small constant ( in our applications), and divide the time interval into time intervals . We let .

-

-

Define the truncated operator

-

-

Initialize .

-

-

Terminal condition Initialize

-

-

time loop For down to

-

-

initialize .

-

-

Non linear iterations for in

-

-

solve for

-

-

Set if and do one more non-linear iteration or

-

–

Set and exit non-linear iterations loop

-

-

-

-

iterate on the time step with set above.

Typically, the number of non linear iterations needed for convergence was small: was enough in our numerical example.

For stability reasons, we use an implicit scheme in the non-linear iterations. An alternative to this method would be to enforce the constraint on the gamma at each time step, but we empirically observe that our method worked quite well. As noticed above, with a constant volatility model, it is enough to enforce the upper bound on on the terminal condition, but this fails to be true with a generic local volatility.

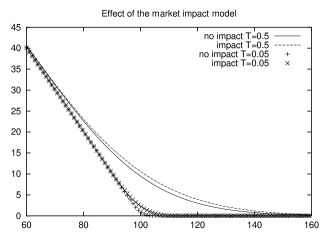

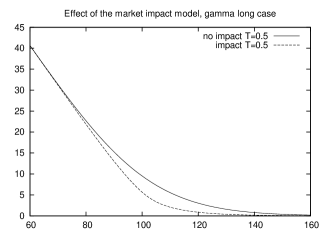

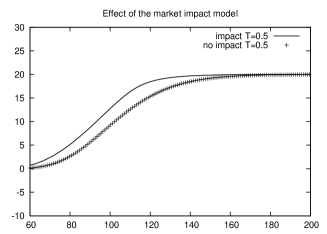

We present the cases of 100-strike put option Figure 3(a) , minus a 100-strike put option Figure 3(b) , and a 90-100 call spread Figure 3(c). The numerical values used are , , no interest rates or dividends. Note that in Figure 3(a) (resp. 3(b)) the option sold is convex (resp. concave), while in Figure 3(c) the second derivative of the payoff changes sign. One sees that in all cases the market impact plays against the option’s seller (the put sold is more expensive, and put bought is cheaper).

Appendix A

A.1. Proof of Theorem 5.17

We perform the change of variable , and consider , which yields that . Under the above assumptions, and have logarithmic growth near and linear growth at , hence have exponential growth. The derivatives of with respect to are bounded up to order 3, and is uniformly Lipschitz as a function of . Then solves

This can be seen as a linear equation of the form

where are bouded, uniformly Lipschitz in , bounded away from 0. Then we can apply classical results of comparison under exponential growth (see [3]).

Appendix B

B.1. Proof of Lemma 5.8

We consider introduced in (89) under the probability , with a -Brownian motion, and the expectation under . We drop the superscripts for the rest of the proof proof. We need first the following Lemma:

Lemma B.1.

There exists such that

| (109) |

Proof of Lemma B.1. First note that is concave, increasing and has limit equal to 0 at . Then since ,

| (110) |

hence is non decreasing. The concavity of implies then that is non-positive. Then we consider defined in (89). Note that as we assume that is a classical solution, then , and as moreover is bounded, is well defined. There holds that

| (111) |

is also non-positive and satisfies

It is therefore a non-positive sub-martingale, and there holds by Fatou’s lemma

This implies that is finite. Then using the concavity and monotonicity of and Itô’s formula, one has

| (112) |

which shows that for ,

is finite as long as is finite. The conclusion of the proof then follows by observing that, from (110),

We now go back to the proof of Lemma 5.8. Since , by standard manipulations on the heat kernel, (51) implies that for some ,

| (113) |

is finite, hence is defined on and . Observe that (resp. is solution to

(resp.

We write for

We consider , which is non-positive. From the concavity and monotonicity of , one obtains by simple calculations that if satisfies (109) for some , then and and hence also satisfy (109) for any . Consider then defined by

Then since satisfies (109), is well defined for for some , and solves

with . Finally we have

where satisfies

| (114) |

with , and satisfies (109). Then we have the following lemma:

Lemma B.2.

Proof. This is a straightforward adaptation of the proof of Tychonoff [35]. The inequality obtained there page 207 adapted to our case is

with . Choosing small enough so that the right hand side is integrable leads to the conclusion that .

Since and satisfy the growth condition (109), Lemma B.2 implies that is indeed equal to defined above up to . The argument can then be repeated up to and yields uniqueness up to . Then , where is non negative, hence we conclude . The other inequality follows directly from (112).

B.2. Proof of Lemma 6.9

To prove the equi-integrability of , we will use Lemma 5.8, hence for all

where the last line comes by using the concavity and the the monotonicity of . As has been observed already, , hence by standard computations on the heat kernel, the last line is uniformly bounded under (51). Hence for ,

where . By Chebyshev’s inequality, this implies that

hence that

Finally summing the two we have that

Appendix C

C.1. Proof of Theorem 5.13

Under the condition , . We first prove the following Lemma:

Lemma C.1.

The constants depend only on the behaviour at and of

Proof of Lemma C.1 We start by constructing two barriers as in the proof of Theorem 5.7: are the inverse of defined by (60, 61) in Lemma 5.8, and , which then yields From the construction of (see Proposition 5.3, point 8), under assumption (51) there holds

and moreover

which imply that

| (116) | |||||

| (117) | |||||

| (118) |

Limits (116, 117, 118) are propagated for time and, for , and are strictly increasing. Moreover, as noted in (110), is non decreasing, hence

The concavity of and (116, 117, 118) imply then a control on the way in which goes to at and goes to as , which passing to yields the lemma.

Proof of Theorem 5.13. We study (57) on compact sets of for small . From Lemma C.1, we see that (57) is uniformly parabolic and that we have an a priori bound for and . We can thus apply Lemma 5.11, to obtain local regularity for for time . As in the proof ot Theorem 5.7, equation (57) on can now be seen as a linear parabolic equation with Hölder coefficients, and Schauder estimates then yield that . By differentiating the equation, further regularity follows if has additional regularity. Then using the left side of the inequality in Lemma C.1, the local regularity of on implies local regularity of on , henceforth of on any compact set of . This achieves the proof of Theorem 5.13.

Appendix D Existence of smooth solutions for general

Here we state a simple result of smoothness for ”good” initial data in the case where , when is constant. In this case, we need to start with well behaved solutions, as the singularity of the solution can not be treated by the Legendre transform technique of the previous section. What we show is the following:

Theorem D.1.

Proof. We only sketch the proof, this is an adaptation of Propositon 5.15 that relies on the estimate formula 6.1. This is a simple consequence of the identity (6.1). From this and the conditions on the boundary data , one can construct a solution such that (6.1) holds and remains bounded above and below. Then classical parabolic regularity theory yields the result.

We make the following observation:

Proposition D.2.

Let , be a smooth increasing function such that and . Then there exists such that

Moreover .

This comes by elementary computations, and shows that under mild conditions on , any fully non-linear pde of the form can be derived as a market impact pricing equation. Note that the conditions imply and .

References

- [1] Frédéric Abergel and Grégoire Loeper. Pricing and hedging contingent claims with liquidity costs and market impact. To appear in the proceedings of the International Workshop on Econophysics and Sociophysics, Springer, New Economic Window, 2016.

- [2] R.A. Almgren. Equity market impact. RISK, July, 2005.

- [3] Andrea Pascucci (auth.). PDE and Martingale Methods in Option Pricing. Bocconi & Springer Series. Springer-Verlag Mailand, 1 edition, 2011.

- [4] G. Barles. Solutions de viscosité des équations de Hamilton-Jacobi. Mathématiques & Applications [Mathematics & Applications], 17. Springer-Verlag, Paris, 1994.

- [5] B. Bouchard, G. Loeper, and Y. Zou. Almost sure hedging with permanent price impact. Finance stoch. to appear.

- [6] B. Bouchard, G. Loeper, and Y. Zou. Hedging of covered options in a linear market impact model. http://arxiv.org/abs/1512.07087.

- [7] Y. Brenier. Polar factorization and monotone rearrangement of vector-valued functions. Comm. Pure Appl. Math., 44(4):375–417, 1991.

- [8] Umut Çetin, Robert A. Jarrow, and Philip Protter. Liquidity risk and arbitrage pricing theory. Finance Stoch., 8(3):311–341, 2004.

- [9] Umut Çetin, H. Mete Soner, and Nizar Touzi. Option hedging for small investors under liquidity costs. Finance Stoch., 14(3):317–341, 2010.

- [10] Patrick Cheridito, H. Mete Soner, Nizar Touzi, and Nicolas Victoir. Second-order backward stochastic differential equations and fully nonlinear parabolic PDEs. Comm. Pure Appl. Math., 60(7):1081–1110, 2007.

- [11] Michael Crandall and Michel Pierre. Regularizing effects for in . J. Funct. Anal., 45(2):194–212, 1982.

- [12] Michael G. Crandall, Hitoshi Ishii, and Pierre-Louis Lions. User’s guide to viscosity solutions of second order partial differential equations. Bull. Amer. Math. Soc. (N.S.), 27(1):1–67, 1992.

- [13] Michael G. Crandall and Michel Pierre. Regularizing effects for . Trans. Amer. Math. Soc., 274(1):159–168, 1982.

- [14] R. Frey. Perfect option hedging for a large trader. Finance and Stochastics, 2(2):115–141.

- [15] R. Frey and A. Stremme. Market volatility and feedback effects from dynamic hedging. Mathematical Finance, 7(4):351–374, 1997.

- [16] D. Gilbarg and N. S. Trudinger. Elliptic partial differential equations of second order, volume 224 of Grundlehren der Mathematischen Wissenschaften [Fundamental Principles of Mathematical Sciences]. Springer-Verlag, Berlin, second edition, 1983.

- [17] L. V. Kantorovich. On mass transportation. Dokl. Akad. Nauk. SSSR, 37:227–229, 1942.

- [18] L. V. Kantorovich. On a problem of Monge. Uspekhi Mat.Nauk., 3:225–226, 1948.

- [19] Ioannis Karatzas and Steven E. Shreve. Brownian motion and stochastic calculus, volume 113 of Graduate Texts in Mathematics. Springer-Verlag, New York, second edition, 1991.

- [20] Robert V. Kohn and Sylvia Serfaty. A deterministic-control-based approach to fully nonlinear parabolic and elliptic equations. Comm. Pure Appl. Math., 63(10):1298–1350, 2010.

- [21] D. Lamberton, H. Pham, and M. Schweizer. Local risk-minimization under transaction costs. Mathematics of Operations Research, 23:585–612, 1997.

- [22] Gary M. Lieberman. Second order parabolic differential equations. World Scientific, Singapore, River Edge (N.J.), 1996. R impression : 1998.

- [23] H. Liu and J. M. Yong. Option pricing with an illiquid underlying asset market. Journal of Economic Dynamics and Control, 29:2125–2156, 2005.

- [24] G. Loeper. The reconstruction problem for the Euler-Poisson system in cosmology. Arch. Ration. Mech. Anal., 179(2):153–216, 2006.

- [25] H. M. Soner P. Cheridito and N. Touzi. The multi-dimensional super-replication problem under gamma constraints. Annales de l ’Institut Henri Poincar , S rie C: Analyse Non-Lin aire, 22:633–666, 2005.

- [26] E. Platen and M. Schweizer. On feedback effects from hedging derivatives. Mathematical Finance, 8(1):67–84, 1998.

- [27] R. T. Rockafellar. Convex analysis. Princeton Landmarks in Mathematics. Princeton University Press, Princeton, NJ, 1997. Reprint of the 1970 original, Princeton Paperbacks.

- [28] P. J. Schönbucher and P. Wilmott. The feedback effect of hedging in illiquid markets. SIAM J. Appl. Maths, 61(1):232–272, 2000.

- [29] H. M. Soner and N. Touzi. Superreplication under gamma constraints. SIAM J. Control Optim., 39:73–96, 2000.

- [30] H. M. Soner and N. Touzi. Dynamic programming for stochastic target problems and geometric flows. Journal of the European Mathematical Society, 4:201–236, 2002.

- [31] H. M. Soner and N. Touzi. Hedging under gamma constraints by optimal stopping and face-lifting. Mathematical finance, 17:59–80, 2007.

- [32] H. Mete Soner, Nizar Touzi, and Jianfeng Zhang. Dual formulation of second order target problems. Ann. Appl. Probab., 23(1):308–347, 2013.

- [33] Xiaolu Tan and Nizar Touzi. Optimal transportation under controlled stochastic dynamics. Ann. Probab., 41(5):3201–3240, 2013.

- [34] B. Tóth, Z. Eisler, F. Lillo, J. Kockelkoren, J.-P. Bouchaud, and J. D. Farmer. How does the market react to your order flow? Quant. Finance, 12(7):1015–1024, 2012.

- [35] A. Tychonoff. Théorèmes d’unicité pour l’équation de la chaleur. Rec. Math. Moscou, 42(2):199–216, 1935.

- [36] Juan Luis Vázquez. Smoothing and decay estimates for nonlinear diffusion equations, volume 33 of Oxford Lecture Series in Mathematics and its Applications. Oxford University Press, Oxford, 2006. Equations of porous medium type.

- [37] C. Villani. Topics in optimal transportation, volume 58 of Graduate Studies in Mathematics. American Mathematical Society, Providence, RI, 2003.

- [38] Xu-Jia Wang. Schauder estimates for elliptic and parabolic equations. Chinese Ann. Math. Ser. B, 27(6):637–642, 2006.

Gregoire Loeper

Monash University

School of Mathematics

9 Rainforest Walk

3800 CLAYTON VIC, AUSTRALIA

email: gregoire.loeper@monash.edu