Birth-death processes

Abstract

Many important stochastic counting models can be written as general birth-death processes (BDPs). BDPs are continuous-time Markov chains on the non-negative integers in which only jumps to adjacent states are allowed. BDPs can be used to easily parameterize a rich variety of probability distributions on the non-negative integers, and straightforward conditions guarantee that these distributions are proper. BDPs also provide a mechanistic interpretation – birth and death of actual particles or organisms – that has proven useful in evolution, ecology, physics, and chemistry. Although the theoretical properties of general BDPs are well understood, traditionally statistical work on BDPs has been limited to the simple linear (Kendall) process, which arises in ecology and evolutionary applications. Aside from a few simple cases, it remains impossible to find analytic expressions for the likelihood of a discretely-observed BDP, and computational difficulties have hindered development of tools for statistical inference. But the gap between BDP theory and practical methods for estimation has narrowed in recent years. There are now robust methods for evaluating likelihoods for realizations of BDPs: finite-time transition, first passage, equilibrium probabilities, and distributions of summary statistics that arise commonly in applications. Recent work has also exploited the connection between continuously- and discretely-observed BDPs to derive EM algorithms for maximum likelihood estimation. Likelihood-based inference for previously intractable BDPs is much easier than previously thought and regression approaches analogous to Poisson regression are straightforward to derive. In this review, we outline the basic mathematical theory for BDPs and demonstrate new tools for statistical inference using data from BDPs. We give six examples of BDPs and derive EM algorithms to fit their parameters by maximum likelihood. We show how to compute the distribution of integral summary statistics and give an example application to the total cost of an epidemic. Finally, we suggest future directions for innovation in this important class of stochastic processes.

1 Introduction

Birth-death processes (BDPs) are a flexible class of continuous-time Markov chains that model the number of “particles” in a system, where each particle can “give birth” to another particle or “die” (Feller, 1971; Karlin and Taylor, 1975). The rate of births and deaths at any given time depends on how many extant particles there are. When there are particles, a birth occurs with instantaneous rate and a death with instantaneous rate . In the classical “simple linear” BDP, and so that per-particle birth and death rates remain constant. In a “general” BDP, and can be any function of but are time-homogeneous (Kendall, 1948, 1949). Table 1 gives examples of well-known BDPs and their birth and death rates. Figure 1 shows an example realization from a BDP.

The usefulness of BDPs lies in the fact that “particle” can refer to a member of any discrete potentially interacting system in which one only keeps track of the number of objects in existence. BDPs are popular modeling tools in evolution, population biology, genetics, and ecology (Novozhilov et al, 2006). For example, if we interpret the particles as species in a macro-evolutionary setting, BDPs can be used to study speciation and extinction over evolutionary timescales (Nee et al, 1994; Nee, 2006). BDPs can also be used to study infectious disease dynamics in a finite population, where the number of individuals infected is the quantity of interest (Bailey, 1964; Andersson and Britton, 2000). In molecular evolution, BDPs can model inserted and deleted nucleotides in a DNA or RNA sequence as part of a probabilistic alignment method (Thorne et al, 1991; Holmes and Bruno, 2001), mobile/transposable genetic elements (Rosenberg et al, 2003), gene families (Demuth et al, 2006), or even whole chromosomes (Mayrose et al, 2010). BDPs can model populations of organisms in a resource-limited environment (Tan and Piantadosi, 1991; Renshaw, 1993, 2011). In finite populations, BDPs are commonly used to model quantities of interest in an evolutionary setting, such as allele frequencies, selection, or coalescence (Moran, 1958; Krone and Neuhauser, 1997; Kingman, 1982).

Many important models in queuing theory can be written as general BDPs (Ross, 1995; Norris, 1998; Renshaw, 2011). In basic Markovian queues, customers arrive into a queue or buffer as a Poisson process with rate , and waiting customers are served (removed from the queue) with per-customer service rate . In the queue, also known as the immigration-death process, there are infinitely many servers, so the arrival and service (birth and death) rates are and for . In the queue, also known as the immigration-emigration model, there is only a single server, so the rates are and . In the queue, there are exactly servers, so .

BDPs can also be useful for defining arbitrary probability distributions on the non-negative integers. Crawford and Zelterman (2013) demonstrate that any sum of exchangeable Bernoulli random variables can be exactly represented as a pure-birth BDP. In fact, Faddy (1997) shows that one can define a pure birth process (a BDP with death rates for all ) whose transition probabilities reproduce any discrete distribution on the counting numbers. Klar et al (2010) establish a correspondence between several power law distributions and the long-time limit of specially constructed BDPs, providing a time-dependent interpretation that may be useful for modelling mechanistic processes that give rise to power law outcomes. Crawford and Suchard (2012) define a BDP to mimic a process of frameshift-aware insertions and deletions in DNA sequences. Lee et al (2011) set the birth and death rates of a BDP to exhibit over-dispersion relative to the Poisson distribution, and Crawford et al (2014b) define a BDP to model rounding in counts of sex partners to multiples of 5, 10, 25, or 50 in self-reported counts of sex partners in a public health study.

There is a rich history of theoretical research into the properties of BDPs. Kendall (1948, 1949) introduce the process with constant per-particle birth and death rates and finds the transition probabilities by a generating function argument. In their groundbreaking series of papers, Karlin and McGregor analyze properties of BDPs, including stationary distributions, moments, transition probabilities, recurrence and passage times, and other quantities of interest (Karlin and McGregor, 1957b, a). They also explore in-depth applications of this theory to BDPs whose rates depend linearly on (Karlin and McGregor, 1958a), and queuing processes (Karlin and McGregor, 1958b).

Beyond the work of Karlin and McGregor, many authors have discovered extensions and deeper interpretations for the theoretical properties of BDPs. For example, the theory of BDPs is intimately related to properties of continued fractions (Guillemin and Pinchon, 1999). Flajolet and Guillemin (2000) elucidate the relationship between sample trajectories (or state paths) of a BDP and lattice path combinatorics via continued fractions and develop expressions for a variety of recurrence and passage time variables in terms of continued fractions. Lenin and Parthasarathy (2000) and Parthasarathy et al (1998) discuss further some well-known continued fractions whose connection to BDPs previously went unappreciated.

| Model | ||

|---|---|---|

| Poisson | 0 | |

| Yule/Pure birth | 0 | |

| Survival/Pure death | 0 | |

| Kendall | ||

| Kendall immigration | ||

| queue | ||

| queue | ||

| queue | ||

| SI/Logistic | 0 | |

| SIS | ||

| Moran/Ehrenfest |

The study of BDPs has benefited from wide interest in the theoretical properties of this class of processes. But their usefulness as flexible tools for statistical inference has been under-appreciated. In this review, we outline basic properties of BDPs and show how to perform principled statistical inference using data from continuous and discrete observation of BDPs. First, we present the basic time-evolution equations of general BDPs, derive the transition probabilities for the Kendall process (Feller, 1971; Kendall, 1948), and describe the analytic theory developed by Karlin and McGregor (1957b, a) for general BDPs. Then we outline a computational strategy for evaluating BDP transition probabilities using a continued fraction representation of their Laplace transform, which allows routine computation of likelihoods for discretely observed processes (Crawford and Suchard, 2012). We describe a generic class of EM algorithms for maximum likelihood (or maximum a posteriori) inference for discretely observed BDPs (Crawford et al, 2014a). Finally, we derive the distribution of integral summary statistics of BDPs that arise often in applications.

2 Background

A BDP is a continuous-time Markov chain counting the number of particles in a system at time , taking values on the non-negative integers . To construct a general BDP in a formal way, we must define the rules according to which the number of particles evolves. We do this by specifying the behavior of the process for a very short time , when there are particles in the system. If is very small, the probability of an event during that occurs with rate is approximately . Therefore, the probability of a birth in the interval , given , is

| (1) |

Intuitively, this means that the probability of more than one birth event in a small time is negligibly small. The probability of a death in is likewise

| (2) |

where . Together, these assumptions imply that the probability of no births or deaths occurring during is

| (3) |

2.1 Transition probabilities

Let be the transition probability from state to . We can use the above expressions to form a differential equation describing the change in transition probabilities over time. Suppose that . At the current time , we want to know the probability that in the next units of time, the process will reach state . We look into the future by writing the probabilities of three types of events that can take the process to state : birth from , death from , or no change from :

| (4) |

Subtracting from both sides, dividing by , and sending to zero, we obtain the Kolmogorov forward equations:

| (5) |

where if and zero otherwise. In this article, we always assume ; this keeps the process on the non-negative integers. Letting in matrix form, (5) becomes

| (6) |

where is the infinitesimal generator matrix with entries , , , and . In the matrix case, the initial condition becomes . This infinite sequence of coupled ordinary differential equations can be difficult or impossible to solve for many general BDPs (Novozhilov et al, 2006; Renshaw, 2011).

2.1.1 Kendall process

In the simple linear BDP, also known as the Kendall process where and , it is possible to solve for these transition probabilities explicitly by finding a generating function solution to the forward equations (Bailey, 1964; Lange, 2010). To illustrate, let . Let in (5), multiply both sides by , and sum on to obtain

| (7) |

with the initial condition . The solution is

| (8) |

Inverting and finding the th coefficient of the power series , we find the transition probabilities

| (9) |

where

| (10) |

2.1.2 General BDPs

The problem becomes much more complicated for general BDPs. Karlin and McGregor (1957b) present the definitive treatment of the existence of transition probabilities and other properties of BDPs. They obtain the following integral form for the transition probabilities:

| (11) |

where and for . Here, , is a system of orthogonal polynomials and is an orthogonalizing spectral measure that are specific to a particular set of birth and death rates.

This integral representation is intuitively satisfying because the time-dependency of is contained entirely in the exponential term, and depends on and in a simple way. In addition, we have the obvious corollary that

| (12) |

Beyond these simple results related to the interpretation of (11), the formalism developed by Karlin and McGregor (1957b) makes possible deep analytic insight into the behavior of general BDPs, including recurrence times and first passage times.

2.2 Equilibrium probabilities and explosion

Equilibrium solutions are straightforward to obtain (Renshaw, 2011). Setting the left-hand side of the Kolmogorov forward equations (5) to zero and replacing the finite-time transition probabilities with the equilibrium probabilities , we find that

| (13) |

Since this is the case for every , it is true for in particular, and , so both sides of (13) are zero for every by induction. This gives the detailed balance condition for continuous-time Markov chains,

| (14) |

Therefore every general BDP is a reversible Markov chain. Iterating the recurrence (14), we find that

| (15) |

where we have chosen so that . Note that for every .

The birth and death rates for a general BDP may be such that the process “runs away” to infinity in finite time. This is known as explosive growth. Formally, suppose the process begins at and there are no absorbing states. Renshaw (2011) shows that the expected first passage time to infinity is

| (16) |

where and

| (17) |

for . When (16) diverges, the process is non-explosive, and the first passage time from to any finite state is almost surely finite. When (16) is finite, the first passage time to infinity is finite with non-zero probability.

One result of special interest to us gives the conditions under which a BDP with a given generator is unique: Karlin and McGregor show that there is only one transition probability matrix that satisfies (6) if and only if

| (18) |

This property assures that probability is conserved on the non-negative integers. We will always assume this is the case in what follows.

Despite the elegant representation (11) for the transition probabilities, it can be very difficult to find the polynomials (Renshaw, 2011; Novozhilov et al, 2006). In addition, the problem of finding these polynomials and measure is a fundamentally analytical task, and is generally not amenable to computational solution. In other words, one cannot simply compute using a computer for an arbitrary set of birth and death rates and using the formula (11) alone. For this reason, nearly all modeling applications use the simple linear BDP since it is analytically tractable. Renshaw (2011, page 111) writes of the need for an alternative approach to solving the forward system in order to find transition probabilities for general BDPs:

“A worthwhile and potentially rewarding challenge would be to develop a simplified and user-friendly version of this technique which would work over a wide range of stochastic processes.”

The next section is devoted to this task.

3 Transition probabilities for general BDPs

We now outline a method, first presented in Crawford and Suchard (2012) and based on work by Murphy and O’Donohoe (1975), for numerically computing the transition probabilities for a general BDP with arbitrary birth and death rates. To proceed, denote the Laplace transform of as

| (19) |

Now, applying the Laplace transform to (5) with , we have

| (20) |

for . Recalling that and for , we rearrange (20) to find

| (21) |

By combining these recurrence relations, we obtain the generalized continued fraction

| (22) |

that is an exact expression for the Laplace transform of the transition probability (Karlin and McGregor, 1957b; Bordes and Roehner, 1983; Guillemin and Pinchon, 1999; Flajolet and Guillemin, 2000). Now define , , and for . Then (22) becomes

| (23) |

in more concise notation. We denote the th convergent of the Laplace transform by

| (24) |

The main result of Crawford and Suchard (2012) is the following theorem giving continued fraction expressions for the Laplace transform of the transition probability in a general birth-death process.

Theorem 1.

The Laplace transform of the transition probability is given by

| (25) |

where , , and are as defined above.

The proof of this theorem relies on elementary manipulation of the continued fraction recurrences (21). Crawford and Suchard (2012) obtain time-domain transition probabilities from (25) by numerically inverting the Laplace transforms. We refer the reader to that publication for the computational details. The method returns transition probabilities for many general BDPs that have eluded previous analytical and numerical methods.

3.1 First passage times

Now consider the time of first arrival of a BDP into an arbitrary set of taboo states, and suppose . This first passage time is defined formally as

| (26) |

To find the relationship between first passage times and the expressions for transition probabilities discussed above, construct a new process identical to except that for every , so every state in is absorbing. Then for this modified process, with ,

| (27) |

The intuitive reason for this equality is the absorbing nature of the states in : if reaches an absorbing state at any time before , we must have . Furthermore, cannot visit more than one state in , so the absorption events are mutually exclusive and the probability of absorption is simply the sum of the individual absorption probabilities. Therefore the cumulative distribution function of the first passage time into is given by the sum of the transition probabilities from to every taboo state in for the modified process .

4 Likelihoods

One factor hindering more widespread adoption of BDPs by applied researchers is the difficulty in performing statistical estimation of the unknown parameters in a BDP using real-world data (Holmes and Bruno, 2001; Doss et al, 2013). Typically efforts in estimation for BDPs have been limited to continuous observation of the process (Moran, 1951, 1953; Anscombe, 1953; Darwin, 1956; Wolff, 1965; Reynolds, 1973). In addition, most work to date has focused on the simple linear BDP because it is analytically tractable (Keiding, 1975; Thorne et al, 1991; Dauxois, 2004; Rosenberg et al, 2003). However, in practice researchers often observe data from BDPs only at discrete times through longitudinal sampling. In addition, the simple linear BDP may be unappealing because it fails to capture more complicated dynamics of population growth and decay that arise when particles do not behave independently. To learn from discretely-observed general BDPs, we will need more advanced statistical tools.

4.1 Likelihood for the continuously-observed process

In a discretely-observed general BDP, the likelihood cannot be written in closed form, making analytic maximum likelihood estimation impossible. However, the likelihood of a continuously-observed BDP is straightforward to express (Reynolds, 1973; Keiding, 1975). To develop the likelihood for continuously-observed data from a general BDP, we note the following important fact: the exponentially distributed waiting time of a continuous-time Markov process in a certain state is independent of the destination of the next jump (Lange, 2010). Recall that the waiting time for the first event to occur from state is exponentially distributed with rate . If the waiting time in the current state is , and the next change is a birth,

| (28) |

Likewise, the probability of a waiting time followed by a death is

| (29) |

Since we can only observe the process for a finite time , the last observation will be the waiting time in some state from the time of the jump to to the end of observation. Using the same reasoning,

| (30) |

To write the likelihood of a continuously-observed BDP from time to , we introduce some notation to ease our presentation. Suppose we observe jumps in the time interval , and label the jumps . Let be the waiting time in the current state just before the th jump. Define the indicator if the th jump is a birth, and if the th jump is a death. Let be the times of the jumps, with and . Then the likelihood of a sequence of observations is

| (31) |

where is the state just before the th jump. This cumbersome notation can be eliminated if we instead keep track of the total waiting time in each state and the number of births and deaths from each state. Define to be the indicator of an event , and let

| (32) |

be the total time spent in state over all visits to . Then let

| (33) |

be the number of up steps (births) from state , and let

| (34) |

be the number of down steps (deaths) from state . Then we can re-write the likelihood (31) in much simpler and more transparent form as

| (35) |

Of course, in a BDP observed continuously for a finite time (for which (18) holds), there are only finitely many jumps observed, so the product above is not really infinite in practice.

Equation (35) also reveals that the likelihood for a continuously-observed BDP is a member of the exponential family, where , , and for are the sufficient statistics of the continuously-observed BDP likelihood. In other words, one only needs to know the total number of up and down steps from, and time spent in, each state visited by the process in order to compute the likelihood.

4.2 Example: continuously-observed Kendall process

Maximum likelihood estimation for continuously-observed BDPs is often straightforward. Consider the simple linear BDP with birth rate and death rate . The likelihood (35) of a single observation becomes, up to a normalizing constant, becomes

| (36) |

where is the total number of up steps (births), is the total number of down steps (deaths) during the interval , and

| (37) |

is the “total particle time” or total time lived by every particle that existed during the interval . Maximizing (36) with respect to the unknown parameters and , we obtain the maximum likelihood estimators

| (38) |

first given by Reynolds (1973). Although the estimators provided by (38) involve an integral over the state path of the process, the integrand is simply a step function that is fully observed over .

4.3 Likelihood for the discretely-observed process

Suppose now that the process is observed only discretely, once at time and again at time , without loss of generality owing to the Markov assumption. Let us label the state of the BDP at these times as and . Then given that , the probability that is the transition probability . In section 3 we outlined a method for numerically computing this probability for any general BDP. If we regard the transition probability as a function of some unknown parameters which control the birth and death rates, writing , then we have the likelihood of our observation,

| (39) |

In principle, we could numerically maximize the likelihood for discrete observations to find an estimate of . However, as the number of parameters increases, naïve numerical optimization often suffers from poor convergence (Doss et al, 2013). The difficulty in writing or computing the likelihood for discrete observations from BDPs has limited the usefulness of BDPs in applications.

In contrast to the appealing analytic characterization (35) of the continuously-observed process likelihood, the discretely-observed process is hard to characterize. To bridge this gap, it is helpful to view computation of the likelihood in the discretely-observed process as a missing data problem. When a BDP is observed discretely, we do not know the sufficient statistics . This perspective suggests that we exploit analytic information about these statistics, conditional on the start and end states of the observed process.

5 EM algorithms for maximum likelihood estimation

In this section, we review the estimation machinery developed by Crawford et al (2014a) for maximum likelihood or maximum a posteriori estimation in BDPs. When a BDP is discretely sampled, , , and are unobserved for every ; we cannot maximize the likelihood without knowing these statistics. We therefore appeal to the expectation-maximization (EM) algorithm for iterative maximum likelihood estimation with missing data (Dempster et al, 1977). When the incomplete data likelihood is intractable but the complete data likelihood has a simple form, the EM algorithm operates by replacing each missing datum by a conditional expectation as follows. If is the complete (unobserved data), represents the incomplete (observed) data, and is the complete data log-likelihood, we form a surrogate function as the expectation of the complete data likelihood, conditional on the observed data and the current (th) parameter iterate:

| (40) |

This is the E-step of the EM algorithm, and it accomplishes a minorization of at . The M-step maximizes (or takes a step toward the maximum of) . By alternating these steps — minorizing by , then finding a that increases — the EM algorithm drives succeeding iterates toward the MLE.

Taking the expectation of the logarithm of (35), conditional on the observed data and the current parameter estimate , we write the surrogate function for the BDP as follows:

| (41) |

In the above equation and many that follow, we omit the dependence of the conditional expectations on from the th iterate for visual clarity.

To calculate the conditional expectations necessary for the E-step of the EM algorithm, we appeal to the following integral expressions

| (42a) | ||||

| (42b) | ||||

| (42c) | ||||

These expressions have appeared repeatedly in literature on inference for discretely-observed continuous-time Markov chains (Lange, 1995; Holmes and Rubin, 2002; Bladt and Sorensen, 2005; Hobolth and Jensen, 2005; Metzner et al, 2007). When the process takes only finitely many states, matrix solutions are possible using the uniformization method (Neuts, 1995). Hobolth and Stone (2009) develop efficient Monte Carlo methods using simulation conditioned on the start and end points of the discrete observation . Finally, Doss et al (2013) study a linear BDP on an infinite state space and derive the expectations analytically using a generating function argument. None of the exact methods is a general approach for arbitrary BDPs on an infinite state space. The Monte Carlo approaches, while not reliant on a particular parameterization of the process, can suffer from poor performance when observed realizations occur with low probability. The lack of a reliable method for computing the E-step of the EM algorithm for discretely-observed BDPs has hindered progress on statistical inference for these processes.

An alternative approach introduced by Crawford et al (2014a) takes advantage of the Laplace transforms of the transition probabilities (25). The numerators in (42) are time-domain convolutions of transition probabilities. The functional form of these expressions suggests using the Laplace convolution property to obtain

| (43a) | ||||

| (43b) | ||||

| (43c) | ||||

where denotes inverse Laplace transformation. These expressions are formally equivalent to (42), but they offer substantial computational time savings over numerical integration of (42), and make possible efficient computation of conditional expectations for EM algorithms for any BDP (Crawford et al, 2014a).

We now show how to complete the M-step for several BDP models. The first two, variations on the simple linear (Kendall) process, were given in Crawford et al (2014a). The others are novel, yet remarkably easy to derive and implement computationally. In each case, we describe the surrogate likelihood function and give the M-step updates for each unknown parameter.

5.1 Example: discretely-observed Kendall process

In the simple linear BDP, births and deaths happen at constant per-particle rates, so and . The unknown is . The surrogate function becomes

| (44) |

Maximizing (44) with respect to the yields the updates:

| (45a) | ||||

| (45b) | ||||

where

| (46) |

and we have again suppressed the dependence of the conditional expectations on for typographic clarity. These expressions are identical in form to the estimators given in (38), but are instead iterative updates in the EM algorithm.

5.2 Example: linear BDP with immigration

The linear BDP with immigration is similar to the simple linear BDP, but there is a source of new arrivals whose rate is constant and does not depend on the number of particles already in existence. This yields the birth and death rates and . The log-likelihood becomes

| (47) |

Unfortunately, it is difficult to maximize the resulting surrogate function analytically. But since each term in the sum is a concave function of the unknown parameters, we can separate them in a second minorizing function such that for all , and . To accomplish the minorization, note that

| (48) |

We form a minorizing log-likelihood function as follows:

| (49) |

where

| (50) |

Exploiting this surrogate function and maximizing with respect to the unknown sufficient statistics gives the updates

| (51a) | ||||

| (51b) | ||||

The update for is the same as (45b).

5.3 Example: pure-birth and generalized Poisson processes

Recall that the Poisson process with arrival rate is a BDP with , for all . Many researchers have found that real-world count data are sometimes over- or under-dispersed relative to the Poisson distribution. Statisticians seeking a more flexible distribution for count outcomes that can accommodate over- and under-dispersion have arrived at several alternative distributions. A notable example that fits neatly into the BDP framework is the general pure-birth process with arbitrary birth rates , , and for all . This class of processes has an appealing property: it can recover any discrete probability distribution on the counting numbers by appropriately setting the birth rates (Faddy, 1997; Faddy and Bosch, 2001). Crawford and Zelterman (2013) show that any such pure-birth process can be represented as a sum of exchangeable Bernoulli random variables, a result that connects BDPs with phenomenological models often used for dependent outcomes in toxicology and epidemiology. Renshaw (2011, page 65) gives an analytic form for these transition probabilities

| (52) |

for and provided that for all and . While (52) has an appealing form, it depends on none of the birth rates being equal. Another potentially serious drawback is that it can be numerically troublesome to compute; the summands may be alternating in sign and the product of small differences in the denominators can lead to serious roundoff error. In many scenarios, especially when some observed counts are large and some ’s are nearly or exactly equal, (52) provides an unappealing way to compute the likelihood. Exactly equal may arise, for example, when entertaining a Bayesian non-parametric prior. Fortunately, the EM framework does not require use of (52). We now provide an example of a pure birth process intended to generalize the Poisson distribution to accommodate over- and under-dispersion.

Faddy (1997) describes a class of pure-birth BDPs with and , where corresponds to a Poisson process with rate , results in overdispersion relative to Poisson, and results in underdispersion. The log-likelihood for the continuously-observed process beginning at and ending at is

| (53) |

Letting , the surrogate function is

| (54) |

The update for is given by

| (55) |

but the updates for and are not available in closed form. However, Lange (1995) shows that one step of a gradient ascent algorithm suffices to preserve the ascent property of the EM algorithm. Therefore a Newton-Raphson update can be derived, and

| (56) |

where and are the gradient and Hessian of with respect to and respectively.

5.4 Example: Moran model

The Moran process models genetic drift in a finite population by keeping track of the number of alleles of a certain type at a biallelic locus in a haploid population of constant size . Call the two alleles and , and suppose we wish to keep track of the number of carriers in the population. In the Moran model with selection, carriers of have fitness , and carriers of have fitness . For the sake of identifiability in a statistical setting, we specify and let denote the relative fitness of carriers over carriers. Furthermore, mutates to in one generation with probability , and vice versa with probability . When an existing individual dies, a new allele is drawn at random. The birth and death rates are

| (57) |

for . Forming the surrogate function from (41), we see that maximizing the log-likelihood with respect to the unknowns , , and is difficult. However, we can again construct a minorizing function to separate the parameters in the logarithm terms. We minorize the birth rate as

| (58) |

where

| (59) |

Although (58) and (59) may appear complicated, this minorization has the effect of separating the parameters and in the surrogate function, allowing closed-form updates. In a similar way, we minorize the death rate as

| (60) |

where

| (61) |

We form the complete minorizing function as

| (62) |

and the surrogate function is . A simple way to proceed is to find updates for each of the unknowns individually, conditional on the previous (th) estimate of the others, giving a cyclic coordinate ascent algorithm. The update for is

| (63) |

The update for is the positive solution of the quadratic equation

| (64) |

when . The update for is obtained by similar manipulations.

5.5 Example: maximum a posteriori estimation for the Kendall process

In a Bayesian setting, a prior distribution on the unknown parameters is given, and we seek to maximize the log-posterior distribution of the parameters, given the data, to obtain the maximum a posteriori (MAP) estimate of . Here the surrogate function becomes . To illustrate, suppose that independent observations from a BDP follow the simple linear model, and we believe that and are a priori independent and are Gamma-distributed:

| (65) |

Then the unknowns are and the log-prior for is

| (66) |

Ignoring irrelevant terms, the surrogate function becomes

| (67) |

The MAP updates are

| (68a) | ||||

| (68b) | ||||

5.6 Example: regression for count data

Perhaps the most interesting use of EM algorithms for BDP inference is to provide a unified framework for regression estimation. To illustrate, consider a collection of independent BDPs, with and for , where is a vector of covariates and is a covariate vector of corresponding dimension and for all . Then letting and for each , the log-likelihood becomes

| (69) |

This is the log-likelihood for classical Poisson regression, and updates are found using a Newton-Raphson step (Dobson, 2001).

It is possible to formulate an analogous model for the Kendall process. Let and let be the birth and death rates of a BDP . The log-likelihood is

| (70) |

where the statistics , , and correspond to observation . When the process is discretely-observed, we form the surrogate as in Section 5.1, and find the gradient vector

| (71) |

for . The Hessian matrix is

| (72) |

Then, the Newton-Raphson update for becomes

| (73) |

A similar update is available for . We contrast the simplicity of the update expressions (73) with the formula for the Kendall process transition probability (9).

6 Integral functionals of BDPs

Many important real-life applications of BDPs can be characterized as questions about the distribution of summary statistics. A common feature of stochastic processes in decision-making contexts is that the parameters estimated by the statistical inference procedure are not always the ones of interest in the application. Often the quantity of interest is a summary statistic related to the time-integral of the process. To illustrate, let be a function and let be a set of “taboo” or prohibited states. Suppose the initial state of the BDP is . Define the functional

| (74) |

where the upper limit of integration is the first passage time

| (75) |

Here, is a functional because it maps a realization of the stochastic process to its integral. Figure 2 shows an example realization of a BDP and its integral with . The left-hand side shows a BDP beginning at , and ending at . The right-hand plot shows over the same time interval, and the area under the trajectory is .

Expressions like (74) arise often in applied work. For example, epidemiologists usually estimate the parameters (contact/infection rate and recovery rate) of an epidemic process from data, but their objective is to make inference of the predictive distribution of the cost of the epidemic in the future. Operations researchers may estimate the arrival rate and service rate in a queuing process, but the object of inference is the distribution of customer-hours waited. Traffic engineers may be interested in the number of vehicle-hours waited in models for highway accident delays (Gaver, 1969).

To illustrate the role of integral summaries of BDPs in statistical prediction, let be the density of given . The posterior predictive uncertainty about the statistic is the marginal distribution

| (76) |

where is the sampling distribution of given the realized data . In a Bayesian context, is a posterior distribution, and we might estimate by a Monte Carlo approximation involving draws via

| (77) |

6.1 Background on integrals of BDPs

Karlin and McGregor (1957a, b) provided the first theoretical tools for working with integral functionals of general BDPs. Puri (1966, 1968) derives the characteristic function for the joint distribution of simple linear BDP and its integral and gives expressions for moments and limiting distributions (Puri, 1971, 1972a, 1972b). McNeil (1970) gives the first results for general BDPs, Gani and McNeil (1971) derive expressions for the joint distribution of a general BDP and its integral, and Kaplan (1974) provides limit theorems for integrals of simple BDPs with immigration. Straightforward methods for moments of integrals of general BDPs using Laplace transforms are also available (Hernández-Suárez and Castillo-Chavez, 1999; Pollett and Stefanov, 2003; Pollett, 2003; Gani and Swift, 2008). However, most analyses of integral functionals of general BDPs are limited to simple analytically tractable models or focused on moments.

Now we consider the problem of computing the distribution of (74). Our emphasis on first-passage times as the upper limit of integration in (74) has two benefits. First, our analyses need not be conditional on an arbitrary time in the future. Second, first passage times allow us to exploit powerful analytic tools that establish a correspondence between transition probabilities and first-passage times, enabling analytic progress on integrals for arbitrary well-behaved processes. Our presentation follows the outline given by McNeil (1970). Let be the Laplace transform of . Note that if then , , and so . Now by an analogous conditioning argument for , we re-write the Laplace transform as

| (78) |

that gives

| (79) |

Now dividing both sides of the above by , we find that

| (80) |

where and . Therefore, we see that (80) is simply the backward equation for a modified process with birth and death rates and for . The forward equation for the cumulative distribution function of is therefore equivalent to (5) with the modified birth and death rates.

Pollett (2003) gives the conditions, analogous to those for (16), under which this modified process explodes. We note that differentiation of solutions of (80) yields the moments of , as noted by McNeil (1970) and subsequently refined by Hernández-Suárez and Castillo-Chavez (1999), Stefanov and Wang (2000), and Pollett (2003). We refer interested readers to those papers and focus here on results for the distribution of that are more useful in statistical and decision applications.

To take advantage of (80), we modify (26) as follows. Fix and suppose is a general BDP with rates and with starting state . Suppose is a positive function defined for all . Let be a general BDP with rates and for all , and for every . Then let . We then have

| (81) |

If instead of the cumulative distribution function of , we wish to have the probability density, we could numerically differentiate (81). However, using the properties of the Laplace transform,

| (82) |

where is the Laplace transform of , denotes Laplace inversion, and for all since we have assumed .

6.2 Example: probabilistic control of an epidemic

In infectious disease epidemiology, stochastic modeling can give valuable insight into both disease dynamics and optimal intervention strategies (Wickwire, 1977; Ball, 1986). The total cost of an infectious disease epidemic is proportional to the area under the time trajectory of the number of infected people (Jerwood, 1970; Gani and Jerwood, 1972). To illustrate, we model the number of infected persons in a homogeneously mixing population as a type of general BDP. This simple model, called the susceptible-infected-susceptible (SIS) model, keeps track of the number of infected in a finite population of size (Bailey, 1957). If there are currently infected persons in the population, the rate of new infections is proportional to the product of the number infected and susceptible . The contact/transmission rate between infected and susceptible persons is . Infected persons recover and revert to susceptible status with constant per-person rate . For a SIS process , the addition and removal rates are

| (83) |

where is a positive control parameter related to vaccination or some other public health intervention strategy. Suppose the initial number of infected is and we are interested in the total cost of the epidemic until its eventual extinction, so . Let the cost of managing the epidemic per unit time be . Additionally, let the cost per infected person per unit time be , so the cost function becomes . Then the total cost is

| (84) |

where is the time to extinction of the epidemic.

Most optimal control models seek a policy that minimizes the expected total cost, corresponding to the expectation of (74) under certain conditions on the intervention and cost functions (Lefévre, 1981; Cai and Luo, 1994; Clancy, 1999; Guo and Hernández-Lerma, 2009). The availability of probability distributions for the total cost allows us to seek the minimal intervention policy that guarantees that the total cost of the epidemic is small with high probability. Let be the process with rates given by (83) for a certain control setting . Then we wish to find the smallest such that

| (85) |

where is a desired bound on the total cost, and is a small probability. Assuming this probability is continuous and increases monotonically with near , it is straightforward to find the smallest that satisfies (85).

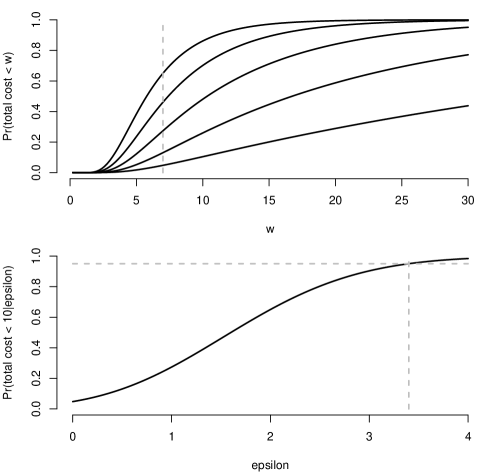

Figure 3 shows how to find the minimal for a SIS process with individuals, , infectivity , recovery rate , control cost , and per-infected cost per unit time. The top traces show the cumulative distribution function of the total cost for . The vertical gray line shows , and we wish to keep the total cost less than 7 with probability . The bottom trace shows as a function of . The horizontal gray dashed line shows 0.95 probability, and the vertical gray dashed line shows the smallest value of () that achieves this bound.

7 Discussion: likelihood-based inference for BDPs

BDPs are vital tools for modeling stochastic counting processes in epidemiology, evolution, ecology, chemistry, physics, and other fields. Modeling with BDPs is often straightforward; by considering rates of addition of new particles and removal of existing particles, conditional on the number already present, researchers can specify the birth and death rates . The ease of modeling with BDPs stands in stark contrast to the difficulty of inference using stochastic realizations of BDPs. Routine use of BDPs in statistical settings has been thwarted by intractable likelihoods and burdensome computations. A unified perspective on BDPs with arbitrary birth and death rates has remained elusive, until recently.

Laplace transforms of transition probabilities provide the essential analytic tools for bridging this gap in practice. Our approach for computing transition probabilities (likelihoods) in (25) and conditional expectations in the E-step (43) is general, robust, and computationally efficient. Laplace transforms of first-passage times also play an important role in finding the distribution of integral functionals of BDPs in applications. As a theoretic tool, this Laplace-perspective is not new; Karlin and McGregor (1957a, b, 1958a) discuss the fundamental importance of Laplace transforms for analysis of BDPs. More recent results related to combinatorial properties of BDPs also rely on Laplace transforms (Guillemin and Pinchon, 1998, 1999) and Flajolet and Guillemin (2000).

In this article, we have outlined new tools for practical likelihood-based analysis inference of BDP parameters under discrete and continuous observation of the process. In particular, BDP generalizations of Poisson regression yield more flexible and easy-to-fit models for count data. We have intentionally limited our discussion to basic computation of likelihoods, algorithms for maximum likelihood estimation, and finding the distribution of integral summary statistics for general BDPs. But these are only the first steps toward a comprehensive theory of estimation for BDPs. Ideally, we would like to see an analysis of identifiability, consistency and other statistical properties, like the groundbreaking work of Guttorp (1991) for Galton-Watson branching processes. We hope this review will stimulate statistical research related to BDPs with a view to bringing this rich class of stochastic models into wider use by applied scientists.

Acknowledgements

FWC was supported by NIH grant T32GM008185 and startup funds from the Yale School of Public Health. MAS was supported by NIH grants R01 AI107034 and R01 HG006139, and NSF grant DMS 1264153 and IIS 1251151.

References

- Andersson and Britton (2000) Andersson H, Britton T (2000) Stochastic Epidemic Models and their Statistical Analysis. Lecture notes in statistics, Springer New York

- Anscombe (1953) Anscombe FJ (1953) Sequential estimation. J Roy Stat Soc B 15(1):1–29

- Bailey (1957) Bailey NTJ (1957) The Mathematical Theory of Epidemics. Griffin London

- Bailey (1964) Bailey NTJ (1964) The Elements of Stochastic Processes with Applications to the Natural Sciences. Wiley New York

- Ball (1986) Ball F (1986) A unified approach to the distribution of total size and total area under the trajectory of infectives in epidemic models. Adv Appl Probab pp 289–310

- Bladt and Sorensen (2005) Bladt M, Sorensen M (2005) Statistical inference for discretely observed Markov jump processes. J Roy Stat Soc B 67(3):395–410

- Bordes and Roehner (1983) Bordes G, Roehner B (1983) Application of Stieltjes theory for S-fractions to birth and death processes. Adv Appl Probab 15(3):507–530

- Cai and Luo (1994) Cai H, Luo X (1994) Stochastic control of an epidemic process. Int J Syst Sci 25(4):821–828

- Clancy (1999) Clancy D (1999) Optimal intervention for epidemic models with general infection and removal rate functions. J Math Biol 39(4):309–331

- Crawford and Suchard (2012) Crawford FW, Suchard MA (2012) Transition probabilities for general birth-death processes with applications in ecology, genetics, and evolution. J Math Biol 65:553–580

- Crawford and Zelterman (2013) Crawford FW, Zelterman D (2013) Counting processes for correlated binary responses. arXiv preprint arXiv:13051656

- Crawford et al (2014a) Crawford FW, Minin VN, Suchard MA (2014a) Estimation for general birth-death processes. J Am Stat Assoc 109(506):730–747, URL http://www.tandfonline.com/doi/full/10.1080/01621459.2013.866565

- Crawford et al (2014b) Crawford FW, Weiss RE, Suchard MA (2014b) Sex, lies, and self-reported counts: Bayesian mixture models for longitudinal heaped count data via birth-death processes. arXiv preprint arXiv:14054265

- Darwin (1956) Darwin JH (1956) The behaviour of an estimator for a simple birth and death process. Biometrika 43(1):23–31

- Dauxois (2004) Dauxois J (2004) Bayesian inference for linear growth birth and death processes. J Stat Plan Infer 121(1):1–19

- Dempster et al (1977) Dempster AP, Laird NM, Rubin DB (1977) Maximum likelihood from incomplete data via the EM algorithm. J Roy Stat Soc B 39(1):1–38

- Demuth et al (2006) Demuth JP, Bie TD, Stajich JE, Cristianini N, Hahn MW (2006) The evolution of mammalian gene families. PLoS ONE 1(1):e85

- Dobson (2001) Dobson AJ (2001) An introduction to generalized linear models. CRC press

- Doss et al (2013) Doss CR, Suchard MA, Holmes I, Kato-Maeda M, Minin VN, et al (2013) Fitting birth–death processes to panel data with applications to bacterial dna fingerprinting. Ann Appl Stat 7(4):2315–2335

- Faddy (1997) Faddy M (1997) Extended Poisson process modelling and analysis of count data. Biom J 39(4):431–440

- Faddy and Bosch (2001) Faddy M, Bosch R (2001) Likelihood-based modeling and analysis of data underdispersed relative to the Poisson distribution. Biometrics 57(2):620–624

- Feller (1971) Feller W (1971) An Introduction to Probability Theory and its Applications. Wiley New York

- Flajolet and Guillemin (2000) Flajolet P, Guillemin F (2000) The formal theory of birth-and-death processes, lattice path combinatorics and continued fractions. Adv Appl Probab 32(3):750–778

- Gani and Jerwood (1972) Gani J, Jerwood D (1972) The cost of a general stochastic epidemic. J Appl Probab 9(2):257–269

- Gani and McNeil (1971) Gani J, McNeil DR (1971) Joint distributions of random variables and their integrals for certain birth-death and diffusion processes. Adv Appl Probab 3(2):339–352

- Gani and Swift (2008) Gani J, Swift R (2008) A simple approach to the integrals under three stochastic processes. J Stat Theory Pract 2(4):559–568

- Gaver (1969) Gaver D (1969) Highway delays resulting from flow-stopping incidents. J Appl Probab 6(1):137–153

- Guillemin and Pinchon (1998) Guillemin F, Pinchon D (1998) Continued fraction analysis of the duration of an excursion in an system. J Appl Probab 35(1):165–183

- Guillemin and Pinchon (1999) Guillemin F, Pinchon D (1999) Excursions of birth and death processes, orthogonal polynomials, and continued fractions. J Appl Probab 36(3):752–770

- Guo and Hernández-Lerma (2009) Guo X, Hernández-Lerma O (2009) Continuous-Time Markov Decision Processes. Springer

- Guttorp (1991) Guttorp P (1991) Statistical Inference for Branching Processes. Wiley Series in Probability and Statistics, Wiley-Interscience

- Hernández-Suárez and Castillo-Chavez (1999) Hernández-Suárez C, Castillo-Chavez C (1999) A basic result on the integral for birth-death Markov processes. Math Biosci 161(1):95–104

- Hobolth and Jensen (2005) Hobolth A, Jensen JL (2005) Statistical inference in evolutionary models of DNA sequences via the EM algorithm. Stat Appl Genet Mol 4(1):1–19

- Hobolth and Stone (2009) Hobolth A, Stone EA (2009) Simulation from endpoint-conditioned, continuous-time Markov chains on a finite state space, with applications to molecular evolution. Ann Appl Stat 3(3):1024–1231

- Holmes and Bruno (2001) Holmes I, Bruno WJ (2001) Evolutionary HMMs: a Bayesian approach to multiple alignment. Bioinformatics 17(9):803–820

- Holmes and Rubin (2002) Holmes I, Rubin G (2002) An expectation maximization algorithm for training hidden substitution models. J Mol Biol 317(5):753–764

- Jerwood (1970) Jerwood D (1970) A note on the cost of the simple epidemic. J Appl Probab 7(2):440–443

- Kaplan (1974) Kaplan N (1974) Limit theorems for the integral of a population process with immigration. Stoch Proc Appl 2(3):281–294

- Karlin and McGregor (1957a) Karlin S, McGregor J (1957a) The classification of birth and death processes. Trans Am Math Soc 86(2):366–400

- Karlin and McGregor (1957b) Karlin S, McGregor J (1957b) The differential equations of birth-and-death processes, and the Stieltjes moment problem. Trans Am Math Soc 85(2):589–646

- Karlin and McGregor (1958a) Karlin S, McGregor J (1958a) Linear growth, birth and death processes. J Math Mech 7(4):643–662

- Karlin and McGregor (1958b) Karlin S, McGregor J (1958b) Many server queueing processes with Poisson input and exponential service times. Pacific J Math 8(1):87–118

- Karlin and Taylor (1975) Karlin S, Taylor HM (1975) A First Course in Stochastic Processes. Academic Press

- Keiding (1975) Keiding N (1975) Maximum likelihood estimation in the birth-and-death process. Ann Stat 3(2):363–372

- Kendall (1948) Kendall DG (1948) On the generalized “birth-and-death” process. Ann Math Stat 19(1):1–15

- Kendall (1949) Kendall DG (1949) Stochastic processes and population growth. J Roy Stat Soc B Met 11(2):230–282

- Kingman (1982) Kingman JFC (1982) On the genealogy of large populations. J Appl Probab 19:27–43

- Klar et al (2010) Klar B, Parthasarathy PR, Henze N (2010) Zipf and Lerch limit of birth and death processes. Probab Eng Inform Sc 24(01):129–144

- Krone and Neuhauser (1997) Krone SM, Neuhauser C (1997) Ancestral processes with selection. Theor Popul Biol 51:210–237

- Lange (1995) Lange K (1995) A gradient algorithm locally equivalent to the EM algorithm. J Roy Stat Soc B Met 57(2):425–437

- Lange (2010) Lange K (2010) Applied Probability, 2nd edn. Springer texts in statistics, Springer New York

- Lee et al (2011) Lee J, Weiss RE, Suchard MA (2011) Using a birth-death process to account for reporting errors in longitudinal self-reported counts of behavior. Unpublished UCLA Biostatistics Technical report

- Lefévre (1981) Lefévre C (1981) Optimal control of a birth and death epidemic process. Oper Res 29(5):971–982

- Lenin and Parthasarathy (2000) Lenin RB, Parthasarathy PR (2000) A birth-death process suggested by a chain sequence. Comput Math Appl 40(2-3):239–247

- Mayrose et al (2010) Mayrose I, Barker MS, Otto SP (2010) Probabilistic models of chromosome number evolution and the inference of polyploidy. Syst Biol 59(2):132–144

- McNeil (1970) McNeil D (1970) Integral functionals of birth and death processes and related limiting distributions. Ann Math Stat pp 480–485

- Metzner et al (2007) Metzner P, Dittmer E, Jahnke T, Schütte C (2007) Generator estimation of Markov jump processes. J Comput Phys 227:353–375

- Moran (1951) Moran PAP (1951) Estimation methods for evolutive processes. J Roy Stat Soc B Met 13(1):141–146

- Moran (1953) Moran PAP (1953) The estimation of the parameters of a birth and death process. J Roy Stat Soc B Met 15(2):241–245

- Moran (1958) Moran PAP (1958) Random processes in genetics. Math Proc Cambridge 54(01):60–71

- Murphy and O’Donohoe (1975) Murphy JA, O’Donohoe MR (1975) Some properties of continued fractions with applications in Markov processes. IMA J Appl Math 16(1):57–71

- Nee (2006) Nee S (2006) Birth-death models in macroevolution. Annu Rev Ecol Evol S 37:1–17

- Nee et al (1994) Nee S, May RM, Harvey PH (1994) The reconstructed evolutionary process. Philos T Roy Soc B 344(1309):305–311

- Neuts (1995) Neuts MF (1995) Algorithmic Probability: A Collection of Problems (Stochastic Modeling Series). Chapman and Hall/CRC

- Norris (1998) Norris JR (1998) Markov Chains. 2008, Cambridge university press

- Novozhilov et al (2006) Novozhilov AS, Karev GP, Koonin EV (2006) Biological applications of the theory of birth-and-death processes. Brief Bioinform 7(1):70–85

- Parthasarathy et al (1998) Parthasarathy PR, Lenin RB, Schoutens W, Assche WV (1998) A birth and death process related to the Rogers-Ramanujan continued fraction. J Math Anal Appl 224(2):297–315

- Pollett (2003) Pollett P (2003) Integrals for continuous-time markov chains. Math Biosci 182(2):213–225

- Pollett and Stefanov (2003) Pollett P, Stefanov V (2003) A method for evaluating the distribution of the total cost of a random process over its lifetime. In: International Congress on Modelling and Simulation, Modelling and Simulation Society of Australia and New Zealand, vol 4, pp 1863–1867

- Puri (1966) Puri P (1966) On the homogeneous birth-and-death process and its integral. Biometrika 53(1-2):61–71

- Puri (1968) Puri P (1968) Some further results on the birth-and-death process and its integral. In: Mat Proc Cambridge, Cambridge Univ Press, vol 64, pp 141–154

- Puri (1972a) Puri P (1972a) A method for studying the integral functional of stochastic processes with applications ii. sojourn time distributions for markov chains. Probab Theory Rel 23(2):85–96

- Puri (1971) Puri PS (1971) A method for studying the integral functionals of stochastic processes with applications: I. markov chains case. J Appl Probab 8:331–343

- Puri (1972b) Puri PS (1972b) A method for studying the integral functionals of stochastic processes with applications III. In: Proc. Sixth Berkeley Symp. on Math. Statist. and Prob., Univ. of Calif. Press, vol 3, pp 481–500

- Renshaw (1993) Renshaw E (1993) Modelling Biological Populations in Space and Time. Cambridge Studies in Mathematical Biology, Cambridge University Press

- Renshaw (2011) Renshaw E (2011) Stochastic Population Processes: Analysis, Approximations, Simulations. Oxord University Press

- Reynolds (1973) Reynolds JF (1973) On estimating the parameters of a birth-death process. Aust J Stat 15(1):35–43

- Rosenberg et al (2003) Rosenberg NA, Tsolaki AG, Tanaka MM (2003) Estimating change rates of genetic markers using serial samples: applications to the transposon IS6110 in Mycobacterium tuberculosis. Theor Popul Biol 63(4):347–363

- Ross (1995) Ross SM (1995) Stochastic Processes, 2nd edn. Wiley

- Stefanov and Wang (2000) Stefanov V, Wang S (2000) A note on integrals for birth-death processes. Math Biosci 168(2):161–165

- Tan and Piantadosi (1991) Tan WY, Piantadosi S (1991) On stochastic growth processes with application to stochastic logistic growth. Stat Sinica 1:527–540

- Thorne et al (1991) Thorne J, Kishino H, Felsenstein J (1991) An evolutionary model for maximum likelihood alignment of DNA sequences. J Mol Evol 33(2):114–124

- Wickwire (1977) Wickwire K (1977) Mathematical models for the control of pests and infectious diseases: a survey. Theor Popul Biol 11(2):182–238

- Wolff (1965) Wolff RW (1965) Problems of statistical inference for birth and death queuing models. Oper Res 13(3):343–357