Conservation laws, financial entropy and the Eurozone crisis

Abstract

The report attempts of apply econophysics concepts to the Eurozone crisis. It starts by examining the idea of conservation laws as applied to market economies. It formulates a measure of financial entropy and gives numerical simulations indicating that this tends to rise. We discuss an analogue for free energy released during this process. The concepts of real and symbolic appropriation are introduced as a means to analyse debt and taxation.

We then examine the conflict between the conservation laws that apply to commodity exchange with the exponential growth implied by capital accumulation and how these have necessitated a sequence of evolutionary forms for money, and go on to present a simple stochastic model for the formation of rates of interest and a model for the time evolution of the rate of profit.

Finally we apply the conservation law model to examining the Euro Crisis and the European Stability pact, arguing that if the laws we hypothesise actually hold, then the goals of the stability pact are unobtainable.

1 Conservation laws in market exchange

In the physical sciences conservation laws provide a basic framework within which theories are cast. They are so fundamental that it is hard to conceive of any mathematically expressed system of mechanics that does not rest on such laws.

Do similar laws exist in economic theory?

In a sense yes, where they are termed ‘accounting identities’ and regarded as something pretty trivial. We want to argue that this view of them as something trivial is misplaced, and that they can actually tell us a lot more about the nature of social relations and their degree of constrainedness than is generally realised.

Marx, to an extent greater than is sometimes recognised, wanted to establish a theory of the capitalist economy informed by the laws of physics. [3, ch. 2] This comes across in several ways: his avowed aim to write a book on the ‘laws of motion’ of capitalism; his distinction between the concept of labour and labour power; his presentation of value as the crystalisation of human energy; and his analysis of commodity exchange as an equivalence relation.

Marx said that in Capital he was investigating the ‘laws of motion’ of capitalism. This might be understood as only a metaphor derived from physics, but we think that it is worth taking it seriously. If you think of the time he was writing – the 1860s – one of the key recent discoveries of physics was the idea of the conservation of energy. The conservation of energy had been formalised by Helmholtz and Grove in the late 1840s. This held that although energy might appear in various forms: heat, motion, gravitational potential, it was conserved in its exchange between these forms.222“What Lucretius says is self-evident; ‘nil posse creari de nihilo,’ out of nothing, nothing can be created. Creation of value is transformation of labour-power into labour. Labourpower itself is energy transferred to a human organism by means of nourishing matter.” [20, ch. 9]

Marx’s initial argument in Capital, before he derives labour power as the source of surplus value is similar. Value is neither created nor destroyed in the exchange process, but can only change its form. His argument asserts in effect a law of the conservation of value in exchange.

Think of the distinction between ‘labour’ and ‘labour power’. This is so closely parallels Watt’s distinction between ‘work’ and ‘power’, that it is surprising that the similarity is rarely remarked on.333This need not have been via a direct study of Watt by Marx. Watt’s distinction between work done and power: the ability to perform work, measured in standard horse-powers had become a commonplace of industrial society. His analysis of commodity exchange is also structured like an analysis of a conservation law [20]. He introduces as an example

20 yards of linen = 1 coat or 20 yards of linen are worth 1 coat,

in this notation he says that the coat plays the role of the equivalent and that it implies also the converse relation

1 coat = 20 yards of linen or 1 coat is worth 20 yards of linen.

He then presents what he calls the expanded form of the relation

20 yards of linen = 1 coat

20 yards of linen = 10 lbs of tea, etc.

And goes on from this to state that 1 coat will be equal to 10 lbs tea. What he is doing here is setting out what in modern mathematical terminology is an equivalence relation. For some relational operator we say that is an equivalence relation if the relations is commutative, transitive and reflexive, that is

-

•

if

-

•

and if implies

-

•

and if and implies

then the relation is an equivalence relation. In his case would stand for exchange of commodities. Now equivalence relations are interesting because systems goverened by conservation laws display them. Thus in a many-body gravitational problem with a predefined collection of particle masses, the set of possible configurations of particle position and velocities is partitioned into equivalence sets with respect to energy. Within each set all configurations share the same total energy and the conservation of energy prevents transitions of configurations between these sets.

This is in essence what we understand by a conservation law.

We infer the existence of energy as a conserved quantity by the fact that, in closed systems, we never observe transitions between configurations with different total energies.

Marx’s demonstration that commodity exchange is an equivalence relation is then used to infer that there is a conserved quantity ‘value’, the sum of which is unchanged under the operation of exchanges. Commodity exchange is governed by a conservation law. To borrow much later terminology, exchange is shown to be a zero-sum game.

This may seem a trivial observation, but it leads to an important deduction: that in a conservative system, any surplus of value – profit – must arise from outside of the system and thus that profit must originate from production rather than exchange. Marx argued that the conserved quantity in commodity exchanges is human energy expended as labour and that this energy provides the external input that allows a surplus. At the economy’s two ends, production and consumption, the process is nonconservative but in between them lies market exchange: a conservative system.

1.1 Finance and conservation laws

Although economists are sometimes dismissive of conservation laws, disparagingly called ‘accounting identities’, these identities can still throw useful light on the financial crisis that has been unfolding these last few years. But to do this we need to uncover the specific laws of motion, that is to say both the conservation laws and the particle dynamics that govern the financial system.

That we have to think of the financial system using tools derived from statistical mechanics should be obvious by now. It is over a quarter of a century since it was shown that the regulation of prices by labour content arises directly from statistical mechanical considerations [11].

If we look at the more recent work on the statistical mechanics of money [8, 10], we can see a similar structure of argumentation – pushed somewhat by the use of more sophisticated physics. This research argues that if we treat trades between commodity owners as a random process that conserves money, then you can use statistical mechanics to make deductions about the distribution of money. Money as a conserved quantity randomly transfered in exchanges between agents, models the transfer of energy between gas molecules and it follows that the maximum entropy distribution of money will be a Gibbs-Boltzmann one. The statistical mechanics of money shows that this distribution fits the observed distribution of money for most of the population, but that a small minority of very rich people fall off this distribution – their wealth follows a power-law. The Gibbs distribution falls of sharply at high levels of wealth, whereas the the tail of the power law distribution extends much further.

The probability of anyone being as rich as Bill Gates or Warren Buffet as a result of simple commodity trading is vanishingly small, so [9, 24] conclude that there has to be some mechanism outside of equivalent exchange that gives rise to their extraordinary wealth: the effect of compound interest which is a non-random process.

Research in agent-based modeling has shown that if you partition the population into buyers and sellers of labour power and run agent-based simulations, you a reproduce the combination of Gibbs and power-law distributions of wealth [32] observed in real capitalist economies [9, 24]. Further, when producers can specialise in and switch between different commodity-types, Marx’s law of labour value appear as an emergent phenomenon from local and distributed market exchanges [33].

1.2 The phase space of finance

A basic tool of conceptual analysis in statistical mechanics is the concept of phase space. If you consider a collection of particles (for example stars) in a closed volume, each particle can be described by 6 numbers which specify its position and momentum in terms of a three-dimensional Cartesian coordinate system: 3 numbers to specify the position and 3 numbers to specify its momentum. We say that each particle has 6 degrees of freedom.

So if we have a million particles, for instance if one is considering the dynamics of a galaxy, the system has 6 million degrees of freedom and we can consider these to be a coordinate system such that every possible configuration of molecular positions and moments constitutes a point in this 6 million dimensional space. We call such a space a phase space. The laws of motion then specify a trajectory of the whole system through this phase space.

The overall system is governed by conservation laws. The mass is conserved, and relative to the center of gravity of the system as a whole the sum of the momenta in each of the directions of our Cartesian system must sum to zero.

Why is this relevant to finance?

Well we are again dealing with a system with very large numbers of agents and we have analogues of position and momentum. The total debt/credit position of an agent is analogous to its mass, and the rate of change of its debt/credit position is analogous to its momentum. Thus if two billion people in the world are enmeshed in debt/credit relations then the whole system can be thought of as a phase space of 2 billion dimensions.

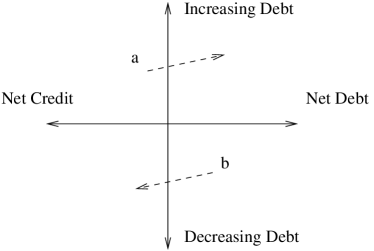

It is impossible to visualise a space with high numbers of dimensions, so there are graphical techniques that people use to reason about them. One trick is to project the high dimensional phase space down onto only two dimensions: for example, position and momentum in the direction of one of the axes of the coordinate system. This allows one to create a phase diagram. Applied to the financial system, a possible phase diagram is shown in Figure 1.

We could show every agent (firm, individual, state) as a point on this plane. Or in a more abstract way we could say that there is a density function which gives the probability of finding an agent in a given area in the phase plane. Using this probablility density function (PDF) we can formulate two conservation laws analogous to the conservation of mass and momentum.

-

i.

The total ‘mass’ on the left of the origin equals the mass on the right of the origin. Since the mass to the left is credit, and that to the right is debt, this is another way of saying that the total debt and total credit must balance.

(1) -

ii.

The total ‘mass’ above the origin must equal the mass below the origin, that is to say that any growth in debt must be compensated for by a growth in credit. This is an ‘equal and opposite reaction’ effect.

(2)

These very basic points establish that there is no net value or net wealth embodied in the financial system and that there is no flow of value into or out of the financial system. It shows the fallacy of the conception, popular among some political economists that capital has ‘moved into finance’ because of the low rate of profit pertaining in industry.

This is a fundamental misconception, capital is value, and it can not flow into the financial system, since the sum of value here is always zero. A moment’s thought about the materiality of value confirms this. Real-economic value – what the classical economists understood to be the labour content of physical products [22] – can not be converted into financial instruments which are just information structures.

A similar dimensional argument shows the fallacy of the idea of the ‘money supply’ used in orthodox economics. The notion of a supply originates with physical flows like the supply of water to a town, or the supply of cars provided by all the car factories in the world. There are flows in the financial system, e.g. flows of agents towards greater debt, but these are exactly balanced by flows towards greater credit positions, so the net flow is zero. If the term money supply is taken instead to mean a stock of money, and this is taken to include bank deposits, one then has the problem that both negative and positive money exist: liabilities and assets of the banking system respectively. Taken as a whole the positive and negative stocks cancel.

We believe it is better to try and understand the system in terms of its laws of motion. These laws are both the conservation laws (1) and (2), and the forces acting on the individual particles (capitalist firms, states, etc.). We will argue that the degree of ‘disorder’ or entropy of a financial system tends to increase over time. We would expect this of any chaotic system governed by conservation laws, but an examination of the force fields acting on the particles will show why this takes place.

1.3 Tendancy of financial entropy to rise

With the density function we can compute the entropy of a system, denoted , using the standard Boltzman formula,

| (3) |

and we assert that for a financial system will rise over time.

Why does the entropy tend to increase?

First a common-sense explanation. Consider a collection of firms or enterprises, distributed on the phase plane diagram as in Figure 1. Each firm can be considered a particle subject to forces which determine its rate of change of debt. There are three cases to consider:

-

(A)

A firm whose debt is rising because its profits are too low even to meet its interest payments to the banks. Such a firm has to borrow more from the bank to stay in operation. This firm is an involuntary borrower.

-

(B)

A firm may be voluntarily borrowing because it has a high rate of profit, well in excess of the interest rate, and thus can increase its profit of enterprise by taking on bank loans to invest and expand its business.

-

(C)

A firm may reckon that the rate of profit it can earn is lower than the rate of interest, but its current debt level may be quite low so that it is in a position to pay off its debts to the bank with some of its retained profit. A firm may even have no net borrowing and find that it is more profitable to earn interest on its cash than it is to invest it productively. Such a firm is a voluntary lender.

The total amount of borrowing must equal to the total amount of lending, thus if the quantity of voluntary borrowing by firms in group (B) falls below the quantity of lending by firms in group (C), the lack of demand from investments will automatically create sufficient firms in (A) trying to stay in operation through involuntary borrowing, ensuring that equation (2) is met. The net effect of this is to polarise capital in the phase plane as borrowers and lenders, giving rise to a tadpole shape with a head of productive firms and a tail of rentier firms, who earn their revenue from financial rather than productive assets. Therefore, as the dispersion or spread of the probability density function increases, the entropy rises, representing more disorder.

In previous work [5] we presented a numerical simulation model based on the methodology developed in [32] that models a simple capitalist economy with a large number of capitalists and workers. The state of indebtedness/credit of each of the capitals is tracked as the economy evolves. The capitalists interact via a very simple financial system represented by a single bank which maintains debit and credit accounts for agents based on a certain amount of base money which acts as its reserve. The evolution can be visualised in a phase plane diagram. For clarity we normalise the net debt of each firm by its total capital stock, which is known as the ‘debt ratio’.444Note that a firm with a net credit position has a negative debt ratio, . The capital stock was calculated from the current value of the commodity stocks and equipment of the enterprise. Similarly the rate of change of debt is normalised by its total capital stock. Initially the capitalists are clustered around the origin of the phase plane diagram, but as time passes the distribution becomes elongated with head of relatively indebted capitalists and long ‘rentier tail’ of capitalists with a negative debt ratio. This process is illustrated in Figure 2. The increase in entropy of the debt ratio PDF over time is shown.555Calculated using a per pixel binning of the PDF.

| PDF in the phase plane | ||

|---|---|---|

| 2 | 3.29 | |

| 5 | 3.72 | |

| 20 | 4.74 |

The greater is the dispersion of the rates of profit666Technically what we mean here is its coefficient of variation, its standard deviation relative to its mean. and the smaller the gap between the rate of profit and the rate of interest, the stronger will be this polarisation process and the more rapid will be the growth in financial entropy.777As we said earlier the net lending always sums to zero. As such it is analogous to a motorway with a stream of cars of equal weight heading past one another at 100kph in opposite directions. The sum of the momentums of the cars is zero. But if we square their positive or negative velocities times their weights we get the energy stored in the traffic. One can view the sum of the squares of the lending positions of all agents as a bit like energy in that it does not sum to zero as the activity of the financial system increases but with the important proviso, that this quantity is not conserved. It can grow without immediate limit. We will explain later why this growth in financial energy leads to crises.

The polarisation process generates a tadpole shape in the phase plane888It should be noted that so far this conclusion is based on theoretical arguments and the evidence from numerical simulations. An empirical investigation of the distribution of firms on the phase plane remains to be done. with a body of active firms clustered round the origin and a rentier tail of firms that progressively enlongates as the simulation goes on. Why do we get this asymetrical distribution?

Because the debt ratio of a capitalist can not for long exceed unity. A capitalist with more debts than assets is technically bankrupt and will shortly cease trading. There is on the other hand no limit to how negative the debt ratio of a capitalist can be. That is to say, no limit to how much money a capitalist can have in the bank.

What the argument above shows is that it is possible to derive a small set of laws of motion that characterise the basic development of a capitalist financial system. The essentials of the phenomenon that has been called ‘financialisation’, i.e., the growth of financial assets/liabilities relative to real assets, occurs even in a very simple model. The entropy of the system will increase, polarisation will occur, and a rentier class will be precipitated out, unless social work is done to curtail the growth of entropy.

In a more complex model with joint stock firms a similar polarisation will tend to occur, but in this case there may be pressure for firms with a very negative debt ratio (lots of cash) to distribute this to their shareholders.

This distribution is unlikely to put a halt to the polarisation process because in the case of cash being distributed from firms to individual capitalists the total of positive balances with the banking system does not change, it just shifts from abstract legal persons to concrete ones. The only mechanism by which the polarisation can be conservatively reduced is by the class of creditor firms and capitalists to purchase commodities from the class of debtor firms and capitalists. This will happen only to the extent that a distribution of money from cash-rich firms to rentiers results in an increase in the consumption of the rentier class.

Commodity exchange is a conservative system, i.e., one governed by conservation laws. This does not apply to taxation. Taxation is a non-equivalent transfer of value. Heavy taxation of the rentier class is a form of social work that reduces the entropy of the system.999The statistical mechanical effects on money distribution under different taxation schemes has recently been studied by [7]. The introduction of a regulated or planned economy is an even more powerful form of social work. In a planned economy the degree of chaos and disorder is reduced and coherent patterns are established which curb the growth of entropy characteristic of the free market.

1.4 Relation to the productive economy

The model above is very simple, it involves no inter-bank lending nor the issue of any complex financial instruments. All growth in debt arises from the behavior of basic actors in the real economy: capitalists and workers. But it is still able to generate the polarisation of the capitalist class into productive capitalists and financiers.

In a physical system, as it moves from a low entropy state to a high entropy state we are in principle able extract work from it. Is there any equivalent in the financial system?

Does it release any analogue of free energy as it evolves?

It is a commonplace observation that an economy with a low initial level of debt can grow rapidly as the debt builds up, but what is happening here?

We have said that there is no value absorbed in or contained in the financial system. The financial system is an information structure recording the mutual obligations of agents. But this does not mean that there may not be real value correlates of financial relations. If we look at all the firms with net debt – the integral over the right hand side of the phase plane in Fig. 1 – then these firms have all absorbed real resources from the left hand side of the plane. When capitalists on the bottom half of the phase plane fail to invest and capitalists on the top half do invest in excess of their income, the financial system sets up a system of obligations between the debtors and the saving capitalists. But at the same time, the firms on the bottom are provided with a market for their output on the top of the phase plane. There a transfer of real commodities from the bottom to the top.

A firm on the bottom, produces 10,000 buses containing perhaps 100 million hours of labour which are bought by agents on the top half. In return the bus company obtains not value but a credit account at the bank. This is not strictly speaking a commodity exchange. A credit account in a bank is not value. Had they been paid in gold and got back 1 million oz of gold bullion, that would have been a commodity exchange, an exchange of equivalents, since the gold would have contained real value: the human energy, labour, required to make it.

The sale of the buses for say 1,000 million Euros is a nonequivalent transaction in real terms since embodied labour is transfered between owners without a compensating movement of labour in the other direction. And, by our previous assumption, it is a transfer between a bus firm who were deciding to save 1,000 million rather than invest it productively. This transfer is thus one which would not have occured in the absence of the credit system. Had gold coins been the medium of exchange101010The existence of gold as a standard of value is not the same thing as its use as a medium of exchange. The gold standard persisted long after commodity circulation was generally carried out on credit., the million oz of gold would have lain in their safe at the bus factory and those purchasers who lacked cash (those who are on the right of the phase plane diagram in Fig. 1) would not have been able to buy the buses. The sale would thus never have taken place, and the total output of buses would have had to be 10,000 lower. Buses could still have been sold to firms who had ready cash, but this would have been a smaller number.

Readers of Marx’s Capital [20] may recall that he analysed the circulation of commodities as being of the form

i.e., commodity, money, commodity. He argues that this form already contains the possibility of crisis.111111“Nothing can be more childish than the dogma, that because every sale is a purchase, and every purchase a sale, therefore the circulation of commodities necessarily implies an equilibrium of sales and purchases. If this means that the number of actual sales is equal to the number of purchases, it is mere tautology. But its real purport is to prove that every seller brings his buyer to market with him. Nothing of the kind. The sale and the purchase constitute one identical act, an exchange between a commodity-owner and an owner of money, between two persons as opposed to each other as the two poles of a magnet. They form two distinct acts, of polar and opposite characters, when performed by one single person. Hence the identity of sale and purchase implies that the commodity is useless, if, on being thrown into the alchemistical retort of circulation, it does not come out again in the shape of money; if, in other words, it cannot be sold by its owner, and therefore be bought by the owner of the money. That identity further implies that the exchange, if it do take place, constitutes a period of rest, an interval, long or short, in the life of the commodity. Since the first metamorphosis of a commodity is at once a sale and a purchase, it is also an independent process in itself. The purchaser has the commodity, the seller has the money, i.e., a commodity ready to go into circulation at any time. No one can sell unless some one else purchases. But no one is forthwith bound to purchase, because he has just sold. Circulation bursts through all restrictions as to time, place, and individuals, imposed by direct barter, and this it effects by splitting up, into the antithesis of a sale and a purchase, the direct identity that in barter does exist between the alienation of one’s own and the acquisition of some other man’s product. To say that these two independent and antithetical acts have an intrinsic unity, are essentially one, is the same as to say that this intrinsic oneness expresses itself in an external antithesis. If the interval in time between the two complementary phases of the complete metamorphosis of a commodity become too great, if the split between the sale and the purchase become too pronounced, the intimate connexion between them, their oneness, asserts itself by producing — a crisis. The antithesis, use-value and value; the contradictions that private labour is bound to manifest itself as direct social labour, that a particularised concrete kind of labour has to pass for abstract human labour; the contradiction between the personification of objects and the representation of persons by things; all these antitheses and contradictions, which are immanent in commodities, assert themselves, and develop their modes of motion, in the antithetical phases of the metamorphosis of a commodity. These modes therefore imply the possibility, and no more than the possibility, of crises. The conversion of this mere possibility into a reality is the result of a long series of relations, that, from our present standpoint of simple circulation, have as yet no existence.” [20, ch. 2, sec. 2] The potential crisis is caused by the formation of gold hoards, gold which is withdrawn from circulation and saved. This interruption of the circuit by money lying idle means that goods can not be sold: ‘No one can sell unless some one else purchases’.

With credit the circuit is replaced from the standpoint of the seller with one of the form where is a financial asset: a bill of exchange, or a record of credit with a bank. If both the purchaser and the seller have financial assets this is the same as the old monetary circulation:

The financial asset has just changed places, but if we have purchase on credit we get:

Here the purchase is funded by the spontaneous creation of a financial asset/liability pair by the debt creation operation giving rise to and . Within this whole process real value is conserved, since the only real value entering was and leaves having merely changed owner whilst the liability and asset cancel: .

The ‘work’ done by credit is thus to allow the production and distribution of goods embodying real labour that could not otherwise occur given the private organisation of production. This is the free energy extracted by the increase in entropy of the financial system. Of course the financial system itself does not do any real work. The real additional physical work is done by the employees of companies who are net lenders. The ‘work’ done by by the credit system is social, it is work to overcome the potential barrier that private property would otherwise impose on the expansion of production.

Commodity exchange requires and exchange of equivalents. Where these equivalents are not in the hands of the purchasers, the financial system allows transfers that are in real terms non-equivalent exchanges, whilst creating instead a symbolic recompensation for the seller.

This symbolic recompensation in Euros or Dollars is a theoretical command over future labour. The borrower in this case is the real appropriator of the labour value embodied in the capital goods they acquire. The lender obtains merely a formal or symbolic appropriation of value.

Private ownership creates a potential barrier to the movement of goods which credit overcomes. The increasing entropy of the financial system reflects the ‘work’ that has been extracted in overcoming this barrier and is why it appears to ‘create wealth’. It allows the creation of wealth by labour whose expenditure would otherwise have been inhibited by the private organisation of the economy.

If one were to ask a banker what productive role they paid in the economy the answer would probably be in terms of the banks providing the finance that the economy needs.121212“Now let’s turn to the purpose of banks in a capitalist economy. Finance is an intermediary good: You cannot eat it, experience it, or physically use it. The purpose of finance is to support other activities in the economy. Banks are meant to allocate capital (funds) to the best possible use. In a capitalist economy, this means allocating money to the people or entities that will create the greatest wealth for the overall society. At the same time, risk management is supposedly a primary skill for bankers. When capital is allocated well and available to wealth creating entities, societies flourish. When capital is poorly allocated, economies can collapse.” [16] Money according to Adam Smith is the ability to command the labour of others.131313“Wealth, as Mr Hobbes says, is power. But the person who either acquires, or succeeds to a great fortune, does not necessarily acquire or succeed to any political power, either civil or military. His fortune may, perhaps, afford him the means of acquiring both; but the mere possession of that fortune does not necessarily convey to him either. The power which that possession immediately and directly conveys to him, is the power of purchasing a certain command over all the labour, or over all the produce of labour which is then in the market. His fortune is greater or less, precisely in proportion to the extent of this power, or to the quantity either of other men’s labour, or, what is the same thing, of the produce of other men’s labour, which it enables him to purchase or command.”[26, ch. 5]. The provision of credit gives a capitalist the authority or permission to commandeer part of the pool of social labour to his project.

In this sense the provision of a line of credit by a bank is like any other official act of giving permission. It is like for example a building control office issuing a permit allowing a house to be built. But the right to hand out such permissions does not make the person handing them out productive.

It is bricklayer’s and carpenters that actually produce the house, not the bureaucrat who signs it off. When such permissions are in demand, the official handing them out may ask for a cut: “You want to have this house built, you know your application might go much more smoothly were you to show your generosity in some way”. In an analogous fashion bankers ask for their cut: interest.

It may appear that a loan to a builder, unlike a building permit, actually gives the resources to build a house but this is an illusion generated by the legal relations underwhich it is done. The loan does not give the resources to proceed. The means are bricks and workers, the loan gives the right to command these, this is again the removal of a legal impediment in that a private citizen can not print their own money or issue generally acceptable credits to authorise the work, whilst banks, unlike other agents, can do this without legal impediment. The right to command labour is in the end a juridical relation, a more complex and indirect one than that given by a building warrant, but still ultimately a legal one backed in the end by the acceptance by the tax authorities of drafts on the private bank. The fact that the bank holds an account with the state bank is what ultimately gives the bank an ability to issue the authority to command labour. This is in the end a legal delegation of authority by the state.

At one time the charging of interest (usury) as regarded as the moral equivalent of an official taking a bribe. With the rise of bankers to political dominance, their very wealth, obtained in this way comes to be seen as a token of social respectability.141414“This disposition to admire, and almost to worship, the rich and the powerful, and to despise, or, at least, to neglect persons of poor and mean condition, though necessary both to establish and to maintain the distinction of ranks and the order of society, is, at the same time, the great and most universal cause of the corruption of our moral sentiments. That wealth and greatness are often regarded with the respect and admiration which are due only to wisdom and virtue; and that the contempt, of which vice and folly are the only proper objects, is often most unjustly bestowed upon poverty and weakness, has been the complaint of moralists in all ages.” [25, p. 53]

1.5 Contradiction between real and formal appropriation of value

Why do capitalists seek profits?

On the one hand it is something that is imposed by the nature of competition. Only profitable firms survive, the more profitable they are the more likely they are to survive, so a mechanism analogous to natural selection establishes the profit motive as the driving force of the system.

But there is another way of looking at this.

Whatever its historical form – gold, banknotes, bank accounts – money has been the power of command over labour. In all class societies, members of the upper class had been driven to increase their power over the labouring classes.

Slave owners tried to obtain as many slaves as they could. Feudal landowners sought to do this indirectly by building up their landed estates, since attached to the land were serfs. Capitalists do it by accumulating money. A billion Euros gives a capitalist command over about 100,000 person years of labour, say 2000 working lifetimes of indirect labour in commodities, perhaps twice that if they employ people directly. The more money you have, the more people are at your command.

Building up a bank balance gives you a symbolic command over lots of future labour but this is different from really having the product of this labour, as the fable of Midas long ago pointed out. By the nature of credit, a thrifty symbolic appropriator depends for his very existence on the spendthrift debtors.

The credit system socialises this dependence, makes it impersonal, so that money seems to simply represent abstract value, abstract command over labour. But the labour it is command over, is that of the debtor classes as a whole. The sub-prime crisis, like all credit crises, brings to the fore the fragile and mirage-like quality of this symbolic command, which can grow beyond any possibility of conversion into a real appropriation.

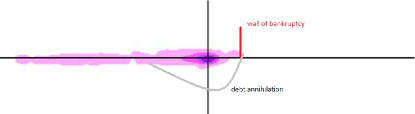

Think back to the phase diagram. The symbolic wealth of the rentier classes is the tadpoles tail. As it wiggles and extends, it drives the head towards the right towards the wall of bankruptcy (Figure 3). Hit the wall and the credit creation operator becomes its terrible twin the anihilation operator which cancels out the debt of the bankrupt at the same time as it wipes out the asset of the creditor.151515 We admit to ‘coquetting’ with Dirac in our terminology as Marx admitted to doing with Hegel.

2 Nonconservation laws of capital accumulation

If the characteristic or signature of commodity exchange, , implies a conservation law, then the signature of capital,

breaks that conservation as denotes an increase in the money above the initial sum spent on commodities in production . Marx famously attempted to explain how such expansion is possible [20, ch. 5-6]. It could not, he argued, come about in the sphere of commodity exchange, since this was governed by a law of conservation of values. Thus, he argued, profit could only be explained outside the realm of commodity exchange, by the extraction of surplus labour in the production process: Within capitalist firms – where Freedom, Equality and Bentham do not prevail – the working day is extended beyond the time required to produce the workers’ means of consumption, in order to provide a surplus that funds profits.

If one takes the aggregate of all capitalist firms, the signature of this process can be represented as

| (4) |

where represents the production process that generates a physical surplus product after the consumption of the present working population has been met. Moreover, through the compulsion of market dependency capitalist firms seek an indefinite expansion

by reinvesting the profit in greater productive capacity. This process is therefore governed by nonconservative laws of exponential growth. Relative growth rates are measured as per unit of time, i.e., , and a small change in such a rate may produce dramatic differences over time. For instance, if some quantity grows at 1% per annum it doubles in size approximately every 70 years. But if it grows at 10% per annum it doubles every 7 years.

As we show below, the nonconservative laws of capital accumulation interacts with systems outside the capitalist sector which provide it with labour, natural resources and the material conditions for habitability in general.

2.1 Profit rate constraints

Capitalist firms reinvest their profit – and rentiers finance expansion in various branches of production – based on the rate of return on the capital invested. Consider a firm earning annual profit flow of Euros per annum, before interest, rents and tax expenditure, with a stock of fixed capital Euros invested in the form of buildings, machines, equipment etc. The firm then earns an annual profit rate on its capital stock and the dimension of this rate is . If new investment in the firm is to be attractive, the profit rate should exceed the real interest rate or else it would be more profitable to simply earn interest on saved profits.161616As pointed out by Marx and Keynes [23].

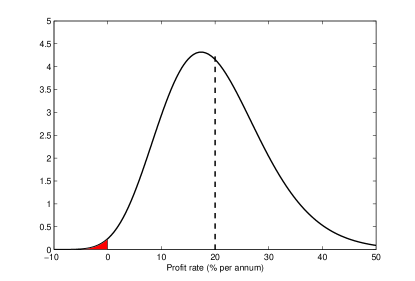

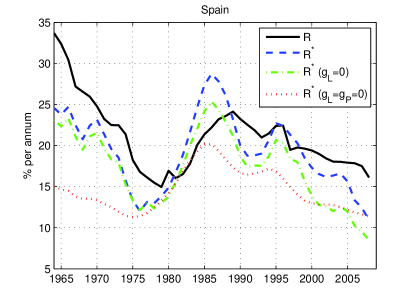

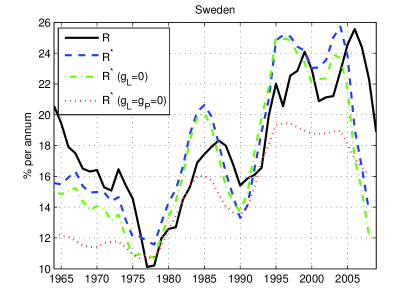

Next, consider the aggregate of all capitalist firms in the economy. The total capital stock invested earns different rates of profit in various firms and branches as illustrated in Figure 4.

Due to varying technical conditions in production and the random churning of the market, the distribution will always be dispersed. The process of financial polarisation of capital into net creditors and debtors, described in the previous section, will also increase the dispersion of profit rates after net interest payments. Firms with higher levels of net debt will have lower retained profit rates, whereas firms accumulating credit accounts experience higher retained profit rates.

Further, as (4) signifies, the aggregate profit flow is predicated on the production of a surplus product of commodities which requires an annual flow of labour expended in production,

| (5) |

On the basis of the Law of Large Numbers it can then be shown that average profit rate over all capital invested, denoted , is well approximated by

| (6) |

where denotes aggregate labour expended per unit of time, denotes the labour time required to reproduce the total capital stock, and is the fraction of surplus labour-time performed above the consumption of the workforce [11].

The significance of the average profit rate is that it constrains the entire distribution of profit rates in the capitalist sector as illustrated in Figure 5. Further, it sets the upper limit to the growth rate of the total capital stock. The average profit rate rises when the amount of labour expended grows faster than the labour-value of the total capital stock, and vice versa.

The amount of labour time required to reproduce the capital stock, , is lowered by productivity growth and the rate of depreciation , but rises as the surplus product assumes the form of capital goods invested in production. Based on this insight it is possible to derive a dynamic equilibrium of the average profit rate,

| (7) |

where denotes the relative growth rate of labour expended and the ratio of aggregate gross investments to total profits.171717The derivation is based on computing the relative growth , and solving for when , cf. [34, 6]. In words, the evolution of the average profit rate is constrained by the balance between the proportion of profit that is reinvested, on the one hand, and depreciation, productivity growth and the growth of labour, on the other.

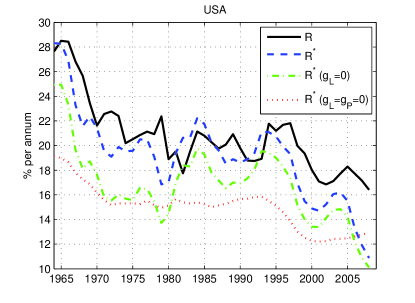

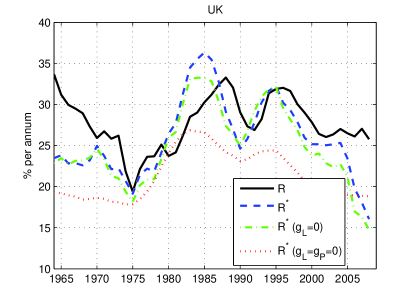

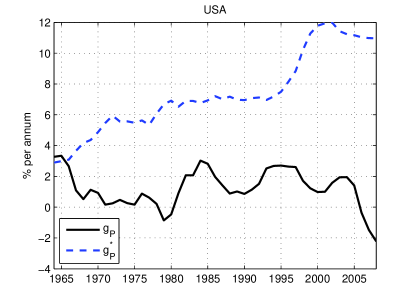

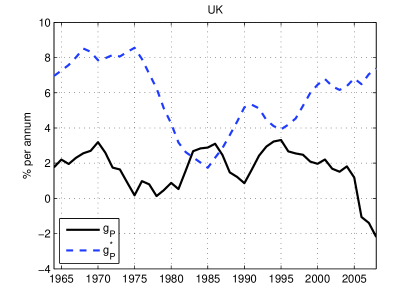

For sake of illustration, suppose the expenditure of labour and productivity in the capitalist sector grows by 2% per annum and 3% per annum, respectively. If the aggregate depreciation rate is 10% per annum and the ratio of investments to profits is 0.60, then the average profit rate is inexorably driven to 25% per annum, irrespective of the distribution between profits and wages! Figure 6 shows how the trajectory of the average profit rate in the USA and UK have been constrained by the equilibrium profit rate.

2.2 Resource constraints

The signature of capital (4) illustrates that the capitalist sector is dependent on an element produced outside its units of production, namely the capacity to work, which provides a flow of labour, , into the production process. But there are more such elements. In fact, the process involves an annual flow of any natural resource expended in production,

| (8) |

This includes important inputs such as oil, scarce minerals and arable land. Let denote the growth rate of expenditure and denote the rate of regeneration, both relative to the stock of a particular natural resource. Then is the relative depletion rate of the stock of that resource. Provided the depletion rate is not too rapid, alternative inputs and technologies can be found; otherwise the rising scarcity of resource deposits require increasing inputs of labour in extraction per unit, which lowers productivity of labour . It may also require a higher fraction of profits reinvested in fixed capital to sustain such extraction. From (7) we see that such pattern of development would lower the equilibrium profit rate.

2.3 Emission constraints

Finally, the capitalist sector does not only absorb labour and natural resources from outside, but produces emissions that deteriorate the conditions for habitability. For an annual flow of any particular emission from production, we can illustrate this as

| (9) |

The most critical emission is greenhouse gases, in particular carbondioxide . Let denote the growth rate and denote the rate of absorption of the emission, both relative to the stock of accumulated emissions. When the relative emission rate, , is positive, the pollution level is rising. This acts negatively on the productivity of labour in the agricultural sector, which again would lower the equilibrium profit rate (7). Furthermore, for a given living standard, it would necessitate an increasing share of labour expended in the production of wage-goods consumed by the population as well as in pollution management. Such a pattern of development would reduce the relative surplus appropriated by the capitalist classes.

2.4 Contradictions of exponential accumulation

In summary, the competitive dynamics arising from capitalist property relations subject the firms to the compulsion of exponential accumulation. The capitalist sector as a whole is thus geared towards an indefinite accumulation of resources – natural and human – in the form of productive assets and commodities. With finite resources the exponential growth path must continuously hit constraints that need to be overcome for further accumulation. To an individual rentier such constraints may appear irrelevant; indeed there is no tangible resource limit to continuously growing profit income in the form of increasing symbols in a bank account or on paper bills. These symbols, however, command real material resources embodied in goods and services.

In the world-historic conjuncture of the twenty-first century each constraint – labour , natural resources and emissions – presents obstacles on a scale that cannot be circumvented by the private capitalist sector alone but would ultimately require massive state intervention and an increasing public appropriation of the social surplus.

First, as the length of the working day can only be extended to a certain limit, exponential growth of labour time expended in the capitalist sector is ultimately constrained by demographic factors. Once labour reserves from the countryside have been absorbed, the growth rate is ultimately set by the rate of population growth. Further, as societies industrialise the net cost of rearing children brings the natural population growth rate close to zero, and is compensated only by net immigration in certain countries. In the advanced capitalist world as a whole the growth rate of employment was hovering just below 1% per annum, prior to the recent crisis. The trend in East Asia was similar, just above 1% per annum.181818The crisis has of course brought down the growth rate even further, cf. [14]. Southern Asia, the Middle East and Northern Africa will experience the same trend if the regions follow the path of industrialisation and urbanisation.

The equilibrium profit rate (7) tells us that the growth of labour therefore ceases to be a source of profitability, it is rather the specific balance of investments and productivity growth that can sustain conditions for average profitability in the capitalist sector. This depends on the specific technological phase of an economy and its institutional structure of investments. If the technological conditions are not favourable, the capitalist class is better off dissipating a greater fraction of the surplus product in the form of luxury consumption rather than reinvesting profits in the productive capital stock. Only public enterprises that operate according to break-even criteria, rather than rate of return on capital investment, will undertake large-scale investments under such conditions. Short of such commitments by the state under rentier-dominated capitalism, the unproductive pattern has sustained mass unemployment in the advance capitalist countries since the 1980s [27].

Second, the competitive and anarchic dynamics of the capitalist sector inexorably drive firms to exploit energy sources and materials that can satisfy the compulsion of exponential accumulation; if only over a short time horizon. The early capitalist factory system that arose in England was initially powered by water. But the supply of labour was concentrated in populous towns; hence factories that employed more mobile steam-engines could establish there and get a competive edge. Unlike the water wheel, steam-engines were powered by a scarce fossil fuel: coal. This was the genesis of fossil fuels as the primary source of energy in capitalism [18]. Further, exponential accumulation must be met by exponential consumption for profits to be realised. This does not only increase the scale of material inputs but also reduces arable land and fresh water supplies.

Misallocation of critical scarce resources through the market mechanism can thus only be counteracted by state intervention to bring down the depletion rates to viable levels, i.e., imposing quotas and a controlled scale of extraction. Further the composition of consumption among higher-income populations would need to be steered away from material goods and towards sustainable services, including socialised forms of consumption. Public taxation as well as lower workhours provide mechanisms for changing consumption patterns.

Third, emissions of greenhouse gases impose serious risks of deteriorating the viability of the global capitalist economy. Under current global emission trends the average world temperature will increase beyond +2 degrees Celsius by the year 2050, and rapidly approaching +4∘C. The effects of such climatic changes are an increased frequency of heat waves; decline in crop yields; exacerbated water scarcity; high-intensity tropical cyclones; and irreversible loss of biodiversity with unpredictable effects on human life [30]. All of which undermine the reproduction of the source of value – the workforce.

The bulk of emissions in the global economy, about one quarter, arises in electricity and heat, followed by industry, transport and agriculture. Deforestation further exacerbates this by reducing the absorption rate [13]. Reducing per capita emissions at a sufficient rate to counteract global warming requires large-scale investments in power generation and an energy-efficient transformation of the assets in production, transport and housing. This is well beyond the what private research and development in the capitalist sector can commit to alone. As the material conditions deteriorate, a coordinated effort by states akin to wartime planning will become increasingly necessary to sustain a viable productive sector and workforce.

3 Contradictions between laws of market exchange and capital accumulation

We now consider the dynamics that arise from the interaction between the conservative laws of market exchange and the nonconservative laws of capital accumulation.

3.1 Value conservation and the signature of capital

Marx only partly answered the problem of “where the money comes from” in the process . He explained how capitalists obtained a net income from their capital, but this was only half the problem. If the capitalists follow the maxim ascribed to them by Marx – “Accumulate, accumulate! That is Moses and the prophets!” – then the signature of capital extends into

which requires exponential growth in the quantity of money. In the 19th century, the British economy, like most others, depended on precious metal for its monetary base. An exponential growth in the quantity of money implies the same sort of growth for gold stock. But if we look at historical data for the growth of the world gold stock, we find that during the 19th century it was growing at well under 1% per annum. Given that the British economy grew at over 2% a year, there was a discrepancy between the growth of gold and the growth of commodity circulation.

| Stock | Annual growth | |

|---|---|---|

| Period | (million troy oz.) | (percent) |

| 1840–1850 | 617.9 | |

| 1851–1875 | 771.9 | |

| 1876–1900 | 953.9 | |

| 1901–1925 | 1430.9 | |

| 1926–1950 | 2130.9 | |

| 1951–1975 | 3115.9 | |

| 1976–2000 | 4569.9 |

Since gold stocks could not grow fast enough to support the expansion of the economy, capitalists had to resort to commercial bills. An Iron Master taking delivery of coal would typically write a bill of exchange, a private certificate of debt, promising to pay within 30 or 90 days.

Payment of wages would generally have to be done in cash. Capitalists have tried at times to pay wages in tokens redeemable only at company stores (‘scrip’) but legislation by the state, eager to maintain its monopoly of coinage if not to defend the interests if the workers, tended to put a stop to this. Payment in cash represents a transfer from the safes of capitalists to the pockets of their employees, with a corresponding cancellation of wage debts. At the end of the week, the wage debt has been cleared to zero, and there has been an equal and compensating movement of cash.

Workers then spend their wages on consumer goods. For the sake of simplicity, assume that there is no net saving by workers so that in the course of the week all of the money they have been paid is spent. This implies that immediately after pay-day, the money holdings of the workers are equal to one week’s wages. If these wages were paid in coin this would have set a lower limit to the quantity of coin required for the economy to function.

When workers spend their wages on consumer goods they transfer money only to those firms who sell consumer goods – shopkeepers, inn-keepers and so on. We can expect these firms not only to make up the money they had paid out in wages, but to retain a considerable surplus. The final sellers of consumer goods will thus end up with more money than they paid out in wages. From this extra cash they can afford to redeem the bills of exchange that they issued to their suppliers.

In the absence of bank credit, suppliers of manufactured consumer goods would be entirely dependent for cash on money arriving when the bills of exchange, in which they had initially been paid, were eventually redeemed by shopkeepers and merchants. The payment situation facing raw materials firms was even more indirect: they could not be paid unless the manufacturers had sufficient cash to redeem bills of exchange issued for yarn, coal, grain, etc.

The process of trade between capitalists leads to the build-up of inter-firm debt. We suggest that the total volume of inter-firm debt that could be stably supported would have been some multiple of the coinage available, after allowing for that required to pay wages. If one takes the aggregate of all firms the ideal signature of this process can be represented as:

where represents the production process that generates a physical surplus of commodities after the consumption needs of the present working population has been met. If there is no new issue of coin by the state then the cannot be ‘real money’; rather, it must be in the form of bills of exchange and other inter-firm credit.

For the capitalist class considered as a whole this should not be a problem since the is secured against the accumulated commodity surplus . There is a net accumulation of value as commodities, and accounting practice allows both the debts owed to a firm and stocks of commodities on hand to be included in the value of its notional capital. As the process of accumulation proceeds in this way the ratio of commercial debt to real money will rise. If the period for which commercial credit is extended remains fixed – say at 90 days – then a growing number of debts will be falling due each day. If these have to be paid off in money, then a growing number of firms will have difficulty meeting their debts in cash.

The basic contradiction between capital’s exponentially growing need for money and the much slower growth of gold production led to a series of transformations of the monetary system during the 19th and 20th centuries.191919“One of the principal costs of circulation is money itself, being value in itself. It is economised through credit in three ways. A. By dropping away entirely in a great many transactions. B. By the accelerated circulation of the circulating medium. … On the one hand, the acceleration is technical; i.e., with the same magnitude and number of actual turnovers of commodities for consumption, a smaller quantity of money or money tokens performs the same service. This is bound up with the technique of banking. On the other hand, credit accelerates the velocity of the metamorphoses of commodities and thereby the velocity of money circulation. C. Substitution of paper for gold money.” [21, ch. 27]

-

1.

Gold was supplemented by commercial credit. This displaced gold from transactions between capitalists.

-

2.

Commercial credit was supplemented by the discounting of bills of exchange by the banks.

-

3.

Payment in bills of exchange was largely replaced by payments by cheque and commercial credit by bank credit.

-

4.

Gold coins were withdrawn from circulation to be replaced by banknotes with gold only used in settlements between international banks. This meant that wage payments no longer depended on precious metal.

-

5.

National currencies were then completely removed from the gold standard, and state notes became the base money. This was completed by the withdrawal of the dollar from the gold standard in the 1970s.

-

6.

With the development of computerisation in the third quarter of the 20th century it became practical to pay wages directly into bank accounts. This meant that state base money circulating could be substantially less than the monthly or weekly wage bill.

-

7.

Finally with the general issue of credit cards, the credit system spread from the capitalist class to all classes in society.

When money was still gold, this gold was value – it was embodied labour and had a value internationally because in all countries the production of gold required a great deal of labour. With the modern system of national and supernational currencies money is no longer value. No significant work goes into the printing of 100 Euro notes. Why then can they function the same way that gold used to?

Central bank notes used to be issued under the gold standard, but these were just tokens for gold, and could be redemed for bullion on demand at the central bank. There is no promise by the ECB to redeem Euros to gold at any fixed exchange rate.202020Though collectively the central banks of the Euro area held over 430 billion Euros in gold reserves. These can potentially be used in settlement with other central banks to settle foreign trade debts, but in practice there is little or no intervention by the ECB using gold to support the value of the Euro. Since there is no definite link between the Euro and gold or between the Pound and gold, how can these currencies function as a measure of value and medium of exchange?

Why are they worth anything?

Well for one thing they are legal tender, but what does this mean and why is it important?

Throughout the Eurozone the following is held to apply in cases where a payment obligation exists:

• Mandatory acceptance of Euro cash; a means of payment with legal tender status cannot be refused by the creditor of a payment obligation, unless the parties have agreed on other means of payment

• Acceptance at full face value; the monetary value of a means of payment with legal tender status is equal to the amount indicated on the means of payment

• Power to discharge from payment obligations; a debtor can discharge himself from a payment obligation by transferring a means of payment with legal tender status to the creditor. [1]

The circulation of the Euro is legally enforced in the relationship between shops and customers, but between businesses they can in principle both agree to settle obligations in something other than Euros. But with retail commerce and all taxes payable in Euros, its circulation is effectively enforced.

But there is a difference between the previous generation of state monies like the Franc or D-mark and the Euro. The previous generation fell into the general category of state token monies. This is a very old category of money [15, 17, 31]. Precious metal money was prevalent in early modern Europe. But in China the monetary system was from a much earlier stage based either on copper tokens or on paper notes [28, 29] and it is arguable that for much of the Roman Empire the Denarius was little more than a copper token with merely a symbolic coating of silver [4]. In such a system the circulation of money goes illustrated in table 2.

| State | Pay | Lackeys | Purchases | Producers | Tax | State | |

| Emperor/ | Emperor/ | ||||||

| King | Soldiers | Artisans | King | ||||

| Bureacrats | Peasants | ||||||

The empire or state imposes the circulation of its token currency by obliging the producers to pay taxes in money. Since the producers must ‘render unto Ceasar’, they are forced to sell their product to the employees of Ceasar. The state creates money tokens with which it pays its employees. The state employees willingly work for the state in return for these tokens knowing that these tokens will enable them to command the labour of others in their turn. The state thus breaks down the self-sufficient or barter economies of the countryside and enforces the spread of commodity exchange. Forestater gives a dramatic account of how this process was enforced in the British Empire [12].

In a pre-monetary tax system, the tax is levied in the form of a direct duty on the population to work for or deliver goods to the state. In this case the real appropriation of labour by the state is directly visible. In a monetary tax system with token money the real appropriation of surplus labour occurs when soldiers and other state employees deliver goods and services to the Emperor. There is a distinct formal or symbolic appropriation when the taxes are levied on the producers. This is similar to the relationship that we previously analysed between formal and symbolic appropriation in the credit system, but with this difference: the formal transfer in the tax system has no pretence of equivalence.

The value of a state token money is based on something historically prior to commodity production, something that goes right back to the earliest state forms: the power of the state to command the labour of its inhabitants. The value of the Swedish Krona is set by the fact that the Swedish state (Crown) directly or indirectly appropriates more than half the labour in the Kingdom.212121This is a slight simplification, public expenditure is over 53% of GNP, but a part of that is indirect appropriation of labour as social protection, where individual citizens are paid social benefits in Krona. The sum in Krona paid out for that directly social labour has its value set by this labour that the Crown directly commands. This rate of exchange between royal tokens and labour sets the monetary equivalent of labour time in Sweden, which then operates via the medium of commodity trade within the remaining private part of the economy. The direct royal command over the labour of his subjects is then symbolically appropriated by the capitalist class in the form of Krona credits in the Svenska Handelsbanken, etc. to give them command over the privately employed working class.

For a monetary system like this to work, you need a clearly defined and controlled territory of the empire, an efficient tax system, and a state that commands a substantial portion of the total labour of society. And that state has to have the sovereign right to issue its own currency. These conditions are not met in the Eurozone.

3.2 Formation of interest

The formation of credit and debt relations in the capitalist sector demands further an analysis of the formation of interest in the banking system. The specific feature of this system is deposit taking.

A deposit-taking banker is in a perilous position since he accepts cash over and above his own capital which he then lends out. Because he has lent out cash that was not his own capital, and is under an obligation to encash deposits on demand (or after some fixed warning period), he can easily become insolvent. The remaining cash he holds in his safe is never enough to meet his maximum obligation to his creditors. Should the day dawn on which too many of them demand their money back, he is lost.

Suppose we model this as a stream of customers arriving at the banker’s till at random intervals. Each customer either makes a deposit or a withdrawal. The customers may make a withdrawal of any amount up to their current credit balance. We further assume that in a steady state customers are as likely to make a deposit as to make a withdrawal. Then the more customers that a bank has, the smaller will be the proportional variation in the withdrawals from day to day.

As the number of customers rises, the variation in the amount withdrawn in any week falls, and so too does the maximum withdrawal that can be expected. A very small bank would have to keep all its deposits in the safe as an insurance against having to pay them out, but a bank with 20,000 customers might never see more than a few percent of its cash deposits withdrawn in any week. A bank with that number of customers could safely issue as loans several times as much in paper banknotes as the coin that it held in its vaults, safe in the knowledge that the probability of it ever having to pay out that much in one day was vanishingly small. Thus with a starting capital of 10 million the bank could lend out 200 million after building up its network of customers. This creation of new paper money by the banks was the hidden secret behind the signature of capital.

The cost to a bank of making a loan is related to the likelihood that the reserves left after the loan will be too small to cover fluctuating withdrawals. If this happens the bank may lose its capital.

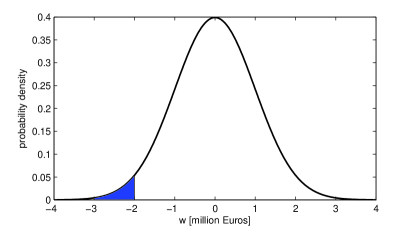

Let denote the maximal excursion of reserves from their mean position during a year, due to random deposits and withdrawals by customers. Let us assume that follows a Gaussian distribution, with a standard deviation of 1 million Euros. Suppose that the banker had a capital of 5,000,000 and that he would lose his capital if the bank failed. Then, if he started with reserves of 3 million, making a loan of 1 million would reduce the reserves to 2 million and the loan would have an expected cost of , where is the probability that the withdrawals exceed the resulting reserve level after the loan.222222In other words, for a zero-mean Gaussian variable with standard deviation . Figure 7 illustrates this.

This amounts to an expected cost of about 107,000, which sets a lower limit on the interest it would be rational for the banker to charge for the loan, namely 10.7% in this case.

Different banks will charge different rates of interest, but through the pressures of bankruptcies the lower safety rate is likely to emerge from capitalist banking practices. As the ratio of reserves to deposits fall, this pressure would be reflected in higher interest rates. There would thus be an inverse relationship between the reserve to deposit ratio and the interest rate.

At the birth of the banking system the reserves of the private banks were in bullion. Now the reserves are in the form of credit accounts with the state bank. These come into existence when the state pays people for services rendered, or makes state grants. One of the authors recalls that his student grant, and payments for attending Research Council meetings were in the form of bits of paper that looked like cheques but instead of being drawn on a bank, they were drafts made out on ‘The Queen and Lord Treasurer’s Remembrancer’. Private banks can present these government drafts to the Bank of England, and have their account with the Bank of England credited by a like amount.

The other side of the coin is when a citizen pays taxes to the Exchequer using a cheque drawn on a commercial Bank. The Exchequer then passes these to the Bank of England which writes down the credit account of the relevant commercial bank.

If are the reserves of the private banking system, it follows that where is government payments, are tax payments and is the sale of government securities, all per unit time. Sales of government securities obviously reduce the monetary reserves of the private banking system.

By adjusting its sales of securities, the state can manipulate the reserves of the private banking system and thus control the rate of interest. In a state with its own central bank, it is an illusion to think that the government is at the mercy of the ‘money market’ when selling these securities. A state where , i.e., one with a budget deficit can if it wishes simply refrain from selling securities for a while and in due course the growth of the reserves of the private banks will force a fall in the market interest rate. In the end, the private banks are forced to buy government debt. Any reserves exceeding the level required for the safety of their loans to the private sector are simply dead assets, yielding no income. The only way for the banking system as a whole to get income from these assets is to buy government securities.

If the state bank wishes, it can buy back government securities from the private banks forcing the interest rate down even faster. This is the mechanism by which so-called Quantitative Easing reduces the interest rate.

3.3 Dynamics of sector balances

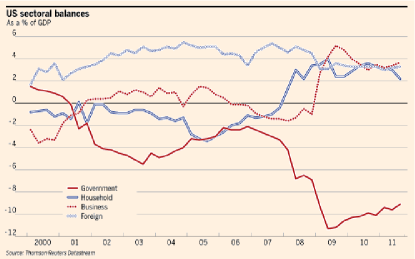

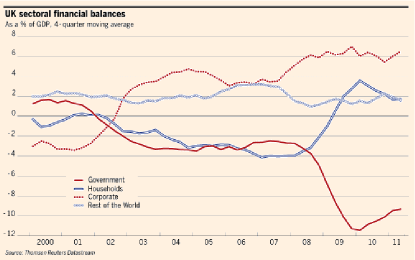

The reader may recall equation (2) showed that the sum of borrowing and lending have to balance. That equation was defined over all agents, but it also applies if, instead of agents, we consider economic sectors: households, non-financial companies, banks, the state, and the ‘rest of the world’. Figure 8 illustrates these sector balances for the USA and UK. In Table 3 we present such data for the Eurozone.

Now the sum of the sectoral balances have to equal 0. Look at the business sector you can see that, as for most years, this sector was running a financial surplus. This surplus was only possible because of the deficits, i.e., borrowing, by the household and state sectors. After the sub-prime mortgage crisis lending to working-class and middle-class borrowers became much more restrictive and the household sector became net lenders. This does not mean that the working class became net lenders of course, it is just that the propertied and working classes are aggregated in the household sector statistics. Once working-class borrowing fell, then the saving by the propertied classes became the dominant factor in the household sector. This constrains the market for consumer goods producing the recession.

The balances make it clear that the business sector can only run a financial surplus if other sectors run a deficit, and given the poor competitive position of US and UK manufacturing the rest of the world is not going to run a deficit with them. That leaves only the household or the state as possible absorbers of the financial surplus of the corporate sector.

The limitation of the financial system to support borrowing in 2008 had in the short term little to do with profitability of industry, as it was lending to working class households not to industry. Their ability to borrow was constrained by low wages. The repackaging of mortgages hid the fact that a large portion of working class borrowers were bound to default on their loans, but it could only hide it for a while, eventually the poverty of the working class borrowers became the determining factor. In longer term though one has to ask why the corporate sector ran a financial surplus? In other words, saving a portion of its profit income rather than reinvesting?

The share of profits expended as net investments has rarely exceeded 25% in the advanced economies, since the post-WWII boom [19]. We would argue that this is a structural feature of a modern capitalist economy. As the demographic transition is completed and production technologies mature, the growth rates of labour, , and productivity, , become moderated. Then it becomes increasingly difficult to maintain average profitability when firms are reinvesting a large portion of their retained profits, as seen in equation (7). Fig. 9 illustrates the productivity growth required to sustain average profitability at the post-WWII boom levels, under the actual demographic and investment trends. Short of such such spectacular growth rates, rapid capital accumulation is unsustainable in the capitalist sector and a substantial portion of profits will instead be accumulated as financial surpluses and spent on luxury consumption.

4 The crisis in the Eurozone

From the standpoint of exchange being a conservative system, the exponential growth of value implied by compound interest has to be a temporary disequilibrium phenomenon – tied to an exponential growth in whatever is the source of value. If the expenditure of human energy is the source, then the accumulation of capital value must depend on a similar exponential growth of the working population.

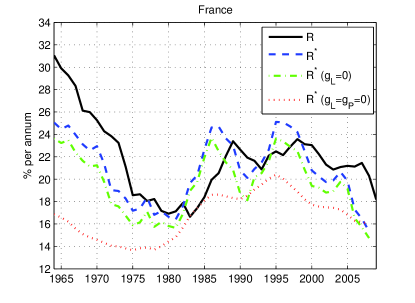

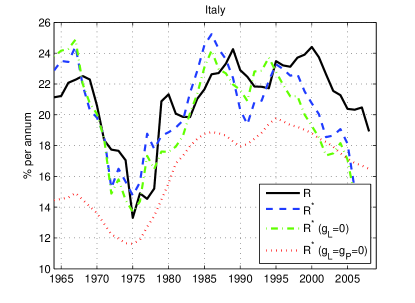

We know that historically the process of industrialisation has combined rapid accumulations of capital values with an exponential growth in the working population. But we also know that societies undergo a demographic transition once they have developed further – with a shift to zero or negative rates of natural population growth. As we have argued above, the end to population growth is bound eventually to make the productive expansion of capitalism unviable. Figure 10 illustrates the trajectories of the average profit rates, and their determinants, in the advanced economies of Western Europe.

If we look at Western Europe and Japan, the natural rate of population growth is very low. In the face of this constraint we see a set of displacement processes:

-

1.

Pressure of immigration from areas of high birth rate. On the one hand this is what one would expect simply as a diffusion process, but there is also political ‘pressure’ by capitalists interests to reduce barriers to movement of labour in order to allow continued capital growth.

-

2.

As it becomes harder to reinvest profits in new labour employing activities, there is an increasing dislocation between the apparent accumulation of capital in financial instruments and the reality, in which the surplus product is actually being socially used by the state.

There is a fundamental conflict between the attempt to maintain a mechanism of symbolic appropriation of the surplus by private owners and the European demographic conditions which mean that little real accumulation is now possible in the private sector. The greater part of the social surplus product now has really to be appropriated by the state as representative of society. The continuation of a private claim on this surplus becomes actually infeasible. The conflict between an exponential growth of financial claims and a stagnant population upon whom those claims rest arguably lies at the heart of the ‘Euro Crisis’.

4.1 Greek debt

For example we know that the Greek trade deficit with Germany and the German trade surplus with Greece must sum to zero. It is impossible to reduce one without reducing the other. If austerity in Greece reduces their deficit with Germany, there must be a reduction in German exports. If the objective is to reduce the trade imbalance between Germany and Southern Europe, it would be better to give Germans longer and better paid holidays so that they could spend more on Mediteranean holidays rather than impoverishing both sides.

It is also helpful to look at the problem of state debts this way. If at the end of a period the state is to reduce its liabilities and improve its net worth, this necessarily implies a reduction in the assets held by the state’s creditors. How to reduce state debt and how to impoverish the holders of state debt are one and the same problem. In this light, a choice of options become visible

-

•

debts can simply be repudiated,

-

•

inflation can be engineered to reduce the real value of the debt,

-

•

firms and individuals holding state bonds can be relieved of them by the taxman,

In contrast to these direct measures, austerity imposed on the non-bondholding classes, is much less effective. Since liabilities between sectors of an economy must sum to zero, taxing those too poor to save will only reduce state debt to the extent that the poor are driven to take out increased personal loans. The increase in the liabilities of the poor then compensates for the fall in state debt. The poor, however, are not very credit worthy as the sub-prime mortgage collapse showed.

4.2 The Stability Pact

The key measures to solve the Euro crisis according to the treaty recently adopted by most of the EU are to establish a balanced budget or a budget surplus for the state sector.

BEARING IN MIND that the need for governments to maintain sound and sustainable public finances and to prevent a general government deficit becoming excessive is of essential importance to safeguard the stability of the euro area as a whole, and accordingly, requires the introduction of specific rules, including a ‘balanced budget rule’ and an automatic mechanism to take corrective action; [2, p.2]

The Contracting Parties shall apply the rules set out in this paragraph in addition and without prejudice to their obligations under European Union law: (a) the budgetary position of the general government of a Contracting Party shall be balanced or in surplus; [2, article 3]

The drafters of this treaty imagine that it is possible, by an act of international law to impose a unilateral constraint on one item in a mutually dependent complex of relations. The surplus or deficit position of the government sector in the Eurozone depends upon the net positions of all other sectors.