A Simple Approach to

Maximum Intractable Likelihood Estimation

Abstract

Approximate Bayesian Computation (ABC) can be viewed as an analytic approximation of an intractable likelihood coupled with an elementary simulation step. Such a view, combined with a suitable instrumental prior distribution permits maximum-likelihood (or maximum-a-posteriori) inference to be conducted, approximately, using essentially the same techniques. An elementary approach to this problem which simply obtains a nonparametric approximation of the likelihood surface which is then used as a smooth proxy for the likelihood in a subsequent maximisation step is developed here and the convergence of this class of algorithms is characterised theoretically. The use of non-sufficient summary statistics in this context is considered. Applying the proposed method to four problems demonstrates good performance. The proposed approach provides an alternative for approximating the maximum likelihood estimator (MLE) in complex scenarios.

Keywords: Approximate Bayesian Computation; Density Estimation; Maximum Likelihood Estimation; Monte Carlo Methods.

1 Introduction

Modern applied statistics must deal with many settings in which the pointwise evaluation of the likelihood function, even up to a normalising constant, is impossible or computationally infeasible. Areas such as financial modelling, genetics, geostatistics, neurophysiology and stochastic dynamical systems provide numerous examples of this (see e.g. Cox and Smith, 1954; Pritchard et al., 1999; and Toni et al., 2009). It is consequently difficult to perform any inference (classical or Bayesian) about the parameters of the model. Various approaches to overcome this difficulty have been proposed. For instance, Composite Likelihood methods (Cox and Reid, 2004), for approximating the likelihood function, and Approximate Bayesian Computational methods (ABC; Pritchard et al., 1999; Beaumont et al., 2002), for approximating the posterior distribution, have been extensively studied in the statistical literature. Here, we study the use of ABC methods, under an appropriate choice of instrumental prior distribution, to approximate the maximum likelihood estimator.

It is well-known that ABC produces a sample approximation of the posterior distribution (Beaumont et al., 2002) in which there exists a deterministic approximation error in addition to Monte Carlo variability. The quality of the approximation to the posterior and theoretical properties of the estimators obtained with ABC have been studied in Wilkinson (2008); Marin et al. (2011); Dean et al. (2011) and Fearnhead and Prangle (2012). The use of ABC posterior samples for conducting model comparison was studied in Didelot et al. (2011) and Robert et al. (2011). Using this sample approximation to characterise the mode of the posterior would in principle allow (approximate) maximum a posteriori (MAP) estimation. Furthermore, using a uniform prior distribution, under the parameterisation of interest, over any set which contains the MLE will lead to a MAP estimate which coincides with the MLE. In low-dimensional problems if we have a sample from the posterior distribution of the parameters, we can estimate its mode by using either nonparametric estimators of the density or another mode–seeking technique such as the mean-shift algorithm (Fukunaga and Hostetler, 1975). Therefore, in contexts where the likelihood function is intractable we can use these results to obtain an approximation of the MLE. We will denote the estimator obtained with this approximation AMLE.

Although Marjoram et al. (2003) noted that “It [ABC] can also be used in frequentist applications, in particular for maximum-likelihood estimation” this idea does not seem to have been developed. A method based around maximisation of a non-parametric estimate of the log likelihood function was proposed by Diggle and Gratton (1984) in the particular case of simple random samples; their approach involved sampling numerous replicates of the data for each parameter value and estimating the density in the data space. de Valpine (2004) proposes an importance sampling technique, rather closer in spirit to the approach developed here, by which a smoothed kernel estimation of the likelihood function up to a proportionality constant can be obtained in the particular case of state space models provided that techniques for sampling from the joint distribution of unknown parameters and latent states are available — not a requirement of the more general ABC technique developed below. The same idea was applied and analysed in the context of the estimation of location parameters, with particular emphasis on symmetric distributions, by Jaki and West (2008). The particular case of parameter estimation in hidden Markov models was also investigated by Dean et al. (2011), who relied upon the specific structure of that problem. To the best of our knowledge neither MAP estimation nor maximum likelihood estimation in general, implemented directly via the “ABC approximation” combined with maximisation of an estimated density, have been studied in the literature. However, there has been a lot of interest in this type of problem using different approaches (Cox and Kartsonaki, 2012; Fan et al., 2012; Mengersen et al., 2012) since we completed the first version of this work (Rubio and Johansen, 2012).

The estimation of the mode of nonparametric kernel density estimators which may seem, at first, to be a hopeless task has also received a lot of attention (see e.g. Parzen, 1962; Konakov, 1973; Romano, 1988; Abraham et al., 2003; Bickel and Früwirth, 2006). Alternative nonparametric density estimators which could also be considered within the AMLE context have been proposed recently in Cule et al. (2010); Jing et al. (2012).

The remainder of this paper is organised as follows. In Section 2, we present a brief description of ABC methods. In Section 3 we describe how to use these methods to approximate the MLE and present theoretical results to justify such use of ABC methods. In Section 4, we present simulated and real examples to illustrate the use of the proposed MLE approximation. Section 5 concludes with a discussion of both the developed techniques and the likelihood approximation obtained via ABC in general.

2 Approximate Bayesian Computation

We assume throughout this and the following section that all distributions of interest admit densities with respect to an appropriate version of Lebesgue measure, wherever this is possible, although this assumption can easily be relaxed. Let be a simple random sample from a distribution with support contained in , ; be the corresponding likelihood function, be a prior distribution over the parameter and the corresponding posterior distribution. Consider the following approximation to the posterior

| (1) |

where

| (2) |

is an approximation of the likelihood function and is a normalised Markov kernel. is typically concentrated around with acting as a scale parameter. It’s clear that (2) is a smoothed version of the true likelihood and it has been argued that the maximisation of such an approximation can in some circumstances lead to better performance than the maximisation of the likelihood itself (Ionides, 2005), providing an additional motivation for the investigation of MLE via this approximation. The approximation can be further motivated by noting that under weak regularity conditions, the distribution is close (in some sense) to the true posterior when is sufficiently small. The simplest approach to ABC samples directly from by the rejection sampling approach presented in Algorithm 1.

Now, let be a summary statistic, be a metric and . The simplest ABC algorithm can be formulated in this way using the kernel

| (3) |

The ABC rejection algorithm of Pritchard et al. (1999) can be obtained simply by setting . Several improvements to the ABC method have been proposed in order to increase the acceptance rate, see Beaumont et al. (2002), Marjoram et al. (2003) and Sisson (2007) for good surveys of these. An exhaustive summary of these developments falls outside the scope of the present paper.

3 Maximising Intractable Likelihoods

3.1 Algorithm

Point estimation of , by MLE and MAP estimation in particular, has been extensively studied (Lehmann and Casella, 1998). Recall that the MLE, , and the MAP estimator are the values of which maximise the likelihood or posterior density for the realised data.

These two quantities coincide when the prior distribution is constant (e.g. a uniform prior on a suitable (necessarily compact) set which contains ). Therefore, if we use a suitable uniform prior, it is possible to approximate the MLE by using ABC methods to generate an approximate sample from the posterior and then approximating the MAP using this sample. In a different context in which the likelihood can be evaluated pointwise, simulation-based MLEs which use a similar construction have been shown to perform well (see, e.g., Gaetan and Yao, 2003, Lele et al., 2007 and Johansen et al., 2008). In the present setting the optimisation step can be implemented by estimating the posterior density of using a nonparametric estimator (e.g. a kernel density estimator) and then maximising this function: Algorithm 2.

We note that we have not here considered similar simulation-based approaches to the direct optimisation of the likelihood function for a number of reasons. One is computational cost (not having access to the likelihood even pointwise means that distributions concentrated around the mode could be constructed only by introducing several replicates of the data and the rejection or other mechanism used to produce samples from this distribution will become increasingly inefficient as the number of replicates increases); another is that the proposed method has the additional advantages that it fully characterises the likelihood surface and can be conducted concurrently with Bayesian analysis with no additional simulation effort.

Note that the first step of this algorithm can be implemented rather generally by using essentially any algorithm which can be used in the standard ABC context. It is not necessary to obtain an iid sample from the distribution : provided the sample is appropriate for approximating that distribution it can in principle be employed in the AMLE context (although correlation between samples obtained using MCMC techniques and importance weights and dependence arising from the use of SMC can complicate density estimation, it is not as problematic as might be expected (Sköld et al., 2003)).

A still more general algorithm could be implemented: using any prior which has mass in some neighbourhood of the MLE and maximising the product of the estimated likelihood and the reciprocal of this prior (assuming that the likelihood estimate has lighter tails than the prior, not an onerous condition when density estimation is used to obtain that estimate) will also provide an estimate of the likelihood maximiser, an approach which was exploited by de Valpine (2004) (who provided also an analysis of the smoothing bias produced by this technique in their context). In the interests of parsimony we do not pursue this approach here, and throughout the remainder of this document we assume that a uniform prior over some set which includes the MLE is used, although we note that such an extension eliminates the requirement that a compact set containing a maximiser of the likelihood be identified in advance.

One obvious concern is that the approach could not be expected to work well when the parameter space is of high dimension: it is well known that density estimators in high-dimensional settings converge very slowly. Three things mitigate this problem in the present context:

-

•

Many of the applications of ABC have been to problems with extremely complex likelihoods which have only a small number of parameters (such as the examples considered below).

-

•

When the parameter space is of high dimension one could employ composite likelihood techniques with low-dimensional components estimated via AMLE. Provided appropriate parameter subsets are selected, the loss of efficiency will not be too severe in many cases. Alternatively, a different mode-seeking algorithm could be employed (Fukunaga and Hostetler, 1975).

-

•

In certain contexts, as discussed below Proposition 2, it may not be necessary to employ the density estimation step at all.

3.2 Asymptotic Behaviour

In this section we provide some theoretical results which justify the approach presented in Section 3.1 under similar conditions to those used to motivate the standard ABC approach. We assume throughout that the MLE exists in the model under consideration but that the likelihood is intractable; in the case of non-compact parameter spaces, for example, this may require verification on a case-by-case basis.

We begin by showing pointwise convergence of the posterior (and hence likelihood) approximation under reasonable regularity conditions. It is convenient first to introduce the following concentration condition on the class of ABC kernels which are employed:

- Condition K

-

A family of symmetric Markov kernels with densities indexed by is said to satisfy the concentration condition provided that its members become increasingly concentrated as decreases such that

where .

As the user can freely specify this is not a problematic condition. It serves only to control the degree of smoothing which the ABC approximation of precision can effect.

Proposition 1.

Let be a sample from a continuous distribution with support contained in , ; be a compact set that contains , the MLE of ; and let be the densities of a family of symmetric Markov kernels, which satisfies the concentration condition (K).

Suppose that

for some . Then, for each

Proof.

It follows from the concentration condition that:

Furthermore, for each

| (4) |

which converges to 0 as by continuity. Therefore .

Now, by bounded convergence (noting that boundedness of , for , follows from that of itself), we have that:

| (5) |

This result can be strengthened by noting that it is straightforward to obtain bounds on the error introduced at finite if we assume Lipschitz continuity of the true likelihood. Unfortunately, such conditions are not typically verifiable in problems of interest. The following result, in which we show that whenever a sufficient statistic is employed the ABC approximation converges pointwise to the posterior distribution, follows as a simple corollary to the previous proposition. However, we provide an explicit proof based on a slightly different argument in order to emphasize the role of sufficiency.

Corollary 1.

Let be a sample from a distribution over , be a sufficient statistic for , be a metric and suppose that the density of , , is continuous for every . Let be a compact set, suppose that

where for some fixed. Then, for each and the kernel

Proof.

Using the integral Mean Value Theorem (as used in a similar context by Dean et al. (2011, Equation 6)) we find that for and any :

for some , where is the Lebesgue measure. Then

As this holds for any sufficiently small , we have by continuity of :

| (6) |

Using the Dominated Convergence Theorem we have

| (7) |

By the Fisher-Neyman factorization Theorem we have that there exists a function such that

| (8) |

The result follows by combining , and .

With only a slight strengthening of the conditions, Proposition 1 allows us to show convergence of the mode as to that of the true likelihood. It is known that pointwise convergence together with equicontinuity on a compact set implies uniform convergence (Rudin, 1976; Whitney, 1991). Therefore, if in addition to the conditions in Proposition 1 we assume equicontinuity of on , a rather weak additional condition, then the convergence to is uniform and we have the following direct corollary to Proposition 1:

Corollary 2.

Let achieve its global maximum at for each and suppose that has unique maximiser . Under the conditions in Proposition 1; if is equicontinuous, then

Using these results we can show that for a simple random sample from the distribution with mode at and an estimator , based on , of , such that almost surely when , we have that for any there exists such that

That is, in the case of a sufficiently well-behaved density estimation procedure, using the simple form of the ABC estimator (Algorithm 1) we have that for any level of precision , the maximum of the AMLE approximation will, for large enough ABC samples, almost surely be close to the maximum of the posterior distribution of interest, which coincides with the MLE under the given conditions. A simple continuity argument suffices to justify the use of to approximate for large and small .

The convergence shown in the above results depends on the use of a sufficient statistic. In contexts where the likelihood is intractable, this may not be available. In the ABC literature, it has become common to employ summary statistics which are not sufficient in this setting. Although it is possible to characterise the likelihood approximation in this setting, it is difficult to draw useful conclusions from such a characterisation. The construction of appropriate summary statistics remains an active research area (see e.g. Peters et al., 2010 and Fearnhead and Prangle, 2012).

We finally provide one result which provides some support for the use of certain non-sufficient statistics when there is a sufficient quantity of data available. In particular we appeal to the large-sample limit in which it can be seen that for a class of summary statistics the AMLE can almost surely be made arbitrarily close to the true parameter value if a sufficiently small value of can be used. This is, of course, an idealisation, but provides some guidance on the properties required for summary statistics to be suitable for this purpose and it provides some reassurance that the use of such statistics can in principle lead to good estimation performance. In this result we assume that the AMLE algorithm is applied with the summary statistics filling the role of the data and hence the ABC kernel is defined directly on the space of the summary statistics.

In order to establish this result, we require that, allowing to denote a sequence of -dimensional summary statistics, the following four conditions hold:

-

S.i

for

-

S.ii

is an injective mapping. Letting denote the image of the feasible parameter space under , is an -Lipschitz continuous function for some .

-

S.iii

The ABC kernels, defined in the space of the summary statistics, satisfy condition K, i.e. it is concentrated within a ball of radius for all :

-

S.iv

The nonparametric estimator used always provides an estimate of the mode which lies within the convex hull of the sample.

Some interpretation of these conditions seems appropriate. The first tells us simply that the summary statistics converge to some function of the parameters in the large sample limit, a mild requirement which is clearly necessary to allow recovery of the parameters from the statistics. The second condition strengthens this slightly, requiring that the limiting values of the statistics and parameters exist in one-to-one correspondence and that this correspondence is regular in a Lipschitz-sense. The remaining conditions simply characterise the behaviour of the ABC approximation and the AMLE algorithm.

Proposition 2.

Let denote a sample with joint measure for some . Let denote a prior density over . Let denote a sequence of -dimensional summary statistics with distributions . Allow to denote an observed value of the sequence of statistics obtained from the model with .

Assume that conditions S.i–S.iv hold. Then:

-

(a)

for -almost every for -almost every .

-

(b)

The AMLE approximation of the MLE lies within almost surely.

Proof.

Allowing to denote the ABC approximation of the density of given , we have:

where with the final equality following from S.i (noting that almost sure convergence of to implies convergence in distribution of to a degenerate random variable taking the value .

From which it is clear that by S.iii.

And the ABC approximation to the posterior density of , , may be similarly constrained:

using S.ii. And by assumption S.i, S.ii and the continuous mapping theorem we have that giving result (a); result (b) follows immediately from S.iv. ∎

It is noteworthy that this proposition suggests that, at least in the large sample limit, one can use any estimate of the mode which lies within the convex hull of the sampled parameter values. The posterior mean would satisfy this requirement and thus for large enough data sets it is not necessary to employ the nonparametric density estimator at all in order to implement AMLE. This is perhaps an unsurprising result and seems a natural consequence of the usual Bayesian consistency results but it does have implications for implementation of AMLE in settings with large amounts of data for which the summary statistics are with high probability close to their limiting values.

Example 1 (Location-Scale Families and Empirical Quantiles).

Consider a simple random sample from a location-scale family, in which we can write the distribution functions in the form:

Allow and to denote to empirical quantiles. By the Glivenko-Cantelli theorem, these empirical quantiles converge almost-surely to the true quantiles:

In the case of the location-scale family, we have that:

and we can find explicitly the mapping :

provided that which can be assured if is strictly increasing and . In this case we even obtain an explicit form for .

3.3 Use of kernel density estimators

In this section we demonstrate that the simple Parzen estimator can be employed within the AMLE context with the support of the results of the previous section.

Definition 1.

(Parzen, 1962) Consider the problem of estimating a density with support on from independent random vectors . Let be a kernel, be a bandwidth such that when , then a kernel density estimator is defined by

Under the conditions and together with Theorem from Abraham et al. (2003), we have that as . Therefore, the results presented in the previous section apply to the use of kernel density estimation. This demonstrates that this simple non-parametric estimator is adequate for approximation of the MLE via the AMLE strategy, at least asymptotically.

This is, of course, just one of many ways in which the density could be estimated and more sophisticated techniques could very easily be employed and justified in the AMLE context.

4 Examples

We present four examples in increasing order of complexity. The first two examples illustrate the performance of the algorithm in simple scenarios in which the solution is known; the third compares the algorithm with a quantile-based method in a setting which has recently been studied using ABC and the final example demonstrates performance on a challenging estimation problem which has recently attracted some attention in the literature. In all the examples the simple ABC rejection algorithm was used, together with ABC kernel . For the second, third and fourth examples, kernel density estimation is conducted using the R command ‘kde’ together with the bandwidth matrix obtained via the smoothed cross validation approach of Duong and Hazelton (2005) using the command ‘Hscv’ from the R package ‘ks’ (Duong, 2011). R source code for these examples is available from the first author upon request.

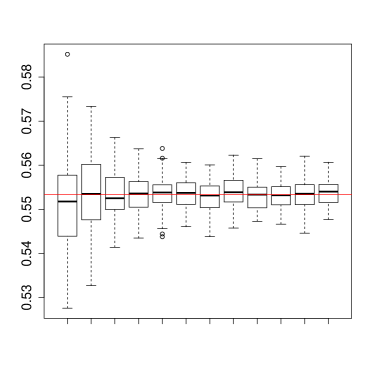

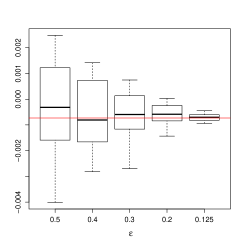

4.1 Binomial Model

Consider a sample of size simulated from a Binomial with . Using the prior , a tolerance , a sufficient statistic and the Euclidean metric we simulate an ABC sample of size which, together with Gaussian kernel estimation of the posterior, gives the AMLE .

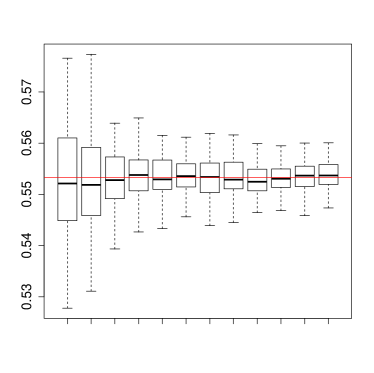

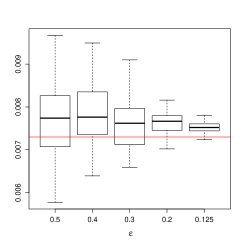

There are three quantities affecting the precision in the estimation of : , and . Figure 1 illustrates the effect of varying for a fixed , two different choices of and an ABC sample of size . Boxplots were obtained using replications of the (stochastic) AMLE algorithm. This demonstrates that although, unsurprising the acceptance rate and hence computational efficienct is improved when some which is relatively concentrated around the MLE is available, estimation precision remains good when the full support of the parameter space is included in albeit at greater computational cost (the choice produces an acceptance rate about 5 times greater than the choice ). Figure 2 shows the effect of for a fixed and two different choices of . In this case we can note that the effect of on the precision is significant. Again, the choice of affects only the acceptance rate.

|

|

| (a) | (b) |

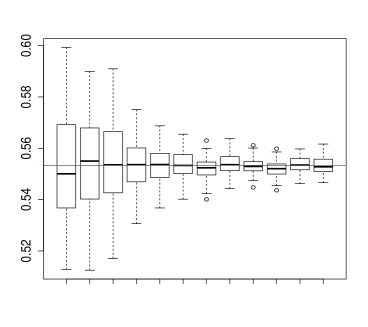

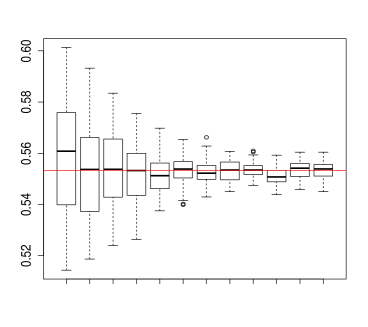

4.2 Normal Model

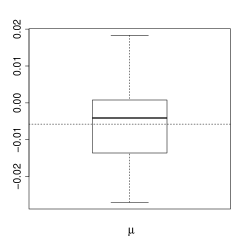

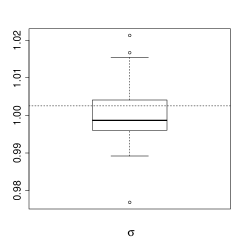

Consider a sample of size simulated from a Normal with sample mean and sample variance . Suppose that both parameters are unknown. The MLE of is simply .

Consider the priors and (crude estimates of location and scale can often be obtained from data, justifying such a choice; using broader prior support here increases computational cost but does not prevent good estimation), a tolerance , a sufficient statistic , the Euclidean metric, an ABC sample of size , and Gaussian kernel estimation of the posterior. Figure 3 illustrates Monte Carlo variability of the AMLE of . Boxplots were obtained using replicates of the algorithm.

|

|

| (a) | (b) |

4.3 Financial application

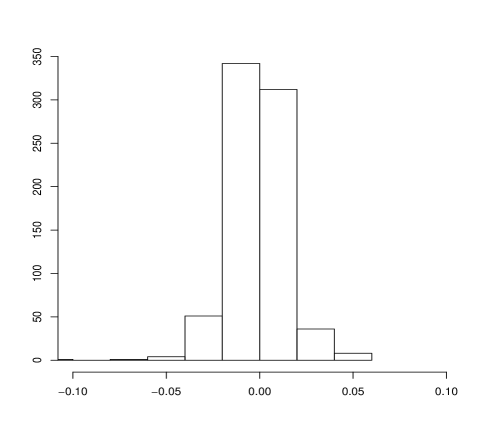

Logarithmic daily return prices are typically modelled using Lévy processes. For this reason, it is necessary to model the increments (logarithmic returns) using an infinitely divisible distribution. It has been found empirically that these observations have tails heavier than those of the normal distribution, and therefore an attractive option is the use of the parameter stable family of distributions, which can account for this behaviour. It is well known that maximum likelihood estimation for this family of distributions is difficult. Various numerical approximations of the MLE have been proposed (see e.g. McCulloch, 1986; Nolan, 2001). From a Bayesian perspective, Peters et al. (2010) proposed the use of ABC methods to obtain an approximate posterior sample of the parameters. They propose six summary statistics that can be used for this purpose.

Here, we analyse the logarithmic daily returns using the closing price of IBM ordinary stock from Jan. 1 2009 to Jan. 1 2012. Figure 4 shows the corresponding histogram. For this data set, the MLE using McCulloch’s quantile method implemented in the R package ‘fBasics’ (Wuertz et al., 2010) is .

Given the symmetry observed and in the spirit of parsimony, we consider the skewness parameter to be in order to calculate the AMLE of the parameters . Based on the interpretation of these parameters (shape, location and scale) and the data we use the priors

which due to the scale of the data may appear concentrated but are, in fact, rather uninformative, allowing a location parameter essentially anywhere within the convex hull of the data, scale motivated by similar considerations and any value of the shape parameter consistent with the problem at hand.

For the (non-sufficient) summary statistic we use proposal of Peters et al. (2010), which consists of the values of the empirical characteristic function evaluated on an appropriate grid. We use the grid -250, -200, -100, -50, -10, 10, 50, 100, 200, 250, an ABC sample of size , a tolerance and Gaussian kernel density estimation. Figure 5 illustrates Monte Carlo variability of the AMLE of . Boxplots were obtained using replicates of the AMLE procedure. A simulation study considering several simulated data sets produced with common parameter values (results not shown) suggest that the sampling variability in McCulloch’s estimator exceeds the difference between that estimator and the AMLE based upon . In general, considerable care must of course be taken in the selection of statistics — it is noteworthy that the quantiles used in McCulloch’s own estimator satisfy most of the requirements of Proposition 2, although it is not clear that it is possible to demonstrate the Lipschitz-continuity of in this case.

|

|

|

|

| (a) | (b) | (c) |

4.4 Superposed gamma point processes

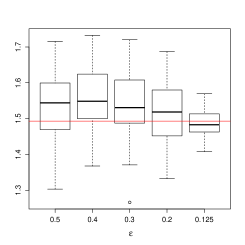

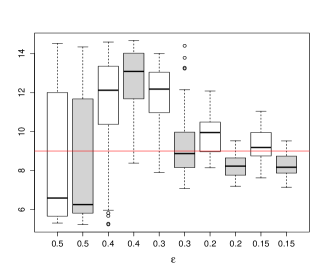

The modelling of an unknown number of superposed gamma point processes provides another scenario with intractable likelihoods which is currently attracting some attention (Cox and Kartsonaki, 2012; Mengersen et al., 2012). Intractability of the likelihood in this case is a consequence of the dependency between the observations, which complicates the construction of their joint distribution. Superposed point processes have applications in a variety of areas, for instance Cox and Smith (1954) present an application of this kind of processes in the context of neurophysiology. In this example we consider a simulated sample of size of superposed point processes with inter-arrival times identically distributed as a gamma random variable with shape parameter and rate parameter observed in the interval , with . This choice is inspired by the simulated example presented in Cox and Kartsonaki (2012).

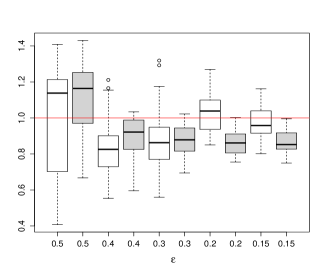

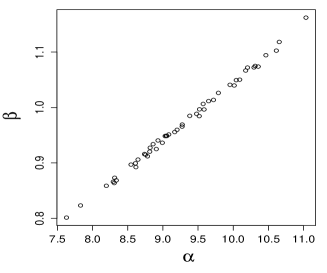

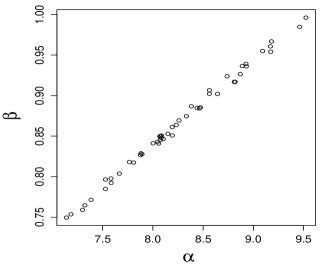

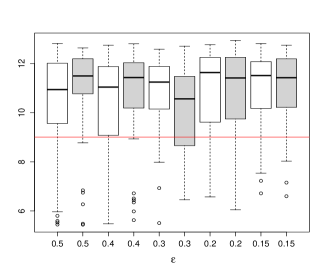

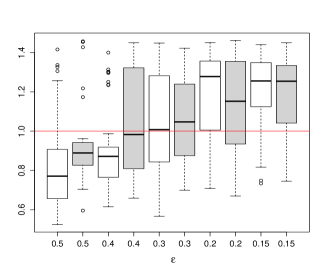

In order to make inference on the parameters using the AMLE approach, we implement two ABC samplers using the priors , , , tolerances and two sets of summary statistics. The first set of summary statistics, proposed in Cox and Kartsonaki (2012) and subsequently used in Mengersen et al. (2012), consists of the mean rate of occurrence, the coefficient of variation of the intervals between successive points, the sum of the first five autocorrelations of the intervals, the mean of the intervals, and the Poisson indexes of dispersion, variance divided by mean, for intervals of length 1, 5, 10 and 20. Cox and Kartsonaki (2012) mention that summary statistics based on the intervals between successive points are likely to be useful when is small, therefore we consider a second set of summary statistics by adding a ninth quantity based on the third moment: the sample skewness of the intervals between successive points . Note that, unlike Cox and Kartsonaki (2012) and Mengersen et al. (2012), we are taking the discrete nature of the parameter into account. The AMLE approach is still applicable in this context given that the maximisation of the joint posterior distribution of can be conducted by conditioning on . We also considered a continuous prior, uniform over and obtained comparable results (not shown) – although, naturally, by using a discrete prior on instead of a continuous one, the uncertainty in the estimation of and is reduced. Although allowing to take a continuous range of values leads to an analysis which is arguably more immediately comparable to those presented previously in the literature, we prefer to restrict to a discrete set as this is consistent with the statistical interpretation of the parameter and the possibility of doing so is a clear advantage of the AMLE methodology. Figure 6 shows the Monte Carlo variability, estimated by using AMLE samples, for each of the two AMLE approaches based on ABC samples of size . We can notice that the precision in the estimation of increases faster, as the tolerance decreases, when using 9 summary statistics. We can observe the same phenomenon from Table 1 in the estimation of . (Note that the horizontal line shows the parameters used to generate the data not the true value of the MLE). The uncertainty in the estimation of and using the AMLE approach with the set of 9 summary statistics seems to be qualitatively comparable with that in Cox and Kartsonaki (2012) for a small tolerance . Figure 7 shows scatter plots of the AMLE estimators of and for and both sets of summary statistics. This scatterplot demonstrates that the mean () of the gamma distribution is much more tightly constrained by the data than the shape parameter, leading to a nearly-flat ridge in the likelihood surface. The variability in the estimated value of is, in fact, rather small; while the variability in estimation of the shape parameter reflects the lack of information about this quantity in the data and the consequent flatness of the likelihood surface.

|

|

| (a) | (b) |

|

|

| (a) | (b) |

| 8 summary statistics | 9 summary statistics | |||||||

| 1 | 2 | 3 | 4 | 1 | 2 | 3 | 4 | |

| 29 | 0 | 1 | 20 | 33 | 0 | 15 | 2 | |

| 5 | 0 | 35 | 10 | 0 | 0 | 50 | 0 | |

| 0 | 4 | 46 | 0 | 0 | 37 | 13 | 0 | |

| 0 | 50 | 0 | 0 | 0 | 50 | 0 | 0 | |

| 0 | 50 | 0 | 0 | 0 | 50 | 0 | 0 | |

To show the variability of the estimator with different data, we also compare the variability of the estimators obtained using 50 different data sets. For each data set we obtain the corresponding AMLE of by using the priors , and , tolerances and the two sets of summary statistics mentioned above. Figure 8 shows the boxplots of the AMLEs for obtained using ABC samples of size . We can observe that the behaviour of the estimators of is fairly similar for both sets of summary statistics. Table 1 also suggests an improvement in the estimation of produced by the inclusion of the sample skewness.

|

|

| (a) | (b) |

| 8 summary statistics | 9 summary statistics | |||||||

| 1 | 2 | 3 | 4 | 1 | 2 | 3 | 4 | |

| 7 | 0 | 24 | 19 | 5 | 0 | 43 | 2 | |

| 8 | 0 | 41 | 1 | 3 | 0 | 24 | 23 | |

| 1 | 27 | 22 | 0 | 0 | 43 | 7 | 0 | |

| 0 | 46 | 4 | 0 | 0 | 44 | 6 | 0 | |

| 0 | 47 | 3 | 0 | 0 | 46 | 4 | 0 | |

5 Discussion

This paper presents a simple algorithm for conducting maximum likelihood estimation via simulation in settings in which the likelihood cannot (readily) be evaluated and provides theoretical and empirical support for that algorithm. This adds another tool to the “approximate computation” toolbox. This allows the (approximate) use of the MLE in most settings in which ABC is possible: desirable both in itself and because it is unsatisfactory for the approach to inference to be dictated by computational considerations. Furthermore, even in settings in which one wishes to adopt a Bayesian approach to inference it may be interesting to obtain also a likelihood-based estimate as agreement or disagreement between the approaches. Naturally, both ABC and AMLE being based upon the same approximation, the difficulties and limitations of ABC are largely inherited by AMLE. Selection of statistics in the case in which sufficient statistics are not available remains a critical question. There has been considerable work on this topic in recent years (see e.g. Fearnhead and Prangle, 2012).

A side-effect of the AMLE algorithm is an approximate characterisation of the likelihood surface, or in Bayesian settings of the posterior surface. We would strongly recommend that this surface be inspected whenever ABC or related techniques are used as even in settings in which the original likelihood contains strong information about the parameters it is possible for a poor choice of summary statistic to lead to the loss of this information. Without explicit consideration of the approximation, perhaps combined with prior sensitivity analysis, this type of issue is difficult to detect.

Acknowledgements

AMJ gratefully acknowledges support from EPSRC grant EP/I017984/1. FJR acknowledges support from Conacyt, México.

References

- Abraham et al. (2003) Abraham, C., Biau, G. and Cadre, B. (2003). Simple estimation of the mode of a multivariate density. The Canadian Journal of Statistics 31: 23–34.

- Beaumont et al. (2002) Beaumont, M. A., Zhang, W. and Balding, D. J. (2002). Approximate Bayesian computation in population genetics. Genetics 162: 2025–2035.

- Besag (1975) Besag, J. (1975). Statistical Analysis of Non-Lattice Data. The Statistician 24:179–195.

- Bickel and Früwirth (2006) Bickel, D. R. and Früwirth, R. (2006). On a fast, robust estimator of the mode: Comparisons to other robust estimators with applications . Computational Statistics & Data Analysis 50: 3500–3530.

- Cox and Kartsonaki (2012) Cox, D. R. and Kartsonaki, C. (2012). The fitting of complex parametric models. Biometrika 99: 741–747.

- Cox and Reid (2004) Cox, D. R. and Reid, N. (2004). A note on pseudolikelihood constructed from marginal densities. Biometrika 91: 729–737.

- Cox and Smith (1954) Cox, D. R. and Smith, W. L. (1954). On the superposition of renewal processes. Biometrika 41: 91- 9.

- Cule et al. (2010) Cule, M. L., Samworth, R. J. and Stewart, M. I. (2010), Maximum likelihood estimation of a multi-dimensional log-concave density. Journal Royal Statistical Society B 72: 545–600.

- Dean et al. (2011) Dean, T. A., Singh, S. S., Jasra A. and Peters G. W. (2011). Parameter estimation for hidden Markov models with intractable likelihoods. Arxiv preprint arXiv:1103.5399v1.

- de Valpine (2004) de Valpine, P. (2004) Monte Carlo state space likelihoods by weighted posterior kernel density estimation. Journal of the American Statistical Society 99: 523 -536.

- Didelot et al. (2011) Didelot, X., Everitt, R. G., Johansen, A. M. and Lawson, D. J. (2011). Likelihood-free estimation of model evidence. Bayesian Analysis 6: 49–76.

- Diggle and Gratton (1984) Diggle, P. J. and Gratton, R. J. (1984) Monte Carlo Methods of Inference for Implicit Statistical Models. Journal of the Royal Statistical Society. Series B (Methodological) 46:193–227.

- Duong and Hazelton (2005) Duong, T. and Hazleton, M. L. (2005). Cross-validation bandwidth matrices for multivariate kernel density estimation. Scandinavian Journal of Statistics 32:485–506.

- Duong (2011) Duong, T. (2011). ks: Kernel smoothing. R package version 1.8.5. http://CRAN.R-project.org/package=ks

- Fan et al. (2012) Fan, Y., Nott, D. J. and Sisson, S. A. (2012). Approximate Bayesian Computation via Regression Density Estimation. Arxiv preprint arXiv:1212.1479

- Fearnhead and Prangle (2012) Fearnhead, P. and Prangle, D. (2012). Constructing Summary Statistics for Approximate Bayesian Computation: Semi-automatic ABC (with discussion). Journal of the Royal Statistical Society Series B (Methodology) in press.

- Fukunaga and Hostetler (1975) Fukunaga, K. and Hostetler, L. D. (1975). The Estimation of the Gradient of a Density Function, with Applications in Pattern Recognition. IEEE Transactions on Information Theory 21: 32–40.

- Gaetan and Yao (2003) Gaetan, C. and Yao, J. F. (2003). A multiple-imputation Metropolis version of the EM algorithm. Biometrika 90: 643–654.

- Ionides (2005) Ionides, E. (2005). Maximum Smoothed Likelihood Estimation. Statistica Sinica 15: 1003–1014.

- Jaki and West (2008) Jaki, T. and West, R. W. (2008). Maximum Kernel Likelihood Estimation. Journal of Computational and Graphical Statistics 17: 976.

- Jing et al. (2012) Jing, J., Koch, I. and Naito, K (2012). Polynomial Histograms for Multivariate Density and Mode Estimation. Scandinavian Journal of Statistics 39:75–96.

- Johansen et al. (2008) Johansen, A. M., Doucet, A. and Davy, M. (2008). Particle methods for maximum likelihood parameter estimation in latent variable models. Statistics and Computing 18: 47–57.

- Konakov (1973) Konakov, V. D. (1973). On asymptotic normality of the sample mode of multivariate distributions. Theory of Probability and its Applications 18: 836–842.

- Lehmann and Casella (1998) Lehmann, E. and Casella, G. (1998). Theory of Point Estimation (revised edition). Springer-Verlag, New York.

- Lele et al. (2007) Lele, S. R., Dennis, B. and Lutscher, F. (2007). Data cloning: easy maximum likelihood estimation for complex ecological models using Bayesian Markov chain Monte Carlo methods. Ecology Letters 10: 551–563.

- McCulloch (1986) McCulloch, J. H. (1986). Simple consistent estimators of stable distribution parameters. Communications in Statistics: Simulation and Computation 15: 1109–1136.

- Marin et al. (2011) Marin, J., Pudlo, P., Robert, C. P. and Ryder, R. (2011). Approximate Bayesian Computational methods. Statistics and Computing in press.

- Marjoram et al. (2003) Marjoram, P., Molitor, J., Plagnol, V. and Tavaré, S. (2003). Markov chain Monte Carlo without likelihoods. Proceedings of the National Academy of Sciences USA: 15324–15328.

- Mengersen et al. (2012) Mengersen, K. L., Pudlo, P. and Robert, C. P. (2012). Approximate Bayesian computation via empirical likelihood. Proceedings of the National Academy of Sciences of the United States of America, forthcoming.

- Nolan (2001) Nolan, J. P. (2001). Maximum likelihood estimation and diagnostics for stable distributions. In: O.E. Barndorff-Nielsen, T. Mikosh, and S. Resnick, Eds., Lévy Processes, Birkhauser, Boston, 379–400.

- Parzen (1962) Parzen, E. (1962). On estimation of a probability density function and mode. Annals of Mathematical Statistics 33: 1065–1076.

- Peters et al. (2010) Peters, G. W., Sisson, S. A. and Fan, Y. (2010). Likelihood-free Bayesian inference for stable models. Computational Statistics & Data Analysis in press. http://dx.doi.org/10.1016/j.csda.2010.10.004

- Pritchard et al. (1999) Pritchard, J. K., Seielstad, M. T., Perez-Lezaun, A., and Feldman, M. T. (1999). Population Growth of Human Y Chromosomes: A Study of Y Chromosome Microsatellites. Molecular Biology and Evolution 16: 1791–1798.

- Robert (2007) Robert, C. P. (2007). The Bayesian Choice (2nd ed.). New York: Springer.

- Robert et al. (2011) Robert, C. P., Cornuet, J., Marin, J. and Pillai, N. S. (2011). Lack of confidence in ABC model choice. Proceedings of the National Academy of Sciences of the United States of America 108: 15112–15117.

- Romano (1988) Romano, J. P. (1988). On weak convergence and optimality of kernel density estimates of the mode. The Annals of Statistics 16: 629–647.

- Rubio and Johansen (2012) Rubio, F. J. and Johansen, A. M. J. (March, 2012). On Maximum Intractable Likelihood. CRiSM working paper 12–04.

- Rudin (1976) Rudin, W. (1976). Principles of Mathematical Analysis. New York: McGraw-Hill.

- Sisson (2007) Sisson, S. A., Fan, Y., and Tanaka, M. M. (2007). Sequential Monte Carlo without likelihoods. Proceedings of the National Academy of Sciences, 104: 1760–1765.

- Sköld et al. (2003) Sköld, M. and Roberts, G. O. (2003). Density estimation for the Metropolis–Hastings algorithm. Scandinavian Journal of Statistics 30: 699–718.

- Tavaré et al. (1997) Tavaré, S., Balding, D., Griffith, R. and Donelly, P. (1997). Inferring coalescence times from DNA sequence data. Genetics 145: 505–518.

- Toni et al. (2009) Toni, T.; Welch, D.; Strelkowa, N.; Ipsen, A.; Stumpf, M.P.H. (2009). Approximate Bayesian computation scheme for parameter inference and model selection in dynamical systems. Journal of the Royal Society Interface 6: 187–202.

- Whitney (1991) Whitney, K. N. (1991). Uniform Convergence in probability and stochastic equicontinuity. Econometrica 59: 1161–1167.

- Wilkinson (2008) Wilkinson, R. D. (2008). Approximate Bayesian computation (ABC) gives exact results under the assumption of error model. Arxiv preprint arXiv:0811.3355.

- Wuertz et al. (2010) Wuertz, D. and core team members R (2010). fBasics: Rmetrics - Markets and Basic Statistics. R package version 2110.79. http://CRAN.R-project.org/package=fBasics